Car Subscription Market Size, Share, Trends and Forecast by Service Providers, Vehicle Type, Subscription Period, End Use, and Region, 2026-2034

Car Subscription Market Size, Share, Trends & Forecast (2026-2034)

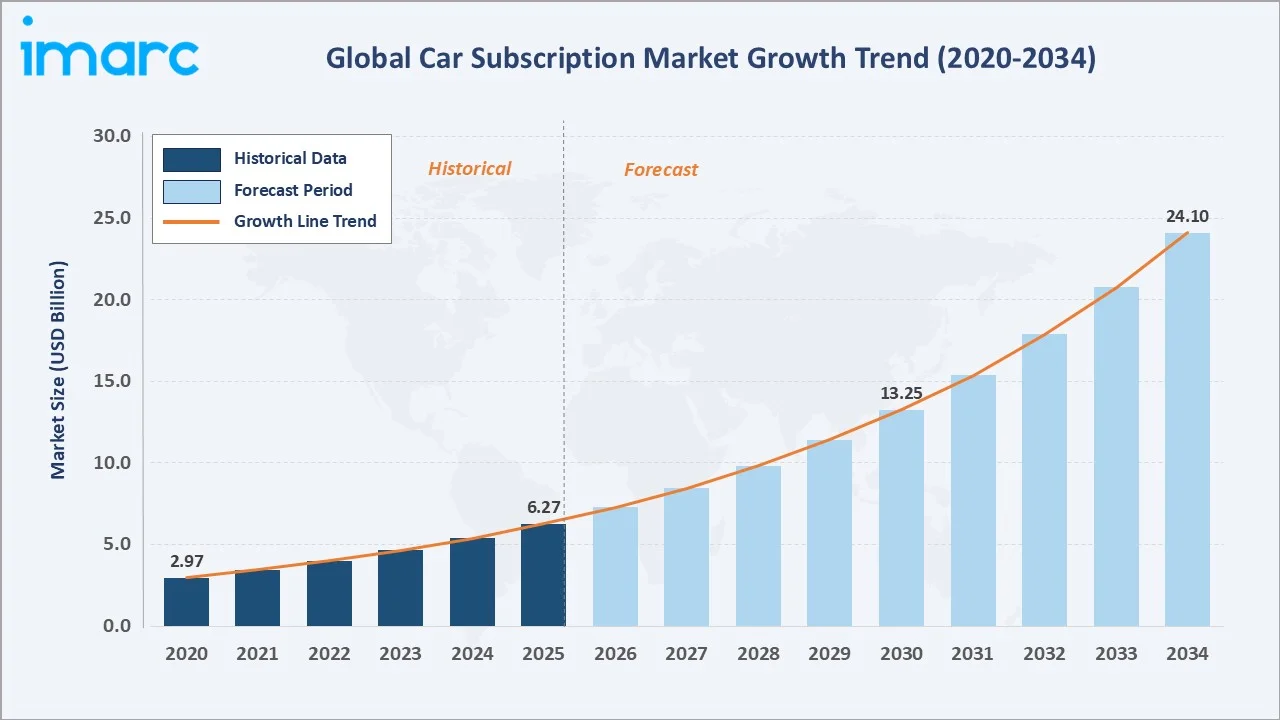

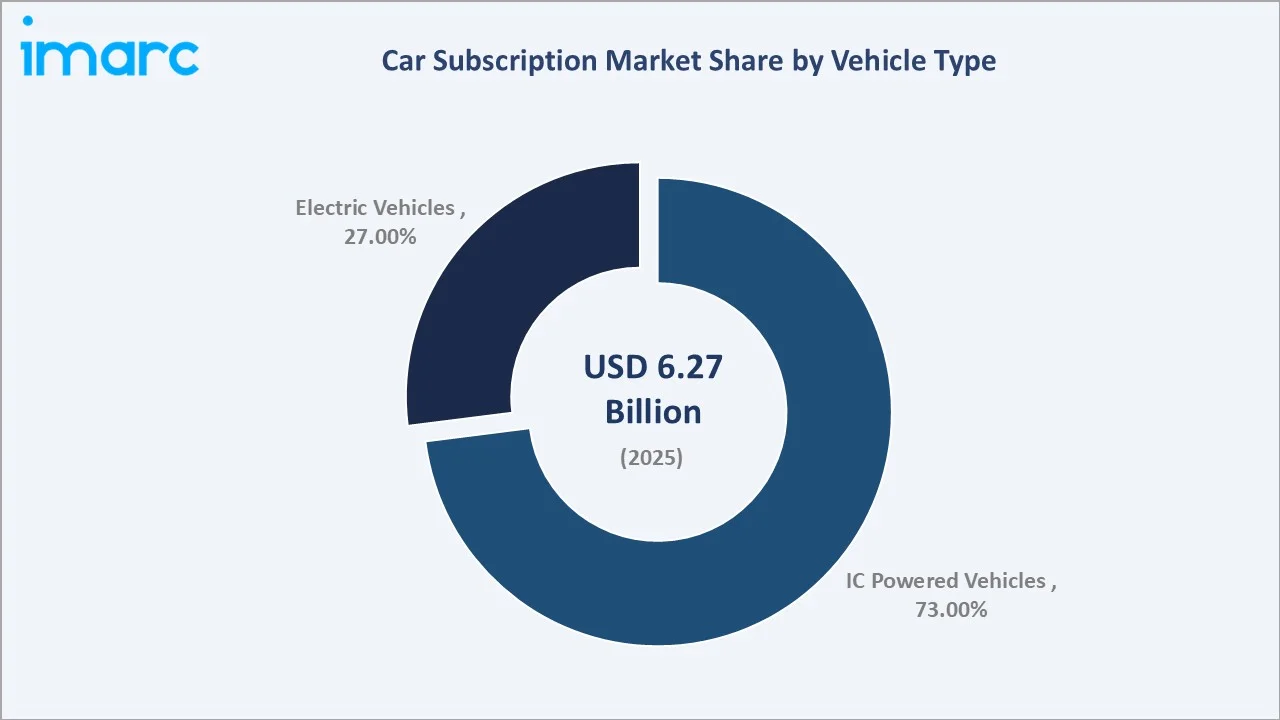

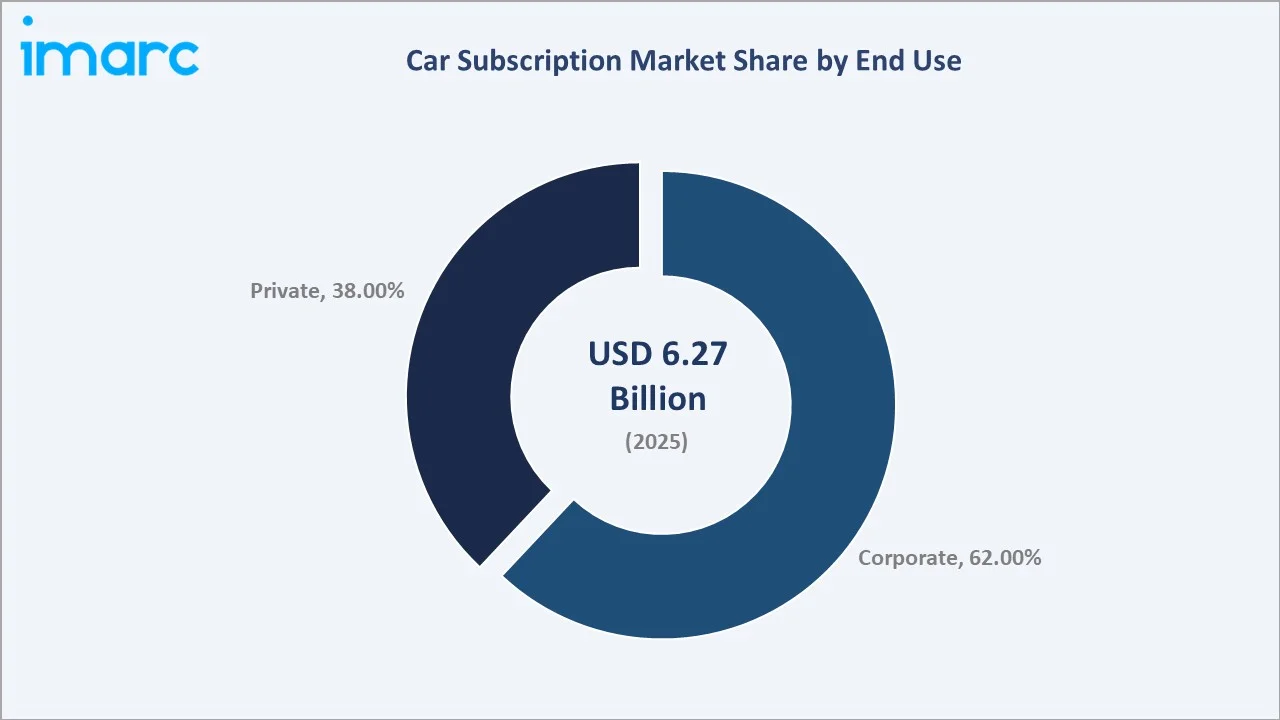

The global car subscription market reached USD 6.27 Billion in 2025 and is projected to reach USD 24.10 Billion by 2034, growing at a CAGR of 16.14% during 2026-2034. Rising consumer preference for flexible, all-inclusive mobility solutions, rapid urbanization, and the accelerating transition toward electric vehicles are key growth drivers.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 6.27 Billion |

|

Forecast Market Size (2034) |

USD 24.10 Billion |

|

CAGR (2026-2034) |

16.14% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Europe (41.9% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific |

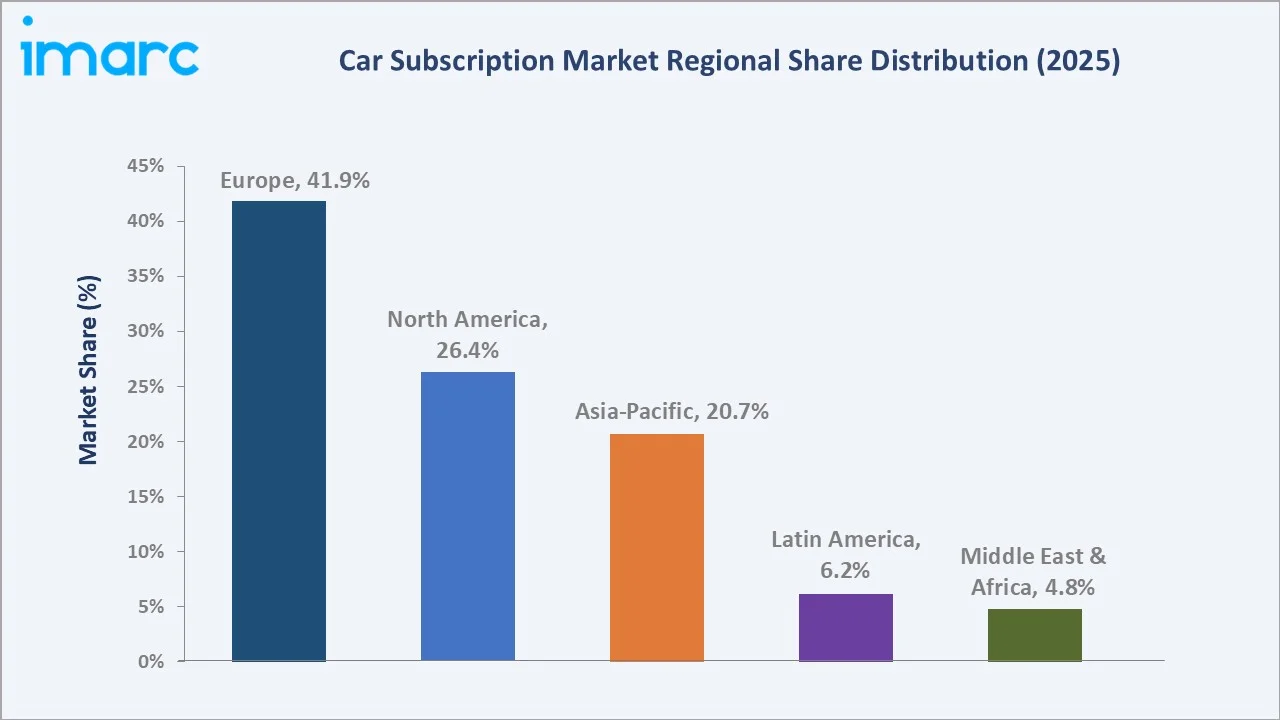

Europe dominates, holding a 41.9% market share in 2025, while the corporate end-use segment leads with 62.0%. IC powered vehicles remain the dominant vehicle type with a 73.0% share. The car subscription model offers consumers unmatched flexibility, bundling insurance, maintenance, and roadside assistance into a single monthly fee, making it a preferred alternative to traditional vehicle ownership and long-term leasing across both individual and enterprise segments.

To get more information on this market, Request Sample

With applications spanning corporate fleet management, individual urban mobility, and short-term travel needs, the market is expected to continue expanding, supported by innovations in digital onboarding platforms, EV fleet integration, and AI-driven subscription personalization across geographies with high urbanization and rising vehicle costs.

Executive Summary

The global car subscription market is on a sustained growth path, underpinned by shifting consumer attitudes toward vehicle access over ownership, accelerating fleet electrification, and the rapid maturation of digital subscription platforms. The market reached USD 6.27 Billion in 2025 and is forecast to surpass USD 24.10 Billion by 2034. This trajectory reflects a robust CAGR of 16.14% over the forecast period.

Europe leads globally with a 41.9% revenue share in 2025, driven by stringent emissions regulations, high urbanization, and a mature ecosystem of OEM-backed and independent subscription providers. Asia-Pacific, at 20.7%, represents the fastest-growing opportunity, with China, Japan, and India investing heavily in mobility-as-a-service infrastructure and digital automotive platforms.

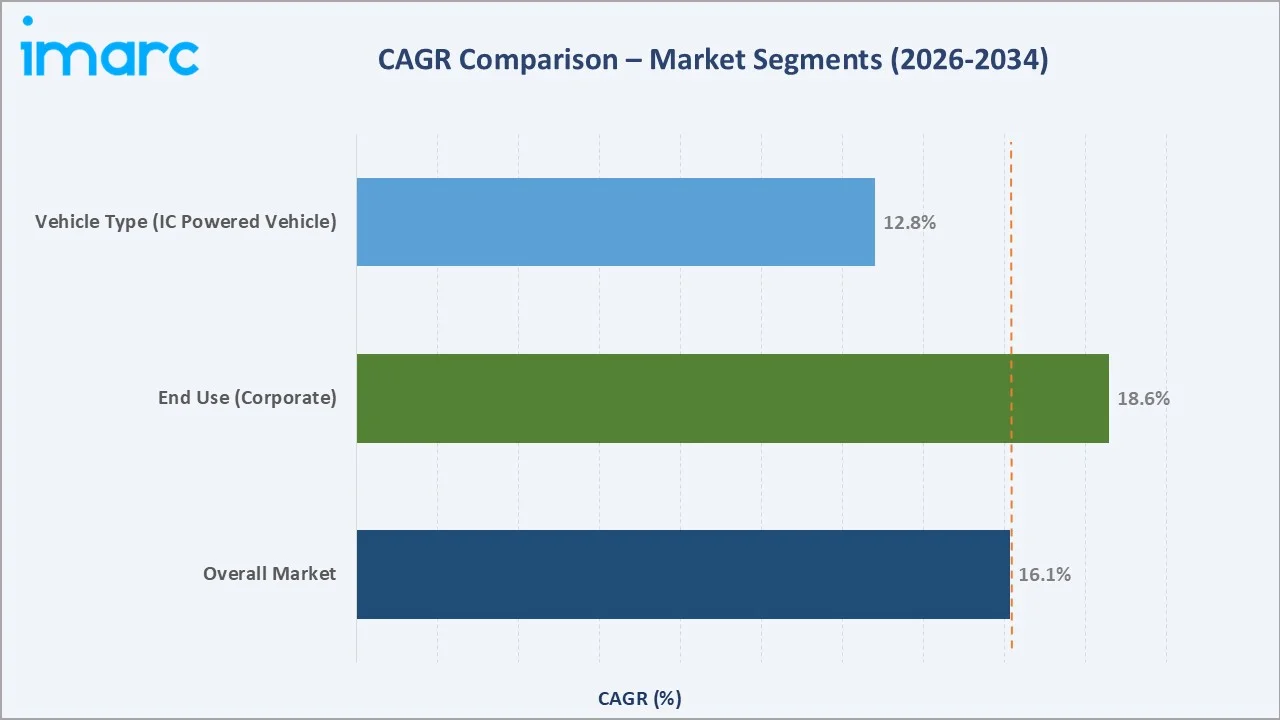

IC powered vehicles dominate vehicle type with a 73.0% share, though EV subscriptions are growing at over twice the overall market rate. Corporate end-use commands the largest segment at 62.0%, reflecting enterprise demand for flexible fleet solutions that enable ESG compliance without long-term asset commitments. Key players continue to invest in fleet electrification, AI-driven logistics, and geographic expansion to capture growing demand across emerging markets.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Vehicle Type) |

IC Powered Vehicle – 73.0% share (2025) |

|

Largest Segment (End Use) |

Corporate – 62.0% share (2025) |

|

Leading Region |

Europe – 41.9% revenue share (2025) |

|

Fastest Growing Region |

Asia-Pacific (urbanization + digital mobility adoption) |

|

Top Companies |

The Hertz Corporation., Lyft, Inc., Cox Automotive., Carly Car Subscription Pty Ltd, Wagonex Limited, OpenRoad Group, and Zoomcar India Private Limited. |

|

Market Opportunity |

EV subscription segment growing at ~37.65% CAGR through 2034 |

Key Analytical Observations Supporting The Above Data:

- IC Powered Vehicles account for 73.0% of the car subscription market in 2025, preferred for their lower subscription pricing, widespread availability, and established refueling infrastructure, particularly in markets where EV charging networks remain underdeveloped.

- The corporate end-use segment leads with 62.0% share (2025), fueled by enterprise demand for flexible fleet access, ESG-driven fleet electrification strategies, and the need to keep vehicle assets off corporate balance sheets amid elevated interest rates.

- Europe holds 41.9% of the global market in 2025, led by Germany, the UK, France, and the Netherlands, all of which have regulatory mandates promoting low-emission vehicle transitions and strong OEM-backed subscription ecosystems.

- Asia-Pacific is emerging as the fastest-growing region, driven by urbanization, rising middle-class incomes, and platform-driven mobility adoption in China, Japan, India, and South Korea.

- EV subscriptions are gaining regulatory momentum globally, with corporate fleets in Europe increasingly adopting six-month EV trials to satisfy 2025 interim sustainability targets without long-term depreciation risk exposure.

Global Car Subscription Market Overview

Car subscription is a flexible mobility model in which consumers and enterprises pay a recurring monthly fee to access vehicles without the financial and administrative burdens of ownership. Originally a niche offering by premium automakers in select Western European markets, subscription services have expanded rapidly into a global industry spanning OEM captive programs, independent multi-brand platforms, and tech-enabled startups.

The market ecosystem encompasses vehicle manufacturers, fleet management operators, insurance underwriters, telematics providers, digital platform developers, and end-user segments ranging from urban individuals to multinational corporate fleets.

Macroeconomic factors, including rising vehicle prices, elevated interest rates, and growing awareness of the total cost of vehicle ownership, are primary growth catalysts. Car subscriptions deliver financial predictability through fixed monthly fees that bundle insurance, maintenance, and roadside assistance, while simultaneously providing the flexibility to switch vehicles based on evolving personal or business mobility needs.

Market Dynamics

To evaluate market opportunities, Request Sample

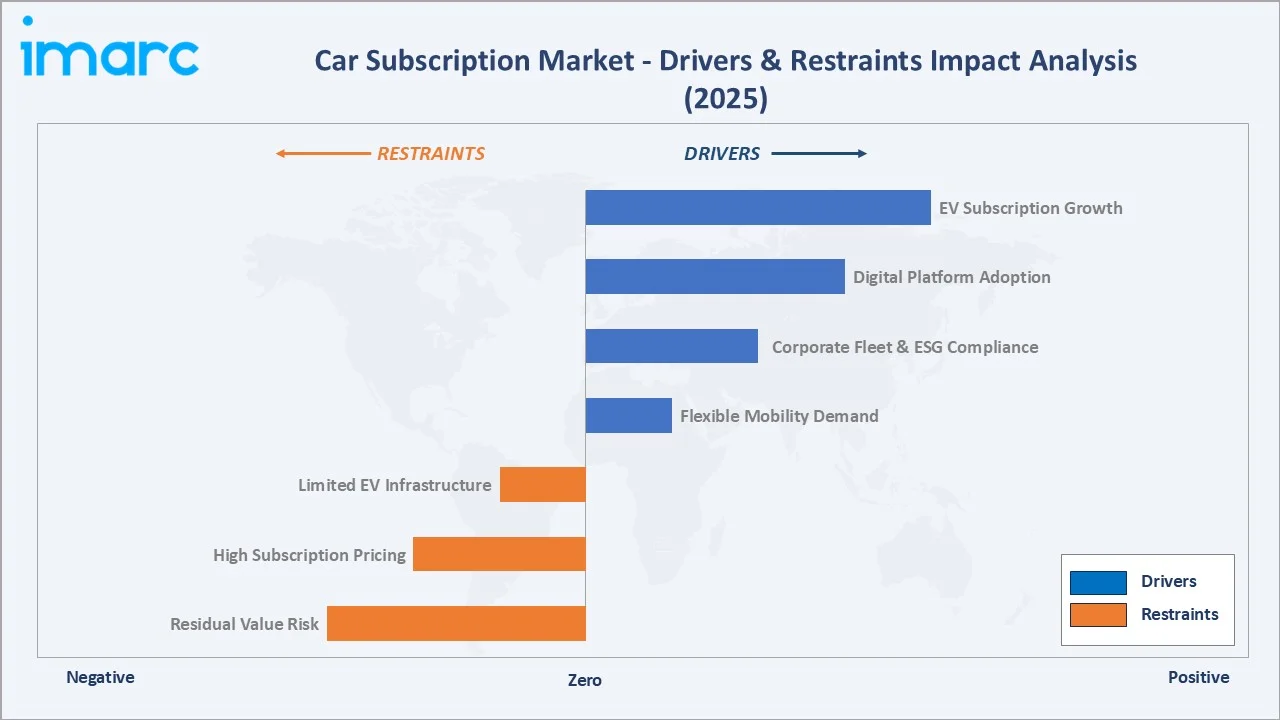

Market Drivers

- Rising Demand for Flexible Mobility Solutions: A recent survey by Cox Automotive found that approximately 35% of customers globally identify flexible commitment as their top priority when selecting a vehicle access model, driving rapid adoption plans that allow monthly vehicle changes without penalties or long-term financial commitments.

- Accelerating EV Adoption via Subscription Models: EV subscriptions are growing at a CAGR of approximately 37.65%, significantly outpacing the overall market, as consumers use subscriptions to trial electric vehicles without long-term ownership depreciation risks and technology obsolescence concerns.

- Corporate Fleet Optimization and ESG Compliance: Businesses are increasingly leveraging subscriptions to manage fleet costs dynamically, meet interim sustainability targets, and keep vehicle assets off balance sheets.

- Digital Platform Proliferation: AI-driven logistics, app-based onboarding, and telematics integration have reduced subscriber acquisition costs and improved operational efficiency, enabling providers to scale rapidly while delivering superior customer experiences across urban markets.

These drivers reinforce a self-sustaining growth cycle – regulatory mandates drive institutional EV adoption, which accelerates fleet electrification at scale, reducing per-subscription costs and expanding accessibility to private consumers across emerging markets.

Market Restraints

- Residual Value Risk and Fleet Management Complexity: Currently, many electric vehicles (EVs) depreciate by 50–65% within five years, with some models experiencing even greater losses, creating significant financial exposure for subscription providers who absorb depreciation risk on behalf of subscribers, compressing provider margins.

- High Subscription Pricing vs. Traditional Alternatives: Monthly subscription fees, which bundle insurance and maintenance, often exceed the cost of conventional leasing for consumers who do not value the bundled services or flexibility premium, limiting mass-market penetration in cost-sensitive demographics.

- Limited EV Charging Infrastructure in Emerging Markets: The appeal of EV subscriptions is constrained in regions with underdeveloped charging networks, including parts of Latin America, Southeast Asia, and Africa, restricting the addressable market for electrified subscription offerings.

Market Opportunities

- Corporate Sustainability Mandates Driving Fleet Electrification: The enforcement of CSRD requirements in Europe from 2025 mandates that large corporations report Scope 1 emissions in detail, directly incentivizing enterprise fleet transitions to EV subscriptions as the most operationally flexible compliance pathway.

- Emerging Market Expansion: Latin America and Southeast Asia collectively represent a multi-billion-dollar incremental opportunity by 2034, driven by urbanization, rising incomes, and platform adoption among young, mobility-conscious populations seeking alternatives to traditional ownership.

- Multi-Modal Mobility-as-a-Service Integration: The convergence of car subscriptions with ride-sharing, public transit, and parking solutions into unified MaaS platforms represents a nascent but rapidly growing segment expected to fundamentally reshape urban mobility ecosystems through 2034.

Market Challenges

- Fleet Procurement and Inventory Management: Maintaining diverse, current-model vehicle fleets while managing residual values, maintenance schedules, and geographic deployment logistics represents a complex operational challenge that increases capital requirements and operational risk for subscription providers.

- Regulatory Fragmentation Across Geographies: Diverging consumer protection regulations, insurance requirements, and tax treatment of subscription fees across the EU, U.S., and Asia-Pacific create compliance complexity and cost burdens for providers operating in multiple markets simultaneously.

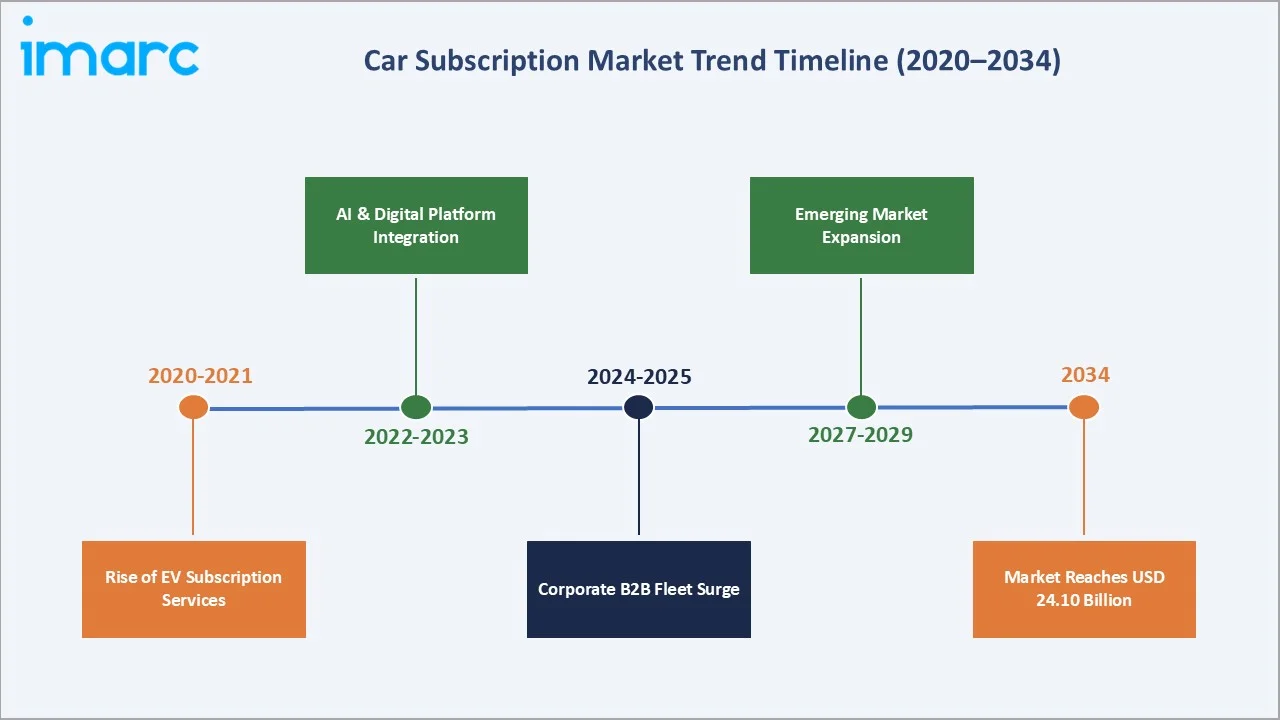

Emerging Market Trends

1. Rise of Electric Vehicle Subscription Services

EV-specific subscription plans allow users to experience electric driving without battery depreciation concerns, charging anxiety, or long-term technology lock-in. In December 2024, Toyota launched Alphard and Vellfire PHEV models through its KINTO subscription service in Japan, enabling corporate clients to claim subscription fees as tax-deductible business expenses.

2. AI and Digital Platform Integration

Leading providers are leveraging no-code AI automation to manage end-to-end logistics for hundreds of vehicle deliveries daily, significantly reducing per-delivery operating costs. Mobile-first platforms with instant approval processes have compressed onboarding times from days to under 24 hours in leading markets, dramatically improving conversion rates and subscriber satisfaction scores across urban demographics.

3. Corporate B2B Subscription Surge

Corporations are using six-month subscription contracts to trial EV fleets, satisfy ESG reporting requirements, and maintain financial flexibility amid economic uncertainty. In 2025, Europe saw the sale of 2,585,187 battery electric vehicles, marking a significant 29.7% increase from the 1,992,803 units sold in 2024. The introduction of Total Cost of Usership metrics, replacing traditional Total Cost of Ownership frameworks, is further cementing subscription models as the preferred enterprise fleet strategy.

4. Expansion into Emerging Markets

Astara launched its Move subscription service in Chile in April 2025, its first Latin American market, offering a fully digital platform with customizable terms. Simultaneous entry by regional providers in Indonesia, India, and Brazil reflects growing operator confidence in these markets’ long-term demand fundamentals, supported by expanding 4G/5G connectivity and a young, mobile-oriented consumer base.

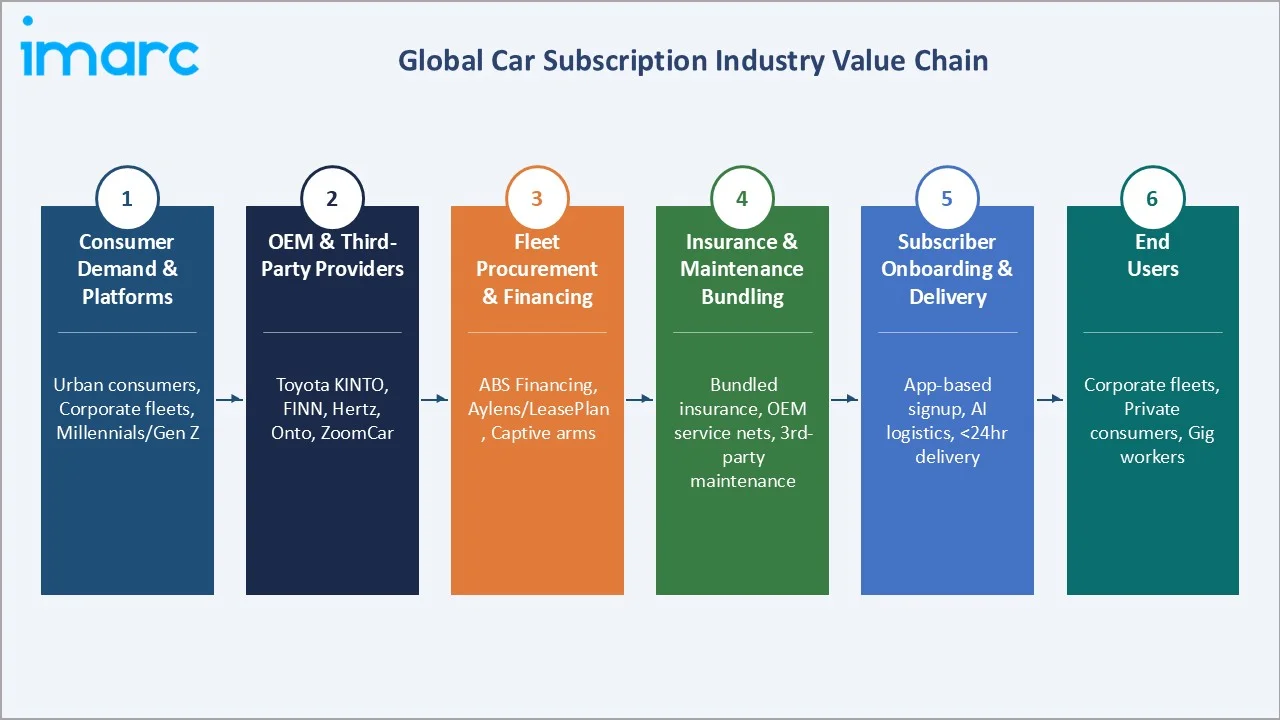

Industry Value Chain Analysis

The car subscription value chain spans vehicle manufacturing through end-user mobility delivery, with each stage populated by specialized operators whose performance directly influences subscriber experience, operational efficiency, and financial sustainability.

|

Stage |

Key Players / Examples |

|

Vehicle Manufacturing |

OEMs: Toyota (KINTO), Stellantis (Finn partnership), Hyundai, Volvo, BMW |

|

Fleet Procurement & Financing |

Captive finance arms, ABS financing (FINN EUR 1B, 2025), leasing companies (Ayvens) |

|

Subscription Platform Technology |

Digital onboarding platforms, AI-driven pricing engines, and telematics providers (OCTO Telematics) |

|

Insurance & Maintenance Bundling |

Bundled insurance underwriters, OEM-backed service networks, third-party maintenance providers |

|

Fleet Logistics & Delivery |

Last-mile vehicle delivery specialists, dealership-based local distribution, direct-to-subscriber networks |

|

End Users |

Corporate fleets, private urban consumers, short-term travelers, tech-forward millennials, and Gen Z |

Technology Landscape in the Car Subscription Industry

AI-Driven Subscription Management Platforms

Advanced ML algorithms enable dynamic pricing models that adjust subscription rates based on real-time demand signals, vehicle availability, and competitive positioning. Each year, around 4 million commercial motor vehicle inspections are carried out by the Commercial Vehicle Safety Alliance (CVSA) to promote road safety. Predictive maintenance plays a crucial role in preventing common CVSA inspection violations, including brake system failures, tire wear, and engine malfunctions.

Telematics and Connected Vehicle Integration

For EV subscriptions, battery state-of-health monitoring allows providers to enforce contractual minimum range guarantees and proactively swap vehicles before battery degradation impacts subscriber experience. In October 2023, Flexcar announced a collaboration with OCTO Telematics to optimize its subscription experience using real-time vehicle diagnostics, illustrating the strategic importance of connected vehicle technology in the competitive landscape.

Blockchain and Smart Contracts for Subscription Management

Smart contract technology enables automatic subscription renewals, real-time revenue sharing between OEM and platform partners, and instant ownership transfer during vehicle swaps, reducing administrative overhead and improving contract enforcement accuracy across multi-stakeholder subscription ecosystems.

Second-Life Asset Optimization

Second-life asset strategies, in which subscription vehicles are re-subscribed across multiple lifecycle phases rather than sold immediately at vehicle end-of-first-life, are generating significant margin improvements for leading operators, with profit margins on older re-subscribed assets increasing by approximately 15% compared to single-cycle fleet models.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Service Providers | Independent/Third Party Service Provider | 37.8% | 2025 |

| Vehicle Type | IC Powered Vehicle | 73.0% | 2025 |

| Subscription Period | 6 to 12 Months | 45.3% | 2025 |

| End Use | Corporate | 62.0% | 2025 |

| Region | Europe | 41.9% | 2025 |

By Vehicle Type

IC powered vehicles dominate the vehicle type segment with a 73.0% share in 2025 (equivalent to approximately USD 4.58 Billion). Their dominance reflects lower subscription pricing compared to electric alternatives, an extensive refueling infrastructure network, and broad vehicle availability across economy, executive, and luxury categories that ensure demand can be matched efficiently across diverse subscriber profiles and geographies.

To access detailed market analysis, Request Sample

Electric vehicles account for 27.0% of the market (approximately USD 1.69 Billion in 2025), growing at a CAGR substantially above the overall market average, driven by corporate ESG mandates, government EV incentives, and subscribers' desire to experience electric driving without ownership risk. The EV subscription segment is particularly prominent in Norway, the Netherlands, Germany, and California, where regulatory incentives and charging infrastructure maturity align to create favorable adoption conditions.

By End Use

The corporate end-use segment leads the market with a 62.0% share in 2025 (approximately USD 3.89 Billion), reflecting enterprises’ structural need for flexible vehicle fleet solutions that support dynamic workforce requirements without the capital expenditure and administrative complexity of fleet ownership or long-term leasing.

Private end-use represents 38.0% of the market (approximately USD 2.38 Billion in 2025), and is expected to grow at the fastest CAGR within the segment as subscription pricing becomes more competitive and consumer awareness increases. Urban professionals, particularly millennials and Gen Z consumers who prioritize experiences over asset ownership, represent the most receptive private subscriber demographic.

Regional Market Insights

Europe’s market leadership (41.9%, 2025) reflects decades of progressive automotive regulatory frameworks and strong OEM engagement with subscription models. FINN, headquartered in Munich, secured EUR 1 billion in ABS financing in 2025 to expand its pan-European fleet, while Spotawheel raised EUR 300 million to target used-car subscription markets in Poland, Romania, and Greece, reflecting sustained investor confidence in the region’s growth trajectory.

|

Region |

Share (2025) |

Key Growth Drivers |

Regulatory Impact |

|

Europe |

41.9% |

OEM programs, ESG mandates, EV fleet trials, and urban mobility demand |

Euro 7 standards; CSRD sustainability reporting; EV tax incentives |

|

North America |

26.4% |

Rising vehicle costs, corporate fleet demand, and urban driver preference for subscriptions |

State EV mandates (California); NHTSA safety standards; federal EV credits |

|

Asia-Pacific |

20.7% |

Urbanization, rising incomes, MaaS adoption, OEM digital platforms (KINTO) |

National EV targets; import duty structures; MaaS regulatory frameworks |

|

Latin America |

6.2% |

Youth demographics, digital-first consumers, and rising urban populations |

Latin NCAP (safety ratings), PROCONVE (Brazil's vehicle emissions program); EV incentive pilots; digital platform regulations |

|

Middle East & Africa |

4.8% |

Expatriate mobility needs, premium service demand, and smart city initiatives |

GCC sustainability goals; UAE/KSA smart mobility frameworks |

Asia-Pacific is the highest-growth region, with China’s expanding EV infrastructure and government-backed mobility platform initiatives positioning it as the world’s largest incremental subscription market by 2030. Japan’s KINTO platform, South Korea’s smart city programs, and India’s rapidly expanding urban middle class are collectively creating a multi-billion-dollar subscription opportunity across the region through 2034.

Competitive Landscape

The global car subscription market exhibits a moderately fragmented competitive structure. OEM captive programs, established rental and leasing conglomerates, and agile technology-first startups co-exist, each pursuing distinct competitive strategies. OEMs leverage existing customer relationships and brand equity to offer subscription services as loyalty retention tools and recurring revenue generators.

|

Company Name |

Service Brand |

Market Position |

Core Strength |

|

The Hertz Corporation. |

Hertz My Car |

Market Leader |

Global fleet scale; hybrid EV integration; extensive airport network across 160+ countries |

|

Lyft, Inc. |

Express Drive |

Market Leader |

Technology-first platform; gig economy driver fleet; data-driven demand optimization |

|

Cox Automotive. |

Clutch Technologies |

Strong Challenger |

Dealer network integration; B2B corporate fleet specialization; Socium Ventures innovation fund |

|

Carly Car Subscription Pty Ltd

|

Carly |

Challenger |

Australian car subscription marketplace operating in Australia and New Zealand |

|

Wagonex Limited |

Wagonex |

Challenger |

UK multi-brand marketplace; white-label platform for dealer groups; consumer subscription focus |

|

OpenRoad Group. |

PORTFOLIO by OpenRoad |

Niche Player |

Dealer-backed subscription model; premium brand access |

|

Zoomcar India Private Limited. |

ZoomCar |

Niche Player |

Asia-Pacific peer-to-peer leader; India market focus; host-vehicle model expanding in SEA |

Consolidation activity is accelerating, with five major M&A transactions completed in 2025 alone as leasing conglomerates acquire successful subscription startups. Residual value management, fleet electrification strategy, and technology platform sophistication are the primary competitive differentiators in the evolving landscape.

Key Company Profiles

The Hertz Corporation.

The Hertz Corporation., headquartered in Estero, Florida, is one of the world’s largest vehicle subscription and rental operators, with an active fleet spanning 160+ countries. Hertz has strategically repositioned its global operations to integrate subscription services alongside traditional rental offerings, with a growing emphasis on EV integration across its North American and European fleet operations.

- Product Portfolio: Hertz My Car subscription service and corporate fleet management programs.

- Recent Developments: The 2025 strategy is fleet rationalization and rotation of 100,000 vehicles to improve economics.

- Strategic Focus: Fleet rationalization toward EV-centric subscriptions; airport-adjacent subscription hub expansion; corporate B2B contract growth across North America and Europe.

Lyft, Inc.

Lyft, Inc., headquartered in San Francisco, California, operates a technology-first mobility platform encompassing ride-sharing, vehicle rental, and fleet subscription services across the U.S., Canada, and Europe. Lyft’s subscription division leverages its extensive digital platform infrastructure and driver data analytics to offer competitively priced, flexible vehicle access programs targeting both gig economy workers and urban commuters.

- Product Portfolio: Express Drive vehicle subscription for gig drivers, and bundled mobility packages integrating ride-sharing credits with subscription access.

- Recent Developments: Continued expansion of the Express Drive program in metropolitan markets.

- Strategic Focus: Deepening integration between ride-sharing and subscription platforms; autonomous vehicle subscription readiness; geographic expansion into mid-tier US urban markets.

Zoomcar India Private Limited.

Zoomcar India Private Limited, headquartered in Bengaluru, India, operates Asia-Pacific’s largest peer-to-peer car sharing and subscription platform, enabling vehicle owners to monetize idle assets while providing subscribers access to a diverse fleet without centralized procurement requirements. ZoomCar’s asset-light model positions it competitively in emerging markets where capital constraints limit traditional fleet ownership models.

- Product Portfolio: Short-term and long-term car subscriptions, peer-to-peer vehicle sharing, self-drive rental packages, and corporate fleet access programs across India.

- Recent Developments: Expanded host network to approx. 40,221 registered Host vehicles across India, with strategic entry into Indonesia and Vietnam through partnerships with local automotive dealers and fleet operators.

- Strategic Focus: Host network densification in Tier 2 Indian cities; EV subscription product development aligned with India’s national EV adoption targets.

Market Concentration Analysis

The car subscription market exhibits moderate concentration at the platform and fleet management level, with the top five global operators, The Hertz Corporation., Lyft, Inc., Cox Automotive., Carly Car Subscription Pty Ltd, Wagonex Limited, collectively holding approximately 35–40% of global subscription revenue in 2025. A significant long tail of regional providers, OEM-captive programs, and dealer-backed local subscription services accounts for the balance, ensuring substantial fragmentation below the top tier, particularly in Asia-Pacific and Latin America.

Consolidation activity is accelerating, driven by the capital intensity of EV fleet procurement, residual value management complexity, and the need for sophisticated technology platforms to compete effectively. Five major M&A transactions were completed in 2025 alone as established leasing conglomerates, including Ayvens (the merged ALD/LeasePlan entity), acquired successful subscription startups to rapidly scale capabilities and geographic reach.

Investment & Growth Opportunities

Fastest Growing Segments

EV subscription services (estimated CAGR 37.65%), corporate B2B fleet programs (approximately 30.2% CAGR), and multi-modal MaaS-integrated subscriptions represent the three highest-growth investment vectors through 2034. Together, these niches address a total addressable market of approximately USD 8.5 Billion in incremental annual revenue by 2030, representing significant capital deployment opportunities for both strategic and financial investors.

Emerging Market Expansion

Latin America, Southeast Asia, and the Middle East collectively represent an incremental multi-billion-dollar subscription opportunity by 2034. Entry strategies favored by global operators include digital-first platform launches in major urban centers, strategic partnerships with local dealership groups, alignment with national EV adoption incentive programs, and OEM joint ventures that leverage existing vehicle distribution networks to rapidly build subscription fleet capacity without centralized procurement capex.

Venture and Institutional Investment Trends

- Key investment themes include AI-driven subscription pricing optimization, EV battery health monitoring platforms, and blockchain-enabled fleet provenance tracking systems that improve residual value predictability and investor confidence in fleet asset quality.

- Family offices and private equity firms are increasingly targeting vertical integration plays – consolidating vehicle procurement, fleet management, insurance bundling, and subscriber platforms into single portfolio companies that capture value across the entire subscription value chain.

Future Market Outlook (2026-2034)

The global car subscription market is positioned for sustained, broad-based growth through 2034. From a base of USD 6.27 Billion in 2025, the market is projected to reach USD 24.10 Billion by 2034, representing total incremental value creation of approximately USD 17.83 Billion over the forecast decade, reflecting a robust CAGR of 16.14%.

The regulatory environment will drive significant corporate fleet subscription acceleration through 2028. Subscription providers that establish differentiated EV fleet management capabilities, superior digital subscriber experiences, and scalable multi-market operational infrastructure by 2026 are positioned to capture a disproportionate share of the high-value corporate segment’s growing subscription budgets.

Long-term, the market’s trajectory is tied to three structural macro-themes: accelerating urbanization (creating space-constrained markets where subscription access is more practical than ownership), climate regulation, and generational ownership disintermediation. Car subscriptions sit at the intersection of all three, providing a durable structural demand foundation through the end of the forecast period and beyond.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 120 industry participants in 2024–2025, including car subscription platform operators, OEM mobility division executives, corporate fleet managers, insurance underwriters, and end-user subscribers across Europe, North America, and Asia-Pacific. Key informants provided granular insights into subscription pricing dynamics, EV fleet management practices, and corporate procurement decision frameworks.

Secondary Research

Secondary research encompassed a systematic review of company annual reports, regulatory filings, OEM mobility division disclosures, industry databases (Euromonitor, IBISWorld, S&P Global Mobility), trade publications (Fleet Management Weekly, Automotive News Europe), and publicly available financial data from subscription platform operators and their investors. Over 240 secondary sources were reviewed and triangulated to ensure data accuracy and analytical robustness.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating macroeconomic indicators, urbanization rates, EV adoption trajectories, corporate fleet procurement budgets, and historical subscription market evolution data. A base-case CAGR of 16.14% reflects consensus analyst estimates validated against reported platform revenue growth rates, investor disclosures from key subscription operators, and OEM mobility division strategic guidance.

Car Subscription Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Service Providers Covered | OEMs and Captives, Independent/Third Party Service Provider |

| Vehicle Types Covered | IC Powered Vehicle, Electric Vehicle |

| Subscription Periods Covered | 1 to 6 Months, 6 to 12 Months, More Than 12 Months |

| End Uses Covered | Private, Corporate |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | The Hertz Corporation., Lyft, Inc., Cox Automotive., Carly Car Subscription Pty Ltd, Wagonex Limited, OpenRoad Group., Zoomcar India Private Limited., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the car subscription market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global car subscription market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the car subscription industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Car Subscription Market Report

The global car subscription market reached USD 6.27 Billion in 2025. It is projected to reach USD 24.10 Billion by 2034, representing a CAGR of 16.14% over the forecast period 2026-2034.

The car subscription market is expected to grow at a CAGR of 16.14% during the forecast period from 2026-2034, supported by consistent demand from corporate fleet operators, rising consumer preference for flexible mobility, and accelerating EV subscription adoption across major global markets.

Europe leads the market with a 41.9% revenue share in 2025, driven by stringent environmental regulations including Euro 7 standards, strong OEM-backed subscription ecosystems in Germany, the UK, and France, and high consumer and enterprise receptiveness to Vehicle-as-a-Service mobility models.

IC Powered Vehicles dominate the vehicle type segment with a 73.0% share in 2025, valued at approximately USD 4.58 Billion. Their dominance is driven by lower subscription pricing, widespread vehicle availability, and established refueling infrastructure across all major markets.

The corporate end-use segment holds the largest share at 62.0% in 2025 (approximately USD 3.89 Billion), driven by enterprise demand for flexible fleet access, ESG-driven fleet electrification strategies, and the need to manage vehicle assets off corporate balance sheets amid elevated interest rates and sustainability reporting requirements.

Key players include The Hertz Corporation., Lyft, Inc., Cox Automotive., Carly Car Subscription Pty Ltd, Wagonex Limited, OpenRoad Group., and Zoomcar India Private Limited.

EV subscriptions are the fastest-growing segment within the car subscription market, expanding at approximately 37.65% CAGR. Corporate fleets are transitioning to EV subscriptions to satisfy ESG mandates, while private consumers use subscriptions to trial electric vehicles without long-term ownership risks, battery obsolescence concerns, or residual value uncertainty.

Key challenges include residual value risk from EV depreciation, high subscription pricing relative to traditional leasing for non-EV vehicles, limited EV charging infrastructure in emerging markets, regulatory fragmentation across geographies, and the capital intensity required to maintain diverse, current-model subscription fleets at scale.

Significant investment opportunities exist in EV fleet subscription platforms, AI-driven subscription management technology, emerging market expansion in Latin America and Southeast Asia, multi-modal MaaS integration, and corporate B2B fleet electrification programs, with the market projected to reach USD 24.10 Billion by 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)