Cocoa Processing Market Size, Share, Trends and Forecast by Bean Type, Product Type, Application, and Region, 2026-2034

Cocoa Processing Market Size, Share, Trends & Forecast (2026-2034)

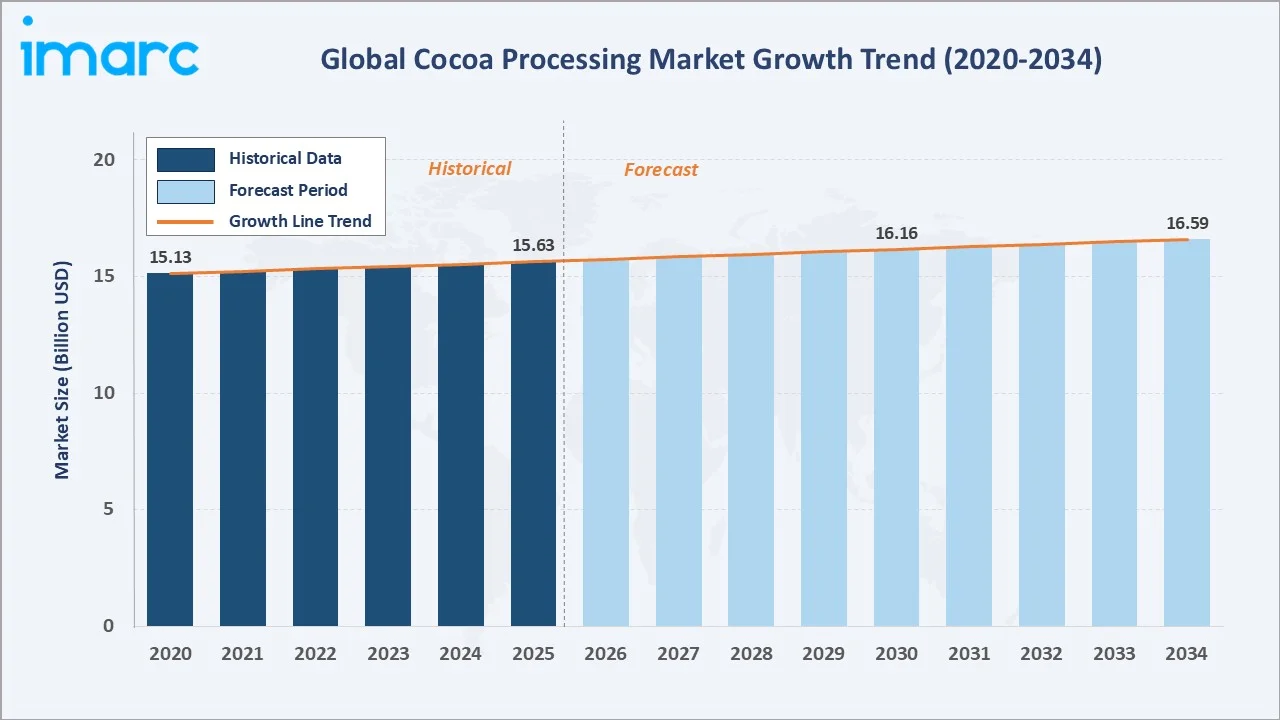

The global cocoa processing market reached USD 15.63 Billion in 2025 and is projected to reach USD 16.59 Billion by 2034. Increasing demand for ethically sourced and certified cocoa, the rising adoption of bean-to-bar processing concepts, growing utilization of cocoa-derived ingredients in pharmaceuticals and cosmetics, and the expansion of artisanal and craft chocolate production are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 15.63 Billion |

|

Forecast Market Size (2034) |

USD 16.59 Billion |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Europe (29.7% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

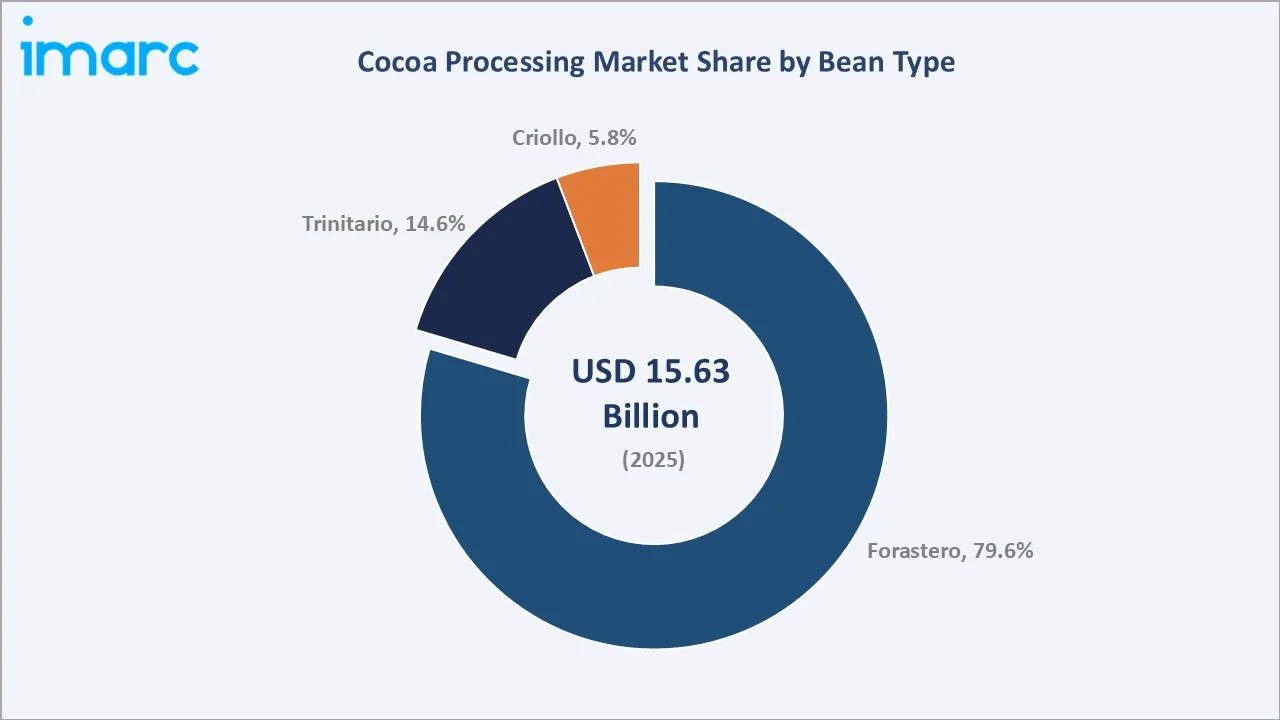

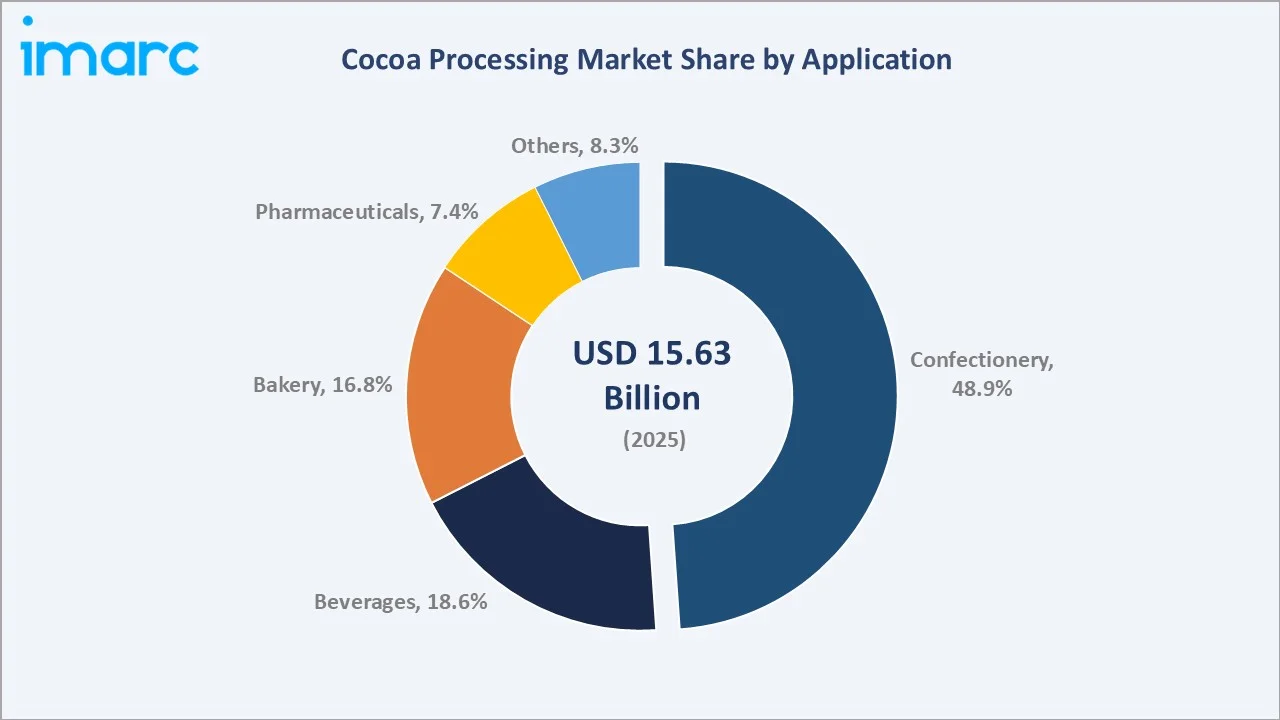

Europe dominates, holding a 29.7% market share in 2025, while confectionery leads application demand at 48.9%. Forastero remains the dominant bean type with a 79.6% share. Cocoa processing encompasses techniques that transform cocoa beans into diverse products, including cocoa butter, cocoa powder, and chocolate liquor.

To get more information on this market, Request Sample

With applications spanning confectionery, bakery, beverages, pharmaceuticals, and cosmetics, the market is expected to continue expanding, supported by innovations in sustainable processing technology, the growing bean-to-bar movement, and increasing adoption of functional cocoa ingredients in health and wellness product categories across emerging and developed economies.

Executive Summary

The global cocoa processing market is on a stable, demand-driven growth path, underpinned by the expanding confectionery and bakery industries, rising consumer preference for premium and functional chocolate, and the growing incorporation of cocoa derivatives in pharmaceutical formulations and cosmetics. The market reached USD 15.63 Billion in 2025 and is forecast to reach USD 16.59 Billion by 2034.

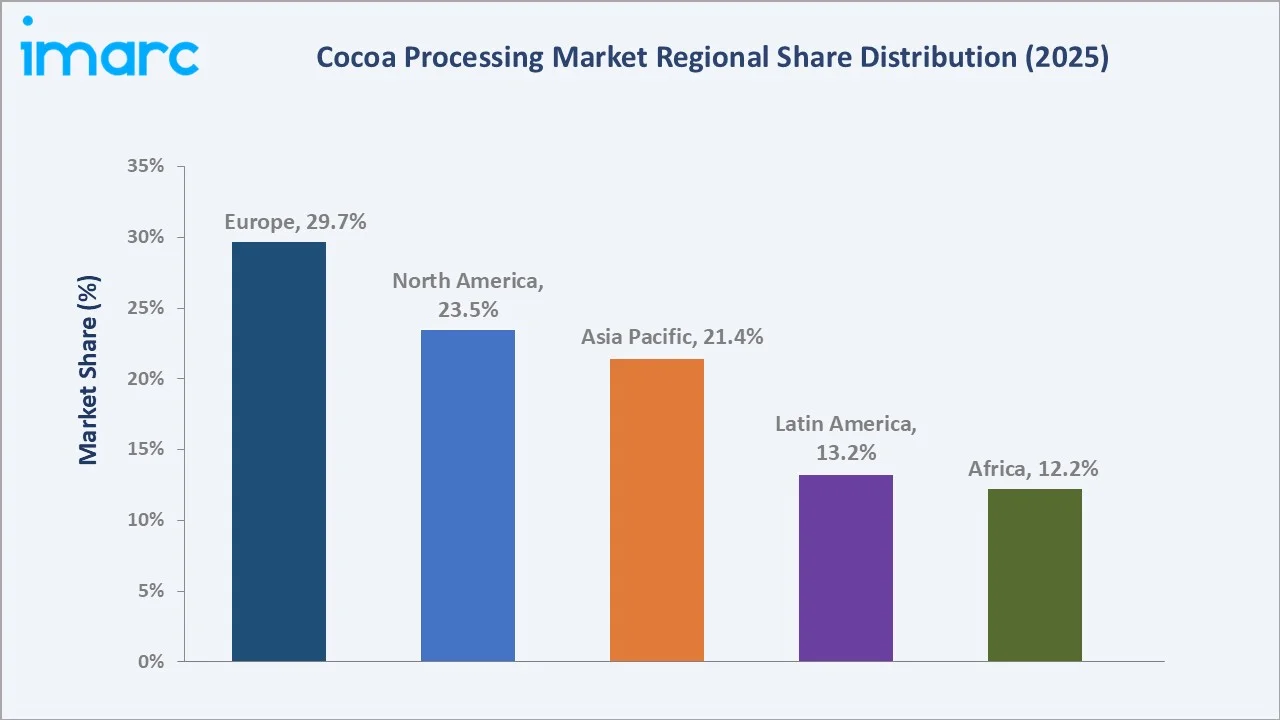

Europe leads globally with a 29.7% revenue share in 2025, driven by the Netherlands, the world's largest cocoa grinding country, alongside Belgium's premium chocolate sector and Germany's confectionery manufacturing base. Asia Pacific, at 21.4%, represents the fastest-growing opportunity, with rising chocolate consumption in China, India, Japan, and Southeast Asia fueling significant processing demand.

Confectionery applications command the largest share at 48.9%, followed by beverages (18.6%) and bakery (16.8%). Leading processors, including Barry Callebaut, Cargill, Incorporated, Olam Group, Guan Chong Berhad (GCB), and ECOM Agroindustrial Corp. Limited, continue to invest in sustainable sourcing programs, digital traceability infrastructure, and precision fermentation technologies to align with tightening EU Deforestation Regulation (EUDR) requirements and evolving consumer expectations.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Bean Type) |

Forastero – 79.6% share (2025) |

|

Largest Segment (Application) |

Confectionery – 48.9% share (2025) |

|

Leading Region |

Europe – 29.7% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific (rising chocolate consumption) |

|

Top Companies |

Barry Callebaut, Cargill, Incorporated, Olam Group, Guan Chong Berhad (GCB), and ECOM Agroindustrial Corp. Limited |

|

Market Opportunity |

Organic & pharmaceutical cocoa ingredients, high-growth niches |

Key Analytical Observations Supporting the Above Data:

- Forastero accounts for 79.6% of cocoa bean processing in 2025, underpinning global bulk chocolate production. Its high yield, disease resistance, and adaptability across West Africa, Brazil, and Ecuador make it the commercially dominant variety for industrial-scale cocoa grinding.

- Confectionery is the dominant application at 48.9% (2025), driven by sustained demand for premium chocolates, chocolate-coated confections, and compound coatings across European, North American, and Asian markets.

- Europe holds 29.7% of the global cocoa processing market in 2025, supported by Belgium, Germany, France, and the Netherlands, home to the world's highest density of large-scale industrial cocoa processing and grinding facilities.

- Asia Pacific is emerging as the fastest-growing region, driven by a rapidly expanding middle class, urbanization, and growing Western dietary influences on chocolate consumption in China, India, and Southeast Asia.

- The pharmaceutical and nutraceutical application segment is experiencing accelerating growth, driven by mounting clinical evidence linking cocoa flavanols to cardiovascular health, cognitive function, and anti-inflammatory benefits.

Global Cocoa Processing Market Overview

Cocoa processing encompasses the full range of industrial techniques that transform raw cocoa beans into commercially viable intermediate and finished products. The process begins with sorting and roasting to develop flavor, followed by winnowing to separate shells from nibs, and grinding nibs into cocoa liquor (also known as cocoa mass).

This liquor is pressed to separate cocoa butter from cocoa solids, which are milled into cocoa powder. Alkalization adjusts pH and color, while the conching stage refines the final chocolate texture and flavor profile.

Macroeconomic factors, including rising disposable incomes in emerging markets, rapid urbanization, expanding functional food categories, and the global proliferation of premium confectionery brands, are primary growth catalysts.

The market ecosystem spans upstream cocoa bean sourcing (predominantly Ivory Coast, Ghana, Indonesia, and Ecuador), midstream processing infrastructure across Europe and Asia, and downstream application markets across food, beverage, pharmaceutical, and cosmetic industries.

Market Dynamics

To evaluate market opportunities, Request Sample

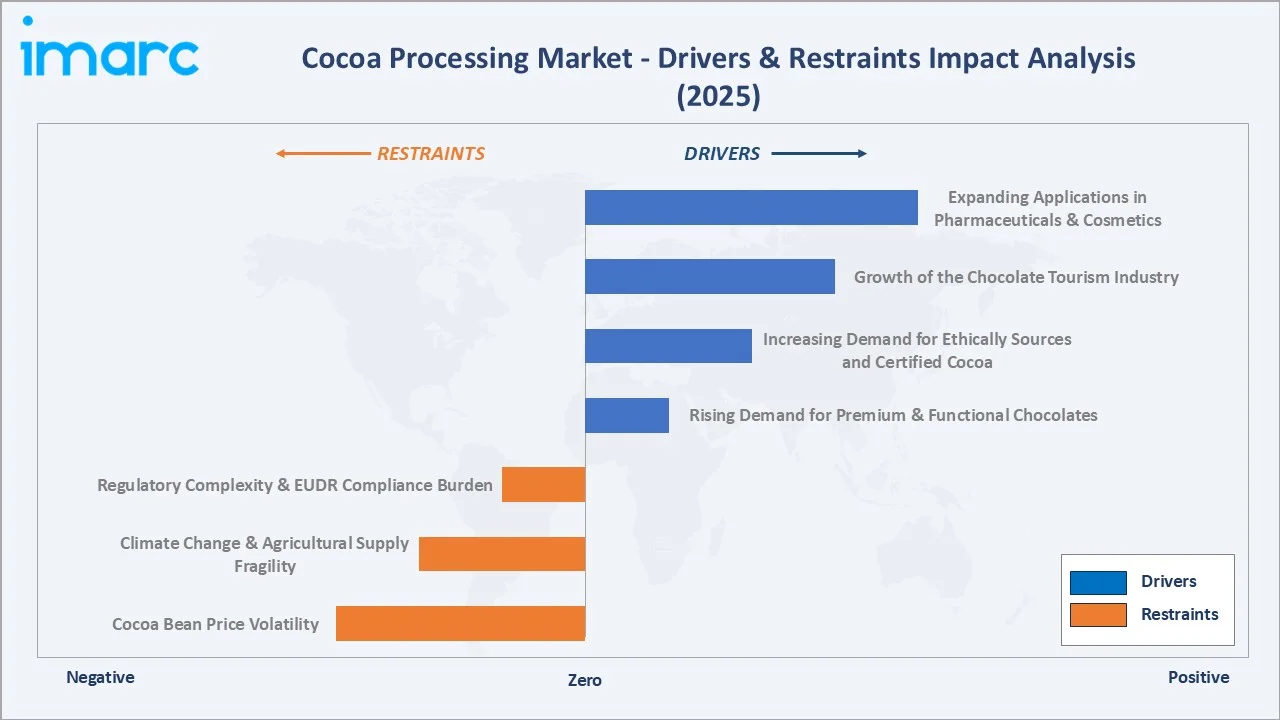

Market Drivers

- Rising Demand for Premium and Functional Chocolates: According to the International Cocoa Organization (ICCO), global cocoa grindings reached approximately 4,606 thousand tons in 2024/25, reflecting sustained industrial demand. Premium chocolate categories grew at approximately 6.2% annually between 2020 and 2025 in Europe and North America, consistently outpacing the growth of conventional confectionery segments.

- Increasing Demand for Ethically Sourced and Certified Cocoa: EU Deforestation Regulation (EUDR), effective from 2025, mandates comprehensive due diligence for cocoa entering European markets. Barry Callebaut and Cargill, Incorporated have committed to 100% sustainably sourced cocoa, driving investment across origin traceability, farmer training, and certified supply chain programs.

- Growth of the Chocolate Tourism Industry: Barry Callebaut operates 26 Chocolate Academy Centers globally. This trend reinforces consumer willingness to pay premiums for traceable, high-quality cocoa products, boosting demand for fine-flavor Criollo and Trinitario varieties.

- Expanding Applications in Pharmaceuticals and Cosmetics: The global nutraceuticals market is projected to exceed USD 909.2 Billion by 2034, with cocoa-derived polyphenol extracts as one of the fastest-growing active ingredient categories. Simultaneously, cocoa butter's emollient properties continue to drive premium cosmetic formulations.

Market Restraints

- Cocoa Bean Price Volatility: Cocoa has experienced significant volatility in recent years. Prices soared above USD 10,000 per metric ton in early 2025 before undergoing a sharp correction. By April 2026, cocoa futures had climbed back above the USD 3,500 mark.

- Climate Change and Agricultural Supply Fragility: The IPCC projects that up to 50% of current cocoa-growing zones in Ghana and the Ivory Coast could become climatically unsuitable by 2050 without significant adaptation measures, creating long-term supply security risks for global processors.

- Regulatory Complexity and EUDR Compliance Burden: Compliance with the EU Deforestation Regulation requires comprehensive supply chain mapping to the farm level, imposing significant operational and technology investment burdens, particularly on processors sourcing from fragmented smallholder supply chains across West Africa and Southeast Asia.

Market Opportunities

- Precision Fermentation and Cellular Cocoa Technology: Start-ups such as California Cultured initiated commercial cultivation of cocoa from plant cell cultures in September 2024, with product introductions planned for 2025-2026. This technology has the potential to decouple cocoa supply from climate and land-use limitations.

- Organic and Single-Origin Cocoa Ingredient Demand: OFI launched the deZaan Master 01, a 100% segregated organic cocoa powder with fully traceable supply chain credentials. Demand for organic cocoa ingredients is growing at approximately 8% annually, supported by clean-label procurement requirements across European and North American food manufacturers and rapidly expanding health-conscious consumer segments.

- Emerging Market Expansion and Origin Processing: Ivory Coast and Ghana collectively account for approximately 60-70% of global cocoa production, but a disproportionately small share of finished cocoa ingredient value. Policy-driven local processing incentives, including export taxes on raw beans in the Ivory Coast, are progressively accelerating this structural shift.

Market Challenges

- Deforestation and Land Use Compliance: The EUDR requires processors to provide geo-location data for all cocoa farms in their supply chains, creating significant operational complexity for large-scale processors managing tens of thousands of smallholder farmers across fragmented West African supply networks.

- Quality Inconsistency Across Smallholder Supply Chains: Over 90% of global cocoa is grown by smallholder farmers on plots of less than 5 hectares. Inconsistent fermentation and drying practices lead to variable bean quality, increasing rejection rates and processing inefficiencies. Addressing this structural challenge requires sustained, multi-year farmer training investment across origin countries.

Emerging Market Trends

1. Bean-to-Bar Movement and Artisanal Chocolate Expansion

The global bean-to-bar movement has fundamentally shifted sourcing and processing dynamics. This trend increases processor emphasis on single-origin and specialty cocoa varieties, including Criollo (5.8% share) and Trinitario (14.6%), beans that command price premiums of 30-80% over standard Forastero grades.

2. Machine Learning Innovations

Barry Callebaut has partnered with NotCo to use AI and machine learning to develop next‑generation chocolate products with improved taste, texture, and sustainability, accelerating innovation across its portfolio. The collaboration aims to leverage NotCo’s proprietary AI platform to create plant‑based and hybrid chocolate formulations that meet consumer demands while reducing environmental impact.

3. AI-Driven Quality Control and Process Optimization

AI vision systems for cocoa bean quality inspection, detecting mold, fermentation defects, insect damage, and moisture content, are projected to reduce processing waste by up to 12%. Large processors are integrating machine learning models trained on millions of bean images to achieve consistent quality grading at origin, significantly reducing rejection rates at industrial grinding facilities.

4. Growth of Functional and Organic Cocoa Products

OFI's deZaan range and Barry Callebaut's NotCo to use AI and machine learning to develop innovative chocolate products (November 2025) feature nutrient-dense formulations addressing wellness-conscious consumer demand.

Industry Value Chain Analysis

The cocoa processing value chain spans raw cocoa bean sourcing through finished ingredient delivery to end-use manufacturers, with each stage populated by specialized operators whose performance directly influences product quality, sustainability credentials, and ingredient cost.

|

Stage |

Key Players / Examples |

|

Cocoa Bean Farming & Sourcing |

Smallholder cooperatives (West Africa), certified farms, Ecom Agroindustrial Corp., Touton S.A. |

|

Fermentation & Drying (Origin) |

Origin cooperatives, ECOM, Touton, Olam Group |

|

Industrial Grinding & Pressing |

Barry Callebaut, Cargill, Incorporated, Olam Group, Guan Chong Berhad (GCB), and ECOM Agroindustrial Corp. Limited |

|

Cocoa Ingredient Manufacturing |

Barry Callebaut, Cargill Cocoa & Chocolate, Cémoi Group |

|

Distribution Channels |

Direct B2B supply, commodity traders, specialty ingredient distributors |

|

End Users |

Confectionery brands, bakeries, beverage manufacturers, nutraceutical/pharmaceutical companies, cosmetic firms |

Technology Landscape in the Cocoa Processing Industry

Advanced Fermentation Monitoring and Flavor Engineering

Companies including Uncommon Cacao and Cocoa Runners apply precision fermentation protocols that increase flavor complexity and reduce batch-to-batch variability by up to 20%. Remote fermentation monitoring is enabling processors to maintain quality standards across thousands of smallholder farms without physical presence.

Continuous Grinding and Energy-Efficient Refining Systems

Modern continuous ball mill and bead mill systems have replaced traditional batch grinding in large-scale facilities, reducing energy consumption per metric ton of cocoa liquor by approximately 18-22%. Equipment suppliers, including Buhler Group and Royal Duyvis Wiener, are leading innovation for large-scale processors, integrating real-time quality monitoring sensors that optimize grinding parameters dynamically.

Blockchain and Satellite-Based Supply Chain Traceability

Satellite imagery combined with farm-level geolocation data enables processors to verify deforestation-free sourcing at scale, a mandatory requirement under the EU Deforestation Regulation from 2025. Barry Callebaut and Cargill, Incorporated both operate proprietary platforms, while emerging third-party solutions from providers such as Rainforest Alliance, Sourcemap, and Meridia offer scalable traceability infrastructure to mid-tier processors.

Cellular Cocoa and Lab-Grown Ingredient Technology

California Cultured (Sacramento, USA) initiated commercial cultivation of cocoa from plant cell cultures in September 2024. This technology produces cocoa butter and cocoa flavor compounds with zero agricultural footprint, addressing deforestation, child labor, and supply volatility concerns simultaneously.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Bean Type | Forastero | 79.6% | 2025 |

| Product Type | 🔒 | 🔒 | 2025 |

| Application | Confectionery | 48.9% | 2025 |

| Region | Europe | 29.7% | 2025 |

By Bean Type

Forastero dominates the bean type segment with a 79.6% share in 2025. Its dominance reflects superior agronomic characteristics, high yield, disease resistance, and adaptability across diverse climatic zones in the Ivory Coast, Ghana, Brazil, and Ecuador. Forastero beans are the backbone of global bulk chocolate production, including milk chocolate, compound coatings, and cocoa powder for food service applications.

To access detailed market analysis, Request Sample

Trinitario holds 14.6% of the market, valued as a hybrid variety combining Forastero's productivity with Criollo's aromatic complexity. Trinitario beans are increasingly favored in single-origin and premium dark chocolate production. Criollo, the rarest and most prized variety at 5.8% share, commands price premiums of 30-80% over Forastero grades in the artisanal, fine flavor, and craft chocolate markets.

By Application

Confectionery leads application demand at 48.9% in 2025. This segment encompasses chocolate bars, bonbons, chocolate-coated confections, truffles, and compound coatings for snack applications. Strong institutional demand from multinational confectionery brands, including Nestlé, Mondelez International, Mars, and Ferrero, drives stable, high-volume cocoa liquor and cocoa butter procurement from industrial processors.

Beverages hold an 18.6% share, driven by hot cocoa, cocoa-infused dairy beverages, and premium drinking chocolate. Bakery applications account for 16.8%, with widespread use of cocoa powder and compound chocolate in cakes, biscuits, brownies, and pastry fillings. Pharmaceuticals represent 7.4% and are the fastest-growing application, driven by clinical validation of cocoa flavanols in cardiovascular and cognitive health management.

Regional Market Insights

Europe's market leadership reflects centuries of confectionery manufacturing heritage and the presence of world-class industrial processing facilities. In 2025, the Netherlands exported cocoa products valued at EUR 12.4 billion, with EUR 11.4 billion coming from re-exports. Belgium's premium chocolate sector drives sustained demand for fine-flavor cocoa liquor.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Europe |

29.7% |

Premium confectionery, EUDR compliance, and advanced grinding infrastructure |

|

North America |

23.5% |

Functional food growth, craft chocolate boom, snack market expansion |

|

Asia Pacific |

21.4% |

Rising middle-class consumption, urbanization, and growing chocolate demand in China and India |

|

Latin America |

13.2% |

Origin-country processing growth, Ecuador specialty cocoa, Brazil domestic market expansion |

|

Africa |

12.2% |

Growing domestic processing in the Ivory Coast and Ghana, value addition at the origin policy |

Asia Pacific is the highest-growth region, with China's chocolate market growing at approximately 7% annually through 2034. In December 2025, Malaysian cocoa grinder Guan Chong Bhd is pushing ahead with a major expansion of its cocoa‑grinding capacity from 335,000 to 500,000 tons annually to strengthen competitiveness internationally.

Competitive Landscape

The global cocoa processing market exhibits a moderately concentrated structure at the industrial grinding level. The top three processors, Barry Callebaut, Cargill, Incorporated, and Olam Group, collectively account for approximately 55-60% of global cocoa grinding capacity in 2025.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Barry Callebaut |

Callebaut, Cacao Barry |

Market Leader |

World's largest chocolate and cocoa manufacturer; 66 production sites; 138-country distribution network |

|

Cargill, Incorporated |

Gerkens |

Market Leader |

Global agribusiness leader; USD 100M Ivory Coast plant expansion (2021); 70-country operations |

|

Olam Group |

deZaan, Unicao, Joanes, Macao, Huysman, Britannia, BT Cocoa, Twenty Degrees |

Strong Challenger |

Integrated agri-supply chain; major West Africa cocoa sourcing and processing; organic ingredient leadership |

|

Guan Chong Berhad (GCB) |

SCHOKINAG, Carlyle Cocoa, Favorich Chocolate |

Strong Challenger |

One of the world’s largest cocoa grinders, 400,000+ MT/year capacity, strong Asia Pacific and European presence |

|

ECOM Agroindustrial Corp. Limited |

ECOM Cocoa |

Niche Player |

Specialty origin cocoa; farmer training programs; fine flavor bean sourcing across Latin America and Asia |

Guan Chong Berhad (GCB) and ECOM Agroindustrial Corp. Limited are the next-largest processors, collectively holding approximately 10-12% combined share. Regional and specialty processors account for the remaining balance, particularly in the Asia Pacific and Latin America.

Key Company Profiles

Barry Callebaut

Barry Callebaut, headquartered in Zurich, Switzerland, is the world's largest manufacturer of chocolate and cocoa products by volume. Founded in 1996 through the merger of Callebaut (Belgium) and Cacao Barry (France), the company operates 66 production sites across more than 60 countries, serving artisans, chefs, and food manufacturers in over 138 countries.

- Product Portfolio: Full-spectrum cocoa ingredients (cocoa butter, liquor, powder) and chocolate solutions for food manufacturers, artisans, and professional chefs.

- Recent Developments: In April 2025, Barry Callebaut planned to expand U.S. production at a key facility to about 100,000 tons. The move reflects efforts to strengthen its local footprint and supply chain resilience in a challenging trade and cocoa price climate.

- Strategic Focus: Achieving 100% sustainably sourced cocoa; premium ingredient innovation and direct customer partnership expansion across all geographies.

Cargill, Incorporated

Cargill, Incorporated, headquartered in Wayzata, Minnesota (founded 1865), is one of the world's largest agribusiness companies and a global leader in cocoa processing. The company operates in 70 countries with approximately 160,000 employees across all divisions.

- Product Portfolio: Cocoa butter, cocoa liquor, cocoa powder, and chocolate solutions for food manufacturers in bakery, confectionery, dairy, and beverage sectors.

- Recent Developments: In July 2025, Cargill, Incorporated set a new global benchmark for sustainable cocoa supply chains by investing in interconnected initiatives, from biomass boilers in Côte d’Ivoire and solar power in Ghana to fully electric barges and solar warehouses in Europe.

- Strategic Focus: Sustainable cocoa sourcing at scale via the Cargill Cocoa Promise program; digital supply chain traceability; expansion of emerging market processing footprint; EUDR compliance infrastructure investment.

Olam Group

Olam Group, headquartered in Singapore and founded in 1989, operates one of the most integrated agricultural supply chains globally. Its cocoa operations span bean sourcing in West Africa, South America, and Asia, through processing hubs in Europe, North America, and the Asia Pacific.

- Product Portfolio: Cocoa beans, butter, liquor, powder (including deZaan premium range); organic and single-origin cocoa ingredients; functional cocoa extracts for pharmaceutical and nutraceutical applications.

- Recent Developments: Olam Group reported a PATMI of SGD 444.1 million for 2025, up 414% year‑on‑year, driven by stronger operating performance and higher revenues. The company also saw operating profit (EBIT) rise about 38% to SGD 1.3 billion.

- Strategic Focus: Supply chain integration from farm to ingredient; sustainable sourcing and traceability; specialty and organic ingredient differentiation; expansion of processing capacity in the Asia Pacific to serve growing demand.

Market Concentration Analysis

The cocoa processing market exhibits moderate concentration at the industrial grinding level. The top three processors, Barry Callebaut, Cargill, Incorporated, and Olam Group, account for approximately 55-60% of global cocoa grinding capacity in 2025. Guan Chong Berhad (GCB) and ECOM Agroindustrial Corp. Limited hold approximately 10-12% combined share. Regional and specialty processors, particularly in Asia Pacific and Latin America, account for the remaining 28-35%.

Consolidation is accelerating, driven by the capital intensity of EUDR-compliant traceability systems, sustainability certification requirements, and the scale efficiencies inherent in large-volume cocoa grinding and pressing operations. Between 2020 and 2024, notable strategic activity included Olam's carve-out of OFI as a standalone food ingredients business and Barry Callebaut's continued geographic facility expansion across North America and the Asia Pacific.

Investment & Growth Opportunities

Fastest Growing Segments

Pharmaceutical and nutraceutical cocoa applications (estimated CAGR approximately 2.5%), organic and single-origin cocoa ingredients (approximately 8% CAGR), and cellular and precision-fermentation cocoa technology represent the three highest-growth investment vectors through 2034.

Emerging Market Expansion

Africa-origin value-added processing and Asia Pacific demand growth collectively represent the most significant structural expansion opportunities for cocoa processors through 2034. The Malaysian International Cocoa Fair (MICF) 2025, scheduled for May 24-27 in Sabah, underscores the Asia Pacific's strategic ambition to expand its role as a global cocoa processing hub.

Venture and Institutional Investment Trends

- Precision fermentation and cellular cocoa technology, addressing supply chain climate vulnerability, deforestation concerns, and price volatility simultaneously.

- Blockchain traceability platforms providing EUDR-compliant farm-to-factory mapping for the European and North American supply chains.

- Investments in renewable energy-powered cocoa processing facilities to meet Scope 1 and Scope 2 net-zero emissions commitments.

- Premium origin cocoa cooperatives in Ecuador (Nacional/Arriba), Madagascar, and Papua New Guinea, targeting fine flavor confectionery manufacturers globally.

Future Market Outlook (2034)

The global cocoa processing market is positioned for stable, quality-driven growth through 2034. From a base of USD 15.63 Billion in 2025, the market is projected to reach USD 16.59 Billion by 2034, representing total incremental value creation of approximately USD 960 Million.

Regulatory evolution, principally the EU Deforestation Regulation, FDA food safety requirements, and ICCO sustainability standards, will drive significant supply chain restructuring and capital investment across the industry. Processors that achieve EUDR-ready traceability infrastructure and sustainability certifications by 2025-2026 are positioned to capture a disproportionate share of institutional procurement from European and North American confectionery brands.

Long-term, the market's trajectory is tied to three structural macro-themes: rising emerging market chocolate consumption in Asia Pacific, Africa, and Latin America; health and functional food trends driving pharmaceutical and nutraceutical cocoa demand; and supply chain sustainability imperatives rewarding certified, traceable, and deforestation-free cocoa ingredient providers.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and consultations with over 120 industry stakeholders in 2024-2025, including cocoa processors, confectionery manufacturers, procurement officers, cocoa traders, sustainability consultants, and regulatory experts across Europe, North America, Asia Pacific, and West Africa.

Secondary Research

Secondary research encompassed a systematic review of ICCO annual reports, company financial filings, EU regulatory documentation (EUDR), USDA Foreign Agricultural Service trade data, FAO commodity statistics, World Cocoa Foundation reports, Rainforest Alliance certification data, and publicly available corporate sustainability reports.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating historical ICCO grinding data, cocoa bean production statistics, macroeconomic indicators (GDP growth, disposable income, urbanization rates), and application demand trends by end-use sector.

Cocoa Processing Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Bean Types Covered | Forastero, Criollo, Trinitario |

| Product Types Covered | Cocoa Butter, Cocoa Liquor, Cocoa Powder |

| Applications Covered | Confectionary, Bakery, Beverages, Pharmaceuticals, Others |

| Regions Covered | Europe, Africa, North America, Latin America, Asia Pacific |

| Companies Covered | Barry Callebaut, Cargill, Incorporated, Olam Group, Guan Chong Berhad (GCB), ECOM Agroindustrial Corp. Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the cocoa processing market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global cocoa processing market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the cocoa processing industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Cocoa Processing Market Report

The global cocoa processing market reached USD 15.63 Billion in 2025 and is projected to reach USD 16.59 Billion by 2034.

Europe dominates the global cocoa processing market with a 29.7% revenue share in 2025, driven by the Netherlands (the world's largest cocoa grinder), Belgium's premium chocolate sector, and Germany's confectionery manufacturing industry. North America holds a 23.5% share, followed by Asia Pacific at 21.4%.

Forastero is the dominant bean type with a 79.6% share in 2025, equivalent to approximately USD 12.44 Billion. Its high yield, disease resistance, and adaptability across diverse growing regions make it the preferred variety for bulk industrial cocoa processing globally.

Confectionery is the dominant application segment at 48.9% in 2025, approximately USD 7.64 Billion, driven by sustained demand for chocolate bars, bonbons, compound coatings, and chocolate-coated snacks from multinational confectionery brands including Nestlé, Mondelez International, Mars, and Ferrero.

Key players in the global cocoa processing market include Barry Callebaut, Cargill, Incorporated, Olam Group, Guan Chong Berhad (GCB), and ECOM Agroindustrial Corp. Limited.

The bean-to-bar movement is driving increased demand for fine-flavor cocoa varieties (Criollo and Trinitario), single-origin processing protocols, and direct farmer-to-processor relationships. This trend is elevating quality standards across the value chain and supporting premium pricing for certified, traceable cocoa ingredients, particularly in European and North American artisanal markets.

Key challenges include extreme cocoa bean price volatility (ICE cocoa futures exceeding USD 10,000/MT in 2024), compliance with the EU Deforestation Regulation requiring farm-level supply chain traceability, climate change impacts on West African growing regions, and quality inconsistency across fragmented smallholder supply chains.

Key investment opportunities include organic and functional cocoa ingredient manufacturing, pharmaceutical and nutraceutical applications of cocoa polyphenols, cellular cocoa, and precision fermentation technology.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade