Center Stack Display Market Report by Display Technology (TFT LCD, OLED), Display Size (Up to 7 Inch, More Than 7 Inch), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles), Application (Navigation, HVAC Control, Infotainment, and Others), Sales Channel (OEM, Aftermarket), and Region 2026-2034

Global Center Stack Display Market:

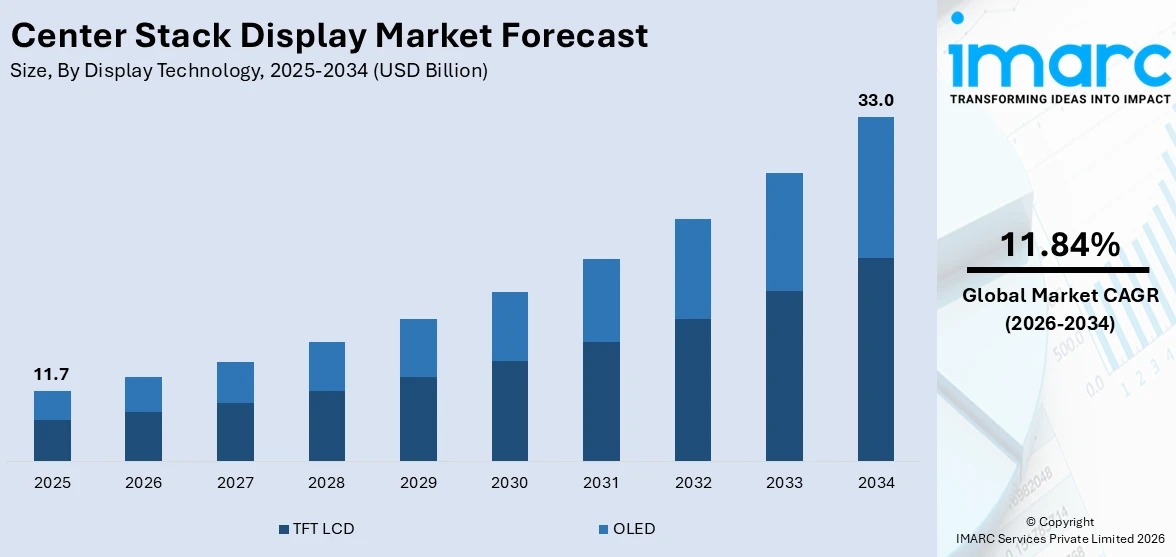

The global center stack display market size reached USD 11.7 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 33.0 Billion by 2034, exhibiting a growth rate (CAGR) of 11.84% during 2026-2034. The rapid advancements in display materials and technologies for improved durability, the increasing consumer interest in customizable dashboards and display layouts, and the rising focus of automakers on creating smart and connected vehicles are some of the factors propelling the market growth.

|

Report Attribute

|

Key Statistics |

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 11.7 Billion |

| Market Forecast in 2034 | USD 33.0 Billion |

| Market Growth Rate (2026-2034) | 11.84% |

Center Stack Display Market Analysis:

- Major Market Drivers: Increasing vehicle ownership and the rising demand for advanced vehicle infotainment systems are primarily driving the growth of the market. Additionally, the escalating consumer preference for intuitive and user-friendly interfaces is also contributing to the market growth.

- Key Market Trends: Automakers are leveraging cutting-edge touchscreen technology, augmented reality features, and voice-activated controls to create interactive and user-friendly displays, providing seamless integration between the vehicle and its occupants, which is acting as a significant growth-inducing factor for the market growth.

- Competitive Landscape: Some of the leading center stack display market companies include Alps Electric Co. Ltd., Continental AG (Schaeffler Technologies AG & Co. KG), HARMAN International (Samsung Electronics Co. Ltd.), Panasonic Holdings Corporation, Preh GmbH, Robert Bosch GmbH, and Visteon Corporation, among others.

- Geographical Trends: According to the report, Asia Pacific holds a significant market share. This can be attributed to the presence of major automotive manufacturers, a tech-savvy population, and rising consumer preferences for premium in-car features. The region's emphasis on enhancing the driving experience with cutting-edge displays, offering seamless connectivity and intuitive user interfaces, is accelerating the market growth.

- Challenges and Opportunities: Challenges in the center stack display market include increasing competition, evolving consumer preferences, and technological advancements driving the need for constant innovation. Opportunities lie in integrating advanced features like AI assistants, enhanced connectivity, and customizable user interfaces to meet evolving consumer demands and create differentiated offerings.

To get more information on this market Request Sample

Center Stack Display Market Trends:

Growing Popularity of Electric and Autonomous Vehicles

The growing popularity of electric and autonomous vehicles is driving demand for sophisticated center stack displays that not only provide entertainment and connectivity but also offer real-time information about battery status, charging stations, energy consumption, and range estimation. Moreover, the increasing ownership of these vehicles is creating a significant demand for center stack displays. For instance, as of March 2023, there were more than 2.3 million electric vehicles in India. Moreover, it is expected that the number of autonomous vehicles will surpass 54 million in 2024. In autonomous vehicles, the center stack display becomes even more critical as it serves as the primary interface for passengers, displaying route information, entertainment options, and communication services. As a result, with the increasing number of autonomous and electric vehicles, the installation of center stack displays is also rising, which is positively impacting the center stack display market outlook.

Technological Advancements

Technological developments in augmented reality (AR) and heads-up display (HUD) systems have revolutionized the automotive industry, contributing significantly to enhanced driving experiences and safety. Various key market players are increasingly investing in developing and launching automotive displays with enhanced features, which is offering lucrative growth opportunities to the overall market. For instance, in January 2024, Tata launched the Tata Punch EV with dual 10.25-inch displays and an updated center console. Besides this, as safety concerns about distracted driving are also increasing, Google is rolling out a new initiative for app developers targeting car users. This program aims to speed up the approval process for apps to be used in cars. As part of this effort, Google will review mobile apps in advance that work well with the bigger screens commonly found in newer cars. Moreover, in July 2023, MINI, a British automotive brand, launched its new model with the MINI Interaction Unit, which is a round OLED display with a 240 mm diameter. Its positioning within the cabin allows it to be used comfortably by the driver and front passenger. Such innovations are projected to propel the center stack display market share in the coming years.

Regulatory Requirements

Stringent safety regulations and guidelines, such as those related to distracted driving, are encouraging the adoption of hands-free interfaces and voice-controlled systems, which is creating a positive outlook for the market. Certifying an in-car display is a complex and rigorous process. The car makers go to organizations such as the Society of Automotive Engineers (SAE) and the International Organization for Standardization (ISO), for compliance and standardization. SAE and ISO are international organizations that can certify displays for use in vehicles around the world, ensuring that they meet the standards and regulations of different countries. For instance, ISO has set standards like ISO 16232, which covers the design and performance requirements for in-vehicle information and communication systems, including displays. Similarly, ISO 16255 covers the design and performance requirements for vehicle displays that present safety-related information, such as warnings and alerts. In addition to meeting the standards set by organizations like SAE and ISO, in-car displays must also comply with regulations set by governmental bodies in different countries, such as the Federal Motor Vehicle Safety Standards (FMVSS) in the United States. Such a stringent regulatory framework for car displays is prompting manufacturers to launch displays that meet these standards, ensuring driver and passenger safety, hence bolstering the center stack display market revenue.

Global Center Stack Display Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global center stack display market report, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on display technology, display size, vehicle type, application, and sales channel.

Breakup by Display Technology:

- TFT LCD

- OLED

TFT LCD dominates the market

The report has provided a detailed breakup and analysis of the market based on the display technology. This includes TFT LCD and OLED. According to the report, TFT LCD represented the largest segment.

TFT LCDs have been widely used in various devices, including smartphones, tablets, and automotive displays. In the context of antibiotics, TFT LCDs find application in medical devices, such as diagnostic equipment and patient monitors, where reliable and cost-effective displays are essential. The increasing demand for medical devices and advancements in healthcare infrastructure is driving the growth of this segment.

Besides this, the center stack display market forecast indicates that OLED displays are also gaining popularity due to their superior image quality, flexibility, and energy efficiency. OLED technology is used in high-end smartphones, wearable devices, and other consumer electronics. For instance, in July 2023, MINI, a British automotive brand, launched its new model with the MINI Interaction Unit, which is a round OLED display with a 240 mm diameter. These units are rich colors that blend perfectly into the interior of the new MINI family. Its positioning within the cabin allows it to be used comfortably by the driver and front passenger.

Breakup by Display Size:

- Up to 7 Inch

- More Than 7 Inch

Up to 7 inch dominates the market

The center stack display market report has provided a detailed breakup and analysis of the market based on the display size. This includes up to 7 inch and more than 7 inch. According to the report, up to 7 inch represented the largest segment.

Displays with sizes up to 7 inches find applications in various portable and handheld medical devices, such as point-of-care diagnostic tools, mobile health monitoring devices, and wearable medical technology. The compact form factor and portability of these smaller displays make them ideal for use in various medical settings, facilitating immediate access to critical information and data.

On the other hand, displays larger than 7 inches are employed in more extensive medical equipment and systems, including patient monitoring stations, medical imaging devices, and surgical navigation systems. These larger displays offer greater visual clarity, allowing medical professionals to analyze complex data and images with precision and detail.

Breakup by Vehicle Type:

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

The report has provided a detailed breakup and analysis of the market based on the vehicle type. This includes passenger cars, light commercial vehicles, and heavy commercial vehicles.

The center stack display market statistics by IMARC indicate that passenger cars account for a substantial share of the automotive market, and advancements in display technology have become essential to enhancing the in-car experience for drivers and passengers. Advanced center stack displays in passenger cars offer seamless connectivity, infotainment, and navigation features, elevating the overall driving pleasure and convenience. Such an increase in the ownership of passenger cars is bolstering the deployment of center stack displays.

Furthermore, displays in light commercial vehicles are critical in improving fleet management and vehicle efficiency. These displays provide essential information to drivers, helping them optimize routes, monitor fuel consumption, and comply with safety regulations. Whereas displays for heavy commercial vehicles are instrumental in providing critical data for logistics and fleet management.

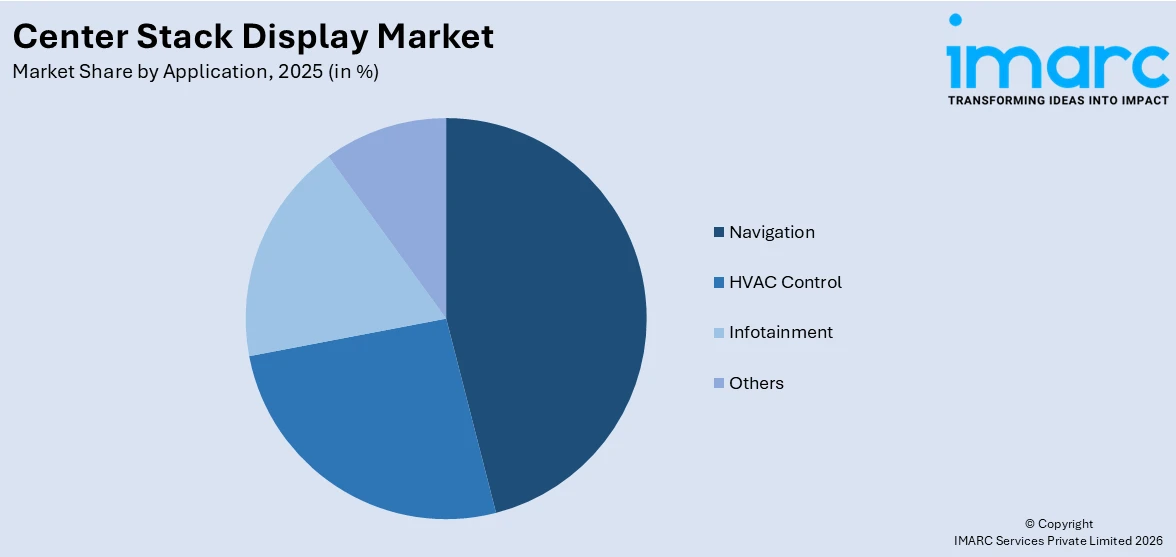

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Navigation

- HVAC Control

- Infotainment

- Others

The report has provided a detailed breakup and analysis of the market based on the application. This includes navigation, HVAC control, infotainment, and others.

Navigation systems, an essential application in vehicles, utilize center stack displays to provide real-time GPS guidance, route optimization, and traffic updates. As the demand for advanced navigation systems increases, the need for high-quality displays with intuitive interfaces also rises, catalyzing the market growth.

Furthermore, HVAC control applications use center stack displays to manage vehicle climate settings, ensuring passenger comfort and efficient energy usage. The demand for sophisticated HVAC control displays is increasing as automakers focus on eco-friendly and energy-efficient vehicle designs.

Breakup by Sales Channel:

- OEM

- Aftermarket

The report has provided a detailed breakup and analysis of the market based on the sales channel. This includes OEM and aftermarket.

OEM sales channel involves the direct supply of displays to vehicle manufacturers during the production process. As automakers continuously seek innovative displays to differentiate their vehicles, partnerships with OEMs to integrate cutting-edge displays become critical. The growing automotive industry and the demand for advanced displays in new vehicles are bolstering the market growth through OEMs.

The aftermarket sales channel provides opportunities for display manufacturers to offer retrofit and upgrade solutions for existing vehicles. Consumers increasingly seek to enhance their driving experience through aftermarket displays that offer advanced infotainment and navigation features. The growing trend of vehicle customization and aftermarket installations further boosts the market growth.

Breakup by Region:

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Asia Pacific exhibits a clear dominance, accounting for the largest center stack display market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, Asia Pacific accounted for the largest market share.

In Asia Pacific, the market is succeeding due to the presence of major automotive manufacturers, a tech-savvy population, and rising consumer preferences for premium in-car features. The expanding automotive industry, particularly in countries like China, Japan, India, and South Korea, is fueling the center stack display market demand. In China, the number of OEMs deploying AI went up by 4% points, from 5% to 9%, during 2017-2018. This growth was accelerated by open-source platforms for AI technology by major technology companies. For instance, the internet giant, Baidu, developed an open-source platform, Apollo, which witnessed partnerships from well over 130 companies. Moreover, India is an emerging economy, and global OEMs are increasingly setting up their manufacturing facilities in India. The demand for automotive center stack displays is strong in India due to the presence of global manufacturers, such as Faurecia SA and BHTC, and the huge aftermarket demand. Furthermore, elevating levels of urbanization, increasing disposable income, and a strong affinity for advanced automotive technologies are propelling the center stack display market’s recent price.

Competitive Landscape:

Top center stack display companies are playing a vital role in strengthening the market growth by continuously innovating and offering cutting-edge display solutions. These companies invest heavily in research and development to develop advanced display technologies, such as high-resolution touchscreens, gesture control, and augmented reality features. Moreover, they focus on creating user-friendly interfaces, seamless integration with other in-car systems, and compatibility with various vehicles to cater to diverse customer needs. By collaborating with automakers and other stakeholders in the automotive industry, these companies ensure that their displays meet industry standards and market demands. Furthermore, the top companies actively monitor market trends and customer preferences to anticipate future requirements and stay ahead of the competition. Through their technological prowess, strategic partnerships, and customer-centric approach, they fuel the adoption of center stack displays, thus strengthening the overall market growth and transforming the driving experience for consumers worldwide.

The report has provided a comprehensive analysis of the competitive landscape in the center stack display market. Detailed profiles of all major companies have also been provided.

- Alps Electric Co. Ltd.

- Continental AG (Schaeffler Technologies AG & Co. KG)

- HARMAN International (Samsung Electronics Co. Ltd.)

- Panasonic Holdings Corporation

- Preh GmbH

- Robert Bosch GmbH

- Visteon Corporation

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

Center Stack Display Market Recent Developments:

- April 2024: Mahindra launched the XUV 3XO (XUV 300 Facelift) with a newly designed dashboard, including a new center console, central AC vents, and displays. The displays are big with a screen size of 10.25 inches.

- January 2024: Tata launched the Tata Punch EV with dual 10.25-inch displays and an updated center console.

- May 2023: Visteon announced the inauguration of India’s first automotive display bonding center in Chennai. The state-of-the-art 13,000-square-foot facility is an expansion to the existing Visteon Electronics India center, allowing the company to better serve its customers in the region and across the globe.

Global Center Stack Display Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Display Technologies Covered | TFT LCD, OLED |

| Display Sizes Covered | Up to 7 Inch, More Than 7 Inch |

| Vehicle Types Covered | Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles |

| Applications Covered | Navigation, HVAC Control, Infotainment, Others |

| Sales Channels Covered | OEM, Aftermarket |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, and Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Alps Electric Co. Ltd., Continental AG (Schaeffler Technologies AG & Co. KG), HARMAN International (Samsung Electronics Co. Ltd.), Panasonic Holdings Corporation, Preh GmbH, Robert Bosch GmbH, Visteon Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the global center stack display market performed so far, and how will it perform in the coming years?

- What are the recent center stack display market opportunities?

- What are the drivers, restraints, and opportunities in the global center stack display market?

- What is the impact of each driver, restraint, and opportunity on the global center stack display market?

- What are the key regional markets?

- Which countries represent the most attractive center stack display market?

- What is the breakup of the market based on the display technology?

- Which is the most attractive display technology in the global center stack display market?

- What is the breakup of the market based on the display size?

- Which is the most attractive display size in the global center stack display market?

- What is the breakup of the market based on the vehicle type?

- Which is the most attractive vehicle type in the global center stack display market?

- What is the breakup of the market based on the application?

- Which is the most attractive application in the global center stack display market?

- What is the breakup of the market based on the sales channel?

- Which is the most attractive sales channel in the global center stack display market?

- What is the competitive structure of the global center stack display market?

- Who are the key players/companies in the global center stack display market?

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the center stack display market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global center stack display market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the center stack display industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)