Cell-based Assay Market Size, Share, Trends and Forecast by Product and Services, Technology, Application, End-User, and Region, 2026-2034

Cell-Based Assay Market Size, Share, Trends & Forecast (2026-2034)

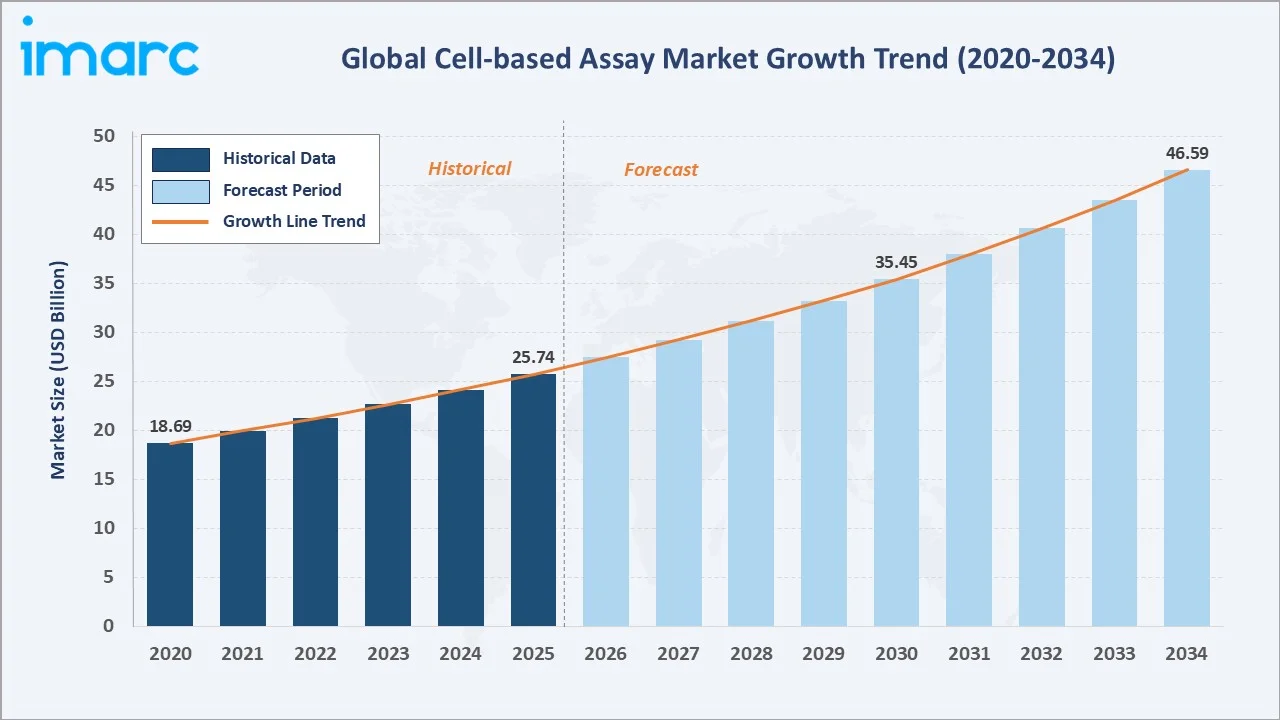

The Cell-Based assay market was valued at USD 25.74 Billion in 2025 and is projected to reach USD 46.59 Billion by 2034, exhibiting a CAGR of 6.61% during 2026-2034. Rising pharmaceutical R&D investments, increasing cancer prevalence, and the regulatory shift away from animal testing are the primary drivers shaping the market growth. In March 2025, the California Institute for Regenerative Medicine (CIRM) approved funding of USD 425 Million for Cell-Based research across discovery, preclinical, and clinical stages, underscoring the robust government support propelling this market forward.

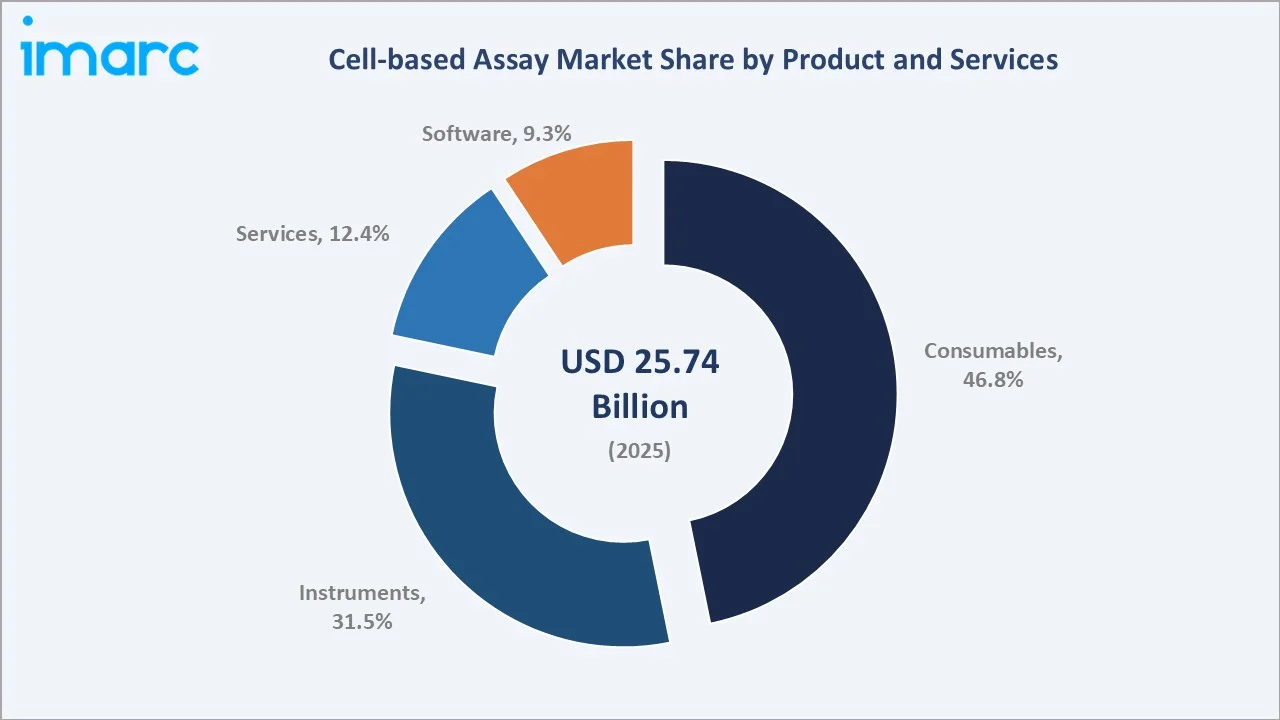

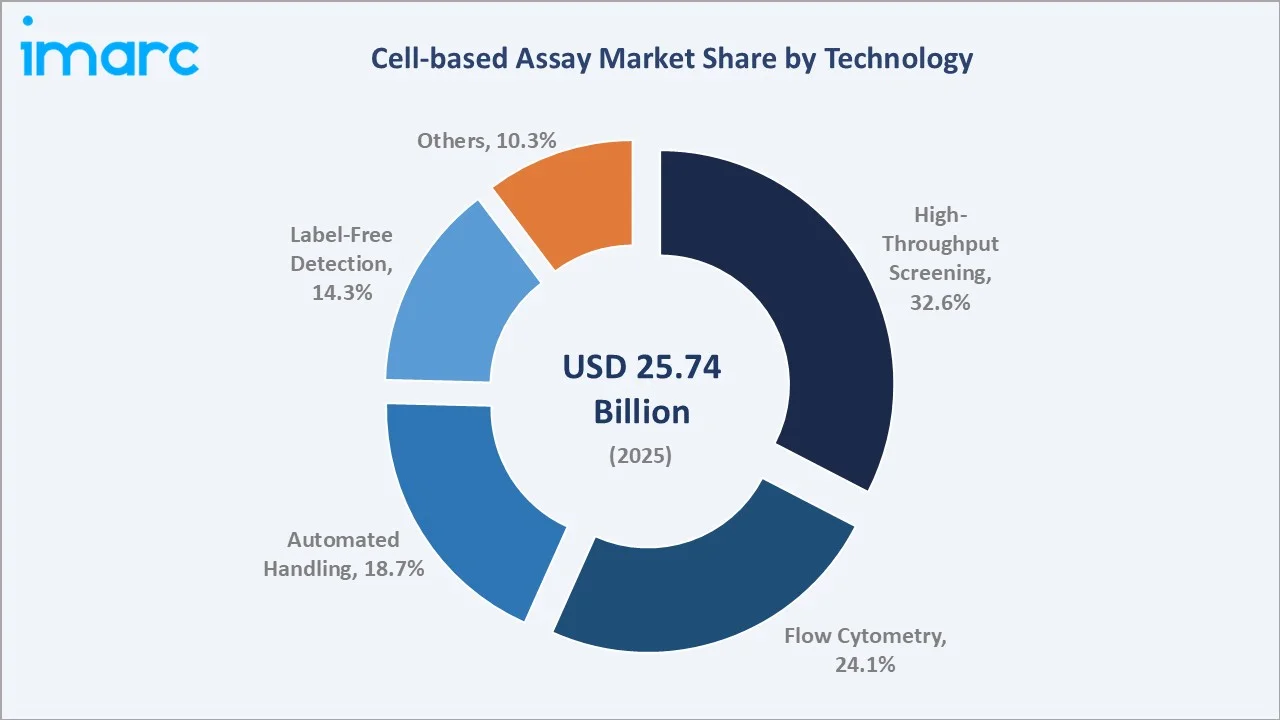

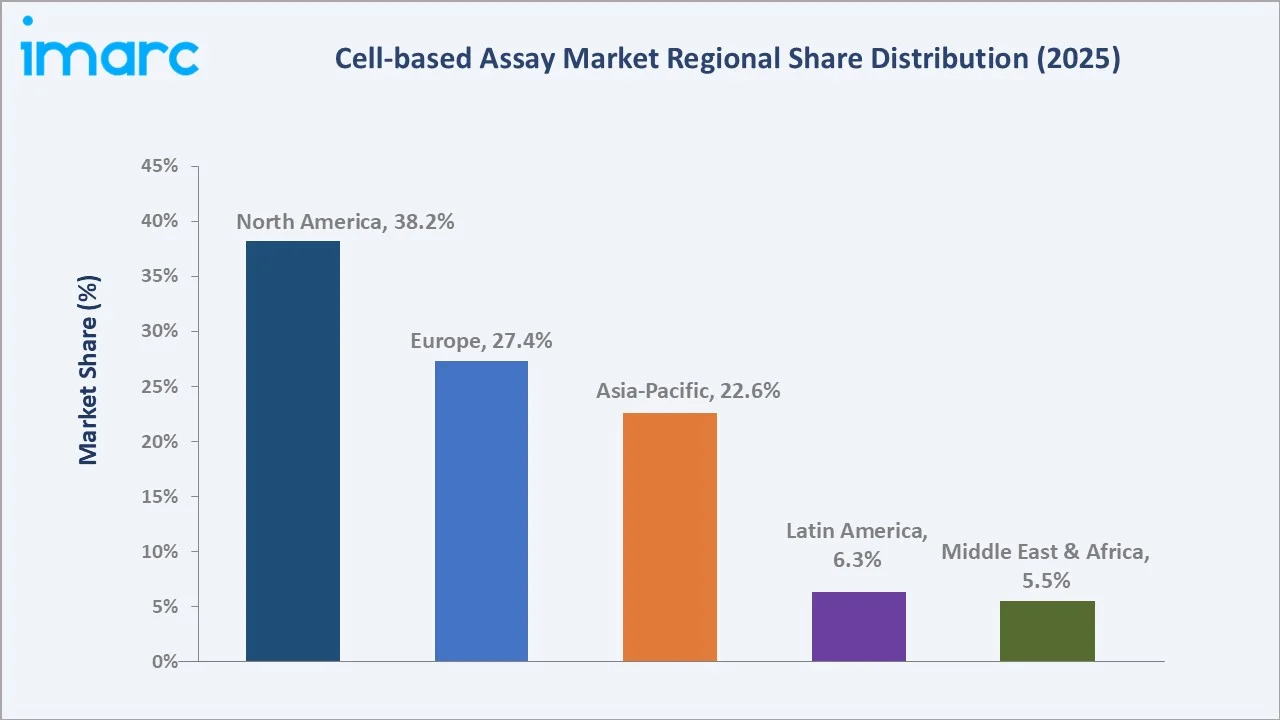

Consumables lead the product and services segment at 46.8%, high-throughput screening dominates the technology segment at 32.6%, and North America commands 38.2% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 25.74 Billion |

|

Forecast Market Size (2034) |

USD 46.59 Billion |

|

CAGR (2026-2034) |

6.61% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (38.2%, 2025) |

|

Fastest Growing Region |

Asia-Pacific (22.6%, 2025) |

|

Leading Product and Services Segment |

Consumables (46.8%, 2025) |

|

Leading Technology |

High-Throughput Screening (32.6%, 2025) |

The Cell-Based assay market expanded from USD 18.69 Billion in 2020 to USD 25.74 Billion in 2025, driven by accelerating drug discovery pipelines, advancing screening technologies, and supportive regulatory frameworks. Anchored at USD 35.45 Billion in 2030, the forecast to USD 46.59 Billion by 2034 is supported by growing demand for human-relevant in vitro models and artificial intelligence (AI)-integrated analytics.

To get more information on this market, Request Sample

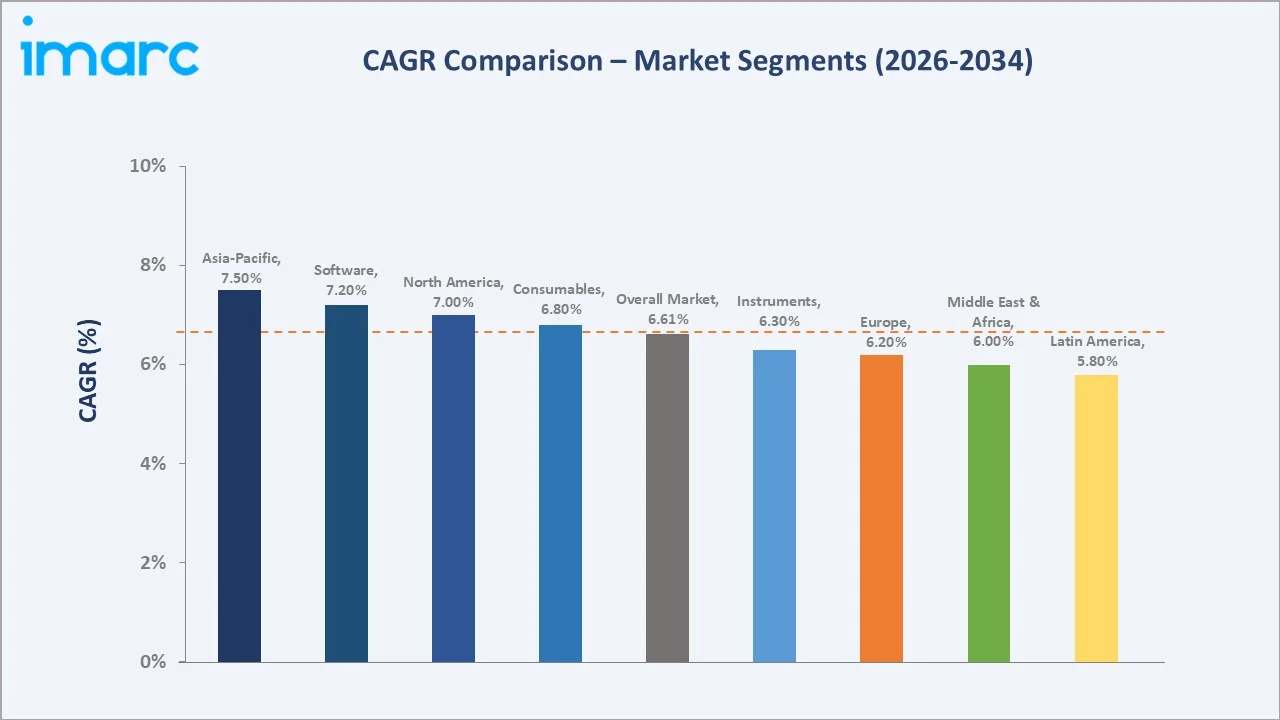

CAGR trajectories across product and services and technology sub-segments show software and Asia-Pacific expanding faster than the overall 6.61% market CAGR, driven by AI-enabled analytics and expanding biotech ecosystems in emerging economies.

Executive Summary

The Cell-Based assay market is on a strong growth path from USD 18.69 Billion in 2020 to USD 46.59 Billion by 2034. Cell-Based assays have evolved from specialized laboratory techniques to indispensable tools across drug discovery, toxicology screening, and personalized medicine. Declining costs of high-throughput screening instruments and growing preference for physiologically relevant testing models are encouraging broader adoption.

Consumables dominate the product and services segment at 46.8% in 2025, driven by recurring demand for reagents, assay kits, and cell lines across pharmaceutical and academic laboratories. High-throughput screening leads the technology segment at 32.6%, supported by its established role in large-scale compound screening and dose-response profiling. North America commands a 38.2% share, led by the United States, fueled by robust biopharma R&D budgets and deep institutional research infrastructure. As per the National Science Foundation, funding for R&D is on the rise in the United States, with an anticipated total of USD 993 Billion spent on R&D in 2024.

Key Market Insights

|

Insight |

Data |

|

Leading Product and Services Segment |

Consumables - 46.8% share (2025) |

|

Second Product and Services Segment |

Instruments - 31.5% share (2025) |

|

Leading Technology |

High-Throughput Screening - 32.6% share (2025) |

|

Second Technology |

Flow Cytometry - 24.1% share (2025) |

|

Leading Region |

North America - 38.2% share (2025) |

|

Fastest Growing Region |

Asia-Pacific - 22.6% share (2025) |

|

Top Companies |

Thermo Fisher Scientific Inc., Danaher Corporation, BD, Promega Corporation, Lonza, Charles River Laboratories |

Key Analytical Observations Expanding on the Data Above:

- Consumables dominance at 46.8% is driven by the recurring consumption of reagents, assay kits, cell lines, and microplates essential for daily laboratory operations across pharmaceutical and academic research settings.

- Instruments at 31.5% reflect sustained capital investment in flow cytometers, plate readers, and high-content imaging systems that enable multi-parameter cellular analysis at scale.

- High-throughput screening leadership at 32.6% is supported by its well-established role in large-scale compound libraries screening and its integration with automated liquid handling platforms for drug discovery workflows.

- Flow cytometry at 24.1% is expanding through spectral technologies that enable simultaneous multi-parameter cellular analysis, supporting advanced immunophenotyping and cell sorting applications.

- North America at 38.2% dominates owing to the concentration of leading biopharma companies, strong NIH funding allocations, and advanced CRO infrastructure. In FY 2024, the Congressional budget allocation for NIH reached USD 48.6 Billion, reflecting an increase of USD 300 Million over FY 2023.

Cell-Based Assay Market Overview

Cell-Based assays are laboratory techniques that use living cells to measure biological activity, cell viability, proliferation, cytotoxicity, and signaling pathway modulation. These assays are widely applied in drug discovery, toxicity screening, and basic biomedical research.

The global ecosystem integrates reagent and cell line suppliers, instrument manufacturers, assay development service providers, contract research organizations, regulatory bodies, and end-use institutions including pharmaceutical companies, academic laboratories, and diagnostic facilities. Together, they enable the development of predictive, human-relevant testing models that are replacing traditional animal-based approaches.

Market Dynamics

To evaluate market opportunities, Request Sample

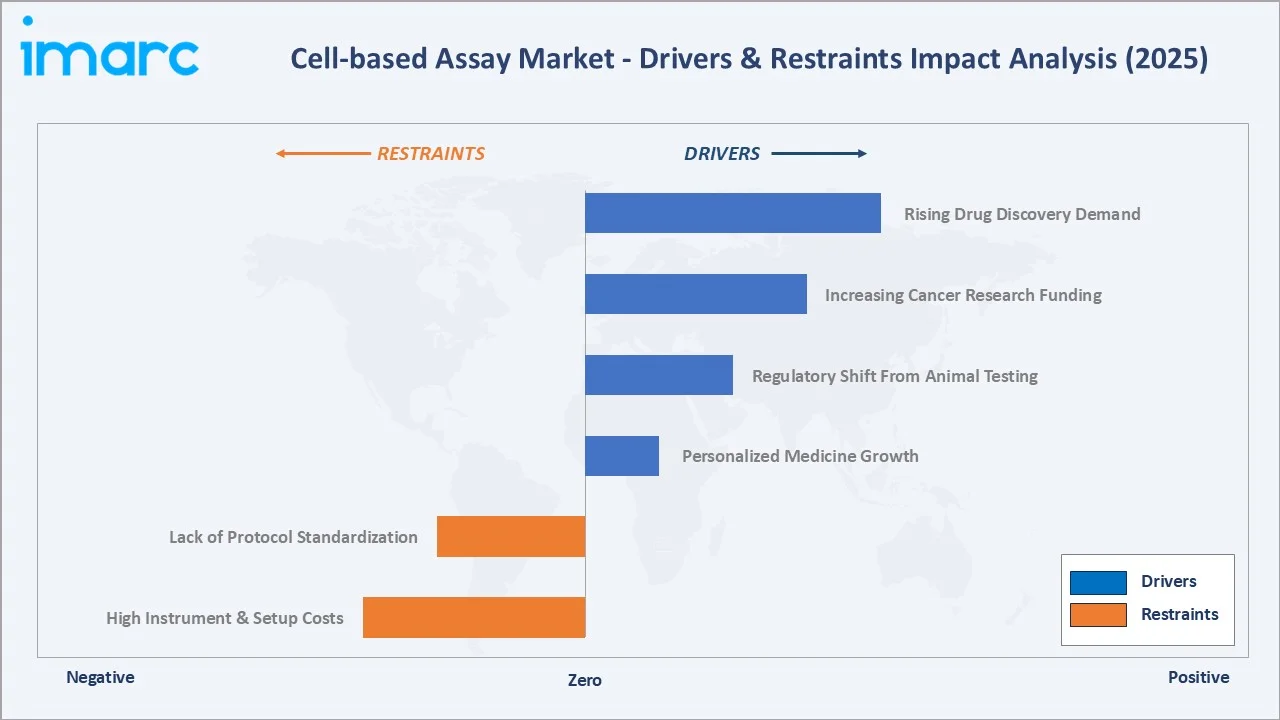

Market Drivers

- Rising Drug Discovery and Development Demand: Pharmaceutical and biotechnology companies are increasingly relying on Cell-Based assays to screen compound libraries, assess drug efficacy, and evaluate safety profiles, driving steady demand growth across the industry.

- Increasing Cancer Research Funding: Growing government and private-sector investments in oncology research are expanding the utilization of Cell-Based assays for tumor profiling, immunotherapy development, and anti-cancer compound screening.

- Regulatory Shift Away From Animal Testing: The April 2025 FDA decision to phase out animal testing requirements is positioning validated Cell-Based platforms at the center of regulatory-compliant drug development, accelerating market adoption across therapeutic areas.

- Personalized Medicine Growth: The expanding focus on precision therapeutics is increasing demand for patient-specific cellular models, driving adoption of advanced assay platforms for targeted drug response profiling.

Market Restraints

- High Instrument and Setup Costs: Advanced Cell-Based assay instruments, including high-content imaging systems and automated liquid handlers, require significant capital investment. This creates affordability barriers for smaller research institutions and emerging-market laboratories.

- Lack of Protocol Standardization: Variations in assay protocols, cell culture conditions, and data interpretation frameworks across laboratories create reproducibility challenges. The absence of universally accepted validation benchmarks further complicates cross-study comparisons and regulatory alignment.

Market Opportunities

- AI Integration in Screening Workflows: AI and machine learning (ML) are being integrated with high-content screening platforms to enable automated image analysis, phenotypic classification, and predictive modeling, opening new efficiency gains in drug discovery.

- Emerging Market Expansion: Rapidly growing biotech sectors in China, India, and South Korea, supported by expanding government research funding and CRO infrastructure development, present strong opportunities for market penetration.

Market Challenges

- Complex Assay Design Requirements: Developing physiologically relevant assay models, including 3D cell cultures and organ-on-chip systems, requires specialized expertise and multi-disciplinary coordination that many laboratories still lack.

- Skilled Personnel Shortage: The increasing complexity of Cell-Based assay technologies is creating demand for highly trained professionals with expertise in cell biology, automation, and data analytics, which remains a constraint across both developed and emerging markets.

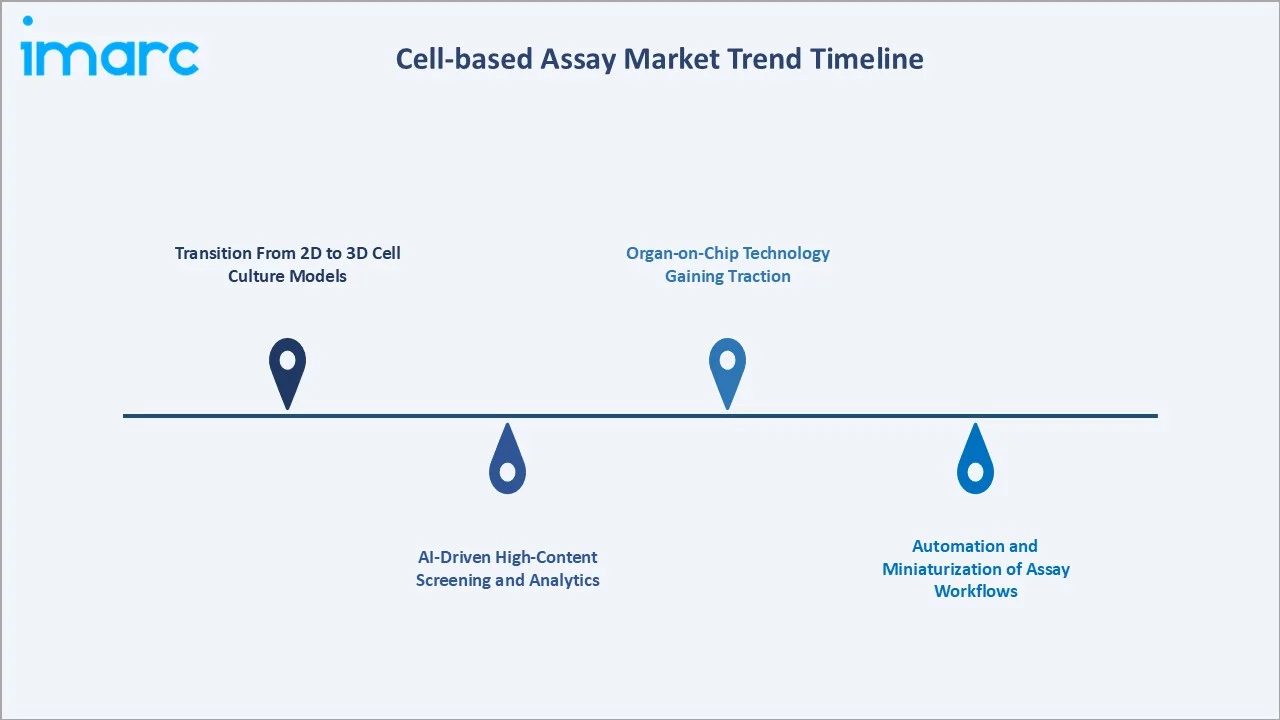

Emerging Market Trends

1. Transition From 2D to 3D Cell Culture Models

Three-dimensional cell culture models, including spheroids, organoids, and tumoroids, are increasingly replacing traditional 2D monolayer cultures in drug screening and toxicity testing. These models provide more physiologically relevant microenvironments that better replicate in vivo tissue architecture. This transition is improving the predictive accuracy of preclinical studies and reducing late-stage drug attrition rates.

2. AI-Driven High-Content Screening and Analytics

ML algorithms are being integrated with high-content imaging platforms to automate cellular phenotype classification, identify subtle morphological changes, and predict compound activity patterns. This integration is accelerating screening throughput while reducing manual analysis bottlenecks across pharmaceutical and biotech R&D workflows.

3. Organ-on-Chip Technology Gaining Traction

Microfluidic organ-on-chip devices that simulate human organ functions are emerging as next-generation alternatives for toxicity and efficacy testing. These platforms enable multi-organ interaction modeling, offering improved translational relevance compared to single-cell-type assays.

4. Automation and Miniaturization of Assay Workflows

Laboratory automation platforms incorporating robotic liquid handling, automated plate readers, and integrated data management systems are streamlining Cell-Based assay workflows. Assay miniaturization is reducing reagent consumption and enabling higher-throughput screening at lower per-assay costs.

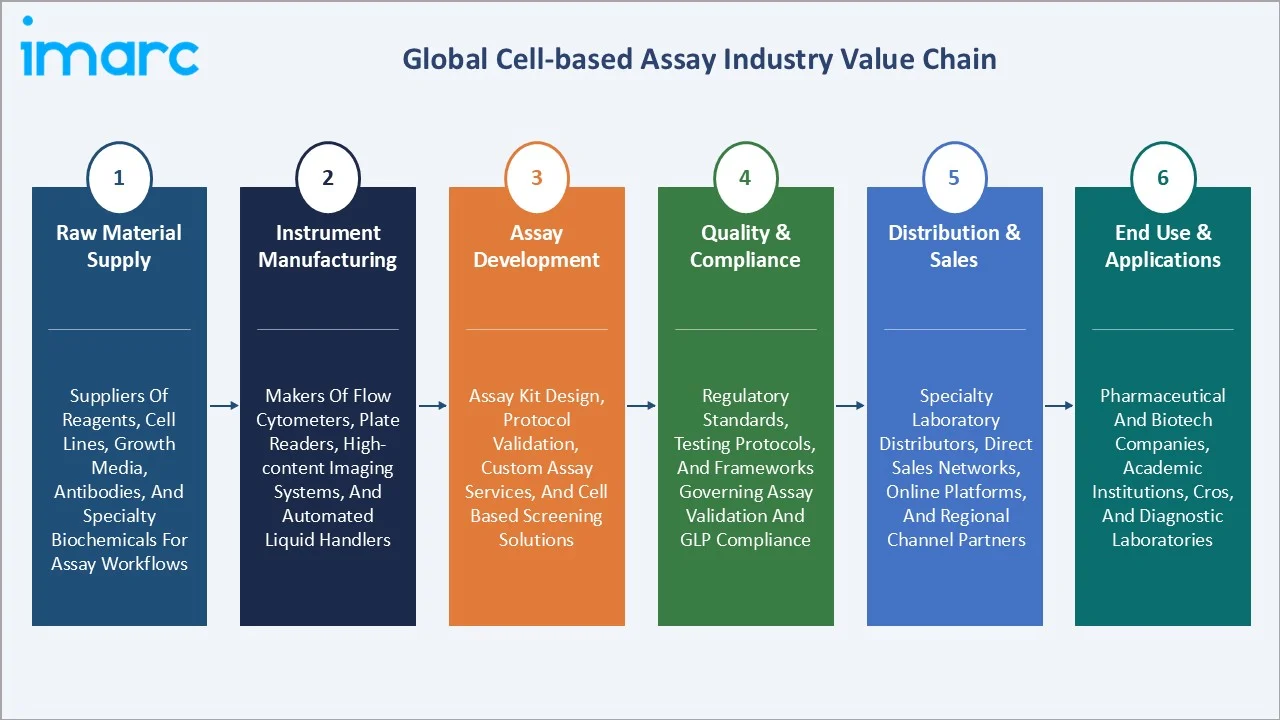

Industry Value Chain Analysis

The Cell-Based assay value chain spans six stages from raw material supply through end use applications. Instrument manufacturing and assay development capture the highest value-add, while distribution relationships and end user service contracts generate downstream competitive advantages in this technology-intensive category.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Suppliers of reagents, cell lines, growth media, antibodies, and specialty biochemicals supporting assay development and research workflows |

|

Instrument Manufacturing |

Manufacturers of flow cytometers, plate readers, high-content imaging systems, and automated liquid handling platforms for laboratory use |

|

Assay Development |

Companies specializing in assay kit design, protocol validation, custom assay services, and Cell-Based screening solutions for drug discovery |

|

Quality & Compliance |

Regulatory standards, testing protocols, and frameworks governing assay validation, GLP compliance, and data integrity across research applications |

|

Distribution & Sales |

Specialty laboratory distributors, direct sales networks, online platforms, and regional channel partners serving research institutions |

|

End Use & Applications |

Pharmaceutical and biotechnology companies, academic research institutions, contract research organizations, and diagnostic laboratories |

Vertically integrated players, which span reagent supply through instrument manufacturing and service delivery, achieve superior cost control and portfolio breadth versus specialized niche competitors. Their integrated capabilities also support faster workflow optimization and stronger customer retention across research and clinical applications.

Technology Landscape in the Cell-Based Assay Industry

High-Throughput and High-Content Screening

High-throughput screening platforms remain the backbone of large-scale compound evaluation in drug discovery. The integration of high-content screening capabilities, which combine automated microscopy with multi-parameter image analysis, is enabling deeper phenotypic characterization of cellular responses. These combined platforms are improving hit identification rates and reducing false-positive progression in early-stage pipelines.

Flow Cytometry and Spectral Analysis

Multi-parameter flow cytometry has advanced significantly with the introduction of spectral detection technologies that enable simultaneous analysis of multiple cellular markers. These innovations are expanding applications in immunophenotyping, cell sorting, and rare-cell detection. New spectral platforms with AI-integrated analysis are further improving data resolution and experimental reproducibility.

Label-Free Detection Technologies

Label-free assay platforms based on impedance sensing, surface plasmon resonance, and optical biosensors are gaining adoption for real-time monitoring of cell adhesion, proliferation, and morphology changes. These technologies eliminate the need for fluorescent or radioactive labels, providing unperturbed measurements of cellular behavior that improve assay reliability and reduce experimental artifacts.

Automation and Digital Integration

Connected laboratory systems with cloud-based data management, robotic sample handling, and AI-driven workflow optimization are transforming Cell-Based assay operations. These capabilities enable higher reproducibility, reduced manual intervention, and seamless integration with electronic laboratory notebooks and LIMS platforms across multi-site research operations.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product and Services |

Consumables |

46.8% |

2025 |

|

Technology |

High-Throughput Screening |

32.6% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

End-User |

🔒 |

🔒 |

2025 |

|

Region |

North America |

38.2% |

2025 |

By Product and Services

Consumables command a 46.8% majority share in 2025, driven by the recurring consumption of reagents, assay kits, cell lines, microplates, and probes across pharmaceutical, biotechnology, and academic laboratories. These products form the operational backbone of daily assay workflows and generate steady repeat-purchase demand.

To access detailed market analysis, Request Sample

Instruments at 31.5% in 2025 reflect ongoing capital investments in flow cytometers, plate readers, high-content imagers, and automated liquid handling systems. Growing emphasis on high-throughput screening, workflow automation, and data accuracy is further supporting demand for advanced analytical instrumentation across research and clinical laboratories.

By Technology

High-throughput screening dominates with 32.6% share in 2025, reflecting its established role in large-scale compound library screening and dose-response profiling for drug discovery programs. The technology benefits from mature automation infrastructure and broad adoption across pharmaceutical and CRO settings.

Flow cytometry at 24.1% in 2025serves critical applications in immunology, oncology, and stem cell research. Advancements in multi-parameter analysis and spectral detection technologies are further expanding its role in complex cellular characterization and biomarker discovery.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

38.2% |

Strong biopharma R&D investment, favorable regulatory frameworks, advanced research infrastructure, and leading CRO presence |

|

Europe |

27.4% |

Established pharmaceutical industry clusters, supportive academic research funding, growing adoption of advanced screening technologies |

|

Asia-Pacific |

22.6% |

Expanding biotech sector, increasing government research funding, growing pharmaceutical outsourcing, and rapid CRO infrastructure development |

|

Latin America |

6.3% |

Growing pharmaceutical sector, expanding clinical trial activity, increasing academic research investment, and rising healthcare modernization |

|

Middle East & Africa |

5.5% |

Emerging research infrastructure, growing healthcare investment, expanding university-based research programs, and increasing international collaborations |

North America at 38.2% in 2025 leads the global market, supported by the concentration of major pharmaceutical and biotechnology companies, substantial NIH research funding, FDA regulatory guidance favoring Cell-Based testing, and a well-established network of contract research organizations. Deep institutional research infrastructure and industry-academia partnerships are further supporting sustained adoption.

Asia-Pacific at 22.6% is the highest-growth region through 2034. Strong government funding initiatives, rapid biotech sector expansion in China and India, and increasing pharmaceutical outsourcing activity are driving regional market acceleration.

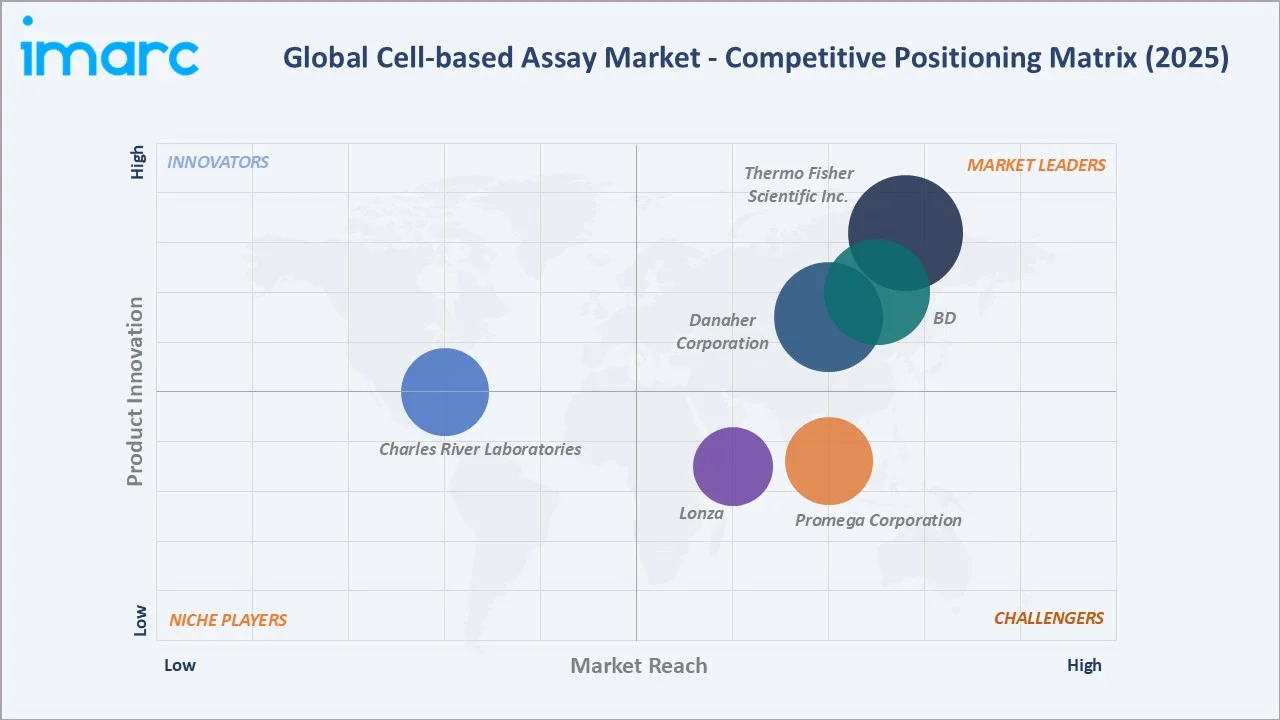

Competitive Landscape

The Cell-Based assay market is moderately fragmented, with established life science conglomerates dominating product breadth and distribution networks while specialized innovators serve niche technology and application segments. Portfolio depth, automation capabilities, and integrated service offerings form the key competitive differentiators.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Thermo Fisher Scientific Inc. |

Invitrogen, Gibco, Applied Biosystems |

Leader |

Broad portfolio spanning reagents, instruments, and services; global distribution network |

|

Danaher Corporation |

Beckman Coulter Life Sciences, Molecular Devices |

Leader |

Multi-brand strategy across flow cytometry, imaging, and screening platforms |

|

BD |

BD Biosciences, BD FACSDiscover |

Leader |

Spectral flow cytometry innovation; broad clinical and research applications |

|

Promega Corporation |

CellTiter-Glo Luminescent Cell Viability Assay, TarSeer BRETSA |

Challenger |

Bioluminescence-based assay leadership; live-cell target engagement platforms |

|

Lonza |

Cocoon Platform |

Challenger |

Cell therapy manufacturing and quality testing; automated platform solutions |

|

Charles River Laboratories |

Endosafe, Celsis |

Emerging |

Contract research and preclinical testing services; integrated assay solutions |

Key players include Thermo Fisher Scientific Inc., Danaher Corporation, BD, Promega Corporation, Lonza, and Charles River Laboratories, among others.

Key Company Profiles

Thermo Fisher Scientific Inc.

Thermo Fisher Scientific Inc. is the global leader in Cell-Based assay solutions, offering an integrated portfolio of reagents, instruments, software, and services through its Invitrogen and Applied Biosystems brands deployed across pharmaceutical, biotechnology, and academic laboratories worldwide.

- Product Portfolio: PrestoBlue and CyQUANT cell viability assay kits, Gibco cell culture media and reagents, and assay-ready tumoroids for cancer research.

- Recent Developments: In April 2025, the company announced plans to invest USD 2 Billion in United States innovation and manufacturing capabilities over four years, including USD 1.5 Billion in capital expenditures and USD 500 Million in R&D focused on high-impact innovation.

- Strategic Focus: Vertically integrated approach combining reagent supply, instrument manufacturing, and service delivery through global distribution and direct sales channels.

Danaher Corporation

Danaher Corporation is a diversified life sciences and diagnostics company providing advanced flow cytometry, imaging, and screening solutions for cell-based assay applications worldwide. The company continues to expand its presence through investments in automation, high-throughput technologies, and integrated analytical platforms supporting biomedical research and drug discovery workflows.

- Product Portfolio: CytoFLEX benchtop flow cytometers and ImageXpress Micro-Confocal high-content imaging system.

- Recent Developments: The company continues to strengthen its life sciences portfolio through ongoing investments in automation, spectral analysis capabilities, workflow integration, and next-generation analytical technologies supporting complex cellular research applications.

- Strategic Focus: Multi-brand portfolio strategy with deep specialization across flow cytometry, high-content imaging, and microplate-based screening technologies.

Promega Corporation

Promega Corporation is a multinational biotechnology company specializing in bioluminescence-based Cell-Based assay technologies, providing innovative solutions for drug discovery, target engagement, and cellular analysis across pharmaceutical and academic research settings.

- Product Portfolio: CellTiter-Glo luminescent cell viability assay and TarSeer BRETSA Target Engagement.

- Recent Developments: At SLAS 2026, the company introduced the TarSeer BRETSA Target Engagement system, a live-cell assay technology enabling researchers to measure compound binding directly inside intact cells for improved drug discovery workflows.

- Strategic Focus: Bioluminescence technology leadership with expanding live-cell target engagement platforms and strong academic research partnerships.

Market Concentration Analysis

The Cell-Based assay market is moderately concentrated, with the top six companies (Thermo Fisher Scientific Inc., Danaher Corporation, BD, Promega Corporation, Lonza, and Charles River Laboratories) estimated to hold approximately 55-65% of global revenue share in 2025.

Barriers to entry include extensive product validation and regulatory compliance requirements, multi-year customer relationship building, and the integrated platform capabilities needed for full-workflow solutions. These factors favor well-capitalized incumbents with deep reagent supply chains, established instrument portfolios, and global service networks.

Consolidation is accelerating through strategic acquisitions of niche assay developers, AI analytics platform integrations, and instrument-reagent-software bundling. Scale advantages in manufacturing, distribution, and technical support are further reinforcing the competitive position of established players across all major market segments.

Investment & Growth Opportunities

Fastest-Growing Segments

Software at 9.3% share is the fastest-growing product and services sub-segment through 2034, driven by AI-enabled analytics, automated image analysis, and laboratory information management platforms. Label-free detection at 14.3% is the fastest-growing technology category as real-time cellular monitoring applications expand across drug discovery and toxicology workflows.

Emerging Markets

Asia-Pacific at 22.6% is the highest-growth region, with China, India, Japan, and South Korea leading installations. China and India represent the largest untapped opportunities as expanding government research funding, growing biotech sectors, and increasing pharmaceutical outsourcing unlock mass-market adoption.

Venture & Investment Trends

Investment activity is concentrated in AI-powered screening platforms, 3D cell culture and organ-on-chip technologies, automated assay development services, and next-generation label-free detection systems. Capital is also flowing into cell therapy manufacturing platforms and companion diagnostic assay solutions that leverage Cell-Based testing methodologies.

Future Market Outlook (2026-2034)

The Cell-Based assay market is forecast to expand from USD 25.74 Billion in 2025 to USD 46.59 Billion by 2034 at a CAGR of 6.61%, adding roughly USD 20.85 Billion in incremental market value over the forecast period.

Four forces will shape the market through 2034: the regulatory mandate for human-relevant testing models replacing animal studies; AI and ML integration across screening and analysis workflows; the maturation of 3D culture and organ-on-chip platforms into mainstream drug development tools; and the expansion of Cell-Based assay applications into personalized medicine, cell therapy, and companion diagnostics.

By 2034, Cell-Based assays will be embedded as standard components across pharmaceutical development pipelines, serving as primary gatekeepers for compound progression from discovery through clinical development. Software and AI-integrated platforms are expected to capture an increasing share of total market value as data-driven decision-making becomes central to drug development.

Research Methodology

Primary Research

Primary research included interviews with senior product managers at leading assay manufacturers, pharmaceutical R&D executives, contract research organization leadership, academic core facility directors, and laboratory procurement specialists, validating market sizing, regional demand, technology adoption patterns, and competitive positioning.

Secondary Research

Secondary sources included NIH funding databases, FDA regulatory guidance documents, WHO Global Health Observatory data, peer-reviewed journals, industry association publications, company annual reports, investor presentations, and press releases from listed manufacturers and service providers.

Forecasting Models

Market forecasts used top-down and bottom-up models combining pharmaceutical R&D expenditure data, drug discovery pipeline analysis, technology adoption curves, regional research funding trends, and end-user demand modeling. Scenario analysis addressed instrument pricing variation and regulatory environment changes.

Cell-Based Assay Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product and Services Covered |

|

| Technologies Covered | Automated Handling, Flow Cytometry, Label-Free Detection, High-Throughput Screening, Others |

| Applications Covered | Drug Discovery, Basic Research, ADME Studies, Predictive Toxicology, Others |

| End-Users Covered | Pharmaceutical and Biotechnology Companies, Academic and Government Institutions, Contract Research Organizations, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Thermo Fisher Scientific Inc., Danaher Corporation, BD, Promega Corporation, Lonza, Charles River Laboratories, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the cell-based assay market from 2020-2034.

- The research report study provides the latest information on the market drivers, challenges, and opportunities in the global cell-based assay market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the cell-based assay industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Cell-based Assay Market Report

The global market was valued at USD 25.74 Billion in 2025, driven by rising drug discovery demand, advancing screening technologies, and supportive regulatory frameworks.

The market is projected to grow at 6.61% CAGR from 2026 to 2034, reaching USD 46.59 Billion, supported by AI integration and expanding personalized medicine applications.

Consumables lead at 46.8% in 2025, fueled by recurring demand for reagents, kits, and cell lines. Software at 9.3% is the fastest-growing sub-segment.

High-throughput screening dominates at 32.6% in 2025, supported by established automation infrastructure.

North America commands a 38.2% share in 2025, led by the United States, fueled by strong biopharma R&D investment and advanced research infrastructure. Asia-Pacific at 22.6% is the fastest-growing region.

Leading players include Thermo Fisher Scientific Inc., Danaher Corporation, BD, Promega Corporation, Lonza, and Charles River Laboratories.

Regulatory mandates, ethical considerations, improved predictive accuracy, and cost efficiency are accelerating the adoption of Cell-Based models over traditional animal studies.

AI integration enables automated image analysis, phenotypic classification, predictive compound modeling, and workflow optimization, reducing screening timelines and improving decision accuracy.

Three-dimensional models, such as organoids and spheroids, provide physiologically relevant testing environments, improving drug screening accuracy and reducing late-stage clinical failures.

High instrument costs, protocol standardization gaps, complex assay design requirements, and skilled personnel shortages remain the primary challenges across the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade