Cement Market Size, Share, Trends and Forecast by Type, End Use, and Region, 2026-2034

Cement Market Size, Share, Trends & Forecast (2026-2034)

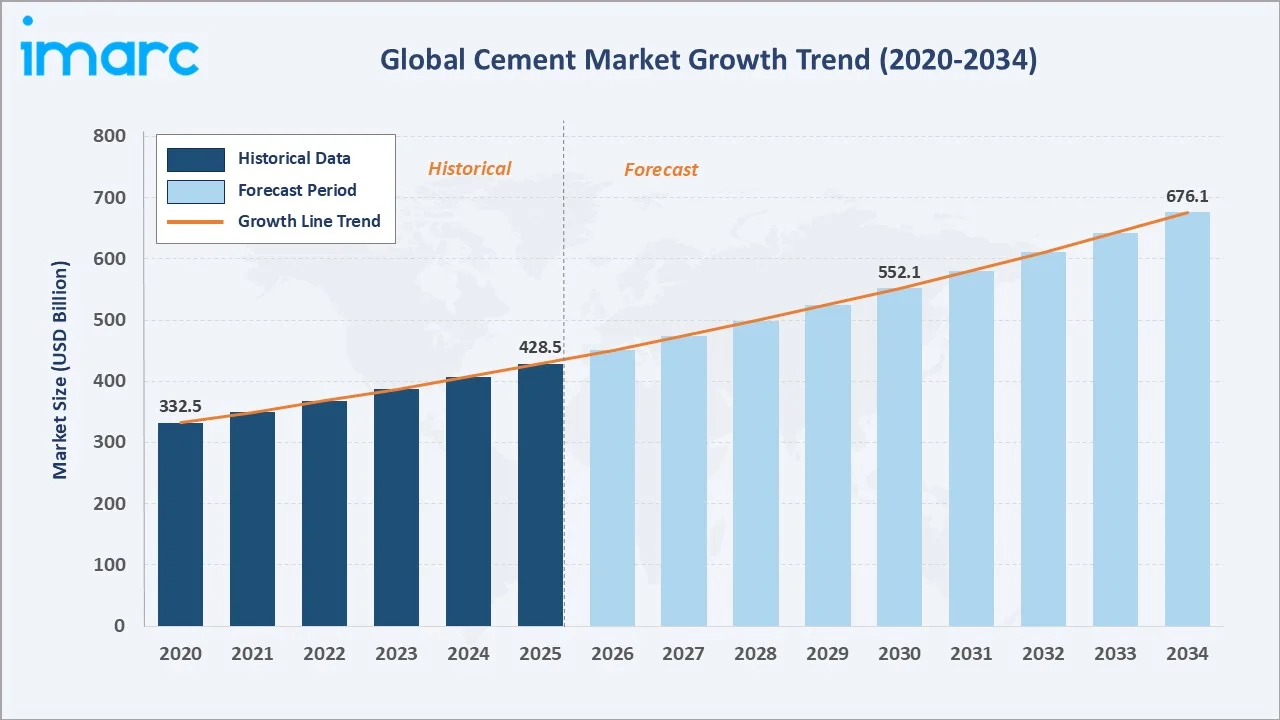

The cement market was valued at USD 428.5 Billion in 2025 and is projected to reach USD 676.1 Billion by 2034, exhibiting a CAGR of 5.20% during 2026-2034. Rapid urbanization across Asia-Pacific, large-scale government infrastructure programs, and rising residential construction activity across emerging economies are the primary drivers shaping sustained market expansion over the forecast period.

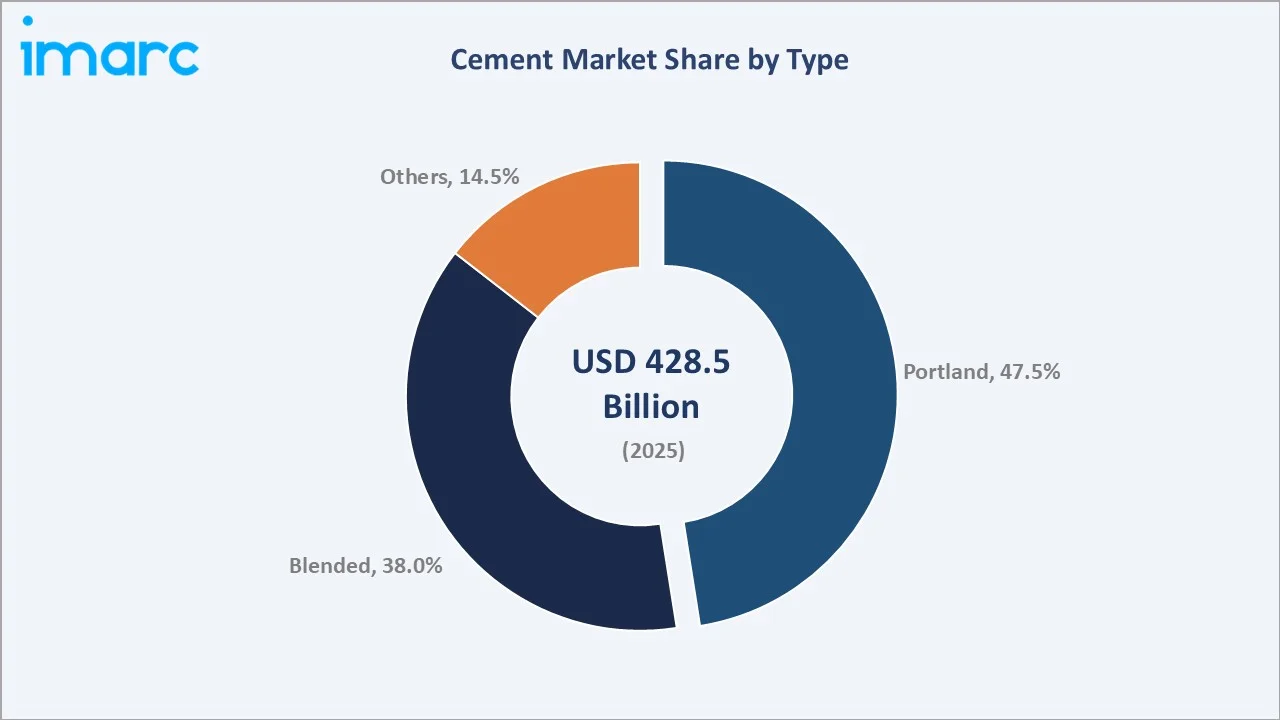

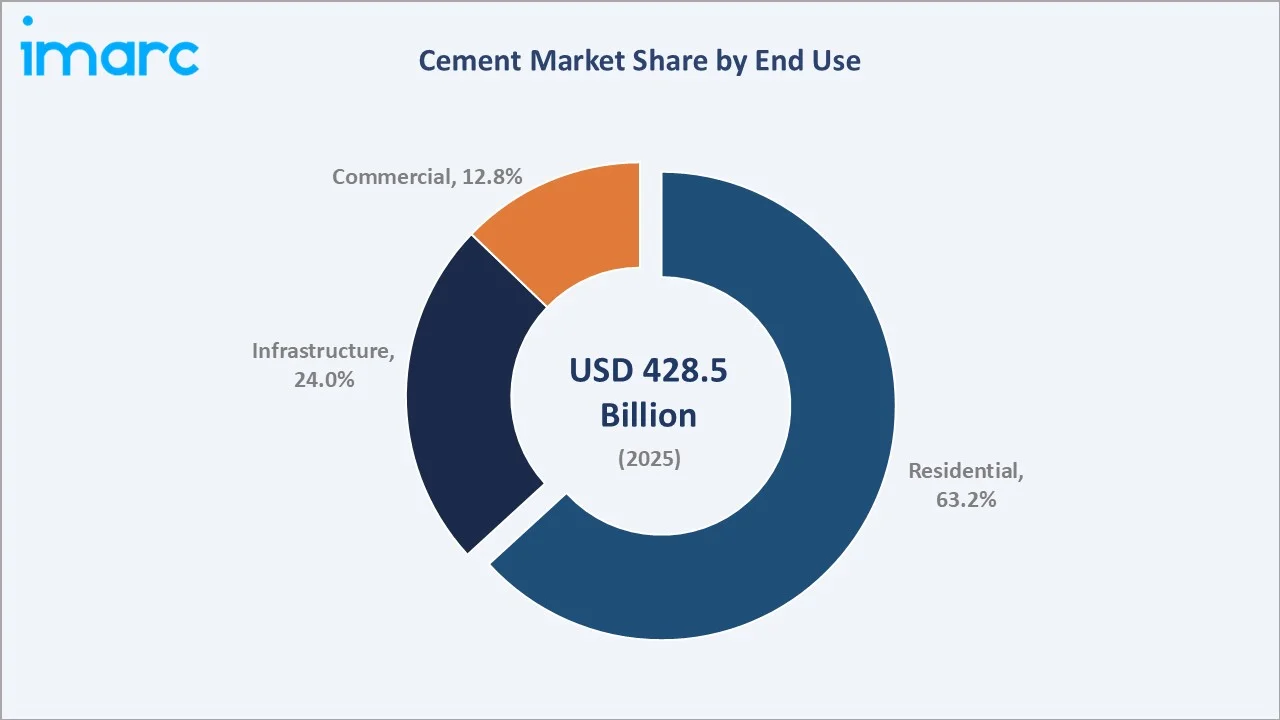

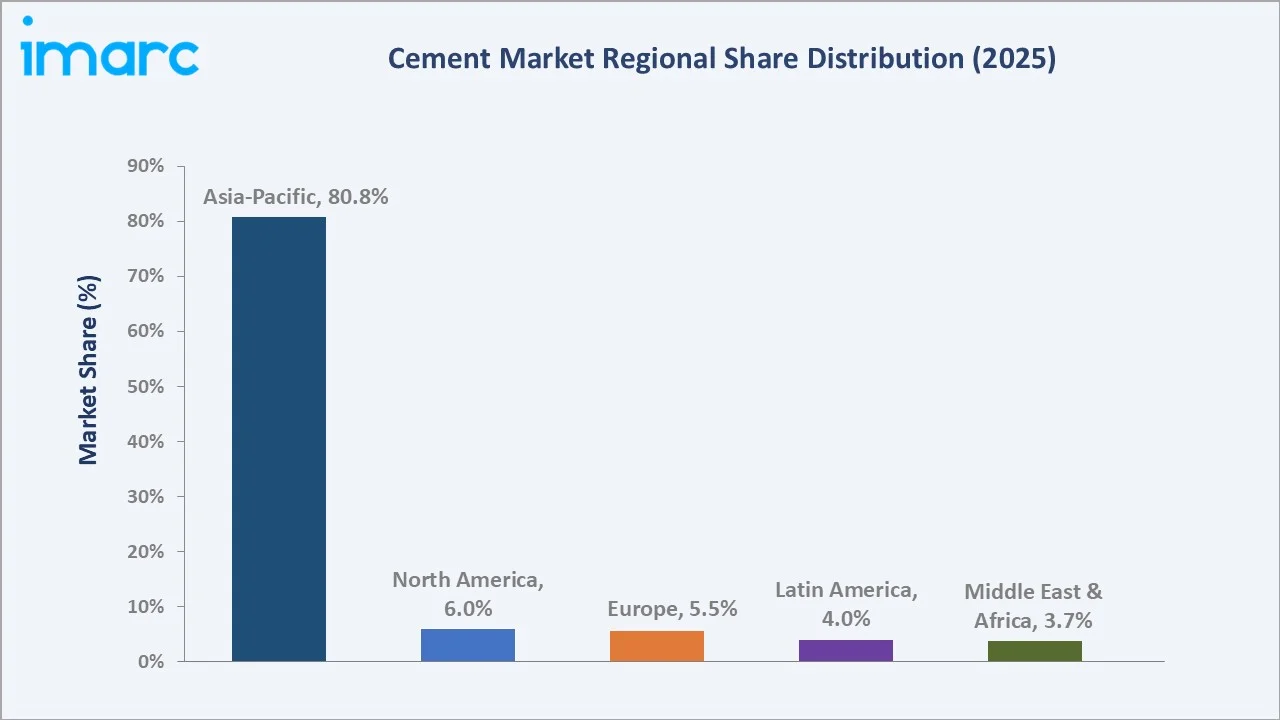

Portland leads the type segment at 47.5%, residential commands 63.2% of the end use segment, and Asia-Pacific holds 80.8% regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 428.5 Billion |

|

Forecast Market Size (2034) |

USD 676.1 Billion |

|

CAGR (2026-2034) |

5.20% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (80.8%, 2025) |

|

Fastest Growing Region |

Asia-Pacific (5.60% CAGR, 2026-2034) |

|

Leading Type |

Portland (47.5%, 2025) |

|

Leading End Use |

Residential (63.2%, 2025) |

The cement market grew from USD 332.5 Billion in 2020 to USD 428.5 Billion in 2025, driven by accelerating urbanization, post-pandemic infrastructure recovery spending, and government-backed affordable housing programs across South and Southeast Asia. Projected to reach USD 552.1 Billion in 2030 and USD 676.1 Billion by 2034, the forecast is supported by continued megaproject development in the Middle East, green building code adoption expanding blended cement demand, and capacity investments by leading producers across high-growth markets.

To get more information on this market, Request Sample

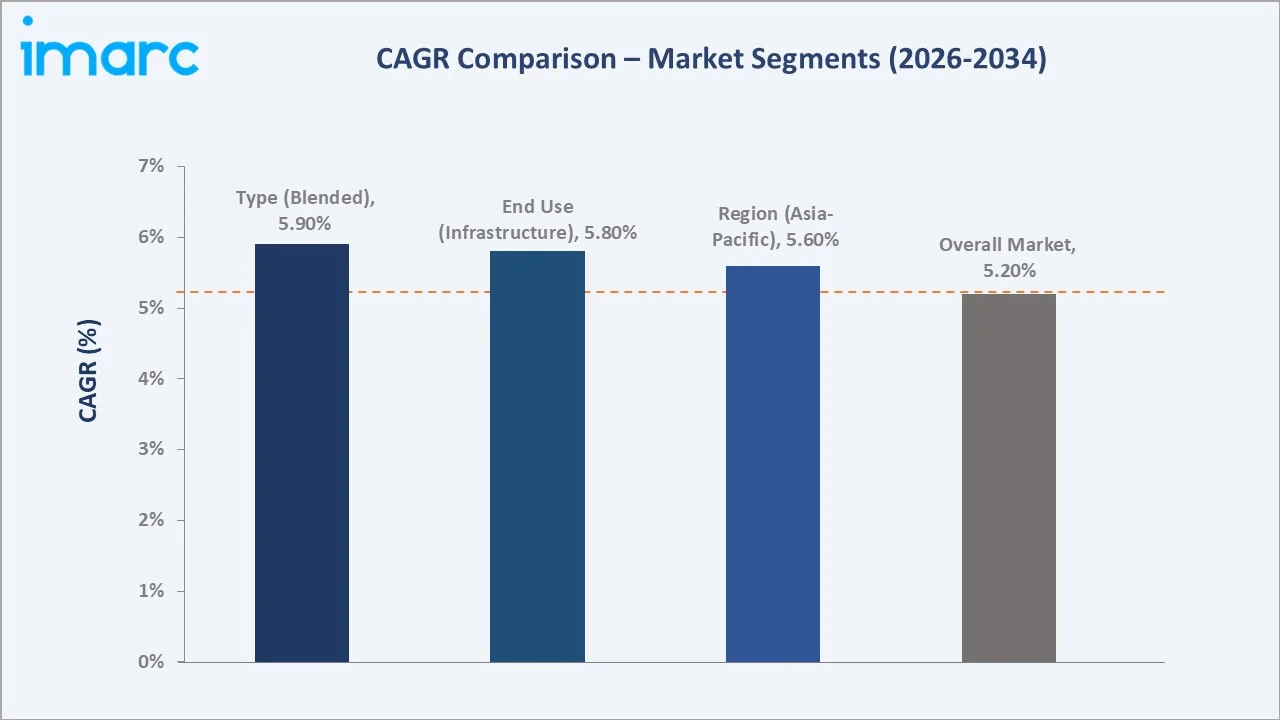

CAGR trajectories across type and end use sub-segments indicate that blended and infrastructure are growing faster than the overall 5.20% market CAGR, driven by green building regulations, expanding road and rail programs, and rising adoption of supplementary cementitious materials in developed markets.

Executive Summary

The cement market is on a strong growth trajectory from USD 332.5 Billion in 2020 to USD 676.1 Billion by 2034. The segment has evolved from a construction commodity to a technically differentiated industry where low-carbon products, digital manufacturing, and material innovation are redefining competitive advantage. Infrastructure investment cycles and urbanization-driven housing demand have collectively accelerated volume growth across Asia-Pacific, the Middle East, and Sub-Saharan Africa.

Portland leads the type segment at 47.5% in 2025, supported by its long-established role as the foundation of structural concrete across residential, commercial, and infrastructure applications. Residential commands 63.2% of the end use segment, anchored by mass housing programs, rural urbanization, and individual home construction in emerging markets. Asia-Pacific dominates the market at 80.8%, fueled by rapid urbanization, expanding industrial activity, and sustained residential construction demand across major emerging economies. By 2036, 600 Million people will reside in towns and cities in India, constituting 40% of the population, up from 31% in 2011.

Key Market Insights

|

Insight |

Data |

|

Leading Type |

Portland – 47.5% share (2025) |

|

Second Largest Type |

Blended – 38.0% share (2025) |

|

Leading End Use |

Residential – 63.2% share (2025) |

|

Second Largest End Use |

Infrastructure – 24.0% share (2025) |

|

Leading Region |

Asia-Pacific – 80.8% share (2025) |

|

Second Largest Region |

North America – 6.0% share (2025) |

|

Top Companies |

HOLCIM, Cemex S.A.B DE C.V., UltraTech Cement Ltd., Buzzi S.p.A., |

Key Analytical Observations Expanding On The Data Above:

- Portland at 47.5% dominates the type segment due to its universal applicability in structural concrete, broad availability of raw materials, and well-established production infrastructure across all major manufacturing regions. The segment benefits from long-standing contractor familiarity, regulatory acceptance in building codes globally, and suitability for high-strength applications in bridges, dams, and high-rise construction.

- Blended at 38.0% is the second largest type segment, driven by growing regulatory pressure on carbon emissions, rising acceptance of fly ash and slag-based formulations in green building certification systems, and economic advantages from lower clinker content reducing energy and raw material costs for manufacturers.

- Residential at 63.2% leads the end use segment, anchored by large-scale affordable housing programs across South Asia and Sub-Saharan Africa, sustained individual home construction in rural and semi-urban areas, and government subsidized housing initiatives that maintain high-volume cement demand independent of commercial real estate cycles.

- Infrastructure share at 24.0% represents the second largest end use segment, supported by sustained public investment in transportation networks, urban transit systems, ports, airports, energy facilities, and water infrastructure projects. In December 2025, the South Korean government revealed plans to allocate 2.7 Trillion Won (USD 1.8 Billion) for building a combined civilian-military airport in the TK region, encompassing Daegu and North Gyeongsang Province.

- Asia-Pacific at 80.8% commands dominant regional share, supported by ongoing urbanization, smart city development programs, and large-scale infrastructure investment across the transportation, energy, and water management sectors.

Cement Market Overview

Cement is a hydraulic binder produced by calcining limestone and other minerals at high temperatures to form clinker, which is then ground with gypsum and supplementary cementitious materials into fine powder. The cement market spans a broad ecosystem integrating limestone quarrying operations, coal and energy suppliers, clinker producers, cement grinding facilities, packaging and logistics networks, construction product distributors, and end users ranging from residential homebuilders to large-scale infrastructure contractors.

The global ecosystem integrates raw material extractors, energy suppliers, equipment manufacturers, logistics and port operators, distributors and dealers, regulatory authorities, and construction end users. Macroeconomic drivers, including GDP growth, urbanization rates, government infrastructure spending, and housing policy, directly shape demand cycles, while energy price volatility, carbon pricing mechanisms, and raw material availability influence supply-side cost structures and investment decisions.

Market Dynamics

To evaluate market opportunities, Request Sample

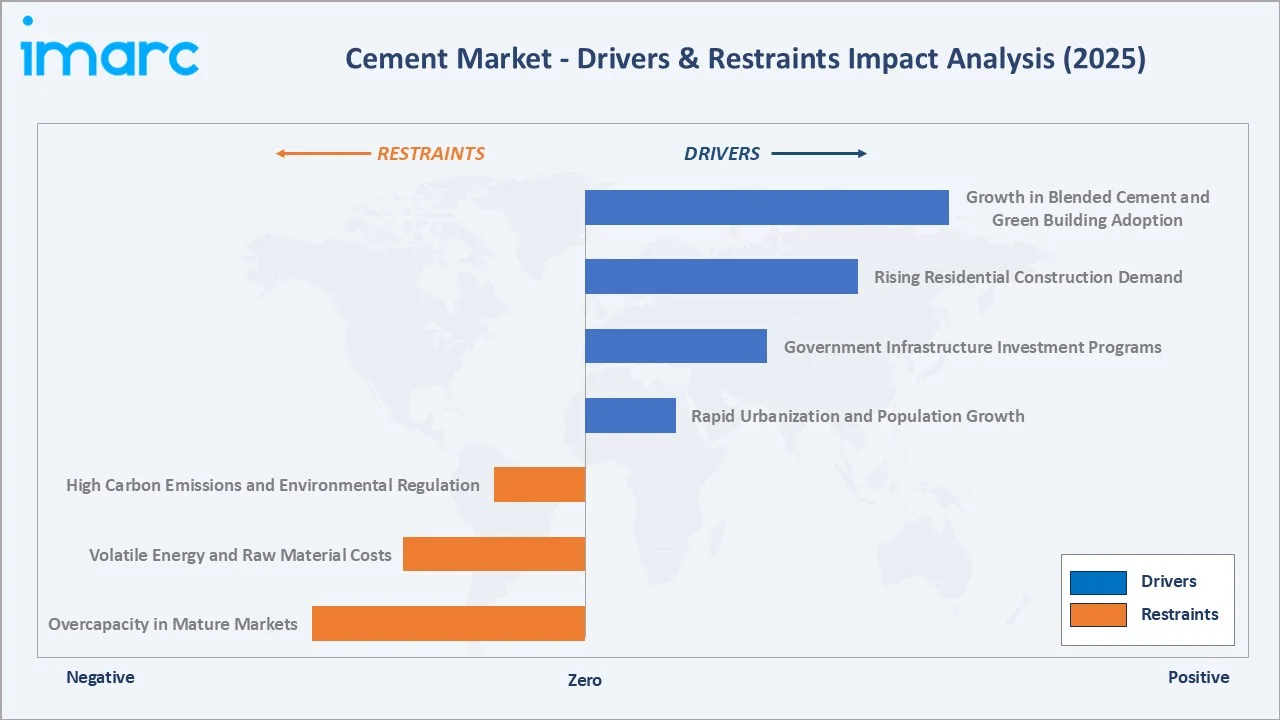

Market Drivers

- Rapid Urbanization and Population Growth: Accelerating urban migration across Asia-Pacific, Africa, and Latin America is generating sustained demand for residential construction, urban infrastructure, and public facilities. Simultaneously, growing populations are increasing the need for new housing, schools, healthcare facilities, and transportation networks, thereby driving long-term cement consumption across both urban and peri-urban regions. The 2024 World Population Prospects report from the United Nations estimates that the world population will hit 9.7 Billion by the year 2050.

- Government Infrastructure Investment Programs: Large-scale national infrastructure initiatives, including highway construction, metro rail expansion, port development, and energy infrastructure projects, across India, China, Southeast Asia, and the Middle East are among the most significant cement demand drivers. Government capital expenditure programs consistently translate into multi-year cement offtake agreements and support regional capacity expansion decisions.

- Rising Residential Construction Demand: Housing shortfalls across developing economies, low-income housing subsidy programs, and growing middle-class demand for urban housing are sustaining high residential cement consumption. Large-scale urban housing developments, apartment construction projects, and suburban residential expansion are increasing cement consumption volumes across both emerging and developed markets.

- Growth in Blended Cement and Green Building Adoption: Tightening building codes, green building certification systems, and corporate sustainability commitments by construction companies are accelerating substitution of Portland cement with blended variants containing supplementary cementitious materials. This shift is driving revenue premiumization for manufacturers with established blended product portfolios and positions innovation-focused producers for favorable competitive positioning through 2034.

Market Restraints

- High Carbon Emissions and Environmental Regulation: Cement manufacturing remains one of the most carbon-intensive industrial activities due to emissions generated during both clinker production and fuel combustion processes. Increasingly stringent environmental regulations, carbon pricing mechanisms, and sustainability reporting requirements are compelling producers to invest in low-carbon technologies, alternative fuels, and emission-reduction initiatives, thereby increasing operational and capital expenditure burdens.

- Volatile Energy and Raw Material Costs: Clinker production requires sustained high-temperature kiln operation that is highly sensitive to coal, natural gas, and electricity prices. Raw material cost shocks reduce producer margins in markets where cement prices are regulated or where competitive intensity limits pass-through capacity, constraining investment in capacity expansion and technology upgrades, particularly among smaller regional producers.

- Overcapacity in Mature Markets: Structural overcapacity in European, North American, and select Asian markets depresses pricing power, reduces capacity utilization rates, and creates margin pressure for producers unable to differentiate through product mix or cost optimization. Oversupply cycles in China and parts of Europe have historically constrained global cement price levels and discouraged new capacity investment in affected regions.

Market Opportunities

- Carbon Capture and Low-Carbon Cement Development: Emerging technologies including carbon capture utilization and storage at cement plants, clinker substitution through novel supplementary cementitious materials, and calcined clay-based LC3 cements offer producers pathways to differentiate on carbon intensity. Early movers in low-carbon cement product lines are securing premium positioning with sustainability-focused developers, government procurement programs, and export markets with stringent carbon import standards.

- Smart Manufacturing and Digital Process Optimization: Adoption of AI-driven kiln control systems, predictive maintenance platforms, and advanced process control technology is enabling leading producers to reduce specific energy consumption, minimize kiln downtime, and optimize raw mix quality. These investments deliver both cost reduction and capacity efficiency improvements that translate to competitive margin advantages over producers relying on conventional process management.

Market Challenges

- Transition to Net-Zero Production: Achieving science-based emissions reduction targets requires simultaneous investment in alternative fuels, carbon capture infrastructure, and product reformulation, creating capital intensity pressures that are most acute for mid-size producers lacking the balance sheet depth of global multinationals. Technology readiness gaps for industrial-scale carbon capture at competitive cost remain a near-term implementation barrier.

- Logistics and Distribution Inefficiencies: Cement is a weight-intensive bulk commodity with relatively low value-to-weight ratios, making transportation costs a critical competitive factor. Inadequate road, rail, and port infrastructure in Sub-Saharan Africa, parts of South Asia, and inland regions of Latin America constrains market reach, inflates delivered costs, and limits the addressable market for formal sector producers in high-growth regions.

Emerging Market Trends

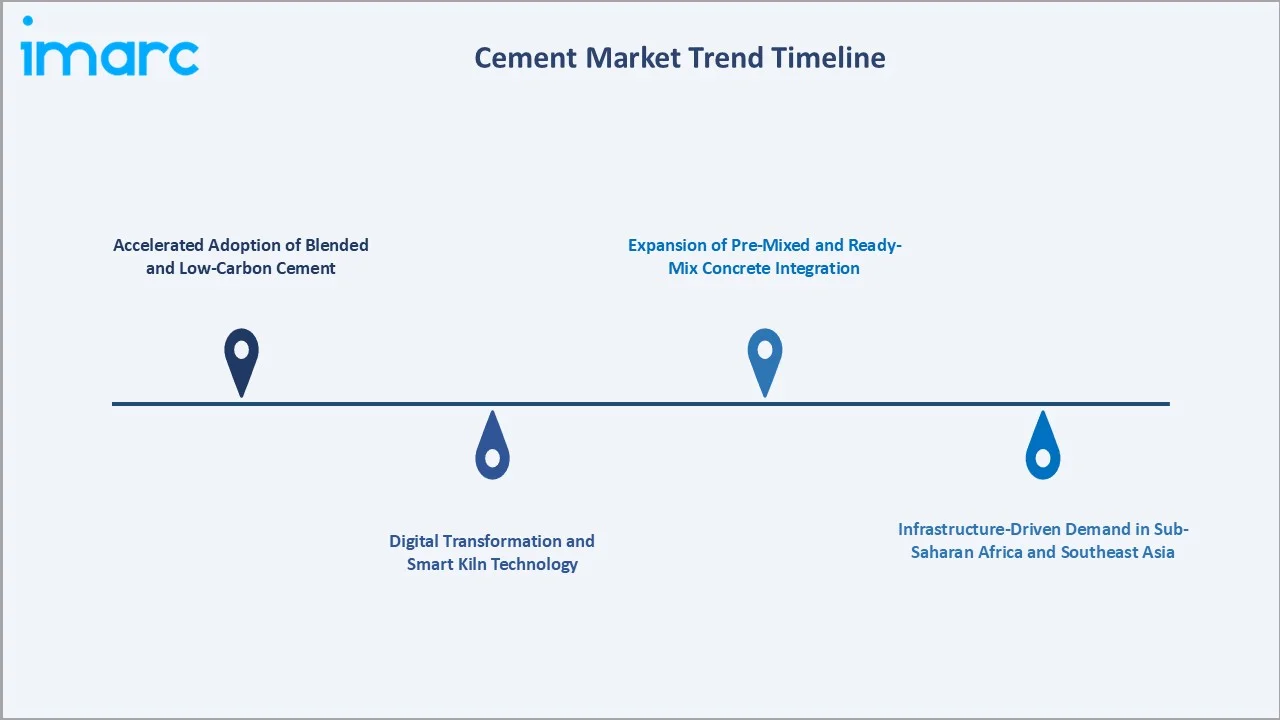

1. Accelerated Adoption of Blended and Low-Carbon Cement

Construction companies and national procurement bodies are increasingly specifying blended cement products to meet embodied carbon targets in green building certification programs. Producers are investing in grinding capacity, supplementary cementitious material sourcing, and quality assurance systems to scale blended product output. The share of blended cement in total production is projected to rise materially through 2034 as carbon pricing mechanisms expand across major consuming regions.

2. Digital Transformation and Smart Kiln Technology

Leading producers are deploying advanced process control systems, AI-driven quality prediction models, and real-time energy management platforms that reduce specific heat consumption and optimize clinker factor. Digital integration across the production value chain is enabling manufacturers to operate closer to theoretical efficiency limits, reducing variable costs and improving environmental performance simultaneously. The use of digital twins for virtual plant commissioning is shortening new capacity ramp-up cycles.

3. Expansion of Pre-Mixed and Ready-Mix Concrete Integration

Vertical integration between cement producers and ready-mix concrete operations is intensifying as major producers seek to capture downstream value and secure cement offtake in urbanizing markets. Integration reduces distribution costs, enables product quality assurance at the point of use, and provides producers with direct access to construction data that informs product development and commercial strategy.

4. Infrastructure-Driven Demand in Sub-Saharan Africa and Southeast Asia

Demographic growth, rapid urbanization, and accelerating government infrastructure programs in Nigeria, Ethiopia, Tanzania, Vietnam, Indonesia, and the Philippines are positioning Sub-Saharan Africa and Southeast Asia as high-growth cement markets through 2034. New capacity investments by regional and international producers are targeting these markets, with greenfield cement plants and grinding station networks expanding distribution reach into high-density urban corridors.

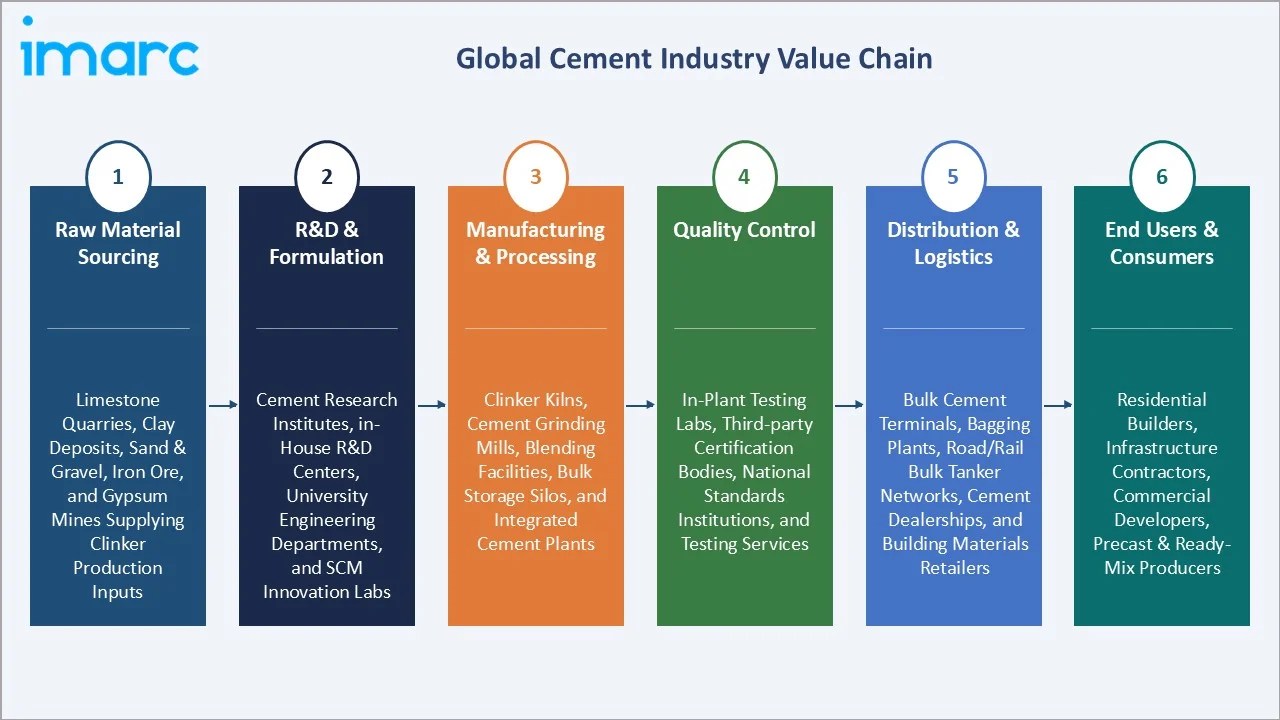

Industry Value Chain Analysis

The cement market value chain spans six stages from raw material extraction through end user application. Manufacturing, quality control, and logistics capture the highest value-add, while innovation in raw material substitution and digital process integration increasingly determines sustainable competitive differentiation in this capital-intensive industry.

|

Stage |

Key Players / Examples |

|

Raw Material Sourcing |

Limestone quarries, clay deposits, sand and gravel suppliers, iron ore sources, and gypsum mines supplying the primary inputs for clinker production |

|

R&D & Formulation |

Cement research institutes, in-house R&D centers at major producers, university engineering departments, and supplementary cementitious material innovation labs developing blended cement formulations |

|

Manufacturing & Processing |

Clinker kilns, cement grinding mills, blending facilities, bulk storage silos, and integrated cement plants producing finished cement in bulk and packaged formats |

|

Quality Control |

In-plant testing laboratories, third-party quality certification bodies, national standards institutions, and construction materials testing services ensuring product conformance |

|

Distribution & Logistics |

Bulk cement terminals, bagging plants, road and rail bulk tanker networks, cement dealerships, and building materials retailers and wholesalers |

|

End Users & Consumers |

Residential homebuilders, infrastructure contractors, commercial developers, precast concrete manufacturers, ready-mix concrete producers, and government procurement agencies |

Vertically integrated companies controlling limestone reserves, clinker production, cement grinding, and distribution networks are positioned to capture the greatest value across the chain. Producers owning proprietary blended cement formulations and co-processing capabilities for alternative fuels hold structural competitive advantages over commodity-focused intermediaries dependent on spot raw material and energy markets.

Technology Landscape in the Cement Industry

Advanced Kiln and Process Control Technology

Multi-stage cyclone preheater and precalciner kiln systems have become the industry standard for new installations, offering thermal efficiencies significantly above older wet and dry process kilns. Advanced process control systems incorporating machine learning (ML) algorithms are now being deployed by tier-1 producers to continuously optimize kiln feed, fuel consumption, and clinker chemistry in real time, reducing specific energy consumption and improving clinker quality consistency.

Carbon Capture, Utilization, and Storage

Post-combustion carbon capture systems, oxyfuel combustion technology, and direct separation of process CO₂ from kiln gases are at various stages of pilot and commercial demonstration at cement plants globally. Captured carbon is increasingly being explored for utilization in concrete curing, synthetic fuel production, and industrial applications, supporting the industry's long-term decarbonization objectives while creating potential value-added revenue streams.

Digital Manufacturing and Industry 4.0 Integration

Industrial IoT sensor networks enabling real-time monitoring of kiln, mill, and packaging line performance are being integrated with enterprise manufacturing execution systems to reduce unplanned downtime, optimize maintenance schedules, and improve throughput consistency. Drone-based quarry surveying, autonomous crusher management, and AI-powered blending optimization are progressively reducing operating labor intensity while improving raw mix quality and reducing extraction costs at integrated cement operations.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Portland |

47.5% |

2025 |

|

End Use |

Residential |

63.2% |

2025 |

|

Region |

Asia-Pacific |

80.8% |

2025 |

By Type

Portland commands 47.5% majority share in 2025, driven by its universal acceptance in structural concrete applications, compatibility with existing construction specifications and building codes, and the broad raw material availability that supports cost-competitive production across all major geographies. Portland cement is the default specification for high-strength concrete in bridges, dams, industrial floors, and multi-story building structures, ensuring stable demand from the infrastructure and commercial construction segments.

To access detailed market analysis, Request Sample

Blended at 38.0% in 2025 is the second largest type segment, supported by green building certification requirements, carbon reduction commitments by construction companies, and economic advantages from lower clinker-to-cement ratios that reduce energy and raw material costs. The segment benefits from growing fly ash and slag availability from steel and power generation industries, providing a cost-competitive feedstock base that supports margin improvement for producers investing in blended cement production capacity.

By End Use

Residential commands 63.2% share in 2025, reflecting the dominant role of housing construction in driving cement demand across developing economies. Mass housing programs, individual home construction in urbanizing markets, and apartment development in tier-2 and tier-3 cities across Asia and Africa maintain consistent residential cement offtake that is relatively resilient to short-term economic fluctuations due to structural housing supply deficits across high-growth markets.

Infrastructure at 24.0% in 2025 serves highway, bridge, metro, airport, port, dam, and utility construction projects funded predominantly by government capital expenditure programs. The segment is characterized by large-volume, multi-year project demand profiles that provide revenue visibility for cement producers and support investment in bulk logistics infrastructure.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

80.8% |

Large-scale urbanization and housing programs, major infrastructure investment across China and India, high residential construction activity, and growing government transport infrastructure spending driving sustained high-volume cement demand |

|

North America |

6.0% |

Infrastructure renewal programs, federal highway and bridge investment, sustained residential construction in Sun Belt states, and commercial real estate development in major metropolitan areas supporting moderate market growth |

|

Europe |

5.5% |

Green building code adoption supporting blended cement demand, EU infrastructure cohesion fund spending in Eastern Europe, building renovation wave programs, and decarbonization mandates shaping product mix evolution toward low-carbon formulations |

|

Latin America |

4.0% |

Urban housing deficit reduction programs, road and port infrastructure investment, growth in mining-related construction, and government-sponsored social housing initiatives driving incremental cement demand across Brazil, Mexico, and Colombia |

|

Middle East and Africa |

3.7% |

Megaproject construction programs in Gulf Cooperation Council countries, urban infrastructure expansion across Sub-Saharan Africa, growing population centers requiring housing and utility infrastructure, and diversification-driven development investment in non-oil sectors |

Asia-Pacific at 80.8% in 2025 leads the regional landscape by an overwhelming margin, anchored by China's position as the world's leading cement producer and consumer, India's rapidly expanding infrastructure and housing construction pipeline, and the combined demand from Southeast Asian emerging economies undergoing rapid urbanization.

North America at 6.0% is the second largest region, supported by significant federal infrastructure investment through multi-year transportation and public works funding bills, sustained residential construction in high-growth southern and western United States markets, and incremental commercial construction activity in logistics, data center, and manufacturing facility segments.

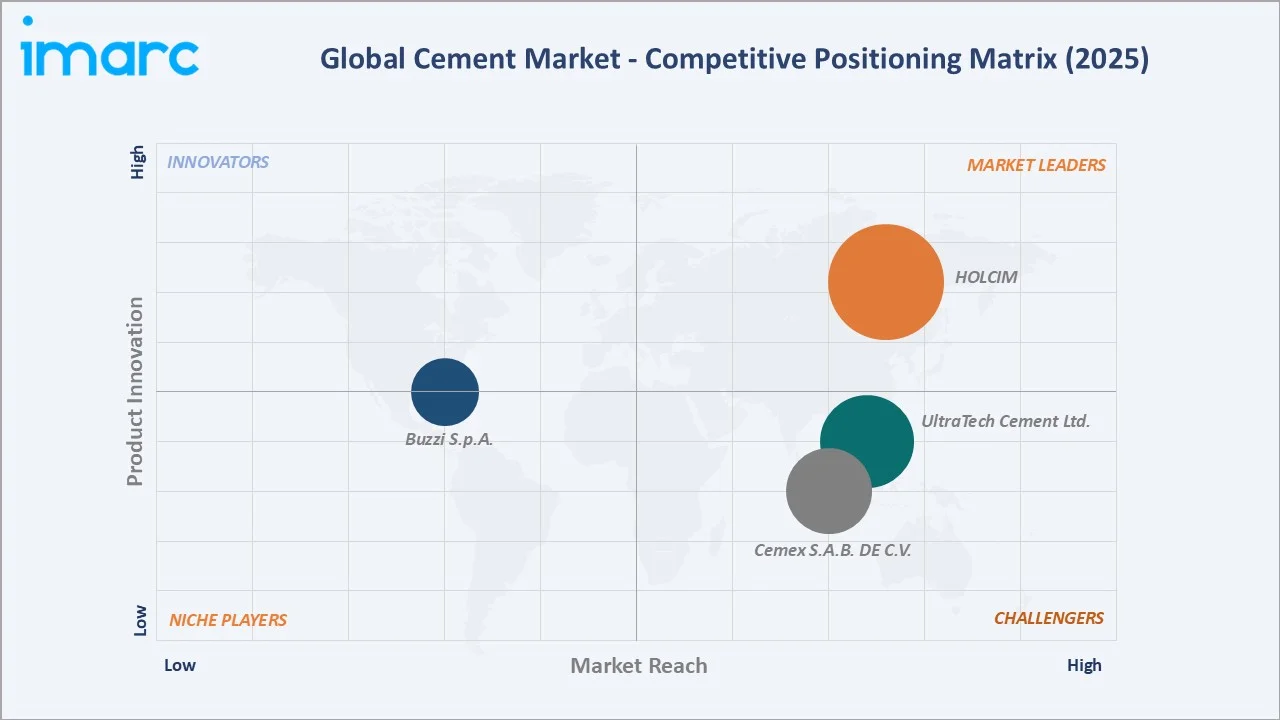

Competitive Landscape

The cement market is moderately consolidated at the global level, with a small number of multinational producers accounting for a significant share of international trade, technology licensing, and investment-grade capacity additions. Regional and national producers command strong positions in domestic markets through proximity advantages, distribution networks, and government relationships, creating a layered competitive structure where global scale and local market depth are both necessary for sustained competitive position.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

HOLCIM |

ECOPlanet |

Leader |

Expanding low-carbon cement portfolio and circular economy construction solutions globally |

|

Cemex S.A.B DE C.V. |

Vertua |

Challenger |

Developing sustainable building solutions and expanding ready-mix and concrete products integration alongside core cement operations |

|

UltraTech Cement Ltd. |

UltraTech Premium, Birla White |

Challenger |

Strengthening domestic market leadership in India through capacity expansion and growing presence in East Africa and select export markets |

|

Buzzi S.p.A. |

Dyckerhoff, Alamo Cement |

Established Player |

Growing European and North American market footprint through operational efficiency improvement and selective geographic expansion |

Key players include HOLCIM, Cemex S.A.B DE C.V., UltraTech Cement Ltd., and Buzzi S.p.A., among others.

Key Company Profiles

HOLCIM

HOLCIM is one of the world's largest building materials companies, headquartered in Zug, Switzerland, with operations spanning cement, aggregates, ready-mix concrete, and building solutions across several markets globally. The company serves residential, infrastructure, and commercial construction customers through an integrated portfolio of conventional and sustainable construction materials, with a strategic focus on low-carbon products and circular construction solutions.

- Product Portfolio: Portland and blended cement products under the ECOPlanet low-carbon cement brand line and a range of building solutions targeting sustainable infrastructure and green building certification applications.

- Recent Development: HOLCIM continued to strengthen its sustainable construction portfolio through investments in low-carbon cement technologies, operational efficiency improvements, and initiatives supporting circular construction and decarbonization across its global operations.

- Strategic Focus: Expanding the low-carbon cement and sustainable building products portfolio through carbon capture investment, circular economy material integration, and digitally enabled construction solutions across key global markets.

Cemex S.A.B DE C.V.

Cemex S.A.B DE C.V. is a global construction materials company with operations across the Americas, Europe, Africa, the Middle East, and Asia. The company produces and markets cement, ready-mix concrete, aggregates, and related construction materials, serving residential, infrastructure, and commercial customers across its global footprint through a network of manufacturing plants and distribution terminals.

- Product Portfolio: Portland, blended, and specialty cement products with low-carbon variants under the Vertua product line, aggregates, ready-mix concrete, and building solutions targeting sustainable construction and green building applications across its operating markets.

- Recent Development: Cemex S.A.B DE C.V. has been advancing its portfolio transformation strategy, divesting select assets to optimize its geographic footprint while focusing on operational efficiency and strengthening its position in its core markets.

- Strategic Focus: Developing sustainable construction solutions integrating low-carbon cement with broader concrete and building products, and improving operational efficiency through its ongoing cost optimization program across global operations.

UltraTech Cement Ltd.

UltraTech Cement Ltd. is one of the largest cement producers in the world outside China, headquartered in Mumbai, India, and part of the Aditya Birla Group. The company operates a large network of integrated cement plants, grinding units, and bulk terminals across India and internationally, serving residential, infrastructure, and commercial construction customers through an extensive distribution and dealer network.

- Product Portfolio: Portland, blended, and specialty grey cement under the UltraTech brand and its premium variants for high-performance applications, white cement and wall care products under the Birla White brand, and ready-mix concrete through an extensive network of batching plants.

- Recent Development: UltraTech Cement Ltd. has been expanding its manufacturing capacity and distribution network to strengthen its position across domestic and international markets, with continued investment in sustainable and efficient production technologies.

- Strategic Focus: Strengthening cement market leadership through capacity expansion, broadening product portfolio across grey and white cement segments, and growing presence in international markets to support long-term revenue diversification.

Market Concentration Analysis

The cement market exhibits moderate concentration at the global level. The top four producers – HOLCIM, Cemex S.A.B DE C.V., UltraTech Cement Ltd., and Buzzi S.p.A., – collectively account for an estimated 40–45% of global cement production capacity and a somewhat higher share of international trade in cement and clinker.

Barriers to entry in the organized segment are substantial, requiring significant capital investment in clinker production facilities, limestone reserve access, environmental permitting, and distribution infrastructure. These factors favor established producers with long-term raw material access, scale-based cost advantages, and regulatory compliance track records.

Consolidation activity in the global cement industry has been ongoing for decades, with large multinationals periodically acquiring regional producers to expand geographic coverage, consolidate market positions, and capture distribution synergies. Emerging market capacity additions from domestic producers in India, Vietnam, and Sub-Saharan Africa are gradually increasing the number of significant market participants without materially reducing concentration among the global tier-1 producers.

Investment & Growth Opportunities

Fastest-Growing Segments

Blended growing at an estimated 5.90% CAGR through 2034 represents the fastest-growing type segment, driven by green building code adoption, carbon pricing expansion, and economic advantages from lower clinker factor production. Infrastructure at an estimated 5.80% CAGR is the fastest growing end use segment, anchored by sustained government capital expenditure programs across Asia-Pacific, the Middle East, and Sub-Saharan Africa.

Emerging Markets

Asia-Pacific at an estimated 5.60% CAGR is the fastest growing region, underpinned by China and India's sustained construction demand and Southeast Asian urbanization driving incremental cement consumption well above the overall market rate of 5.20%.

Venture & Investment Trends

Investment is flowing into cement producers and technology startups focused on carbon capture and storage at cement plants, novel supplementary cementitious material development, digital kiln optimization platforms, and construction technology integration that bundles cement with broader building material and service offerings. Green bond issuances by major cement producers have become an established mechanism for financing sustainability-linked capital expenditure, with proceeds directed toward alternative fuel infrastructure, low-carbon product capacity, and energy efficiency upgrades.

Future Market Outlook (2026-2034)

The cement market is forecast to expand from USD 428.5 Billion in 2025 to USD 676.1 Billion by 2034 at a CAGR of 5.20%, adding approximately USD 247.6 Billion in incremental annual market value over the forecast period.

Three structural forces will define the market through 2034: first, escalating decarbonization mandates in Europe and North America compelling producers to accelerate carbon capture investment and low-carbon product portfolio development; second, sustained infrastructure and housing construction investment across Asia-Pacific, the Middle East, and Sub-Saharan Africa maintaining high-volume demand growth for conventional and blended cement products; and third, digital manufacturing transformation enabling leading producers to improve efficiency, reduce emissions intensity, and differentiate service offerings beyond product specifications.

By 2034, the cement market is expected to be defined by a clear bifurcation between producers that have successfully invested in decarbonization technology and low-carbon product portfolios commanding premium pricing in developed markets, and volume-focused producers serving high-growth emerging markets with standard formulations at competitive cost structures.

Research Methodology

Primary Research

Primary research included structured interviews with cement manufacturers, construction contractors, building materials distributors, engineering consultants, and regulatory specialists across key geographies. Validation of market sizing, regional demand patterns, segment mix evolution, and technology adoption trends was conducted through direct industry engagement with professionals active across the cement value chain in Asia-Pacific, Europe, North America, and the Middle East.

Secondary Research

Secondary sources included publications from the Global Cement and Concrete Association, International Energy Agency, World Bank infrastructure investment reports, national construction industry associations, cement producer annual reports and investor presentations, trade data from national customs authorities, and building permit and construction start statistics from government statistical agencies in major consuming markets.

Forecasting Models

Market forecasts used top-down and bottom-up models combining regional cement consumption data, construction activity indicators, capacity utilization trends, product mix evolution, carbon regulation transition scenarios, and macroeconomic investment variables. Scenario analysis addressed infrastructure spending cycle variability, green building code adoption pace, carbon capture technology commercialization timelines, and demand evolution in high-growth emerging markets through 2034.

Cement Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Blended, Portland, Others |

| End Uses Covered | Residential, Commercial, Infrastructure |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | HOLCIM, Cemex S.A.B DE C.V., UltraTech Cement Ltd., Buzzi S.p.A., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the cement Industry from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global cement market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the cement industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Cement Market Report

The cement market was valued at USD 428.5 Billion in 2025, driven by urbanization, infrastructure investment, and residential construction demand across Asia-Pacific and emerging markets globally.

The market is projected to grow at a CAGR of 5.20% from 2026 to 2034, reaching USD 676.1 Billion, supported by infrastructure programs, housing demand, and blended cement adoption.

Portland leads at 47.5% in 2025, driven by universal applicability in structural concrete, broad raw material availability, and acceptance across all major building code systems globally.

Residential dominates at 63.2% in 2025, anchored by mass housing programs, individual home construction in urbanizing markets, and government-subsidized affordable housing initiatives.

Asia-Pacific commands 80.8% in 2025 and is also the fastest growing region at an estimated 5.60% CAGR through 2034, led by China and India's combined cement demand, rapid urbanization, and large-scale government infrastructure investment across the region.

Leading players include HOLCIM, Cemex S.A.B DE C.V., UltraTech Cement Ltd., and Buzzi S.p.A., among others.

Key drivers include rapid urbanization, government infrastructure programs, rising residential construction demand, blended cement adoption, and expansion of construction activity in Sub-Saharan Africa and Southeast Asia.

High carbon emissions and regulatory pressure, volatile energy costs, overcapacity in mature markets, and logistics constraints in developing markets are the primary restraints.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)