Cell Dissociation Market Size, Share, Trends and Forecast by Product, Type, End Use, and Region, 2026-2034

Global Cell Dissociation Market Size, Share, Trends & Forecast (2026-2034)

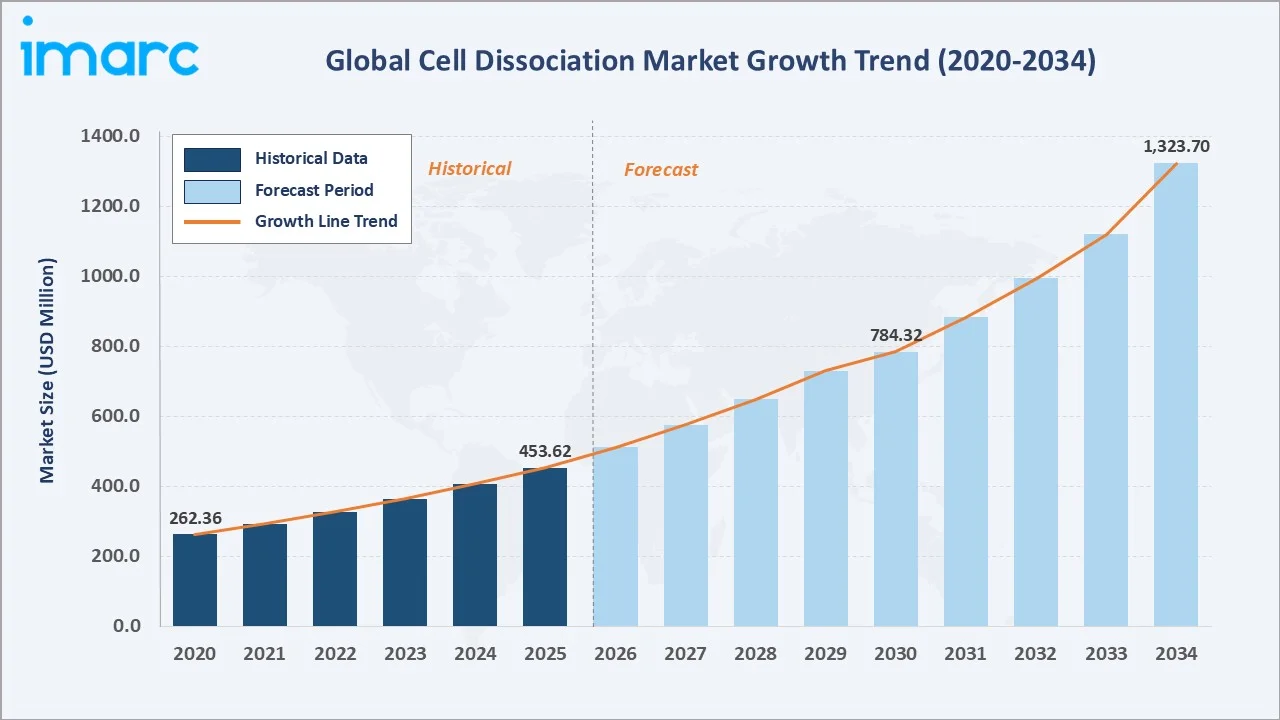

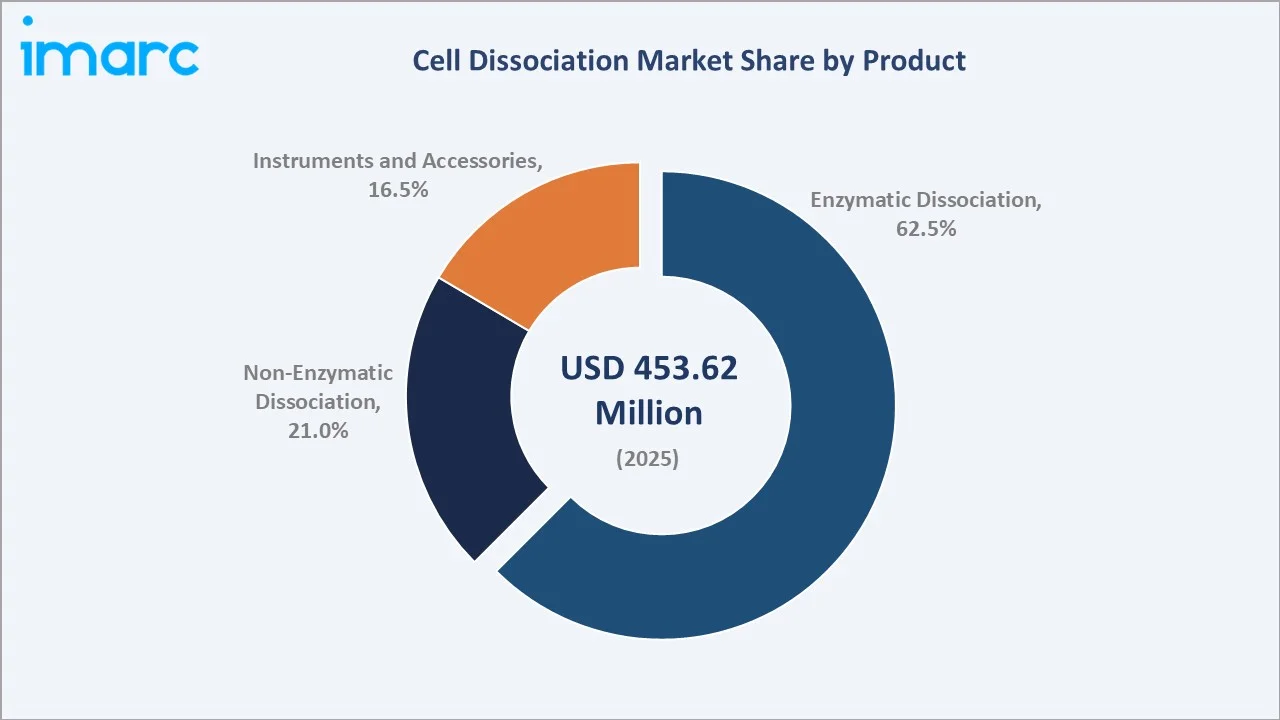

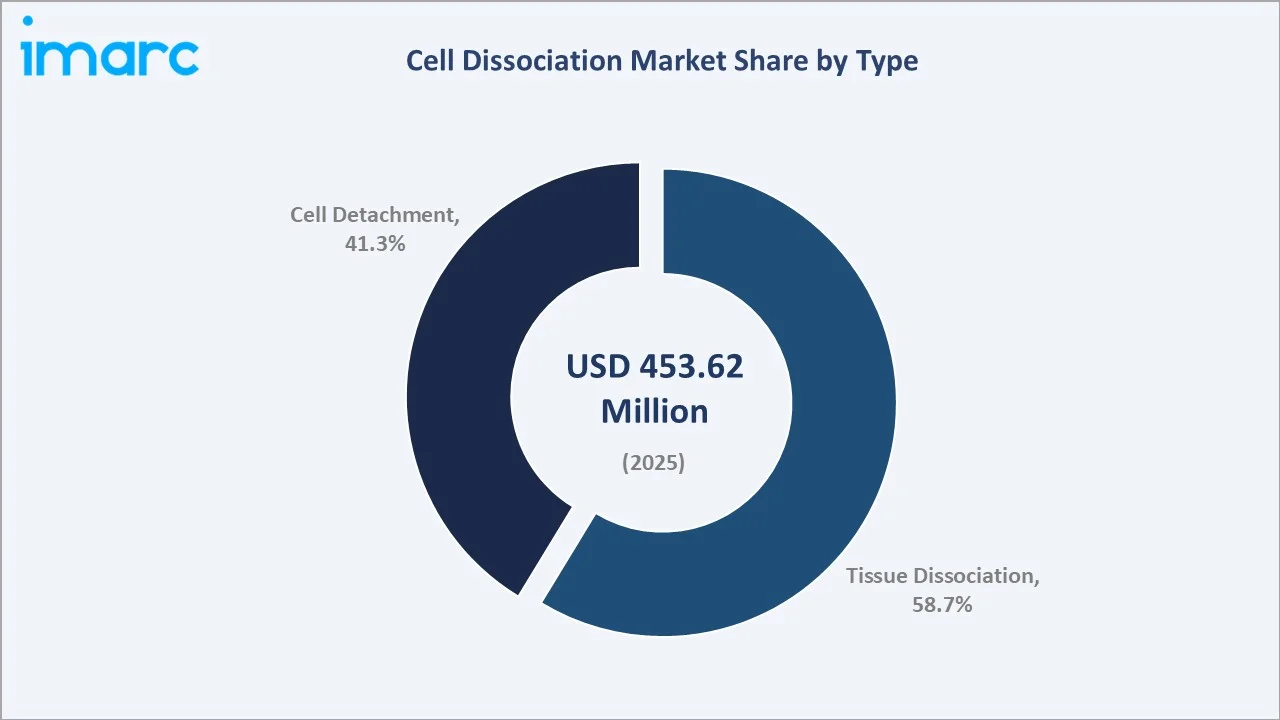

The global cell dissociation market size was valued at USD 453.62 Million in 2025 and is projected to reach USD 1,323.70 Million by 2034, exhibiting a CAGR of 11.57% during 2026-2034. Rising biopharmaceutical R&D investment, growing cell and gene therapy adoption, and expanding single-cell genomics research are fuelling cell dissociation market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 453.62 Million |

|

Forecast Market Size (2034) |

USD 1,323.70 Million |

|

CAGR (2026-2034) |

11.57% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

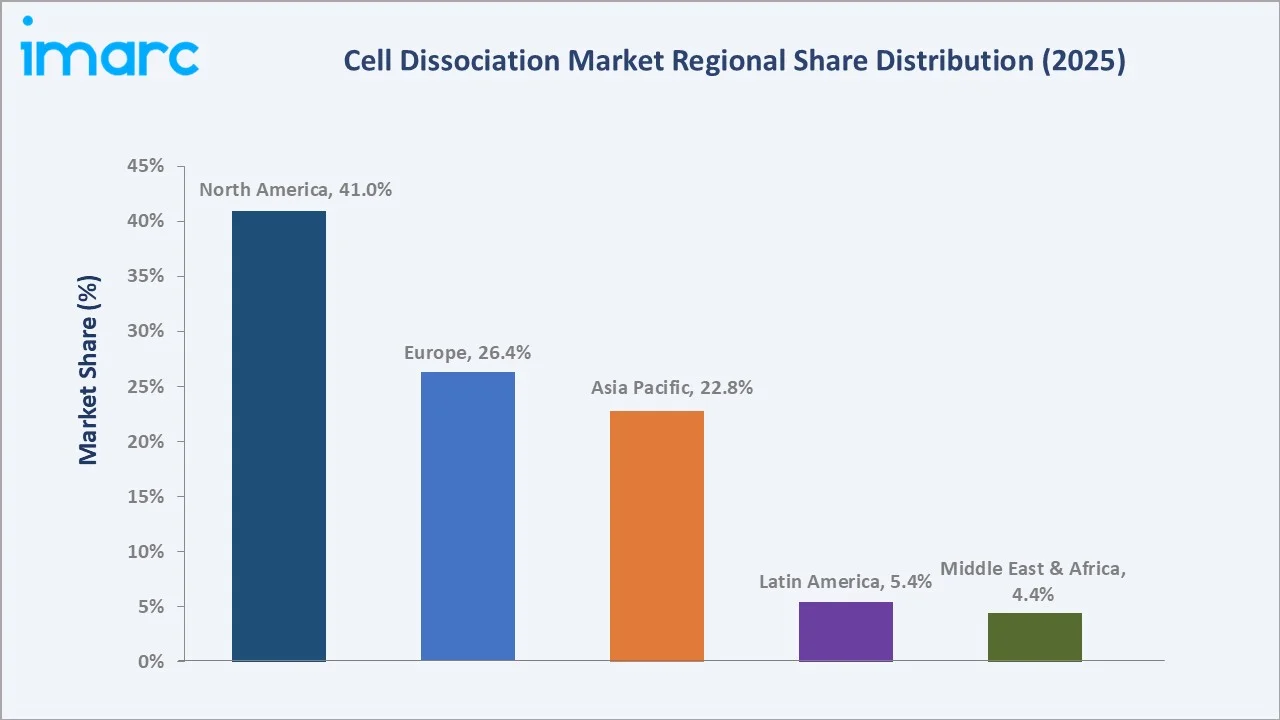

North America (41.0% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

|

Leading Product |

Enzymatic Dissociation (62.5%, 2025) |

|

Leading Type |

Tissue Dissociation (58.7%, 2025) |

The chart below illustrates the global cell dissociation market growth trajectory from 2020 through 2034, contrasting historical expansion with a sustained forecast curve powered by cell therapy adoption, oncology research, and bioproduction scale-up across pharmaceutical and academic end users.

To get more information on this market, Request Sample

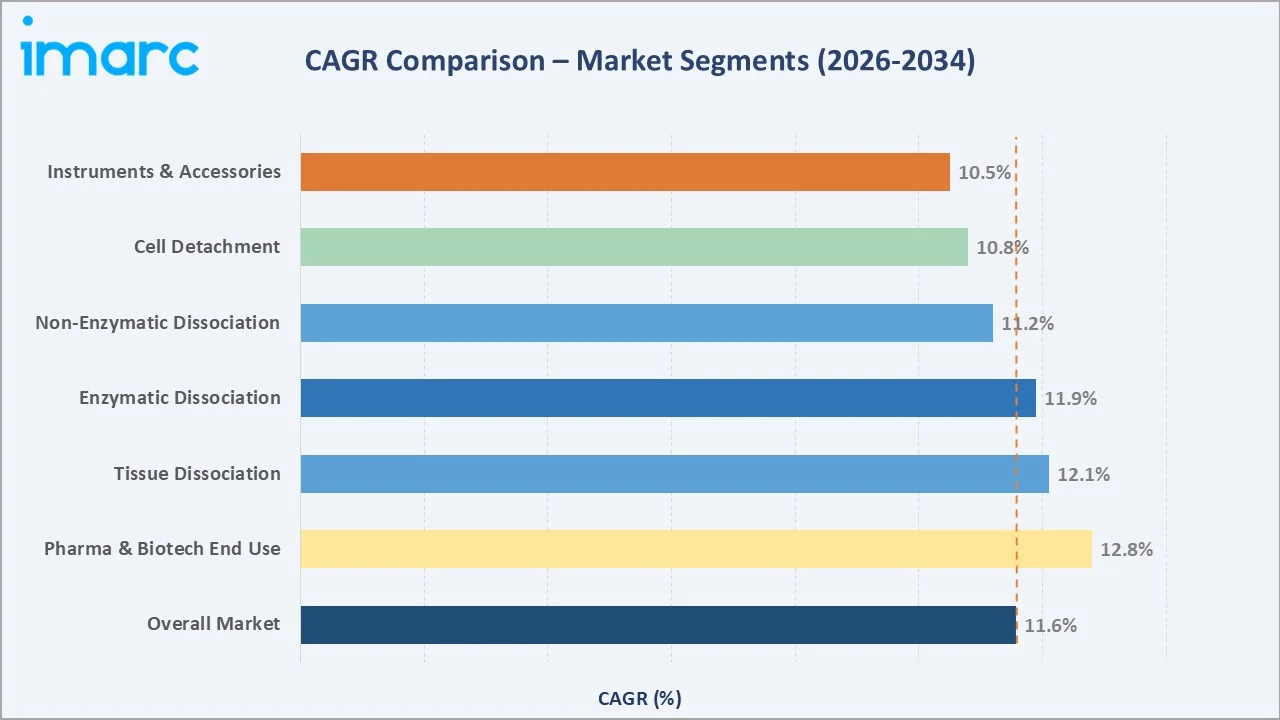

Segment-level CAGR comparisons below highlight tissue dissociation and enzymatic dissociation as the fastest-growing sub-categories within the global cell dissociation market forecast through 2034, both surpassing the 11.57% overall market CAGR.

Executive Summary

The global cell dissociation market is undergoing robust transformation driven by exponential growth in biopharmaceutical R&D, cell and gene therapy pipelines, and high-throughput single-cell analysis workflows. Valued at USD 453.62 Million in 2025, the market is forecast to reach USD 1,323.70 Million by 2034 at a CAGR of 11.57%.

Enzymatic dissociation commands 62.5% product share in 2025, underpinned by trypsin, collagenase, and dispase enzymes that remain the gold standard for primary cell isolation. Non-enzymatic approaches hold 21.0%, gaining traction in stem cell and organoid research settings requiring gentle dissociation without proteolytic damage. Instruments and accessories represent 16.5%, with automated tissue dissociators and gentleMACS platforms expanding lab throughput across academic and industrial environments.

Tissue dissociation leads type segmentation at 58.7% share (2025), reflecting demand from oncology, immunology, and primary cell culture workflows. North America dominates with 41.0% global share, anchored by NIH-funded research, FDA-approved CAR-T therapies, and leading life science instrument manufacturers.

Key Market Insights

|

Insight |

Data |

|

Largest Product |

Enzymatic Dissociation – 62.5% share (2025) |

|

Second Product |

Non-Enzymatic Dissociation – 21.0% share (2025) |

|

Largest Type |

Tissue Dissociation – 58.7% share (2025) |

|

Fastest Growing Type |

Cell Detachment – ~10.8% CAGR (2026-2034) |

|

Leading Region |

North America – 41.0% revenue share (2025) |

|

Top Companies |

Thermo Fisher Scientific Inc., BD, F. Hoffmann-La Roche Ltd., Sartorius AG, Cytiva, Miltenyi Biotec, STEMCELL Technologies, Capricorn Scientific, PAN-Biotech, Vitacyte LLC |

|

Market Opportunity |

CAR-T and stem cell therapy pipelines driving premium reagent demand through 2034 |

Key Analytical Observations Supporting The Above Data:

- Enzymatic dissociation's 62.5% dominance in 2025 reflects the indispensable role of trypsin and collagenase in primary tissue processing for oncology drug discovery, immunology, and CAR-T cell manufacturing workflows globally.

- Non-enzymatic dissociation at 21.0% share is gaining momentum in sensitive applications such as iPSC passaging, organoid culture, and single-cell sequencing where traditional enzymatic agents risk receptor cleavage and surface antigen loss.

- Tissue dissociation's 58.7% type dominance is driven by surging demand for patient-derived tumor models, primary immune cell isolation for immuno-oncology research, and tissue biobanking initiatives across North America and Europe in 2025.

- North America holds 41.0% global revenue supported by NIH funding exceeding USD 47 Billion in 2024, the U.S. FDA’s accelerated approval of cell and gene therapies, and the dense concentration of biopharmaceutical R&D hubs in Boston, San Francisco, and Research Triangle Park.

- Asia Pacific is the fastest-growing region, advancing at an estimated CAGR of ~13.5% through 2034, driven by China’s biopharmaceutical manufacturing push, South Korea’s cell therapy approvals, and India’s expanding contract research ecosystem.

Global Cell Dissociation Market Overview

Cell dissociation refers to the controlled separation of cells from tissues or culture substrates using enzymatic, mechanical, or chemical means. The global cell dissociation market encompasses enzymatic reagents such as trypsin, collagenase, and dispase; non-enzymatic solutions including EDTA-based buffers and chelating agents; and instruments ranging from tissue dissociators to cell strainers and dissociation kits.

The industry operates at the intersection of life science research, clinical biotechnology, and biopharmaceutical manufacturing. Growth is supported by macroeconomic drivers including increasing global healthcare R&D spending, rising government investment in genomics and precision medicine, and the rapid expansion of GMP-compliant cell therapy manufacturing facilities worldwide.

Market Dynamics

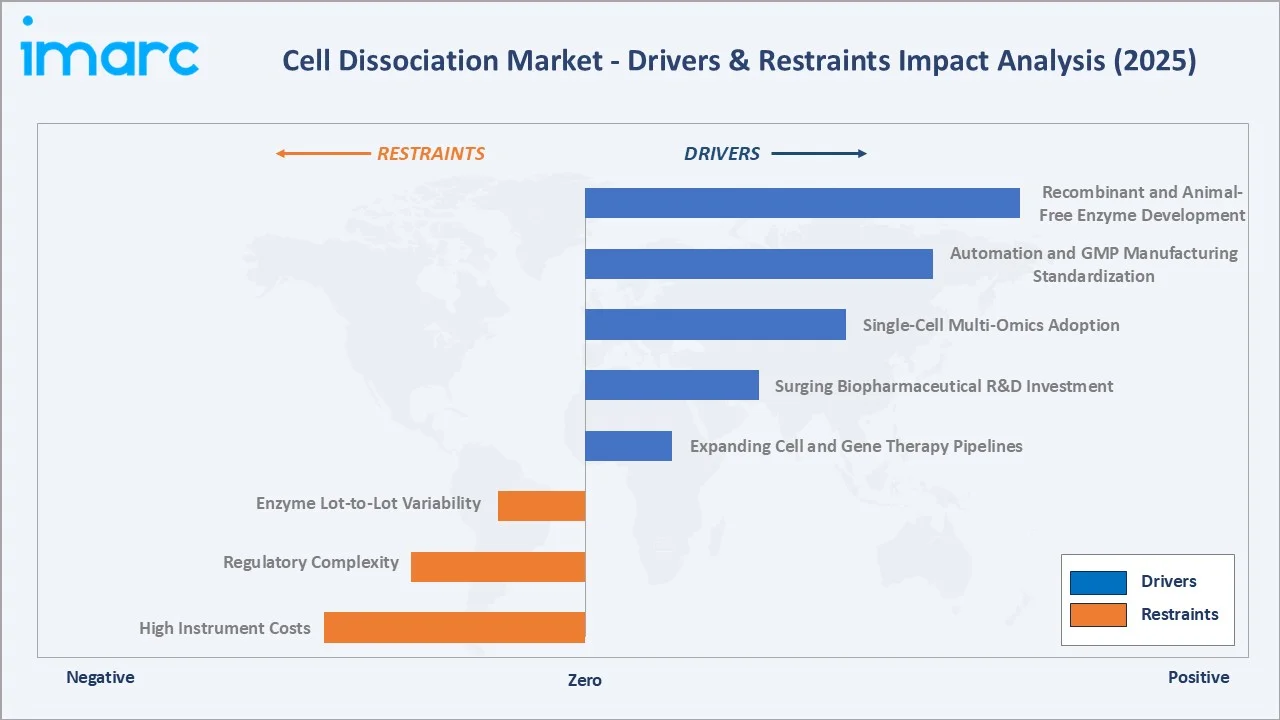

The figure below captures the relative impact weight of key drivers and restraints shaping the global cell dissociation market in 2025, reflecting survey inputs from industry stakeholders across biopharmaceutical R&D, academic research, and clinical manufacturing.

To evaluate market opportunities, Request Sample

Market Drivers

- Expanding Cell and Gene Therapy Pipelines: The global CAR-T, NK cell, and TCR-T therapy pipeline has grown to include over a thousand active clinical trials, each requiring scalable and reproducible cell dissociation at multiple manufacturing steps, which is driving significant demand for reagents and instruments in the industry.

- Surging Biopharmaceutical R&D Investment: The top 50 pharmaceutical companies alone are estimated to have spent a total of USD 167 billion in R&D in 2022. Increasing focus on oncology biologics, mRNA therapeutics, and personalized medicine is expanding the use of primary cell models.

- Single-Cell Multi-Omics Adoption: Single-cell RNA sequencing workflows, now widely adopted across major academic research institutions globally, require high-viability single-cell suspensions. This need directly drives demand for premium enzymatic dissociation products, representing a significant portion of industry demand.

- Automation and GMP Manufacturing Standardization: GMP-grade cell therapy manufacturing is increasingly automated, with platforms that enable reproducible, operator-independent tissue processing. This represents the most influential market driver, reflecting a structural shift toward closed-system bioprocessing.

Market Restraints

- High Instrument Costs: Automated tissue dissociation systems are high-cost, which can limit adoption in price-sensitive emerging markets and resource-constrained academic laboratories, representing a notable market restraint.

- Regulatory Complexity: Regulations such as FDA 21 CFR Part 1271 and EMA ATMP guidelines mandate extensive validated documentation for every dissociation reagent used in cell therapy manufacturing, creating significant compliance cost barriers and acting as a major market restraint.

- Enzyme Lot-to-Lot Variability: Variability in animal-derived enzymes, such as collagenase, can cause inconsistencies in cell yield and viability, leading to costly protocol re-validation and supplier changes, representing a significant market restraint.

- Supply Chain Fragility: Enzymes sourced from porcine, bovine, or microbial origins are vulnerable to supply disruptions due to biosafety regulations and geopolitical trade restrictions, representing the most significant market restraint.

Market Opportunities

- Recombinant and Animal-Free Enzyme Development: Rising demand for xeno-free and GMP-compliant cell therapy manufacturing is driving the development of recombinant trypsin, animal-component-free collagenase blends, and synthetic dissociation buffers. This premium segment is projected to grow at robust rates through 2030.

- Organoid and 3D Cell Culture Expansion: The global organoid market is projected to experience significant growth in the coming years. Organoid workflows require specialized, gentle dissociation protocols, creating new product development opportunities for reagent manufacturers offering validated kits.

- Emerging Market Penetration: China's biopharmaceutical sector (Chinese biopharma is responsible for about 70% of the global development of antibody drug conjugates), and India’s expanding CRO ecosystem are creating high-volume procurement opportunities for cost-competitive enzymatic dissociation reagents and standardized kits through 2034.

Market Challenges

- Ethical Constraints on Animal-Derived Components: Increasing pressure to eliminate animal-derived enzymes from manufacturing workflows requires costly reformulation and re-validation cycles, particularly for established products with long regulatory histories and existing customer bases.

- Distribution Channel Fragmentation: Serving both specialty research channels and direct-to-consumer online platforms requires differentiated documentation, cold-chain fulfilment, and pricing strategies that strain operational resources for manufacturers lacking digital commerce infrastructure.

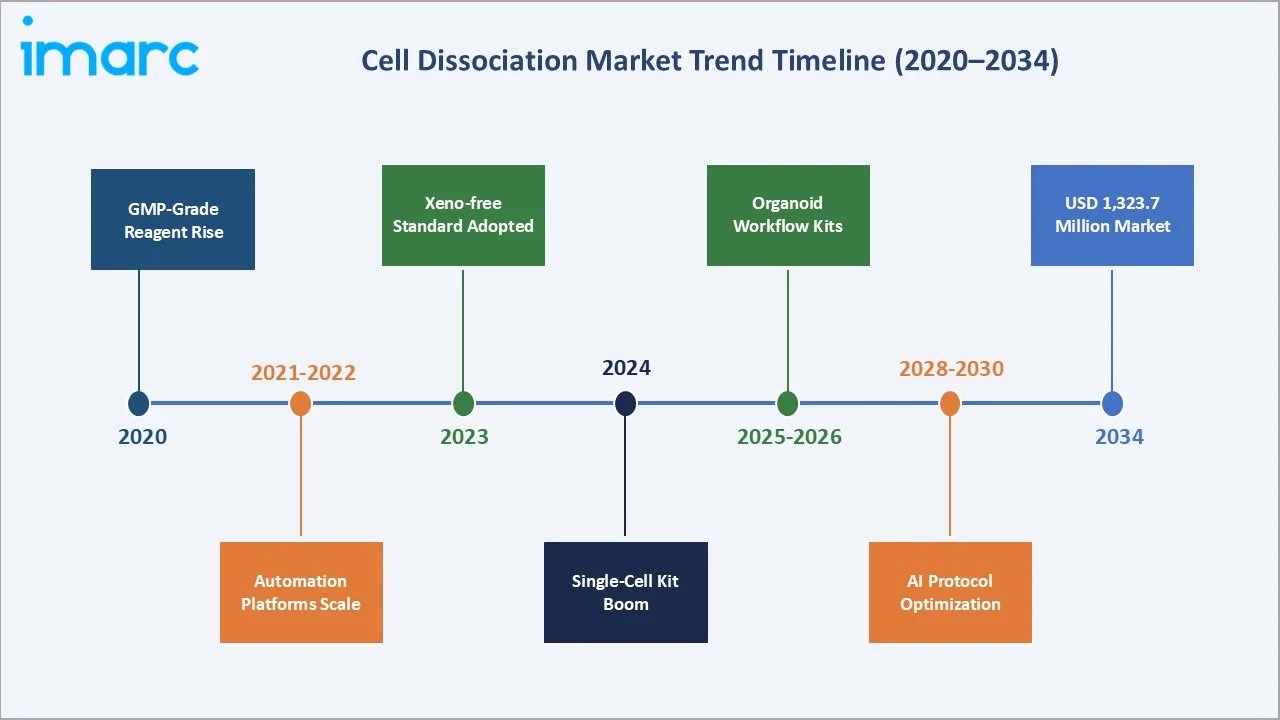

Emerging Market Trends

The timeline below maps key inflection points in cell dissociation market trends, highlighting the progression from early GMP reagent standardization to AI-assisted protocol optimization and major market growth milestones.

1. Rise of GMP-Grade and Xeno-Free Dissociation Reagents

Regulatory pressure and clinical manufacturing standards are driving rapid adoption of GMP-certified, animal-component-free (ACF) dissociation reagents. Products such as TrypLE (Thermo Fisher) and Accutase are replacing traditional porcine trypsin in stem cell and CAR-T manufacturing workflows.

2. Automation and Intelligent Tissue Processing

Automated tissue dissociation platforms are transitioning from research to clinical-grade manufacturing. Systems integrating mechanical and enzymatic dissociation with real-time viability monitoring are enabling standardized, operator-independent workflows.

3. Single-Cell Analysis Driving Premium Reagent Demand

The exponential growth of 10x Genomics Chromium and similar scRNA-seq platforms requires highly viable, non-clumped single-cell suspensions. Cold-active proteases and optimized dissociation kits tailored for single-cell workflows represent one of the fastest-growing product niches, with demand tied directly to sequencing instrument installed base expansion.

4. Organoid and Tumoroid Workflow Specialization

Patient-derived tumor organoid (PDO) models are emerging as the preferred preclinical screening platform for oncology drug discovery. These workflows require tailored enzymatic cocktails, with market leaders launching organoid-specific dissociation kits over standard reagents to capture this high-value segment.

5. AI Protocol Optimization and Closed-System Processing

AI-driven reagent selection platforms and smart dissociation instruments with feedback control loops are emerging to optimize enzyme concentration, incubation time, and mechanical agitation parameters in real time. GMP-compliant closed-system tissue processing bags are enabling contamination-free primary cell isolation, converging cell dissociation with downstream bioreactor workflows by 2028–2030.

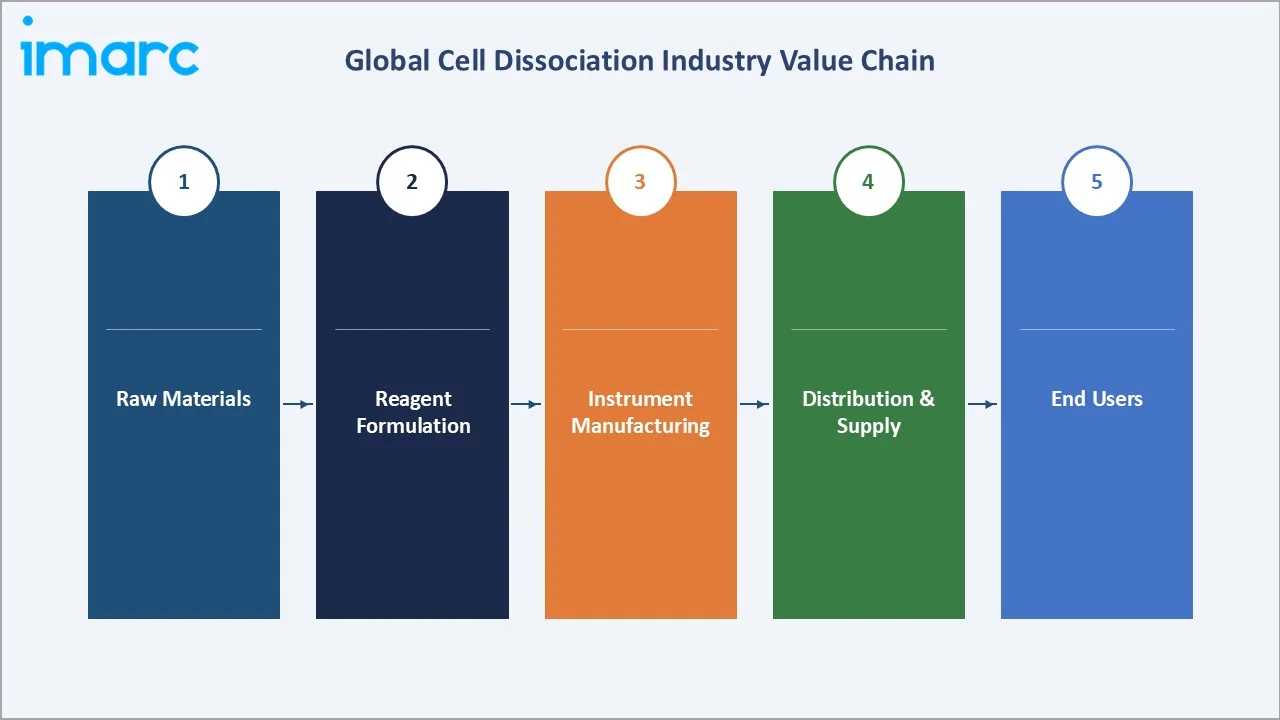

Industry Value Chain Analysis

The global cell dissociation industry value chain spans five integrated stages from raw biological material supply through end-user application. Each stage presents distinct competitive dynamics, regulatory requirements, and margin profiles relevant to overall cell dissociation market analysis.

|

Stage |

Key Activities |

|

Raw Materials |

Biological enzyme extraction (porcine pancreas, microbial fermentation), recombinant protein production, chelating agent synthesis |

|

Reagent Formulation |

Enzymatic blend development, quality control, lyophilization, sterile filtration, ACF formulation |

|

Instrument Manufacturing |

Tissue dissociator design, microfluidic chip production, cell strainer manufacturing, automation integration |

|

Distribution & Supply Chain |

Cold chain logistics, regulatory documentation, regional distributor networks, e-commerce fulfilment |

|

End Users |

Primary cell isolation, cell therapy manufacturing, scRNA-seq sample prep, organoid culture, drug discovery assays |

The diagram below illustrates the linear flow of the cell dissociation value chain, from raw material sourcing through reagent formulation, instrument manufacturing, distribution, and final end-user application in research and clinical manufacturing settings.

Technology Landscape in the Cell Dissociation Industry

Enzymatic Technology Innovation

Advances in recombinant enzyme engineering are yielding highly specific, lot-consistent collagenase blends and recombinant trypsin variants. Cold-active proteases capable of gentle dissociation at low temperatures are emerging commercially, enabling low-stress single-cell preparation. Specialized thermolysin-collagenase combination kits for islet cell isolation represent a notable specialty sub-segment in the market.

Automation and Microfluidics

Microfluidic chip-based dissociation platforms are advancing standardized sample preparation for single-cell sequencing. Integrated devices that combine tissue mincing, enzyme incubation, filtration, and viability assessment into single closed-system workflows are significantly reducing hands-on time compared with manual protocols, enabling higher throughput in clinical manufacturing settings.

Digital and AI-Assisted Protocol Optimization

AI-driven reagent selection platforms and smart dissociation instruments with feedback control loops are emerging to optimize enzyme concentration, incubation time, and mechanical agitation parameters in real time. These systems improve cell yield consistency and reduce protocol development timelines, addressing a critical pain point for cell therapy developers scaling from research to clinical manufacturing in 2025.

GMP and Closed-System Processing

GMP-compliant, closed-system tissue processing bags and automated dissociation consumables are enabling contamination-free primary cell isolation for clinical applications. Sartorius AG and Cytiva (Danaher) are integrating cell dissociation modules into their broader bioprocessing single-use system portfolios, supporting the convergence of upstream cell isolation and downstream bioreactor workflows.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Enzymatic Dissociation |

62.5% |

2025 |

|

Type |

Tissue Dissociation |

58.7% |

2025 |

|

End Use |

Pharmaceutical and Biotechnology Companies |

🔒 |

2025 |

|

Region |

North America |

41.0% |

2025 |

By Product

Enzymatic Dissociation dominates with 62.5% revenue share in 2025. Trypsin, collagenase, dispase, and papain remain the foundational tools for primary tissue processing, organoid generation, and cell therapy manufacturing. The sub-segment is benefiting from growing adoption of recombinant, animal-component-free formulations priced at significant premiums over conventional options.

To access detailed market analysis, Request Sample

By Type

Tissue Dissociation leads type segmentation at 58.7% share in 2025. Demand is driven by patient-derived tumor model development for precision oncology, primary cell isolation for immunology research, and biobanking programs requiring reproducible tissue-to-cell conversion protocols.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

41.0% |

NIH R&D funding, FDA CAR-T approvals, biopharmaceutical R&D hubs, academic research density |

|

Europe |

26.4% |

EU Horizon Europe funding, ATMP regulatory framework, strong biopharma presence in UK/Germany/Switzerland |

|

Asia Pacific |

22.8% |

China biopharma manufacturing scale-up, South Korea cell therapy approvals, India CRO expansion |

|

Latin America |

5.4% |

Brazil/Mexico biotech growth, academic research expansion, growing pharma outsourcing |

|

Middle East & Africa |

4.4% |

UAE/Saudi Arabia life science investment, academic infrastructure development, growing diagnostic demand |

North America commands 41.0% global revenue share in 2025. The U.S. remains the world’s largest cell dissociation market, driven by NIH funding exceeding USD 47 Billion in FY2024, the FDA’s approval of six CAR-T cell therapies by 2025, and the concentration of biopharma R&D sites along the Boston-Cambridge and San Francisco Bay Area corridors.

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Thermo Fisher Scientific Inc. |

TrypLE, Gibco, StemPro Accutase |

Leader |

Broadest product portfolio, global distribution, GMP-grade reagents |

|

BD |

BD Biosciences, BD IMag |

Leader |

Flow cytometry integration, cell processing instruments |

|

F. Hoffmann-La Roche Ltd. |

Roche Diagnostics |

Leader |

Tissue biobanking, oncology-focused dissociation kits |

|

Sartorius AG |

Ambr Multi-Parallel Bioreactors |

Challenger |

GMP bioprocessing integration, single-use systems |

|

Cytiva |

WAVE Bioreactor system |

Challenger |

Bioprocess automation, closed-system cell isolation |

|

Miltenyi Biotec |

gentleMACS Dissociator |

Challenger |

Automated tissue dissociation leadership, CAR-T workflows |

|

STEMCELL Technologies |

EasySep |

Emerging |

Specialty stem cell and organoid dissociation kits |

|

Capricorn Scientific |

Capricorn Scientific |

Niche |

European specialty reagents, academic focus |

|

PAN-Biotech |

PAN-Biotech |

Niche |

European GMP-grade cell culture solutions |

|

Vitacyte LLC |

VitaCyte |

Niche |

Islet isolation enzyme specialist |

The global cell dissociation market competitive landscape is moderately concentrated, with Thermo Fisher Scientific Inc., BD, F. Hoffmann-La Roche Ltd., Sartorius AG, Cytiva, Miltenyi Biotec, STEMCELL Technologies, Capricorn Scientific, PAN-Biotech, and Vitacyte LLC.

Key Company Profiles

Thermo Fisher Scientific Inc.

Thermo Fisher Scientific Inc. is a leading global provider of scientific instruments, reagents, consumables, and laboratory services that support research, clinical diagnostics, and biopharmaceutical manufacturing. Headquartered in Waltham, Massachusetts, the company operates worldwide with a broad portfolio spanning analytical instruments, life sciences solutions, specialty diagnostics, and laboratory products and services.

- Product Portfolio: Key cell dissociation offerings include TrypLE Express (recombinant trypsin substitute), Accutase Cell Detachment Solution, Gibco collagenase formulations, and a comprehensive range of Invitrogen-branded tissue dissociation kits optimized for specific tissue types including tumor, liver, and cardiac tissue.

- Recent Developments: In 2026, Thermo Fisher Scientific announced the global launch of the Gibco CTS Compleo Fill and Finish System, an automated, functionally closed solution designed to streamline formulation and filling in cell therapy manufacturing.

- Strategic Focus: Strategy centers on GMP reagent standardization, integrated bioprocessing solutions, and digital lab ecosystem development to support cell therapy manufacturers from bench to clinic.

BD

Becton, Dickinson and Company is a U.S.–based multinational medical technology company that develops, manufactures, and sells a broad range of medical devices, instrument systems, and laboratory equipment. Founded in 1897 and headquartered in Franklin Lakes, New Jersey, BD operates through key segments including BD Medical, BD Life Sciences, and BD Interventional.

- Product Portfolio: BD’s cell dissociation portfolio includes BD IMag cell separation systems, BD Rhapsody single-cell analysis platforms requiring validated dissociation inputs, and BD Horizon-branded reagents supporting downstream flow cytometry workflows.

- Recent Developments: In 2023, BD has introduced the BD FACSDiscover S8 Cell Sorter, featuring BD CellView Image Technology and BD SpectralFX Technology. The platform enables high-speed, image-based cell sorting and full-spectrum analysis, expanding capabilities for single-cell research.

- Strategic Focus: BD’s strategy integrates cell dissociation workflow optimization with its downstream flow cytometry and single-cell analysis instrumentation ecosystem, targeting pharmaceutical QC and academic immunology as priority segments.

Miltenyi Biotec

Miltenyi Biotec is a privately held German life science company headquartered in Bergisch Gladbach, Germany, specializing in cell separation, cell therapy manufacturing, and tissue dissociation technologies across 70 countries.

- Product Portfolio: Miltenyi’s flagship dissociation product line includes the gentleMACS Octo Dissociator, gentleMACS C Tubes, and a comprehensive library of tissue-specific dissociation kits covering human tumor, mouse brain, liver, lung, kidney, and spleen tissues, with specialized programs for CAR-T and TIL manufacturing.

- Recent Developments: In 2024, Miltenyi Biotec has launched its first office in India and will establish a Centre of Excellence (CoE). The CoE will provide scientists, researchers, and clinicians with classroom and hands-on training in cell and gene therapy, covering workflows from proof of concept to pre-clinical and clinical development, as well as commercialization.

- Strategic Focus: Miltenyi’s strategy focuses on end-to-end cell therapy manufacturing workflow integration, combining automated tissue dissociation with magnetic cell separation, expansion, and quality control into standardized closed-system GMP platforms.

Market Concentration Analysis

The global cell dissociation market exhibits moderate concentration. The top five players – Thermo Fisher Scientific Inc., BD, F. Hoffmann-La Roche Ltd., Sartorius AG, Cytiva – collectively account for an estimated 35–42% of global reagent and instrument revenue in 2025.

The market is experiencing a bifurcated dynamic. At the premium GMP and clinical-grade tier, consolidation is occurring around GMP certification, regulatory validation packages, and integrated workflow solutions. Simultaneously, cost-competitive Asian manufacturers are scaling catalog reagent production and entering international markets through e-commerce channels and CRO partnerships, intensifying price competition in the research-grade segment through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

GMP-grade and xeno-free enzymatic reagents are the highest-growth product sub-segment, expanding at estimated CAGRs exceeding 15% through 2030. Automated tissue dissociation instruments for clinical manufacturing represent the premium instrument opportunity. Single-cell analysis sample preparation kits are expanding in parallel with scRNA-seq instrument installed base growth.

Emerging Market Expansion

Asia Pacific represents a high-potential emerging opportunity, with China’s National Biotechnology Development Strategy driving investment in domestic biopharma and cell therapy infrastructure. India’s expanding contract research and manufacturing ecosystem provides a significant procurement channel for standardized dissociation reagents, serving both domestic and multinational clients.

Strategic Investment Trends

Strategic M&A is reshaping the competitive landscape. Danaher Corporation’s acquisition of Cytiva and integration of cell processing tools into its bioprocessing portfolio exemplifies the platform consolidation trend. Investment in AI-assisted protocol optimization tools, recombinant enzyme development, and single-use closed-system dissociation instruments are the primary focus areas for venture and corporate capital in the cell dissociation space through 2034.

Future Market Outlook (2026-2034)

The global cell dissociation market forecast projects sustained value expansion from USD 453.62 Million in 2025 to USD 1,323.70 Million by 2034 at a CAGR of 11.57%. North America will retain leadership, while Asia Pacific is forecast to close the gap meaningfully by 2030, driven by China and South Korea’s cell therapy commercialization programs.

Three structural shifts will define the market through 2034. First, GMP standardization will progressively bifurcate the market into premium clinical-grade and commodity research-grade tiers, with margin expansion concentrated in validated, certified product lines.

Second, automation convergence will embed cell dissociation as an integrated module within closed-system cell therapy manufacturing platforms. Third, precision workflow development will drive demand for tissue- and indication-specific dissociation kits as CAR-T, TIL, NK cell, and stem cell therapies each require uniquely optimized dissociation parameters to meet regulatory viability and identity standards.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024–2025 with cell dissociation market stakeholders, including reagent development scientists at major life science companies, cell therapy manufacturing managers at biopharmaceutical firms, procurement directors at academic research institutions, and clinical development leaders at ATMP-focused biotech companies. Primary insights validated market sizing, segmentation estimates, and technology adoption timelines.

Secondary Research

Secondary sources include NIH funding databases, FDA regulatory filings for cell and gene therapy approvals, Alliance for Regenerative Medicine (ARM) pipeline reports, EU Horizon Europe program documentation, Pharmexcil CRO industry data, company annual reports, and trade publications including BioProcess International, Cell & Gene Therapy Insights, and Lab Manager Magazine.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating biopharma R&D expenditure growth rates, clinical trial pipeline volume, instrument installed base expansion, and historical reagent consumption patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for regulatory and pipeline-related uncertainty.

Cell Dissociation Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Products Covered |

|

| Types Covered | Tissue Dissociation, Cell Detachment |

| End Uses Covered | Pharmaceutical and Biotechnology Companies, Research and Academic Institutes |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Thermo Fisher Scientific Inc., BD, F. Hoffmann-La Roche Ltd., Sartorius AG, Cytiva, Miltenyi Biotec, STEMCELL Technologies, Capricorn Scientific, PAN-Biotech, Vitacyte LLC, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the cell dissociation market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global cell dissociation market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the cell dissociation industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Cell Dissociation Market Report

The global cell dissociation market was valued at USD 453.62 Million in 2025, driven by expanding biopharmaceutical R&D, growing CAR-T cell therapy manufacturing, and rising single-cell genomics research globally.

The market is projected to reach USD 1,323.70 Million by 2034, growing at a CAGR of 11.57% during 2026-2034, supported by cell therapy pipeline expansion, automation adoption, and precision medicine investment.

Enzymatic dissociation leads with a 62.5% share in 2025, driven by the indispensable role of trypsin, collagenase, and dispase in primary cell isolation, CAR-T manufacturing, and organoid generation workflows.

Tissue dissociation leads type segmentation at 58.7% in 2025, reflecting demand for patient-derived tumor models, primary immune cell isolation, and biobanking applications across oncology and immunology research.

North America dominates with 41.0% share in 2025, anchored by NIH research funding exceeding USD 47 Billion, FDA-approved CAR-T therapies, and the high density of biopharma R&D infrastructure across major U.S. biotech hubs.

Key drivers include expanding cell and gene therapy pipelines, biopharmaceutical R&D investment growth, single-cell multi-omics adoption, GMP manufacturing standardization, and automation integration in clinical cell therapy workflows.

Major players include Thermo Fisher Scientific Inc., BD, F. Hoffmann-La Roche Ltd., Sartorius AG, Cytiva, Miltenyi Biotec, STEMCELL Technologies, Capricorn Scientific, PAN-Biotech, and Vitacyte LLC.

Asia Pacific is the fastest-growing region, expanding at an estimated CAGR of ~13.5% through 2034, driven by China's biopharma manufacturing investment, South Korea's cell therapy approvals, and India's expanding CRO and research infrastructure.

Key opportunities include GMP-grade xeno-free reagent development, automated tissue processing platforms for CAR-T manufacturing, organoid workflow-specific kits, and Asia Pacific geographic expansion through local distribution and CRO partnerships.

Non-enzymatic dissociation growth is driven by iPSC culture, organoid workflows, and receptor-binding assay applications where proteolytic enzyme activity risks compromising surface antigen integrity and downstream experimental outcomes.

Automation is a major growth driver, enabling standardized, operator-independent tissue processing for clinical manufacturing. Automated platforms significantly reduce protocol variability, supporting GMP compliance and ensuring reproducibility at clinical scale.

FDA 21 CFR Part 1271, and EMA ATMP regulations and guidelines mandate validated, documented dissociation protocols for cell therapy manufacturing, driving demand for certified GMP-grade reagents and vendor-supported validation packages.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)