Computed Tomography Market Size, Share, Trends and Forecast by Type, Application, End User and Region, 2026-2034

Computed Tomography Market Size and Share:

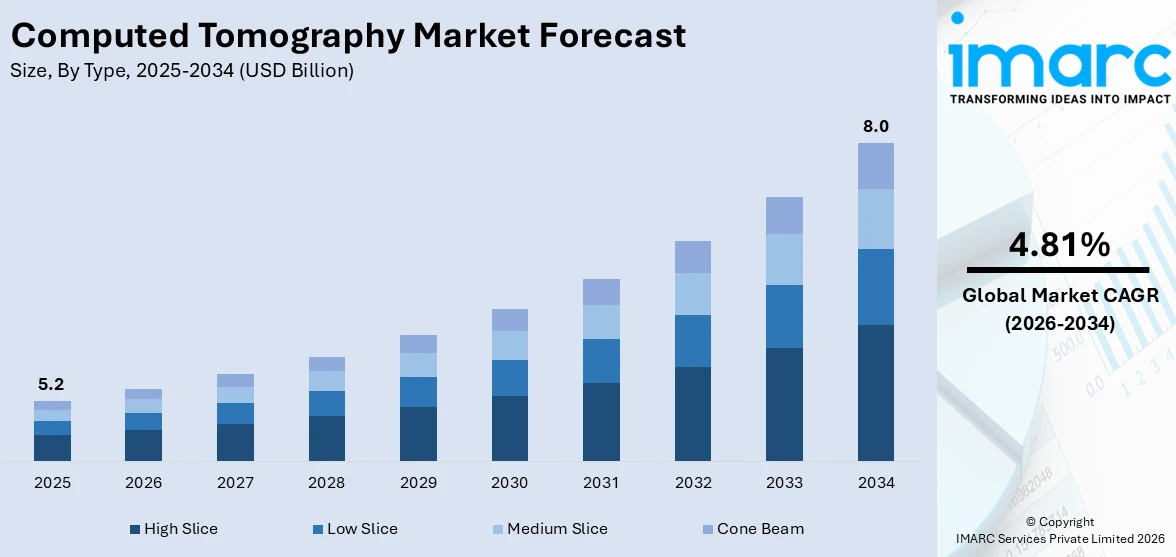

The global computed tomography market size was valued at USD 5.2 Billion in 2025. The market is projected to reach USD 8.0 Billion by 2034, exhibiting a CAGR of 4.81% from 2026-2034. North America currently dominates the market, holding a market share of 38% in 2025. Increasing adoption of artificial intelligence (AI) in healthcare is enhancing diagnostic efficiency. Rising incidence of chronic conditions and heightened awareness among the masses about timely detection and treatment are propelling the computed tomography market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 5.2 Billion |

|

Market Forecast in 2034

|

USD 8.0 Billion |

| Market Growth Rate 2026-2034 | 4.81% |

At present, the market is expanding gradually due to the increased need for sophisticated diagnostic imaging in a variety of medical specialties. Accurate and early diagnosis is becoming increasingly important because of the rising incidence of chronic illnesses, including heart diseases and neurological disorders. The growing geriatric population is further contributing to higher scan volumes. Advancements in technology, such as AI-based image analysis, low-dose radiation systems, and quicker scan periods, are increasing acceptance by improving efficiency and patient safety. The growing cases of trauma and road accidents are also promoting the use of CT scans for quick internal assessments. In addition, the broadening of healthcare infrastructure, greater applications of computed tomography (CT) in oncology and interventional procedures, and rising emphasis on preventive care are bolstering the market growth.

To get more information on this market Request Sample

The United States has emerged as a major region in the computed tomography market owing to many factors. The growing burden of chronic diseases like cancer that require advanced imaging for early and precise diagnosis is offering a favorable computed tomography market outlook. As per the American Cancer Society, in 2024, it was projected that 2,001,140 new cancer cases and 611,720 cancer-related deaths would take place in the United States. The country’s aging population is further catalyzing the demand, as older individuals are more likely to undergo CT scans for multiple health conditions. Strong healthcare infrastructure, coupled with high healthcare spending, is supporting widespread availability and adoption of advanced imaging systems. Technological innovations, including low-dose CT, high-resolution imaging, and AI integration, are enhancing diagnostic accuracy and patient safety, encouraging hospitals and diagnostic centers to upgrade equipment.

Computed Tomography Market Trends:

Growing incidence of chronic ailments

Rising prevalence of chronic conditions, such as cancer, cardiovascular disorders, and neurological conditions, is bolstering the computed tomography market growth, as these illnesses demand precise and timely diagnosis. The National Institutes of Health (NIH) estimates that the burden of chronic disease is set to be about USD 47 Trillion by 2030. CT scans play a critical role in detecting tumors, evaluating heart function, identifying vascular blockages, and assessing brain abnormalities with high accuracy. With lifestyle-related disorders and an aging population contributing to the growing incidence of chronic conditions, healthcare providers increasingly rely on CT imaging for both initial diagnosis and ongoing monitoring of disease progression or treatment response. The non-invasive, rapid, and detailed visualization capabilities of CT make it an indispensable diagnostic tool, leading to greater demand across hospitals and diagnostic centers.

Rising number of trauma and accident cases

Increasing number of trauma and accident cases is driving the market expansion, as these situations require fast and accurate imaging for immediate medical decisions. As per the Istat, in 2024, Italy noted 173,364 traffic incidents with injuries. These events led to 3,030 deaths and 233,853 wounded individuals. CT scans are highly effective in detecting internal bleeding, fractures, head injuries, and organ damage, making them critical in emergency and trauma care. Road accidents, workplace injuries, and natural disasters contribute to rising trauma cases globally, creating consistent demand for CT imaging in emergency departments. High-slice and advanced CT scanners enable rapid whole-body scans with minimal motion artifacts, ensuring quick diagnosis when every second counts. Their ability to provide detailed cross-sectional images supports physicians in prioritizing surgical interventions and improving survival outcomes.

Increasing AI adoption

Rising adoption of AI in healthcare is among the major computed tomography market trends. As per the IMARC Group, the global AI in healthcare market size reached USD 7.8 Billion in 2024. AI-based algorithms enable faster image reconstruction, automated detection of abnormalities, and advanced image interpretation, reducing the burden on radiologists while improving precision. These technologies also assist in minimizing errors, standardizing reporting, and providing decision-support tools for complex cases, such as oncology and cardiology. Furthermore, AI integration allows dose optimization, lowering patient exposure to radiation without compromising image quality. In busy hospital environments, AI helps streamline workflow by prioritizing urgent cases and speeding up reporting, leading to better patient outcomes. As healthcare providers are adopting digital transformation, the synergy of CT systems with AI ensures higher productivity, early disease detection, and cost-effectiveness.

Computed Tomography Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global computed tomography market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on type, application, and end user.

Analysis by Type:

- Low Slice

- Medium Slice

- High Slice

- Cone Beam

High slice held 36% of the market share in 2025. High-slice CT scanners provide superior image quality, faster scan times, and greater diagnostic accuracy compared to lower-slice systems. These scanners can capture detailed images of complex anatomical structures in a single rotation, making them highly effective for advanced applications in cardiology, oncology, and neurology. Their ability to perform whole-body scans quickly with reduced motion artifacts is particularly valuable in trauma and emergency settings, where time is critical. Additionally, high-slice systems support advanced techniques like dual-energy imaging and perfusion studies, expanding their use in precision diagnostics and treatment planning. While the initial investment is higher, the benefits of improved workflow efficiency, patient comfort, and reduced radiation exposure make them highly attractive to large hospitals and advanced diagnostic centers. As per the computed tomography market forecast, with the growing demand for early disease detection, complex case management, and improved patient outcomes, high-slice CT scanners will continue to dominate the industry based on type.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Oncology

- Neurology

- Cardiovascular

- Musculoskeletal

- Others

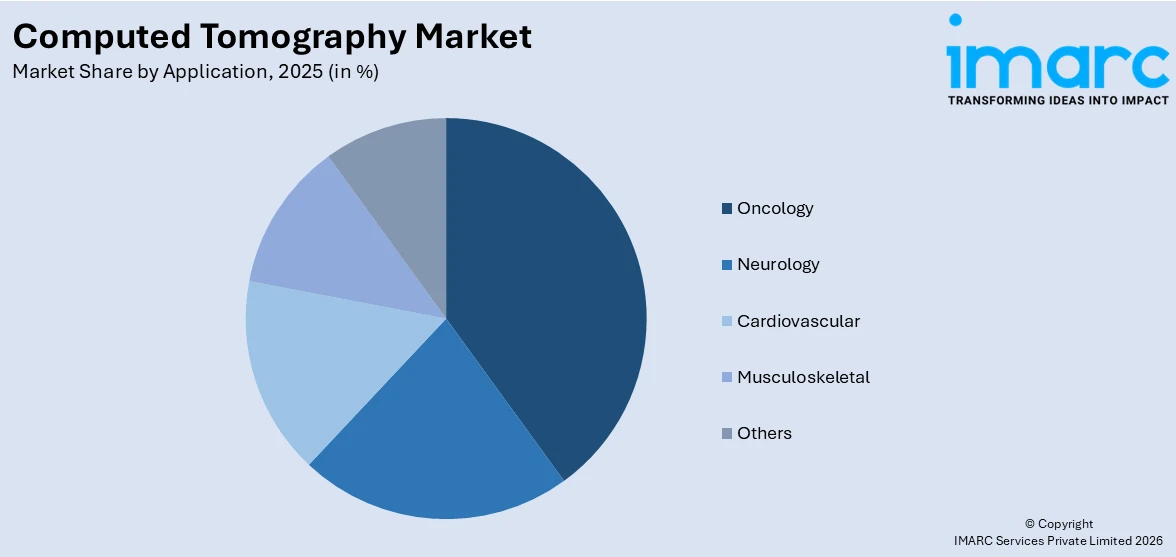

Oncology accounts for 32% of the market share. It relies heavily on precise imaging for diagnosis, staging, and treatment monitoring. CT scans are integral for detecting tumors at early stages, guiding biopsies, and evaluating tumor progression or response to therapy. The increasing global prevalence of cancer has made CT an indispensable tool in oncology, as it provides rapid, detailed, and non-invasive visualization of internal organs and tissues. High-slice and advanced CT systems enable physicians to differentiate between malignant and benign growths with high precision, supporting accurate treatment planning. Furthermore, CT imaging plays a critical role in radiation therapy planning, surgical interventions, and follow-up assessments, ensuring comprehensive care for cancer patients. The encouragement for early detection programs, coupled with rising demand for advanced oncology care and clinical research, is strengthening the dominance of oncology applications in the CT market.

Analysis by End User:

- Hospitals

- Diagnostic Centers

- Others

Hospitals hold 68% of the market share. Hospitals serve as the primary centers for diagnosis, treatment, and emergency care. Hospitals manage large patient volumes daily, encompassing a wide assortment of clinical cases, from trauma and emergency conditions to chronic disease management, where CT imaging is essential. Their ability to invest in high-slice and technologically advanced CT systems allows hospitals to deliver faster, more accurate, and comprehensive imaging services. Additionally, hospitals often integrate CT scanners with other diagnostic and treatment facilities, making them a one-stop solution for patient care. In oncology, cardiology, neurology, and orthopedics, hospitals rely on CT for both routine diagnostics and complex surgical planning. Favorable reimbursement policies, government support, and expanding healthcare infrastructure are further strengthening the adoption of CT in hospitals. With their extensive resources, trained staff, and ability to handle critical cases, hospitals remain the largest end users of CT technology, ensuring accessibility and driving market leadership in this segment.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America, accounting for a share of 38%, enjoys the leading position in the market. The region is noted for its advanced healthcare infrastructure, strong focus on innovations, and widespread adoption of cutting-edge diagnostic technologies. The region has a high incidence of chronic ailments like cardiovascular conditions and neurological disorders, driving continuous demand for precise imaging solutions. The elderly population is further creating the requirement for CT scans, as older individuals are more prone to multiple health complications requiring frequent diagnostic evaluations. As per the Statistics Canada, as of July 2024, the total number of individuals aged 65 and above in Canada was 7,820,121. Additionally, high healthcare spending and favorable reimbursement policies are making advanced imaging more accessible, encouraging hospitals and diagnostic centers to invest in state-of-the-art CT systems. The strong presence of leading manufacturers in the United States and Canada ensures consistent technological advancements, including low-dose imaging, high-speed scanning, and AI integration.

Key Regional Takeaways:

United States Computed Tomography Market Analysis

The United States holds 85% of the market share in North America. The United States computed tomography market is primarily driven by technological advancements, rising healthcare needs, and the growing emphasis on early disease detection. Increasing incidence of chronic conditions, such as cancer, cardiovascular diseases, and respiratory disorders, has heightened the demand for accurate and timely diagnostic tools, with CT scans playing a critical role in clinical decision-making. According to industry reports, in 2024, about 48.6% of people in the United States experienced some form of heart disease. Technological innovations, such as low-dose radiation systems, faster scanning times, and improved image resolution, are enhancing diagnostic capabilities and patient safety, making CT imaging more attractive to healthcare providers. The expanding use of CT in emergency departments for trauma, stroke, and acute pain diagnostics is further boosting utilization. Additionally, the integration of AI in image processing is streamlining workflow efficiency and supporting more precise diagnoses. Government and private sector investments in healthcare infrastructure and imaging facilities are also increasing access to CT services across both urban and rural areas. Other than this, rising awareness among patients and physicians about the benefits of early detection and non-invasive imaging continues to support the widespread adoption of CT technology throughout the United States.

Europe Computed Tomography Market Analysis

The growth of the Europe computed tomography market is largely fueled by an increasing geriatric population and the growing incidence of chronic diseases like cardiovascular conditions and neurological disorders that require advanced diagnostic imaging. According to a 2024 report by the World Heart Federation, more than 60 Million people in Europe were affected by cardiovascular diseases, leading to over 1.7 Million fatalities in the region annually and costing the European economy around €282 Billion. As a result, European countries are investing in modernizing their healthcare systems, which includes upgrading diagnostic infrastructure and adopting high-efficiency CT systems. The demand for less invasive diagnostic methods is also rising, and CT scans offer a non-invasive, fast, and accurate imaging solution. Moreover, advancements in CT technology, such as dual-source, spectral imaging, and low-dose radiation systems, are enhancing diagnostic accuracy while addressing safety concerns. Other than this, academic research initiatives and strong collaborations between healthcare institutions and imaging technology providers are accelerating the adoption of cutting-edge CT systems.

Asia-Pacific Computed Tomography Market Analysis

The Asia-Pacific computed tomography market is expanding due to rapid urbanization, expanding healthcare infrastructure, and high healthcare investments across developing regions. The increasing geriatric population in the region is also contributing substantially to the heightened demand for non-invasive, high-precision diagnostic solutions. Moreover, expanding medical tourism, particularly in countries, such as India, Thailand, and Singapore, is significantly catalyzing the demand for state-of-the-art imaging technologies, solidifying the CT market’s expansion in the Asia Pacific region. For instance, the number of Foreign Tourist Arrivals (FTAs) for medical reasons in India hit 186,644 in 2020, equating to 7% of total FTAs in the country, as per the India Brand Equity Foundation (IBEF). Besides this, government initiatives aimed at improving access to healthcare services, along with the development of new hospitals and diagnostic centers, are also contributing substantially to the market growth. Innovations in technology, such as portable CT scanners and low-dose imaging systems, are enhancing the appeal of CT across both urban and rural settings.

Latin America Computed Tomography Market Analysis

The Latin America computed tomography market is experiencing robust growth due to rising healthcare awareness, increasing prevalence of chronic ailments, and the growing demand for timely and precise diagnosis. As public and private healthcare sectors are expanding, there is greater investment in advanced imaging technologies, including CT systems. The increasing adoption of digital health technologies and the integration of AI in imaging diagnostics are also supporting market growth. Besides this, urbanization and a rising middle-class population are also leading to heightened healthcare expenditures. By 2050, nearly every Latin American nation is anticipated to increase its per capita current health expenditures (CHE) twofold, while certain Caribbean nations will see growth exceeding double.

Middle East and Africa Computed Tomography Market Analysis

The Middle East and Africa computed tomography market is significantly influenced by increasing investments in healthcare infrastructure and a rising focus on modernizing diagnostic capabilities. Governments and private sectors are actively expanding hospitals and diagnostic centers, particularly in urban areas, to meet the growing demand for advanced medical imaging. The rising prevalence of non-communicable diseases, such as cancer and cardiovascular conditions, is also creating the need for early and accurate diagnostics using CT technology. For instance, in Saudi Arabia, the total of new cancer diagnoses hit 28,113 in 2022, resulting in around 13,399 fatalities, according to the International Agency for Research on Cancer (IARC). Other than this, increasing awareness about early disease detection is further supporting the market growth across the area.

Competitive Landscape:

Key players are continuously advancing technology, expanding product portfolios, and meeting evolving clinical needs. Leading manufacturers are focusing on innovations, such as low-dose radiation systems, high-speed scanning, dual-energy CT, and AI-assisted imaging, to enhance diagnostic accuracy and patient safety. Their strong investments in research and development (R&D) activities ensure the launch of next-generation devices that support a wider range of clinical applications, including oncology, cardiology, and neurology. These companies are also broadening their market reach through strategic partnerships, mergers, and acquisitions, improving accessibility in both developed and emerging markets. Furthermore, they provide training, service support, and financing options to hospitals and diagnostic centers, which accelerate adoption. Overall, key players are significantly shaping the market growth through technological leadership and global presence. For instance, in December 2024, Siemens Healthineers revealed the introduction of the Naeotom Alpha series, featuring the dual-source scanner Naeotom Alpha.Pro and the photon-counting CT scanner system Naeotom Alpha.Prime. Through this launch, Siemens Healthineers intended to enhance the availability of photon-counting technologies for healthcare providers and patients.

The report provides a comprehensive analysis of the competitive landscape in the computed tomography market with detailed profiles of all major companies, including:

- Canon Medical Systems Corporation (Canon Inc.)

- FUJIFILM Holdings Corporation

- GE HealthCare (General Electric Company)

- Koning Corporation

- Koninklijke Philips N.V.

- NeuroLogica Corp. (Samsung Electronics Co. Ltd.)

- Neusoft Medical Systems Co. Ltd. (Neusoft Corporation)

- Planmeca Oy

- Siemens Healthineers AG (Siemens AG)

- Stryker Corporation

Latest News and Developments:

- June 2025: PT Kalbe Farma Tbk established Indonesia's inaugural manufacturing facility for advanced CT scanners in collaboration with GE HealthCare. The creation of this facility represented an important advancement in enhancing diagnostic abilities throughout Indonesia and localizing the production of state-of-the-art medical equipment.

- May 2025: Mahajan Imaging & Labs launched the Omni Legend, a 128-Slice Digital PET-CT scanner by GE HealthCare, in North India for precision oncology use. This new facility in Gurugram signified a major progress in holistic cancer treatment and enhanced diagnostics across the Delhi NCR area.

- March 2025: GE HealthCare revealed intentions to introduce its innovative CT system, the Revolution™ Vibe, during the American College of Cardiology 2025 conference. Using Unlimited One-Beat Cardiac Imaging, the innovative device delivered patients dependable, high-quality images, even in challenging circumstances like heavily calcified coronaries and atrial fibrillation.

- January 2025: Royal Philips launched its AI-based CT 5300 CT system at the 23rd Asian Oceanian Congress of Radiology (AOCR) 2025. The CT 5300 incorporated advanced AI features and was designed for screening, intervention, and diagnostic tasks.

Computed Tomography Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Low Slice, Medium Slice, High Slice, Cone Beam |

| Applications Covered | Oncology, Neurology, Cardiovascular, Musculoskeletal, Others |

| End Users Covered | Hospitals, Diagnostic Centers, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Canon Medical Systems Corporation (Canon Inc.), FUJIFILM Holdings Corporation, GE HealthCare (General Electric Company), Koning Corporation, Koninklijke Philips N.V., NeuroLogica Corp. (Samsung Electronics Co. Ltd.), Neusoft Medical Systems Co. Ltd. (Neusoft Corporation), Planmeca Oy, Siemens Healthineers AG (Siemens AG), Stryker Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the computed tomography market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global computed tomography market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the computed tomography industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Computed Tomography Market Report

The computed tomography market was valued at USD 5.2 Billion in 2025.

The computed tomography market is projected to exhibit a CAGR of 4.81% during 2026-2034, reaching a value of USD 8.0 Billion by 2034.

Rising elderly population, which is more prone to multiple health complications, is driving the demand for CT scans. Technological advancements, including low-dose radiation, faster scanning, and AI-enabled image analysis, are improving diagnostic accuracy, patient safety, and workflow efficiency, leading to higher adoption across hospitals and diagnostic centers. Additionally, the surge in trauma cases, road accidents, and emergency care needs is fueling the use of CT for rapid internal assessment.

North America currently dominates the computed tomography market, accounting for a share of 38% in 2025, due to its sophisticated healthcare system, substantial healthcare investments, quick integration of cutting-edge imaging technologies, and significant presence of major companies. Supportive reimbursement policies and a high prevalence of chronic illnesses are driving the market expansion.

Some of the major players in the computed tomography market include Canon Medical Systems Corporation (Canon Inc.), FUJIFILM Holdings Corporation, GE HealthCare (General Electric Company), Koning Corporation, Koninklijke Philips N.V., NeuroLogica Corp. (Samsung Electronics Co. Ltd.), Neusoft Medical Systems Co. Ltd. (Neusoft Corporation), Planmeca Oy, Siemens Healthineers AG (Siemens AG), Stryker Corporation, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)