Commercial Insurance Market Size, Share, Trends and Forecast by Type, Enterprise Size, Distribution Channel, Industry Vertical, and Region, 2026-2034

Commercial Insurance Market Size, Share, Trends & Forecast (2026-2034)

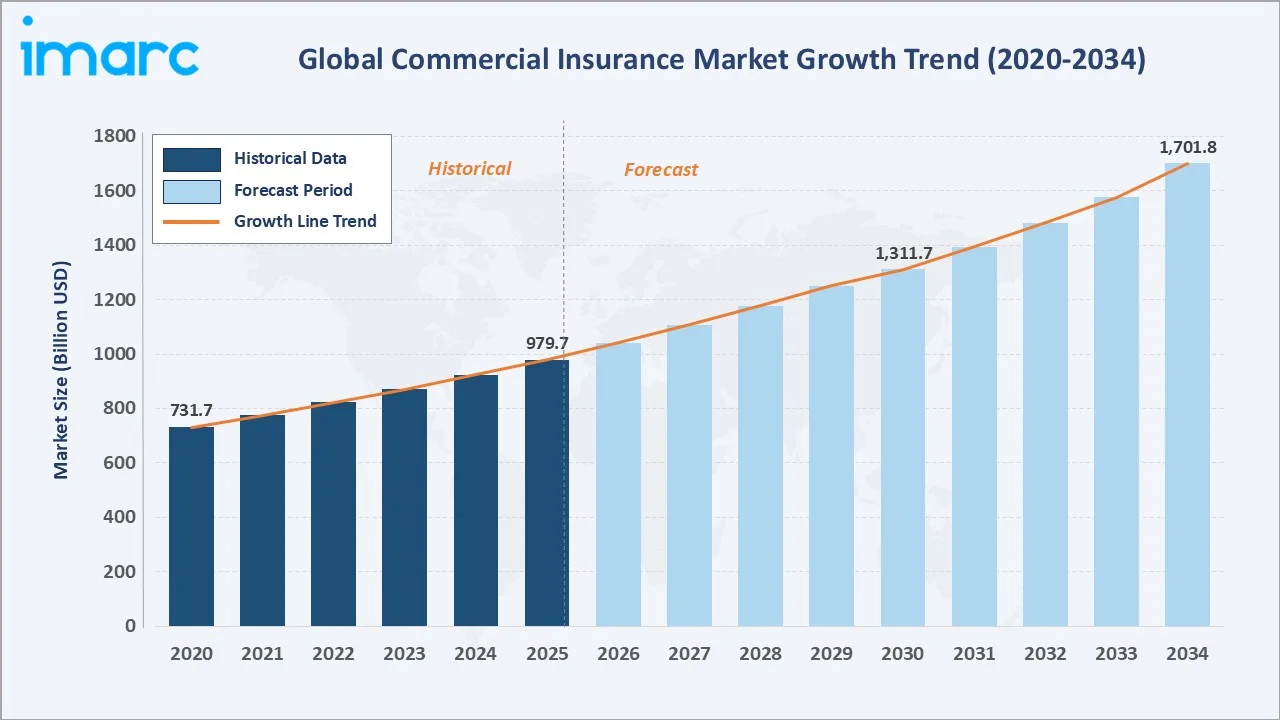

The global commercial insurance market reached USD 979.7 Billion in 2025 and is projected to reach USD 1,701.8 Billion by 2034, growing at a CAGR of 6.01% during 2026–2034. The market is driven by the accelerating frequency of catastrophic natural and cyber events, growing complexity of enterprise risk exposures, and the digital transformation of underwriting and claims processes through artificial intelligence and advanced analytics.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 979.7 Billion |

|

Forecast Market Size (2034) |

USD 1,701.8 Billion |

|

CAGR (2026-2034) |

6.01% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (38.9% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific |

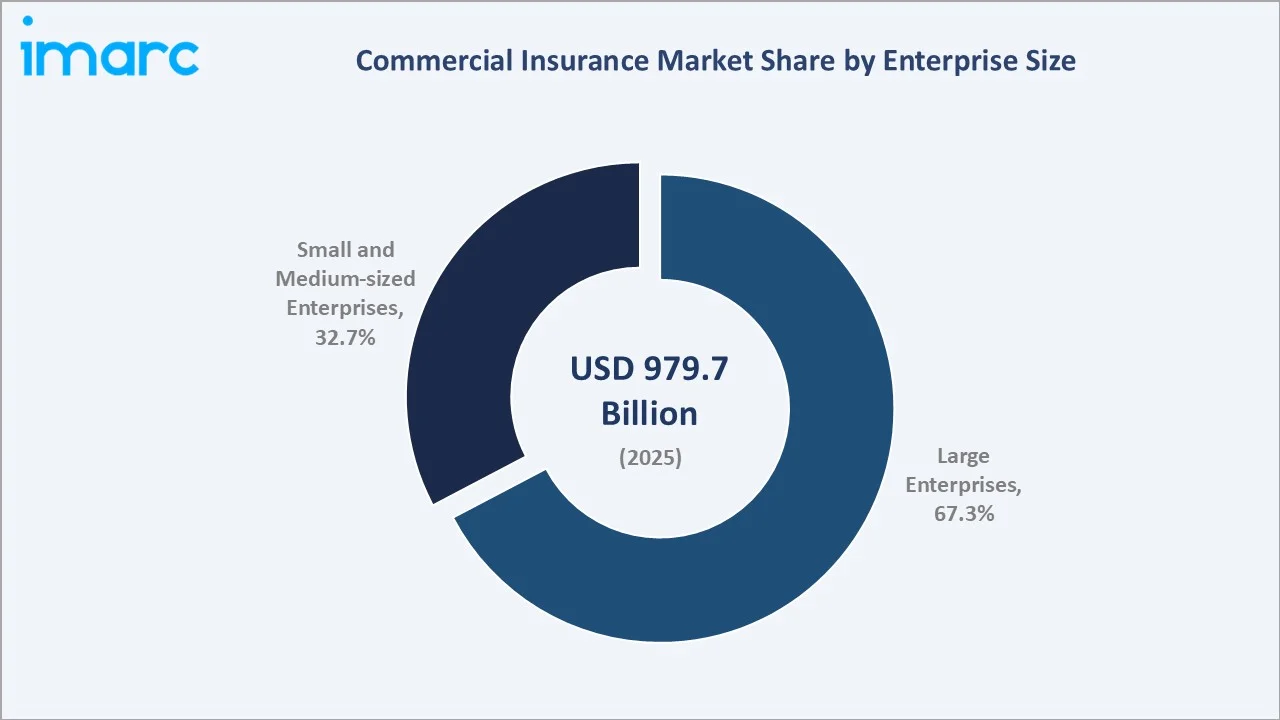

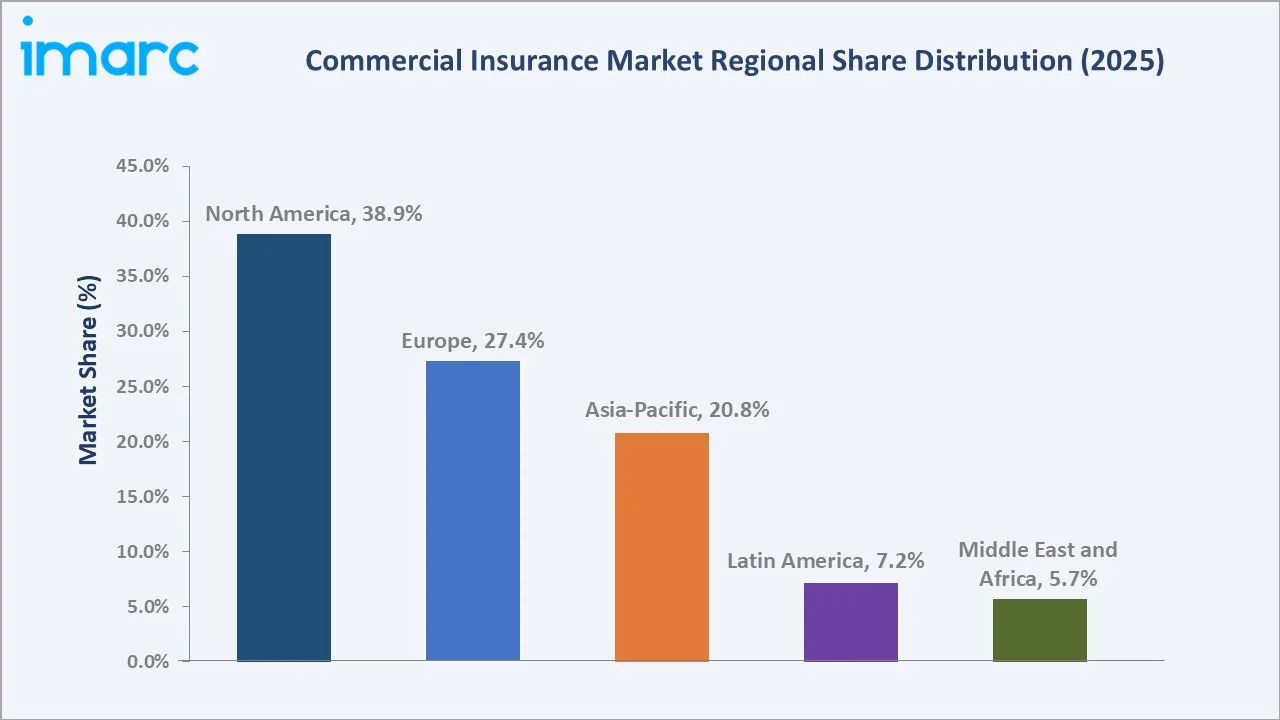

North America leads all regions with a 38.9% share in 2025, while large enterprises command the dominant organizational segment at 67.3%, reflecting their disproportionate need for multi-line, high-limit commercial coverage. The commercial insurance market growth is further supported by expanding SME formalization in emerging economies and the ongoing penetration of digital distribution channels that are improving access to tailored commercial insurance solutions.

To get more information on this market, Request Sample

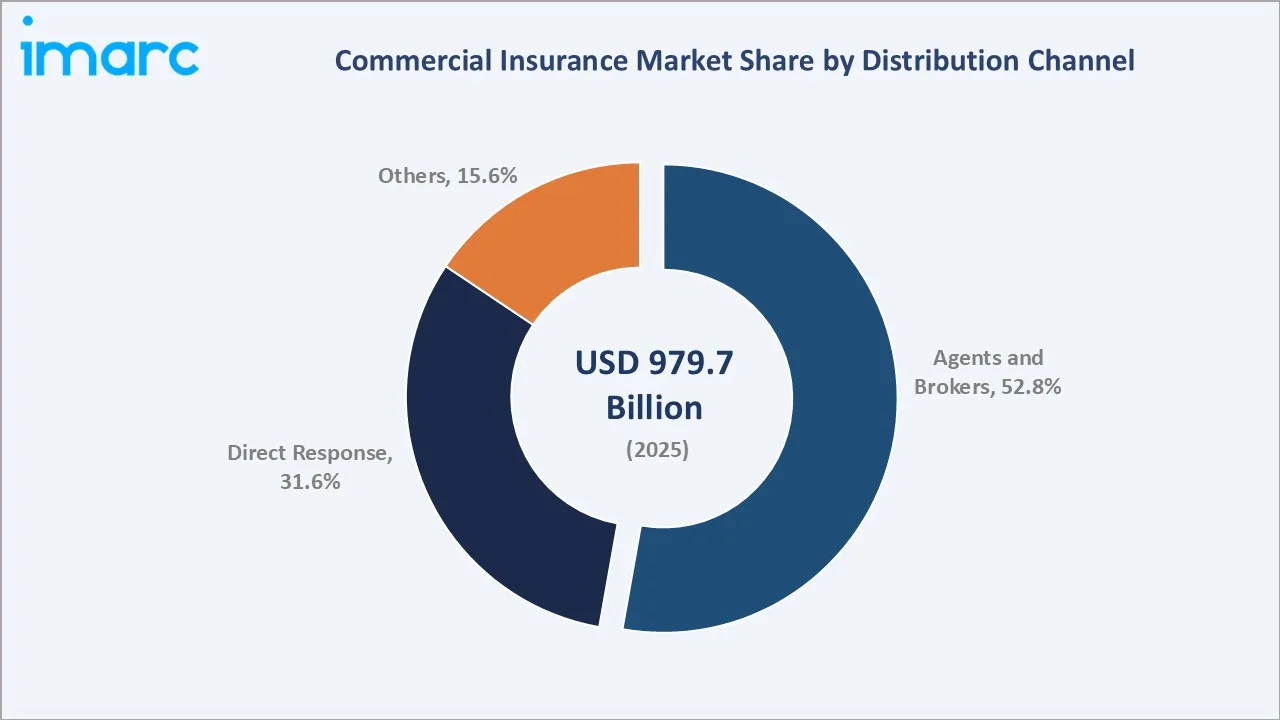

Agents and brokers represent the largest distribution channel at 52.8%, underscoring the relationship-intensive nature of commercial insurance placement. The commercial insurance market forecast through 2034 is shaped by AI-powered underwriting innovation, expansion of cyber and parametric product lines, and the progressive digitalization of broker and direct distribution channels across both developed and emerging markets.

Executive Summary

The global commercial insurance market is expanding on a sustained trajectory, underpinned by rising enterprise risk awareness, climate change-driven catastrophe exposure, and the rapid growth of cyber and technology liability risks. The market reached USD 979.7 Billion in 2025 and is forecast to reach USD 1,701.8 Billion by 2034, reflecting a CAGR of 6.01% over the forecast period.

North America leads globally with a 38.9% share in 2025, driven by the world’s largest commercial insurance market in the United States. Europe follows with 27.4%, anchored by sophisticated corporate risk management practices and stringent mandatory coverage requirements. Asia-Pacific contributes 20.8%, with China, India, and Southeast Asian markets representing the fastest-growing opportunity for commercial insurance penetration.

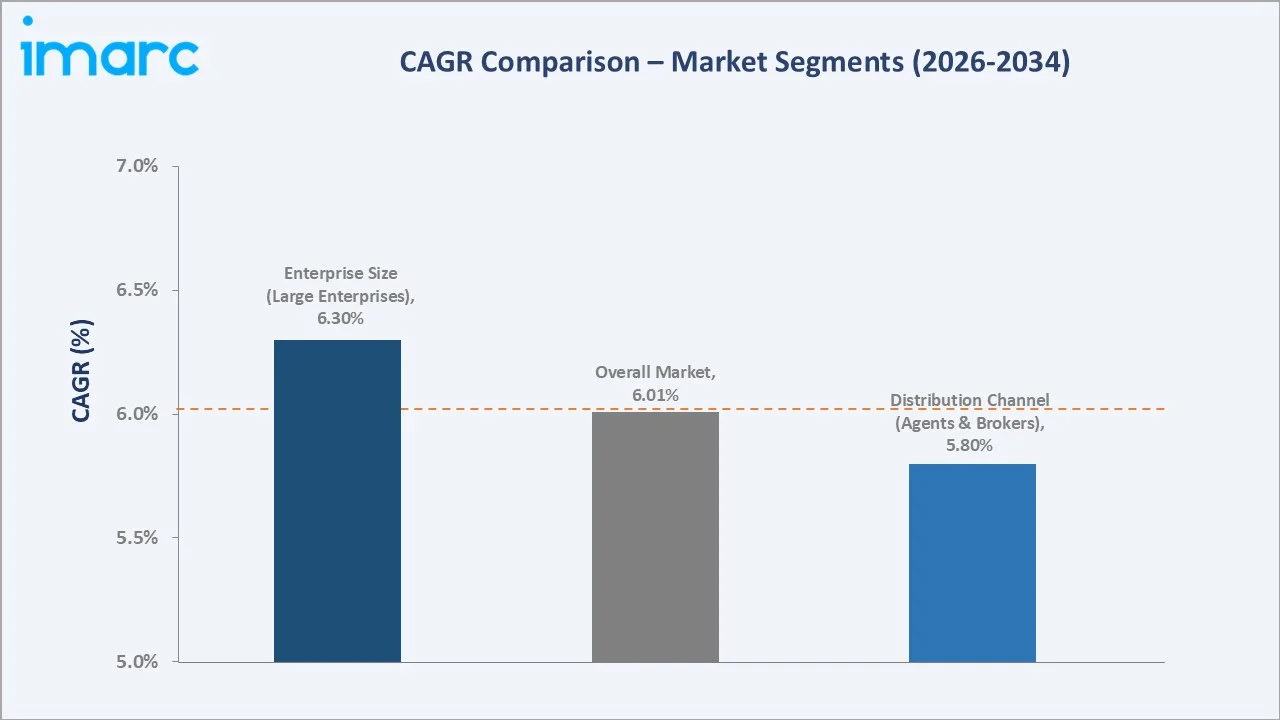

Large enterprises account for 67.3% of the market, while agents and brokers dominate distribution at 52.8%, reflecting the complexity of commercial risk placement that benefits from specialized broker expertise. Key players, including Allianz, AXA, Chubb, Marsh & McLennan Companies Inc., and Zurich, are competing through AI-powered underwriting, specialty product development, and expanded emerging market distribution capabilities.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Enterprise Size) |

Large Enterprises – 67.3% (2025) |

|

Largest Segment (Distribution Channel) |

Agents & Brokers – 52.8% (2025) |

|

Leading Region |

North America – 38.9% share (2025) |

|

Fastest Growing Region |

Asia-Pacific (SME growth + digitalization) |

|

Top Companies |

Allianz, AXA, Chubb, Marsh & McLennan Companies Inc., and Zurich |

Key Analytical Observations:

- Large enterprises account for 67.3% of the commercial insurance market in 2025, reflecting their extensive multi-line coverage requirements spanning property, liability, workers’ compensation, marine, aviation, and professional indemnity lines, generating significantly higher average premium volumes per policyholder than SME clients.

- Agents and brokers hold the dominant distribution position at 52.8% in 2025, as the complexity of commercial insurance placement, requiring coverage design, risk assessment, carrier negotiation, and claims advocacy, continues to drive enterprise buyers toward specialist intermediaries rather than direct purchase channels.

- Asia-Pacific is the fastest-growing region, with China’s commercial insurance market expanding at an estimated 8.5% CAGR through 2034, driven by government-mandated liability coverage, expanding export trade requiring marine and cargo insurance, and rapid SME sector growth in manufacturing and services.

- The commercial insurance market growth in emerging economies is supported by growing awareness of operational risk following high-profile natural catastrophes, supply chain disruptions, and cyber incidents that have demonstrated the financial consequences of inadequate commercial coverage for businesses of all sizes.

Global Commercial Insurance Market Overview

Commercial insurance encompasses the broad category of property, casualty, liability, and specialty insurance products purchased by businesses, institutions, and government entities to protect against operational, financial, and legal risks. Distinct from personal lines insurance serving individual consumers, commercial lines serve organizations ranging from micro-enterprises to Fortune 500 multinationals, requiring bespoke coverage structures, large policy limits, and specialized underwriting expertise.

The primary growth catalyst for the commercial insurance market is the accelerating complexity and frequency of risk events facing enterprises globally. Swiss Re Institute estimates that global insured losses from natural catastrophes reached USD 135 billion in 2024, the fifth consecutive year exceeding USD 100 billion, directly driving commercial property and business interruption premium increases.

The commercial insurance market forecast is further shaped by the proliferation of new risk categories, including cyber liability, supply chain disruption, directors and officers liability, and environmental impairment, that create continuous demand for product innovation and specialized underwriting capacity.

Market Dynamics

To evaluate market opportunities, Request Sample

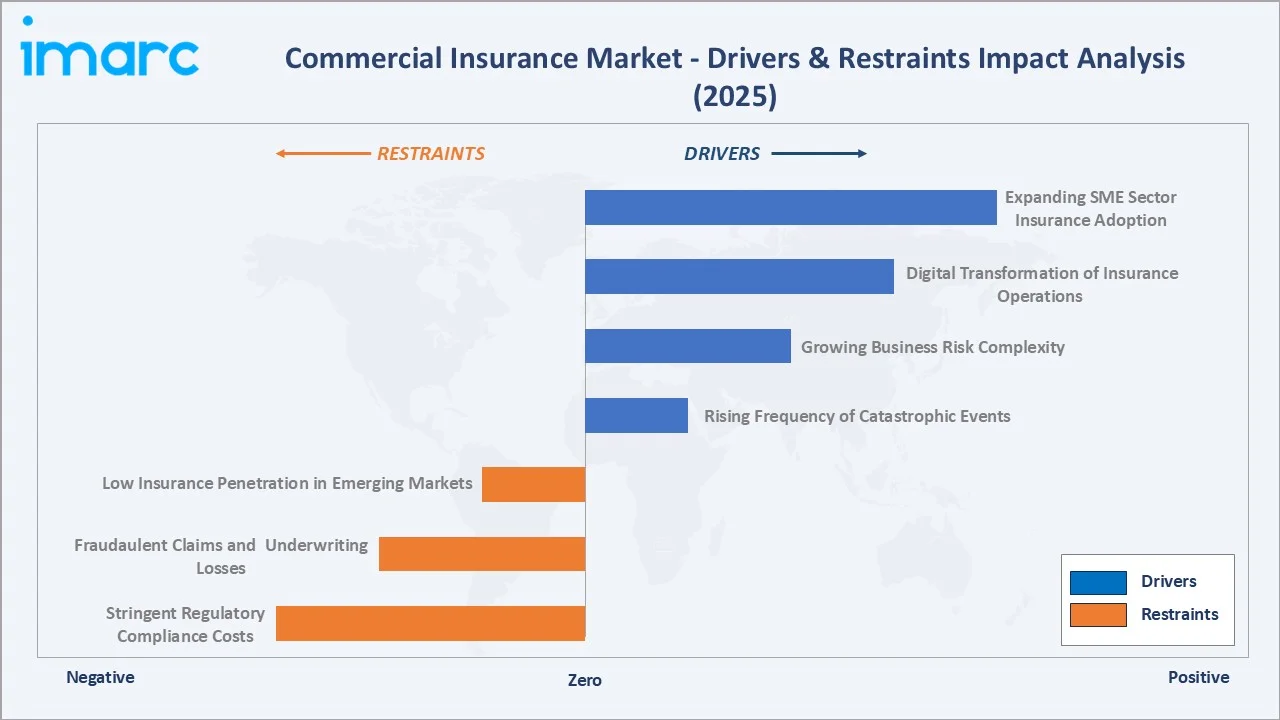

Market Drivers

- Rising Frequency of Catastrophic Events: Swiss Re Institute reported global insured natural catastrophe losses of USD 135 billion in 2024, requiring commercial insurers to deploy additional underwriting capacity while raising premiums across climate-exposed risk categories. The compounding effect of climate change on catastrophe loss frequency is structurally elevating commercial insurance demand across every geography and industry sector.

- Growing Business Risk Complexity: Cyber liability exposure has grown in parallel with enterprise digitalization, with the average cost of a data breach reaching USD 4.88 million in 2024 according to IBM’s annual report. Directors and officers liability, environmental impairment, and political risk coverage are similarly expanding as governance, regulatory, and geopolitical complexity increases for multinational enterprises.

- Digital Transformation of Insurance Operations: AI and machine learning are fundamentally transforming commercial insurance underwriting, pricing, and claims management by offering digital-first small commercial insurance products with instant quoting, binding, and policy management capabilities, expanding the addressable market for commercial coverage among previously underserved small business segments.

- Expanding SME Sector Insurance Adoption: The global SME sector, comprising an estimated 400 million businesses worldwide, represents a structurally underpenetrated commercial insurance opportunity. In developing economies, SME formalization and credit access requirements are driving first-time commercial insurance adoption for property, liability, and trade credit coverage.

Market Restraints

- Stringent Regulatory Compliance Costs: Commercial insurance is one of the most heavily regulated industries globally, subject to solvency capital requirements (Solvency II in Europe, RBC in the U.S.), rate filing regulations, and conduct-of-business rules that impose significant compliance infrastructure costs.

- Fraudulent Claims and Underwriting Losses: Insurance fraud represents an estimated 5–10% of total claims costs globally. High-severity claim years driven by catastrophe events periodically produce combined ratios above 100%, constraining insurer profitability and leading to capacity withdrawals.

- Low Insurance Penetration in Emerging Markets: Despite strong economic growth, commercial insurance penetration in Sub-Saharan Africa, South Asia, and parts of Southeast Asia remains below 2% of GDP, significantly constraining market expansion in these regions.

Market Opportunities

- Cyber Liability and Technology Risk Expansion: The global cyber insurance market is expected to reach approximately USD 30 billion by 2027. As enterprise cyber risk exposure expands with IoT proliferation, AI system dependencies, and evolving ransomware threats, demand for comprehensive cyber coverage is expected to far outpace overall commercial insurance market growth.

- Parametric and Index-Based Insurance Innovation: Parametric commercial insurance products, paying pre-agreed amounts upon specified trigger events rather than assessed actual losses, are gaining traction across agriculture, energy, and infrastructure sectors.

Market Challenges

- Systemic Risk Accumulation and Correlation: Cyber risk, pandemic risk, and geopolitical disruption represent potential systemic loss accumulations that could simultaneously impact millions of commercial insurance policies across multiple lines of business.

- Talent and Underwriting Expertise Scarcity: Complex commercial lines require highly specialized underwriting expertise developed over years of market experience. An aging workforce in specialty insurance segments and competition from technology sectors for data science talent are creating underwriting capacity constraints.

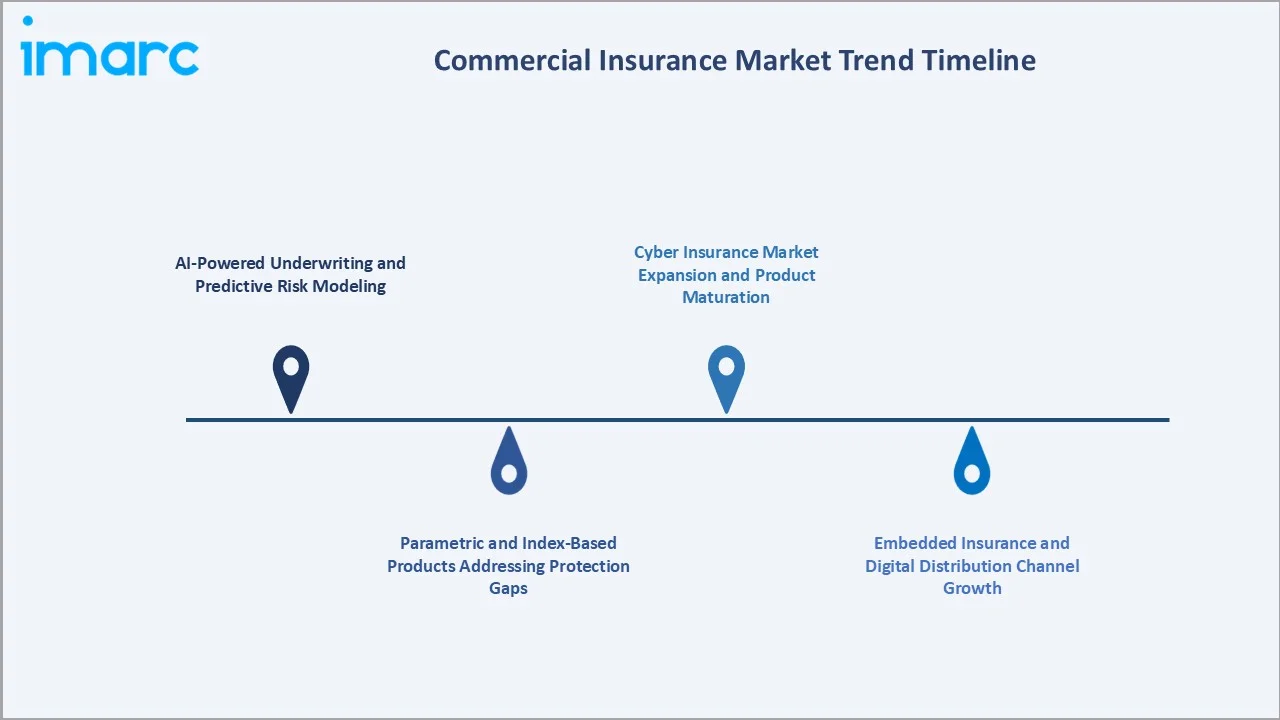

Emerging Market Trends

1. AI-Powered Underwriting and Predictive Risk Modeling

In November 2025, Chubb introduced a new AI‑powered optimization engine within its Chubb Studio platform, using proprietary AI to analyze data and deliver personalized insurance offerings at the point of sale for digital distribution partners. Swiss Re’s sigma research projects that AI-enhanced underwriting will reduce commercial lines combined ratios by 3–5 percentage points industry-wide by 2030, representing tens of billions of dollars in annual profitability improvement for the global commercial insurance industry.

2. Cyber Insurance Market Expansion and Product Maturation

The average cost of a data breach reached USD 4.88 million in 2024, according to IBM’s annual Cost of a Data Breach Report, up 10% from 2023. This directly increases enterprise demand for cyber coverage limits adequate to cover breach response, regulatory fines, business interruption, and third-party liability costs. The commercial insurance market outlook for cyber is exceptionally positive, with premiums projected to reach USD 35+ billion globally by 2028, representing the highest individual line CAGR of any commercial insurance product category through the forecast period.

3. Embedded Insurance and Digital Distribution Channel Growth

B2B platforms, including Shopify, Stripe, and Salesforce, are integrating commercial insurance products directly into their merchant and enterprise software ecosystems, enabling small business operators to purchase coverage with a single click at the point of risk creation. Digital MGAs and insurtech-powered brokers are deploying straight-through processing platforms for small commercial lines that reduce policy issuance time from days to minutes while operating at lower expense ratios than traditional broker channels.

4. Parametric and Index-Based Products Addressing Protection Gaps

Parametric commercial insurance is gaining significant traction as a solution to the protection gaps created by traditional indemnity insurance limitations in covering systemic, slow-onset, and high-frequency weather and climate risks. Swiss Re and Munich Re both reported double-digit growth in parametric commercial insurance structured transactions, with energy, agriculture, and infrastructure sectors representing the largest buyers as enterprises seek reliable, claims-dispute-free risk transfer mechanisms for climate-exposed assets.

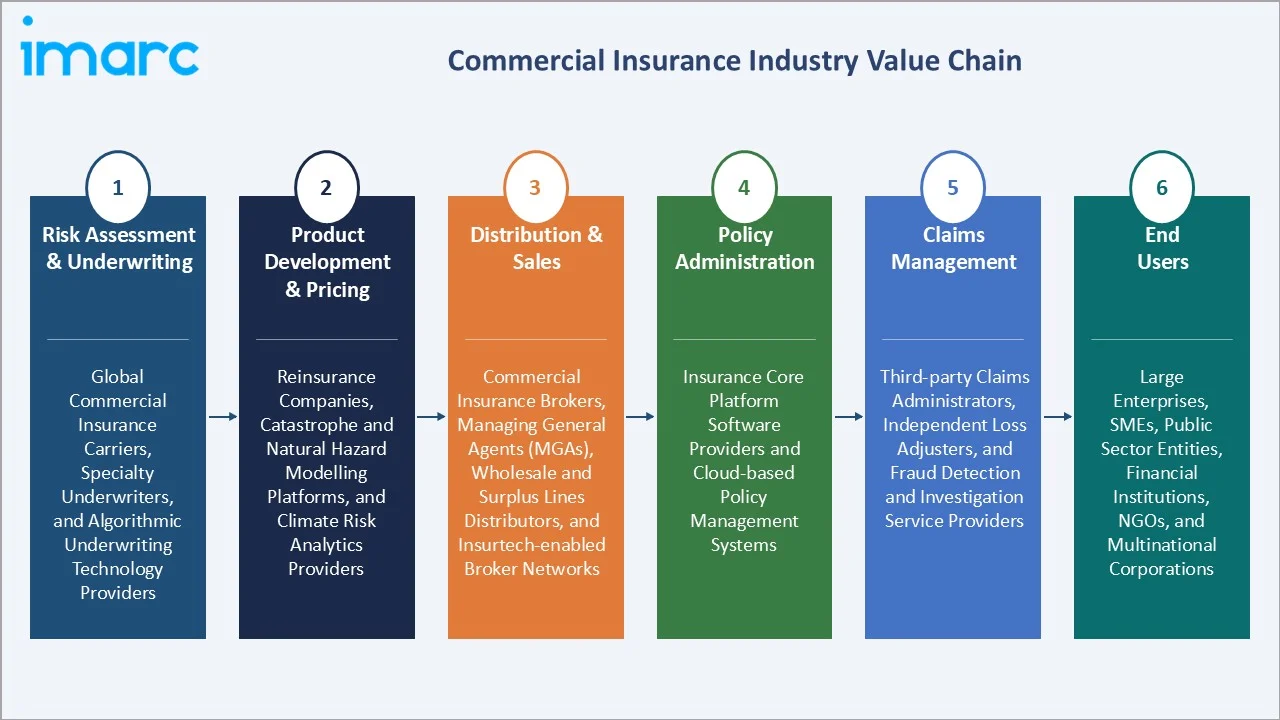

Industry Value Chain Analysis

|

Stage |

Key Players / Examples |

|

Risk Assessment & Underwriting |

Global commercial insurance carriers, specialty underwriters, and algorithmic underwriting technology providers |

|

Product Development & Pricing |

Reinsurance companies, catastrophe and natural hazard modelling platforms, and climate risk analytics providers |

|

Distribution & Sales |

Commercial insurance brokers, managing general agents (MGAs), wholesale and surplus lines distributors, and insurtech-enabled broker networks |

|

Policy Administration |

Insurance core platform software providers and cloud-based policy management systems |

|

Claims Management |

Third-party claims administrators, independent loss adjusters, and fraud detection and investigation service providers |

|

End Users |

Large enterprises, SMEs, public sector entities, financial institutions, NGOs, multinational corporations |

Technology Landscape in the Commercial Insurance Industry

AI-Powered Underwriting and Pricing Engines

Cytora and LexisNexis Risk Solutions have formed a strategic relationship to embed LexisNexis’s advanced data and analytics into Cytora’s AI‑enabled underwriting platform, helping U.S. commercial insurers automate risk selection and improve speed and accuracy in submission triage and entity resolution. This integration aims to reduce manual work, enrich risk data, and streamline underwriting workflows for faster, more data‑driven decision‑making.

Insurtech and Digital Distribution Platforms

API-first commercial insurance platforms are enabling real-time policy quoting, binding, and issuance for small and medium commercial lines at speeds previously impossible through traditional broker workflows. Embedded insurance technology providers, including Boost Insurance, are enabling non-insurance businesses to offer commercial coverage products directly to their SME customers.

Catastrophe Modeling and Climate Risk Analytics

Next-generation catastrophe models incorporating climate change scenario analysis, satellite earth observation data, and high-resolution atmospheric modeling are improving commercial property underwriters’ ability to assess long-term climate risk accumulation in their portfolios. Moody’s RMS launched its Risk Modeler cloud platform in 2024, enabling insurers to run real-time catastrophe analytics on commercial property portfolios at 90-meter spatial resolution.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Liability Insurance |

14.5% |

2025 |

| Enterprize Size | Large Enterprises |

67.3% |

2025 |

| Distribution Channel | Agents and Brokers |

🔒 |

2025 |

| Industry Vertical | Transportation and Logistics |

🔒 |

2025 |

|

Region |

North America |

38.9% |

2025 |

By Enterprise Size

Large enterprises dominate the commercial insurance market with a 67.3% share in 2025. Their market dominance reflects both the scale and complexity of commercial risk exposures that large organizations face, spanning multinational property portfolios, extensive employer liability, complex supply chains, significant D&O and financial lines exposure, and increasingly material cyber risk.

To access detailed market analysis, Request Sample

Small and medium-sized enterprises hold a 32.7% share (2025). The SME segment is growing faster than the large enterprise segment, driven by increasing SME risk awareness, digitally-enabled distribution improvements, and mandatory coverage requirements expanding in key growth markets.

By Distribution Channel

Agents and brokers lead the distribution channel segment with a 52.8% share in 2025. Their dominant position in commercial insurance distribution reflects the relationship-intensive, consultative nature of commercial risk placement. Complex commercial accounts, involving multi-line coverage programs, multinational risk transfer structures, and large policy limits, require the specialized expertise, carrier relationships, and negotiating leverage that professional brokers provide.

Direct response holds 31.6% (2025), growing as digital platforms enable insurers to efficiently service small commercial accounts directly without broker intermediation. The other segment at 15.6% encompasses bancassurance partnerships, embedded insurance integrations, managing general agents, and wholesale market placements through Lloyd’s of London and surplus lines markets for non-standard commercial risks.

Regional Market Insights

North America’s market dominance (38.9%, 2025) reflects the United States’ position as the world’s largest single commercial insurance market, accounting for approximately USD 340 billion in commercial premiums annually. The U.S. market benefits from a highly sophisticated broker distribution network, diversified carrier competition, robust reinsurance capacity, and a litigation environment that drives high demand for liability coverage.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

38.9% |

Cyber risk growth, catastrophe exposure, D&O liability surge |

|

Europe |

27.4% |

Mandatory liability coverage, ESG risk, and Solvency II compliance requirements |

|

Asia-Pacific |

20.8% |

China SME growth, India infrastructure, aviation, and marine expansion |

|

Latin America |

7.2% |

Infrastructure investment, agriculture risk, political risk in corporates |

|

Middle East & Africa |

5.7% |

Oil & gas project risk, Vision 2030, Saudi Arabia, infrastructure development |

The SEC’s 2023 cyber disclosure rules requiring public companies to report material cyber incidents within 96 hours have significantly accelerated cyber insurance adoption among U.S. public companies, with corporate cyber insurance attachment rates rising from 47% to 68% between 2021 and 2024.

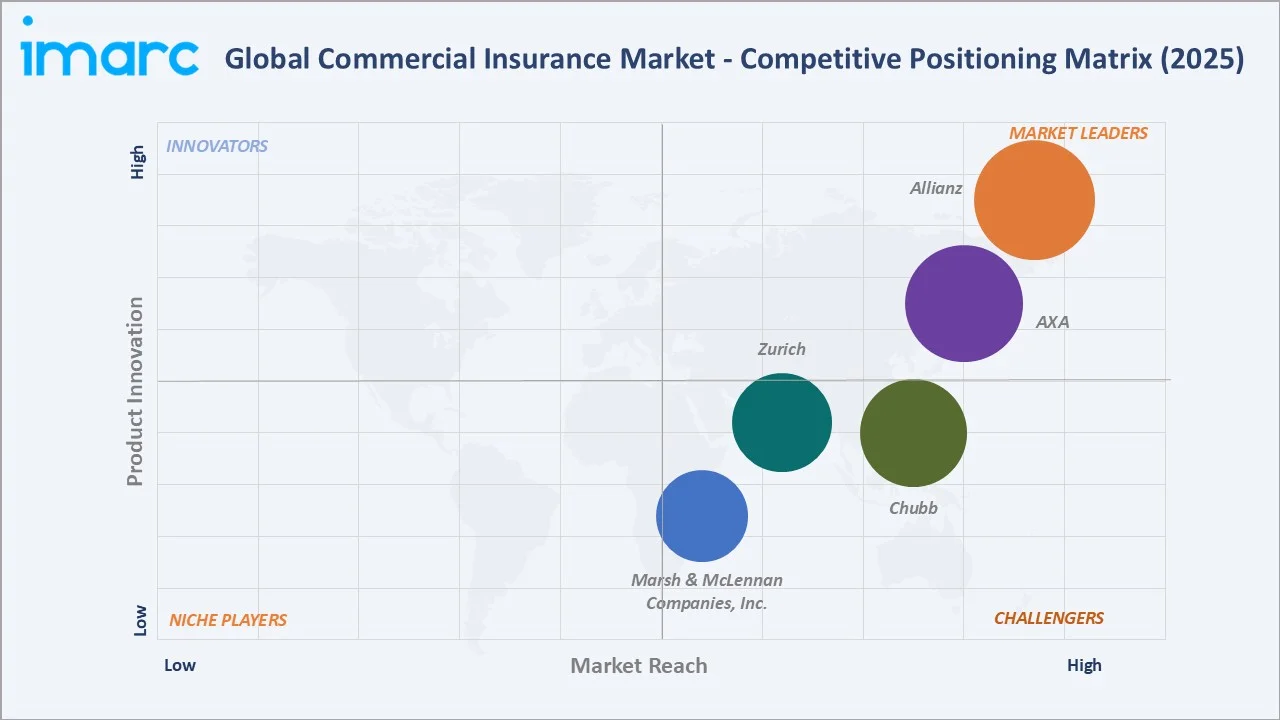

Competitive Landscape

The global commercial insurance market exhibits moderate concentration at the multinational carrier level, with the top operators, Allianz, AXA, Chubb, Marsh & McLennan Companies Inc., and Zurich, collectively representing approximately 25–30% of global commercial premiums.

|

Company |

Brand / Platform/Programs |

Market Position |

Core Strength |

|

Allianz |

Allianz Commercial |

Market Leader |

World's largest insurer by AUM; 70+ country commercial footprint; full multi-line underwriting breadth and depth |

|

AXA |

AXA XL |

Market Leader |

Global commercial P&C and specialty leader; AXA XL wholesale and excess/surplus lines positioning worldwide |

|

Chubb |

Chubb Commercial |

Strong Challenger |

World's largest publicly traded P&C insurer; superior underwriting discipline; AI-driven small commercial platform |

|

Zurich |

Zurich Commercial |

Strong Challenger |

Global corporate P&C specialty; risk engineering expertise; digital commercial product development leadership |

|

Marsh & McLennan Companies, Inc. |

Marsh Risk |

Challenger |

World's largest insurance broker; USD 23B revenue; Sentrisk AI supply chain risk analytics; McGriff acquisition |

A substantial second tier of national champions, specialty insurers, Lloyd’s syndicates, and mutual insurers accounts for the remaining market share. Competitive differentiation is driven by underwriting capacity and financial strength, product breadth and specialization, global distribution network reach, technology investment, and claims service reputation.

Key Company Profiles

Allianz

Allianz, headquartered in Munich, Germany, is the world’s largest insurance company by assets under management and one of the leading commercial insurance underwriters globally. Allianz’s commercial insurance operations span property, liability, marine, aviation, energy, financial lines, and cyber coverage across 70+ countries and territories through its Allianz Commercial business unit.

- Product Portfolio: Global corporate property and casualty; cyber liability; marine and aviation; energy and construction; financial lines; parametric weather products.

- Recent Developments: In March 2026, Allianz Commercial has entered a strategic agreement with Reel Media, under which Reel Media will manage Allianz’s international Entertainment underwriting business (outside the U.S.) from April 1, 2026.

- Strategic Focus: Cyber product leadership; AI-powered underwriting through Allianz Commercial digital platform; ESG risk consulting integration; Asia-Pacific commercial lines growth.

Chubb

Chubb, headquartered in Zurich, Switzerland, is the world’s largest publicly traded property and casualty insurance company. Chubb serves multinational corporations, mid-market companies, and small businesses across property, casualty, accident, health, and specialty lines.

- Product Portfolio: Commercial property and general liability; workers’ compensation; environmental liability; cyber and technology; management liability (D&O, EPLI); surety and fidelity.

- Recent Developments: Chubb’s first‑quarter 2026 profit soared 74.3% to $2.32 billion, driven by strong investment income and lower catastrophe losses, while P&C net premiums written rose 7.2% with commercial insurance up about 4.6%.

- Strategic Focus: Digital transformation of middle market and small commercial distribution; Asia-Pacific market penetration; specialty lines capacity expansion; cyber insurance product development.

Marsh & McLennan Companies, Inc.

Marsh & McLennan, headquartered in New York, is the world’s largest insurance broker and risk management firm, with annual revenues of around USD 27 billion in 2026. Through its Marsh, Guy Carpenter, Mercer, and Oliver Wyman subsidiaries, the company advises enterprises on risk management strategy, insurance program design, reinsurance placement, and analytics.

- Product Portfolio: Commercial insurance brokerage (Marsh Risk); HR and benefits consulting (Mercer); management consulting (Oliver Wyman); Sentrisk AI risk platform.

- Recent Developments: In April 2026, Marsh partnered with Formula 1 as an Official Risk Partner and Official Insurance Brokering Partner to amplify its global risk management and insurance capabilities through association with the sport’s massive fanbase.

- Strategic Focus: AI-powered risk analytics differentiation; middle market commercial broking expansion; climate risk advisory growth; cyber risk quantification leadership.

Market Concentration Analysis

The commercial insurance market exhibits moderate-to-low concentration, with the top five global underwriting groups collectively accounting for approximately 25–30% of total commercial premiums in 2025. The distribution of market share reflects the local nature of commercial insurance regulation, distribution, and risk assessment, which sustains national champions and regional specialists alongside global players.

Consolidation activity in commercial insurance has focused on broking rather than underwriting, with the USD 7.75 billion Marsh McLennan acquisition of McGriff Insurance Services in 2024 representing the largest broking transaction in a decade. On the carrier side, InsurTech-backed MGAs are gaining market share in small commercial lines by using AI and digital distribution to service segments that traditional carriers find operationally expensive.

Investment & Growth Opportunities

Fastest Growing Segments

Cyber liability insurance (estimated CAGR 18%+), parametric and index-based commercial products (CAGR 12%), and SME digital commercial platforms (CAGR 10.5%) represent the three highest-growth investment vectors through 2034. Together, these niches address a total addressable sub-market exceeding USD 180 billion by 2030.

Emerging Market Expansion

India, Indonesia, Vietnam, Saudi Arabia, and Nigeria collectively represent an incremental USD 280 billion commercial insurance opportunity by 2034, driven by rapid economic formalization, expanding trade finance requirements, and government infrastructure investment programs that mandate commercial coverage.

Venture and Institutional Investment Trends

- Key investment themes in commercial insurance technology include AI underwriting engines, cyber risk quantification platforms, parametric insurance infrastructure, embedded commercial insurance APIs, and climate risk analytics for real estate and infrastructure portfolios.

- Private equity continues to invest heavily in insurance distribution, with commercial broking platforms commanding premium valuations reflecting the recurring revenue, low capital intensity, and cross-selling potential of commercial insurance intermediary businesses.

Future Market Outlook (2026-2034)

The global commercial insurance market is positioned for sustained, broad-based growth through 2034. From a base of USD 979.7 Billion in 2025, the market is projected to reach USD 1,701.8 Billion by 2034, representing total incremental value creation of approximately USD 722.1 Billion over the forecast decade, at a CAGR of 6.01%.

Three structural macro-themes underpin this trajectory: the escalating cost and frequency of natural catastrophe and cyber events creating permanent demand increases for commercial coverage; the ongoing digital transformation of commercial insurance operations enabling more efficient risk assessment and distribution; and expanding global economic activity in developing markets creating new commercial insurance demand pools.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 140 industry participants in 2024–2025, including commercial insurance underwriters, insurance brokers, risk managers, actuaries, insurtech executives, reinsurance professionals, and enterprise buyers across North America, Europe, and Asia-Pacific.

Secondary Research

Secondary research encompassed a systematic review of company annual reports, Swiss Re sigma studies, Marsh McLennan market indices, AM Best rating reports, Lloyd’s of London annual reports, regulatory filings, industry publications (Business Insurance, Reactions, Insurance Insider), and publicly available financial data. Over 250 secondary sources were reviewed and triangulated.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating global GDP growth projections, commercial insurance premium-to-GDP ratio trend analysis, line-by-line growth rate forecasting, and historical market evolution from 2020 to 2025.

Commercial Insurance Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Liability Insurance, Commercial Motor Insurance, Commercial Property Insurance, Marine Insurance, Others |

| Enterprise Sizes Covered | Large Enterprises, Small and Medium-sized Enterprises |

| Distribution Channels Covered | Agents and Brokers, Direct Response, Others |

| Industry Verticals Covered | Transportation and Logistics, Manufacturing, Construction, IT and Telecom, Healthcare, Energy and Utilities, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Allianz, AXA, Chubb, Zurich, Marsh & McLennan Companies, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the commercial insurance market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global commercial insurance market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the commercial insurance industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Commercial Insurance Market Report

The global commercial insurance market reached USD 979.7 Billion in 2025. It is projected to reach USD 1,701.8 Billion by 2034.

The commercial insurance market is expected to grow at a CAGR of 6.01% during the forecast period, driven by rising catastrophe frequency, cyber risk expansion, and digital distribution growth.

North America leads with a 38.9% share in 2025, driven by the world’s largest commercial insurance market in the United States.

Large enterprises dominate with a 67.3% share in 2025 (approx. USD 659.3 Billion), driven by their extensive multi-line coverage requirements.

Agents and brokers lead distribution with a 52.8% share in 2025, reflecting the complexity of commercial risk placement that requires specialist intermediary expertise.

Key players include Allianz, AXA, Chubb, Marsh & McLennan Companies Inc., and Zurich.

Key drivers include rising catastrophic event frequency from climate change, growing cyber risk exposure, AI-powered underwriting transformation, expanding SME insurance adoption, and the emergence of new risk categories requiring specialized commercial coverage.

High-value opportunities include cyber liability insurance platforms, AI underwriting technology, parametric commercial products, SME-focused digital distribution platforms, and commercial insurance market expansion in Asia-Pacific and Middle Eastern emerging market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)