Cloud Kitchen Market Size, Share, Trends and Forecast by Type, Product Type, Nature, and Region, 2026-2034

Global Cloud Kitchen Market Size, Share, Trends & Forecast (2026-2034)

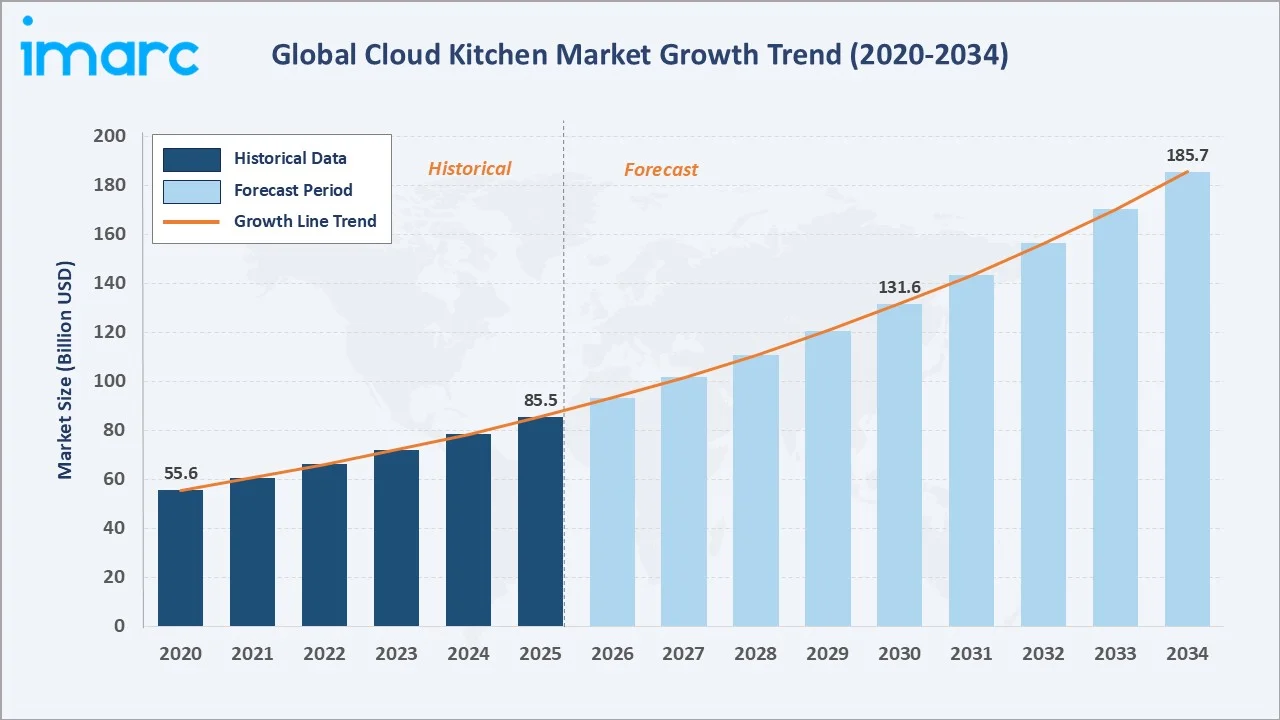

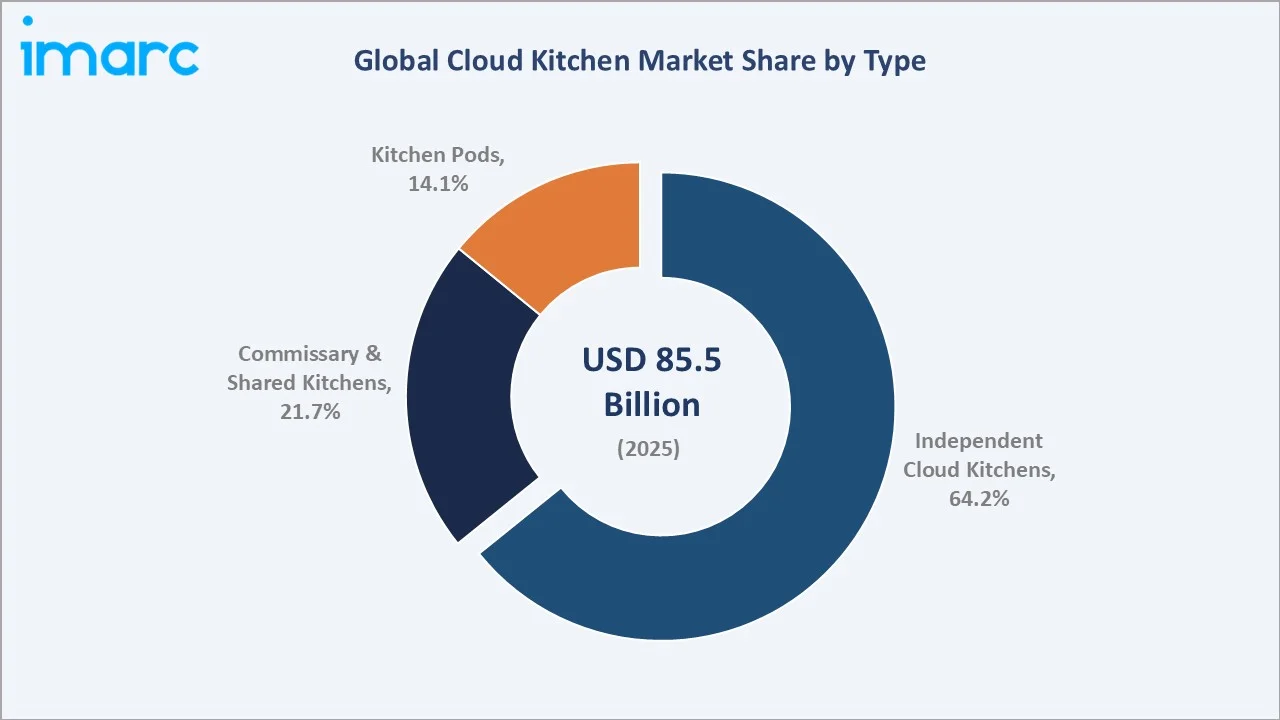

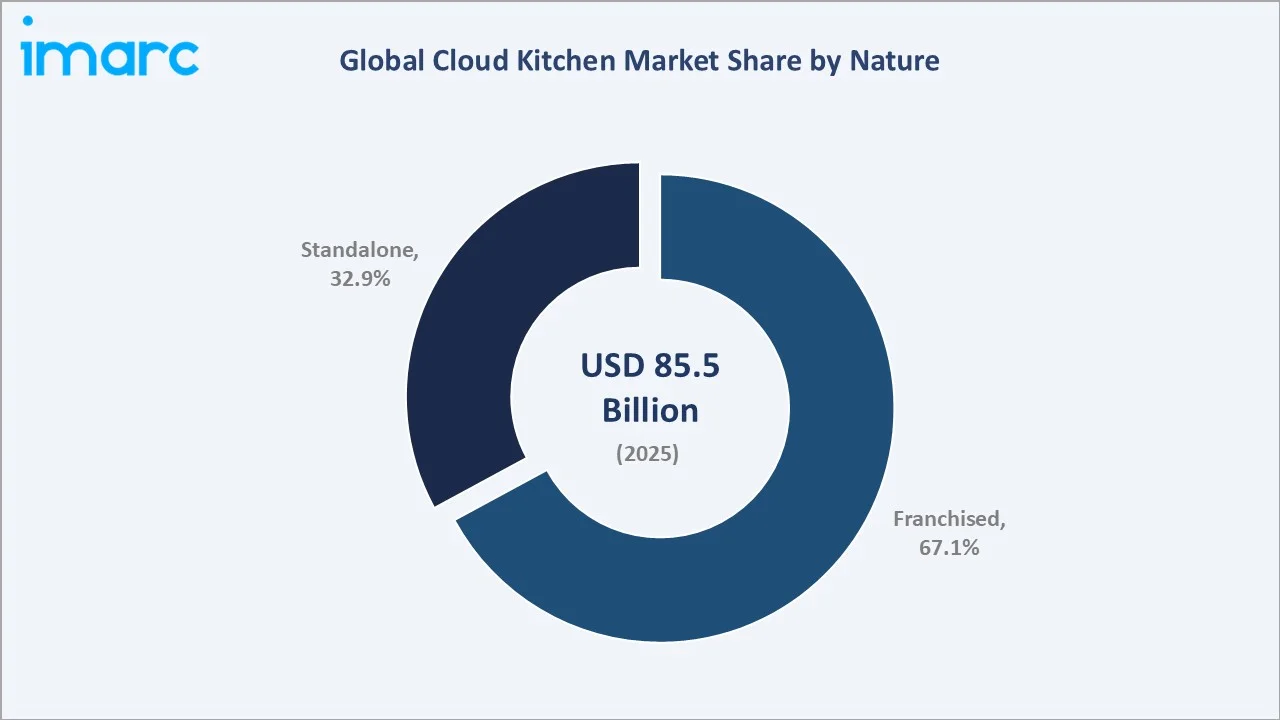

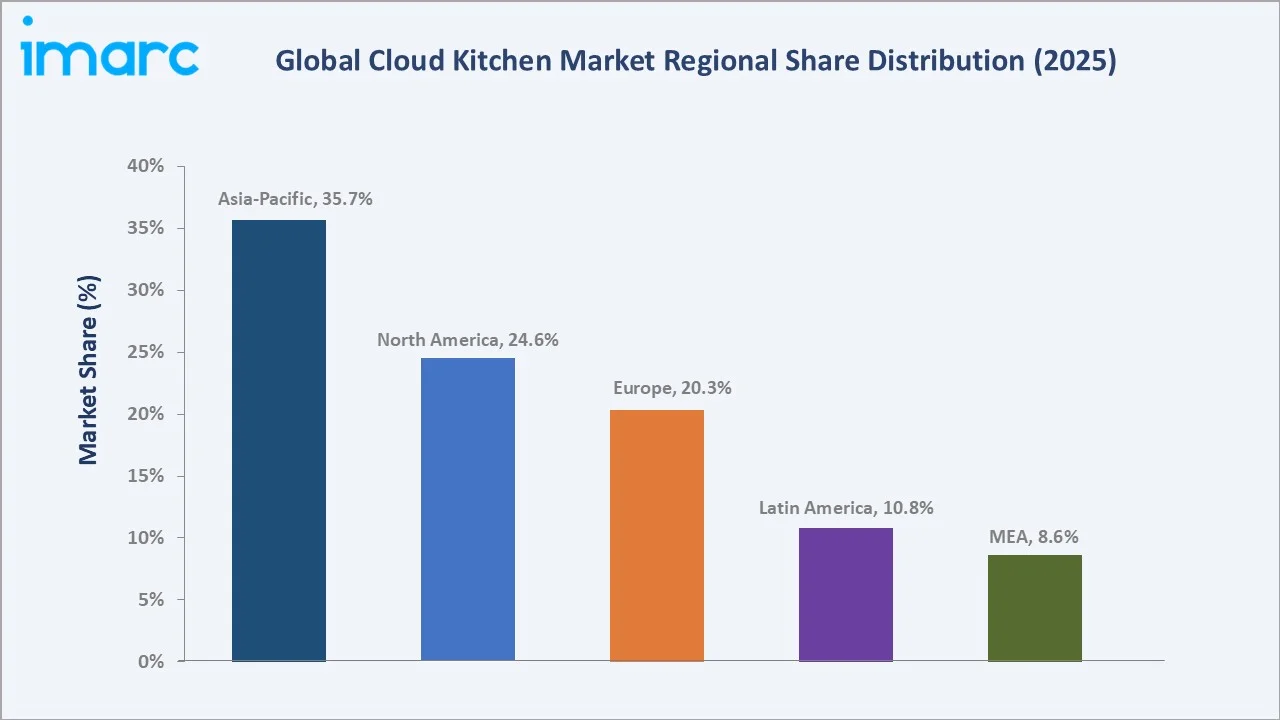

The global cloud kitchen market was valued at USD 85.5 Billion in 2025 and is projected to reach USD 185.7 Billion by 2034, expanding at a CAGR of 9.0% during the forecast period 2026-2034. Growth is driven by surging online food delivery demand, with 12% of India’s food delivery market as of July 2024, low capital requirements versus traditional restaurants, AI-powered menu optimization, and rapid urbanization across Asia-Pacific and emerging markets. Independent cloud kitchens dominate at 64.2% type share, while franchised operators lead at 67.1% by nature. Asia-Pacific commands 35.7% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 85.5 Billion |

|

Forecast Market Size (2034) |

USD 185.7 Billion |

|

CAGR (2026-2034) |

9.0% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Region |

Asia-Pacific (35.7%, 2025) |

|

Fastest Growing Region |

Middle East & Africa (CAGR ~11.2%, 2026-2034) |

The global cloud kitchen market expanded from USD 55.6 Billion in 2020 to USD 85.5 Billion in 2025, propelled by COVID-19 accelerated food delivery demand, the post-pandemic normalization of digital ordering behaviour, and rising urbanization across emerging economies. Anchored at USD 131.6 Billion in 2030, the market is forecast to reach USD 185.7 Billion by 2034, supported by the continued proliferation of delivery platforms, declining logistics costs, and multi-brand virtual restaurant models operated by food tech entrepreneurs.

To get more information on this market, Request Sample

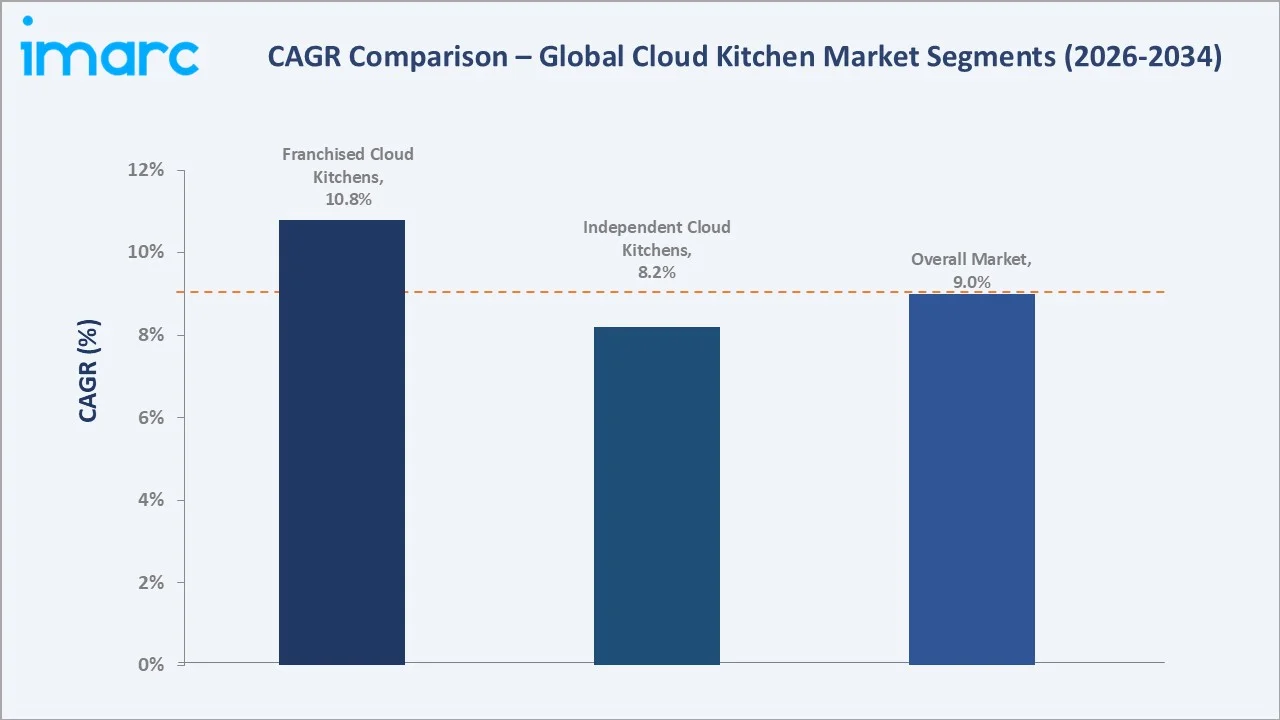

The CAGR across key segments reflects strong structural tailwinds: franchised cloud kitchen models growing at ~10.8% CAGR as established food brands rapidly expand delivery-only footprints, and independent operators growing at ~8.2% CAGR driven by low entry barriers and digital marketplace access. Asia Pacific is the fastest-growing regional market, supported by the emerging trend of co-working kitchen spaces, AI-enabled cooking automation, and subscription meal delivery models gaining mainstream adoption.

Executive Summary

The global cloud kitchen market grew from USD 55.6 Billion in 2020 to USD 85.5 Billion in 2025, propelled by COVID-19’s permanent transformation of food consumption habits, the global democratization of food delivery infrastructure, and the emergence of purpose-built cloud kitchen real estate operators also termed ghost kitchens, dark kitchens, or virtual restaurants operate exclusively for delivery orders without customer-facing dining space, reducing break-even costs, while accessing delivery platform audiences.

The market’s trajectory to USD 185.7 Billion by 2034 at a 9.0% CAGR is anchored by four compounding structural forces: online food delivery becoming a daily habit with 1 in 3 customers in the US use online food ordering services at least twice in a week; the franchise model’s superior unit economics enabling brand-proven operators to scale without proportional capital deployment; kitchen pod technology disrupting secondary city penetration where traditional shared kitchen economics were previously unviable.

Independent cloud kitchens at 64.2% reflect the model’s dominant adoption form, single operators or restaurant groups converting existing commercial kitchen space into delivery-only production facilities without the overhead of commissary infrastructure sharing. Franchised operators at 67.1% demonstrate that brand-leveraged franchise models, where proven food brands license their IP to cloud kitchen operators across delivery platforms, generate superior revenue predictability and customer acquisition cost efficiency versus standalone virtual brands built from scratch. Asia-Pacific’s 35.7% dominance reflects China’s and India’s food delivery platform scale providing the demand foundation that makes Asian cloud kitchen economics globally most favorable.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Independent Cloud Kitchen – 64.2% share (2025) |

|

Dominant Nature |

Franchised – 67.1% share (2025) |

|

Leading Region |

Asia-Pacific – 35.7% share (2025) |

|

Fastest Growing Region |

Middle East & Africa (CAGR ~11.2%, 2026-2034) |

Key Analytical Observations Supporting The Above Data:

- Independent cloud kitchen at 64.2% (2025): The independent model’s dominance reflects the global restaurant industry’s pragmatic adoption of delivery-only operations as a margin improvement strategy. Over 13% of restaurants operate one or more virtual brands, generating incremental revenue from existing kitchen infrastructure with zero additional rent.

- Franchised model at 67.1% driven by proven brand risk reduction: The franchised cloud kitchen model, where established F&B brands license their concepts to cloud kitchen operators for delivery-only production, commands 67.1% market share because brand recognition dramatically reduces customer acquisition cost on delivery platforms.

- Asia-Pacific at 35.7% anchored by China and India delivery scale: China’s Meituan is the world’s single largest cloud kitchen demand aggregator, supporting cloud kitchen operators across tier-1 through tier-4 Chinese cities. In 2025, India’s Swiggy customers placed 93 million orders for biryanis, averaging 194 plates per minute, or 3.25 every second, representing high demand in GMV for cloud kitchen and restaurant partners.

Global Cloud Kitchen Market Overview

Cloud kitchens are professional food production facilities operating exclusively for delivery and takeout without customer-facing dining areas, enabling restaurant operators to serve delivery platform consumers at significantly lower fixed costs than traditional restaurants. The global cloud kitchen ecosystem integrates food and ingredient procurement networks, kitchen infrastructure operators (shared, independent, pod), multi-brand virtual restaurant platforms, food delivery aggregators, restaurant technology providers, and end consumers ordering via mobile applications.

Three distinct operational models define the market: independent cloud kitchens (single or multi-brand operators using their own or leased commercial kitchen space for delivery-only production); commissary or shared kitchens (multiple operators sharing central production infrastructure, equipment, and overhead); and kitchen pods (modular, self-contained pre-fabricated units deployed in high-demand locations).

Applications span all food service categories, from fast-casual burgers and pizza to premium molecular gastronomy available only through delivery, serving urban millennial and Gen Z consumers. Macroeconomic drivers include global smartphone penetration reached 5.78 billion users, 5G connectivity enabling sub-30-minute delivery tracking, urban density creating delivery route economics, COVID-19’s permanent behavioral shift to home dining and rising restaurant real estate costs making delivery-only models financially superior in Tier-1 cities globally.

Market Dynamics

To evaluate market opportunities, Request Sample

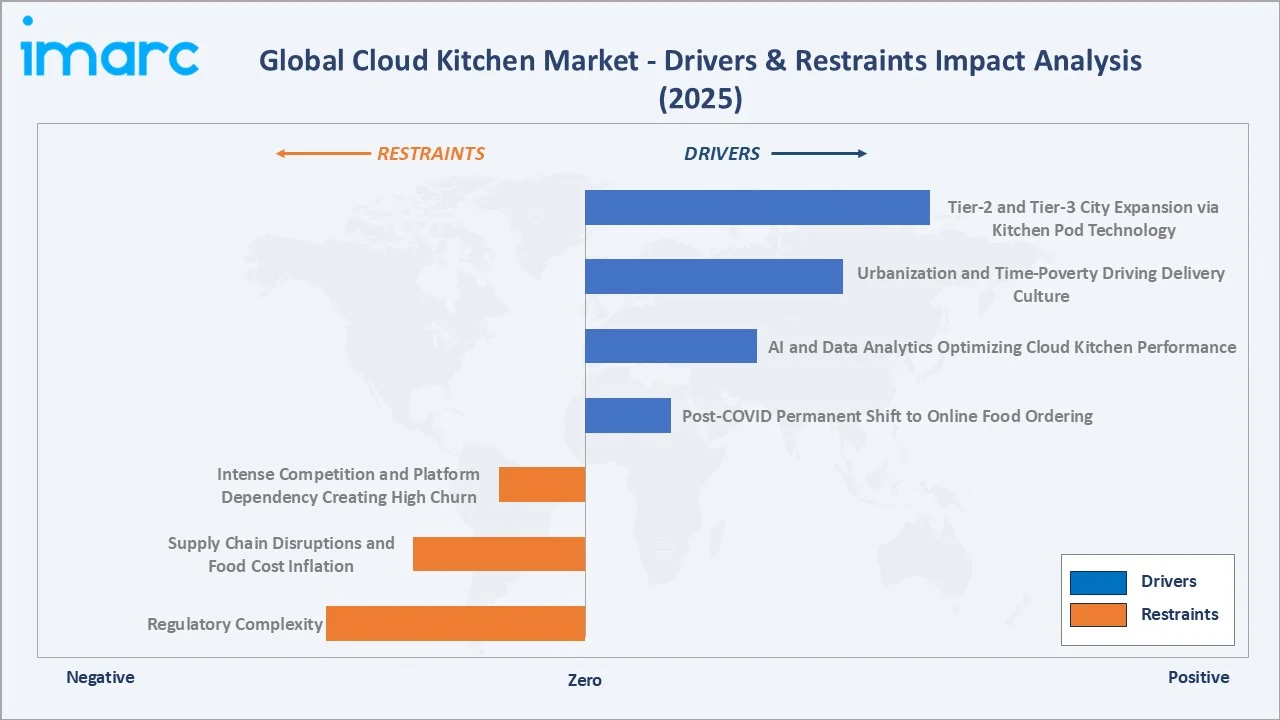

Market Drivers

- Post-COVID Permanent Shift to Online Food Ordering as Daily Habit: COVID-19’s 18-month global restaurant closure forced consumers to adopt food delivery for the first time.

- AI and Data Analytics Optimizing Cloud Kitchen Performance: Delivery platform AI, Swiggy’s Artificial Intelligence for Restaurants, DoorDash’s Merchant Analytics, provides cloud kitchen operators with hyperlocal demand forecasting, real-time menu pricing optimization, and customer preference segmentation that traditional restaurants cannot access.

- Urbanization and Time-Poverty Driving Delivery Culture: Global urban population reaching 4.4 billion, 56% of the world, creates an ever-expanding cloud kitchen addressable market.

Market Restraints

- Intense Competition and Platform Dependency Creating High Churn: Global food delivery platforms charge cloud kitchen operators 15–30% commission on each order, creating margin compression that makes profitability elusive for operators without volume scale or premium pricing power.

- Supply Chain Disruptions and Food Cost Inflation: Global food commodity price volatility disproportionately impacts cloud kitchens versus traditional restaurants because cloud kitchens operate on tighter margins with less pricing power.

- Regulatory Complexity and Health Code Compliance Across Geographies: Cloud kitchen operators scaling across multiple countries face incompatible food safety, labeling, and business license requirements: India’s FSSAI requires separate cloud kitchen registration per operational location; the UK’s FSA Food Hygiene Rating scheme applies to cloud kitchens with public-facing hygiene scores that directly impact delivery platform search ranking.

Market Opportunities

- Tier-2 and Tier-3 City Expansion via Kitchen Pod Technology: The cities globally with high populations represent the next cloud kitchen expansion frontier, where delivery platforms have achieved order density but traditional shared kitchen infrastructure economics remain unviable.

- Corporate and B2B Meal Delivery as Premium Cloud Kitchen Market: Corporate catering with 48% growth and B2B meal delivery, where companies contract cloud kitchen operators for employee breakfast, lunch, and event catering olean higher average order values, lower churn, and predictable demand that enables precision kitchen scheduling.

Market Challenges

- Customer Discovery and Brand Building Without Physical Presence: Traditional restaurants build brand equity through signage, streetfront visibility, and dine-in experience, cumulative physical presence that creates top-of-mind awareness in local communities. Cloud kitchen virtual brands depend entirely on delivery platform search algorithms, digital marketing spend, and user-generated reviews to drive discovery.

- Food Quality and Temperature Control During Delivery: Cloud kitchen menu development is constrained by delivery-friendly food science; not all menu items survive 30–45-minute delivery journeys without quality degradation that generates negative reviews.

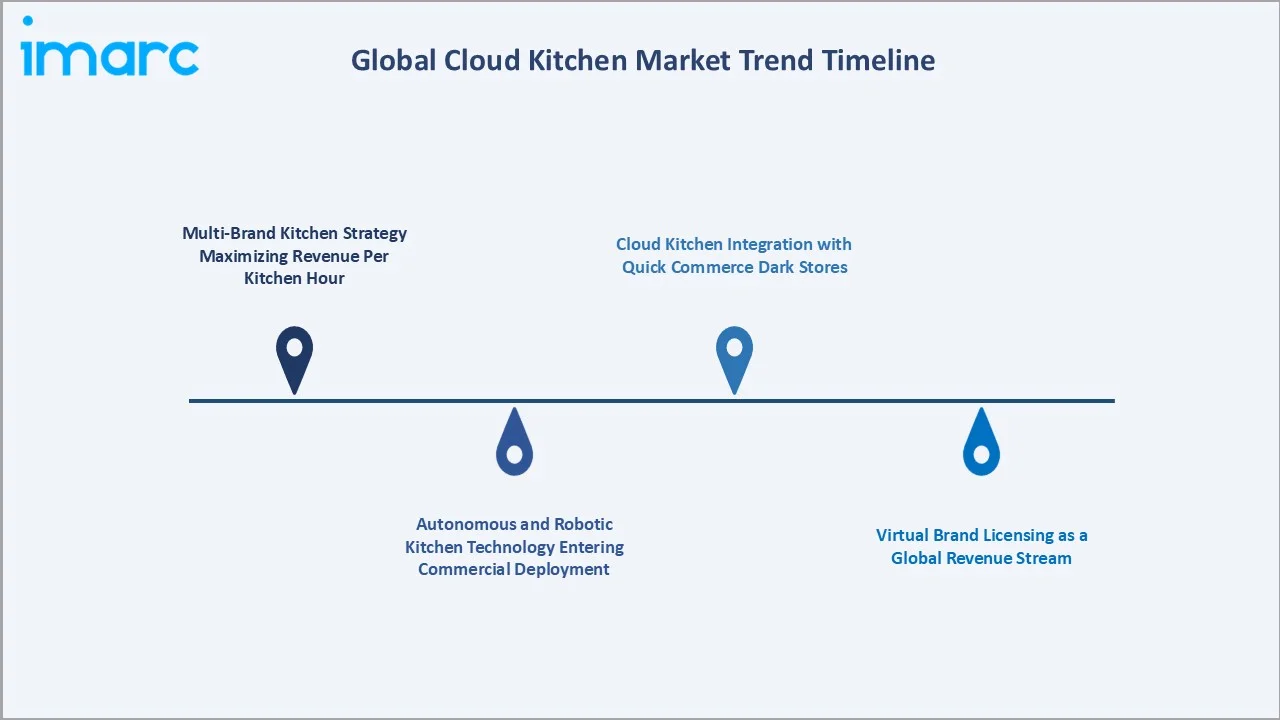

Emerging Market Trends

1. Multi-Brand Kitchen Strategy Maximizing Revenue Per Kitchen Hour

The multi-brand cloud kitchen model, where a single kitchen simultaneously operates more virtual restaurant brands targeting different cuisine categories, price points, and consumer segments, is becoming the dominant profitability strategy for cloud kitchen operators globally.

2. Autonomous and Robotic Kitchen Technology Entering Commercial Deployment

Robotic kitchen technology, automated cooking arms, computer vision quality control, and AI-driven order management are entering commercial cloud kitchen deployment as labour cost management becomes critical. Miso Robotics’ Flippy robotic kitchen assistant has been deployed in cloud kitchens, reducing fry station labour while maintaining consistent cooking quality. .

3. Virtual Brand Licensing as a Global Revenue Stream

Virtual brand licensing, where established restaurant brands license their menu IP to cloud kitchen operators globally for delivery-only production without any physical franchise investment, is creating a new global food IP industry.

4. Cloud Kitchen Integration with Quick Commerce Dark Stores

The operational synergy between cloud kitchens (food delivery) and quick commerce dark stores (grocery and FMCG delivery) is creating a hybrid delivery infrastructure model that reduces last-mile logistics costs through shared rider networks and co-located facilities. Swiggy’s Instamart dark stores are co-located with cloud kitchen hubs in Indian cities, enabling shared rider dispatch that achieves lower per-delivery cost versus separate food and grocery delivery fleets.

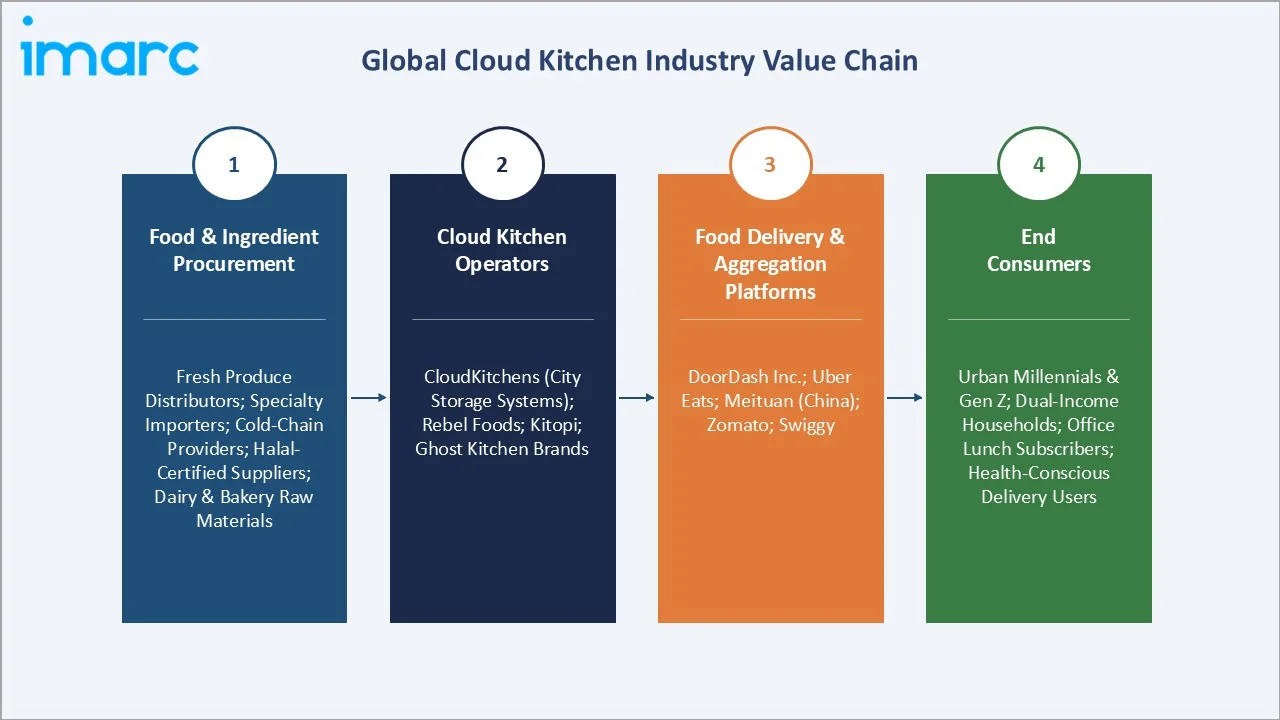

Industry Value Chain Analysis

The global cloud kitchen value chain spans ingredient procurement, kitchen production infrastructure, technology enablement, delivery logistics, and consumer mobile ordering across five distinct operational stages.

|

Stage |

Key Participants |

|

Food & Ingredient Procurement |

Fresh produce distributors; local wholesale markets; specialty ingredient importers; cold-chain logistics providers; agri-tech suppliers; direct farmer networks in Asia; halal-certified meat suppliers; dairy and bakery raw material suppliers |

|

Cloud Kitchen Operators |

CloudKitchens; Rebel Foods; Kitopi |

|

Food Delivery & Aggregation Platforms |

DoorDash Inc, Uber Eats, Zomato, Swiggy |

|

End Consumers |

Urbanized millennials (25–40) and Gen Z food delivery super-users; dual-income households; office lunch delivery subscribers; late-night demand consumers; health-conscious users ordering specialized cuisine (keto, vegan, allergen-free); emerging market mobile-first consumers |

Cloud kitchen operators capture the highest per-order gross margin in the value chain at 30–45% of order value, while delivery platforms extract 15–30% commission from each transaction. Technology providers generate 3–6% of restaurant GMV in SaaS subscription and transaction fees. The most profitable position in the value chain is vertically integrated operators that eliminate platform commissions on their own brands while charging full commission on third-party brands.

Technology Landscape in the Global Cloud Kitchen Industry

Cloud POS and Multi-Platform Order Management

Cloud kitchen operators managing simultaneous orders from DoorDash, Uber Eats, Swiggy, and Zomato require unified order management systems that consolidate multi-platform orders into a single kitchen display workflow.

Robotic Kitchen Automation and Computer Vision Quality Control

Commercial robotic kitchen technology is transitioning from pilot to scale deployment across cloud kitchen chains. Computer vision systems monitor food production quality in real time, alerting kitchen managers to preparation errors before order dispatch.

Sustainable Packaging and Cold-Chain Delivery Innovation

Cloud kitchen packaging technology is evolving to address food quality maintenance, environmental sustainability, and consumer experience simultaneously. Novatek International’s modified atmosphere packaging maintains the crispy texture of fried foods versus standard packaging.

Market Segmentation Analysis

By Type

Independent cloud kitchens lead at 64.2% market share (2025). This category’s dominance reflects the global restaurant industry’s pragmatic conversion of existing commercial kitchen space to delivery-only operations, a model that requires minimal new capital while immediately accessing the growing delivery platform consumer base.

To access detailed market analysis, Request Sample

Commissary and shared kitchens at 21.7% represent the commercial kitchen sharing model where regional operators lease kitchen pods to multiple operators, sharing industrial-grade equipment, cleaning services, and receiving infrastructure. Kitchen pods at 14.1% are the fastest-growing type at ~11.2% CAGR as modular kitchen technology democratizes cloud kitchen geography beyond major metropolitan markets.

By Nature

Franchised cloud kitchens lead at 67.1% market share (2025). The franchised model’s dominance is structural: established food brands’ existing consumer recognition on delivery platforms eliminates the single biggest barrier to cloud kitchen profitability – customer discovery cost. A franchised brand achieves that same order volume within days of platform onboarding due to existing consumer demand.

Standalone cloud kitchens at 32.9% serve culinary entrepreneurs, restaurant groups experimenting with delivery-native concepts, and food-tech startups building proprietary virtual brands. The standalone model’s growth at ~9.8% CAGR – slightly above the overall market CAGR, reflects the emergence of successful standalone virtual brands achieving sufficient scale to create their own consumer loyalty independent of franchise parent brand recognition.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

35.7% |

China’s Meituan-dominated dark kitchen ecosystem with food delivery users; India’s Swiggy and Zomato duopoly supporting cloud kitchen operators |

|

North America |

24.6% |

The USA’s restaurant industry, with high cloud kitchen penetration, DoorDash's US delivery market share is creating demand capture for virtual brands |

|

Europe |

20.3% |

UK’s Deliveroo-dominated market with virtual restaurant brands; Germany’s Delivery Hero cloud kitchen expansion; France’s Uber Eats-Deliveroo competition driving virtual brand proliferation |

|

Latin America |

10.8% |

Brazil’s iFood platform enabling high cloud kitchen operators; Mexico’s Rappi and DiDi Food supporting virtual brand growth in CDMX and Monterrey |

|

Middle East & Africa |

8.6% |

UAE’s Dubai and Abu Dhabi as MENA cloud kitchen capital; Saudi Arabia’s Vision 2030-aligned food-tech investment supporting cloud kitchen expansion |

Asia-Pacific’s 35.7% dominance is underscored by China’s Meituan daily orders and India’s Swiggy-Zomato daily orders, with Swiggy clocking over 1,80,000 orders daily. The APAC cloud kitchen market is unique globally in its platform-operator-consumer density, mega-cities of 5–20+ million people with per-capita delivery ordering rates of 150–300 times annually create cloud kitchen unit economics that are 2–3× more favorable than equivalent US or European markets.

North America’s 24.6% is dominated by CloudKitchens’ real estate platform and DoorDash’s delivery infrastructure, creating the world’s most sophisticated cloud kitchen ecosystem. The US cloud kitchen market is distinctively technology-driven, with AI-powered virtual brand management, robotic kitchen automation pilots, and vertical integration between delivery platforms and kitchen operators being most advanced in the US market, creating innovation that cascades to global markets with 2–3-year lag.

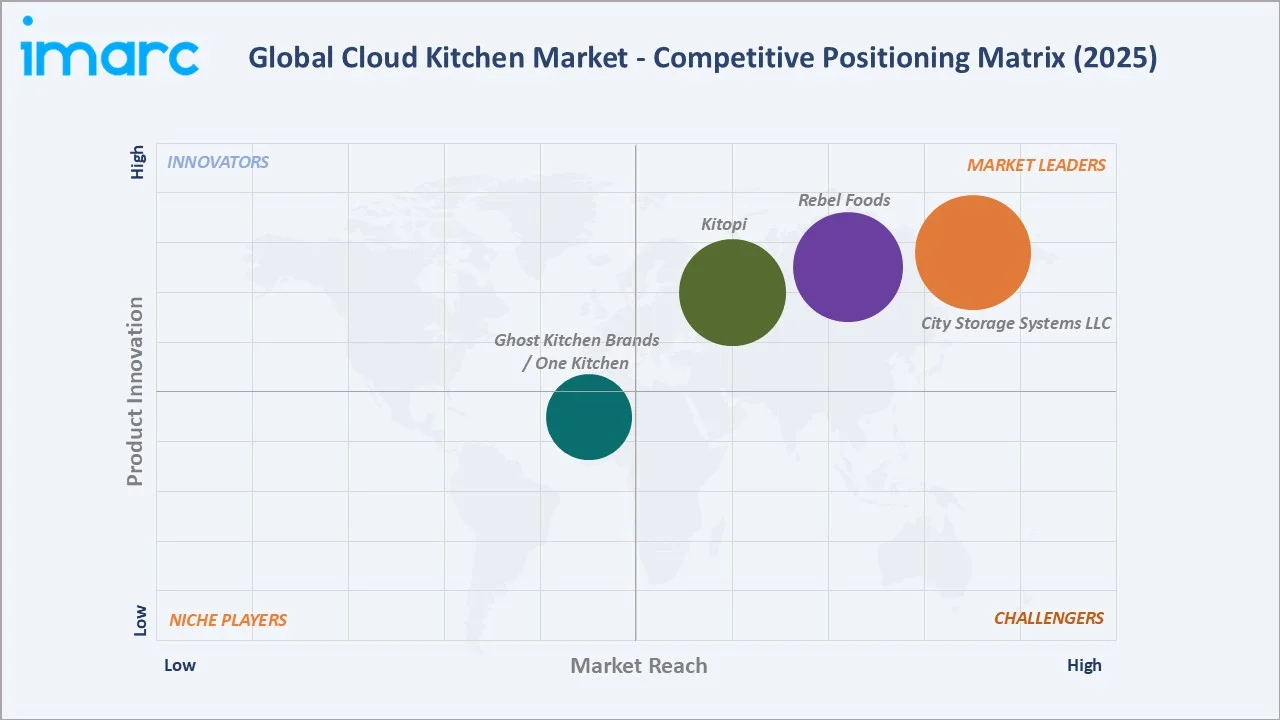

Competitive Landscape

The global cloud kitchen market exhibits a three-tier competitive structure: infrastructure and real estate operators commanding the market’s highest asset values; multi-brand virtual restaurant platforms generating the highest revenue velocity; and enabling technology providers capturing recurring SaaS and transaction fee revenue.

|

Company Name |

Platform / Brand |

Market Position |

Core Strength |

|

City Storage Systems LLC. |

CloudKitchens |

Market Leader |

Located in the West Coast, the Southwest, the Midwest, the Southeast, and the Northeast |

|

Rebel Foods |

Faasos, Behrouz Biryani, Oven Story, Mandarin Oak, Firangi Bake, Lunch Box, The Good Bowl |

Market Leader |

India’s most valuable cloud kitchen unicorn and Asia’s largest multi-brand internet restaurant platform |

|

Kitopi |

Under 500, Luff, Catch 22, Biryani Pot, Chin Chin, Batch, Bunday |

Market Leader |

Dubai-headquartered MENA cloud kitchen leader; proprietary Smart Kitchen OS (SKOS) managing orders, inventory, and staff across multi-brand kitchens in real time |

|

Ghost Kitchen Brands / One Kitchen |

Ghost Kitchen Brands |

Established |

Canadian cloud kitchen franchisor operating branded ghost kitchen locations within existing food service venues |

City Storage Systems, Rebel Foods, and Kitopi’s collectively represent the top-three cloud kitchen operators by venture valuation, while DoorDash and Swiggy represent the delivery platform layer with cloud kitchen infrastructure ambitions.

Key Company Profiles

City Storage Systems LLC.

City Storage Systems LLC. operates the cloud kitchens under CloudKitchens, which is the world’s largest and most capitalized dedicated cloud kitchen real estate and technology operator.

- Product Portfolio: CloudKitchens shared kitchen spaces

- Recent Developments: CloudKitchens India pilot expansion to Tier-2 using modular pod technology

- Strategic Focus: Technology-first cloud kitchen infrastructure; real estate acquisition below market value creates long-term asset appreciation alongside operating lease revenue.

Rebel Foods

Rebel Foods is India’s most valuable cloud kitchen company and one of the world’s largest multi-brand internet restaurant platforms.

- Product Portfolio: Faasos, Behrouz Biryani, Oven Story, Mandarin Oak, Firangi Bake, Lunch Box, The Good Bowl.

- Recent Developments: In February 2025, Rebel Foods entered the 15-minute food delivery market with “QuickiES,” a standalone app promising ultra-fast deliveries.

- Strategic Focus: Multi-brand manufacturing efficiency as core competitive moat; international expansion via kitchen pod technology reducing CAPEX for non-India markets.

Kitopi

Kitopi is the Middle East and North Africa’s leading cloud kitchen operator, the region’s first cloud kitchen unicorn.

- Product Portfolio: Kitopi managed cloud kitchen facilities (brands includes Under 500, Luff, Catch 22, Biryani Pot, Chin Chin, Batch, Bunday); Smart Kitchen OS (SKOS – real-time kitchen management, order routing, inventory management)

- Recent Developments: In February 2026, Kitopi raised $50 million in growth capital after achieving profitability, to scale its portfolio of brands across the Gulf and beyond.

- Strategic Focus: Global expansion of managed cloud kitchen model beyond MENA into US and Southeast Asia; SKOS technology platform licensing to non-competing regional cloud kitchen operators as B2B revenue diversification.

Market Concentration Analysis

The global cloud kitchen market exhibits moderate concentration at the operator tier and high fragmentation at the individual virtual brand tier. City Storage Systems, Rebel Foods, and Kitopi collectively account for approximately 12–15% of global cloud kitchen operator revenue, a relatively low top 3 concentration reflecting the market’s early-stage development, geographic fragmentation, and the massive independent operator base. The delivery platform layer is more concentrated: DoorDash, Meituan, and Swiggy-Zomato create regional delivery platform oligopolies that give these companies disproportionate power over cloud kitchen demand and therefore economics.

Technology fragmentation exists across restaurant tech, where no single provider controls more than 5% of global cloud kitchen technology deployments. This technology fragmentation creates ongoing integration complexity for cloud kitchen operators managing multi-platform orders but simultaneously creates a competitive landscape where new technology entrants with superior AI or integration capabilities can gain rapid traction. The convergence of delivery platforms, kitchen infrastructure, and restaurant technology into vertically integrated cloud kitchen ecosystems, led by DoorDash and Swiggy, is the primary consolidation force that will concentrate the market over 2026–2034.

Investment & Growth Opportunities

Fastest Growing Segments

Kitchen pods (~11.2% CAGR), MEA region (~11.2% CAGR), standalone virtual brand creation (~9.8% CAGR), robotic kitchen automation (~30–40% CAGR from 2025 base), and corporate B2B catering via cloud kitchens (~15–20% CAGR) represent the market’s highest-growth vectors.

Emerging Geographic Opportunities

Sub-Saharan Africa represents the final major global cloud kitchen frontier with urban African consumers, with rapidly growing smartphone penetration and rising food delivery platform adoption. Latin America’s iFood-dominated Brazil market, with cloud kitchen operators already active, represents a market opportunity. Vietnam, the Philippines, and Bangladesh represent Southeast and South Asia’s next wave of cloud kitchen market development following India’s and Indonesia’s established trajectories.

Investment Themes

Global cloud kitchen sector investments are under scrutiny as unit economics and are recovering with sustainability-focused investment from 2025 onwards.

- Key investment themes: Kitchen robotics and automation, AI-driven virtual brand management platforms, sustainable packaging solutions for delivery, kitchen pod modular manufacturing, and cloud kitchen technology for underserved emerging markets.

- Strategic partnership opportunities: Grocery retail-cloud kitchen co-location, hotel and corporate campus kitchen activation, dark kitchen-dark store convergence infrastructure, and delivery platform white-label kitchen operation for brands seeking owned production facilities.

Future Market Outlook (2026-2034)

The global cloud kitchen market is entering its commercial maturation phase. From USD 85.5 Billion in 2025, the market will reach USD 185.7 Billion by 2034, at a consistent 9.0% CAGR that reflects the gradual institutionalization of delivery-only food production as a permanent, mainstream food service category rather than a COVID-era niche. Three structural forces will define the 2026–2030 growth period: kitchen automation’s commercial-scale deployment, reducing the labour cost structure that constrains cloud kitchen margin at scale in high-wage markets; the completion of Tier-2 city cloud kitchen infrastructure build-out globally as kitchen pod economics unlock 3,000+ previously unserved markets; and platform-kitchen vertical integration by DoorDash, Swiggy, and Meituan, creating closed-loop ecosystems where consumer data, kitchen production, and delivery logistics are unified under single corporate umbrellas that achieve gross margins.

Research Methodology

Primary Research

Primary research included structured interviews with 130+ industry stakeholders in 2025, comprising cloud kitchen operators, delivery platform commercial executives, restaurant technology product managers, food service industry analysts, investor relations teams of listed companies, and regional market specialists in India, the UAE, the US, and Europe.

Secondary Research

Secondary research encompassed IMARC Group food service database, Euromonitor International restaurant industry data, Bloomberg F&B market intelligence, public company financial filings, FSSAI cloud kitchen registration database, DoorDash and Uber Eats merchant ecosystem reports, USDA food service market data, and 200+ industry publication sources reviewed.

Forecasting Models

Market forecasts were developed using a bottom-up operator-count × average revenue per kitchen aggregation validated against top-down macroeconomic models. Key inputs include global online food delivery platform GMV forecasts, cloud kitchen-to-total-restaurant revenue mix evolution by region, kitchen automation cost curve projections, and venture investment pipeline analysis for cloud kitchen technology categories.

Cloud Kitchen Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Independent Cloud Kitchen, Commissary/Shared Kitchen, Kitchen Pods |

| Product Types Covered | Burger and Sandwich, Pizza and Pasta, Chicken, Seafood, Mexican and Asian Food, Others |

| Natures Covered | Franchised, Standalone |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | City Storage Systems LLC., Rebel Foods, Kitopi, Ghost Kitchen Brands / One Kitchen, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the cloud kitchen market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global cloud kitchen market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the cloud kitchen industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Cloud Kitchen Market Report

The global cloud kitchen market was valued at USD 85.5 Billion in 2025 and is projected to reach USD 185.7 Billion by 2034.

The global cloud kitchen market is forecast to grow at a CAGR of 9.0% during 2026-2034, driven by post-COVID delivery habit permanence, low capital requirements, AI optimization, and urbanization.

Independent cloud kitchens lead with 64.2% revenue share (2025), reflecting the global restaurant industry’s pragmatic conversion of existing commercial kitchens to delivery-only operations.

Franchised cloud kitchens lead with 67.1% revenue share (2025), as established brand recognition on delivery platforms reduces customer acquisition cost by 3–5× versus standalone virtual brands.

Asia-Pacific leads with 35.7% revenue share (2025), driven by China’s Meituan and India’s Swiggy-Zomato duopoly collectively serving daily cloud kitchen and restaurant orders.

Key companies include City Storage Systems LLC., Rebel Foods, Kitopi, and Ghost Kitchen Brands / One Kitchen.

Key drivers include post-COVID permanent food delivery habit adoption by consumers, lower capital requirements versus traditional restaurants, AI menu optimization, kitchen pod geography expansion, and delivery platform scale in APAC.

Key trends include multi-brand kitchen model, robotic kitchen automation, sustainable kitchen certification, virtual brand IP licensing, and cloud kitchen – quick commerce dark store convergence into integrated last-mile delivery hubs.

China’s Meituan and India’s Swiggy-Zomato create combined daily delivery orders, the world’s highest delivery order density, making APAC cloud kitchen unit economics globally most favorable.

Key challenges include delivery platform commission rates compressing margins, customer discovery cost for virtual brands, supply chain food cost volatility, regulatory complexity across geographies, and food quality degradation during delivery.

Top opportunities include kitchen pod Tier-2 city deployment, robotic kitchen automation technology, virtual brand IP licensing platforms, Africa and Latin America market entry, corporate B2B catering contracts, and cloud kitchen, dark store co-location infrastructure.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade