Caustic Soda Market Size, Share, Trends and Forecast by Product Type, Manufacturing Process, Grade, Application, and Region, 2026-2034

Global Caustic Soda Market Size, Share, Trends & Forecast (2026-2034)

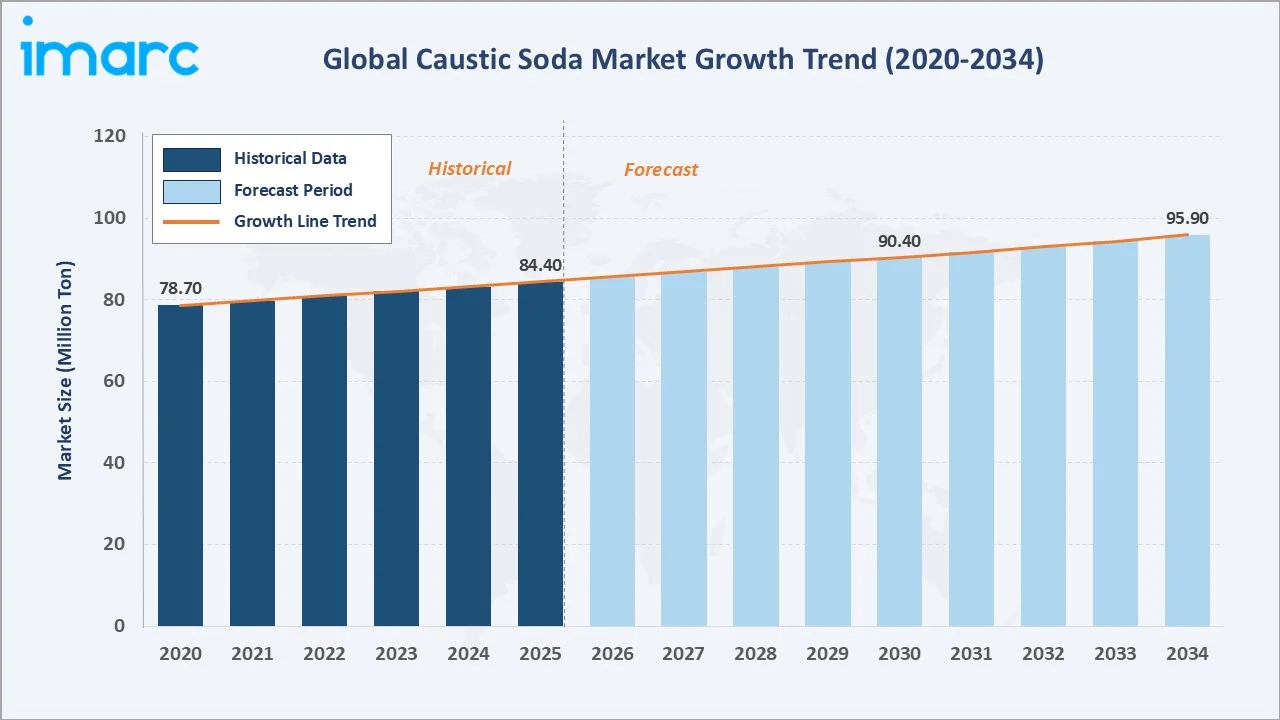

The global caustic soda market size reached 84.4 Million Tons in 2025 and is projected to reach 95.9 Million Tons by 2034, exhibiting a CAGR of 1.39% during the forecast period 2026-2034. Robust demand from alumina refining, rapid expansion in the pulp and paper industry, and rising investments in municipal water treatment infrastructure are the primary growth engines.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

84.4 Million Tons |

|

Forecast Market Size (2034) |

95.9 Million Tons |

|

CAGR (2026-2034) |

1.39% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

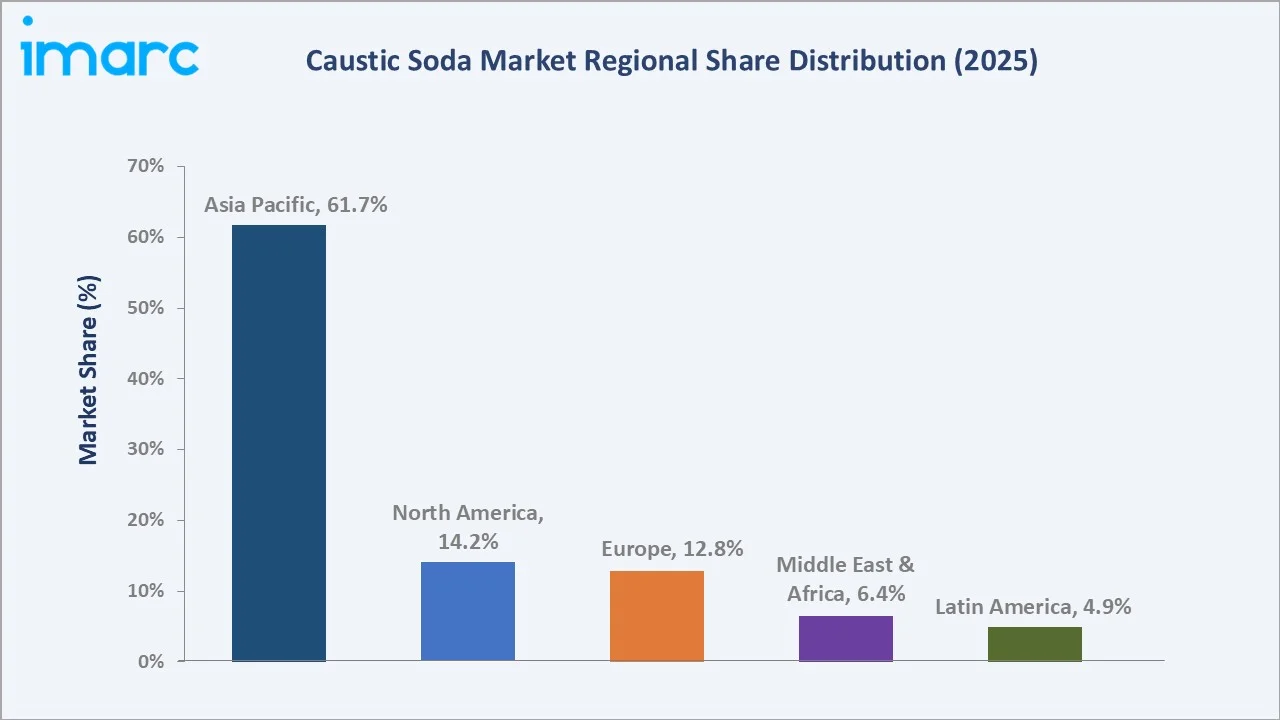

Asia Pacific (61.7% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (~1.7% CAGR) |

|

Largest Product Type |

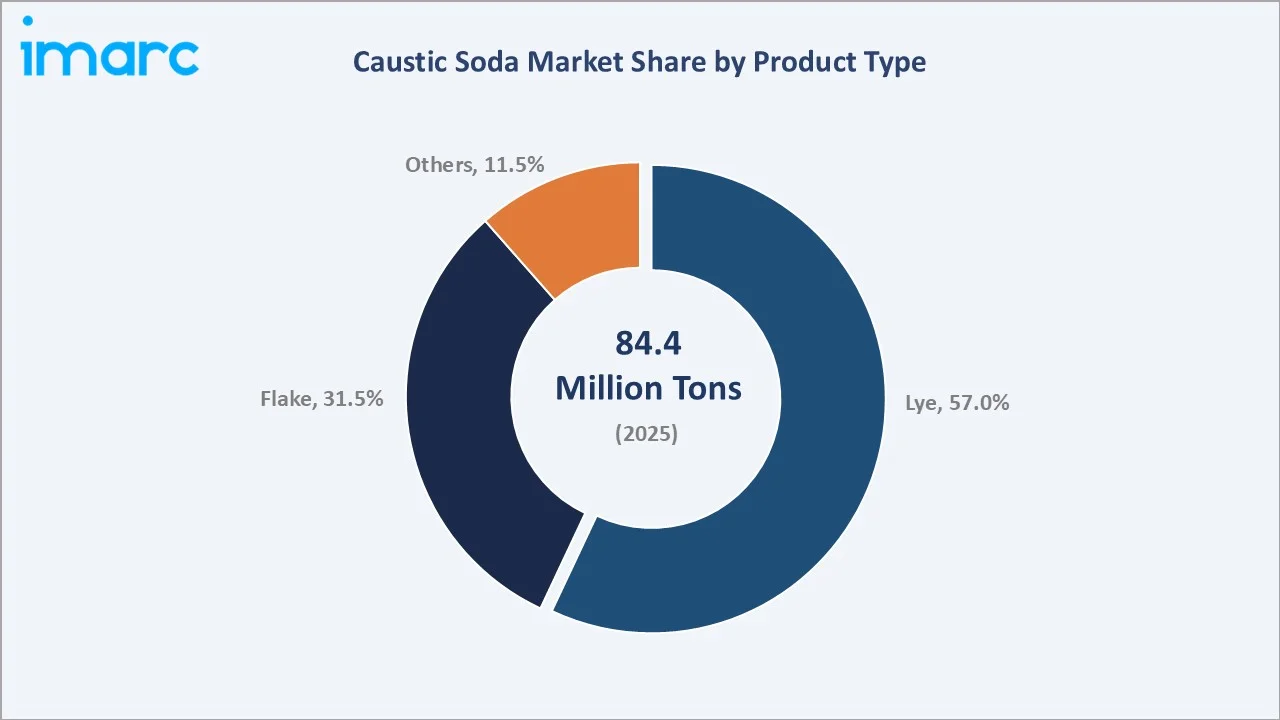

Lye (57.0%, 2025) |

|

Leading Process |

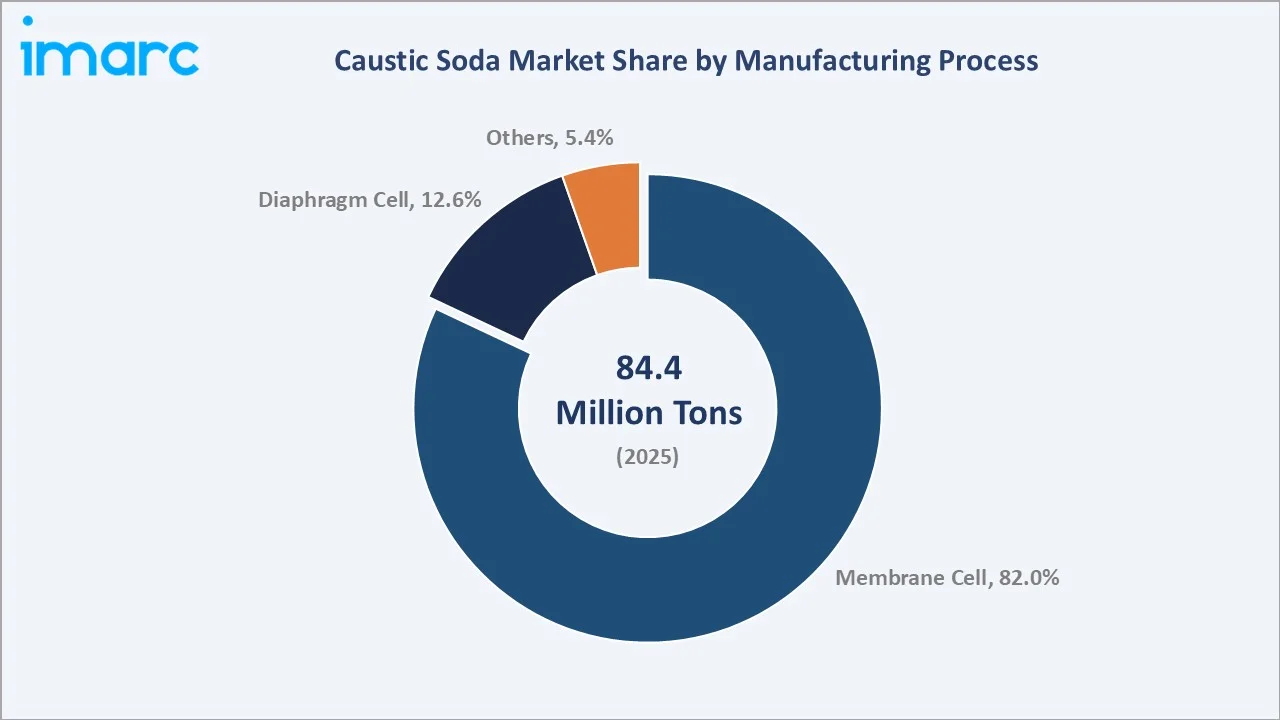

Membrane Cell (82.0%, 2025) |

The global caustic soda market growth trajectory from 2020 through 2034 reflects steady industrial demand - rising from 78.7 Million Tons in 2020 to 84.4 Million Tons in 2025, and reaching 90.4 Million Tons in 2030 before achieving 95.9 Million Tons by 2034. The chart below contrasts historical expansion against the sustained forecast curve.

To get more information on this market, Request Sample

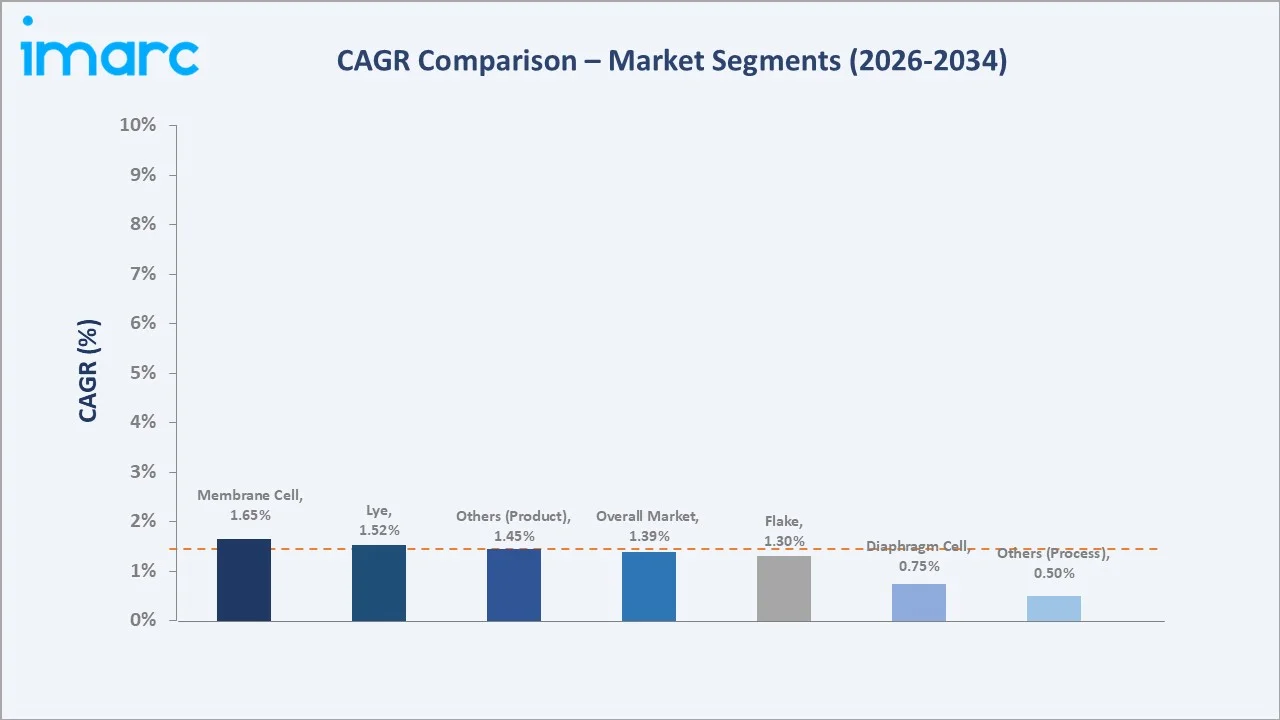

Segment-level CAGR comparisons highlight the membrane cell process and lye product type as the highest-growth sub-categories within the global caustic soda market forecast through 2034. The orange dashed line marks the overall market CAGR of 1.39%.

Executive Summary

The global caustic soda market is experiencing steady, demand-led expansion. It is underpinned by structural growth in alumina production, the paper and pulp sector, and water treatment infrastructure. Volumed at 84.4 Million Tons in 2025, the market is forecast to reach 95.9 Million Tons by 2034 at a CAGR of 1.39%. The market's measured growth reflects the commodity nature of caustic soda - a co-product of chlorine in the chlor-alkali process - where capacity additions are disciplined and tied closely to downstream demand.

Lye dominates the product-type mix with 57.0% revenue share in 2025, reflecting its wide utility in liquid-process industries. Among manufacturing processes, the membrane cell process accounts for 82.0% of global output, driven by its superior energy efficiency and compliance with evolving environmental norms. Diaphragm cell represents a declining 12.6% share, constrained by mercury-free transition mandates.

Asia Pacific leads with a 61.7% global share in 2025, anchored by China's dominant chlor-alkali capacity. North America holds 14.2% while Europe contributes 12.8%. The caustic soda market outlook remains stable through 2034, supported by alumina demand from electric vehicle lightweighting trends.

Key Market Insights

| Insight | Data |

|

Largest Product Type |

Lye – 57.0% share (2025) |

|

Second Product Type |

Flake – 31.5% share (2025) |

|

Dominant Manufacturing Process |

Membrane Cell – 82.0% (2025) |

|

Second Manufacturing Process |

Diaphragm Cell – 12.6% (2025) |

|

Leading Region |

Asia Pacific – 61.7% share (2025) |

|

Top Companies |

Olin Corporation, Westlake Corporation, Formosa Plastics Corporation, Shin-Etsu Chemical Co., Ltd., Tosoh Corporation, Nouryon, INEOS, Tata Chemicals Ltd. |

|

Market Opportunity |

Alumina refining & EV aluminum lightweighting |

Key Analytical Observations Supporting The Above Data:

- Lye's 57.0% dominance in 2025 reflects its critical role in alumina refining through the Bayer process, where caustic soda is extensively consumed for efficient extraction of alumina from bauxite ore. According to the International Aluminium Insititute, the world’s alumina production totalled 147.047 million tonnes in 2024.

- Flake's 31.5% share is anchored by solid-dosing applications in soap manufacture, chemical synthesis, and water treatment facilities in the Middle East and Latin America.

- Membrane cell technology's 82.0% process dominance reflects EU Regulation EC 1102/2008 mandating the phase-out of mercury-based processes. Membrane cells produce higher-purity NaOH while consuming significantly less electricity per ton.

- Asia Pacific's 61.7% regional dominance is driven by China's position as the world's largest installed chlor-alkali capacity base.

- Water treatment demand is a fast-growing niche, with global populations still lacking access to safely managed drinking water driving increased adoption.

Global Caustic Soda Market Overview

Caustic soda (sodium hydroxide, NaOH) is a strong inorganic alkali produced through the electrolysis of brine via the chlor-alkali process, with chlorine as the co-product. It is available in liquid form (lye, typically 50% solution), solid flakes, and granules. Key applications span alumina refining, pulp and paper, chemical manufacturing, textile processing, soap and detergent formulation, water treatment, and food processing. The industry operates within a tightly coupled chlor-alkali ecosystem where caustic soda volumes are structurally linked to chlorine demand.

Macroeconomic growth in emerging markets, rising aluminum consumption from EVs and aerospace, tightening water quality regulations, and industrial expansion across textiles and petrochemicals support sustained demand.

Market Dynamics

To evaluate market opportunities, Request Sample

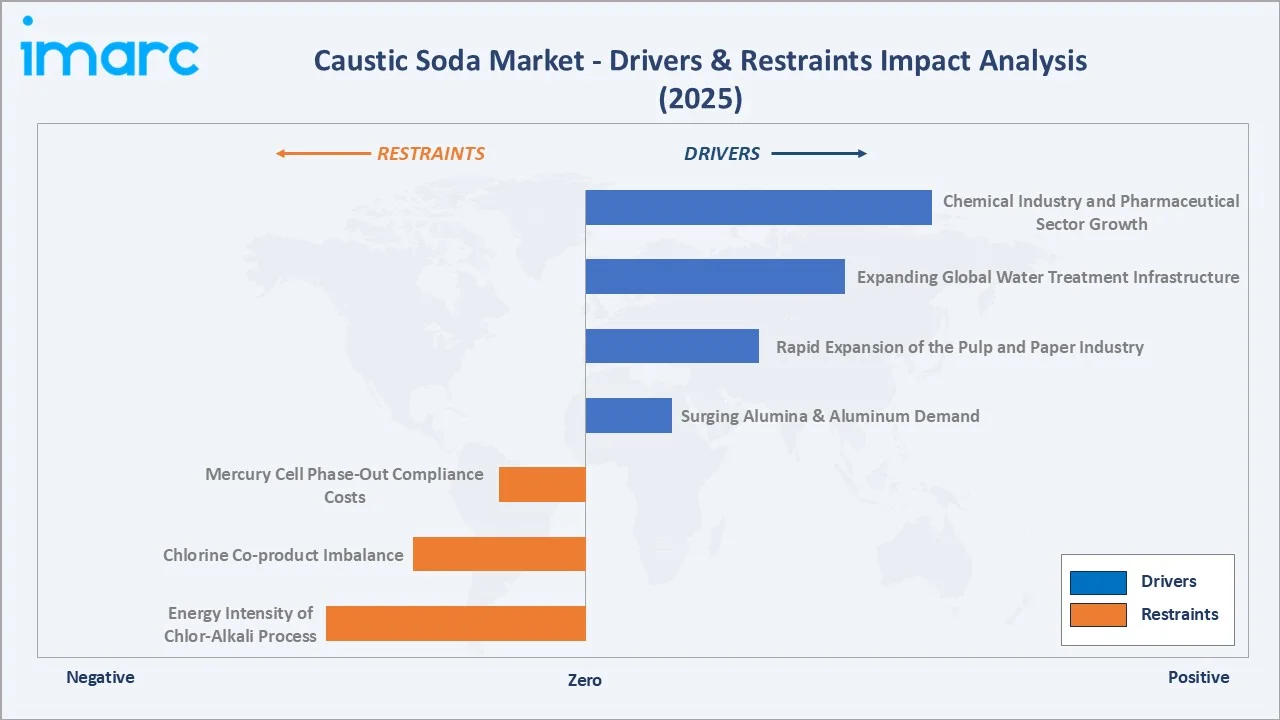

Market Drivers

- Surging Alumina and Aluminum Demand: Alumina refining via the Bayer process is the largest end-use of caustic soda globally, consuming significant volumes per unit of alumina produced. Global aluminum production exceeded 72.76 Million Tons in 2024, a 3.02% year-over-year increase per the International Aluminium Institute.

- Rapid Expansion of the Pulp and Paper Industry: Caustic soda is essential in the kraft pulping process for delignification and bleaching operations. Global pulp market demand stood at 66.02 million tons in 2022 and is expected to reach 73.84 million tons by 2028. E-commerce packaging growth steadily increases demand for containerboard, directly stimulating caustic soda procurement.

- Expanding Global Water Treatment Infrastructure: With global populations still lacking access to safely managed drinking water, governments worldwide are accelerating infrastructure investment. The water treatment chemicals market is projected to grow steadily, creating sustained demand for industrial-grade sodium hydroxid.

- Chemical Industry and Pharmaceutical Sector Growth: The global specialty chemicals market is estimated to grow at a CAGR of 5.68% from 2025 to 2034. Brenntag's December 2024 launch of 100% green caustic soda in the Netherlands and Belgium reflects expanding application diversity and sustainability-driven procurement shifts.

Market Restraints

- Energy Intensity of the Chlor-Alkali Process: Electrolysis represents a major share of total production costs. Electricity price volatility has significantly impacted producer margins and has led to temporary plant shutdowns in several regions.

- Chlorine Co-product Imbalance: Caustic soda output is structurally tied to chlorine production, meaning oversupply of one often forces adjustments in both. Weak demand from downstream sectors can result in inventory imbalances.

- Mercury Cell Phase-Out Compliance Costs: Transitioning from legacy mercury-cell to membrane-cell technology requires substantial capital investment per plant in developing markets.

Market Opportunities

- Green Caustic Soda and Sustainable Production: Increasing adoption of low-carbon and ESG-compliant production methods is reshaping procurement preferences, with buyers in food, pharma, and specialty chemicals showing a clear shift toward sustainable sourcing of NaOH.

- EV Battery and Advanced Material Supply Chains: Rapid expansion of EV manufacturing is creating strong downstream demand for alumina and battery-grade processing chemicals.

- Asia Pacific Industrial Expansion: Large-scale manufacturing initiatives are driving greenfield chlor-alkali capacity additions and long-term investment opportunities in the chemical sector.

Market Challenges

- Transportation and Handling Hazards: Caustic soda is a highly corrosive chemical, and strict regulations governing its movement significantly increase logistics complexity and costs, particularly for long-distance and cross-border supply chains.

- Price Sensitivity and Commodity Cyclicality: Caustic soda prices are highly volatile due to supply-demand imbalances, exposing producers to margin pressure and frequent contract renegotiation risks.

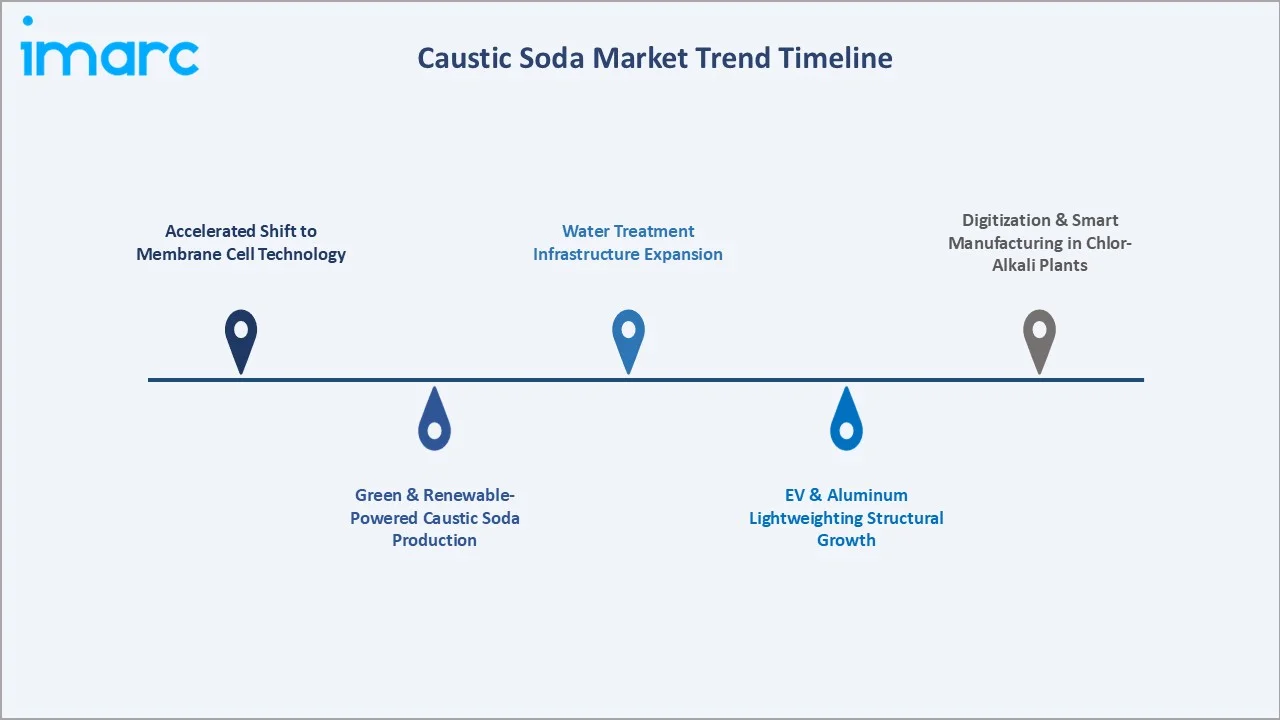

Emerging Market Trends

1. Accelerated Shift to Membrane Cell Technology

The global chlor-alkali industry is steadily shifting from diaphragm and mercury cell technologies toward membrane cell processes. Membrane cells offer lower electricity consumption and higher-purity NaOH output. With membrane technology already accounting for a dominant share of global capacity in 2025, diaphragm cell usage is expected to continue declining through 2034.

2. Green and Renewable-Powered Caustic Soda Production

Mounting ESG pressure and EU ETS Phase IV carbon pricing are encouraging chlor-alkali producers to shift toward renewable-powered electrolysis. Green NaOH is increasingly positioned at a premium in specialty end markets, reflecting early-stage commercialization and sustainability-linked procurement trends.

3. EV and Aluminum Lightweighting as Structural Growth Driver

Global EV production surpassed 17 million units in 2024, each requiring average 70-100 kg of aluminum. This is expanding bauxite-to-alumina conversion requirements, creating multi-year incremental demand for caustic soda across Asia Pacific and Middle Eastern alumina refinery capacity expansions through 2030.

4. Water Treatment Infrastructure Expansion

India’s rural water access programs and large-scale infrastructure initiatives in the Middle East are driving strong investment in water treatment capacity. Caustic soda demand from water treatment applications is expanding steadily, outpacing overall market growth.

5. Digitization and Smart Manufacturing in Chlor-Alkali Plants

AI-driven process optimization platforms deployed by major chlor-alkali producers are improving energy efficiency and extending membrane lifespan. Real-time electrolyzer monitoring also reduces unplanned downtime and enhances product quality consistency, particularly for pharmaceutical and food-grade applications.

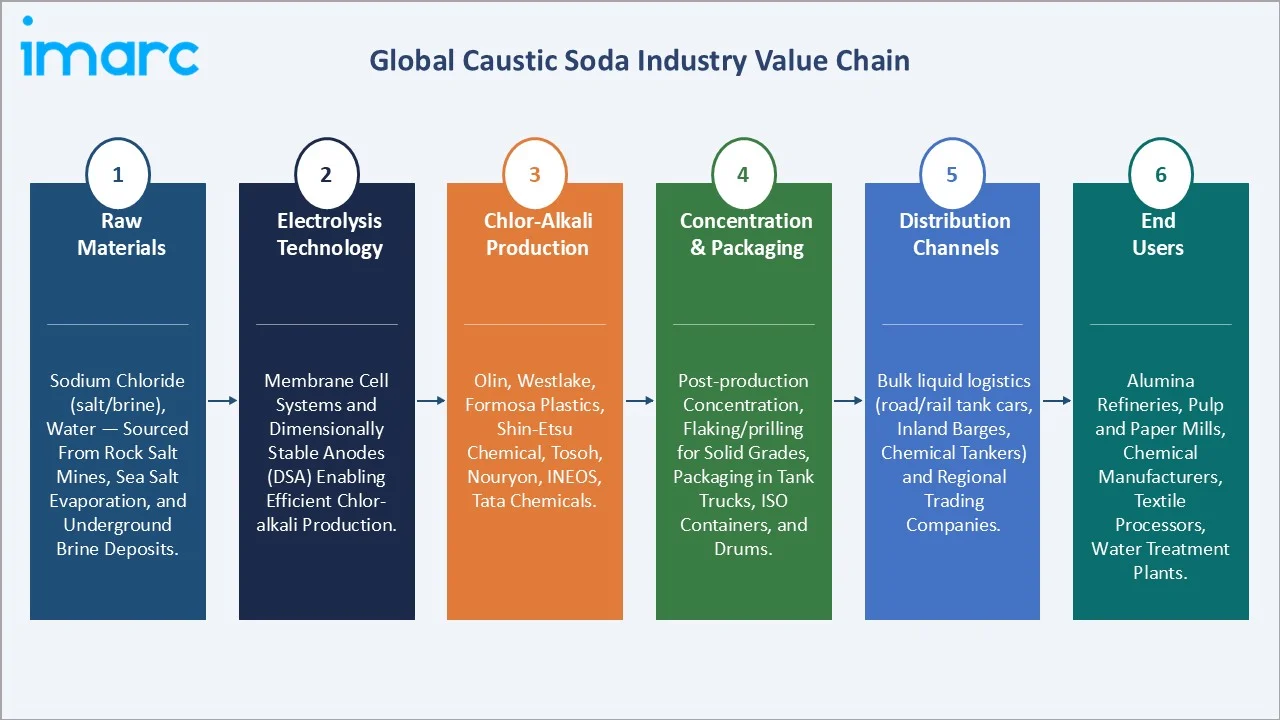

Industry Value Chain Analysis

The global caustic soda industry value chain spans six integrated stages from raw material procurement through end-user consumption. Each stage presents distinct competitive dynamics, energy cost profiles, and regulatory considerations relevant to the overall caustic soda market analysis.

| Value Chain Stage | Description |

|

Raw Materials |

Sodium chloride (salt/brine), water – sourced from rock salt mines, sea salt evaporation, or underground brine deposits; major suppliers in USA, Germany, India, China, and Chile |

|

Electrolysis Technology & Equipment |

Supplying membrane cell systems and dimensionally stable anodes (DSA), enabling efficient chlor-alkali production with lower energy consumption, higher purity output, and improved operational stability. |

|

Chlor-Alkali Production |

Olin Corporation, Westlake Corporation, Formosa Plastics Corporation, Shin-Etsu Chemical Co., Ltd., Tosoh Corporation, Nouryon, INEOS, Tata Chemicals Ltd. |

|

Concentration & Packaging |

Post-production concentration, flaking/prilling for solid grades, and packaging into tank trucks, ISO containers, drums, and bulk ships |

|

Distribution Channels |

Bulk liquid logistics (road/rail tank cars, inland barges, chemical tankers), chemical distributors, and regional trading companies |

|

End Users |

Alumina refineries, pulp and paper mills, chemical manufacturers, textile processors, water treatment plants, soap and detergent producers, oil and gas refineries, food processors, pharmaceutical manufacturers |

Integrated chlor-alkali producers hold the highest strategic value, managing raw material sourcing through quality-controlled NaOH delivery. Chemical distributors are critical intermediaries for small-to-mid-size industrial buyers seeking smaller volumes and just-in-time delivery.

Technology Landscape in the Caustic Soda Industry

Membrane Cell Technology

Membrane cell electrolysis accounts for the majority of global caustic soda production capacity in 2025. Ion-exchange membranes such as Nafion and Flemion grades enable production of high-purity caustic soda solutions. Ongoing advancements in membrane durability have significantly extended operational lifespans, reducing overall per-ton operating costs.

Diaphragm Cell Technology

Diaphragm cells account for a small share of global capacity in 2025, primarily operating in legacy facilities. They produce lower-purity caustic soda that requires additional concentration, resulting in significantly higher energy consumption compared to membrane-based processes.

Oxygen-Depolarized Cathode (ODC) Technology

ODC technology enables significant reductions in electricity consumption compared to standard membrane cell processes. Leading industrial players have conducted commercial-scale demonstrations in Europe, with broader adoption anticipated toward the end of the decade.

Green Hydrogen and Renewable Energy Integration

The chlor-alkali process co-produces hydrogen, increasingly valuable as a clean energy carrier. Coupling electrolysis with renewable power enables simultaneous green NaOH and green hydrogen production, creating dual revenue streams and improving project economics.

Digital Process Optimization

AI-driven process control systems deployed across major chlor-alkali complexes are improving operational efficiency by reducing energy consumption and enhancing process stability. These systems also support more consistent product quality, particularly for high-purity pharmaceutical and food-grade applications.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | Lye | 57.0% | 2025 |

| Manufacturing Process | Membrane Cell | 82.0% | 2025 |

| Grade | Industrial Grade | 42.0% | 2025 |

| Application | Alumina | 17.6% | 2025 |

| Region | Asia-Pacific | 61.7% | 2025 |

By Product Type

To access detailed market analysis, Request Sample

Lye leads the global caustic soda market by product type with a 57.0% share in 2025. Lye - typically supplied as a 50% aqueous solution - is the preferred form for large-scale industrial consumers due to its handling efficiency and direct incorporation into process streams. Alumina refineries, paper mills, and large chemical plants overwhelmingly use lye form.

By Manufacturing Process

Membrane Cell dominates global caustic soda production with an 82.0% share in 2025. Its energy efficiency advantage makes it the technology of choice for both greenfield investments and capacity upgrades. China's capacity has transitioned substantially to membrane technology since 2013 regulatory mandates.

Regional Market Insights

| Region | Share (2025) | Key Growth Drivers |

|

Asia Pacific |

61.7% |

China chlor-alkali capacity, India alumina expansion, ASEAN textile growth, water infrastructure |

|

North America |

14.2% |

Alumina smelting, EV manufacturing, water treatment upgrades, shale-gas chemical complex growth |

|

Europe |

12.8% |

Pulp & paper demand, chemical synthesis, EU carbon pricing driving green NaOH adoption |

|

Middle East & Africa |

6.4% |

Water desalination, alumina refinery projects, petrochemical expansion, Saudi Vision 2030 |

|

Latin America |

4.9% |

Brazil pulp & paper, expanding water treatment, mining chemical applications |

Asia Pacific commands a dominant 61.7% global share in 2025. China holds the largest share of global caustic soda production, supported by extensive chlor-alkali capacity. India remains a key growth market, driven by expanding aluminium refining activities and large-scale water infrastructure programs. The region is expected to witness steady growth over the forecast period.

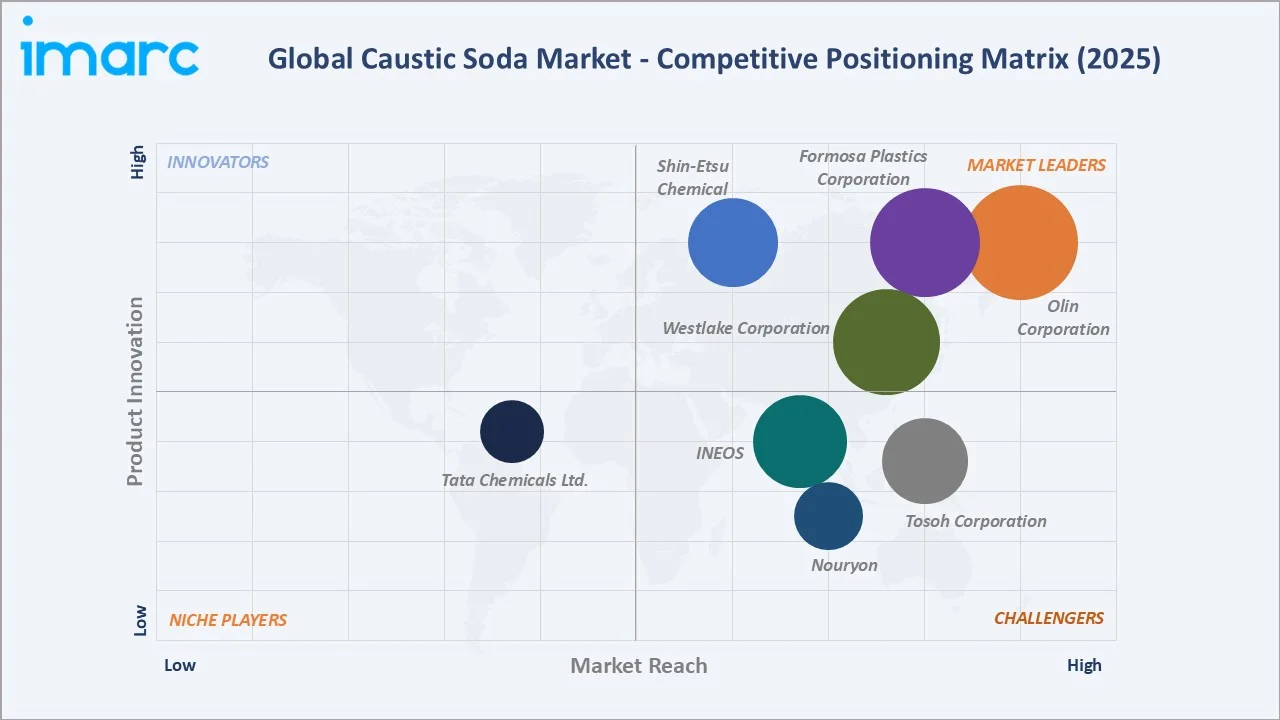

Competitive Landscape

| Company Name | Key Brand / Platform | Market Position | Core Strength |

|

Olin Corporation |

Olin Chlor Alkali Products |

Leader |

Largest U.S. chlor-alkali producer; fully integrated operations; ECU margin management |

|

Westlake Corporation |

Westlake Chlor-alkali |

Leader |

Integrated PVC/VCM/caustic chain; North America and European operations |

|

Formosa Plastics Corporation |

Formosa Plastics Chlor-Alkali |

Leader |

Taiwan-based; integrated chlor-alkali and PVC; major Asia Pacific exporter |

|

Shin-Etsu Chemical Co., Ltd. |

Shin-Etsu PVC/Clor Alkali |

Leader |

Japan's largest chlor-alkali producer; premium quality NaOH for semiconductor and pharma |

|

Tosoh Corporation |

Tosoh Chlor-alkali |

Challenger |

Japan-based; diversified downstream including silica, pharma; specialty NaOH grades |

|

Nouryon |

Nouryon Industrial Chemicals |

Challenger |

Europe-based; specialty and industrial NaOH; green chemistry focus; Brenntag distribution |

|

INEOS |

INEOS Inovyn |

Challenger |

UK-based; major European chlor-alkali; largest UK chlorine producer; Runcorn complex |

|

Tata Chemicals Ltd. |

Allied Chemicals |

Emerging |

India's leading producer; Mithapur complex; serves India domestic & export markets |

The global caustic soda market's competitive landscape is moderately concentrated at the top, with the top five producers. Competition is primarily based on production cost, geographic proximity to downstream consumers, product quality specifications, and long-term supply reliability.

Key Company Profiles

Olin Corporation

Olin Corporation, headquartered in Scottsdale, Arizona, USA, is the world's largest fully integrated chlor-alkali producer by capacity. It operates through its Chlor Alkali Products and Vinyls (CAPV) segment, with production facilities across the United States, Europe, and Asia.

- Product Portfolio: Liquid caustic soda (50% and 73% solutions), caustic flakes, chlorine, hydrochloric acid, bleach, and potassium hydroxide. Serves alumina, pulp & paper, chemical synthesis, and water treatment customers globally.

- Recent Developments: In 2025, Olin Corporation and Mitsui & Co. have mutually agreed to end their Blue Water Alliance joint venture focused on caustic soda and ethylene dichloride (EDC) trading by the end of 2025. The JV was originally formed to strengthen global trading and logistics for chlor-alkali derivatives.

- Strategic Focus: Olin's strategy centers on ECU margin maximization, disciplined capacity management, and long-term off-take agreements with blue-chip industrial buyers, while advancing renewable energy procurement to reduce per-ton electricity costs.

Westlake Corporation

Westlake Corporation, headquartered in Houston, Texas, USA, is a global leader in petrochemicals, polymers, and building products, with caustic soda as a strategic co-product from its integrated PVC and vinyl chain.

- Product Portfolio: Caustic soda (liquid and flake), chlorine, ethylene dichloride, PVC resin, and chlorinated solvents. Major customers include aluminum smelters, paper mills, and water treatment utilities.

- Recent Developments: In 2022, Westlake Corporation officially changed its chemical portfolio while maintaining its core chlor-alkali operations, including chlorine and caustic soda production. The company is focusing on optimizing its integrated assets amid ongoing industry restructuring and cost pressures.

- Strategic Focus: Westlake leverages the vertical integration of its ethylene-PVC-chlor-alkali chain to optimize ECU economics, pursuing membrane cell upgrades at legacy diaphragm-cell facilities to reduce energy consumption.

Formosa Plastics Corporation

Formosa Plastics Corporation, headquartered in Taipei, Taiwan, is one of the largest chlor-alkali and PVC producers in Asia. Its caustic soda operations are integrated with an extensive petrochemical complex, and it is a major exporter across Asia Pacific.

- Product Portfolio: Caustic soda (liquid and flake), chlorine, PVC, ethylene dichloride, and specialty chlorinated products known for high purity and consistent quality.

- Recent Developments: In 2026, Formosa Plastics Corporation highlights continued regulatory compliance of its caustic soda, which meets FDA food-contact standards and is classified as GRAS for approved food applications. The development reinforces its positioning in high-purity, food-grade chemical supply supported by strict GMP and international safety frameworks.

- Strategic Focus: Formosa leverages scale integration and cost-efficient energy procurement to maintain competitive ECU margins in Asia Pacific, expanding Southeast Asian market reach through distribution partnerships in Vietnam and Indonesia.

Market Concentration Analysis

The global caustic soda market exhibits a moderate-to-low concentration profile at the global level, with significant regional fragmentation in Asia. The top five global producers - Olin Corporation, Westlake Corporation, Formosa Plastics Corporation, Shin-Etsu Chemical Co., Ltd., Tosoh Corporation - collectively account for an estimated 25-30% of global production capacity in 2025.

China’s chlor-alkali industry includes many producers, while output is relatively concentrated among leading players. The market remains moderately fragmented, with gradual consolidation being encouraged by stricter energy efficiency standards and regulatory capacity requirements.

The market is experiencing gradual consolidation in developed markets (North America and Europe), where scale economics and compliance costs are raising the minimum viable plant size. Further M&A consolidation is expected through 2034 as energy transition costs require scale for amortization.

Investment & Growth Opportunities

Fastest-Growing Segments

Flake NaOH demand is growing at an above-average pace in Middle Eastern and Southeast Asian markets. The specialty pharmaceutical-grade NaOH segment commands a significant price premium over industrial grades and continues to expand at a steady growth rate. Nearly all recent chlor-alkali project approvals globally are based on membrane cell technology, reflecting its dominance in new capacity additions.

Emerging Market Expansion

India represents one of the highest-potential emerging markets, with domestic caustic soda demand expected to grow at a strong pace through 2030, well above the global average. Bangladesh’s textile sector is also a major consumption hub, with robust growth expected to continue in the coming years driven by export-oriented manufacturing expansion.

Venture and Strategic Investment Trends

Strategic investment is increasingly focused on renewable energy integration for low-carbon NaOH production, adoption of ODC technology to reduce electricity intensity, and expansion of distribution networks across Africa and Southeast Asia. Broader industry momentum is also being supported by green hydrogen initiatives, where caustic soda emerges as a key co-product within evolving decarbonization ecosystems.

Future Market Outlook (2026-2034)

The global caustic soda market forecast projects steady volume expansion from 84.4 Million Tons in 2025 to 95.9 Million Tons by 2034 at a CAGR of 1.39%. Asia Pacific will retain overwhelming regional leadership while expanding structurally. North America and Europe will maintain stable demand supported by alumina, chemicals, and water treatment.

Three structural shifts are expected to reshape the caustic soda market through 2034. First, rising demand from aluminum-intensive and electrification-driven industries will create significant incremental consumption alongside expanding primary aluminum capacity. Second, green NaOH adoption will increasingly segment the market into conventional and sustainability-certified product categories. Third, ongoing capacity consolidation in Asia Pacific is expected to improve operating efficiency and support more stable global pricing dynamics.

By 2034, the global caustic soda market will be dominated by large-scale, low-cost Asian producers operating membrane cell facilities powered by an increasing share of renewable electricity, while North American and European producers differentiate through specialty-grade quality, sustainability certification, and integrated chlorine downstream value chains.

Research Methodology

Primary Research

Primary research conducted in 2024-2025 encompassed structured interviews with chlor-alkali industry stakeholders including plant directors at global NaOH producers, procurement managers at alumina refineries, chemical traders, distribution executives at Brenntag and Univar Solutions, and investment analysts covering the specialty chemicals sector.

Secondary Research

Secondary sources include International Aluminium Institute production reports, UN environment and water access publications, Eurostat chemical production statistics, China National Chlor-Alkali Industry Association data, CEFIC annual reports, company annual reports (Olin Corporation, Westlake Corporation, Formosa Plastics Corporation), Chemical Week and ICIS trade publications.

Forecasting Models

Market size estimations and growth projections employed both bottom-up and top-down forecasting models. Bottom-up aggregation modeled caustic soda consumption across five key end-use sectors across 30+ countries. Scenario analysis (base, optimistic, and conservative) was performed to account for energy price volatility and EV adoption rate uncertainty.

Caustic Soda Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Tons |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Lye, Flake, Others |

| Manufacturing Process Covered | Membrane Cell, Diaphragm Cell, Others |

| Grades Covered | Reagent Grade, Industrial Grade, Pharmaceutical Grade, Others |

| Applications Covered | Alumina, Inorganic Chemicals, Organic Chemicals, Food, Pulp, and Paper, Soap and Detergents, Textiles, Water Treatment, Steel/Metallurgy-Sintering, Others. |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Olin Corporation, Westlake Corporation, Formosa Plastics Corporation, Shin-Etsu Chemical Co., Ltd., Tosoh Corporation, Nouryon, INEOS, Tata Chemicals Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the caustic soda market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global caustic soda market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the caustic soda industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Caustic Soda Market Report

The global caustic soda market reached 84.4 Million Tons in 2025, driven by alumina production, pulp and paper expansion, water treatment infrastructure, and chemical industry growth across emerging economies globally.

The market is projected to reach 95.9 Million Tons by 2034, growing at a CAGR of 1.39% during 2026-2034, supported by EV-driven aluminum demand, water treatment infrastructure expansion, and chemical manufacturing growth.

Lye (liquid caustic soda) leads with 57.0% share in 2025, preferred by large industrial consumers including alumina refineries, paper mills, and chemical plants due to its handling efficiency and direct process integration.

The membrane cell process dominates with 82.0% share in 2025, valued for its 15-30% energy efficiency advantage over diaphragm cells and superior product purity, making it the standard for all new global capacity additions.

Asia Pacific dominates with 61.7% share in 2025. China's massive chlor-alkali installed base and India's expanding alumina and textile industries underpin the region's commanding global leadership.

Key drivers include surging alumina refining demand from EV lightweighting, pulp and paper industry expansion, global water treatment infrastructure investment, chemical manufacturing growth, and sustainable green NaOH product development.

Major players include Olin Corporation, Westlake Corporation, Formosa Plastics Corporation, Shin-Etsu Chemical Co., Ltd., Tosoh Corporation, Nouryon, INEOS, and Tata Chemicals Ltd.

Membrane cell technology and specialty/pharmaceutical-grade NaOH are the fastest-growing segments, expanding at a pace above the overall market due to ongoing technology transitions and rising demand from healthcare and electronics applications.

Green caustic soda is produced using renewable energy-powered electrolysis, yielding carbon-neutral NaOH. Brenntag launched it commercially in the Netherlands and Belgium in December 2024, targeting ESG-driven buyers in food, pharma, and specialty chemical sectors.

Caustic soda and chlorine are co-produced in fixed molar ratios via the chlor-alkali process. Demand imbalances between the two products drive capacity utilization adjustments and global trade flows.

Key challenges include high electricity cost exposure, chlorine co-product demand imbalances, transportation hazard regulations for corrosive materials, and capital-intensive technology conversion requirements from legacy processes.

The global caustic soda market is projected to reach 90.4 Million Tons by 2030, representing approximately 7.1% cumulative growth from the 2025 base, driven by alumina refinery expansions in Asia Pacific and water treatment infrastructure globally.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)