Community Cloud Market Size, Share, Trends and Forecast by Component, Application, Industry Vertical, and Region 2026-2034

Global Community Cloud Market Size, Share, Trends & Forecast (2026-2034)

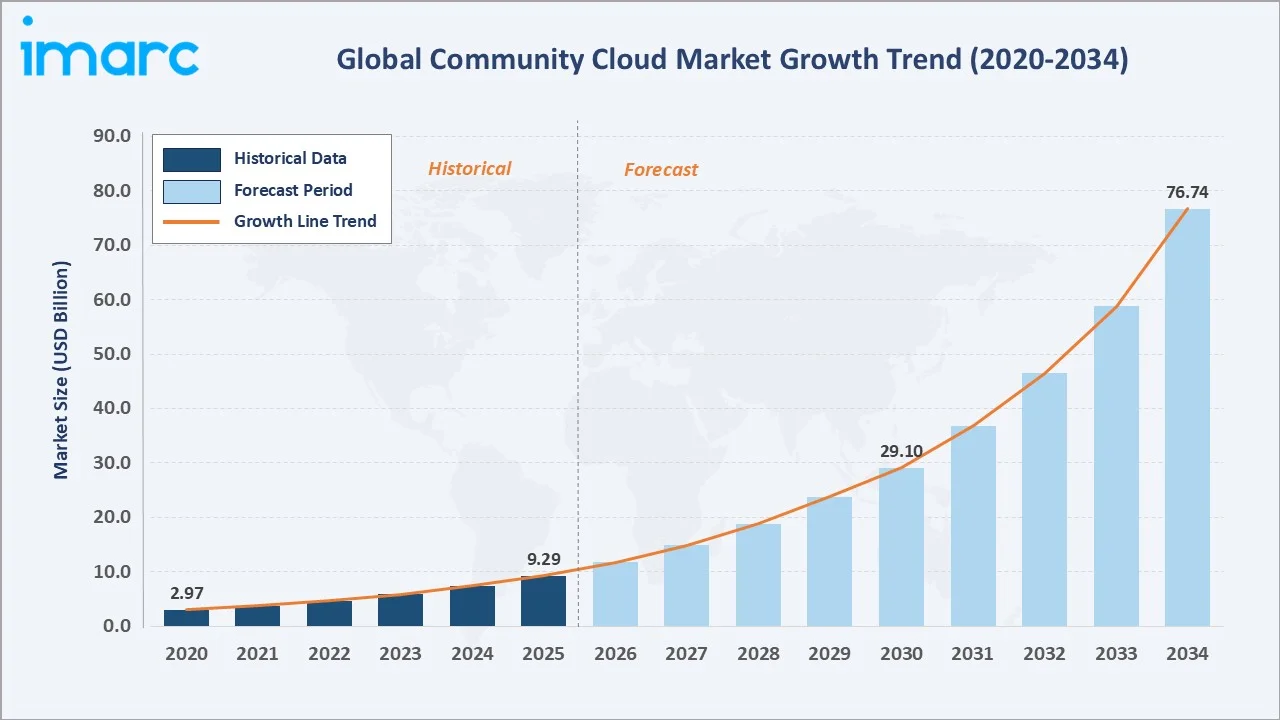

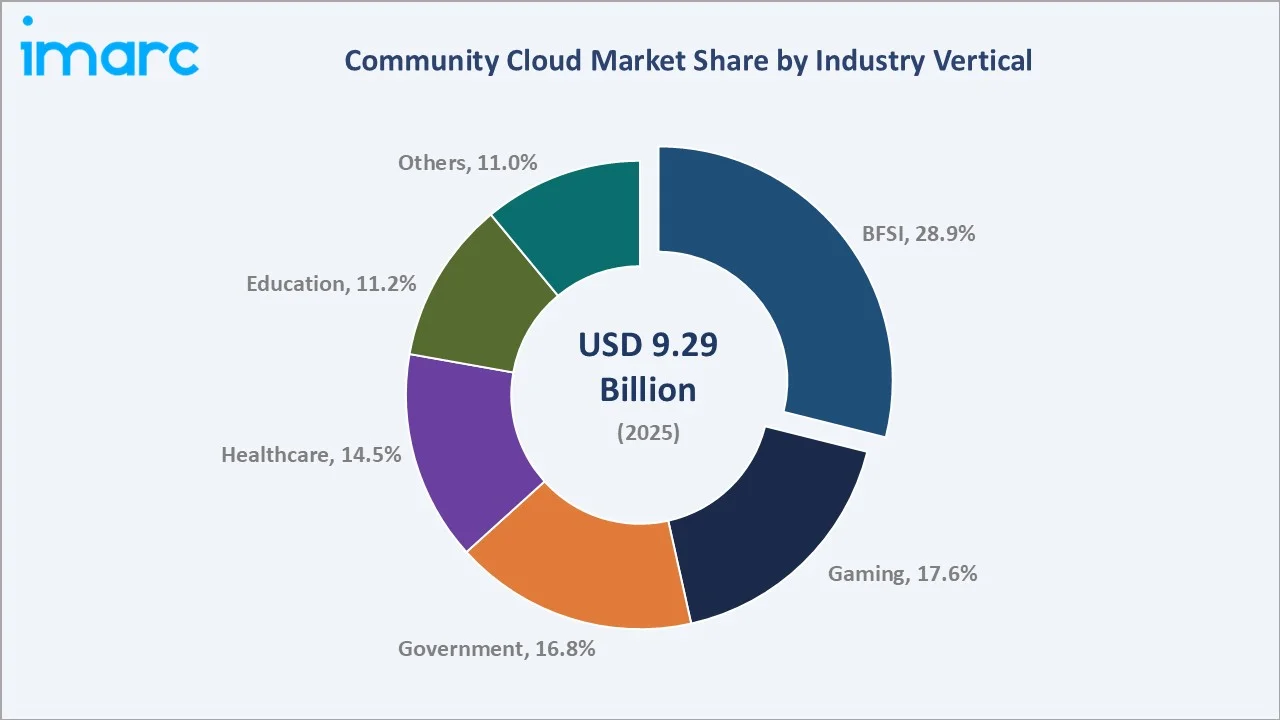

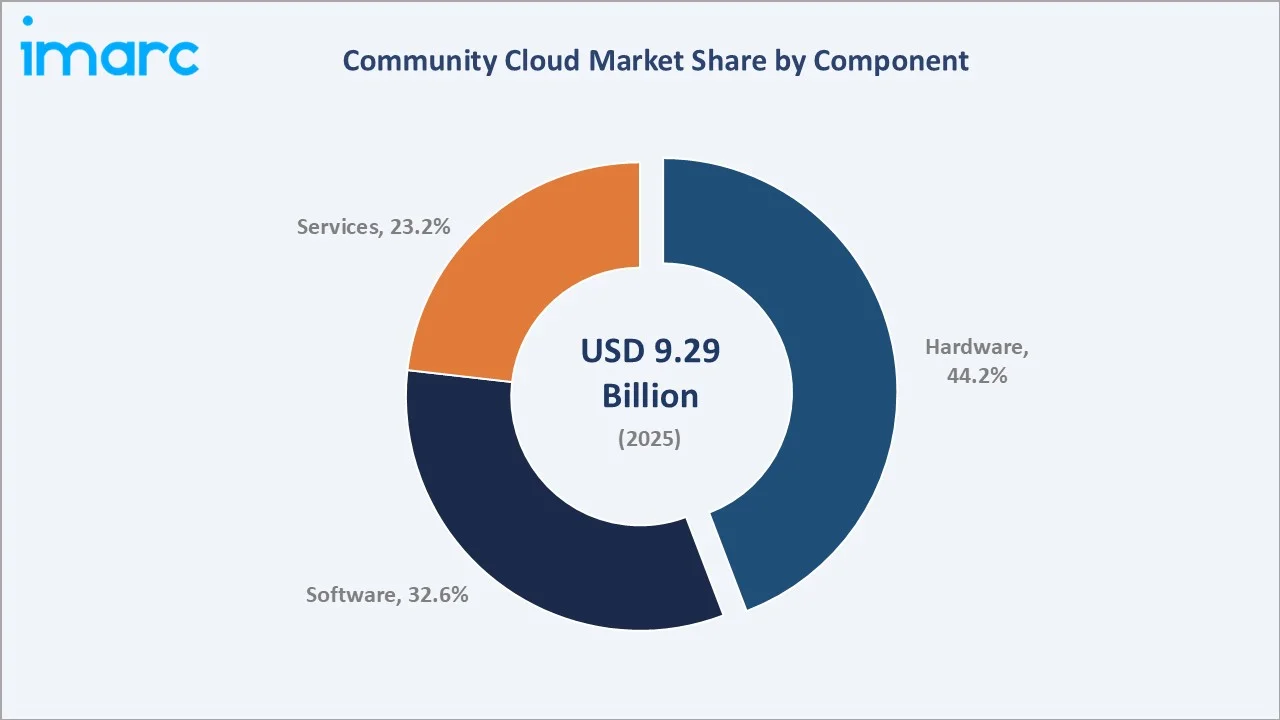

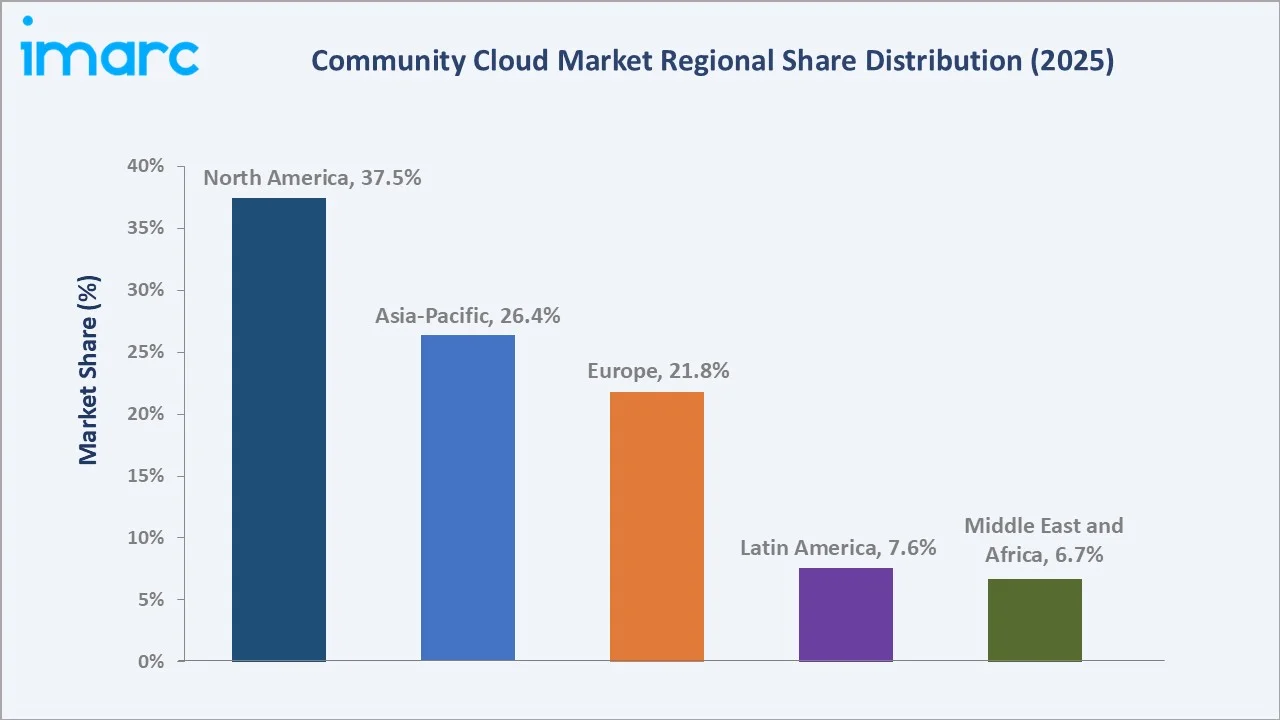

The global community cloud market size was valued at USD 9.3 Billion in 2025 and is projected to reach USD 76.7 Billion by 2034, exhibiting a CAGR of 25.64% during the forecast period 2026-2034. Rising demand for sector-specific, secure, and regulatory-compliant cloud environments is driving the community cloud market growth. BFSI leads industry verticals at 28.9% in 2025, while Hardware dominates the component segment at 44.2%. North America accounts for 37.5% of global revenue in 2025, the world's largest regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 9.3 Billion |

|

Forecast Market Size (2034) |

USD 76.7 Billion |

|

CAGR (2026-2034) |

25.64% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (37.5% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific (CAGR ~31.2%) |

|

Leading Industry Vertical |

BFSI (28.9%, 2025) |

|

Leading Component |

Hardware (44.2%, 2025) |

The global community cloud market growth trajectory from 2020 through 2034, contrasting a consistent historical expansion base against a sustained forecast curve powered by regulatory compliance demands, AI integration, and sector-specific cloud adoption.

To get more information on this market, Request Sample

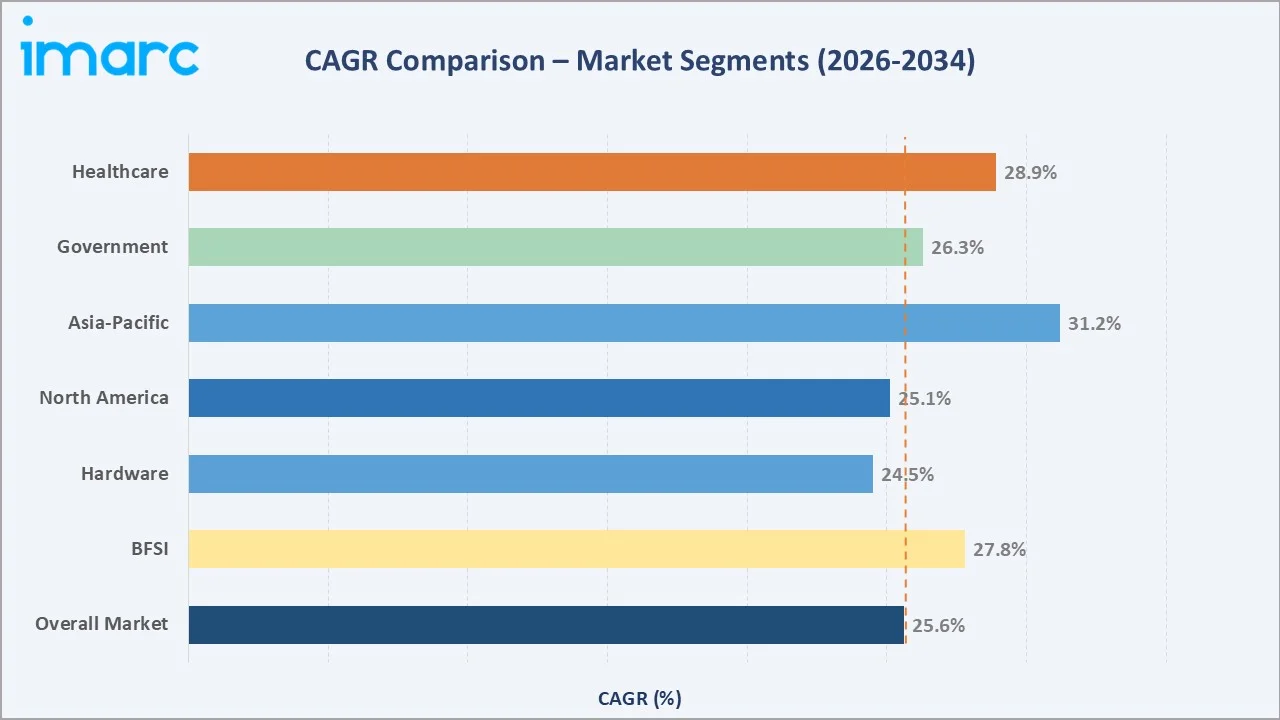

Segment-level CAGR comparisons highlighting Asia-Pacific and BFSI as the two fastest-growing categories within the global community cloud industry analysis through 2034.

Executive Summary

The global community cloud market is undergoing a fundamental transformation driven by escalating regulatory mandates, cross-organizational data collaboration requirements, and the accelerating integration of artificial intelligence across regulated industries. Valued at USD 9.3 Billion in 2025, the market is forecast to reach USD 76.7 Billion by 2034 at a CAGR of 25.64%.

BFSI commands the dominant industry vertical share at 28.9% in 2025, driven by stringent compliance requirements for shared fraud detection, anti-money laundering frameworks, and secure interbank data exchange. Hardware leads the component segment at 44.2%, reflecting the physical infrastructure intensity of private and hybrid community cloud deployments in government and healthcare sectors. The Asia-Pacific region is the fastest-growing market, driven by China's domestic cloud governance frameworks, India's cloud-first government policy, and rapid digital transformation across Southeast Asian financial services.

North America dominates with a 37.5% global revenue share in 2025, led by the United States, where FedRAMP-compliant community cloud solutions underpin federal interagency collaboration and healthcare network connectivity. Across Europe, GDPR enforcement and the EU's GAIA-X sovereign cloud initiative are creating structured demand for compliant shared cloud ecosystems. The community cloud market forecast signals robust expansion, with sovereign cloud mandates, edge-to-cloud AI convergence, and sector-specific platform maturity sustaining growth momentum through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Industry Vertical |

BFSI – 28.9% share (2025) |

|

Leading Component |

Hardware – 44.2% share (2025) |

|

Leading Region |

North America – 37.5% revenue share (2025) |

|

Fastest Growing Region |

Asia-Pacific – CAGR ~31.2% (2026-2034) |

|

Top Companies |

AWS, Microsoft, Google, IBM, Oracle, Alibaba |

|

Market Opportunity |

Sovereign & AI-integrated community cloud platforms |

Key Analytical Observations Supporting The Above Data:

- BFSI's 28.9% dominance in 2025 reflects the sector's need for shared fraud detection systems, regulatory audit infrastructure, and secure interbank collaboration across multi-institutional cloud environments.

- Hardware leads the component segment at 44.2% in 2025, driven by private and hybrid community cloud deployments in regulated industries that require dedicated physical infrastructure for data sovereignty compliance.

- North America's 37.5% global dominance in 2025 reflects the United States' leadership in FedRAMP-compliant government cloud programs and HIPAA-aligned healthcare community cloud platforms.

- Asia-Pacific's ~31.2% CAGR through 2034 reflects China's domestic cloud governance, India's MeghRaj initiative, and Southeast Asia's rapid financial sector digitalization, driving community cloud adoption.

- Sovereign cloud mandates across the EU (GDPR, GAIA-X), GCC (UAE Cloud-First, Saudi Vision 2030), and Asia-Pacific are the most powerful structural demand drivers for the community cloud market through 2034.

Global Community Cloud Market Overview

Community cloud is a cloud deployment model where infrastructure is shared exclusively among organizations with common regulatory, operational, or industry-specific requirements. Unlike public clouds, community clouds offer controlled access, shared governance frameworks, and collaborative security policies tailored to sectors such as BFSI, healthcare, government, gaming, and education. These platforms support workloads including cloud-based storage, backup and disaster recovery, cloud security and data privacy, high-performance computing, and analytics applications.

Applications span the full spectrum of regulated industries: financial consortia managing anti-fraud systems, hospital networks sharing patient EHR data under HIPAA, government agencies managing interagency intelligence, and university clusters supporting collaborative research. Macroeconomic enablers include accelerating digital transformation globally, rising data sovereignty regulations, and surging AI workload requirements—driving enterprises away from generic public cloud toward purpose-built community environments.

Market Dynamics

To evaluate market opportunities, Request Sample

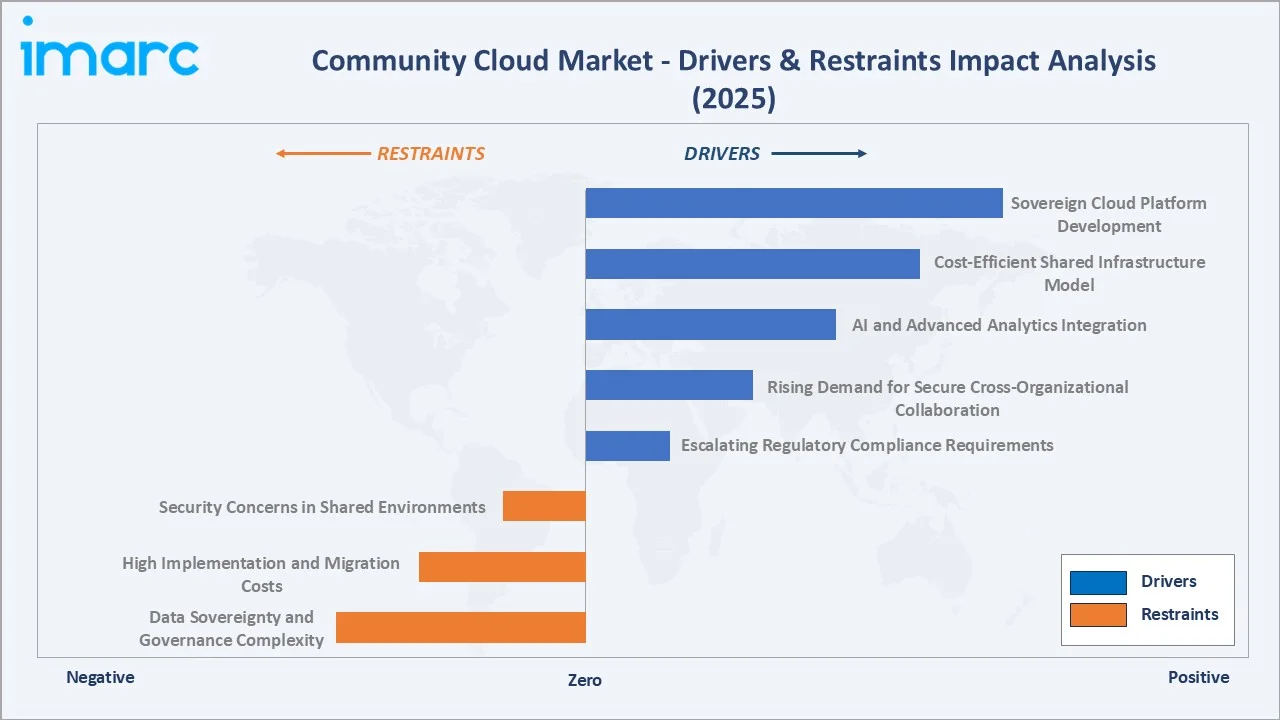

Market Drivers

- Escalating Regulatory Compliance Requirements: Stringent regulations such as HIPAA, GDPR, Basel III, and FedRAMP are driving adoption of community clouds as compliant, sector-specific infrastructure for regulated industries.

- Rising Demand for Secure Cross-Organizational Collaboration: Community clouds enable secure data sharing and collaboration across institutions while maintaining governance controls, supporting use cases like healthcare interoperability and government data exchange, especially in mature markets like the United States.

- AI and Advanced Analytics Integration: AI-enabled community clouds support real-time threat detection, predictive compliance, and collaborative analytics in regulated sectors, enhancing operational efficiency and enabling intelligent automation across multi-organization environments.

- Cost-Efficient Shared Infrastructure Model: By distributing infrastructure and compliance costs across multiple tenants, community clouds reduce capital expenditure compared to private clouds, making them attractive for mid-sized institutions with limited IT budgets

Market Restraints

- Data Sovereignty and Governance Complexity: Cross-border data sharing in community clouds creates regulatory and localization challenges. The Thales Group 2025 Cloud Security Study highlights growing complexity in securing multi-cloud and shared environments.

- High Implementation and Migration Costs: Migration from legacy systems requires substantial upfront investment in redesign, integration, and governance frameworks, slowing adoption among smaller or resource-constrained organizations.

- Security Concerns in Shared Environments: Multi-tenant architectures introduce risks such as insider threats and shared resource vulnerabilities, requiring continuous investment in zero-trust security, identity management, and compliance monitoring systems.

Market Opportunities

- Sovereign Cloud Platform Development: Government-led initiatives such as GAIA-X and MeghRaj are accelerating demand for locally governed, compliance-focused community cloud platforms across regions.

- AI-Powered Compliance Automation: AI integration into compliance workflows—such as automated audits and predictive risk analytics—offers high-margin opportunities, improving efficiency and reducing regulatory management costs.

- Sector-Specific Platform Expansion: Industries like healthcare, education, and gaming present strong growth potential, driven by increasing demand for secure, collaborative, and compliant cloud ecosystems tailored to sector-specific requirements.

Market Challenges

- OS and Platform Fragmentation: Diverse regulatory requirements across community members necessitate complex, multi-standard technology stacks. Ensuring interoperability between legacy on-premise systems and modern community cloud architectures adds significant technical and financial complexity to deployment programs.

- Talent and Expertise Shortage: Specialized expertise in community cloud architecture, compliance engineering, and federated identity management is in short supply globally. This talent gap extends deployment timelines and increases the total cost of community cloud implementation for regulated industry clients.

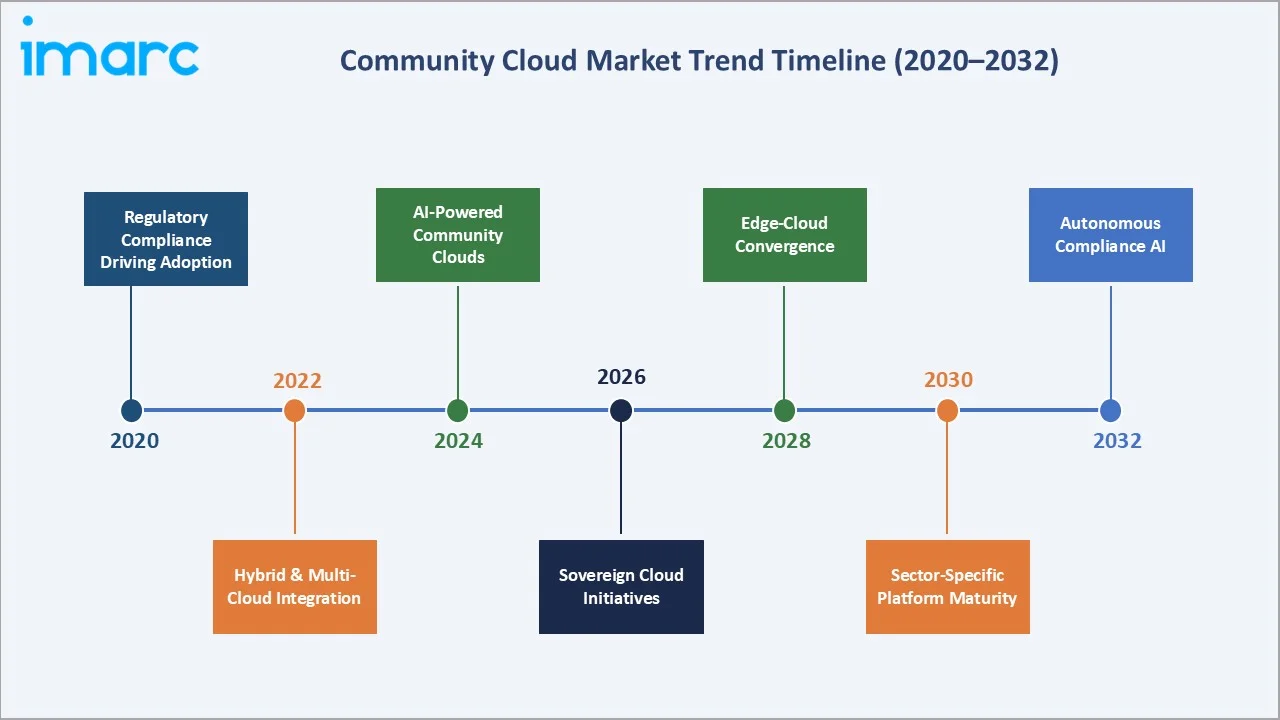

Emerging Market Trends

1. AI and Machine Learning Integration: Transforming Community Cloud Operations

AI-driven capabilities are transforming community clouds through real-time threat detection, predictive compliance, and automated reporting. BFSI and healthcare lead adoption, leveraging AI for fraud analytics and diagnostics within governed, multi-institution environments.

2. Acceleration of Hybrid and Multi-Cloud Community Architectures

Organizations are integrating community clouds into hybrid and multi-cloud strategies, isolating sensitive workloads while using public cloud for scale. Gartner highlights strong growth in cloud spending driven by complex, regulated multi-cloud deployments.

3. Sovereign and Sector-Specific Community Cloud Initiatives

Government-led frameworks like GAIA-X and MeghRaj are accelerating sovereign community cloud adoption, ensuring data localization, regulatory compliance, and sector-specific cloud ecosystems.

4. Edge-to-Cloud Convergence for Regulated Industry Workloads

Edge computing integrated with community cloud enables real-time processing with centralized governance. This supports healthcare IoT, industrial systems, and smart city platforms requiring low latency and compliance-controlled data synchronization.

5. Blockchain-Integrated Community Cloud for Immutable Compliance

Blockchain-enabled community clouds support immutable audit trails and secure data sharing across institutions. Adoption is growing in finance, legal, and supply chains to meet compliance requirements under regulations like MiFID II and SOX.

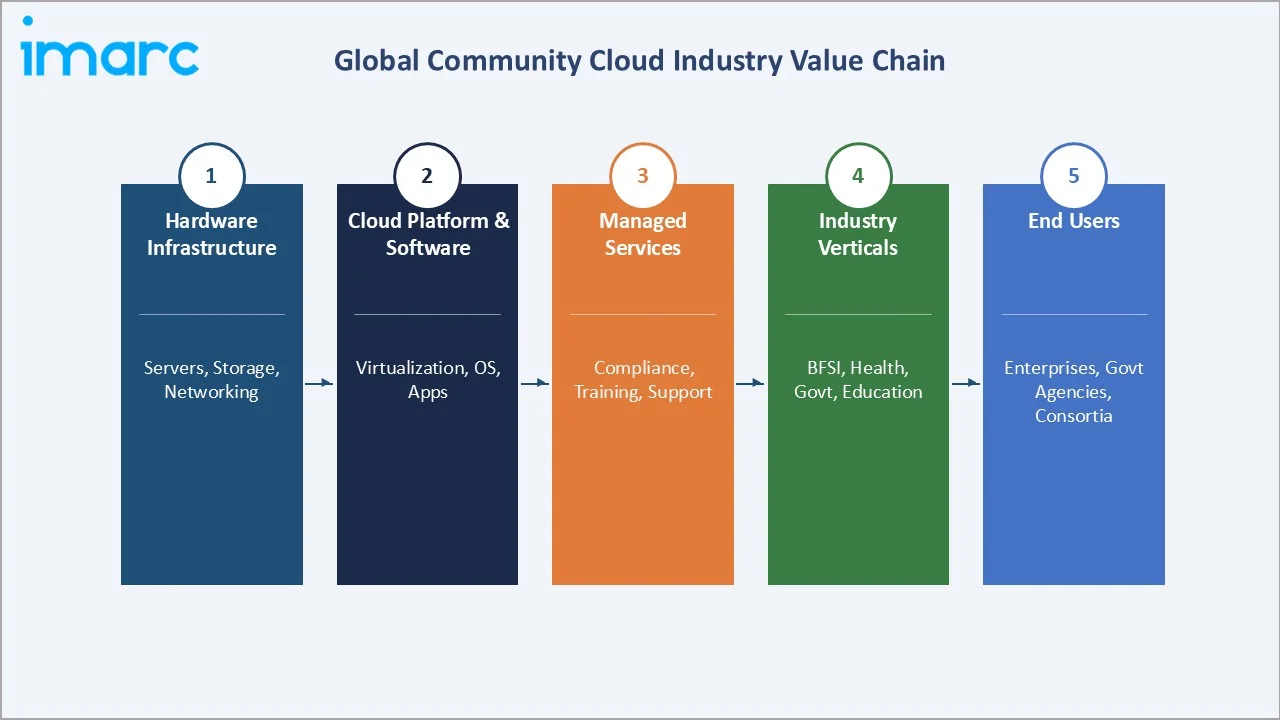

Industry Value Chain Analysis

The community cloud value chain spans five integrated stages from physical infrastructure supply through end-user service delivery. Each stage presents distinct competitive dynamics and technology investment requirements unique to the shared, sector-specific nature of community deployments.

|

Stage |

Key Players / Examples |

|

Hardware Infrastructure |

Dell Technologies, HPE, Cisco, Lenovo, NetApp – servers, networking, storage |

|

Cloud Platform & Software |

AWS, Microsoft Azure, Google Cloud, IBM Cloud – virtualization, |

|

Application & Compliance Software |

SAP, Salesforce, Oracle, ServiceNow – ERP, CRM, compliance automation |

|

Managed & Professional Services |

Accenture, Deloitte, T-Systems, Rackspace – integration, training, and regulation support |

|

End Users & Communities |

BFSI consortia, government agencies, hospital networks, university clusters, gaming platforms |

Hyperscale cloud providers occupy the highest strategic position in the community cloud value chain by integrating infrastructure, software, and compliance frameworks into configurable shared platforms. This position is increasingly challenged by sector-specific managed service providers who offer deeper regulatory specialization and regional data sovereignty guarantees that global hyperscalers cannot always provide within standard service frameworks.

Technology Landscape in the Community Cloud Industry

Virtualization and Container Orchestration

Modern community cloud platforms are built on advanced virtualization layers using hypervisors such as VMware vSphere and KVM, combined with Kubernetes-based container orchestration for workload portability and resource efficiency. Container-native architectures enable organizations within a community to deploy isolated application environments on shared hardware infrastructure, maintaining compliance boundaries while maximizing compute utilization across multi-tenant community deployments.

Zero-Trust Security and Federated Identity Management

Zero-trust architecture has become the foundational security model for community cloud deployments in regulated industries. Identity governance platforms—including Microsoft Azure Active Directory, Okta, and IBM Security Verify—enable granular, policy-enforced access control across multi-institutional community environments. Federated identity frameworks allow community members to authenticate users from their own identity providers while accessing shared resources, eliminating the need for centralized credential management that creates single points of failure.

AI and Automated Compliance Infrastructure

AI-powered compliance automation is transforming community cloud governance through Cloud Security Posture Management (CSPM) platforms that continuously monitor configurations against frameworks like HIPAA, GDPR, ISO 27001, and SOC 2. These tools enable automated remediation, reduce manual audit effort, and improve real-time compliance visibility across shared cloud environments.

Edge Computing and 5G Integration

The integration of 5G connectivity and edge computing nodes with community cloud backbones is enabling real-time data processing for latency-sensitive applications. Healthcare IoT devices, government smart city sensors, and industrial community clouds leverage edge-to-cloud architectures to process sensitive data locally before synchronizing aggregated, anonymized insights with centralized community platforms.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Hardware |

44.2% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Industry Vertical |

BFSI |

28.9% |

2025 |

|

Region |

North America |

37.5% |

2025 |

By Industry Vertical

BFSI commands the largest industry vertical share at 28.9% in 2025, reflecting the sector's critical need for secure, compliant, and highly reliable shared IT infrastructure. Financial institutions—including banks, insurance companies, and payment processors—leverage community clouds for fraud detection collaboration, anti-money laundering analytics, and regulatory reporting across multi-institutional environments.

To access detailed market analysis, Request Sample

Gaming represents the second largest vertical at 17.6% in 2025, driven by the need for high-performance, low-latency shared computing infrastructure supporting multiplayer platforms and game streaming services. Government follows at 16.8%, reflecting nationwide cloud modernization programs. Healthcare accounts for 14.5%, driven by EHR interoperability mandates and clinical research data sharing requirements. Education holds 11.2%, supported by learning management system collaboration among university consortia globally.

By Component

Hardware leads the component segment at 44.2% in 2025, forming the physical foundation of community cloud deployments, particularly in private and hybrid configurations. The hardware layer—encompassing servers, high-density storage systems, and networking equipment—supports mission-critical government, defense, and healthcare workloads requiring dedicated infrastructure for data sovereignty compliance and physical security mandates.

Software accounts for 32.6% in 2025, encompassing enterprise application software, collaboration platforms, and business intelligence tools deployed across community cloud environments. Cloud Security and Data Privacy software represents the fastest-growing software sub-segment, driven by regulatory compliance and rising cyber-risk mitigation needs across BFSI and healthcare communities. Services hold 23.2%, with compliance consulting and managed regulatory support emerging as the highest-growth service categories as community cloud complexity intensifies across multi-jurisdictional deployments.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

37.5% |

FedRAMP compliance, HIPAA healthcare clouds, BFSI digital transformation, and high IT spending |

|

Asia-Pacific |

26.4% |

China governance frameworks, India MeghRaj, Southeast Asia fintech, smart city investments |

|

Europe |

21.8% |

GDPR enforcement, GAIA-X sovereign cloud, Germany/France/UK BFSI and healthcare digitization |

|

Latin America |

7.6% |

Brazil LGPD compliance, Mexico fintech expansion, telecom-led cloud infrastructure growth |

|

Middle East and Africa |

6.7% |

Saudi Vision 2030, UAE Cloud-First Policy, NEOM smart city, GCC BFSI modernization |

North America commands a 37.5% global revenue share in 2025, the most dominant regional position in the community cloud market. The United States is the primary growth engine, with FedRAMP-compliant community cloud deployments across federal agencies and HIPAA-aligned platforms across hospital networks driving sustained investment.

Asia-Pacific holds 26.4% in 2025 and is forecast to register the highest regional CAGR of approximately 31.2% through 2034. China's domestic cloud governance, India's cloud-first policies, Japan's healthcare digitization, and South Korea's advanced technology infrastructure collectively drive the region's rapid adoption of community cloud platforms. The expansion of SMEs across Southeast Asia, embracing community cloud as a cost-efficient alternative to private infrastructure, adds further growth momentum through the forecast period.

Europe holds 21.8% in 2025, driven by GDPR compliance requirements, EU digital sovereignty mandates, and GAIA-X federated cloud infrastructure investments. Germany, France, and the United Kingdom lead within the region. Latin America (7.6%) is emerging, with Brazil's LGPD legislation and Mexico's fintech ecosystem stimulating compliant community cloud demand. The Middle East and Africa (6.7%) is accelerating rapidly, anchored by the UAE's Cloud-First Policy, Saudi Arabia's Vision 2030 digital transformation agenda, and GCC smart city investments.

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Amazon Web Services |

AWS GovCloud / Outposts |

Leader |

Hyperscale compliance, sovereign cloud zones |

|

Microsoft Corporation |

Azure Government / Sovereign |

Leader |

Hybrid cloud, Teams integration, compliance |

|

Google LLC |

Google Cloud / Assured Workloads |

Leader |

AI/ML, data analytics, regulated workloads |

|

IBM Corporation |

IBM Cloud / Red Hat |

Challenger |

Hybrid cloud, BFSI expertise, Red Hat OpenShift |

|

Oracle Corporation |

Oracle Cloud Infrastructure |

Challenger |

Database performance, ERP, govt cloud |

|

Alibaba Group Holding Limited |

Alibaba Cloud |

Leader |

Asia-Pacific dominance, AI cloud services |

|

Tencent Holdings Ltd. |

Tencent Cloud |

Challenger |

Gaming, media, Southeast Asia expansion |

|

Huawei Technologies Co., Ltd. |

Huawei Cloud / Stack |

Challenger |

Telecom integration, Asia-Pacific govt clouds |

|

SAP SE |

SAP BTP / Rise with SAP |

Emerging |

ERP cloud, BFSI compliance automation |

|

OVHcloud |

OVHcloud |

Emerging |

European sovereignty, GDPR-compliant hosting |

The global community cloud competitive landscape is characterized by hyperscale providers commanding broad infrastructure capabilities alongside specialized managed service providers focusing on regulatory depth. Market participants differentiate through compliance certifications (FedRAMP, ISO 27001, HIPAA), geographic availability of sovereign cloud zones, AI-powered compliance automation, and sector-specific platform expertise. Competition is intensifying as sovereign cloud requirements and neocloud providers challenge incumbent hyperscalers in regulated industry verticals.

Key Company Profiles

Amazon Web Services Inc.

Amazon Web Services is a cloud infrastructure services provider. AWS GovCloud and AWS Outposts provide dedicated community cloud environments for U.S. federal agencies, defense contractors, and HIPAA-regulated healthcare organizations.

- Product & Platform Portfolio: AWS GovCloud (US), AWS Outposts, Amazon HealthLake, AWS Clean Rooms, AWS Wickr.

- Recent Developments: In 2025, AWS expanded AI-driven healthcare capabilities, including privacy-preserving data collaboration and synthetic datasets, enabling secure multi-institutional analytics and improved clinical workflows across global healthcare systems.

- Strategic Focus: AWS's strategy centers on deepening sovereign cloud capabilities through GovCloud expansion, healthcare-specific compliance certifications, and AI-powered workload optimization for regulated industry community deployments globally.

Microsoft Corporation

Microsoft Azure is the cloud provider globally. Azure Government and Microsoft Cloud for Healthcare provide FedRAMP-authorized and HIPAA-compliant community cloud environments for public sector and healthcare clients.

- Product & Platform Portfolio: Azure Government, Azure Sovereign Cloud, Microsoft Cloud for Healthcare, Microsoft Cloud for Financial Services, Microsoft Sovereign Cloud.

- Recent Developments: In January 2024, Microsoft and Vodafone signed a 10-year partnership to deliver generative AI, cloud, and digital services to over 300 million consumers, businesses, and public sector organizations.

- Strategic Focus: Microsoft's community cloud strategy prioritizes sector-specific cloud platforms, Azure AI integration for compliance automation, and hybrid cloud deployment via Azure Arc—enabling organizations to manage community workloads across on-premise, multi-cloud, and edge environments.

IBM Corporation

IBM Cloud maintains a strong position in regulated industry community cloud deployments, particularly in BFSI and government sectors, supported by the Red Hat OpenShift hybrid cloud platform and extensive compliance certification portfolio across 11 global regions and 29 availability zones.

- Product & Platform Portfolio: IBM Cloud for Financial Services, IBM Cloud for Government, Red Hat OpenShift, IBM Security QRadar, IBM Blockchain Platform.

- Recent Developments: In October 2025, IBM launched Digital Asset Haven, a blockchain-enabled cloud platform enabling secure digital asset management, multi-party governance, and compliance across financial institutions, governments, and regulated enterprises.

- Strategic Focus: IBM's community cloud strategy leverages Red Hat's open-source hybrid cloud architecture to deliver regulatory-compliant, sector-specific platforms for BFSI, government, and healthcare clients while embedding AI-powered compliance intelligence across shared community cloud deployments.

Market Concentration Analysis

The global community cloud market exhibits moderate-to-high concentration among hyperscale providers and specialized managed service vendors. Amazon Web Services, Microsoft Corporation

and Google LLC collectively hold significant global market influence, with their community-grade offerings (AWS GovCloud, Azure Government, Google Assured Workloads) commanding the majority of BFSI, healthcare, and government community cloud contracts in North America and Europe.

The market is simultaneously experiencing meaningful fragmentation as sovereign cloud requirements incentivize regional providers—including OVHcloud in Europe, Alibaba in Asia-Pacific, and specialized GCC providers—to develop locally compliant community cloud platforms. This dual dynamic of hyperscaler concentration and regional fragmentation creates a bifurcated competitive landscape where global scale and regulatory specialization are coequal competitive imperatives. Consolidation through strategic partnerships between hyperscalers and local telecoms or managed service providers is the dominant entry and expansion strategy in regulated community cloud markets through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Asia-Pacific leads growth (~31% CAGR), driven by government cloud modernization. Healthcare and BFSI dominate due to compliance needs. AI-powered compliance automation delivers the highest-margin opportunities within community cloud software ecosystems.

Emerging Market Expansion

The Middle East and Africa offer underpenetrated growth. GCC cloud strategies and investments drive demand, while Sub-Saharan Africa’s mobile expansion and e-government programs support long-term adoption of cost-efficient community cloud platforms.

Venture & Private Investment Trends

Strong venture and private equity funding targets AI compliance startups, sovereign cloud infrastructure, and vertical platforms. Hyperscalers’ multi-billion-dollar investments in sovereign cloud regions intensify competition and shape long-term market dynamics.

Future Market Outlook (2026-2034)

The global community cloud market is forecast to expand from USD 9.3 Billion in 2025 to USD 76.7 Billion by 2034 at a CAGR of 25.64%—a more-than-eight-fold increase in market value underpinned by sovereign cloud mandates, AI-driven compliance automation, sector-specific platform maturity, and structural digital transformation across BFSI, healthcare, and government verticals globally.

By 2034, three major technology shifts will redefine the community cloud market. First, AI-native platforms will automate compliance, security, and workload optimization, making manual compliance management obsolete by 2028–2030. Second, sovereign cloud convergence across regions like the EU, GCC, and Asia-Pacific will drive interconnected, locally governed ecosystems, pushing hyperscalers toward regional partnerships and regulatory alignment. Third, edge-to-cloud integration—enabled by 5G, IoT, and real-time analytics—will extend community cloud beyond centralized data centers into distributed environments. Together, these shifts will transform community cloud from a compliance-focused model into a strategic AI-powered collaboration platform that supports shared innovation, regulatory coordination, and collective data intelligence across regulated industries.

Research Methodology

Primary Research

Primary research encompassed structured interviews and surveys conducted in 2024–2025 with community cloud industry stakeholders including product directors at hyperscale cloud providers, compliance and IT directors at BFSI and healthcare organizations, government digital transformation program managers, and institutional investors in regulated cloud technology. Primary insights validated market sizing, segmentation estimates, technology adoption timelines, and competitive positioning assessments across key geographies.

Secondary Research

Secondary sources include Gartner Cloud Computing forecasts, IDC cloud infrastructure spending reports, Precedence Research community cloud market analysis, European Commission GAIA-X initiative documentation, U.S. FedRAMP program data, HIPAA Journal cloud compliance reports, GSMA connected technology publications, Synergy Research Group cloud market share data, and company annual reports for AWS, Microsoft, Google, IBM, Oracle, and SAP.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, IT expenditure indices, regulatory adoption timelines, and historical community cloud market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty and varying regulatory adoption velocities across regions and industry verticals.

Community Cloud Market Report Coverage

|

Attribute |

Details |

|

Market Size (Base Year) |

USD 9.3 Billion (2025) |

|

Forecast Market Size |

USD 76.7 Billion (2034) |

|

CAGR |

25.64% (2026-2034) |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Segmentation |

By Industry Vertical (BFSI, Gaming, Government, Healthcare, Education, Others); By Component (Hardware, Software, Services); By Application (Cloud-Based Storage, Cloud Backup and Recovery, Cloud Security and Data Privacy, High Performance Computation, Analytics and Web-Based Applications) |

|

Regional Analysis |

North America, Asia-Pacific, Europe, Latin America, Middle East, and Africa |

|

Countries Covered |

United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

|

Companies Covered |

Amazon Web Services, Microsoft Corporation, Google LLC, IBM Corporation, Oracle Corporation, Alibaba Group Holding Limited, Tencent Holdings Ltd., Huawei Technologies Co. Ltd., SAP SE, OVHcloud, etc. |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10–12 Weeks |

|

Delivery Format |

PDF and Excel through Email (PPT/Word on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the community cloud market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global community cloud market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the community cloud industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Community Cloud Market Report

The global community cloud market was valued at USD 9.3 Billion in 2025, driven by regulatory compliance demands and cross-organizational data collaboration requirements.

The market is projected to reach USD 76.7 Billion by 2034, growing at a CAGR of 25.64% during 2026-2034, driven by sovereign cloud mandates, AI integration, and sector-specific platform adoption globally.

BFSI leads with a 28.9% share in 2025, driven by stringent data security requirements, shared fraud detection infrastructure, and regulatory compliance mandates across banking and financial services institutions.

Hardware leads with a 44.2% share in 2025, driven by private and hybrid community cloud deployments in regulated industries requiring dedicated physical infrastructure for data sovereignty and compliance.

North America leads with a 37.5% share in 2025, driven by FedRAMP-compliant government cloud programs, HIPAA-aligned healthcare community platforms, and high IT spending across BFSI and public sector verticals.

Key drivers include escalating regulatory compliance requirements (HIPAA, GDPR, FedRAMP), AI integration for compliance automation, rising cross-institutional data collaboration demands, and sovereign cloud mandates globally.

Asia-Pacific is forecast to register the highest CAGR of approximately 31.2% through 2034, driven by China's cloud governance frameworks, India's MeghRaj initiative, and Southeast Asia's financial sector digitalization.

Leading companies include Amazon Web Services, Microsoft Corporation, Google LLC, IBM Corporation, Oracle Corporation, Alibaba Group Holding Limited, Tencent Holdings Ltd., Huawei Technologies Co., Ltd., SAP SE, and OVHcloud.

AI enables real-time compliance monitoring, predictive audit readiness, automated regulatory reporting, and intelligent workload optimization across multi-institutional shared cloud environments, reducing compliance costs significantly.

Key applications include cloud-based storage, cloud backup and recovery, cloud security and data privacy, high-performance computation, and analytics and web-based applications across regulated industry verticals.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)