Cancer Cachexia Market Size, Share, Trends and Forecast by Therapeutics, Mode of Action, Distribution Channel, and Region 2026-2034

Global Cancer Cachexia Market Size, Share, Trends & Forecast (2026-2034)

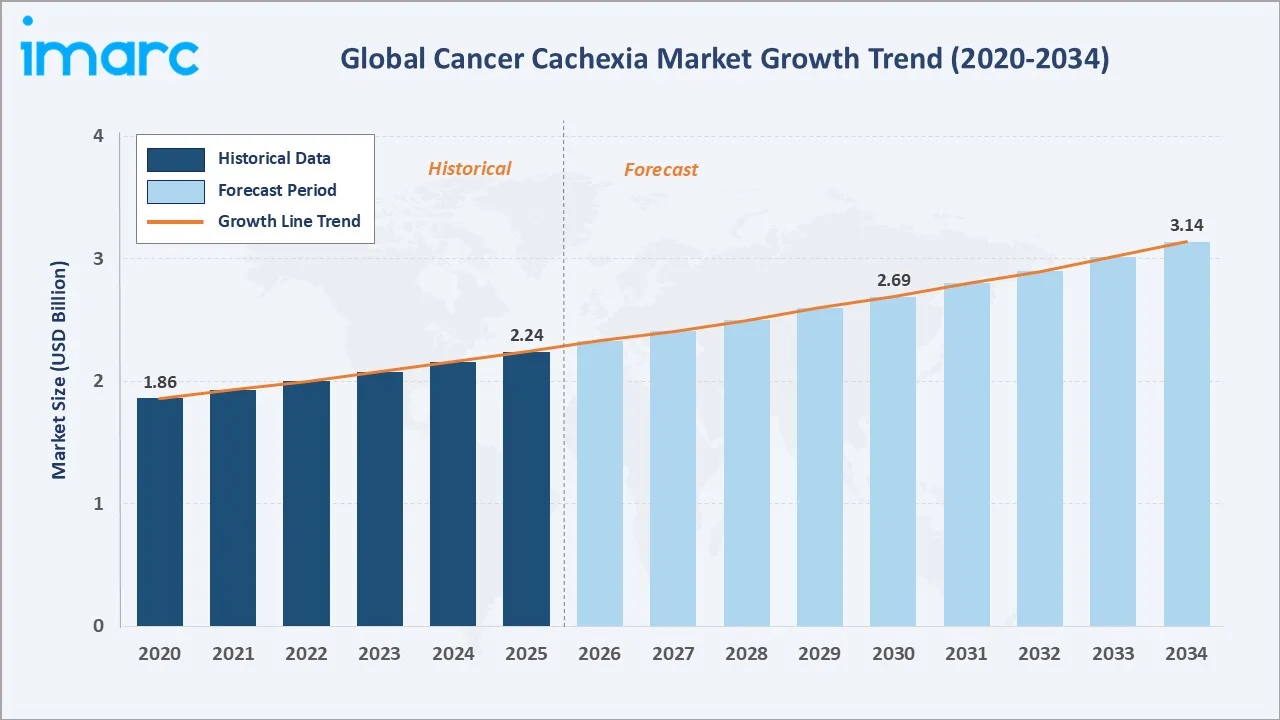

The global cancer cachexia market size reached USD 2.24 Billion in 2025 and is projected to reach USD 3.14 Billion by 2034, exhibiting a CAGR of 3.74% during 2026-2034. Rising global cancer incidence, growing recognition of cachexia's significant impact on patient outcomes, an ageing global population, and accelerating pharmaceutical R&D pipelines targeting muscle wasting and appetite dysregulation are the primary growth drivers.

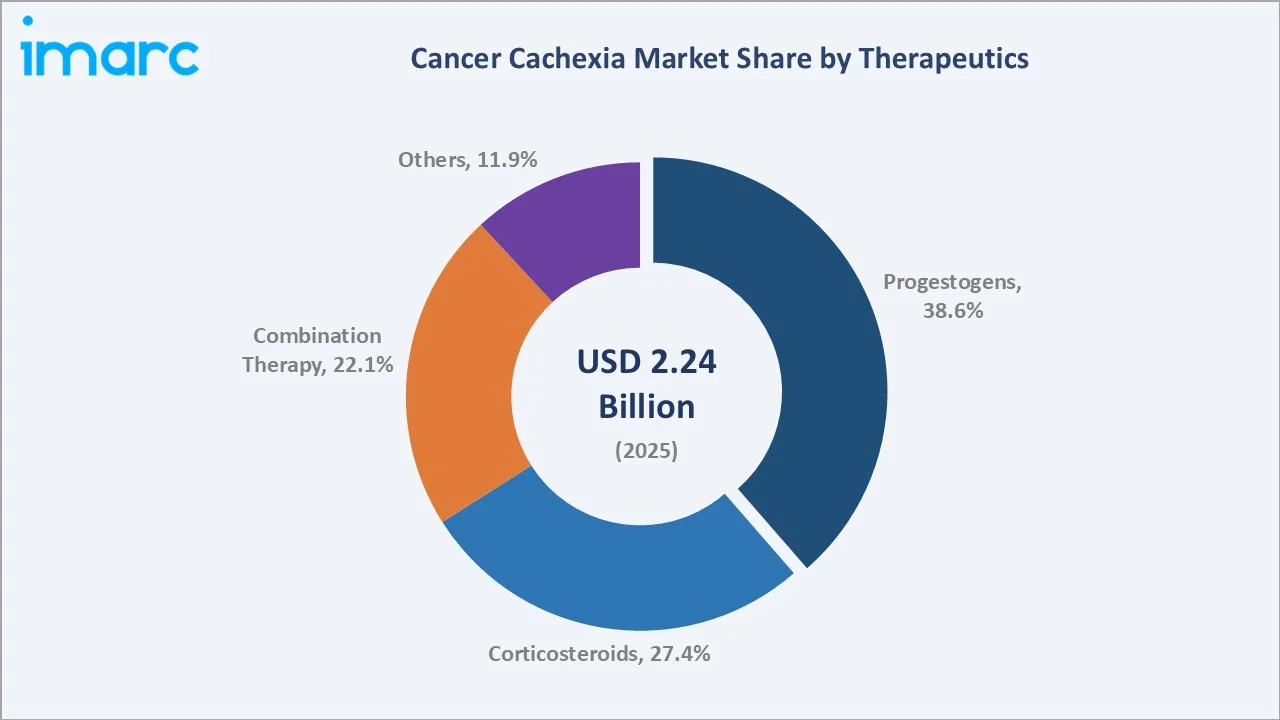

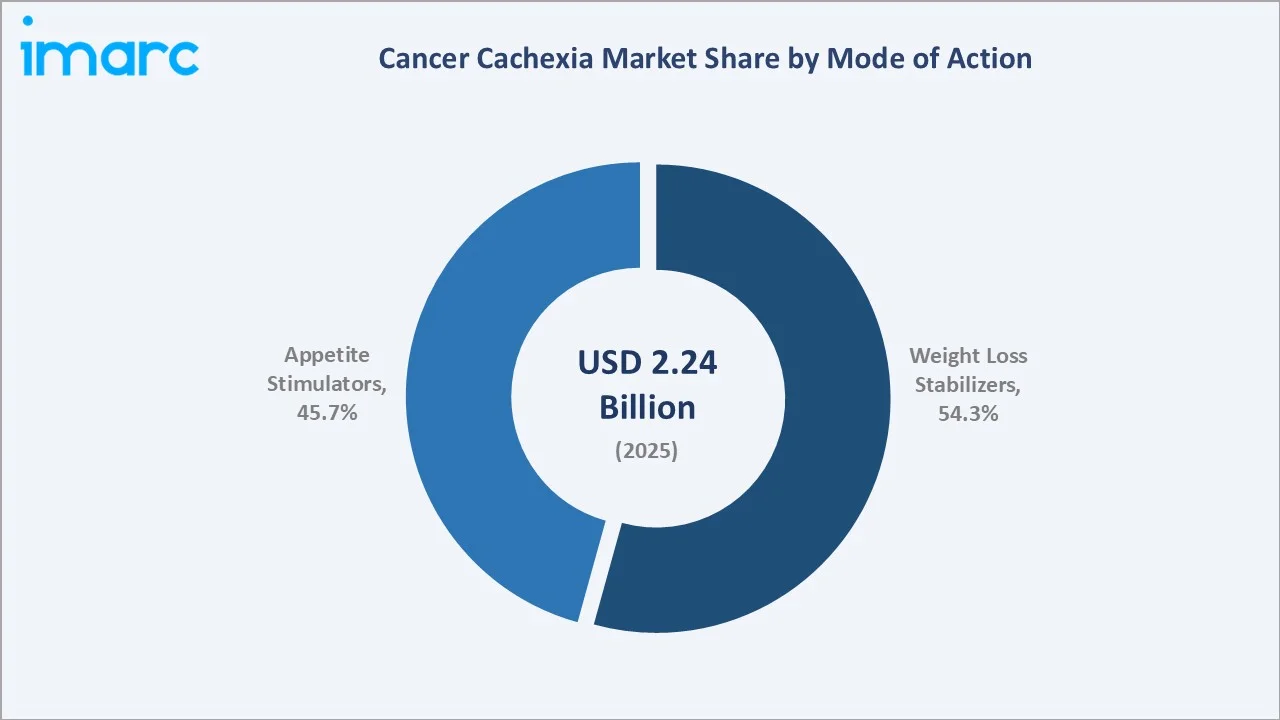

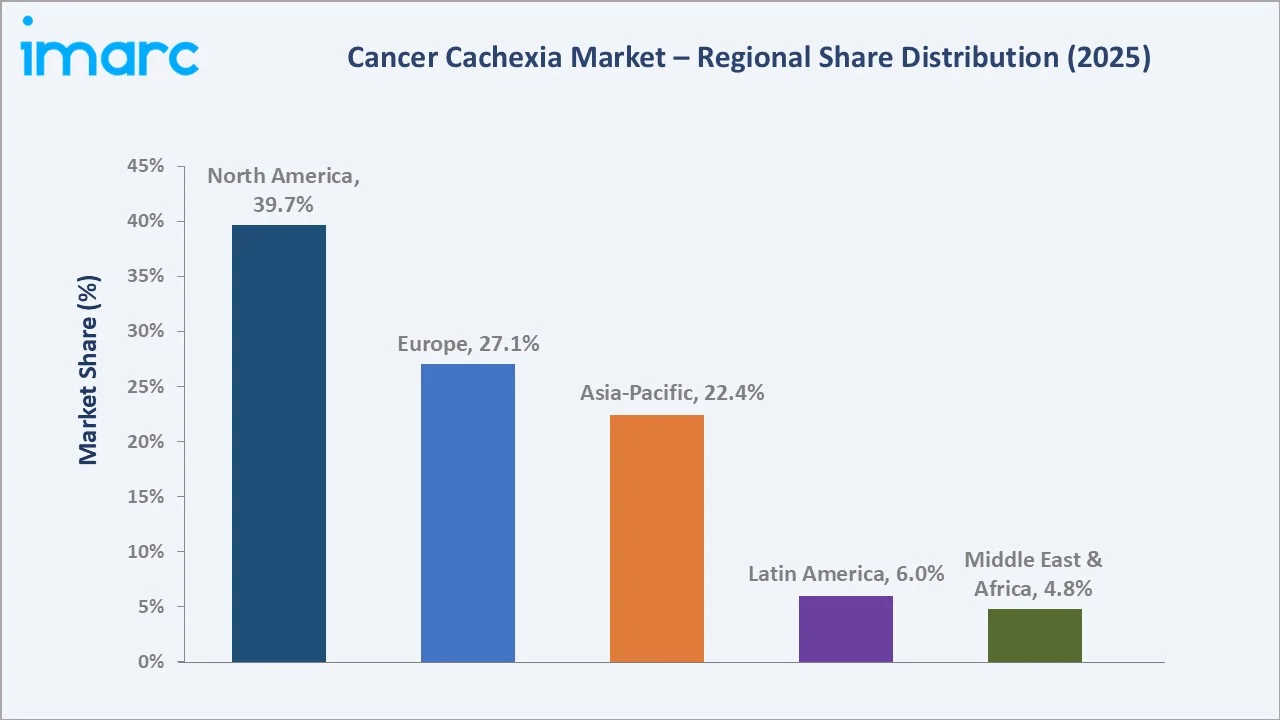

Progestogens lead the therapeutics mix at 38.6%, Weight Loss Stabilizers dominate the mode of action segment at 54.3%, and North America commands 39.7% regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.24 Billion |

|

Forecast Market Size (2034) |

USD 3.14 Billion |

|

CAGR (2026-2034) |

3.74% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Therapeutics |

Progestogens (38.6% share, 2025) |

|

Leading Mode of Action |

Weight Loss Stabilizers (54.3% share, 2025) |

|

Largest Region |

North America (39.7% share, 2025) |

|

Second Largest Region |

Europe (27.1% share, 2025) |

The growth trajectory from 2020 through 2034, with the historical expansion to USD 2.24 Billion in 2025, reflects consistent demand growth driven by oncology investment, clinical awareness improvement, and pipeline commercialisation. The forecast to USD 3.14 Billion captures expanding therapeutic access, multimodal treatment adoption, and new drug approvals across major markets globally.

To get more information on this market, Request Sample

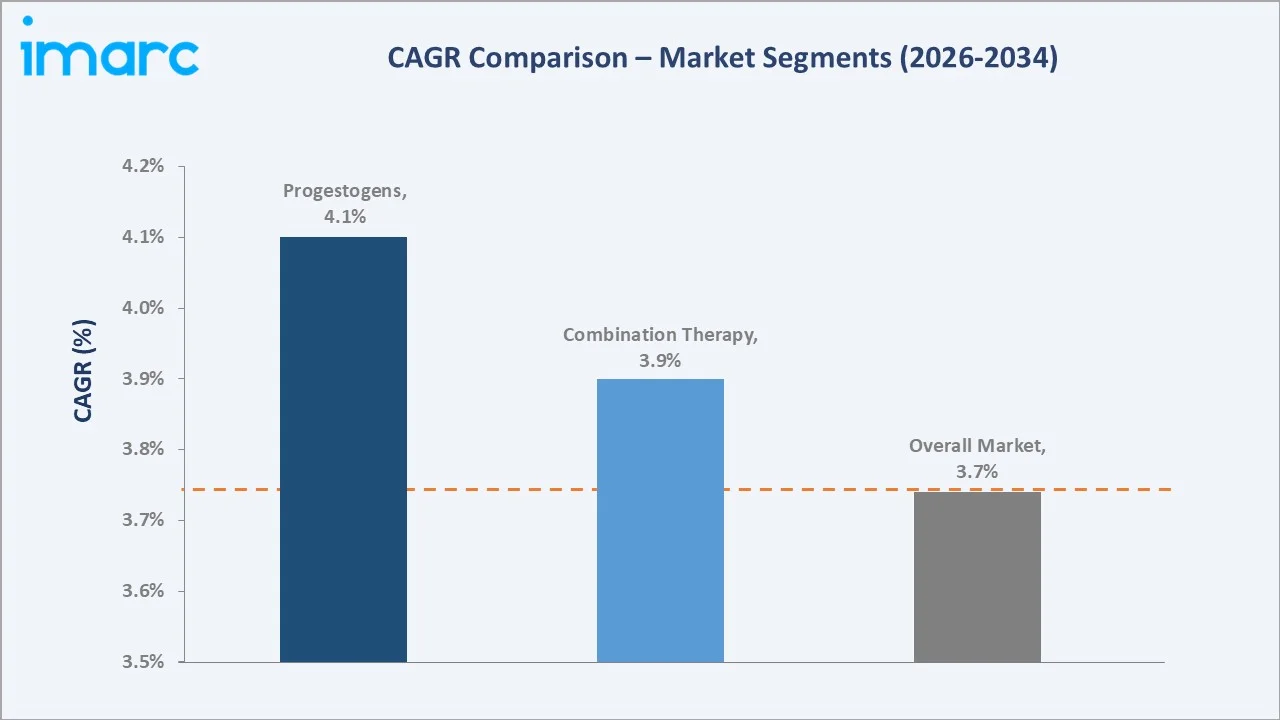

CAGR trajectories across key therapeutics, mode of action, and regional sub-segments, with Progestogens at ~4.1% CAGR and Combination Therapy at ~3.9% CAGR, are the fastest-growing categories within the global cancer cachexia market through 2034.

Executive Summary

The global cancer cachexia market is on a sustained growth trajectory from USD 2.24 Billion in 2025 to USD 3.14 Billion by 2034. Cachexia, a complex metabolic syndrome associated with underlying cancer, drives significant non-discretionary pharmaceutical and nutritional support demand across all major healthcare markets worldwide.

Progestogens dominate the therapeutics mix at 38.6% in 2025, driven by established clinical protocols, physician familiarity, and broad generic availability of megestrol acetate across global oncology care settings in both developed and developing healthcare markets.

Weight Loss Stabilizers lead the mode of action segment at 54.3% in 2025, underpinned by clinical guideline prioritisation of lean muscle mass preservation. North America commands 39.7% regional share, hosting advanced oncology infrastructure and robust pharmaceutical reimbursement frameworks that accelerate therapeutic adoption.

Key Market Insights

|

Insight |

Data |

|

Largest Therapeutics Segment |

Progestogens – 38.6% share (2025) |

|

Leading Mode of Action |

Weight Loss Stabilizers – 54.3% share (2025) |

|

Leading Region |

North America – 39.7% share (2025) |

|

Second Largest Region |

Europe – 27.1% share (2025) |

|

Top Companies |

Fresenius Kabi AG, Helsinn Healthcare SA, and Pfizer Inc. |

Key Analytical Observations Expanding On The Above Data:

- Progestogens, with 38.6% in 2025, dominate because they represent the most established and widely reimbursed pharmacological class for appetite stimulation and weight stabilisation in cachectic cancer patients across diverse global healthcare systems.

- Weight Loss Stabilizers, with 54.3% in 2025, lead because lean body mass preservation is the primary clinical objective in cachexia management, with ghrelin receptor agonists and anabolic agents gaining rapid regulatory and clinical guideline traction in major markets.

- North America, with 39.7% in 2025, dominates due to the highest concentration of oncology centres, per-capita cancer diagnosis rates, and comprehensive private and public insurance reimbursement frameworks supporting cachexia-targeted pharmaceutical and nutritional product utilisation.

- Europe, with 27.1% in 2025, benefits from coordinated multi-country clinical research frameworks, universal healthcare coverage, and strong EMA regulatory guidance supporting cachexia therapeutic approvals and integrated palliative care adoption across member states.

Global Cancer Cachexia Market Overview

Cancer cachexia is a multifactorial metabolic syndrome characterised by ongoing skeletal muscle loss, with or without fat mass loss, that cannot be fully reversed by conventional nutritional support and leads to progressive functional impairment. It affects up to 80% of patients with advanced cancer, representing a substantial and largely underserved therapeutic market opportunity globally.

The global ecosystem encompasses pharmaceutical manufacturers, clinical nutrition companies, contract research organisations, hospital oncology departments, palliative care providers, and health technology assessment bodies that collectively determine the access, reimbursement trajectory, and clinical adoption of cachexia-targeted interventions across all major geographic markets.

Market Dynamics

To evaluate market opportunities, Request Sample

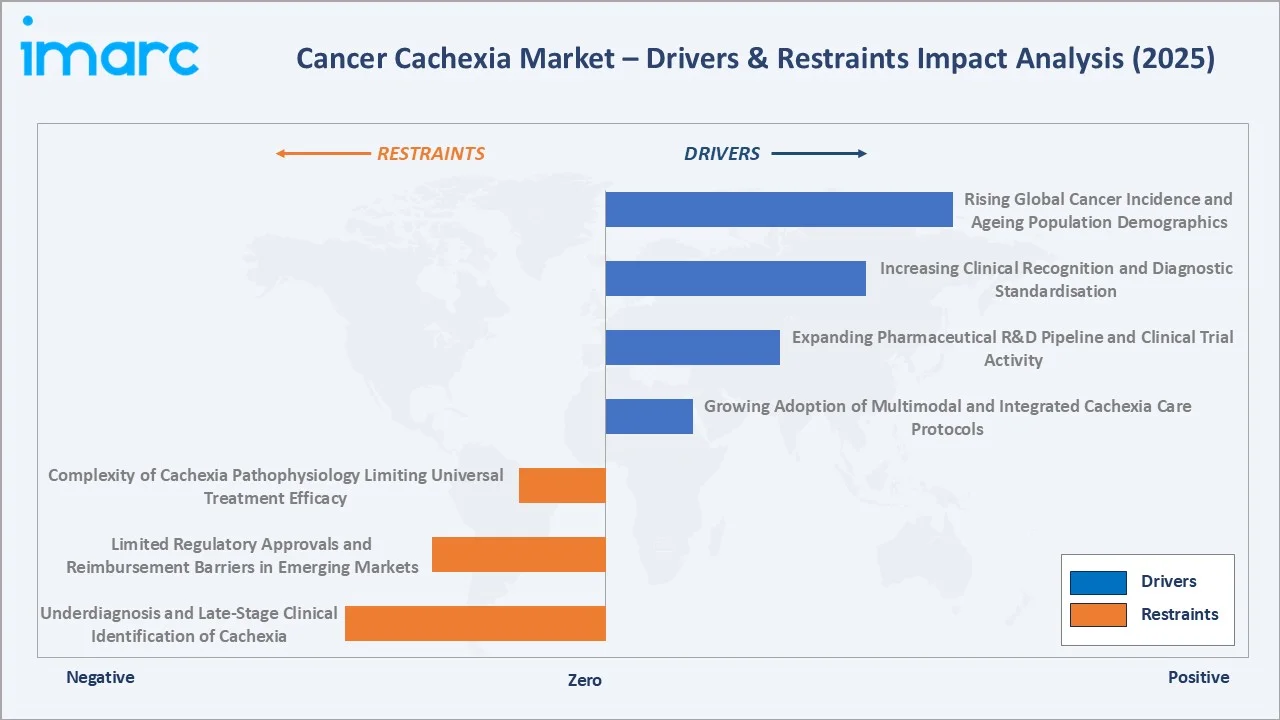

Market Drivers

- Rising Global Cancer Incidence and Ageing Population Demographics: The World Health Organization projects a 77% increase in new cancer cases within three decades, creating an expanding patient pool predisposed to cachexia. The global ageing demographic amplifies this risk, as older patients exhibit accelerated muscle catabolism and metabolic dysfunction, generating stronger non-discretionary demand for preventive and therapeutic cachexia interventions.

- Increasing Clinical Recognition and Diagnostic Standardisation: Growing physician awareness, supported by international consensus definitions from the Society on Sarcopenia, Cachexia, and Wasting Disorders, is driving earlier cachexia identification and treatment initiation. Standardised diagnostic criteria are enabling routine screening integration into oncology workflows, meaningfully expanding the diagnosed and actively treatable patient population in high-income and middle-income countries.

- Expanding Pharmaceutical R&D Pipeline and Clinical Trial Activity: Active clinical investigations of anamorelin, enobosarm, and selective androgen receptor modulators are advancing the therapeutic pipeline. Regulatory fast-track designations and orphan drug status in key markets accelerate approval timelines, with pipeline assets targeting appetite restoration and anabolic muscle repair mechanisms to address the multidimensional pathophysiology of cancer cachexia.

- Growing Adoption of Multimodal and Integrated Cachexia Care Protocols: Healthcare systems are increasingly adopting multimodal care pathways combining pharmacotherapy, medical nutrition therapy, and structured exercise programmes, improving treatment outcomes and market penetration depth. Integrated oncology-nutrition care models endorsed by major oncology societies are broadening prescribing scope and generating sustained compounding demand across therapeutic and nutritional product categories.

Market Restraints

- Complexity of Cachexia Pathophysiology Limiting Universal Treatment Efficacy: The heterogeneous molecular mechanisms underlying cancer cachexia, involving pro-inflammatory cytokines, tumour-derived catabolic factors, and neuroendocrine dysregulation, make universal therapeutic targeting exceptionally challenging. High inter-patient variability in treatment response constrains clinical trial success rates and limits regulatory approvals across the cachexia drug development landscape globally.

- Limited Regulatory Approvals and Reimbursement Barriers in Emerging Markets: Few dedicated cachexia pharmacological agents have received formal regulatory approval globally, with most treatments used off-label in routine clinical practice. In emerging markets, weak reimbursement frameworks and limited oncology infrastructure restrict patient access to evidence-based cachexia therapies, significantly suppressing market realisation relative to the true underlying patient burden.

- Underdiagnosis and Late-Stage Clinical Identification of Cachexia: Cachexia frequently goes unrecognised until advanced disease stages, substantially reducing the available treatment window and achievable efficacy of available interventions. Gaps in primary care and non-specialist oncology training for cachexia recognition delay referral and appropriate intervention, leading to suboptimal patient outcomes and limiting market penetration of available therapeutic products.

Market Opportunities

- Pipeline Drug Approvals and First-in-Class Therapeutic Launches: Successful regulatory approvals of anamorelin and novel selective androgen receptor modulators in new geographies represent transformative market expansion opportunities, with potential to establish cachexia-specific treatment categories and drive premium pricing models that significantly expand total addressable market value through 2034.

- Expansion into Asia-Pacific High-Growth Oncology Markets: Rapidly growing cancer diagnosis rates, improving oncology infrastructure, and expanding health insurance coverage in China, Japan, and South Korea present substantial growth opportunities. Localised clinical trials and regulatory submissions targeting Asia-Pacific approval pathways can accelerate adoption of cachexia therapeutics across the region's high-volume oncology care environments.

Market Challenges

- Clinical Trial Design Complexity for Cachexia-Specific Regulatory Endpoints: Defining regulatory-acceptable, clinically meaningful endpoints for cachexia trials remains actively contested, with ongoing debates around lean body mass, physical function, and quality-of-life outcome measures. Lengthy trial durations and high patient dropout rates from underlying disease progression create costly development programmes that deter smaller pharmaceutical investors.

- Balancing Tumour Treatment and Cachexia Management in Clinical Practice: Integrating cachexia management within active anti-cancer treatment protocols presents significant clinical complexity, as some chemotherapy and immunotherapy regimens exacerbate muscle catabolism. Coordinating oncology and palliative care teams around cachexia-specific interventions requires systematic investment in specialised multidisciplinary care infrastructure not yet widely available globally.

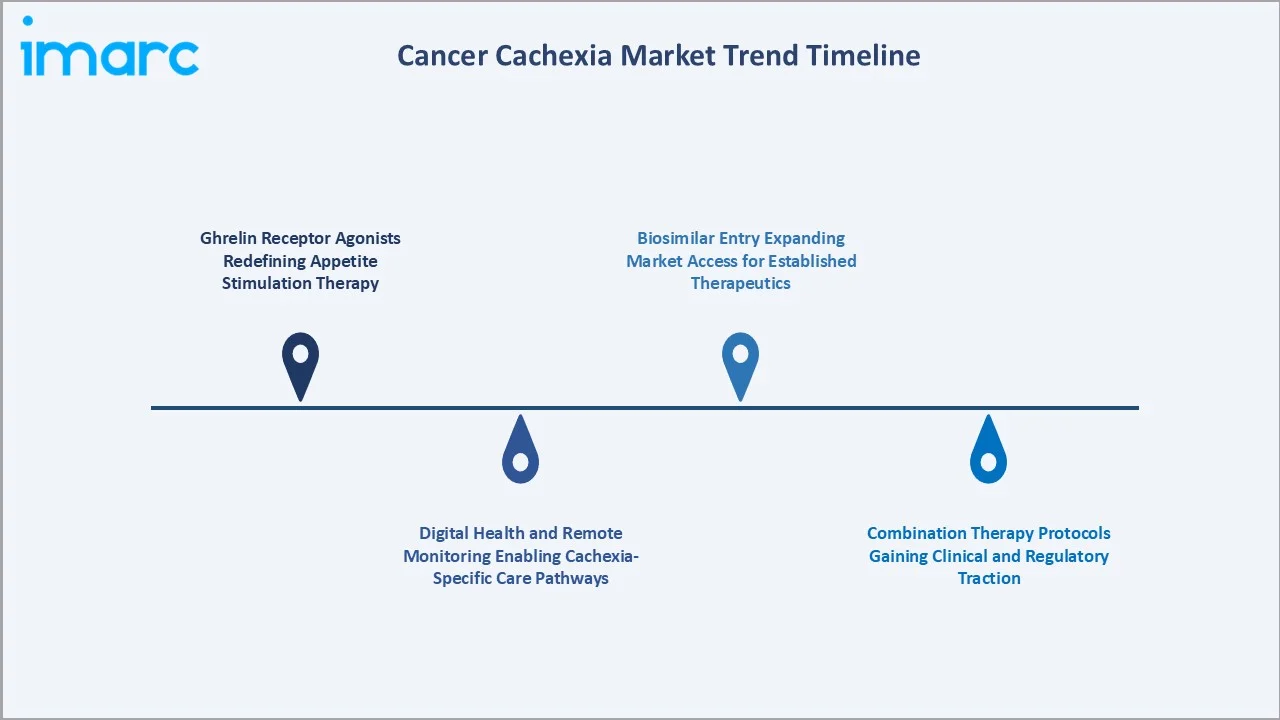

Emerging Market Trends

1. Ghrelin Receptor Agonists Redefining Appetite Stimulation Therapy

Anamorelin's commercial success in Japan and ongoing approvals across additional Asia-Pacific markets are establishing ghrelin mimetics as a new pharmacological standard in cachexia management, shifting the therapeutic paradigm from progestogen-dominant to mechanism-targeted appetite restoration approaches that deliver superior tolerability profiles through the forecast period.

2. Digital Health and Remote Monitoring Enabling Cachexia-Specific Care Pathways

Wearable devices and telehealth platforms are enabling continuous monitoring of body composition, physical activity, and nutritional intake in cachectic patients outside formal clinical settings. Remote care models are expanding market reach by facilitating proactive intervention at earlier cachexia stages, improving clinical outcomes and driving sustained product utilisation across therapeutic and nutritional support categories.

3. Combination Therapy Protocols Gaining Clinical and Regulatory Traction

Growing clinical evidence supports multicomponent cachexia treatment combining appetite stimulants, anti-inflammatory agents, and anabolic compounds simultaneously to address multiple pathophysiological drivers. Pharmaceutical companies are actively developing fixed-dose combination products targeting multiple cachexia pathways, creating new premium-priced product categories with differentiated clinical positioning through 2034.

4. Biosimilar Entry Expanding Market Access for Established Therapeutics

Patent expiries of foundational cachexia therapeutics are enabling biosimilar and generic market entry, particularly for progestogens, meaningfully expanding patient access in cost-sensitive healthcare systems. Increased affordability is growing the actively treated population in Latin America, Southeast Asia, and Eastern Europe, incrementally expanding the global revenue base for market participants.

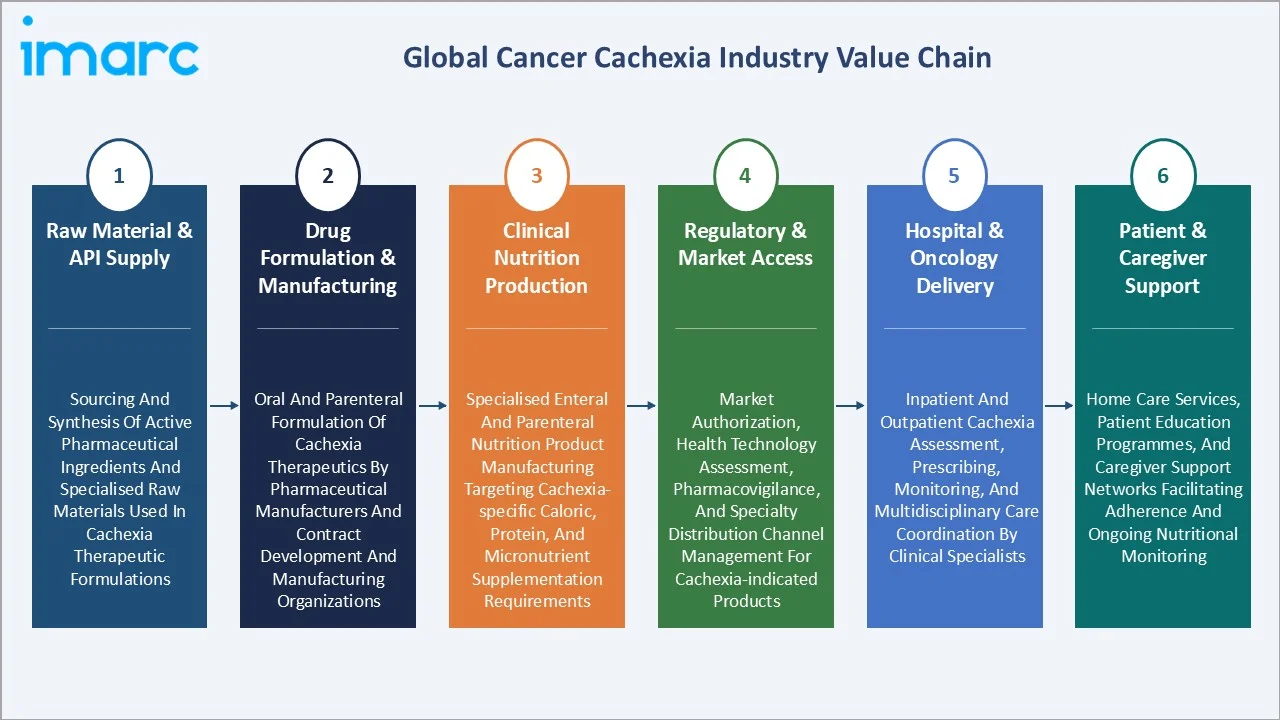

Industry Value Chain Analysis

The global cancer cachexia market value chain spans six core stages from active pharmaceutical ingredient production through patient care delivery. Pharmaceutical formulation and clinical nutrition manufacturing capture the highest value-add margins, while hospital oncology and palliative care delivery constitute the highest-volume patient touchpoint in the full cachexia care continuum.

|

Stage |

Description |

|

Raw Material & API Supply |

Sourcing and synthesis of active pharmaceutical ingredients and specialised raw materials used in cachexia therapeutic formulations |

|

Drug Formulation & Manufacturing |

Oral and parenteral formulation of cachexia therapeutics by pharmaceutical manufacturers and contract development and manufacturing organisations |

|

Clinical Nutrition Production |

Specialised enteral and parenteral nutrition product manufacturing targeting cachexia-specific caloric, protein, and micronutrient supplementation requirements |

|

Regulatory & Market Access |

Market authorisation, health technology assessment, pharmacovigilance, and specialty distribution channel management for cachexia-indicated products |

|

Hospital & Oncology Delivery |

Inpatient and outpatient cachexia assessment, prescribing, monitoring, and multidisciplinary care coordination by clinical specialists |

|

Patient & Caregiver Support |

Home care services, patient education programmes, and caregiver support networks facilitating adherence and ongoing nutritional monitoring |

Technology Landscape in the Global Cancer Cachexia Industry

Ghrelin Receptor Agonists and Novel Anabolic Agents

Anamorelin hydrochloride, a selective ghrelin receptor agonist, has demonstrated statistically significant improvements in lean body mass and patient-reported appetite scores in Phase III clinical trials, marking a paradigm shift in pharmacological cachexia management. Research into selective androgen receptor modulators continues to advance, offering anabolic tissue-specific muscle building without androgenic side effects associated with conventional anabolic steroids.

Biomarker-Guided Personalised Cachexia Therapy Development

Advances in inflammatory biomarker profiling, including interleukin-6, tumour necrosis factor-alpha, and C-reactive protein panels, are enabling personalised cachexia treatment selection matched to individual patient inflammatory phenotypes. Genomic and proteomic approaches are progressively identifying patient subpopulations most likely to respond to specific therapeutic classes, improving clinical trial efficiency and real-world treatment outcomes.

Body Composition Assessment and Monitoring Technologies

CT-based sarcopenia assessment, dual-energy X-ray absorptiometry, and bioelectrical impedance-based body composition monitoring are becoming standard cachexia diagnostic tools in leading oncology centres globally. These technologies enable precise lean mass quantification, supporting regulatory endpoint validation for clinical trials and enabling earlier, more targeted therapeutic intervention strategies.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Therapeutics | Progestogens | 38.6% | 2025 |

| Mode of Action | Weight Loss Stabilizers | 54.3% | 2025 |

| Distribution Channel | 🔒 | 🔒 | 2025 |

| Region | North America | 39.7% | 2025 |

By Therapeutics

Progestogens command a 38.6% majority share in 2025owing to their established clinical track record, physician familiarity, and broad generic availability across global markets. Megestrol acetate, the primary progestogen used in cachexia management, is widely reimbursed and benefits from decades of real-world efficacy and safety data accumulated across diverse oncology care settings internationally.

To access detailed market analysis, Request Sample

Corticosteroids at 27.4% in 2025reflect their rapid onset of appetite stimulation and widespread oncology familiarity among prescribers globally. Short-term corticosteroid regimens remain prevalent in inpatient cachexia management settings where immediate appetite improvement is prioritised alongside ongoing active cancer treatment protocols.

Combination Therapy (22.1%) is gaining traction as clinical evidence accumulates supporting multicomponent approaches addressing appetite stimulation, muscle anabolism, and anti-inflammatory mechanisms concurrently. Others (11.9%) encompass emerging ghrelin agonists, cannabinoid-based therapies, and investigational agents advancing through late-stage global clinical trials.

By Mode of Action

Weight Loss Stabilizers dominate at 54.3% in 2025, reflecting clinical prioritisation of lean body mass preservation as the primary cachexia management objective. Anabolic agents, weight-stabilising nutritional formulations, and muscle-preserving pharmacotherapies collectively constitute this segment, underpinned by strong international clinical guideline endorsements from major oncology and palliative care societies.

Appetite Stimulators at 45.7% in 2025represent the well-established pharmacological and nutritional intervention approach targeting reduced food intake in cachectic cancer patients across all care settings. Progestogens, corticosteroids, and emerging ghrelin agonists drive this segment, with growing clinical evidence supporting appetite restoration as a primary driver of downstream weight stabilisation and functional improvement.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

39.7% |

Advanced oncology infrastructure, comprehensive insurance reimbursement, leading pharmaceutical innovation, and high physician awareness of cachexia management protocols |

|

Europe |

27.1% |

Universal healthcare coverage, EMA regulatory framework, coordinated multi-country clinical research, and strong integration of palliative care into oncology pathways |

|

Asia-Pacific |

22.4% |

Rapidly rising cancer incidence, improving oncology infrastructure, expanding health insurance in China and Japan, and growing regulatory engagement with cachexia therapies |

|

Latin America |

6.0% |

Growing oncology patient volumes, improving hospital infrastructure in Brazil and Mexico, and increasing generic progestogen availability expanding treatment access |

|

Middle East & Africa |

4.8% |

Expanding oncology centre infrastructure in Gulf Cooperation Council states, rising cancer awareness, and growing pharmaceutical distribution network development |

North America's 39.7% dominance in 2025 is driven by the highest concentration of specialised oncology and palliative care centres, comprehensive insurance reimbursement for cachexia therapeutics, and leading pharmaceutical companies headquartered in the region actively investing in cachexia drug development, regulatory submissions, and commercial infrastructure.

Asia-Pacific, with 22.4% share in 2025, is experiencing the most dynamic growth trajectory, anchored by rising cancer diagnosis rates in China, Japan's anamorelin approval establishing a precedent for regional regulatory harmonisation, and rapidly expanding oncology infrastructure across South and Southeast Asian healthcare systems through the forecast period.

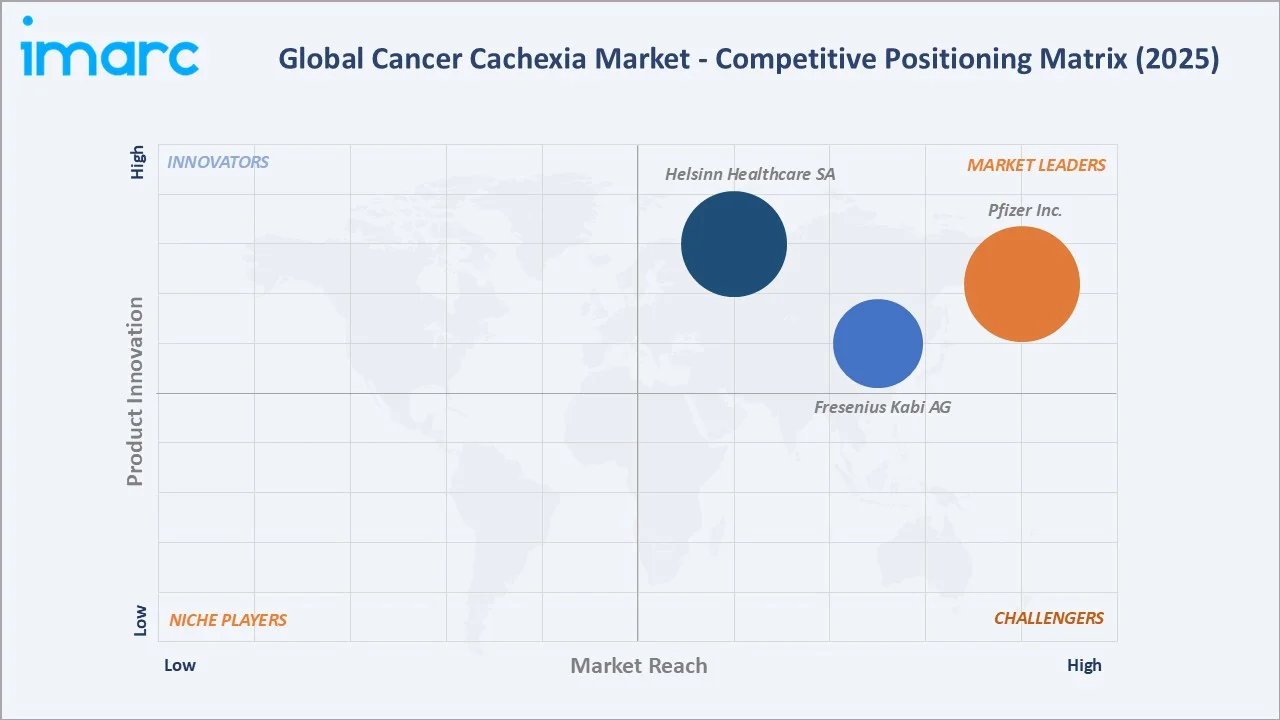

Competitive Landscape

The global cancer cachexia market is served by a mix of large diversified pharmaceutical corporations, specialty oncology companies, and emerging biopharmaceutical firms focused on novel cachexia mechanisms. Competition is intensifying as pipeline assets approach regulatory approval and established players accelerate geographic expansion of approved therapeutics across high-growth markets.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

|

Fresenius Kabi AG |

Clinical nutrition, IV drugs, medical devices |

Leader |

Parenteral and enteral nutrition for oncology patients; hospital pharmacy supply; cachexia-specific nutritional formulae |

|

Helsinn Healthcare SA |

Adlumiz (anamorelin) |

Leader |

First approved cachexia-specific ghrelin receptor agonist; geographic expansion into North America and additional Asia-Pacific markets |

|

Pfizer Inc. |

Ponsegromab |

Leader |

Pipeline investment in anabolic and anti-inflammatory cachexia targets across multiple indications |

Key players include Fresenius Kabi AG, Helsinn Healthcare SA, and Pfizer Inc., among others.

Key Company Profiles

Fresenius Kabi AG

Fresenius Kabi AG is a global leader in clinical nutrition and infusion therapy headquartered in Bad Homburg, Germany. The company is a primary supplier of specialised enteral and parenteral nutritional solutions to oncology departments worldwide, directly addressing the critical nutritional intervention component of cancer cachexia management.

- Product Portfolio: Clinical nutrition, IV drugs, medical devices

- Strategic Focus: Fresenius Kabi's cachexia strategy centres on expanding its specialised oncology nutrition portfolio, partnering with leading cancer centres to integrate evidence-based nutritional therapy into standard cachexia management protocols, and accelerating market access in high-growth Asia-Pacific oncology markets through targeted distribution partnerships.

Helsinn Healthcare SA

Helsinn Healthcare SA is a Swiss private pharmaceutical group headquartered in Lugano, Switzerland, specialising in oncology supportive care. Helsinn developed and commercialised ADLUMIZ (anamorelin), the first ghrelin receptor agonist approved specifically for cancer cachexia in Japan.

- Product Portfolio: ADLUMIZ (anamorelin) (Japan)

- Strategic Focus: Helsinn's strategy focuses on expanding anamorelin regulatory approvals into North American and additional Asia-Pacific markets, establishing global clinical and commercial precedents for ghrelin-mimetic cachexia therapies, and positioning ADLUMIZ as the international standard of care for non-small cell lung cancer-associated cachexia.

Market Concentration Analysis

The global cancer cachexia market is moderately fragmented, with no single company holding more than 15% of total market revenue due to the absence of a dominant universal cachexia therapeutic and the diversity of treatment modalities spanning pharmaceuticals, clinical nutrition, and oncology supportive care products across global healthcare systems.

Consolidation is emerging through strategic licensing agreements, co-development partnerships, and targeted acquisition of cachexia pipeline assets by larger diversified pharmaceutical companies. Helsinn's anamorelin approval is accelerating competitive responses, with multiple Phase II and III cachexia-specific programmes initiated by global pharmaceutical leaders since 2023 across diverse mechanism-of-action targets.

Investment & Growth Opportunities

Fastest-Growing Segments

Combination Therapy at ~3.9% CAGR through 2034 represents the highest-growth therapeutics segment, driven by clinical guideline evolution toward multimodal treatment frameworks addressing multiple cachexia pathways simultaneously. Progestogens at ~4.1% CAGR reflect expanding generic market penetration in emerging economies coupled with growing diagnosed patient populations globally.

Emerging Markets and Applications

Asia-Pacific's rapidly expanding oncology infrastructure, particularly Japan's anamorelin commercialisation and China's growing clinical trial activity in cachexia-specific endpoints, represents the most strategically significant emerging cachexia market. Regulatory harmonisation across ASEAN oncology markets creates scalable market entry opportunities for cachexia therapeutic innovators seeking geographic portfolio expansion.

Venture and Investment Trends

Private investment into cachexia-focused biopharmaceutical programmes reached notable levels in 2024, with gene therapy, selective androgen receptor modulator, and ghrelin agonist platforms attracting substantial venture capital and pharmaceutical partnership investment. Government-funded oncology research grants from the US National Institutes of Health, EU Horizon programme, and Japan Agency for Medical Research are catalysing collaborative cachexia mechanism research globally.

Future Market Outlook (2026-2034)

The global cancer cachexia market is forecast to expand from USD 2.24 Billion in 2025 to USD 3.14 Billion by 2034 at a CAGR of 3.74%, adding USD 0.90 Billion in incremental annual market value over the forecast period, representing sustained therapeutic and nutritional sector expansion aligned with rising global cancer incidence and improving cachexia treatment paradigms.

Three forces will most significantly shape the cancer cachexia market landscape through 2034: Anamorelin's geographic expansion creating a dedicated ghrelin-based therapeutic category globally, combination therapy clinical validation driving international protocol standardisation, and Asia-Pacific regulatory maturation progressively unlocking the region's substantial unmet cachexia patient burden.

Personalised biomarker-guided cachexia therapy, supported by advances in inflammatory profiling and digital body composition monitoring technologies, will further stratify the addressable market, enabling precision prescribing approaches that improve measurable clinical outcomes and support premium pricing frameworks for mechanism-targeted innovative therapeutic agents.

Research Methodology

Primary Research

Primary research encompassed structured interviews with oncologists, palliative care physicians, clinical dietitians, pharmaceutical industry executives, and health technology assessment specialists globally. Primary data collection validated market sizing estimates, segment shares, regional breakdowns, treatment protocol adoption rates, reimbursement dynamics, and drug pipeline development timelines.

Secondary Research

Key secondary sources include World Health Organization cancer incidence and mortality reports, National Cancer Institute clinical trial databases, European Medicines Agency regulatory documents, pharmaceutical company annual reports and pipeline disclosures, peer-reviewed oncology and palliative care journals, and international cachexia consensus society publications and clinical practice guidelines.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting models incorporating cancer incidence growth rates, cachexia prevalence rates by cancer type, therapeutic penetration assumptions by geography, pricing trend analysis, and reimbursement expansion timelines. Scenario analysis across base, optimistic, and conservative cases was performed to account for macroeconomic and regulatory uncertainty.

Cancer Cachexia Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Therapeutics Covered | Progestogens, Corticosteroids, Combination Therapy, Others |

| Modes of Action Covered | Appetite Stimulators, Weight Loss Stabilizers |

| Distribution Channels Covered | Hospital Stores, Retail Pharmacy, Online Pharmacy |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Fresenius Kabi AG, Helsinn Healthcare SA, Pfizer Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the cancer cachexia market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global cancer cachexia market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the cancer cachexia industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Cancer Cachexia Market Report

The global cancer cachexia market reached USD 2.24 Billion in 2025, driven by rising global cancer incidence, growing clinical awareness of cachexia's impact on patient outcomes, and expanding pharmaceutical pipeline investment in targeted therapeutic approaches.

The market is projected to reach USD 3.14 Billion by 2034, growing at a CAGR of 3.74% during 2026-2034, supported by new therapeutic approvals, multimodal treatment adoption, Asia-Pacific market expansion, and increasing physician and patient awareness of cachexia as a distinct clinical entity.

Progestogens lead with a 38.6% therapeutics share in 2025, driven by established clinical protocols, strong physician familiarity, and broad generic availability of megestrol acetate across oncology care settings globally in both developed and developing healthcare markets.

Weight Loss Stabilizers dominate at 54.3% in 2025, valued for lean body mass preservation as the primary clinical management objective in cachexia, supported by anabolic pharmacotherapy, ghrelin-based agents, and specialised clinical nutrition interventions endorsed by major oncology societies.

North America commands 39.7% market share in 2025, driven by advanced oncology infrastructure, comprehensive insurance reimbursement frameworks, high cancer diagnosis rates, and concentrated pharmaceutical innovation and clinical research activity headquartered in the United States.

Asia-Pacific is the fastest-growing region, benefiting from rapidly rising cancer incidence, Japan's anamorelin regulatory precedent, expanding health insurance coverage in China, and accelerating oncology infrastructure investment across South and Southeast Asia through the 2026–2034 forecast period.

Progestogens is the fastest-growing therapeutics segment at ~4.1% CAGR through 2034, reflecting expanding generic market penetration in emerging economies, growing diagnosed patient populations, and well-established reimbursement pathways in major healthcare systems globally.

Leading companies include Fresenius Kabi AG, Helsinn Healthcare SA, and Pfizer Inc.

Primary challenges include the complex and heterogeneous pathophysiology of cachexia limiting universal therapeutic efficacy, limited formal regulatory approvals for cachexia-specific agents, reimbursement barriers in emerging markets, and the clinical difficulty of integrating cachexia management within active anti-cancer treatment protocols in routine oncology practice.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)