Canned Food Market Size, Share, Trends and Forecast by Product Type, Type, Distribution Channel, and Region 2026-2034

Global Canned Food Market Size, Share, Trends & Forecast (2026-2034)

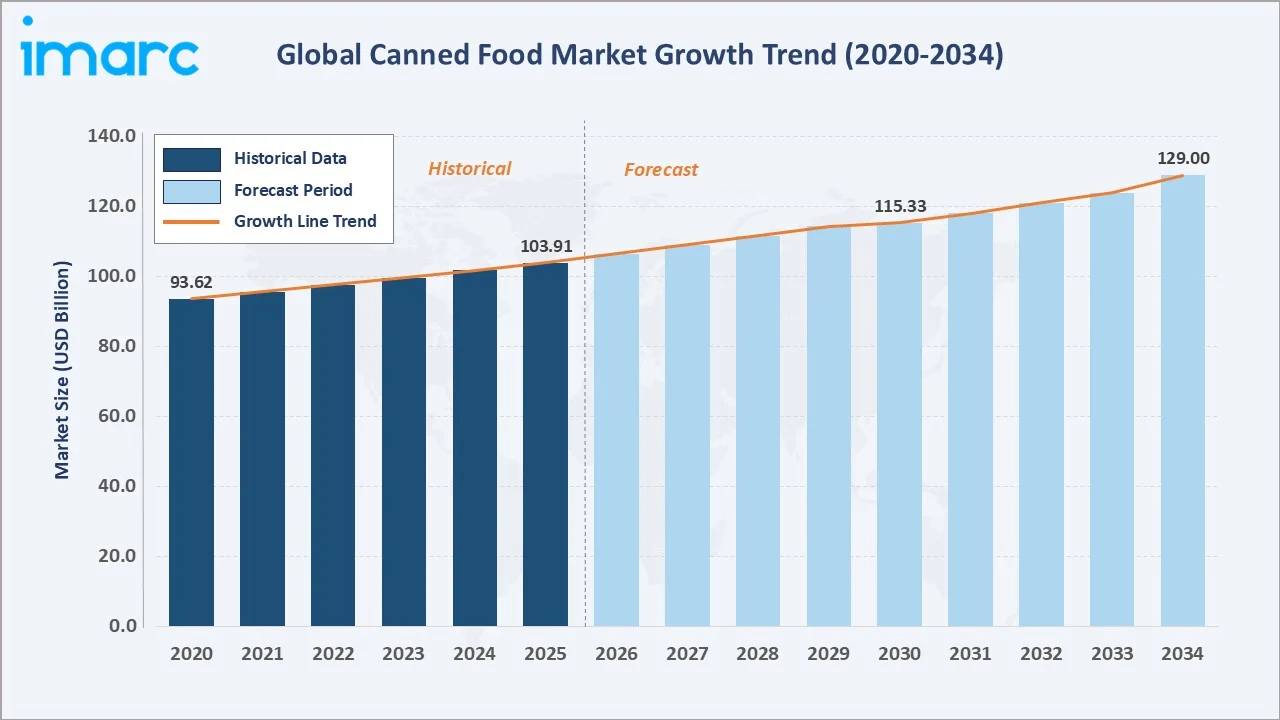

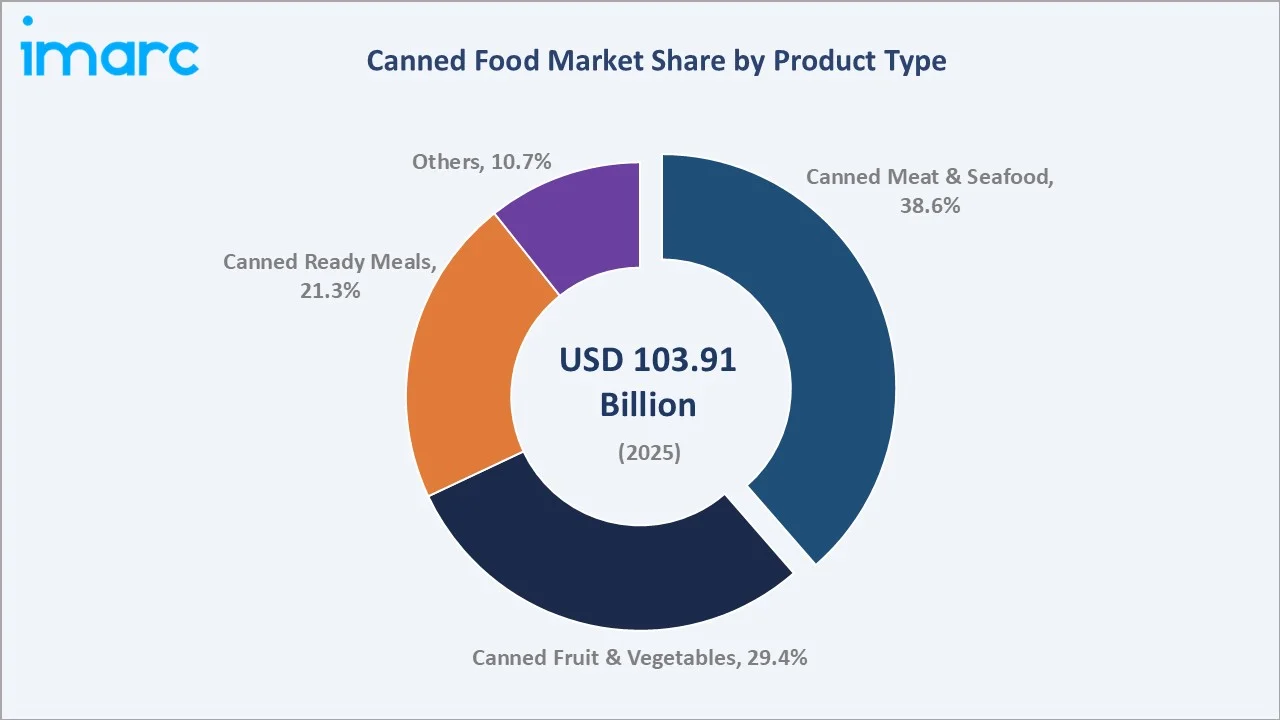

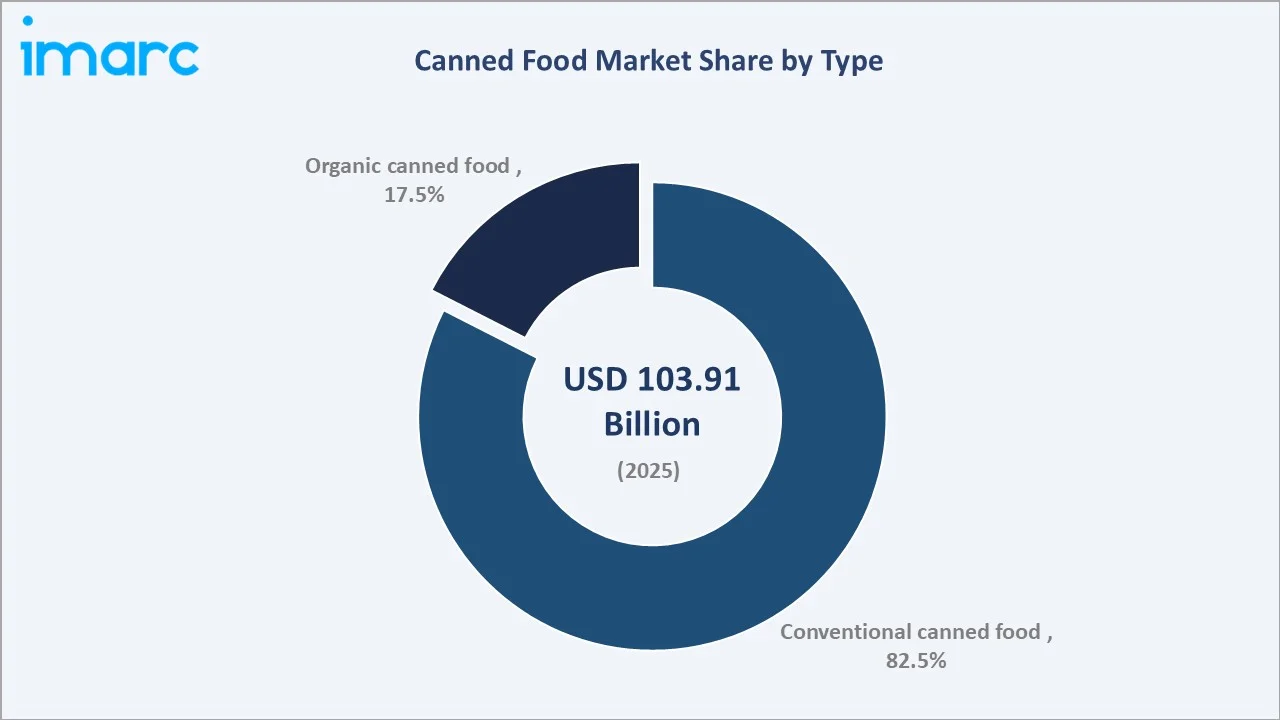

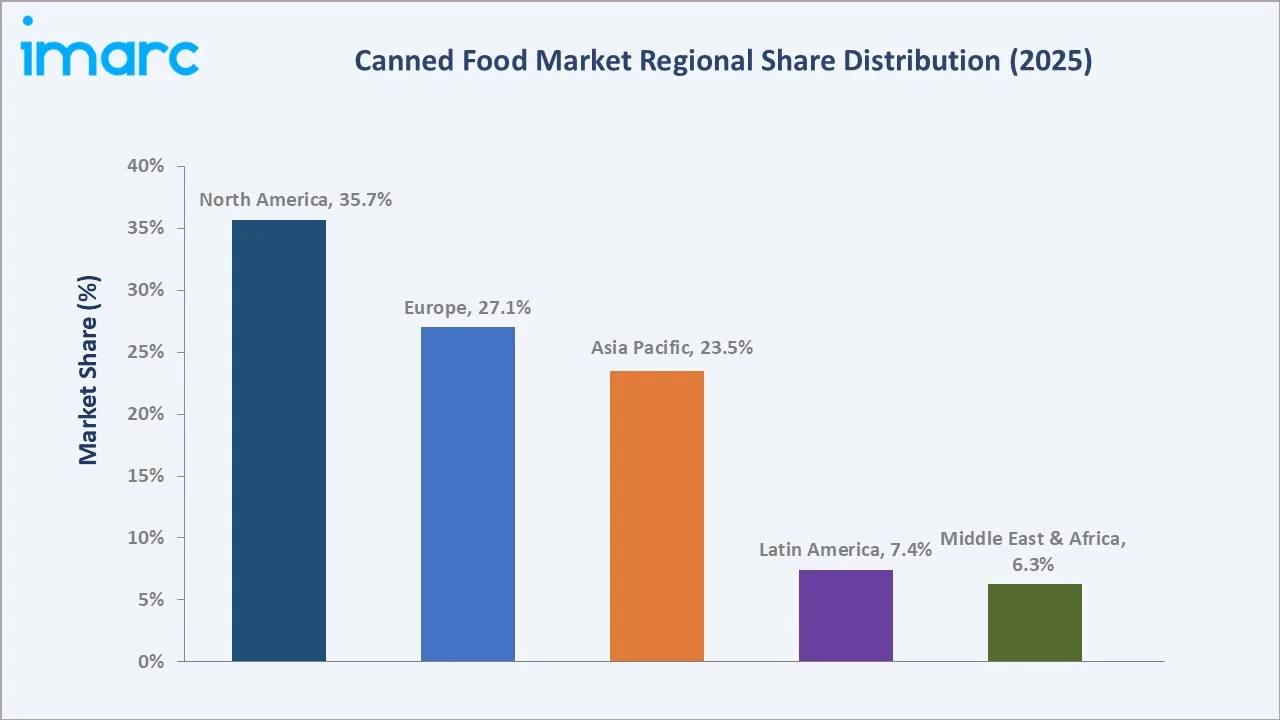

The global canned food market size was valued at USD 103.91 Billion in 2025 and is projected to reach USD 129.00 Billion by 2034, exhibiting a CAGR of 2.11% during the forecast period 2026-2034. Rising demand for convenient, shelf-stable food products, the proliferation of busy urban lifestyles, and expanding retail and e-commerce penetration are the principal growth engines. Canned Meat and Seafood leads by product type at 38.6% in 2025, while Conventional products dominate the type segment at 82.5%. North America holds the largest regional share at 35.7% of global revenue in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2020) |

USD 93.62 Billion |

|

Market Size (2025) |

USD 103.91 Billion |

|

Forecast Market Size (2030) |

USD 115.33 Billion |

|

Forecast Market Size (2034) |

USD 129.00 Billion |

|

CAGR (2026-2034) |

2.11% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (35.7% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~3.5%) |

|

Leading Product Type |

Canned Meat and Seafood (38.6%, 2025) |

|

Leading Type |

Conventional (82.5%, 2025) |

The chart shows global canned food market growth from 2020–2034, with steady historical expansion and sustained future growth driven by urbanization, changing preferences, and product innovation.

To get more information on this market, Request Sample

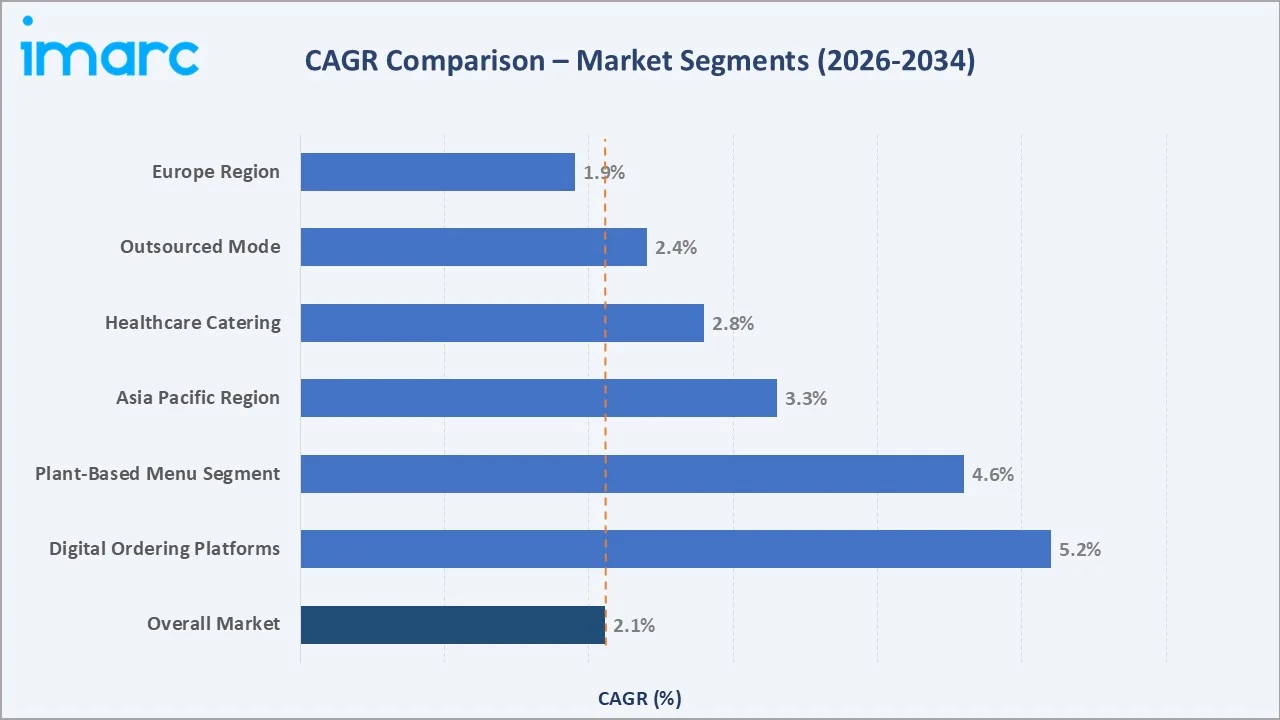

Segment CAGR analysis shows Canned Ready Meals and Organic as the fastest-growing categories through 2034, driven by premiumization and rising wellness-focused consumer demand.

Executive Summary

The global canned food market is expanding due to lifestyle shifts, innovation, and retail growth. Valued at USD 103.91 billion in 2025, it is projected to reach USD 129.00 billion by 2034 (2.11% CAGR). Rising dual-income households and a growing workforce are increasing demand for convenient, long-shelf-life, ready-to-consume canned foods globally.

Canned Meat and Seafood lead with 38.6% share in 2025, driven by high-protein demand, foodservice use, and emergency stocking. Canned Ready Meals (21.3%) is the fastest-growing segment, fuelled by convenience among urban consumers. The Organic segment (17.5%) is expanding quickly, supported by premiumization trends and strong growth in the global organic food market.

North America leads with 35.7% share in 2025, supported by strong retail infrastructure and high per-capita consumption. Europe holds 27.1%, driven by premium and organic demand and private-label growth. Asia Pacific, at 23.5%, is the fastest-growing region, fuelled by urbanization, rising incomes in China and India, and expanding modern retail channels.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Canned Meat and Seafood – 38.6% share (2025) |

|

Second Largest Product Type |

Canned Fruit and Vegetables – 29.4% share (2025) |

|

Leading Type |

Conventional – 82.5% share (2025) |

|

Fastest Growing Type |

Organic – expanding at ~4.85% CAGR (2026-2034) |

|

Leading Region |

North America – 35.7% revenue share (2025) |

|

Second Region |

Europe – 27.1% revenue share (2025) |

|

Top Companies |

Nestlé, Conagra Brands, Del Monte Foods, Hormel Foods, Campbell Soup, Bolton Group |

|

Market Opportunity |

Asia Pacific e-commerce grocery penetration + organic premiumization |

Key Analytical Observations Supporting The Above Data:

- Canned Meat and Seafood's 38.6% dominance in 2025 reflects strong protein demand, emergency preparedness stocking, and consistent use in foodservice and institutional catering segments globally.

- Organic canned food, holding a 17.5% share in 2025, is expanding rapidly as consumers increasingly prefer clean-label, sustainably sourced, and healthier canned food alternatives.

- North America's 35.7% global leadership in 2025 is driven by mature retail infrastructure, high household penetration of canned goods, and strategic emergency food stockpiling post-COVID-19 pandemic in 2020.

- Canned Ready Meals hold a 21.3% share in 2025, driven by dual-income households and increasing demand for convenient, restaurant-quality meal options.

- Asia Pacific holds 23.5% of global revenue in 2025 and is the fastest-growing region, driven by strong digital adoption. China, the world’s largest e-commerce market, generated USD 2.16 trillion in online retail sales in 2024, accelerating online distribution and sales of canned food products.

- Europe holds a 27.1% share in 2025, driven by strict EU food safety standards, expanding retailer private-label offerings, and growing demand for sustainably packaged canned protein products.

Global Canned Food Market Overview

Canned food refers to products preserved through thermal sterilization in airtight containers, extending shelf life to two to five years without refrigeration. The global canned food ecosystem includes manufacturers, agricultural and seafood suppliers, packaging producers, distribution channels such as supermarkets and e-commerce platforms, and end consumers across retail and foodservice segments.

Canned foods are widely used across retail, foodservice, institutional catering, and emergency relief. Growing urbanization 57% of the global population in cities in 2024, projected to reach 68% by 2050 along with expansion of the food and beverage industry, continues to drive demand for convenient, processed food options, including canned products.

Market Dynamics

To evaluate market opportunities, Request Sample

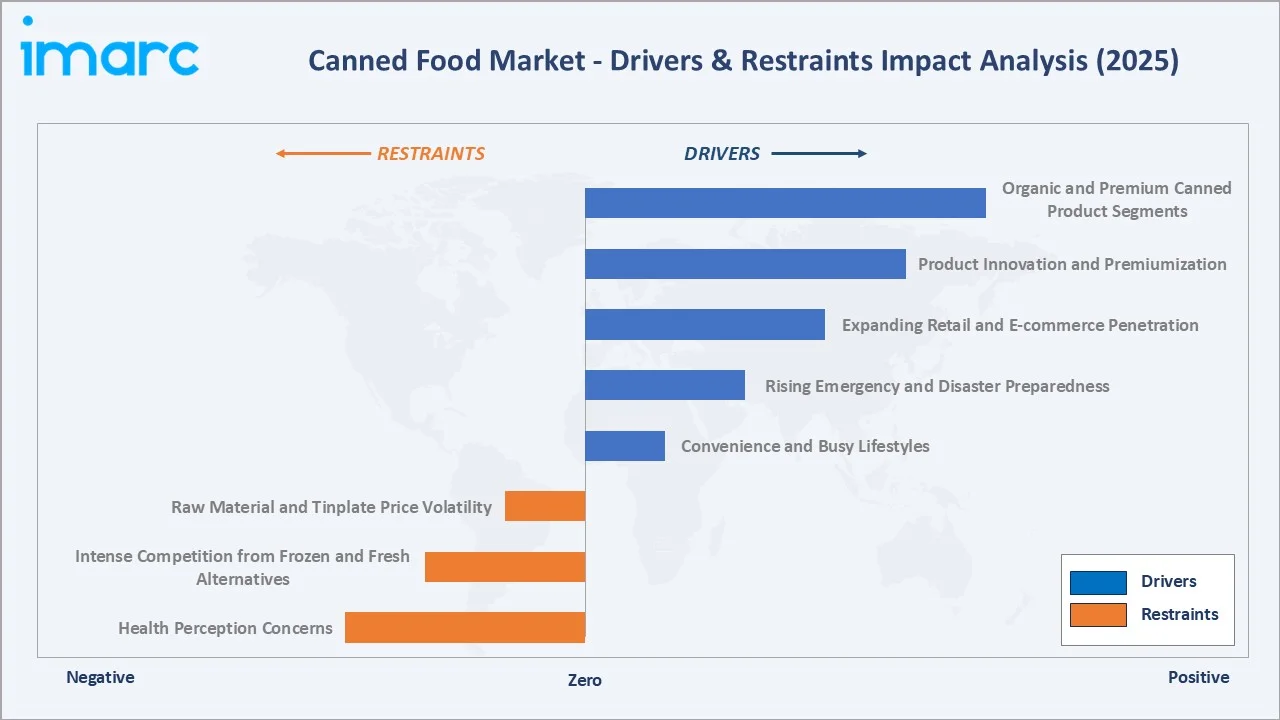

Market Drivers

- Convenience and Busy Lifestyles: Around 55% of U.S. households are dual-income, increasing demand for minimal-preparation meals. Canned and convenience foods reduce cooking effort and planning time, making them suitable for busy consumers and working families.

- Rising Emergency and Disaster Preparedness: Post-COVID-19, stockpiling behaviour increased, boosting demand for shelf-stable and canned foods. This shift continues to drive structural demand for canned proteins, staples, and long-shelf-life food products.

- Expanding Retail and E-commerce Penetration: Global e-commerce grocery sales reached approximately USD 650 Billion in 2024, with canned goods among the top purchased categories due to lightweight shipping economics and no refrigeration requirements.

- Product Innovation and Premiumization: The introduction of BPA-free cans, pull-tab convenience lids, organic and ethnic cuisine variants, and reduced-sodium formulations is expanding the addressable consumer base beyond traditional demographics.

Market Restraints

- Health Perception Concerns: Nearly 40% of consumers consider canned foods less nutritious than frozen, and nearly 60% view them as inferior to fresh options, with health and sodium concerns limiting adoption among wellness-focused consumers.

- Intense Competition from Frozen and Fresh Alternatives: The global frozen food market exceeded USD 295 Billion in 2024, offering comparable convenience with a "fresher" health perception. This positions frozen meals as a direct substitute for canned ready meals.

- Raw Material and Tinplate Price Volatility: Steel and aluminium—key canning materials, face price volatility, with rising metal costs during 2021–2022 increasing packaging expenses and compressing manufacturer margins.

Market Opportunities

- Organic and Premium Canned Product Segments: Organic canned foods carry a premium price over conventional options. Manufacturers obtaining organic certifications can tap into higher-margin opportunities and growing demand for premium, clean-label products.

- Asia Pacific E-commerce Channel Expansion: Alibaba and JD.com dominate China’s online grocery ecosystem, making direct-to-consumer canned food presence on these platforms a strong opportunity for incremental revenue growth for global and regional brands.

- Private Label and Retailer Collaboration: Private-label canned goods hold strong share across European retail, particularly in staple categories like beans and tomatoes. Partnering with private labels enables manufacturers to drive volume while reducing marketing costs.

Market Challenges

- Sustainability and Packaging Perception: Consumer concern about metal packaging recyclability and BPA liner safety is intensifying. While steel cans are 100% recyclable, brand communication around environmental credentials remains a persistent challenge.

- Supply Chain Complexity Across Raw Material Categories: Canned food requires sourcing from diverse agricultural, fishery, and protein supply chains simultaneously, each with independent seasonality, geopolitical, and climate-related disruption risks.

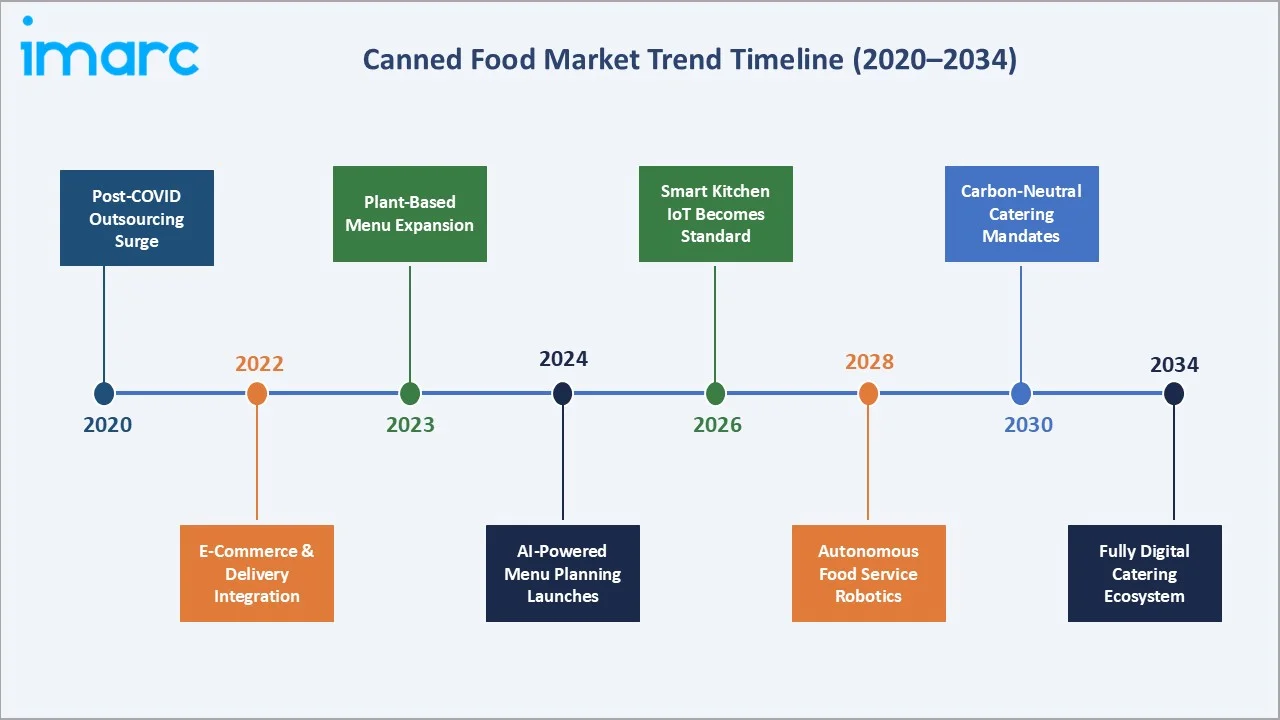

Emerging Market Trends

1. Organic and Clean-Label Canned Product Expansion

Rising consumer willingness to pay for certified-organic canned foods across North America and Western Europe is accelerating premium segment growth, with brands like Amy's Kitchen and Eden Foods outperforming conventional canned categories.

2. Sustainable and BPA-Free Packaging Innovation

Growing consumer concern over BPA in traditional can linings has driven widespread adoption of BPA-free materials across major North American manufacturers. Combined with high steel recycling rates in Europe and the U.S., canned foods present a strong sustainability positioning for environmentally responsible packaging.

3. E-commerce and Direct-to-Consumer Channel Growth

Online grocery channels are becoming an important sales driver for canned foods, with e-commerce capturing a growing share of U.S. grocery purchases. Shelf-stable canned products benefit from favourable shipping economics, while subscription pantry services and direct-to-consumer models are emerging as key growth opportunities.

4. Global Cuisine Diversification in Canned Formats

The expansion of ethnic and international cuisines in canned formats such as Thai curries, Indian dals, Mexican meals, Japanese broths, and Korean specialties is attracting new consumer demographics. Rising global demand for ethnic foods, driven by multicultural exposure and convenience preferences, positions canned formats as an accessible entry point for international Flavors.

5. Functional and Fortified Canned Food Products

Manufacturers are increasingly introducing canned products with functional health claims such as high-protein, reduced sodium, added fiber, and fortified nutrients. The expanding functional food trend is enabling canned formats to reposition toward health-conscious millennial and Gen-Z consumers.

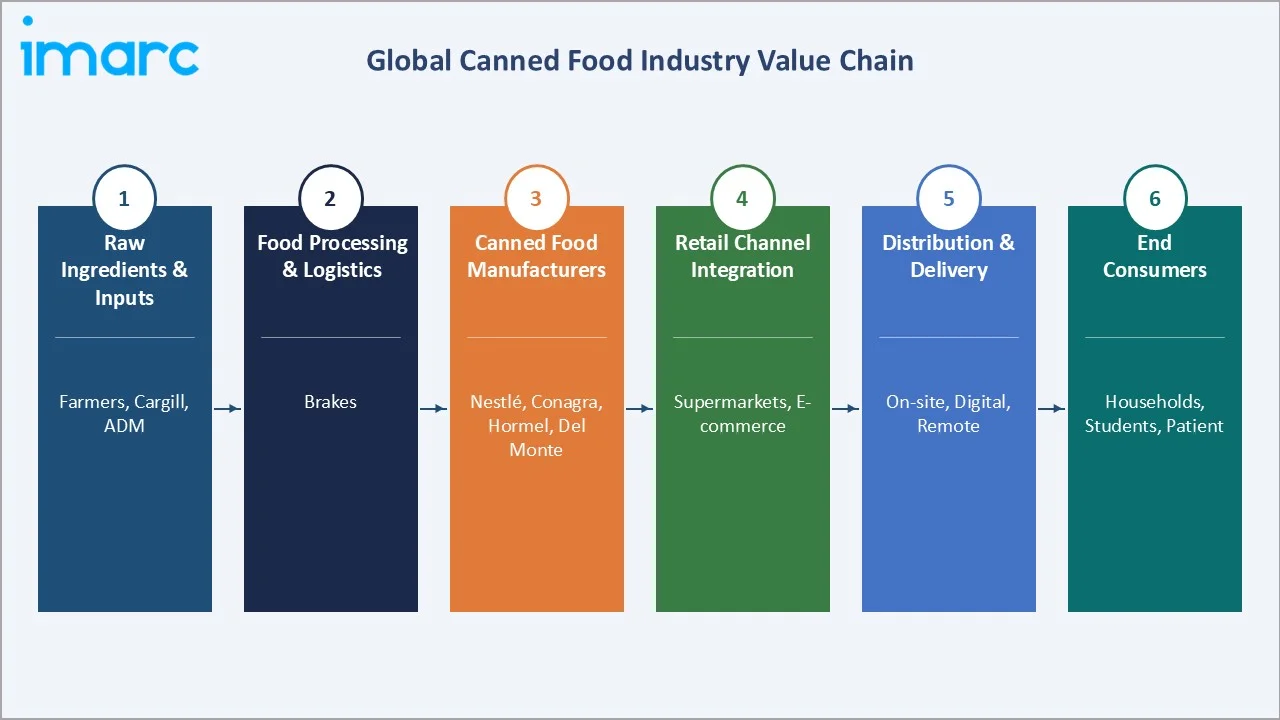

Industry Value Chain Analysis

The canned food value chain includes six stages, from raw material sourcing to consumer delivery, each with unique competitive, quality, and logistics requirements.

|

Stage |

Key Players / Examples |

|

Raw Material Suppliers |

Agricultural producers, commercial fisheries, livestock processors, tin plate & aluminum can manufacturers (Ardagh Group, Crown Holdings, Ball Corporation) |

|

Food Processing & Manufacturing |

Nestlé, Conagra Brands, Hormel Foods, Del Monte Foods, Bolton Group, Princes Group |

|

Packaging & Labeling |

Silgan Containers, Crown Holdings, Trivium Packaging |

|

Distribution & Logistics |

CHEP, XPO Logistics, Sysco (foodservice), Walmart Distribution, Amazon Fulfillment Network |

|

Retail Channels |

Walmart, Kroger, Carrefour, Aldi, Lidl, Amazon Fresh, JD.com, Alibaba Freshippo |

|

End Consumers |

Households, foodservice operators, hospitality sector, institutional catering, emergency relief agencies (WFP, Red Cross) |

Food processing and manufacturing represent the most strategic stage in the canned food value chain. Backward integration into raw material sourcing provides cost and quality advantages. Meanwhile, growing private-label competition increases pressure on branded manufacturers, requiring continuous investment in innovation, branding, and promotional strategies to maintain shelf presence and competitiveness.

Technology Landscape in the Canned Food Industry

Advanced Canning and Sterilization Technology

Retort sterilization using pressurized steam remains the foundation of canned food processing. While high-pressure processing is primarily used in flexible packaging, continuous rotary retorts enhance production efficiency and throughput, supporting high-volume canned food manufacturing.

BPA-Free and Sustainable Lining Innovations

The shift from BPA-based epoxy linings to acrylic, polyester, and alternative coatings has driven significant industry R&D investment. Companies such as Sherwin-Williams and PPG Industries are developing next-generation can coating systems, while recyclable mono-material pouches are emerging as a potential disruptive packaging format.

Smart Packaging and Digital Connectivity

QR-code enabled cans linking consumers to traceability, recipes, and sustainability content are gaining adoption. Emerging smart packaging technologies, including NFC-based connected packaging pilots, offer opportunities for dynamic content, authentication, and loyalty integration as the smart packaging market continues to expand.

Automated Manufacturing and Industry 4.0

Canning lines are increasingly adopting robotics, machine vision, and AI-based quality control to improve efficiency and reduce defects. High-speed automated operations support large-scale production, while digital twin technologies are being piloted to optimize processing parameters and enhance energy efficiency.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Canned Meat and Seafood |

38.6% |

2025 |

|

Type |

Conventional |

82.5% |

2025 |

|

Distribution Channel |

Supermarkets and Hypermarkets |

🔒 |

2025 |

|

Region |

North America |

35.7% |

2025 |

By Product Type

Canned Meat and Seafood commands a 38.6% majority share in 2025, reflecting strong protein demand across household, foodservice, and institutional channels. The segment benefits from long shelf life, typically lasting several years, and growing emergency preparedness demand in North America and Europe. Key sub-categories include canned tuna, salmon, sardines, chicken, and corned beef, with tuna representing the leading share of global canned seafood consumption.

To access detailed market analysis, Request Sample

Canned Fruit and Vegetables at 29.4% in 2025 represent a core household pantry category, supported by year-round availability of seasonal produce and stable pricing. The introduction of no-added-sugar and low-sodium variants is further expanding consumer appeal. Canned Ready Meals at 21.3%, growing steadily, are emerging as a key convenience-driven segment. Others (10.7%) include canned soups, broths, dairy-based products, and infant formula categories.

By Type

Conventional canned food commands 82.5% of global market volume in 2025, supported by price competitiveness, wide retail availability, and strong consumer brand familiarity. Mature canning technologies enable cost-efficient production, keeping prices accessible across income segments. The conventional segment remains particularly dominant in value retail, foodservice, and institutional catering channels.

Organic canned food holds 17.5% market share in 2025 and is expanding faster than the overall canned food market, driven by rising demand for clean-label and sustainably sourced products. Premium organic brands typically command higher price premiums, reflecting perceived quality and health benefits. The implementation of EU Regulation 2018/848 in January 2022 standardized organic certification across member states, improving cross-border trade and providing greater regulatory clarity for export-focused manufacturers.

Regional Market Insights

The regional distribution of the global canned food market in 2025 reflects distinct consumption patterns, retail infrastructure maturity, regulatory environments, and income levels across five major geographies.

The regional share data confirms North America's structural leadership, with Europe and Asia Pacific as co-significant contributors representing over 50% of global revenue combined.

|

Region |

Market Share (2025) |

Key Growth Drivers |

Major Companies |

|

North America |

35.7% |

Emergency preparedness, busy lifestyles, mature retail, high per-capita consumption |

Conagra Brands, Campbell Soup, Hormel Foods, Del Monte Foods |

|

Europe |

27.1% |

Organic premiumization, private-label growth, stringent EU food safety standards (EC 178/2002) |

Nestlé, Bolton Group, Princes Group, Lidl/Aldi private label |

|

Asia Pacific |

23.5% |

Urbanization, rising middle class, e-commerce grocery expansion, China & India growth |

Zishan Group, Ayam Brand, Thai Union, Nissin Foods |

|

Latin America |

7.4% |

Population growth, urbanization, retail formalization, Brazil & Mexico demand |

Sigma Alimentos, Lala, Cárnicos Fray Bentos |

|

Middle East & Africa |

6.3% |

Food security programs, humanitarian aid demand, growing urban middle class |

Al Alali, Princes Group MENA, Gino Foods |

North America

North America accounts for 35.7% of global canned food revenue in 2025, led by the United States. Strong demand for convenient, shelf-stable foods, strict FDA 21 CFR Part 113 safety standards, and sustained post-pandemic pantry stocking continue supporting regional canned food consumption growth.

Europe

Europe contributes 27.1% of global canned food revenue in 2025, with Germany, France, Italy, and the UK representing key national markets. European consumers are leading the organic transition, with organic food sales exceeding €53 billion in 2022. The EU Farm-to-Fork Strategy targeting 25% organic farmland by 2030 is expected to expand organic ingredient supply and support premium canned product growth.

Asia Pacific

Asia Pacific holds 23.5% of global market share in 2025 and represents the fastest-growing region through 2034. Growth is driven by China’s large food processing sector and India’s expanding FMCG retail network. Rapid adoption of e-commerce platforms, including JD.com and Alibaba’s Freshippo, is further strengthening digital-channel opportunities for canned food brands targeting urban consumers.

Competitive Landscape

The global canned food market is moderately consolidated, with multinational brands dominating shelf space, while regional manufacturers and private-label programs remain key competitive forces.

|

Company |

Notable Brand(s) |

Market Position |

Core Strength |

|

Nestlé S.A. |

Carnation, Milkmaid, Libby’s Pumpkin |

Global Leader |

Brand portfolio breadth, global distribution, R&D scale |

|

Conagra Brands, Inc. |

Hunt’s, Van Camp’s, Rotel |

Leader – North America |

U.S. retail dominance, diverse canned food portfolio |

|

Hormel Foods Corporation |

SPAM, Dinty Moore, Hormel Chili |

Leader – Canned Meat |

SPAM global brand recognition, strong Asia Pacific penetration |

|

The Campbell’s Company |

Campbell’s, Swanson, Chunky |

Leader – Soups & Broths |

Soup category leadership, premium Pacific Foods acquisition |

|

Bolton Group S.r.l. |

Rio Mare, Isabel, Saupiquet |

Leader – Europe Tuna |

European seafood canned market leadership, premium positioning |

|

Thai Union Group PCL |

John West, Chicken of the Sea, Petit Navire |

Challenger – Global Seafood |

World's largest tuna processor, broad brand portfolio |

|

NewPrinces S.p.A. |

Princes, Napolina, Fray Bentos |

Challenger – Europe |

UK/Europe canned protein and vegetable distribution scale |

Key Company Profiles

Nestlé S.A.

- Overview: Nestlé is the world's largest food and beverage company, headquartered in Vevey, Switzerland, with annual sales of CHF 91.4 Billion in FY2024. Its canned food operations span soups, ready meals, and canned dairy products across 186 countries.

- Product Portfolio: Carnation evaporated and sweetened condensed milk products, Milkmaid canned condensed milk, and Libby’s Pumpkin.

- Recent Developments: Nestlé launched its "Net Zero Roadmap" in 2023, targeting sustainably sourced raw materials for all major product lines by 2030. In September 2024, Nestlé launched Stouffer's Supreme Shells & Cheese, marking Stouffer's first shelf-stable (ambient) product outside frozen foods.

Conagra Brands

- Overview: Conagra Brands is a leading U.S. food company headquartered in Chicago, Illinois, with net sales of USD 12.3 Billion in fiscal 2024. The company's canned food portfolio covers tomato products, pasta meals, and canned vegetables sold across North American retail and foodservice channels.

- Product Portfolio: Hunt’s (canned tomatoes & sauces), Van Camp’s (canned beans), and ROTEL (canned tomatoes & chilies).

- Recent Developments: In June 2025, Conagra Brands completed the sale of Chef Boyardee (canned pasta meals) to Hometown Food Company. In 2025, Conagra indicated potential price increases for canned foods such as Hunt’s tomatoes due to tariffs on tin-plate steel used in cans.

Hormel Foods Corporation

- Overview: Hormel Foods is a global branded food company headquartered in Austin, Minnesota, with approximately USD 12.1 billion in fiscal 2023 net sales. Its flagship SPAM brand is sold in 40+ countries and maintains particularly strong demand across Asia-Pacific markets, including South Korea, the Philippines, and Japan.

- Product Portfolio: SPAM (canned luncheon meat), Hormel Chili (canned chili), Mary Kitchen Hash (canned corned beef & hash), and Dinty Moore (canned beef stew and meals).

- Recent Developments: In September 2024, Hormel launched SPAM® Gochujang, inspired by Korean cuisine, expanding its canned meat portfolio. In July 2025, Hormel introduced Limited-Edition Green Eggs & SPAM Classic Twin Pack in collaboration with Dr. Seuss Enterprises.

Market Concentration Analysis

The global canned food market exhibits moderate fragmentation, with the top five players - Nestlé, Conagra Brands, Campbell, Hormel Foods, and Bolton Group - collectively accounting for approximately 28-32% of global branded market revenue in 2025. The balance is distributed among hundreds of regional brands, co-manufacturers, and - critically - retailer private-label programs.

Private-label canned food has reached 38% category share in several European markets and approximately 20-25% in the U.S. (IRI/Circana, 2024). This private-label penetration acts as a structural price ceiling for branded manufacturers and incentivizes differentiation through premium ingredients, organic certification, and convenience-format innovation.

Consolidation in the canned food industry has remained moderate but strategically focused. Key transactions include Thai Union’s acquisition of John West (2010, ~EUR 680 million), Conagra’s USD 10.9 billion acquisition of Pinnacle Foods (2018), and Hormel’s USD 3.35 billion purchase of the Planters brand (2021). Additional bolt-on acquisitions targeting organic, premium, and ethnic canned food brands are expected during the forecast period.

Investment & Growth Opportunities

Fastest Growing Segments

- Organic Canned Food: Faster growth in organic canned foods is creating premiumization opportunities, with investments in USDA and EU-certified supply chains and premium SKUs supporting higher-margin growth.

- Canned Ready Meals: Ready-to-eat canned meals represent a fast-growing conventional segment, with co-manufacturing partnerships with restaurant brands offering a low-capital expansion strategy.

- E-commerce-Optimized Canned Products: Subscription pantry services and D2C canned meal kits are emerging channels requiring packaging redesign for parcel shipping and digital-first brand strategy.

Emerging Markets

- China, India, and Southeast Asia represent major underpenetrated markets, supported by strong growth in e-commerce grocery platforms and rising digital grocery adoption in 2024.

- Middle East and Africa Food Security Programs: Regional government food security initiatives and expanding urban middle class in Saudi Arabia, UAE, and Nigeria create structural demand for shelf-stable canned food.

Venture and Strategic Investment Trends

- Packaging Innovation Investments: BPA-free lining, reclosable can formats, and smart packaging integration are attracting both strategic corporate R&D investment and venture capital attention.

- Vertical Integration in Sustainable Sourcing: Investment in traceable, sustainably certified sourcing—such as MSC-certified tuna and Rainforest Alliance agricultural inputs—strengthens brand credibility and reduces ESG risk exposure.

Future Market Outlook (2026-2034)

The global canned food market is projected to grow from USD 103.91 Billion in 2025 to USD 129.00 Billion by 2034, representing net market value addition of USD 25.09 Billion over the forecast period. This sustained, moderate growth reflects the category's structural resilience as a convenience and emergency staple, while acknowledging competitive pressure from fresh, frozen, and ambient pouch food formats.

Technology will drive competitive differentiation, with companies investing in smart packaging, clean-label products, and AI-enabled supply chains expected to outperform. Meanwhile, EU Packaging and Packaging Waste Regulation (PPWR) requirements mandating recyclable packaging by 2030 will accelerate adoption of next-generation sustainable can designs..

Asia Pacific will remain the fastest-growing regional market, with India emerging as a key growth contributor driven by expanding organized retail. Rising private-label penetration in North America and Europe will intensify competition, while faster growth in organic canned foods will support portfolio premiumization across the global market.

Research Methodology

Primary Research

IMARC Group's primary research methodology involves in-depth interviews with senior industry executives, procurement managers, distribution channel partners, and retail category buyers across key geographic markets. A minimum of 150 validated primary interviews inform the base market size estimates for the Global Canned Food Market report.

Secondary Research

Secondary sources include government agricultural and trade databases (USDA, FAO, EU Eurostat), industry associations (Can Manufacturers Institute, World Packaging Organisation), leading trade publications (Food Business News, Prepared Foods, The Grocer), corporate annual reports, SEC filings, and proprietary IMARC Group databases covering 5,000+ food and beverage companies globally.

Forecasting Models

Market sizing employs both bottom-up (segment aggregation from product type, distribution channel, and regional estimates) and top-down (macroeconomic indicator alignment with food expenditure data) methodologies. Forecasts are validated through triangulation with historical CAGR trends, expert consensus, and leading economic indicators including GDP growth, urbanization rates, and retail sales indices. Forecasting model accuracy is validated against prior-period actuals at each annual update cycle.

Canned Food Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Canned Meat and Seafood, Canned Fruit and Vegetables, Canned Ready Meals, Others |

| Types Covered | Organic, Conventional |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, E-commerce, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Nestlé S.A., Conagra Brands, Inc., Hormel Foods Corporation, The Campbell’s Company, Bolton Group S.r.l., Thai Union Group PCL, NewPrinces S.p.A., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, canned food market forecast, and dynamics of the market from 2020-2034.

- The canned food market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the canned food industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Canned Food Market Report

The global canned food market size was valued at USD 103.91 Billion in 2025 and is projected to reach USD 129.00 Billion by 2034, growing at a CAGR of 2.11%.

North America holds the largest share at 35.7% in 2025, supported by high per-capita canned food consumption, mature retail infrastructure, and emergency preparedness culture.

Key drivers include rising urbanization, busy consumer lifestyles, expanding e-commerce grocery channels, organic product premiumization, and persistent emergency preparedness stocking behavior post-COVID-19.

Canned Meat and Seafood leads with a 38.6% share in 2025, followed by Canned Fruit and Vegetables at 29.4% and Canned Ready Meals at 21.3%.

Canned Ready Meals and the Organic type segment are growing fastest, at approximately 3.12% and 4.85% CAGR respectively through 2034, outpacing the overall market rate of 2.11%.

Major players include Nestlé S.A., Conagra Brands, Inc., Hormel Foods Corporation, The Campbell’s Company, Bolton Group S.r.l., Thai Union Group PCL, and NewPrinces S.p.A.

The global canned food market is projected to exhibit a CAGR of 2.11% during the forecast period from 2026 to 2034, reaching USD 129.00 Billion by 2034.

E-commerce grocery channels accounted for approximately 12% of U.S. grocery sales in 2024. Canned food benefits from favorable shipping economics and no refrigeration requirements, supporting strong online channel growth.

Organic canned food holds 17.5% market share in 2025 and is growing at ~4.85% CAGR. Premium pricing and expanding EU and USDA organic certification infrastructure are key growth enablers.

Principal challenges include health perception issues around sodium and BPA content, intense competition from frozen food alternatives, and raw material cost volatility affecting tinplate and aluminum pricing.

Asia Pacific holds 23.5% of global canned food revenue in 2025 and is the fastest-growing region, driven by China's e-commerce grocery expansion, India's urbanizing middle class, and rising modern retail penetration.

IMARC uses combined bottom-up and top-down methodologies, validated through primary interviews with 150+ industry executives and triangulated against macroeconomic indicators including GDP growth, retail sales data, and urbanization rates.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)