Companion Animal Health Market Size, Share, Trends and Forecast by Animal Type, Product, End User, and Region, 2026-2034

Companion Animal Health Market Size and Share:

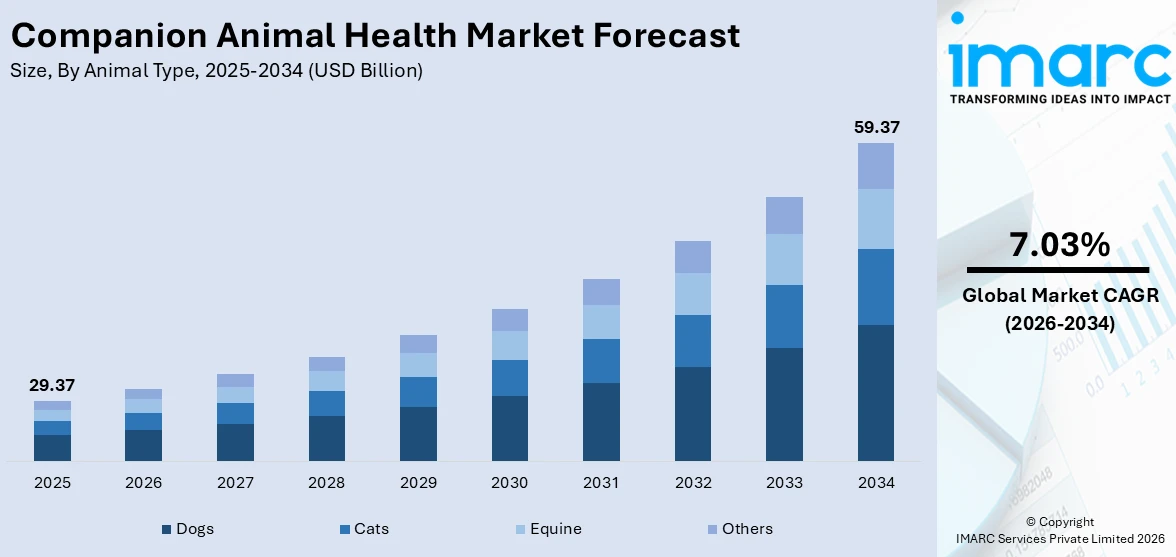

The global companion animal health market size was valued at USD 29.37 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 59.37 Billion by 2034, exhibiting a CAGR of 7.03% from 2026-2034. North America currently dominates the market, holding a market share of 40.5% in 2025. The region benefits from high pet ownership rates, advanced veterinary infrastructure, widespread pet insurance adoption, and robust government support for animal healthcare standards, which collectively sustain strong demand and underpin the companion animal health market share.

The global companion animal health market is experiencing robust growth driven by a convergence of demographic, economic, and scientific factors. The increasing trend of pet humanization has fundamentally transformed how owners approach animal healthcare, with more individuals treating companion animals as family members and seeking premium medical services. Rising disposable incomes across both developed and emerging economies have expanded the willingness to invest in preventive care, diagnostics, and specialized treatments. Growing awareness of zoonotic diseases has further reinforced the importance of regular veterinary care and vaccination programs. Technological advancements in veterinary diagnostics, including point-of-care testing devices and advanced imaging systems, are enabling earlier and more accurate disease detection. The expansion of veterinary telemedicine services has improved accessibility to healthcare advice in underserved regions. Additionally, the surge in pet adoption, particularly during and after the global pandemic period, has structurally increased the companion animal population, thereby creating a sustained and expanding base of demand for health products and services, reflecting favorable companion animal health market growth prospects globally.

The United States has emerged as a major region in the companion animal health market owing to many factors. The country hosts one of the largest companion animal populations in the world, with pets present in millions of households across urban and rural settings. An extensive network of licensed veterinary clinics, animal hospitals, and specialty care centers forms a strong foundation for service delivery. Federal oversight through agencies such as the US Department of Agriculture and the Food and Drug Administration ensures rigorous standards for pharmaceutical approvals and veterinary product safety. The widespread availability of pet insurance coverage has made advanced treatments financially accessible to a broader segment of pet owners, encouraging more frequent veterinary visits and uptake of specialized therapies. Research and development investments in novel biologics and targeted therapeutics are particularly strong within the country.

To get more information on this market Request Sample

Companion Animal Health Market Trends:

Surge in Pet Insurance Adoption

The rising uptake of pet insurance across major markets is significantly reshaping how companion animal healthcare is financed and accessed. As veterinary costs for complex procedures and chronic disease management continue to escalate, more pet owners are turning to insurance plans to manage unexpected medical expenses. This shift is encouraging higher utilization of advanced diagnostics, surgical interventions, and specialist consultations that might otherwise be foregone due to cost constraints. Insurers are increasingly tailoring products to cover a broad range of conditions, from hereditary disorders to dental care and behavioral therapy. The expansion of employer-sponsored pet insurance benefits in North America and parts of Europe has further accelerated enrollment among working-age adults. Technological platforms enabling seamless claims management and policy comparison have lowered barriers to insurance uptake.

Advancements in Veterinary Biologics

The veterinary biologics segment is undergoing a period of rapid scientific advancement, driven by increased research investment and the application of biotechnology platforms to animal health. Novel vaccine formulations leveraging messenger RNA technology are being explored for companion animals, building on methodologies validated during human healthcare applications. Monoclonal antibody therapies have entered the veterinary therapeutics space, offering targeted treatment options for conditions such as allergic dermatitis and osteoarthritis in dogs and cats. These therapies offer compelling advantages over traditional pharmaceuticals, including high specificity, favorable safety profiles, and sustained duration of action. Regulatory agencies in North America and Europe have streamlined approval pathways for priority veterinary biologics, reducing time-to-market for innovative products. Academic-industry collaborations are accelerating the translation of research into commercially viable solutions. The growing pipeline of veterinary biologics reflects broader investment confidence, with major global animal health companies allocating substantial R&D budgets to this area. This trajectory signals a meaningful evolution in treatment paradigms, reflecting positive companion animal health market outlook for the biologics subsegment in the near term.

Expanding Veterinary Telehealth Services

Veterinary telehealth has emerged as a transformative channel within companion animal healthcare, bridging geographic and economic access gaps while enhancing the efficiency of care delivery. Digital platforms connecting pet owners with licensed veterinarians via video consultation, chat, and asynchronous messaging have proliferated following the accelerated digital adoption trends observed in recent years. These services are particularly valuable for initial triage, post-operative monitoring, prescription management, and behavioral consultations, reducing the need for in-person visits for non-emergency cases. The integration of wearable health monitoring devices for pets, capable of tracking vital signs, activity levels, and sleep patterns, is enabling data-driven remote health assessments. Veterinary practices are increasingly adopting hybrid care models that combine in-clinic services with digital touchpoints to improve client engagement and treatment compliance. Regulatory frameworks governing telehealth in veterinary medicine are maturing across key markets, providing greater operational clarity for practitioners and technology providers alike. Growing investment in purpose-built veterinary telehealth infrastructure, including AI-assisted triage tools and cloud-based medical record integration, is further accelerating platform sophistication and scalability. This reflects compelling companion animal health market forecast potential for telehealth-enabled care models globally.

Companion Animal Health Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global companion animal health market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on animal type, product, and end user.

Analysis by Animal Type:

- Dogs

- Cats

- Equine

- Others

Dogs hold 45.0% of the market share. Dogs represent the largest animal type segment within the companion animal health market, reflecting their status as the most widely owned pet species globally. The deep emotional bonds formed between dogs and their owners drive significant spending on preventive care, vaccinations, diagnostics, and treatment of chronic conditions such as arthritis, dermatological disorders, and diabetes. The sheer diversity of dog breeds, each with distinct health predispositions, creates strong demand for a wide array of specialized pharmaceutical and biological products. Growing awareness of preventive wellness programs, including regular screenings and parasite control, has further elevated healthcare engagement among dog owners. The aging dog population in developed markets is contributing to rising demand for senior-specific health solutions, including joint supplements, pain management therapies, and oncology treatments. Furthermore, the premiumization trend in pet care has led owners to seek high-quality, evidence-based medical interventions for their dogs, sustaining consistent revenue growth within this segment and reinforcing its dominant position across the companion animal health industry worldwide.

Analysis by Product:

- Vaccines

- Pharmaceuticals

- Feed Additives

- Diagnostics

- Others

Pharmaceuticals lead the market with a share of 41.0%. Pharmaceuticals represent the cornerstone of companion animal health management, encompassing a broad range of prescription and over-the-counter drugs designed to prevent, treat, and manage diseases across multiple species. The category includes anti-infectives, anti-parasitics, analgesics, anti-inflammatory agents, dermatological preparations, and endocrine therapies, among others. The growing incidence of lifestyle-related conditions in companion animals, including obesity, diabetes, and cardiovascular disorders linked to sedentary environments and processed diets, has amplified pharmaceutical demand. Enhanced regulatory clarity around veterinary drug approvals has facilitated the entry of new formulations with improved efficacy and safety profiles. The development of species-specific dosage forms and palatability-optimized delivery systems has improved owner compliance and treatment adherence. Expansion into novel therapeutic areas, including oncology, neurology, and immunology, reflects the broadening scope of veterinary pharmaceuticals. Continued investment in generic drug development is also improving affordability and access across diverse economic settings, further solidifying pharmaceuticals as the leading product category in the market.

Analysis by End User:

Access the comprehensive market breakdown Request Sample

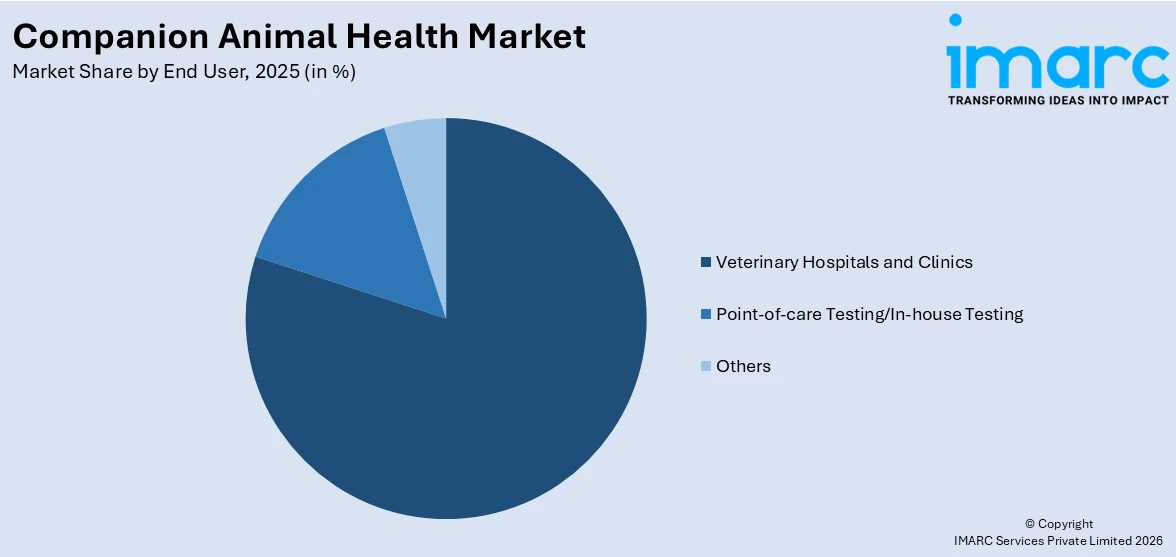

- Point-of-care Testing/In-house Testing

- Veterinary Hospitals and Clinics

- Others

Veterinary hospitals and clinics dominate the market, with a share of 79.8%. These establishments serve as the primary point of contact between companion animals and professional healthcare services, offering comprehensive diagnostic, therapeutic, and surgical capabilities under one roof. The concentration of advanced medical equipment, specialized staff, and established regulatory compliance standards within these settings makes them the preferred channel for complex health interventions, emergency care, and specialist referrals. Rising pet ownership and the growing willingness of owners to invest in preventive wellness programs have translated into higher foot traffic at veterinary facilities worldwide. The ongoing expansion of corporate veterinary chains and multi-specialty animal hospitals across North America, Europe, and Asia-Pacific has enhanced service capacity and standardization. Veterinary hospitals also serve as key distribution points for prescription pharmaceuticals, vaccines, and therapeutic diets, reinforcing their centrality in the health product supply chain. The growing integration of digital tools for appointment scheduling, electronic medical records, and remote monitoring within clinical settings is further strengthening their operational efficiency and competitive position.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America, accounting for 40.5% of the share, holds the leading position in the market. The dominance is further fueled by the exceptionally high pet ownership rate in the region, with a considerable number of households in the United States and Canadian territories boasting the presence of companion animals. The presence of thousands of licensed veterinary clinics, specialty hospitals, and emergency care facilities ensures the provision of top-notch health management services to companion animals in the region. The robust institutional frameworks in place to guide the approval of veterinary products and the management of animal welfare add to the dominance of North America in the companion animal health management industry. The pet insurance culture has increased the affordability of top-notch medical services to pets, allowing for the increased use of diagnostics, specialty treatments, and high-end pharmaceutical products. The high level of consumer expenditure in the companion animal health and wellness industry is a reflection of the culture in the region.

Key Regional Takeaways:

United States Companion Animal Health Market Analysis

The United States holds 95.20% of companion animal health in North America. The United States represents the single largest country-level market within the global companion animal health landscape, driven by a combination of structural, cultural, and regulatory factors that consistently support elevated healthcare spending for pets. The country benefits from one of the most extensive veterinary care networks in the world, encompassing general practice clinics, specialty and emergency hospitals, and academic veterinary medical centers engaged in cutting-edge research. Government agencies including the U.S. Department of Agriculture's Center for Veterinary Biologics and the FDA's Center for Veterinary Medicine maintain rigorous oversight frameworks that foster consumer confidence in approved health products. The rapid growth of the pet insurance sector has meaningfully expanded access to costly procedures, including orthopedic surgeries, oncology treatments, and advanced diagnostics. Consumer spending on companion animal health in the United States continues to grow year-on-year, fueled by humanization trends and a shift toward preventive care philosophies. Strong e-commerce channels for pet health products, alongside growing adoption of digital veterinary health platforms, further companion animal health market trends across the United States.

Europe Companion Animal Health Market Analysis

Europe constitutes a significant and steadily expanding contributor to the global companion animal health market, supported by high pet ownership rates, progressive animal welfare legislation, and a well-established veterinary services sector. The United Kingdom, Germany, France, Italy, and Spain represent the largest national markets within the region, each characterized by dense veterinary clinic networks and sophisticated distribution systems for animal health products. European regulatory bodies, including the European Medicines Agency, apply stringent standards to veterinary pharmaceutical approvals, ensuring product quality and efficacy across member states. The growing adoption of preventive healthcare practices, including routine vaccination, parasite control, and dental care programs, reflects a cultural shift toward proactive animal health management. Rising elderly pet populations in several Western European countries are creating demand for geriatric care solutions, including mobility aids, pain management therapies, and specialized nutritional products.

Asia-Pacific Companion Animal Health Market Analysis

Asia-Pacific represents the fastest-growing regional market for companion animal health, driven by rapidly rising pet ownership in urbanizing economies including China, Japan, South Korea, India, and Australia. Expanding middle-class populations with increasing disposable incomes are embracing companion animals as lifestyle additions, fueling demand for veterinary services and health products. Urbanization and changing family structures, particularly the growing prevalence of single-person and childless households, have reinforced the emotional significance attached to pets across the region. Veterinary infrastructure is expanding rapidly, with significant investments in clinic networks, pharmaceutical distribution, and diagnostic laboratories in key markets. Government initiatives promoting animal disease surveillance and vaccination campaigns are improving formal healthcare penetration for companion animals.

Latin America Companion Animal Health Market Analysis

Latin America represents an emerging growth opportunity within the global companion animal health market, with Brazil and Mexico serving as the primary drivers of regional demand. Rising pet ownership rates, particularly in urban centers, and growing awareness of animal welfare standards are elevating healthcare spending for companion animals across the region. Expanding middle-class segments are increasingly adopting preventive veterinary care practices, including routine vaccinations and parasite management. The rollout of regional veterinary hospital chains and improved pharmaceutical distribution networks is broadening access to quality health products.

Middle East and Africa Companion Animal Health Market Analysis

The Middle East and Africa region represents an emerging and gradually evolving segment within the companion animal health market, driven by rising urbanization, increasing pet adoption in metropolitan areas, and growing awareness of formal veterinary care. The Gulf Cooperation Council countries, particularly the United Arab Emirates and Saudi Arabia, are demonstrating the strongest demand growth, supported by affluent urban populations and a cultural shift toward pet ownership. Government initiatives across several African nations to control zoonotic diseases are indirectly stimulating investment in companion animal health infrastructure.

Competitive Landscape:

The global companion animal health market is characterized by a moderately consolidated competitive profile, with various multinational corporations dominating the market along with a significant number of mid-size companies that specialize in the field of animal health. The major companies in the field continue to invest heavily in research and development activities to enhance their product offerings in the fields of pharmaceuticals, vaccines, and diagnostics, among others. Mergers and acquisitions, partnerships, and collaborations have been significant mechanisms adopted by companies to compete with their peers in the field of animal health products. The various challenges faced by the companies, including the high cost of clinical trials for the development of novel biological products, the high cost of generic products, and the high cost of complying with various regulations in various markets, have been influencing the overall competitive dynamics of the market. The companies are also focusing on the development of precision medicine platforms, data-based disease management platforms, and direct-to-consumer digital initiatives to compete with their peers in the field of animal health products. Partnerships between research institutions and contract development organizations have been driving the overall innovation-based competition in the field of animal health products.

The report provides a comprehensive analysis of the competitive landscape in the companion animal health market with detailed profiles of all major companies, including:

- Agrolabo S.p.A.

- Boehringer Ingelheim International GmbH

- Ceva Sante Animale

- Dechra

- Elanco

- Greencross Vets

- IDEXX Laboratories Inc.

- Indian Immunologicals Ltd.

- Norbrook

- Vetoquinol

- Virbac

- Zoetis Services LLC

Latest News and Developments:

- In February 2026, Zoetis Inc. announced the U.S. commercial launch of its next-generation monoclonal antibody therapy for canine osteoarthritis pain management, expanding the company's pain relief portfolio for companion animals. The product, which targets a specific pain pathway with high selectivity, received expedited review from the U.S. FDA Center for Veterinary Medicine. The launch represents a significant milestone in advancing targeted biologic therapies for chronic pain conditions in dogs.

- In January 2026, For the distribution and marketing of its line of companion animal products in India, Boehringer Ingelheim India Private Limited has reached a deal with Alivira Animal Health Limited, a wholly owned subsidiary of Viyash Scientific Limited. This collaboration will take advantage of the expansion prospects in the Indian pet healthcare industry, which are fueled by rising pet ownership, preventative care awareness, and an increasing focus on animal welfare in India.

Companion Animal Health Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Animal Types Covered | Dogs, Cats, Equine, Others |

| Products Covered | Vaccines, Pharmaceuticals, Feed Additives, Diagnostics, Others |

| End Users Covered | Point-of-care Testing/In-house Testing, Veterinary Hospitals and Clinics, Others |

| Regions Covered | Asia-Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Agrolabo S.p.A., Boehringer Ingelheim International GmbH, Ceva Sante Animale, Dechra, Elanco, Greencross Vets, IDEXX Laboratories Inc., Indian Immunologicals Ltd, Norbrook, Vetoquinol, Virbac, Zoetis Services LLC, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the companion animal health market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global companion animal health market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter’s Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the companion animal health industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Companion Animal Health Market Report

The companion animal health market was valued at USD 29.37 Billion in 2025.

The companion animal health market is projected to exhibit a CAGR of 7.03% during 2026-2034, reaching a value of USD 59.37 Billion by 2034.

Key drivers of the companion animal health market include rising pet humanization trends, growing pet ownership rates globally, increased spending on preventive veterinary care, advancements in veterinary pharmaceuticals and biologics, expanding pet insurance coverage, and the proliferation of digital veterinary health platforms facilitating greater access to professional care services.

North America currently dominates the companion animal health market, accounting for a share of 40.5%. The region benefits from high pet ownership rates, a comprehensive veterinary services network, widespread pet insurance adoption, strong regulatory oversight, and significant investment in animal health research and development.

Some of the major players in the companion animal health market include Agrolabo S.p.A., Boehringer Ingelheim International GmbH, Ceva Sante Animale, Dechra, Elanco, Greencross Vets, IDEXX Laboratories Inc., Indian Immunologicals Ltd, Norbrook, Vetoquinol, Virbac, Zoetis Services LLC, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade