Business Jet Market Size, Share, Trends and Forecast by Type, Business Model, Range, Point of Sale, and Region, 2026-2034

Business Jet Market Size, Share, Trends & Forecast (2026-2034)

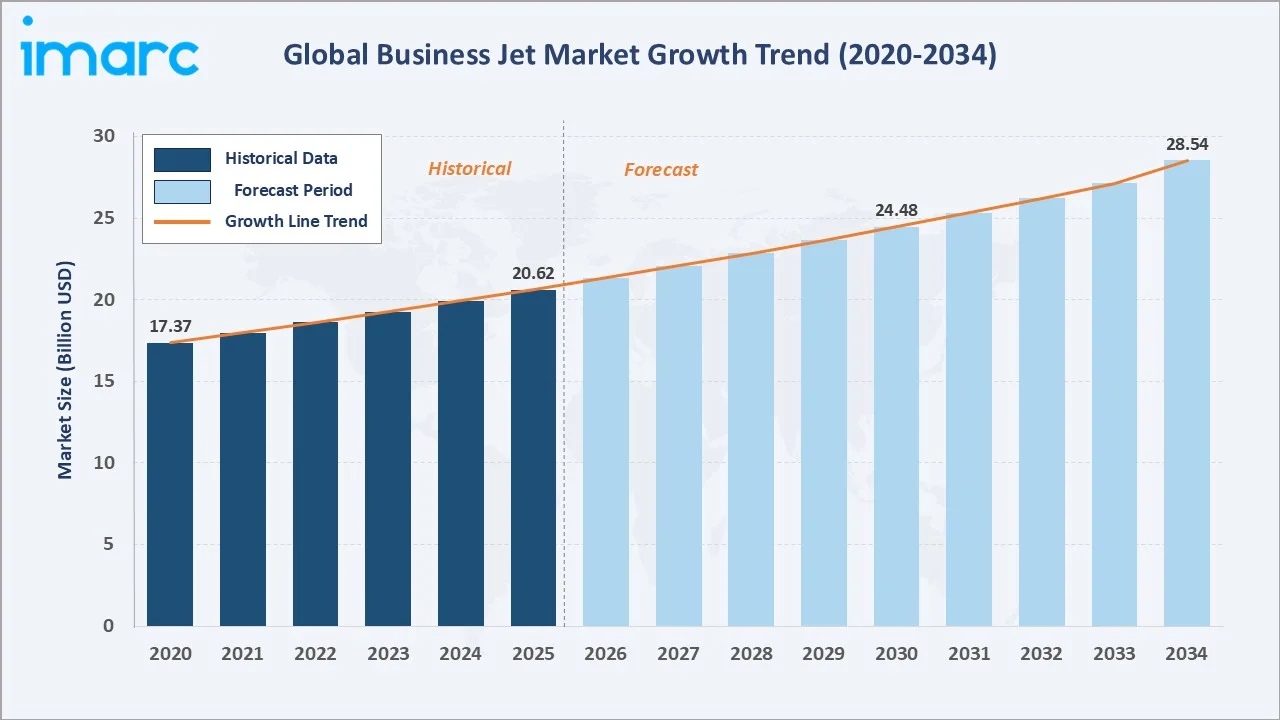

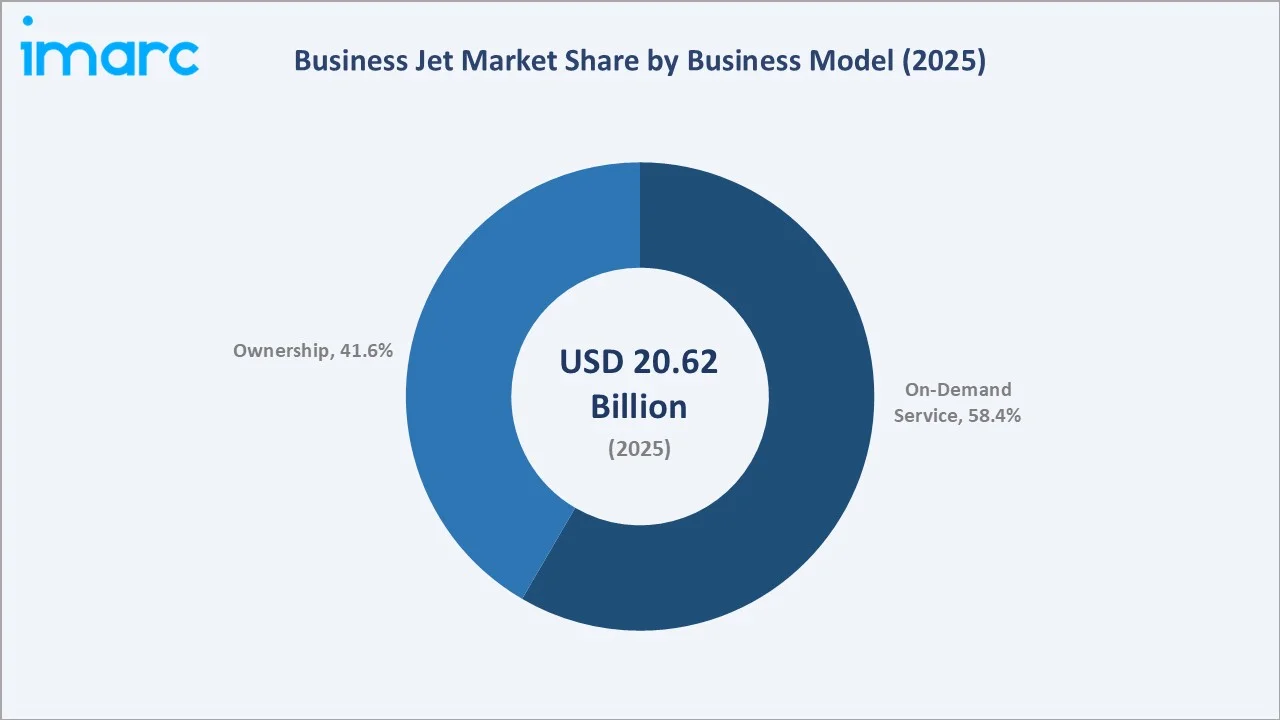

The global business jet market reached USD 20.62 Billion in 2025 and is projected to reach USD 28.54 Billion by 2034, growing at a CAGR of 3.49% during 2026-2034. Rising inclination toward business jets among corporate executives and high-net-worth individuals, growing traction of fractional ownership and jet-sharing models, and increasing requirement for specialized medical transportation for urgent care are key growth drivers.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 20.62 Billion |

|

Forecast Market Size (2034) |

USD 28.54 Billion |

|

CAGR (2026-2034) |

3.49% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (52.4% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

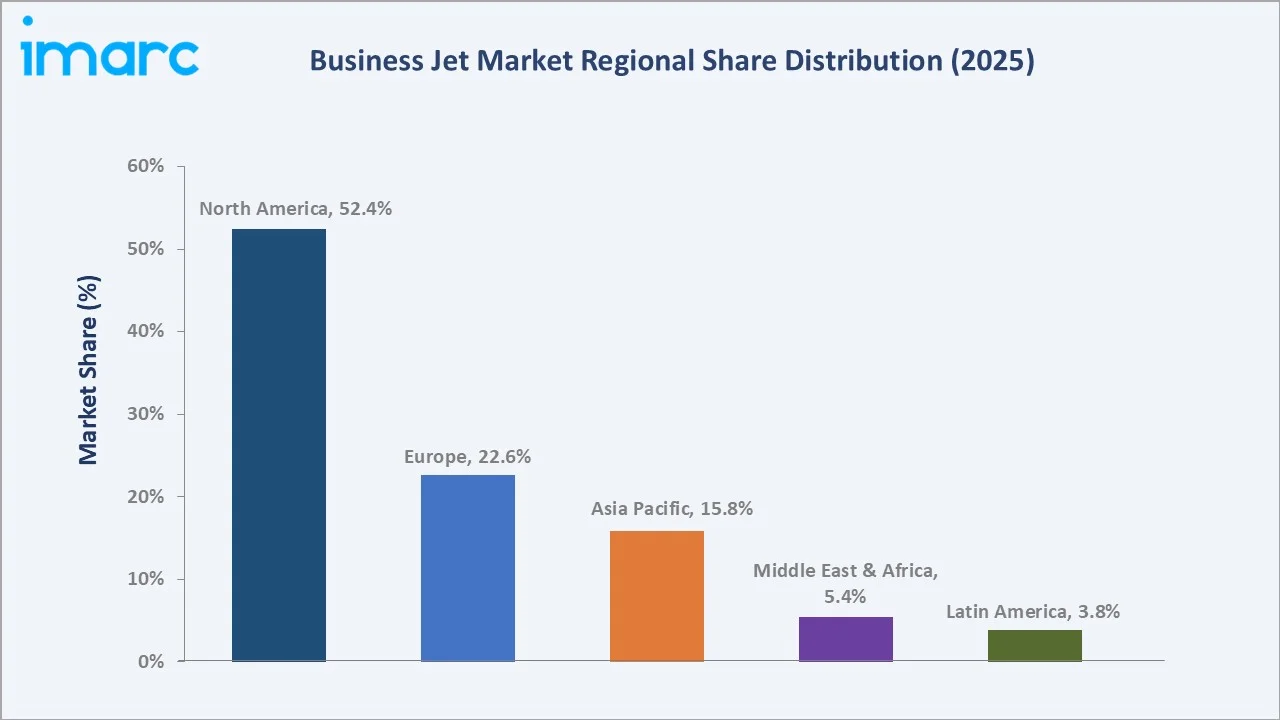

North America dominates, holding a 52.4% market share in 2025, while the on-demand service segment leads business model demand at 58.4%. OEM remains the dominant point of sale with a 62.4% share. Business jets offer significant advantages over commercial aviation, including customized scheduling, access to secondary airports, enhanced privacy and security, and substantially reduced door-to-door travel time for corporate executives and government delegations.

To get more information on this market, Request Sample

With applications spanning various sectors, including corporate travel, government and VVIP transport, medical airlift, and leisure travel, the market is expected to continue expanding, supported by innovation in sustainable aviation technology and increasing adoption across regions with rapidly growing high-net-worth populations.

Executive Summary

The global business jet market is on a sustained growth path, underpinned by increasing corporate mobility requirements, rising adoption of flexible on-demand aviation services, and growing private investment in business aviation infrastructure worldwide. The market reached USD 20.62 Billion in 2025 and is forecast to reach USD 28.54 Billion by 2034, reflecting a CAGR of 3.49% over the forecast period.

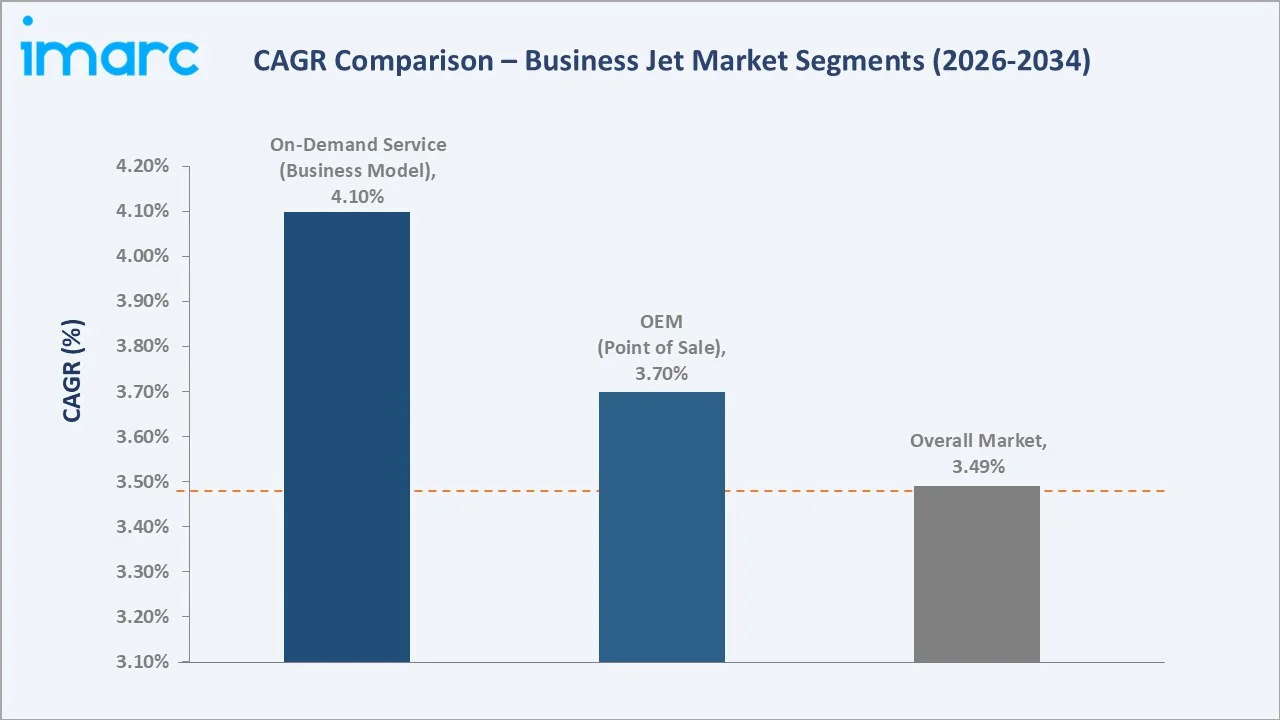

North America leads globally with a 52.4% revenue share in 2025, driven by an extensive network of private terminals and FBOs, a high concentration of Fortune 500 corporate headquarters, and a deeply embedded corporate aviation culture. Asia Pacific, at 15.8%, represents the fastest-growing opportunity, with China, India, and Southeast Asian nations investing heavily in private aviation infrastructure and recording strong UHNWI population growth. On-demand service commands the largest business model share at 58.4%, reflecting the structural shift toward asset-light, utilization-based aviation models that democratize access to business jets.

OEM point of sale commands 62.4% market share, sustained by continued demand for new-generation aircraft featuring advanced avionics, composite airframes, extended range capability, and enhanced cabin specifications. Leading manufacturers, including Gulfstream Aerospace Corporation, Bombardier, Textron Inc., Dassault Aviation, Embraer, and Pilatus Aircraft Ltd., continue to invest in sustainable and technologically advanced platforms to align with evolving regulatory standards and passenger expectations in the business jet market.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Business Model) |

On-Demand Service – 58.4% share (2025) |

|

Largest Segment (Point of Sale) |

OEM – 62.4% share (2025) |

|

Leading Region |

North America – 52.4% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific (wealth creation + aviation infrastructure growth) |

|

Top Companies |

Gulfstream Aerospace Corporation, Bombardier, Textron Inc., Dassault Aviation, Embraer, and Pilatus Aircraft Ltd. |

|

Market Opportunity |

SAF-compatible and hybrid-electric business jets projected at USD 5 Billion+ by 2034 |

Key Analytical Observations Supporting The Above Data:

- On-Demand Service accounts for 58.4% of the business jet market in 2025, preferred by corporates and mid-tier enterprises due to flexible scheduling, access to diverse aircraft types, and elimination of ownership obligations including maintenance and crew management.

- OEM is the dominant point of sale at 62.4% (2025), fueled by corporate and institutional demand for the latest-generation aircraft with advanced Symmetry flight decks, composite airframes, and manufacturer-backed lifecycle support programs.

- North America holds 52.4% of the global market in 2025, led by the United States with over 5,000 public-use airports and an FBO network of over 3,000 facilities, creating unparalleled private aviation connectivity for corporate travelers.

- Asia Pacific is the fastest-growing region, driven by China's population of ultra-wealthy individuals, which is projected to grow from 98,551 UHNWIs in 2023 to 144,897 by 2028, and India’s ongoing UDAN regional airport connectivity program.

- Sustainable aviation fuel adoption mandates and hybrid-electric propulsion R&D commitments by leading OEMs are reshaping long-term fleet replacement cycles, with major manufacturers targeting 10–15% SAF blend usage by 2030.

Global Business Jet Market Overview

Business jets are purpose-built fixed-wing aircraft designed to transport small groups of passengers, typically 4 to 19 individuals, with superior speed, range, and cabin comfort compared to commercial aviation. Originally deployed exclusively by government agencies and large corporations in the mid-twentieth century, business jets have evolved into a multi-tiered asset class encompassing entry-level light jets for short-range regional travel.

It also includes midsize jets for transcontinental routes, and large ultra-long-range platforms capable of nonstop intercontinental travel exceeding 7,000 nautical miles. The broader market ecosystem spans aircraft manufacturers, engine and avionics suppliers, MRO (maintenance, repair, and overhaul) operators, FBO (fixed-base operator) networks, charter management companies, fractional ownership programs, and digital booking platforms.

Business jets uniquely address corporate mobility requirements by enabling direct city-pair connectivity, eliminating layover time, providing secure and productive cabin environments for confidential business deliberations, and accessing secondary airports not served by commercial airlines.

Market Dynamics

To evaluate market opportunities, Request Sample

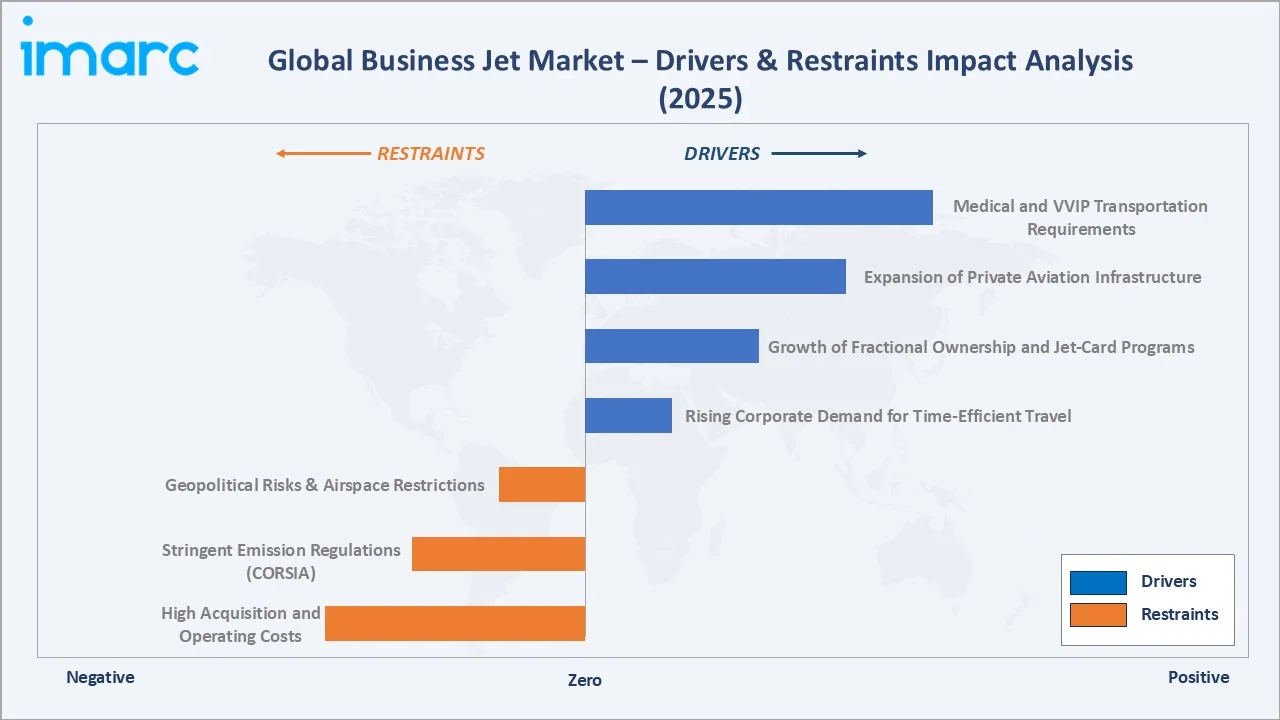

Market Drivers

- Rising Corporate Demand for Time-Efficient Travel: According to the National Business Aviation Association (NBAA), business aviation contributes over USD 150 billion annually to the U.S. economy and supports more than 1.2 million jobs, underscoring the deep integration of private aviation into corporate operations.

- Growth of Fractional Ownership and Jet-Card Programs: Digital charter platforms and fractional ownership programs have democratized business jet access, enabling mid-size enterprises to leverage private aviation without capital-intensive outright ownership, substantially broadening the addressable customer base.

- Expansion of Private Aviation Infrastructure: Governments across the Gulf Cooperation Council, Southeast Asia, and India are investing in dedicated business aviation terminals, customs pre-clearance facilities, and private hangar expansion to accommodate rising demand from corporate and VVIP travelers.

- Medical and VVIP Transportation Requirements: Growing institutional demand for rapid-response medical airlift, organ transport, and head-of-state travel has created a stable, high-priority demand segment for purpose-configured business jets with specialized cabin layouts and medical equipment installations.

These drivers reinforce a self-sustaining growth cycle, rising corporate wealth drives demand for private aviation services, which accelerates fleet investment by operators, which in turn stimulates OEM order books and broader aviation ecosystem development across maintenance, training, and ground services.

Market Restraints

- High Acquisition and Operating Costs: Business jets require capital expenditure ranging from USD 3 million for entry-level light jets to over USD 60 million for ultra-long-range large-cabin platforms, with annual operating costs between USD 500,000 and USD 4 million, limiting market penetration among smaller enterprises.

- Stringent Emission Regulations: Tightening ICAO and regional aviation emission standards, including the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA), are compelling manufacturers and operators to accelerate costly sustainable aviation fuel adoption and fleet replacement cycles.

- Geopolitical Risks and Airspace Restrictions: Evolving geopolitical tensions, sanctioned-nation overflight restrictions, and airspace closures affect trans-regional business jet route planning, increasing operational complexity and cost for international operators.

Market Opportunities

- Sustainable Aviation Fuel (SAF) Integration: Growing regulatory mandates and voluntary corporate sustainability commitments are creating a USD 2 Billion+ SAF supply and integration opportunity within the business jet sector through 2034, incentivizing manufacturers to develop 100% SAF-compatible engine platforms.

- Emerging Market Expansion: Asia Pacific and Latin America collectively represent an incremental USD 3.5 billion business jet market opportunity by 2034. Entry via strategic partnerships with regional FBO operators, alignment with national aviation development programs, and deployment of light-to-midsize jet fleets targeting secondary city routes are the preferred modalities.

- Advanced Propulsion and Digital Connectivity: Hybrid-electric propulsion systems and AI-driven predictive maintenance platforms represent nascent technology segments, expected to grow at 12–18% CAGR through 2034, offering manufacturers differentiated product positioning and operators meaningful total cost of ownership reductions.

Market Challenges

- Disposal and Fleet Lifecycle Management: End-of-life business jet disposal and recycling infrastructure remains underdeveloped, creating growing ESG-related compliance challenges as institutional buyers and regulators demand transparent lifecycle accountability from operators and manufacturers.

- Regulatory Complexity Across Jurisdictions: Diverging airworthiness certification standards across FAA, EASA, CAAC, and DGCA create compliance cost burdens for OEMs seeking multi-geography type certification for new platforms, potentially increasing per-aircraft certification timelines by 18–24 months.

Emerging Market Trends

1. Surge in On-Demand Charter and Digital Booking Platforms

Post-pandemic, the number of private jet flights witnessed a 34% increase compared to 2019, as many of them migrated from commercial first-class travel. This trend is accelerating the adoption of jet-card programs and dynamic charter pricing models across Europe and the Asia Pacific.

2. Rise of Sustainable Aviation Fuel Adoption

Gulfstream Aerospace completed the first transatlantic flight powered entirely by sustainable aviation fuel in 2023, establishing a performance benchmark for the industry. Production capacity assessments show that the EU is on course to achieve the overall mandatory SAF blending target of 6% by 2030.

3. Increased Demand for Long-Range Ultra-Wide Cabin Jets

Orders for aircraft in the Gulfstream G700/G800 and Bombardier Global 7500/8000 categories demonstrated double-digit growth between 2022 and 2025. This trend is driven by post-pandemic reconfiguration of executive travel preferences toward fewer, longer nonstop trips that maximize productivity and minimize airport exposure.

4. Integration of Advanced Avionics and Connectivity Systems

Business jet manufacturers are deploying next-generation avionics featuring synthetic vision displays, head-up displays (HUDs), automatic terrain awareness systems, and high-speed Ku/Ka-band satellite connectivity. Passenger connectivity expectations have elevated from basic Wi-Fi to multi-screen immersive entertainment systems and secure enterprise VPN-compliant networks, with cabin connectivity becoming a standard feature.

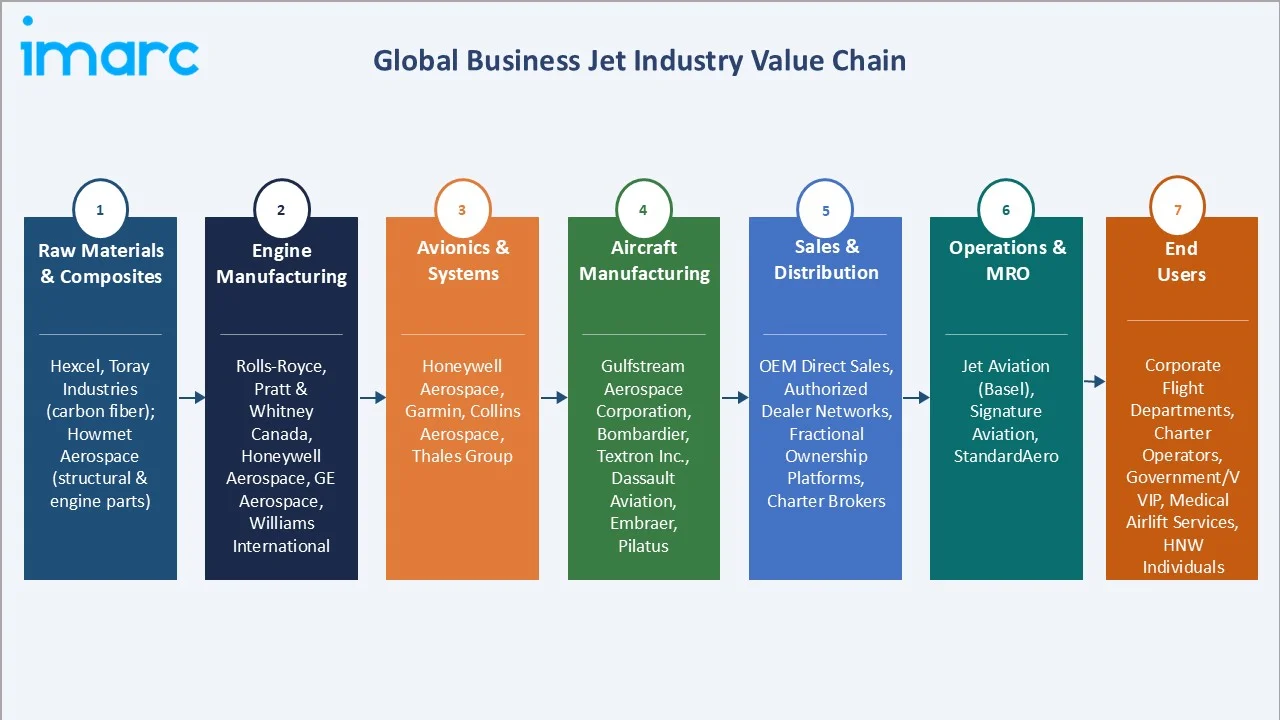

Industry Value Chain Analysis

The business jet value chain spans raw material and component supply through end-operator service delivery, with each stage populated by specialized entities whose performance directly influences aircraft quality, safety, operational economics, and total lifecycle cost.

|

Stage |

Key Players / Examples |

|

Raw Materials & Composites |

Hexcel, Toray Industries (carbon fiber); Howmet Aerospace (aerospace structural components & engine parts) |

|

Engine Manufacturing |

Rolls-Royce, Pratt & Whitney Canada, Honeywell Aerospace, GE Aerospace, Williams International |

|

Avionics & Systems |

Honeywell Aerospace, Garmin, Collins Aerospace, Thales Group |

|

Aircraft Manufacturing (OEM) |

Gulfstream Aerospace Corporation, Bombardier, Textron Inc., Dassault Aviation, Embraer, Pilatus Aircraft Ltd. |

|

Sales & Distribution |

OEM Direct Sales, Authorized Dealer Networks, Fractional Ownership Platforms, Charter Brokers |

|

Operations & MRO |

Jet Aviation (Basel), Signature Aviation, StandardAero |

|

End Users |

Corporate Flight Departments, Charter Operators, Government/VVIP, Medical Airlift Services, HNW Individuals |

Technology Landscape in the Business Jet Industry

Advanced Avionics and Flight Management Systems

Next-generation avionics architectures feature integrated touchscreen flight decks, enhanced ground proximity warning systems, ADS-B Out compliance, and AI-assisted flight management systems that optimize fuel burn across all flight phases. Gulfstream’s Symmetry flight deck, featuring the largest touchscreen display in business aviation, exemplifies the industry shift toward intuitive, reduced-workload cockpit environments.

Sustainable Aviation Fuel and Hybrid Propulsion

Major OEMs and engine manufacturers have committed to delivering 100% SAF-compatible engines by 2030. Rolls-Royce's UltraFan features a 140-inch fan diameter and is claimed to deliver a 25% improvement in fuel efficiency compared to the first generation of Trent engines. (Rolls-Royce).

Advanced Cabin Connectivity

High-throughput satellite (HTS) connectivity systems delivering 100+ Mbps throughput are now standard across large and super-midsize business jet categories. Integration of Starlink maritime/aviation LEO satellite internet by Starlink Aviation across charter fleets provides broadband-equivalent in-flight connectivity at significantly lower costs than legacy geostationary satellite solutions, fundamentally improving the in-flight productivity and entertainment experience.

Predictive Maintenance and Digital Twin Technology

OEM health monitoring platforms and AI-driven predictive maintenance systems analyze real-time engine telemetry, structural sensor data, and avionics diagnostics to forecast component failures before they occur, reducing unscheduled maintenance events by up to 35-40% in early adopter fleets. Bombardier’s Smart Link Plus system and Honeywell’s GoDirect Flight services represent leading implementations of this technology in the business jet segment.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Large | 🔒 | 2025 |

| Business Model | On-Demand Service | 58.4% | 2025 |

| Range | 3,000 - 5,000 NM | 🔒 | 2025 |

| Point of Sale | OEM | 62.4% | 2025 |

| Region | North America | 52.4% | 2025 |

By Business Model

On-Demand Service dominates the business model segment with a 58.4% share in 2025. This model encompasses flexible charter services (branded charters, air taxis), and jet-card programs that pre-purchase flight hours at fixed rates, collectively offering corporate and individual users premium private aviation access without capital-intensive ownership obligations.

To access detailed market analysis, Request Sample

Ownership accounts for 41.6%, comprising fractional ownership programs and full outright ownership. Fractional programs offered by operators allow corporations to purchase specific shares of an aircraft, with guaranteed availability and management handled by the program operator. Full ownership remains prevalent among ultra-high-net-worth individuals and government entities requiring dedicated, fully customized aircraft.

By Point of Sale

OEM accounts for the largest point of sale share at 62.4% in 2025, reflecting sustained appetite for new aircraft deliveries featuring latest-generation avionics, composite airframes, and next-generation engine platforms. OEM purchases include full aircraft customization options, manufacturer warranties, and direct access to proprietary maintenance programs, providing operators with comprehensive lifecycle support ecosystems.

Aftermarket holds 37.6%, encompassing pre-owned aircraft transactions, MRO services, avionics upgrades, cabin refurbishment, and component supply. The robust aftermarket reflects the long operational life of business jets (typically 20–30 years), with a global installed fleet of over 23,000 aircraft requiring continuous maintenance, regulatory compliance updates, and periodic cabin refresh programs to sustain operator and passenger satisfaction.

Regional Market Insights

North America’s market leadership (52.4%, 2025) reflects decades of private aviation infrastructure investment, the world’s highest density of registered business aircraft, and a deeply embedded corporate culture of executive air travel. The United States alone accounts for approximately 68% of North America’s regional business jet market, supported by the NBAA’s estimate that business aviation contributes over USD 150 billion annually to the U.S. economy.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

52.4% |

Corporate culture, FBO density, HNW concentration, Part 91 framework |

|

Europe |

22.6% |

Cross-border executive travel, sports & luxury tourism, jet-card growth |

|

Asia Pacific |

15.8% |

UHNWI wealth creation; UDAN airport scheme; corporate expansion |

|

Middle East & Africa |

5.4% |

GCC VVIP demand, sovereign wealth travel, Vision 2030 tourism |

|

Latin America |

3.8% |

Remote mining/energy connectivity; Brazil UHNWI growth; near-shoring |

Asia Pacific is the highest-growth region, with China targeting the expansion of business aviation infrastructure across tier-2 cities. South Korea and Japan are integrating business jet connectivity for cross-border corporate travel, while India’s growing UHNWI population unlocks new demand corridors for both charter and ownership models.

Competitive Landscape

The global business jet market exhibits a moderately concentrated competitive structure. The top five manufacturers, Gulfstream Aerospace Corporation, Bombardier, Textron Inc., Dassault Aviation, and Embraer, collectively hold approximately 75–80% of global new aircraft delivery revenue in 2025.

|

Company Name |

Brand/Platform |

Market Position |

Core Strength |

|

Gulfstream Aerospace Corporation. |

G700/G800 |

Market Leader |

Ultra-long-range large-cabin leadership; advanced avionics |

|

Bombardier |

Global 7500/8000 |

Market Leader |

World's largest-range business jet; premier cabin technology |

|

Textron Inc. |

Cessna Citation |

Strong Challenger |

Broadest product portfolio from light to large-cabin jets |

|

Dassault Aviation |

Falcon 6X |

Strong Challenger |

European market leadership |

|

Embraer |

Phenom / Praetor |

Challenger |

Light and super-midsize expertise; Latin America dominance |

|

Pilatus Aircraft Ltd |

PC-24 |

Niche Player |

Unpaved runway capability; Swiss precision engineering |

Regional manufacturers and niche players, including Pilatus Aircraft Ltd, serve specialized segments, focusing on customized aircraft solutions for specific market needs. These companies emphasize quality, precision, and innovation to cater to distinct customer demands, often in the light aircraft and training sectors.

Key Company Profiles

Gulfstream Aerospace Corporation

Gulfstream Aerospace Corporation., a wholly owned subsidiary of General Dynamics headquartered in Savannah, Georgia, is the global market leader in ultra-long-range business jets. The company’s G700 and G800 platforms define industry benchmarks for cabin volume, range, and avionics sophistication.

- Product Portfolio: G280, G400, G500, G600, G700, G800 – spanning super-midsize to ultra-long-range categories.

- Recent Developments: In April 2025, Gulfstream’s new G800 received certification from both the U.S. FAA and the EASA, enabling deliveries to begin to customers in North America, Europe, and other global markets.

- Strategic Focus: SAF adoption target of 10% blend by 2030; Symmetry flight deck with full touchscreen avionics; active-noise-cancellation cabin technology.

Bombardier

Bombardier, headquartered in Montreal, Canada, produces the world’s longest-range and largest business jets. Its Global series consistently leads the ultra-long-range segment while the Challenger line addresses the large-cabin mid-market for corporate operators.

- Product Portfolio: Challenger 3500, Global 5500/6500/7500/8000.

- Recent Developments: In January 2026, Bombardier is expanding its manufacturing footprint in Dorval, Quebec, through a C$100 million project, boosting its business aircraft assembly.

- Strategic Focus: Proprietary Nuage seating system; Smart Link Plus predictive maintenance platform; Bombardier Defense division expansion.

Textron Inc.

Textron Inc., through its Cessna Citation and Beechcraft brands, offers the broadest business jet product spectrum of any single manufacturer, serving corporate flight departments, charter operators, and owner-pilot customers globally.

- Product Portfolio: Citation M2 Gen2, CJ series, XLS, Longitude, Ascend.

- Recent Developments: In April 2022, Textron Aviation announced that flyExclusive placed an order for up to 30 Cessna Citation CJ3+ light jets, strengthening its partnership with the aircraft manufacturer.

- Strategic Focus: Digital cockpit connectivity upgrades; global expansion of Citation Service Centers; owner-pilot training programs.

Market Concentration Analysis

The business jet market exhibits moderate-to-high concentration at the OEM manufacturing level, with the top five manufacturers collectively controlling approximately 75–80% of new aircraft delivery revenue in 2025. The aftermarket services, charter brokerage, and MRO segments are considerably more fragmented, with hundreds of regional operators and maintenance providers competing across geographies.

Consolidation activity is a recurring feature, driven by rising certification costs for next-generation platforms, sustainability compliance investment requirements, and the strategic imperative to offer integrated full-lifecycle service ecosystems to institutional buyers.

Between 2020 and 2025, notable consolidation activity included fleet expansions by major charter operators, acquisitions of digital aviation platforms by traditional charter companies, and MRO network consolidations targeting multi-OEM certified maintenance capabilities.

Investment & Growth Opportunities

Fastest Growing Segments

SAF integration and hybrid-electric propulsion programs (estimated CAGR 9.5% through 2034), AI-powered digital charter booking platforms (18% CAGR), and ultra-long-range large-cabin jet platforms (6.2% CAGR) represent the three highest-growth investment vectors within the global business jet market.

Emerging Market Expansion

South and Southeast Asia collectively represent an incremental USD 1.8 Billion business jet opportunity by 2034. Entry via strategic partnerships with regional FBO and charter operators, alignment with national aviation development programs in India and Indonesia, and deployment of light-to-midsize jet fleets are the preferred market entry modalities.

Venture and Institutional Investment Trends

- Urban air mobility convergence with business aviation is attracting institutional capital into eVTOL-to-business-jet intermodal platforms connecting city centers with regional business aviation terminals, with pilot programs underway in the UAE, UK, and Singapore.

- Private equity interest remains elevated in MRO platform consolidation, targeting full-spectrum maintenance service providers with certified capabilities across multiple OEM platforms, as aging global fleets drive increasing aftermarket spending.

Future Market Outlook (2026-2034)

The global business jet market is positioned for sustained, broad-based growth through 2034. From a base of USD 20.62 Billion in 2025, the market is projected to reach USD 28.54 Billion by 2034, representing total incremental value creation of USD 7.92 Billion over the nine-year forecast horizon at a CAGR of 3.49%.

Regulatory evolution, particularly CORSIA Phase 1 carbon offsetting requirements, EASA’s Fit for 55 aviation directives, and growing municipal restrictions on short-haul private jet operations in Europe, will drive significant fleet renewal cycles and accelerate investment in SAF-compatible and lower-emission aircraft platforms. Manufacturers that achieve type certification for SAF-compatible, noise-compliant platforms by 2028 are positioned to capture a disproportionate share of institutional and corporate procurement orders across the forecast period.

Long-term, the business jet market’s trajectory is anchored to three structural macro-themes: continued growth of the global UHNWI and HNWI population, the accelerating shift from commercial to private aviation among time-sensitive corporate travelers, and technology-driven reduction of business jet operating costs. Business aviation sits at the intersection of all three.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 120 industry participants in 2024–2025, including business jet manufacturers, charter and fractional ownership operators, FBO network managers, aircraft finance specialists, MRO service providers, and corporate flight department heads across North America, Europe, and the Asia Pacific.

Secondary Research

Secondary research encompassed a systematic review of OEM annual reports, FAA and EASA regulatory filings, NBAA and EBAA industry association publications, industry databases, trade publications including Aviation Week, AIN Online, and Business Jet Traveler, and publicly available financial data from major manufacturers.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating macroeconomic indicators, UHNWI/HNWI population growth data, corporate travel expenditure patterns, and historical OEM delivery data. A base-case CAGR of 3.49% reflects consensus analyst estimates validated against reported manufacturer order backlogs and fleet utilization metrics.

Business Jet Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Light, Medium, Large |

| Business Models Covered |

|

| Ranges Covered | < 3,000 NM, 3,000 - 5,000 NM, > 5000 NM |

| Point of Sales Covered | OEM, Aftermarket |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Gulfstream Aerospace Corporation., Bombardier, Textron Inc., Dassault Aviation, Embraer, Pilatus Aircraft Ltd, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the business jet market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global business jet market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the business jet industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Business Jet Market Report

The global business jet market reached USD 20.62 Billion in 2025. It is projected to reach USD 28.54 Billion by 2034.

The business jet market is expected to grow at a CAGR of 3.49% during the forecast period from 2026-2034, supported by consistent demand from corporate, government, medical, and leisure travel segments.

North America leads the market with a 52.4% revenue share in 2025, driven by the world’s most extensive private aviation infrastructure, a high concentration of high-net-worth individuals, and an entrenched corporate culture of executive private air travel.

On-Demand Service dominates the business model segment with a 58.4% share in 2025, valued at approximately USD 12.04 Billion. Its dominance is driven by the flexibility, cost efficiency, and access advantages it provides to corporate users compared to outright aircraft ownership.

The OEM point of sale holds the largest share at 62.4% in 2025 (approximately USD 12.87 Billion), driven by sustained new aircraft delivery demand featuring latest-generation avionics, fuel-efficient engines, and advanced composite airframe construction.

Key players include Gulfstream Aerospace Corporation, Bombardier, Textron Inc., Dassault Aviation, Embraer, and Pilatus Aircraft Ltd.

Digital charter platforms and jet-card programs are democratizing business jet access, enabling mid-size enterprises and first-time users to leverage private aviation economics without capital-intensive ownership.

Key challenges include high acquisition and operating costs that limit market penetration among smaller enterprises, stringent and evolving environmental emission regulations requiring costly fleet upgrades, and increasing regulatory complexity across multiple aviation authority jurisdictions.

Significant opportunities exist in SAF integration programs, hybrid-electric propulsion development, AI-driven digital charter platforms, ultra-long-range jet demand from the Asia Pacific, and MRO platform consolidation targeting multi-OEM certified maintenance capabilities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)