China Toys Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, End-User, and Province, 2026-2034

China Toys Market Size, Share, Trends & Forecast (2026-2034)

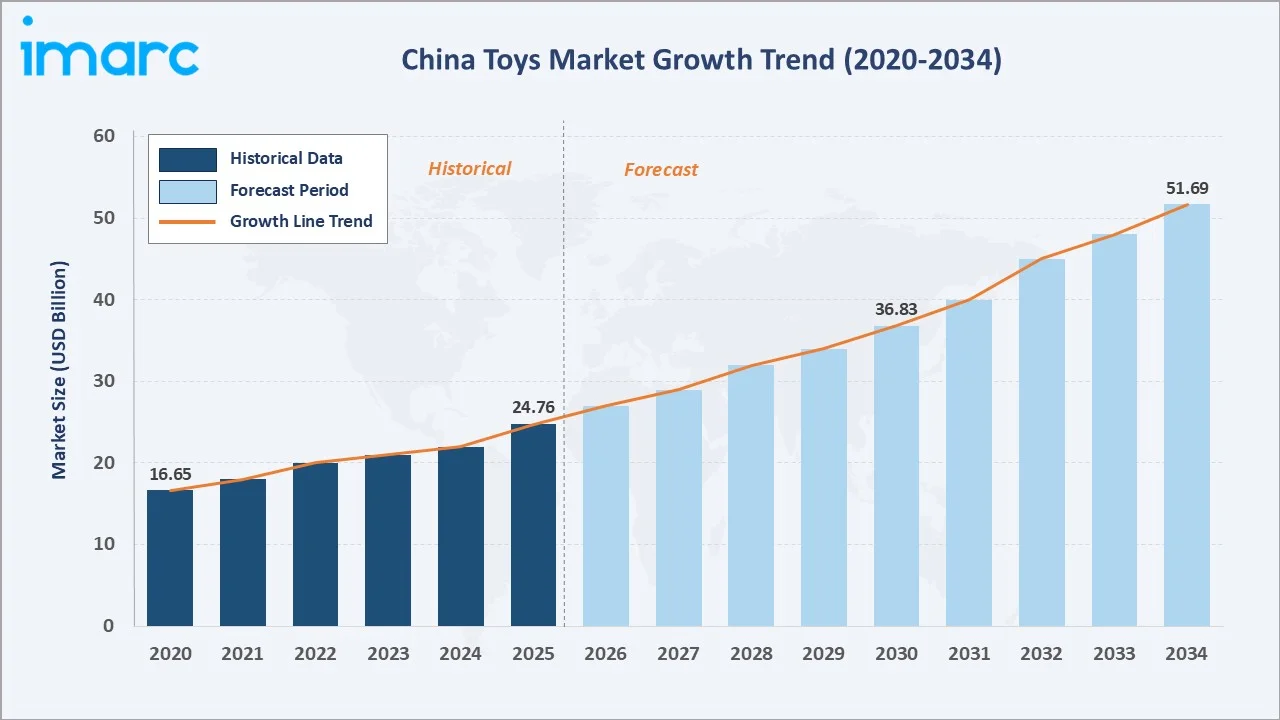

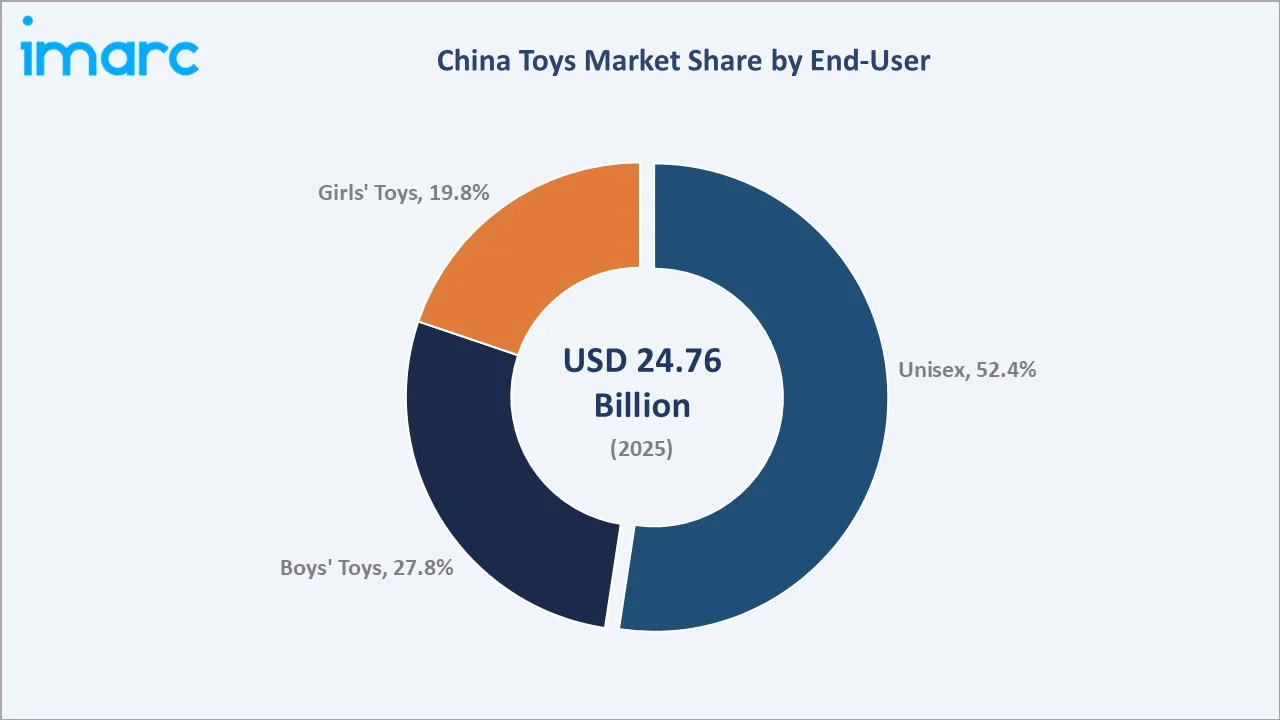

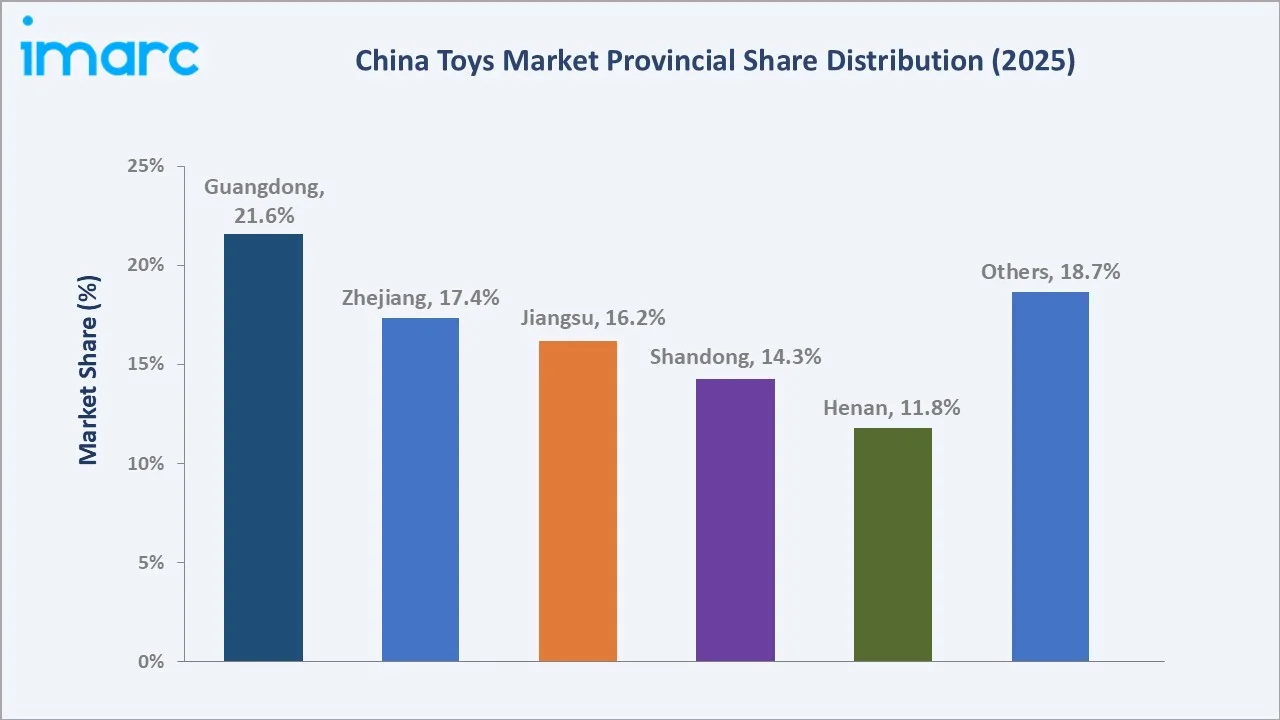

The China toys market was valued at USD 24.76 Billion in 2025 and is projected to reach USD 51.69 Billion by 2034, expanding at a CAGR of 8.26% during 2026-2034. Growth is driven by China’s 58.04 million child population under age five, rising disposable income, premiumizing toy purchasing, STEM and technology-integrated toy adoption, Guochao national brand sentiment driving domestic IP toy demand, and rapid cross-border e-commerce growth. Unisex toys dominate end-user at 52.4%, specialty stores lead distribution at 27.9%, and Guangdong province commands 21.6% of market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 24.76 Billion |

|

Forecast Market Size (2034) |

USD 51.69 Billion |

|

CAGR (2026-2034) |

8.26% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Province |

Guangdong (21.6%, 2025) |

The China toys market growth grew from USD 16.65 Billion in 2020 to USD 24.76 Billion in 2025, driven by COVID-19’s e-commerce acceleration, China’s economic recovery, and the growing middle-class demand for premium educational and electronic toys. Anchored at USD 36.83 Billion in 2030, the forecast to USD 51.69 Billion by 2034.

To get more information on this market, Request Sample

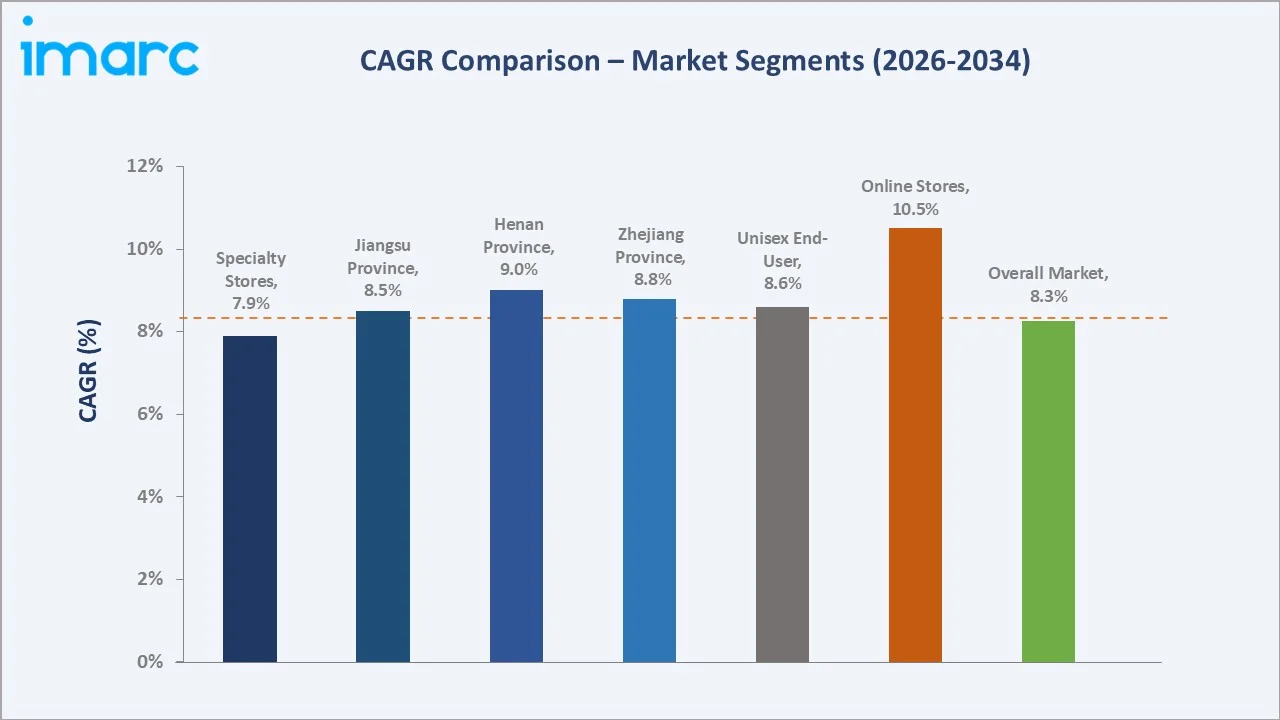

The CAGR across key segments with online stores at ~10.5% CAGR grow fastest by distribution channel, reflecting Douyin’s live-commerce toy sales revolution and JD.com’s same-day logistics enabling impulse toy purchases. Henan province, at ~9.0% CAGR, grows fastest regionally, driven by inland manufacturing expansion, rising rural-to-urban migration, and improving e-commerce infrastructure.

Executive Summary

The China toys market grew from USD 16.65 Billion in 2020 to USD 24.76 Billion in 2025, driven by post-COVID home entertainment demand recovery, the three-child policy’s structural expansion of China’s child population, and China’s rapid premiumization of toy purchasing driven by rising urban household income. China’s toy market is structurally unique in global toys: the world’s largest toy manufacturing base is simultaneously evolving into the world’s fastest-growing major toy consumption market, as Chinese parents transition from viewing toys as commodities to viewing them as developmental tools justifying premium spending.

Unisex toys lead at 52.4% as China’s toy market’s largest segment, encompassing construction toys, board games, puzzles, STEM educational kits, and remote-control vehicles that transcend gender marketing. Specialty stores lead distribution at 27.9% through brand flagship stores. Guangdong’s 21.6% dominance reflects both Shantou’s manufacturing primacy and Guangzhou’s massive consumption market.

Key Market Insights

|

Insight |

Data |

|

Dominant End-User |

Unisex – 52.4% revenue share (2025) |

|

Leading Distribution Channel |

Specialty Stores – 27.9% revenue share (2025) |

|

Leading Province |

Guangdong – 21.6% share (2025) |

Key Analytical Observations Supporting the Above Data:

- Unisex at 52.4% reflecting China’s gender-neutral toy purchasing culture: China’s toy market’s 52.4% unisex dominance is significantly higher than the global average and reflects Chinese parents’ preference for educational and STEM-aligned toys that are marketed on learning benefit rather than gender.

- Specialty stores at 27.9% maintaining leadership through immersive experience: China’s specialty toy retail leadership is sustained by the experiential differentiation that LEGO Certified Stores and ToysRUs China deliver versus the transactional online channel.

- Guangdong at 21.6% as China’s dual manufacturing-consumption epicentre: Guangdong’s 21.6% share uniquely combines supply-side dominance with demand-side scale. Guangdong’s Pearl River Delta toy cluster represents the most vertically integrated single-geography toy ecosystem.

China Toys Market Overview

China’s toy market encompasses the full spectrum of children’s and adult play products, from mass-market plastic toys manufactured in Guangdong’s industrial clusters to premium imported LEGO sets, technology-integrated STEM educational kits, and the rapidly growing adult collectable and blind box segment pioneered by Pop Mart and adopted by international brands. The market serves China’s record of 9.54 million newborns in 2024, an increase of 520,000 compared with 2023, as the primary demographic, with the emerging adult collector segment creating a premium second market.

China’s toy market’s structural distinction from Western toy markets lies in three unique characteristics: the dominant role of e-commerce and live streaming commerce, the primacy of educational positioning in parent-driven purchase decisions, and the Guochao (national trend) consumer movement creating demand for Chinese cultural IP toys that are outgrowing traditional Western brand toy categories in tier-1 cities.

Macro growth drivers include China’s three-child policy demographic expansion, GDP per capita growth enabling toy premiumization, STEM education curriculum integration creating institutional toy purchase cycles, the adult collector economy, and China’s domestic toy IP development. The toy safety regulatory landscape is systematically consolidating manufacturing quality while creating compliance barriers that favor scale manufacturers over informal producers.

Market Dynamics

To evaluate market opportunities, Request Sample

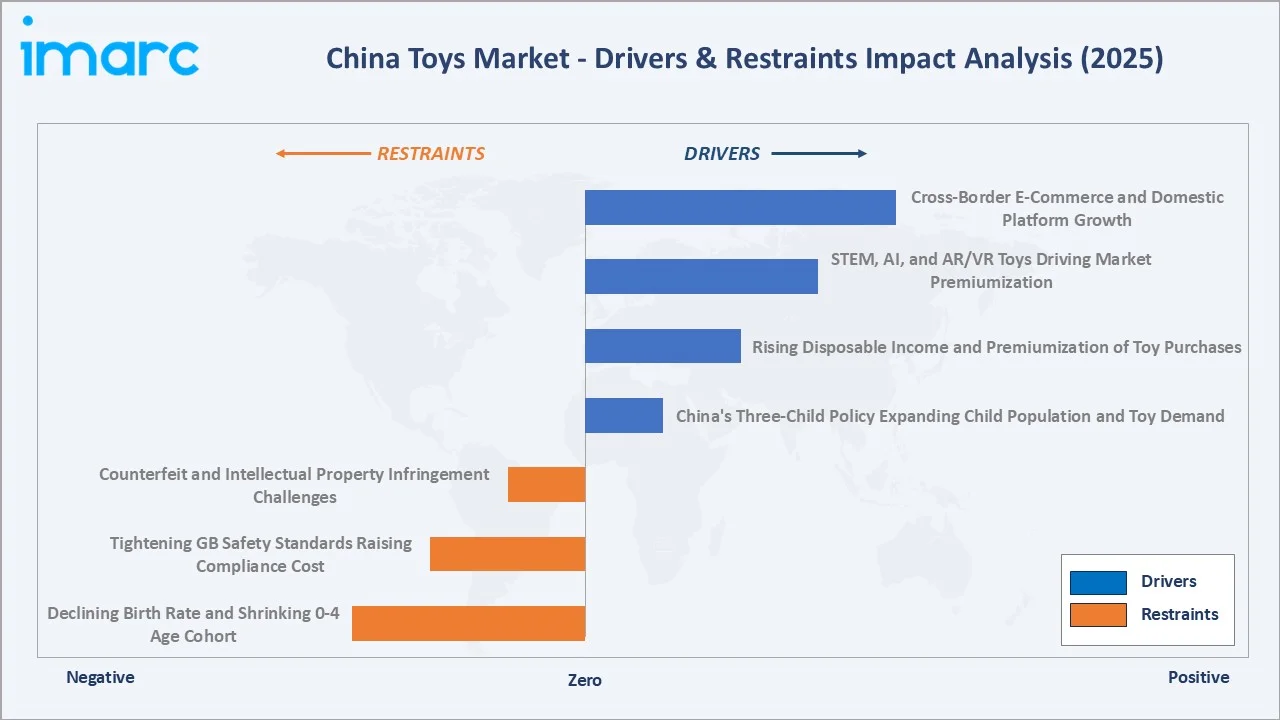

Market Drivers

- China’s Three-Child Policy Expanding Child Population and Toy Demand: China’s government issued the Three-Child Policy (May 2021), accompanied by an accompanying incentive package reversing two decades of population restriction.

- Rising Disposable Income and Premiumization of Toy Purchases: China’s per capita disposable income was 43,377 yuan in 2025, with a growth trajectory that places toy premiumization within reach of urban middle-class consumers.

- STEM, AI, and AR/VR Toys Driving Market Premiumization: The Ministry of Education in China officially added STEM education into the primary school curriculum in 2017, creating institutional demand for educational robots, coding kits, and STEM construction sets that generate China’s highest-ASP toy category.

- Cross-Border E-Commerce and Domestic Platform Growth: China’s cross-border e-commerce toy import market enables Chinese consumers to access LEGO limited editions, Hasbro exclusive collector releases, and European educational toy brands that are unavailable or price-prohibitive in traditional import channels.

Market Restraints

- Declining Birth Rate and Shrinking 0-4 Age Cohort: China’s Total Fertility Rate (TFR) of 1.09, one of the world’s lowest, represents the structural long-term demographic risk for the 0–4 infant and toddler toy segment.

- Tightening GB Safety Standards Raising Compliance Cost: China’s updated GB 6675-2014/Amendment 1 strengthens chemical migration limits for toys’ soft materials, adds mechanical hazard testing for small parts detachment, and extends CCC mandatory certification scope to 38 additional toy categories.

Market Opportunities

- Guochao National Brand Toy Opportunity: China’s Guochao (national trend) consumer movement, where younger Chinese consumers actively prefer domestic brands and Chinese cultural IP over Western equivalents as an expression of national identity, creates a structural market opportunity for Chinese-IP toy products.

- Elderly-Assisted Child Play and Grandparent Gift Economy: China’s family structure creates a multi-generational toy-buying economy where grandparents represent the largest gifting segment by purchase frequency.

Market Challenges

- Supply Chain Disruption and Raw Material Cost Volatility: China’s toy manufacturers are exposed to ABS plastic resin price volatility, rare earth element supply constraints affecting electronic toy components (motors, sensors), and semiconductor availability affecting smart toy production.

- Counterfeit and Intellectual Property Infringement: China’s toy market faces persistent counterfeit challenges, where an estimated 15‐25% of premium toy brand products sold through informal channels in Tier-3 and Tier-4 cities are counterfeit, directly reducing authentic brand owner revenue while creating safety risks from uncertified counterfeit products.

Emerging Market Trends

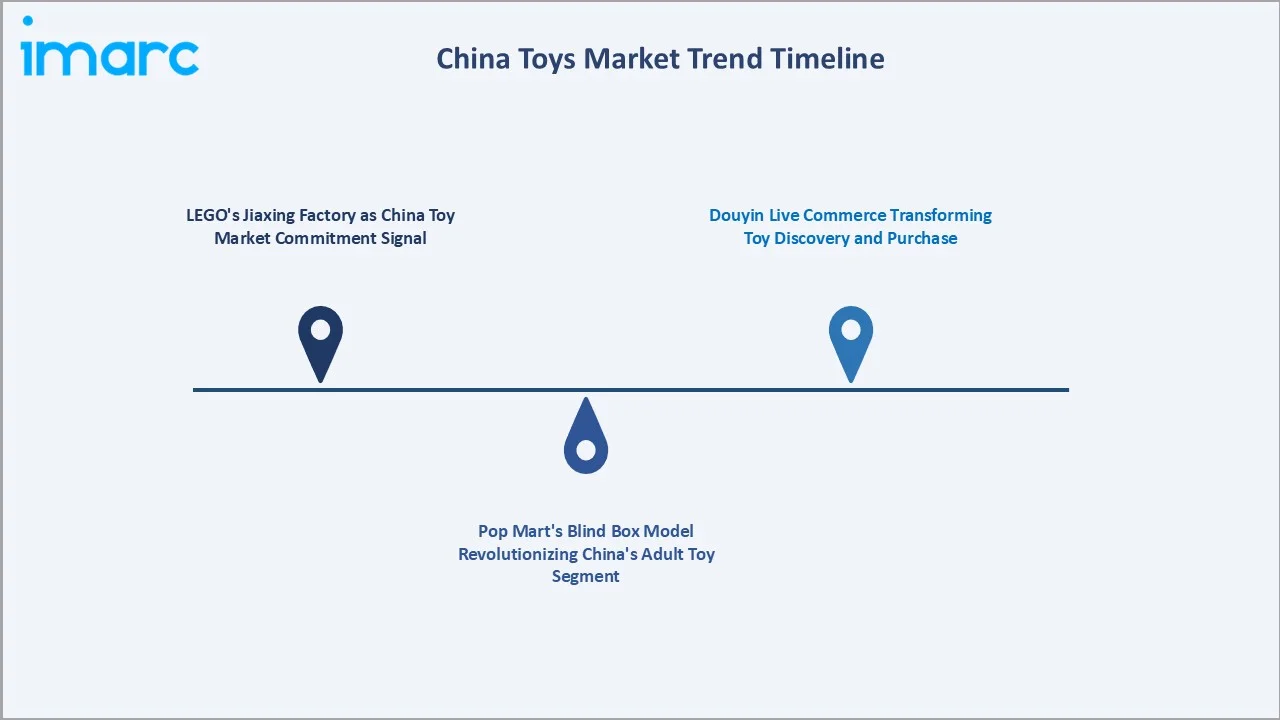

1. LEGO’s Jiaxing Factory as China Toy Market Commitment Signal

In February 2026, LEGO Group launched new products that honor the China’s traditions. The LEGO Galloping Horse Canvas and LEGO Fortune Firecrackers are more than toys; they serve as a cultural bridge during the festive gifting season. This is the single most strategically significant foreign toy company commitment in China’s market history.

2. Pop Mart’s Blind Box Model Revolutionizing China’s Adult Toy Segment

Pop Mart International’s blind box collectible toy model has created the most disruptive toy category innovation in China’s market history: selling mystery-content collectible art toy figurines through gamified purchase mechanics that generate repeat buying behavior from China’s 18–35-year-old consumer base.

3. Douyin Live Commerce Transforming Toy Discovery and Purchase

China’s Douyin live commerce toy market has grown from virtually zero, the world’s fastest-ever retail channel emergence for any consumer goods category. Toy KOL “Unboxing” culture leverages China’s social parenting culture, where parents consult peer recommendations before toy purchase.

Industry Value Chain Analysis

China’s toy industry value chain integrates raw material supply, product design and R&D, manufacturing (the world’s most concentrated toy production cluster), quality certification, multi-channel distribution, and end-user consumption.

|

Stage |

Key Participants |

|

R&D and Design |

Toy concept and product development studios; Chinese gaming companies with toy licensing divisions; domestic IP development studios |

|

Raw Material Procurement |

Plastic resin suppliers; fabric and plush suppliers; electronic components; metal and die-cast; paint and coatings; packaging |

|

Manufacturing |

VTech Holdings Limited, Silverlit Toys Manufactory Ltd., Alpha Group, ZURU |

|

Quality Control |

China Toy & Juvenile Products Association (CTJPA) member certification; SAMR (State Administration for Market Regulation) GB 6675 mandatory safety testing; CCC for toys broadly, including general toys (GB 6675) and electronic toys (GB 19865) |

|

Distribution and Retail |

Specialty toy retail; Online platforms; Supermarkets and hypermarkets; Department stores; cross-border e-commerce |

Toy brands and IP holders capture 35‐50% of total value chain revenue through brand premium and retail margin. China’s OEM manufacturers typically earn 8‐15% net margin on manufacturing-only contracts versus 25‐40% for brands that own the retail IP. The highest-margin value chain tier is IP licensing and collectible toy brand management, where Pop Mart demonstrates 45‐55% gross margins from its designer toy platform. Distribution (retail and online channels) captures 25‐35% of consumer pricing through retail margin. Quality certification and compliance services represent a growing testing services market driven by GB standard expansion.

Technology Landscape in the China Toys Industry

STEM Educational Technology Integration

The Ministry of Education in China officially added STEM education to the primary school curriculum in 2017, creating digital-physical toy convergence where children’s school programming skills become directly applicable to robot toy programming, extending the educational value proposition of STEM toys into formal curriculum alignment.

AI and Voice Interactive Toy Technology

China’s AI toy ecosystem leverages China’s world-leading NLP technology to create voice-interactive educational toys that respond to Mandarin Chinese pronunciation, recognize regional dialect variations, and adapt difficulty based on child age.

Blind Box and Limited Edition Drop Commerce Technology

Pop Mart’s Popmart App creates China’s most sophisticated toy collector ecosystem: real-time inventory tracking for limited drops, secondary market price benchmarking, AR toy display for collection showcase, and blind box probability disclosure.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | Electronic/Remote Control Toys | 🔒 | 2025 |

| Distribution Channel | Specialty Stores | 27.9% | 2025 |

| End-User | Unisex | 52.4% | 2025 |

| Province | Guangdong | 21.6% | 2025 |

By End-User

Unisex toys lead at 52.4% as China’s dominant toy purchase category, reflecting Chinese parents’ educational-primary, gender-secondary purchasing philosophy. Unisex encompasses construction toys, STEM educational kits, board games, puzzles, and remote-control vehicles. The unisex category’s structural advantage in China is that it directly maps to “educational value”, creating an inherently premium purchasing environment where price sensitivity is reduced by developmental narrative.

To access detailed market analysis, Request Sample

Boys’ toys at 27.8% are growing fastest, driven by three premium IP categories: action figures, tech-toy RC and drones, and outdoor battle toys. Girls’ toys at 19.8% anchored by Barbie’s China film-driven renaissance, domestic doll IP, and the premium doll house and fashion accessory segment.

By Distribution Channel

Specialty stores lead at 27.9% through LEGO Certified Stores, ToysRUs China, KidsRobot, and branded flagship stores in Grade-A malls. China’s specialty toy retail’s resilience versus the e-commerce channel’s assault is sustained by the experiential retail model: LEGO stores’ play tables, brick-by-brick customization bars, and interactive LEGO movie experiences create dwell times of 45‐90 minutes per family visit that generate basket sizes 2.5–3.0× higher than online average orders.

Online stores at 24.6% growing fastest via Tmall toy flagship model, JD.com toy category, Douyin live commerce, and Pinduoduo value-market toy segment. Supermarkets and hypermarkets at 18.7% capture China’s impulse toy purchase, seasonal gift and branded toy placement at Walmart China, RT-Mart, and CRV. Departmental stores at 15.3% serve China’s premium toy buyer through curated toy departments. Others at 13.5% includes airport toy retail, hotel gift shops, theme park merchandise, and B2B school and hospital toy procurement.

Regional Market Insights

|

Province |

Share (2025) |

Key Growth Drivers |

|

Guangdong |

21.6% |

Guangdong’s Shantou city generates the largest single-city toy manufacturing cluster, producing dolls, remote-control toys, electronic toys, plastic toys |

|

Zhejiang |

17.4% |

Yiwu International Trade City’s Toy District generates high annual toy wholesale trade through Yiwu’s permanent fair model |

|

Jiangsu |

16.2% |

Nanjing’s premium toy retail market is driven by Jiangsu, the province with one of the highest per-capita disposable incomes, creating an above-average willingness to purchase imported premium toys |

|

Shandong |

14.3% |

Weifang’s Kite Industry generating China’s dominant outdoor kite toy manufacturing cluster |

|

Henan |

11.8% |

Zhengzhou’s Central China transportation hub status – as one of China’s largest inland logistics hubs, generating a toy distribution center concentration that serves China’s inland provinces |

|

Others |

18.7% |

Sichuan, Hubei, Fujian; diverse production profile across 25+ additional provinces |

Guangdong’s 21.6% dominance is simultaneously a manufacturing supply leadership and a consumption demand leadership, a dual role that no other Chinese province replicates at a comparable scale. Shantou’s Chenghai District toy cluster generates more toy product value annually than the entire United Kingdom toy market, positioning Guangdong as the global toy industry’s irreplaceable production epicentre for the foreseeable future.

Zhejiang’s 17.4%, with Yiwu’s International Trade City as the most operationally significant toy wholesale marketplace, and Hangzhou’s Alibaba ecosystem as China’s digital toy commerce infrastructure, creates Zhejiang’s unique position as both a physical and digital toy trade centre. Henan’s 11.8% as China’s fastest-growing interior province toy market reflects Zhengzhou’s cross-border e-commerce pilot zone, creating accelerated premium toy import access for China’s Henan consumers, historically underserved by the import toy retail networks concentrated in coastal tier-1 cities.

Competitive Landscape

China’s toy market exhibits a bicameral competitive structure: the premium foreign brand tier collectively commanding approximately 45‐50% of market revenue through brand premium, IP strength, and product quality positioning; and the domestic brand and OEM tier accounting for 50‐55% of volume-driven market revenue.

|

Company Name |

Product Line |

Market Position |

Core Strength |

|

VTech Holdings Limited |

VTech PAW Patrol Learning Pup Watch – Everest, VTech Gallop & Giggle Horse, VTech Flap & Learn Penguin, VTech Zoo Jamz Hedgehog Tambourine, VTech Baby Snuggle, Jingle & Play Baby Bundle, VTech Get Growing Tractor & Mower Ride-On, VTech Discover & Learn Tablet, VTech Dora More to Explore Learning Laptop, VTech Baby Beep & Go Blocks |

Market Leader |

Hong Kong-headquartered VTech Holdings is leading educational electronic toy company, founded and headquartered in the Greater China region, giving VTech unique cultural and regulatory alignment with China’s toy market |

|

Silverlit Toys Manufactory Ltd. |

Mini Fluff, Snuggle Scoops, LumiMags, Air Wheelz II, RESCUE BEAR, SKY HOVER, FOLDABLE DRONE, SKY AURORA, Mini Hoot, Fizzy Pets |

Market Leader |

Silverlit Toys Manufactory Ltd. is China’s leading remote-control and robotic toy manufacturer, with proprietary electronics design capability that differentiates Silverlit from pure-OEM competitors. |

|

Alpha Group |

Wise Block Police Car, Sky Rover King Helicopter, Wise Block Firetruck, Wise Block Military Vehicle, Wise Block Military Tank, Wise Block Military Helicopter, Wise Block Pavement Roller, Wise Block Off-Road Stunt Racer |

Established |

Alpha Group is China’s leading listed domestic toy company |

|

ZURU |

My Mini Baby Series 1 & 2, My Mini Baby Sweet Hearts, My Mini Baby Disney, Sparkle Girlz Cone Dolls, Sparkle Girlz Styling Heads, Sparkle Girlz Dolls Playsets, Sparkle Girlz Cupcakes, |

Niche Specialist |

ZURU operates China as its primary manufacturing base and one of its fastest-growing consumer markets. |

The market structure is evolving as domestic brands elevate to premium positioning while foreign brands deepen China localization to defend volume share.

Key Company Profiles

VTech Holdings Limited

VTech Holdings is one of China’s leading educational electronic toy companies with unique Greater China origins that provide regulatory, cultural, and operational advantages over toy competitors.

- Product Portfolio: VTech PAW Patrol Learning Pup Watch – Everest, VTech Gallop & Giggle Horse, VTech Flap & Learn Penguin, VTech Zoo Jamz Hedgehog Tambourine, VTech Baby Snuggle, Jingle & Play Baby Bundle, VTech Get Growing Tractor & Mower Ride-On, VTech Discover & Learn Tablet, VTech Dora More to Explore Learning Laptop, VTech Baby Beep & Go Blocks.

- Recent Developments: In February 2026, Vtech launches its newest collection of toys at Toy Fair 2026, spanning early learning, imaginative role-play, music and creative expression.

- Strategic Focus: Children’s GPS tracking device expansion as the safety-conscious Chinese parent market grows; institutional pre-school market expansion through licensed kindergartens adopting digital learning tools.

Alpha Group

Alpha Group, operating its global toy division under the Alpha Toys brand, is one of China's largest publicly listed animation and toy companies.

- Product Portfolio: Wise Block Police Car, Sky Rover King Helicopter, Wise Block Firetruck, Wise Block Military Vehicle, Wise Block Military Tank, Wise Block Military Helicopter, Wise Block Pavement Roller, Wise Block Off-Road Stunt Racer.

- Recent Developments: In March 2024, Alpha Group expanded globally across animation, brand licensing, toys, and consumer goods. At FILMART 2024, AnimationXpress spoke with Echo Jiang, Licensing Director, about their business model, content strategy, and future plans.

- Strategic Focus: Alpha Group operates a pan-entertainment industry chain system integrating animation, toys, licensing, media, film and television, and games with IP as the core, enabling a content-to-toy linkage strategy that differentiates it from pure-play toy manufacturers.

Market Concentration Analysis

China’s toy market is moderately fragmented. The top four foreign brands collectively command approximately 20‐25% of total market revenue, reflecting the market’s vast size relative to any single brand’s addressable consumer base. China’s domestic manufacturers collectively account for 55‐60% of volume-weighted market share but only 30‐35% of revenue-weighted share, reflecting the ASP premium that foreign brands command.

Market concentration is increasing at the premium tier, creating durable competitive advantages that cannot be quickly replicated by domestic challengers. Simultaneously, the adult collectible segment is witnessing concentration, whose IP portfolios generate network effects that smaller collectible brands cannot access.

Investment & Growth Opportunities

Fastest Growing Segments

Online stores channel (~10.5% CAGR), boys’ segment (~9.4% CAGR), adult collectible toys (~20%+ CAGR), STEM/educational technology toys (~15‐18% CAGR), and Guochao domestic IP toys (~25‐35% CAGR from 2025 base) represent China’s toy market’s highest-growth investment vectors.

Emerging Investment Themes

Listed equity access; Private investment: domestic STEM toy startups, blind box collectible IP studios, educational robot companies, strategic themes include China toy IP licensing, cross-border e-commerce toy brand building, and STEM education institutional toy procurement.

- Channel investment: Douyin toy live commerce KOL partnerships, Tmall toy flagship premium positioning, cross-border Tmall Global for imported toy brands entering China market.

- IP development investment: Chinese animation studio partnerships for toy licensing, blind box character IP development, and Chinese cultural heritage IP licensing for toy product development.

Future Market Outlook (2026-2034)

The China toys market is positioned for its most structurally significant and commercially transformative decade. From USD 24.76 Billion in 2025, the market will more than double to USD 51.69 Billion by 2034 at a sustained 8.26% CAGR, making China the world’s undisputed largest single-country toy market by absolute value.

Three structural forces define this growth path with exceptional confidence. First, China’s toy premiumization trajectory is an economic certainty driven by math, creating a 3–4× per-capita spending gap that income growth, the three-child policy, household size expansion, and Guochao brand confidence will systematically close through 2034. Second, China’s adult collector economy represents the toy market’s most durable structural growth engine because adult collector purchasing is income-driven, discretionary-premium, and culturally accelerating as China’s creative economy matures. Third, China’s STEM education mandate creates an institutional toy market within the school system that is effectively recession-proof.

Research Methodology

Primary Research

Primary research included 125+ structured interviews with China toys industry stakeholders in 2025, comprising OEM and branded toy manufacturer commercial directors, toy retail category managers, SAMR toy quality enforcement officers, CNTOYS (China National Toy and Juvenile Products Association) executive board members, educational institution toy procurement managers, and independent China toy industry analysts.

Secondary Research

Secondary research encompassed SAMR national toy quality supervision annual reports, CNTOYS toy industry statistical yearbook, GACC China toy export customs data, MOFCOM China toy retail sales statistical data, IMARC China toys market intelligence database, company annual reports, Tmall and JD.com platform toy category data publications, and ChinaJoy game-toy convergence market reports. Over 115 secondary sources reviewed.

Forecasting Models

IMARC’s Bottom-Up and Top-Down dual estimation methodology was applied. Bottom-Up aggregates China's toy market revenue by end user, distribution channel, and province, weighted by per capita toy spending trajectories, e-commerce penetration growth curves, provincial income convergence models, and birth rate demographic adjustments for the 2026–2034 primary toy consumer age cohort. Top-Down validates against China’s total consumer goods retail growth, children’s product category share, toy import/export statistics, and comparable per capita toy spending benchmarks from Japan and South Korea’s mid-tier income development phases.

China Toys Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Plush Toys, Electronic/Remote Control Toys, Games And Puzzles, Construction And Building Toys, Dolls, Ride-Ons, Sports & Outdoor Play Toys, Infant/Pre-School Toys, Activity Toys, Others |

| End Users Covered | Unisex, Boys, Girls |

| Distribution Channels Covered | Specialty Stores, Supermarkets and Hypermarkets, Departmental Stores, Online Stores, Others |

| Province Covered | Guangdong, Jiangsu, Shandong, Zhejiang, Henan, Others |

| Companies Covered | VTech Holdings Limited, Silverlit Toys Manufactory Ltd., Alpha Group, ZURU, Ltd. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the China toys market from 2020-2034.

- The China toys market research report provides the latest information on the market drivers, challenges, and opportunities in the regional market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key markets within each province.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the China toys industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the China Toys Market Report

The China toys market was valued at USD 24.76 Billion in 2025 and is projected to reach USD 51.69 Billion by 2034.

The China toys market is forecast to grow at a CAGR of 8.26% during 2026-2034, driven by the three-child policy demographic expansion, rising disposable income premiumization, STEM education mandate, Guochao domestic IP development, and Douyin live commerce channel growth.

Unisex leads with 52.4% revenue share (2025), reflecting Chinese parents’ educational-primary purchasing philosophy where STEM construction toys, board games, and remote-control vehicles transcend gender marketing.

Specialty stores lead with 27.9% share (2025), driven by LEGO Certified Stores, ToysRUs China, and experiential brand flagship stores generating 2.5–3.0× higher basket size than online channels.

Guangdong leads with 21.6% share (2025), combining Shantou’s toy manufacturers with Guangzhou and Shenzhen’s massive premium consumption markets.

Key companies include VTech Holdings Limited, Silverlit Toys Manufactory Ltd., Alpha Group, and ZURU.

Key drivers include the Three-Child Policy expanding child household multiplier, rising disposable income enabling toy premiumization, STEM education national curriculum creating institutional toy demand, Guochao domestic IP toy movement, and Douyin live commerce.

Key trends include LEGO’s Jiaxing factory China localization, Pop Mart blind box adult collectible revolution, DJI tech-toy STEM crossover, Douyin live commerce toy channel disruption, Guochao domestic IP toy development, and the China Kidult economy.

Key challenges include declining birth rate structural long-term risk for infant toy segment, counterfeit toy IP infringement, tightening GB safety standards raising SME compliance cost, and Tmall/Douyin traffic cost inflation compressing online channel margins.

Top opportunities include Alpha Group listed equity, domestic STEM toy startup investment, Douyin live commerce toy brand partnership, adult collectible IP development, cross-border Tmall Global for imported toy brands, and China toy factory GB 6675 compliance technology platform investment.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)