Consumer Credit Market Size, Share, Trends and Forecast by Credit Type, Service Type, Issuer, Payment Method, and Region, 2026-2034

Global Consumer Credit Market Size, Share, Trends & Forecast (2026-2034)

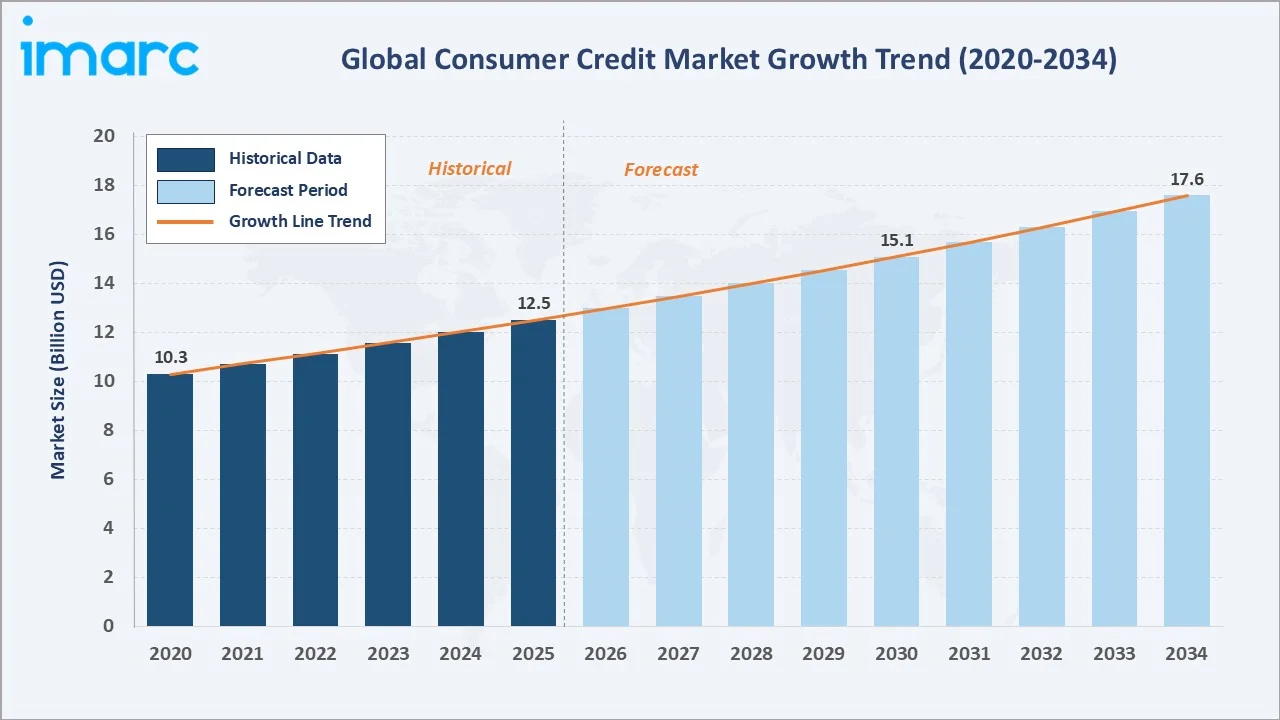

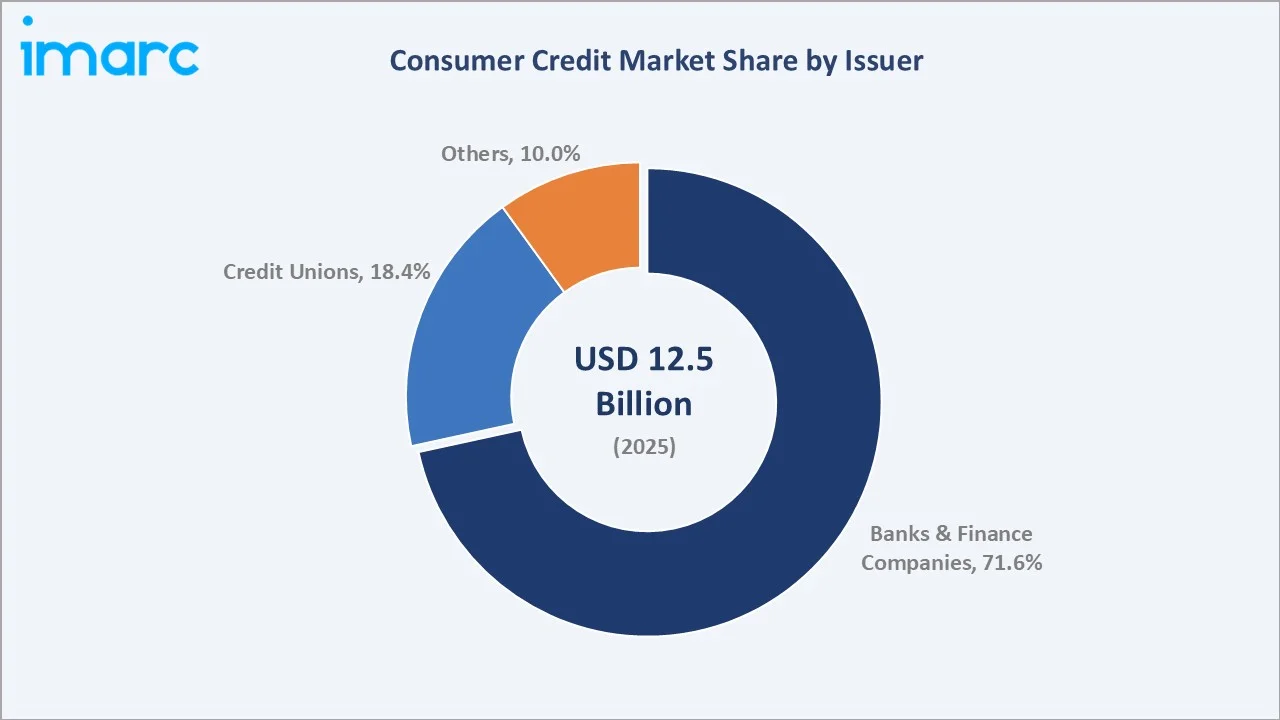

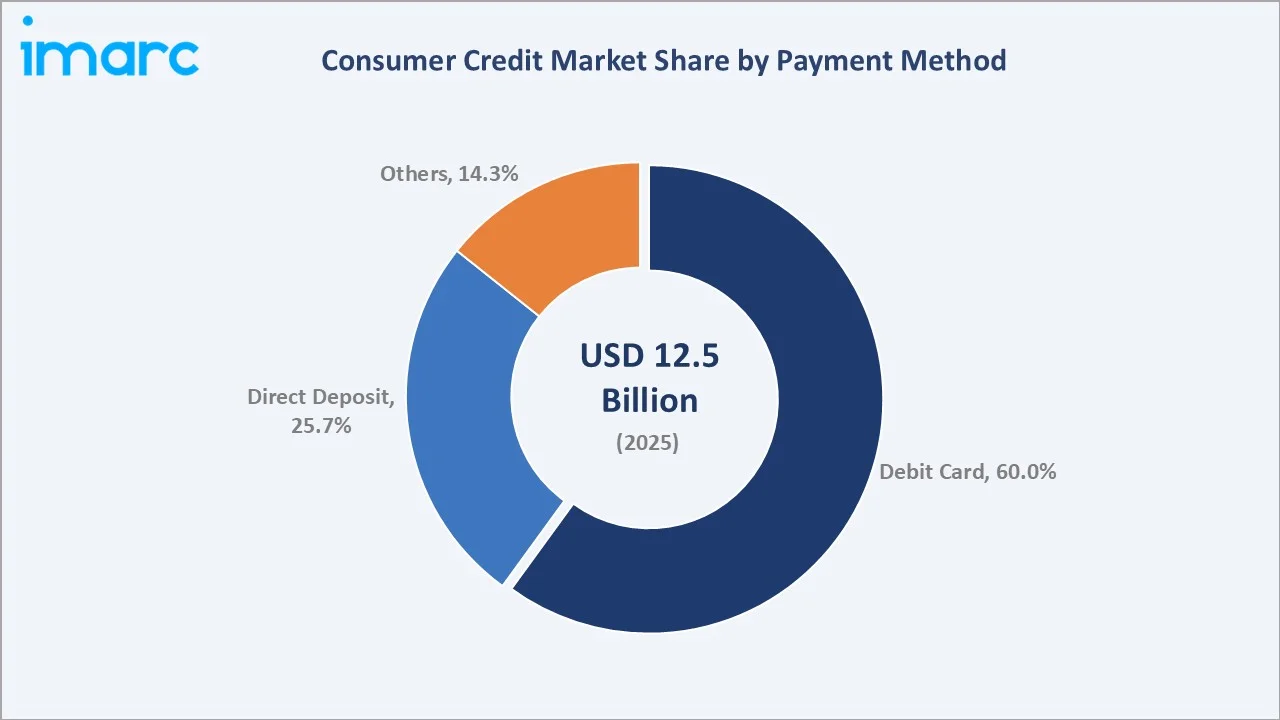

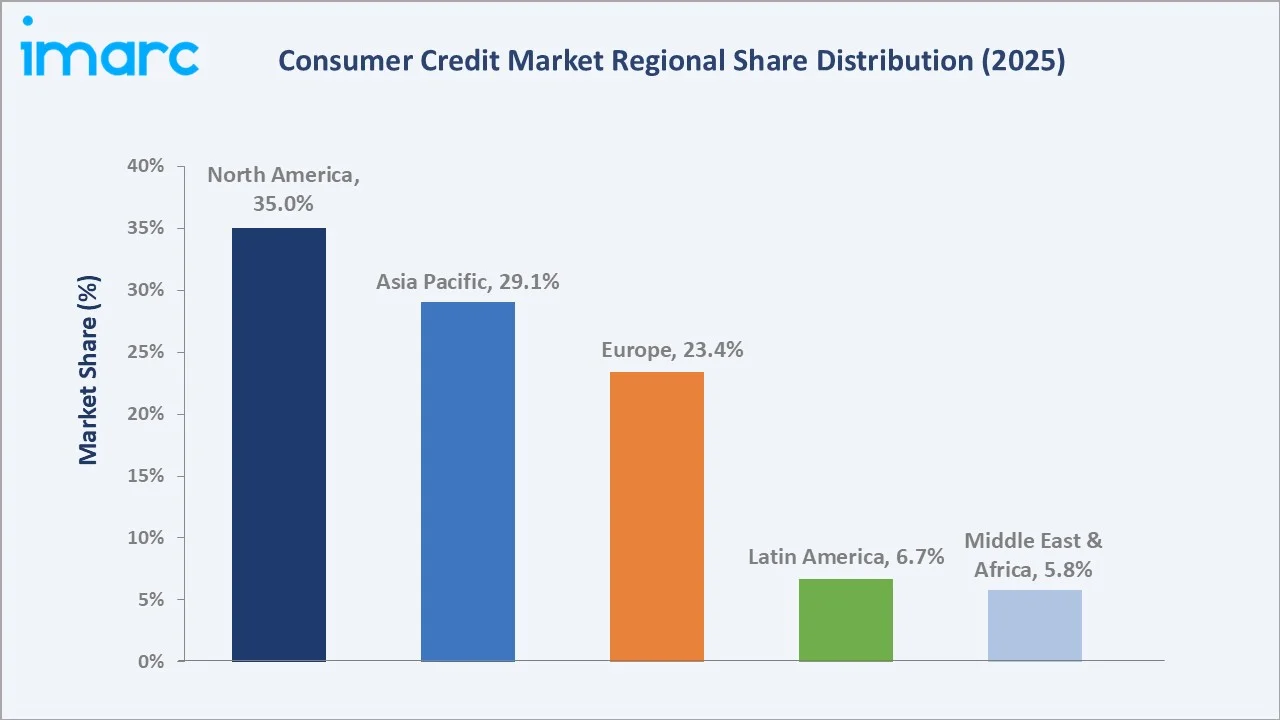

The global consumer credit market size was valued at USD 12.5 Billion in 2025 and is projected to reach USD 17.6 Billion by 2034, at a CAGR of 3.9% during 2026-2034. Rising digitalisation of banking, growing Buy Now Pay Later (BNPL) adoption, expanding MSME credit access, and rising disposable incomes in emerging economies are driving consumer credit market growth. Banks and Finance Companies dominate with a 71.6% share in 2025, while Debit Cards account for 60.0% of payment methods. North America leads with a 35.0% regional share, while Asia Pacific is the fastest-growing region.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 12.5 Billion |

|

Forecast Market Size (2034) |

USD 17.6 Billion |

|

CAGR (2026-2034) |

3.9% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (35.0% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

|

Leading Issuer |

Banks and Finance Companies (71.6%, 2025) |

|

Leading Payment Method |

Debit Card (60.0%, 2025) |

The chart below presents consumer credit market growth from 2020–2034, with digital lending adoption driving the historical trajectory and fintech-led expansion sustaining forecast momentum.

To get more information on this market, Request Sample

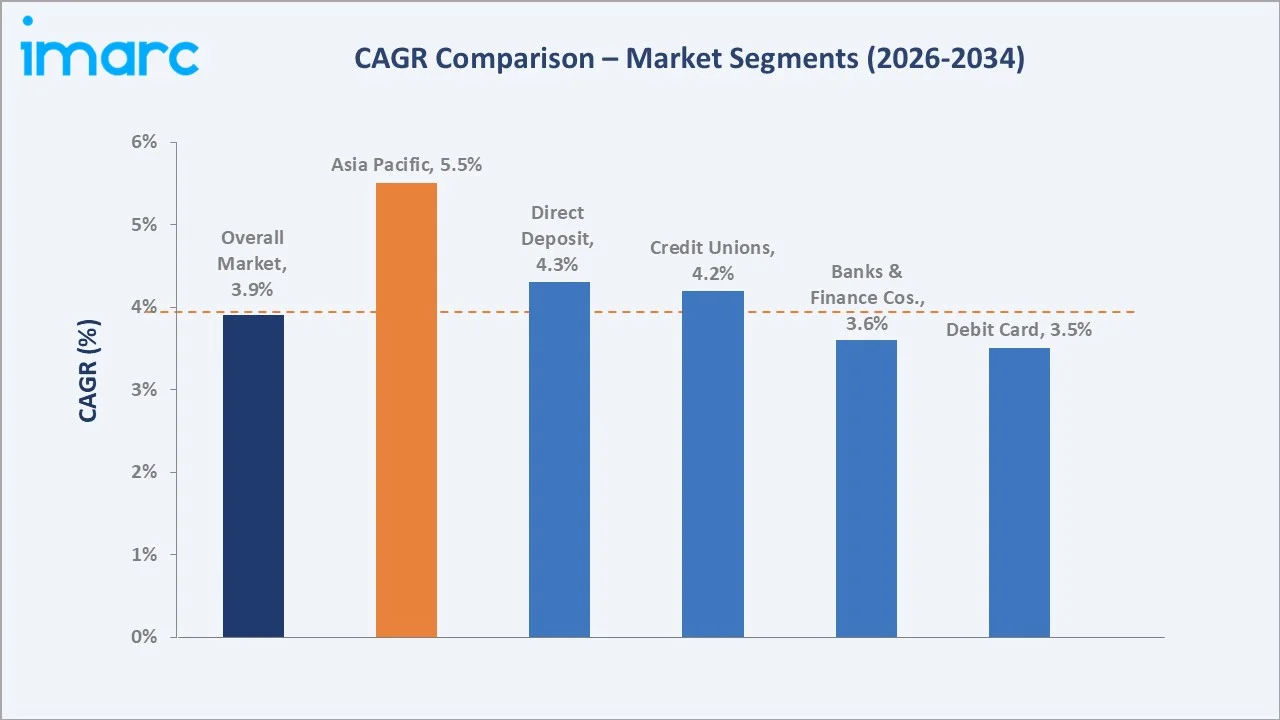

CAGR analysis identifies Asia Pacific and alternative payment methods as the fastest-growing segments in the global consumer credit market through 2034.

Executive Summary

The global consumer credit market is transforming through digital lending, AI-powered credit scoring, and the mainstreaming of Buy Now Pay Later products. Valued at USD 12.5 Billion in 2025, it is projected to reach USD 17.6 Billion by 2034 at a 3.9% CAGR. Expanding middle-class populations, MSME financing demand, and embedded finance partnerships are driving steady credit issuance growth.

Banks and Finance Companies lead the market with a 71.6% share in 2025, supported by large deposit bases and multi-product cross-sell. Debit Cards account for 60.0% of payment methods. Key trends include fintech-led unsecured lending, real-time underwriting, BNPL expansion, and tighter regulatory oversight of digital lenders across the US, EU, and India.

North America leads global demand with a 35.0% share in 2025, anchored by deep credit card penetration and strong US consumer spending. Asia Pacific holds 29.1% and is the fastest-growing region, fuelled by India, China, and Indonesia, where smartphone-based lending platforms are onboarding millions of first-time borrowers. Europe contributes 23.4%.

Key Market Insights

|

Insight |

Data |

|

Largest Issuer Segment |

Banks and Finance Companies – 71.6% share (2025) |

|

Second Issuer Segment |

Credit Unions – 18.4% share (2025) |

|

Leading Payment Method |

Debit Card – 60.0% share (2025) |

|

Leading Region |

North America – 35.0% revenue share (2025) |

|

Second Region |

Asia Pacific – 29.1% revenue share (2025) |

|

Top Companies |

JPMorgan Chase, Bank of America, Citigroup, HSBC, China Construction Bank |

Key Analytical Observations Supporting The Above Data:

- Banks and Finance Companies' 71.6% dominance in 2025 reflects their scale in deposit-linked credit issuance, multi-channel distribution, and regulatory credibility that non-bank lenders are still building across most jurisdictions.

- Credit Unions hold 18.4% in 2025, maintaining relevance through member-owned cooperative models, community lending depth, and relationship-based underwriting that remain competitive in North America and parts of Europe.

- Debit Card-linked credit products at 60.0% in 2025 highlight how card networks such as Visa and Mastercard have become the default payment rail, supported by instalment-based EMI offerings from banks including HDFC and Bank of America.

- Direct Deposit at 25.7% in 2025 remains strong in payroll-linked lending, government disbursement programs, and recurring EMI collection frameworks used across institutional consumer credit portfolios.

- North America's 35.0% global share in 2025 is driven by deep credit card penetration.

- Asia Pacific's position as the fastest-growing region is underpinned by India's MSME expansion, where enterprises generated millions of jobs, and digital-first lending platforms rapidly onboarding previously underserved borrowers.

Global Consumer Credit Market Overview

Consumer credit covers retail loans, credit card balances, auto financing, personal loans, and BNPL products extended to individuals and small businesses for personal, household, or micro-enterprise use. The ecosystem includes deposit-funded banks, fintech lenders, credit bureaus, payment networks, regulators, and merchants that integrate credit at point-of-sale.

Consumer credit spans revolving products such as credit cards and non-revolving instruments like auto, student, and personal instalment loans. Growth is driven by rising disposable incomes, digital underwriting, embedded finance at checkout, and expanding financial inclusion initiatives across emerging economies.

Market Dynamics

To evaluate market opportunities, Request Sample

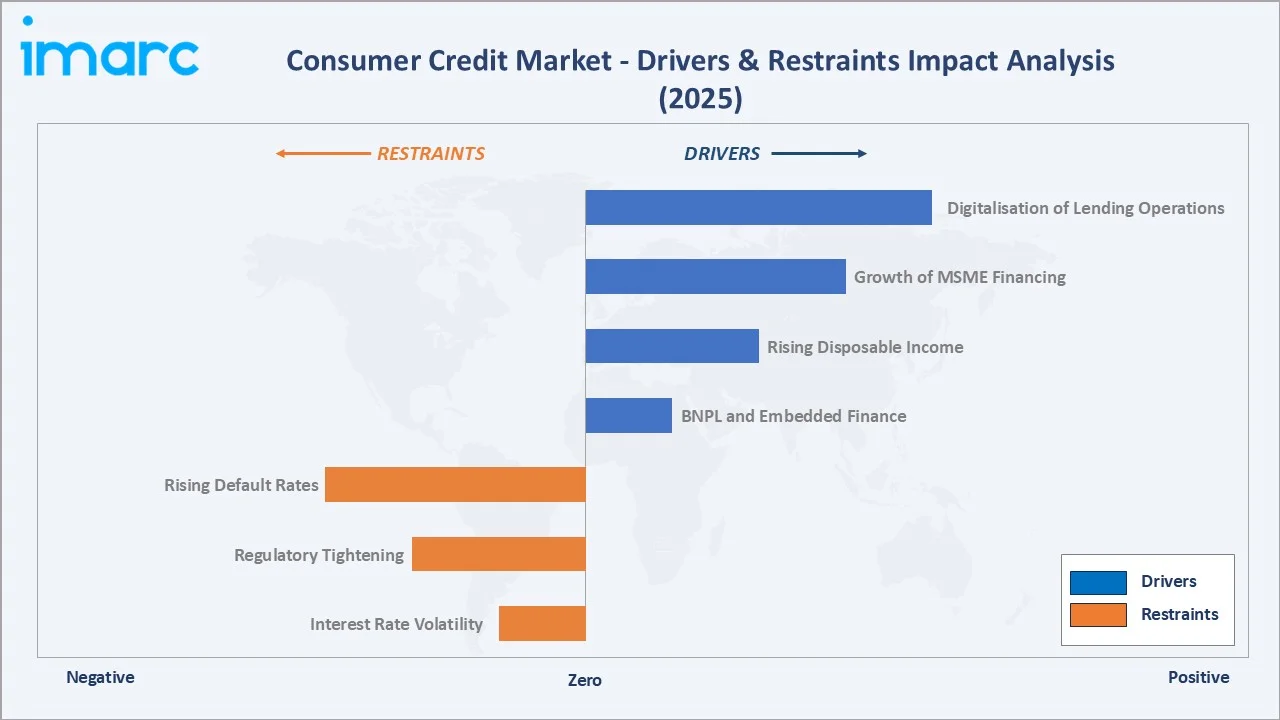

Market Drivers

- Digitalisation of Lending Operations: Rapid digitalisation of banking is enabling real-time underwriting, paperless onboarding, and embedded lending at checkout, expanding addressable borrower populations across retail and MSME segments globally.

- Growth of MSME Financing: Rising MSME credit demand is driving bank and fintech investment. India's MSMEs alone generated over 120 million jobs and contribute about 30% of national GDP, creating sustained credit pipelines.

- Rising Disposable Income: Rising disposable income is boosting demand for auto, education, and home-improvement loans, with U.S. auto loan originations averaging about USD 63 billion per month in recent periods.

- BNPL and Embedded Finance: BNPL products, now embedded with Visa, Affirm, and major retailers, are accelerating credit uptake among younger consumers and shifting issuance toward short-duration, merchant-subsidised credit.

Market Restraints

- Rising Default Rates: Post-pandemic credit stress, rising U.S. credit card delinquencies, and higher unsecured loan risks in parts of Asia have reduced bank profitability, driving increased provisioning and margin pressure, particularly during 2023–2024.

- Regulatory Tightening: Central banks including the Fed, RBI, and ECB have tightened oversight of digital lenders, imposed interest-rate caps, and mandated stricter disclosure rules, increasing compliance costs.

- Interest Rate Volatility: Interest rate volatility during 2022–2024 compressed margins on fixed-rate consumer loans, particularly in mortgage-linked and auto credit portfolios across North America and Europe.

Market Opportunities

- Emerging Market Expansion: Rapid urbanisation, expanding middle class, and smartphone-based lending across India, Indonesia, and Vietnam are opening large, under-penetrated consumer credit markets for banks and fintechs.

- Embedded BNPL Products: Visa's Flexible Credential with Affirm, launched in November 2024, allows seamless switching between debit and BNPL at checkout, unlocking new credit segments across e-commerce.

- AI-Driven Credit Scoring: AI-driven credit scoring, alternative data underwriting, and real-time fraud detection are enabling lenders to profitably serve thin-file and gig-economy borrowers previously ineligible.

Market Challenges

- Unsecured Portfolio Risk: Rising delinquencies in unsecured personal loans, BNPL, and credit cards, particularly among Gen Z borrowers, are creating portfolio quality concerns across major issuers.

- Cybersecurity and Fraud: Increasing phishing, synthetic identity fraud, and account takeover attacks have raised cybersecurity investment needs, placing pressure on smaller and mid-sized credit issuers globally.

- Credit History Gaps: Thousands of first-time borrowers in emerging markets lack formal credit histories, limiting the ability of lenders to price and scale credit responsibly without alternative underwriting.

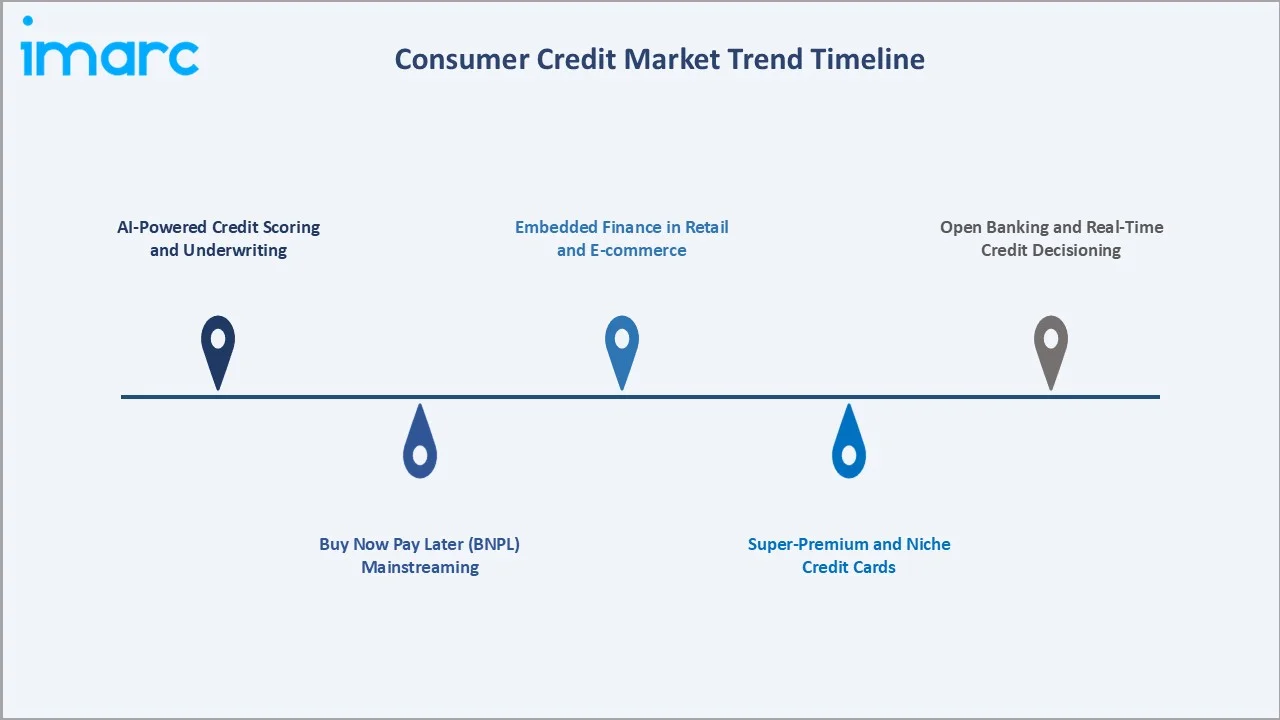

Emerging Market Trends

1. AI-Powered Credit Scoring and Underwriting

Banks and fintechs are adopting AI and machine learning to assess creditworthiness using alternative data including utility bills and transaction history. AI-based underwriting is improving approval rates for thin-file customers while reducing default risk across portfolios.

2. Buy Now Pay Later (BNPL) Mainstreaming

BNPL has moved from niche to standard checkout option. Visa's 2024 Flexible Credential launch with the Affirm Card enabled seamless switching between debit and BNPL, expanding BNPL usage across US e-commerce and travel merchants.

3. Embedded Finance in Retail and E-commerce

Retailers, airlines, and ride-hailing apps are embedding credit products directly into user journeys. This shift is transferring credit origination from bank websites to third-party platforms, reshaping distribution economics.

4. Super-Premium and Niche Credit Cards

Banks are launching invitation-only premium cards targeting high-net-worth customers. Axis Bank's Primus and the Times Black ICICI Bank card illustrate issuer focus on premium segments with higher fee and interchange economics.

5. Open Banking and Real-Time Credit Decisioning

Open banking APIs enable lenders to access verified income and cash-flow data directly, shortening credit decision cycles from days to seconds and improving accuracy of affordability assessments across Europe and Asia Pacific.

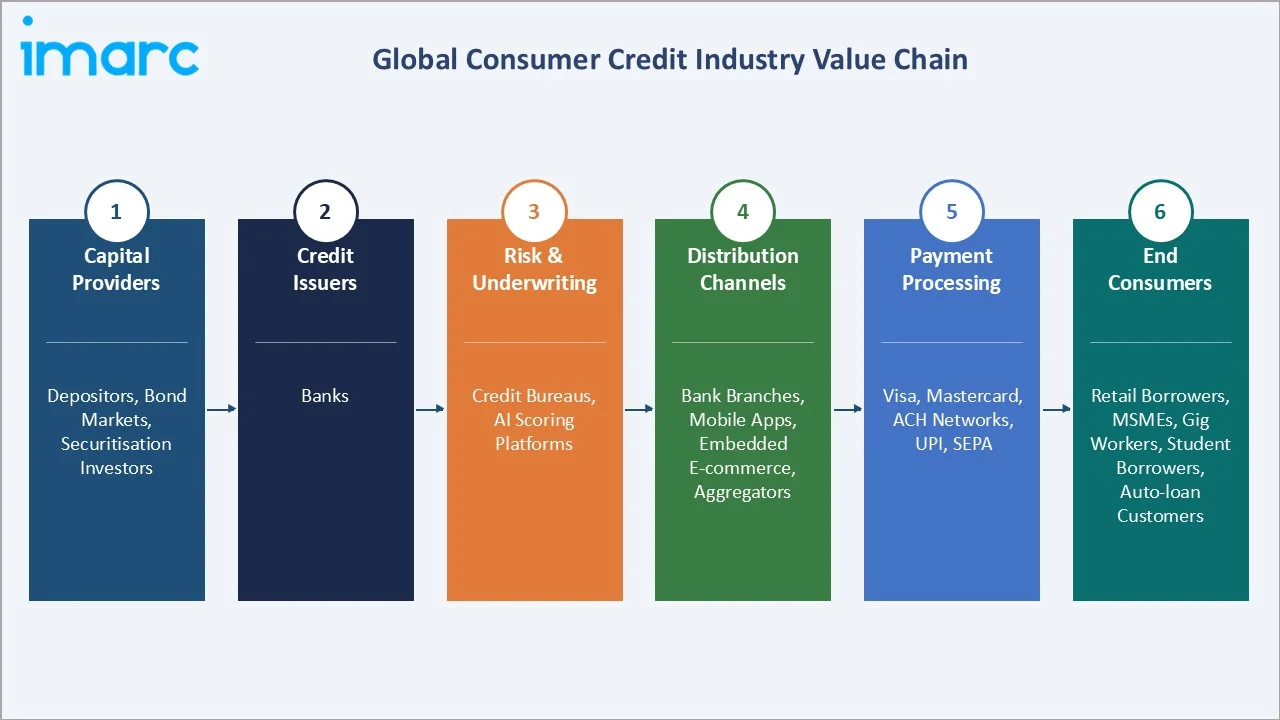

Industry Value Chain Analysis

The consumer credit value chain spans six stages, from capital sourcing to borrower servicing, each with distinct margin pools and regulatory exposure.

|

Stage |

Key Players / Examples |

|

Capital Providers |

Depositors, bond markets, securitisation investors |

|

Credit Issuers |

Banks, Credit Unions, Fintech lenders |

|

Risk & Underwriting |

Credit bureaus, AI scoring platforms |

|

Distribution Channels |

Bank branches, mobile apps, embedded e-commerce, aggregators |

|

Payment Processing |

Visa, Mastercard, ACH networks, UPI, SEPA |

|

End Consumers |

Retail borrowers, MSMEs, gig workers, student borrowers, auto-loan customers |

Tier-1 global banks capture the largest share of value by integrating deposit collection, underwriting, and servicing under a single franchise. Their scale enables better funding costs, risk pooling, and technology investments that smaller lenders cannot match at equivalent unit economics.

Technology Landscape in the Consumer Credit Industry

AI and Machine Learning in Credit Scoring

AI-based credit scoring models ingest alternative data points including utility payments, telecom usage, and e-commerce behaviour to generate richer risk profiles. These platforms are widely adopted by fintech lenders and increasingly by traditional banks to serve thin-file consumers.

Cloud-Native Core Banking and Loan Origination Systems

Cloud-native loan origination systems from Finastra, Temenos, and nCino are replacing legacy mainframe platforms, enabling faster product launches and improved operational efficiency after cloud migration.

Blockchain and Tokenised Credit Products

Early blockchain pilots are exploring tokenised loans, smart-contract-based credit settlement, and decentralised bureaus. JPMorgan's Onyx unit and Swiss banks have demonstrated working tokenised credit settlements for institutional clients.

Real-Time Payments and Instant Settlement Rails

FedNow in the US, UPI in India, and SEPA Instant in Europe enable round-the-clock credit disbursement and repayment. This infrastructure supports real-time lending products and improves collection efficiency across geographies.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Credit Type | Non-revolving Credits | 🔒 |

2025 |

| Service Type | Credit Services | 🔒 |

2025 |

| Issuer | Banks and Finance Companies | 71.6% |

2025 |

| Payment Method | Debit Card | 60.0% |

2025 |

| Region | North America | 35% |

2025 |

By Issuer

Banks and Finance Companies hold a 71.6% share in 2025, underpinned by large deposit bases, multi-product cross-sell, and regulatory credibility that gives incumbents a durable advantage across mature credit markets.

To access detailed market analysis, Request Sample

Credit Unions account for 18.4% in 2025, retaining relevance through member-owned governance, community lending focus, and competitive pricing across the US and parts of Europe. Others, including fintech lenders and BNPL specialists, hold 10.0% and are growing fastest as embedded finance expands.

By Payment Method

Debit Cards lead with 60.0% in 2025, reinforced by EMI-on-debit products from banks such as HDFC (EASYEMI), Bank of America, and Chase that allow borrowers to split purchases into instalments at point-of-sale.

Direct Deposit holds 25.7% in 2025, dominant for payroll-linked personal loans, government disbursements, and scheduled EMI collection frameworks. Other payment methods, including digital wallets and BNPL-native rails, account for 14.3% and are scaling rapidly with Gen Z adoption.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

35.0% |

Deep credit card penetration; mature credit bureaus; total US loans at USD 13.57 trillion (March 2026); strong fintech ecosystem |

|

Asia Pacific |

29.1% |

India MSME credit expansion (120 million jobs); China's urbanisation; Indonesia and Vietnam smartphone-based lending growth |

|

Europe |

23.4% |

784 foreign bank branches in EU (2021); PSD2 open banking adoption; growing BNPL usage in Germany, UK, France |

|

Latin America |

6.7% |

Projected 60% rise in real disposable income (2021-2040); Brazil and Mexico credit card penetration; Pix-enabled credit |

|

Middle East & Africa |

5.8% |

USD 238 Billion ICT spending (2024); Gulf digital banking expansion; mobile-first credit products in Kenya, Nigeria |

North America commands a 35.0% global revenue share in 2025, reflecting its leadership in consumer credit. The United States hosts major issuers including JPMorgan Chase, Bank of America, Citigroup, and Wells Fargo, supported by robust credit card use and the launch of new products such as Hypercard's American Express-backed card in December 2024.

Asia Pacific, with 29.1% in 2025, is the fastest-growing region, driven by India's digital lending ecosystem, China's mobile payment-linked credit, and expanding credit access across Indonesia and Vietnam. Europe holds 23.4%, anchored by established retail banks and accelerating BNPL adoption under PSD2 open banking frameworks that are reshaping distribution across the EU.

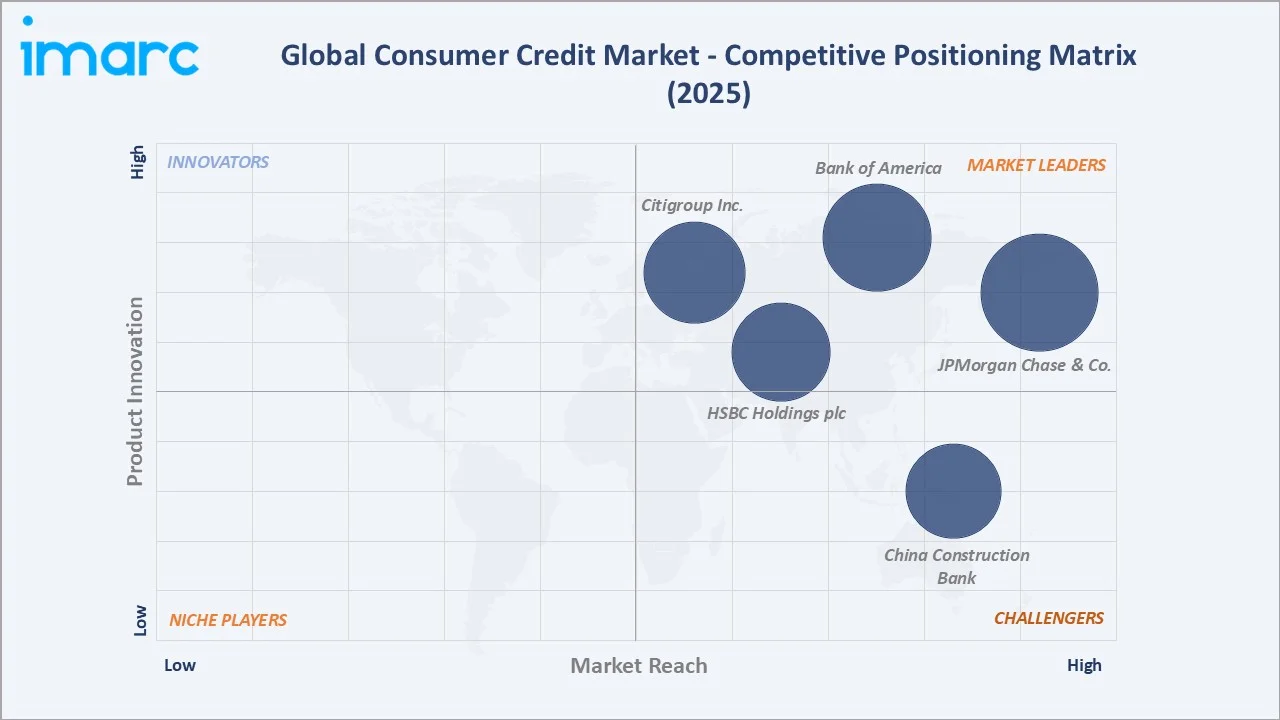

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

JPMorgan Chase & Co. |

Chase / Chase Sapphire |

Leader |

Scale, credit cards, digital platforms |

|

Bank of America Corporation |

Bank of America / Preferred Rewards |

Leader |

US retail banking depth, rewards ecosystem |

|

Citigroup Inc. |

Citi / Citi Double Cash |

Leader |

Global reach, cards, cross-border lending |

|

HSBC Holdings plc |

HSBC / HSBC Premier |

Leader |

Cross-border, wealth-linked credit |

|

China Construction Bank |

CCB / Long Card (Dragon Card) |

Challenger |

Chinese retail credit, mortgage strength |

The consumer credit market is led by a few global banking groups alongside a fragmented pool of regional players and rapidly scaling fintechs. JPMorgan Chase reported over USD 177 Billion in net revenue in 2024, cementing its position as the largest global consumer credit franchise by scale and profitability.

Key Company Profiles

JPMorgan Chase & Co.

JPMorgan Chase, headquartered in New York, is the largest US bank and a global leader in consumer credit. In 2024, the bank reported record net revenue of over USD 177 Billion, with Consumer & Community Banking contributing a major share through credit cards, auto lending, and mortgages.

- Product & Service Portfolio: Chase-branded credit cards (Sapphire, Freedom), personal loans, auto loans, home equity, and co-branded cards with Amazon, Marriott, and United Airlines.

- Recent Developments: In Jan 2026, JPMorgan Chase & Co. has announced a landmark agreement with Apple Inc. to become the new issuer of the Apple Card, replacing Goldman Sachs. The transition is expected to take place over approximately 24 months, with existing customer balances and services continuing uninterrupted during the shift. This strategic move significantly strengthens JPMorgan’s position in the premium consumer credit card segment and expands its already dominant credit card portfolio.

- Strategic Focus: Scaling digital-first credit origination, consumer-SMB cross-sell, and expanding premium card portfolios to capture higher interchange and fee revenue.

Bank of America Corporation

Bank of America Corporation, headquartered in Charlotte, North Carolina, serves approximately 69 million consumer and small business clients. In 2024, consumer banking generated sizeable fee and interest income, supported by deep credit card and auto-lending portfolios across the United States.

- Product & Service Portfolio: Credit cards (Customized Cash Rewards, Travel Rewards, Premium Rewards), personal loans, auto loans, home equity lines, and co-branded cards.

- Recent Developments: In Jan 2024, Bank of America reported continued momentum in its consumer credit segment, with strong credit card account growth through 2025. The expansion reflects sustained customer acquisition and increased investment in its card business, reinforcing its position in the U.S. consumer lending market.

- Strategic Focus: Growing Preferred Rewards loyalty, digital-first credit acquisition, and integrated wealth-credit cross-sell with Merrill Lynch clients.

Citigroup Inc.

Citigroup, headquartered in New York, maintains a globally diversified financial services presence, while streamlining parts of its international consumer banking operations. In 2024, the bank advanced its Asia strategy by planning a wholly owned investment banking unit in China, reinforcing its regional institutional business focus.

- Product & Service Portfolio: Citi Double Cash, Premier, and Custom Cash credit cards, personal loans, US retail banking, and co-branded cards with American Airlines and Costco.

- Recent Developments: In Dec 2025, Citigroup announced a major organizational restructuring, combining its branded cards and retail services units into a new U.S. Consumer Cards division, elevating it as a core business line. The move underscores Citi’s strategic focus on credit cards as a primary growth engine within its consumer banking operations.

- Strategic Focus: US retail banking modernisation, premium card expansion, and cross-border wealth-linked consumer credit for affluent clients.

Market Concentration Analysis

The global consumer credit market is moderately concentrated at the top tier, with JPMorgan Chase, Bank of America, Citigroup, HSBC, and Wells Fargo collectively accounting for an estimated 30–35% of global revenue in 2025. Scale, funding cost advantages, and cross-border technology investments create entry barriers.

Fragmentation increases sharply below the top tier, with regional banks, credit unions, and fintech lenders competing for underserved niches such as thin-file borrowers, gig workers, and MSME credit. This bifurcated structure is typical of mature financial services with strong capital intensity.

Consolidation continues through selective acquisitions, with Barclays-GM's October 2024 GM Rewards Mastercard partnership illustrating how mid-tier banks pursue co-branded deals to secure captive customer bases. ESG and digital compliance are further accelerating consolidation pressure on sub-scale issuers.

Investment & Growth Opportunities

Fastest-Growing Segments

BNPL and embedded credit are the fastest-growing segments through 2034, driven by merchant integration and Gen Z adoption. Visa's Flexible Credential with Affirm is expected to accelerate BNPL issuance across US e-commerce and travel merchants.

MSME credit across Asia Pacific is the highest-growth banked segment. India's MSMEs already generated 120 Million jobs and contribute about 30% of GDP, with digital lending platform rollouts enabling scalable credit delivery to small businesses.

Emerging Market Expansion

The Middle East and Africa region, at 5.8% of global share in 2025, offers large upside through mobile-first digital credit products. Regional ICT spending of USD 238 Billion in 2024 is enabling secure online credit and wider consumer trust in digital lenders.

Latin America, with projected 60% real disposable income growth between 2021 and 2040, is another high-potential region. Rising credit card penetration in Brazil and Mexico, combined with Pix-enabled instant credit, is expanding the addressable base.

Venture & Strategic Investment Trends

Investment activity in consumer credit fintechs remains active. BNPL specialists, AI-underwriting platforms, alternative data credit bureaus, and cybersecurity providers continue to attract venture and strategic capital from incumbent banks seeking technology differentiation.

Future Market Outlook (2026-2034)

The global consumer credit market forecast projects value expansion from USD 12.5 Billion in 2025 to USD 17.6 Billion by 2034 at a CAGR of 3.9% – an incremental addition of over USD 5.1 Billion. Growth will be driven by Asia Pacific expansion, BNPL mainstreaming, AI underwriting, and the shift from branch-led to digital-first credit origination.

Three transformational trends will reshape consumer credit through 2034. AI-based credit scoring will compress decision cycles to seconds and enable profitable lending to thin-file borrowers. Embedded finance will move origination from bank websites to merchant checkouts. Open banking will redefine data ownership, forcing incumbents to compete on product design.

By 2034, consumer credit is expected to evolve from a product category into an embedded service layer across retail, mobility, and wellness journeys. Issuers investing in AI, data platforms, and merchant partnerships are likely to capture disproportionate growth, while sub-scale lenders face margin pressure.

Research Methodology

Primary Research

Primary research included structured interviews and surveys conducted in 2024–2025 with retail credit heads at Tier-1 banks, fintech founders, credit bureau executives, MSME lending specialists, and regulators across North America, Europe, and Asia Pacific.

Secondary Research

Secondary sources include bank annual reports (JPMorgan Chase, Bank of America, Citigroup, HSBC, Barclays), regulatory publications (Federal Reserve, ECB, RBI, OCC), credit bureau data (Experian, TransUnion, Equifax), and IMF and World Bank financial access reports.

Forecasting Models

Market size estimations and growth projections were derived using combined top-down and bottom-up forecasting models, incorporating GDP growth, household debt ratios, credit penetration benchmarks, historical issuance patterns, and scenario analysis.

Consumer Credit Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Credit Types Covered | Revolving Credits, Non-revolving Credits |

| Service Types Covered | Credit Services, Software and IT Support Services |

| Issuers Covered | Banks and Finance Companies, Credit Unions, Others |

| Payment Methods Covered | Direct Deposit, Debit Card, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | JPMorgan Chase & Co., Bank of America Corporation, Citigroup Inc., HSBC Holdings plc, China Construction Bank, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the consumer credit market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global consumer credit market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the consumer credit industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Consumer Credit Market Report

The global consumer credit market was valued at USD 12.5 Billion in 2025, driven by digital lending adoption, rising MSME credit demand, and expanding BNPL products.

The market is projected to reach USD 17.6 Billion by 2034, growing at a CAGR of 3.9% during 2026-2034, supported by Asia Pacific expansion and AI underwriting.

Banks and Finance Companies lead with a 71.6% share in 2025, reflecting their scale, deposit bases, multi-product cross-sell, and regulatory credibility across retail credit markets.

Debit Cards lead with a 60.0% share in 2025, driven by EMI-on-debit products from banks such as HDFC, Bank of America, and Chase enabling easy instalment purchases.

North America leads with a 35.0% share in 2025, anchored by deep credit card penetration, mature credit bureaus, and total United States total loans were approximately USD 13.57 trillion in March 2026.

Key drivers include digitalisation of lending, MSME credit demand, rising disposable incomes, BNPL adoption, AI-based underwriting, and expanding financial inclusion across emerging markets.

Asia Pacific is the fastest-growing region, powered by India MSME expansion, China digital lending, and Indonesia and Vietnam smartphone-based credit platforms through 2034.

Leading companies include JPMorgan Chase & Co., Bank of America Corporation, Citigroup Inc., HSBC Holdings plc, and China Construction Bank.

Credit Unions hold an 18.4% share in 2025, supported by member-owned governance, community lending strength, and competitive pricing across North America and parts of Europe.

BNPL growth is driven by Gen Z adoption, merchant integration, and products such as Visa's November 2024 Flexible Credential with the Affirm Card enabling seamless checkout.

AI-based credit scoring, cloud-native loan origination, open banking APIs, and real-time payment rails are reducing decision times, improving risk accuracy, and expanding borrower access.

Key challenges include rising delinquencies in unsecured portfolios, interest rate volatility, tighter regulation, cybersecurity risk, and limited credit histories in emerging markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade