Conveyor Belt Market Size, Share, Trends and Forecast by Type, End-Use, and Region, 2026-2034

Global Conveyor Belt Market Size, Share, Trends & Forecast (2026-2034)

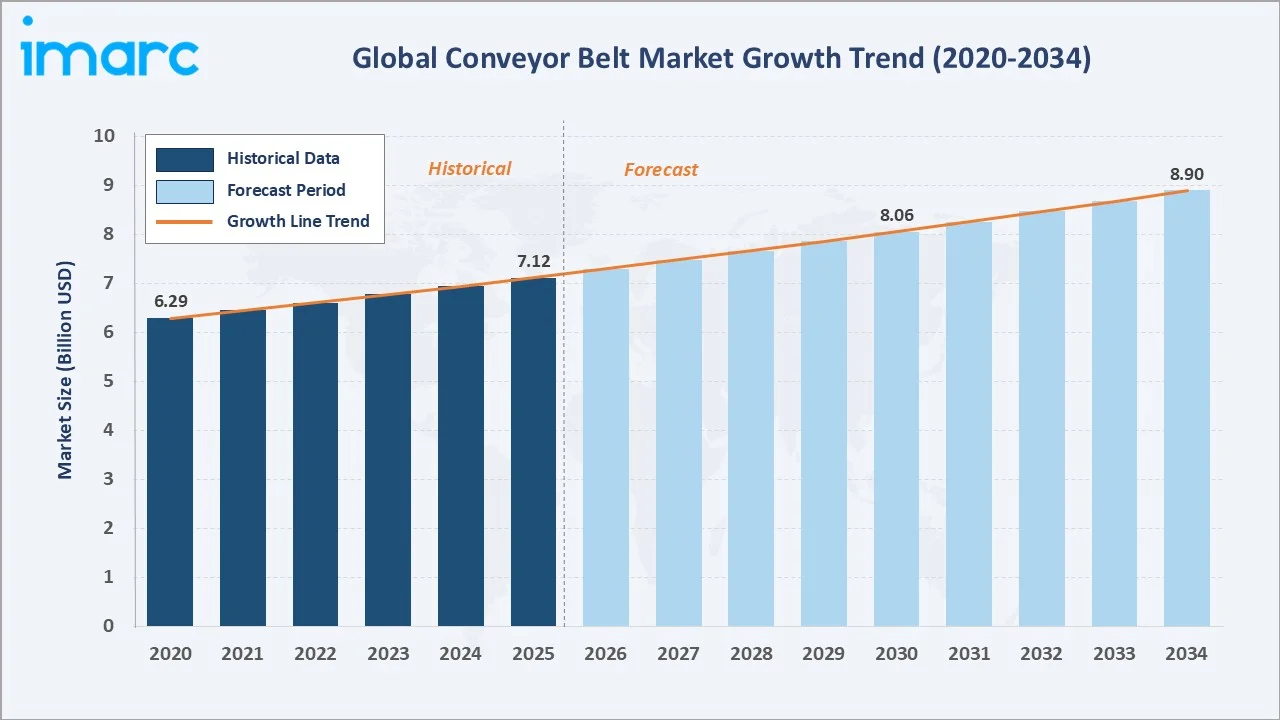

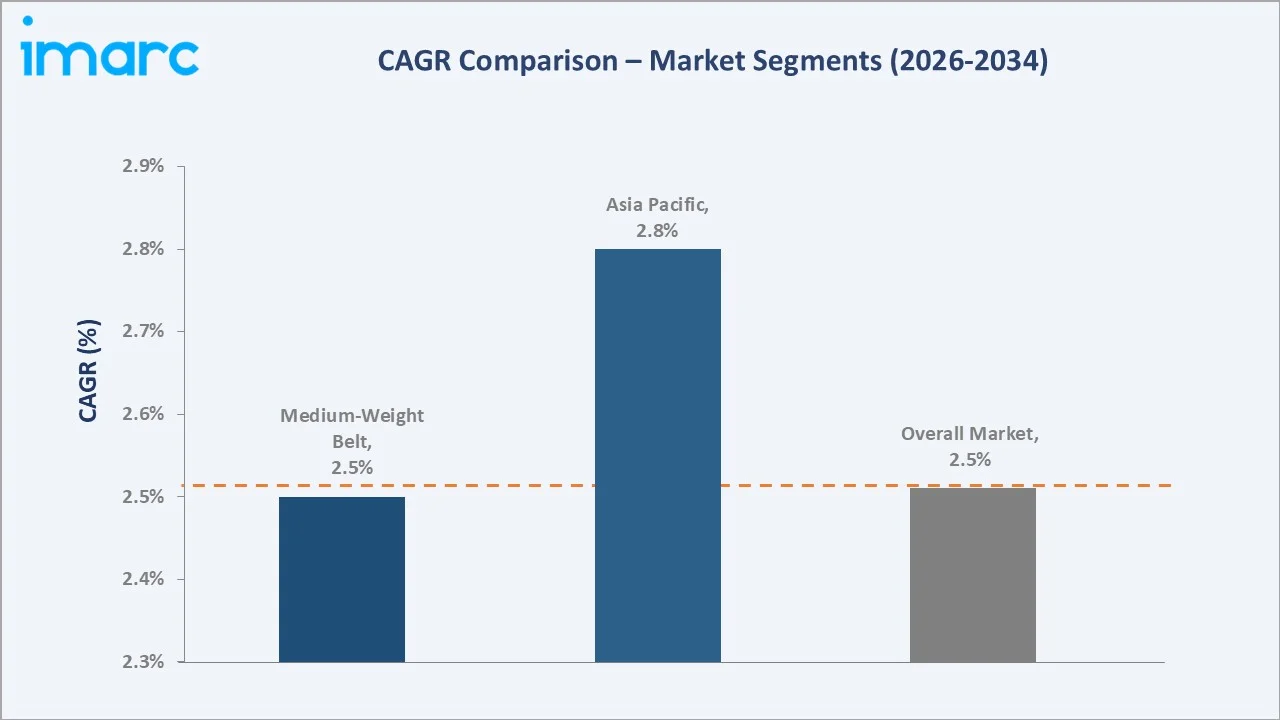

The global conveyor belt market size reached USD 7.12 Billion in 2025 and is projected to reach USD 8.90 Billion by 2034, exhibiting a CAGR of 2.51% during 2026-2034. Rising industrial automation, expanding mining operations, growing e-commerce logistics infrastructure, and broad adoption of conveyor systems in aviation and manufacturing are the primary forces driving market growth.

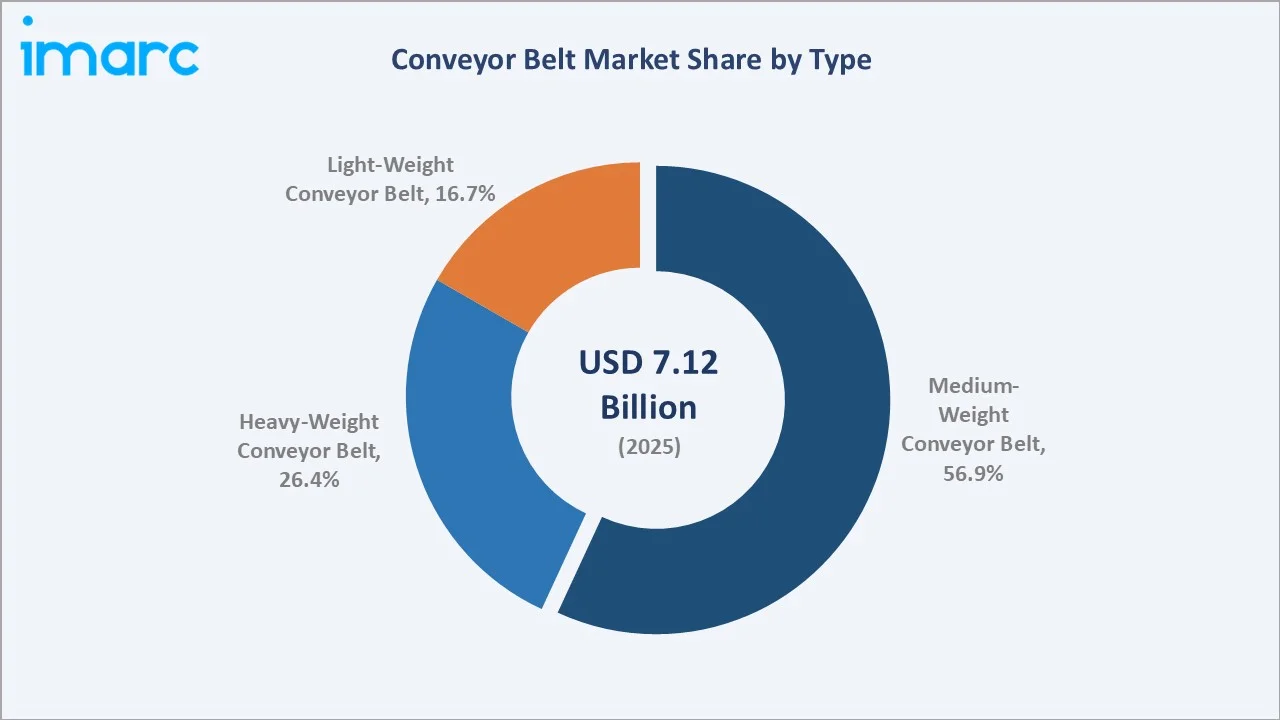

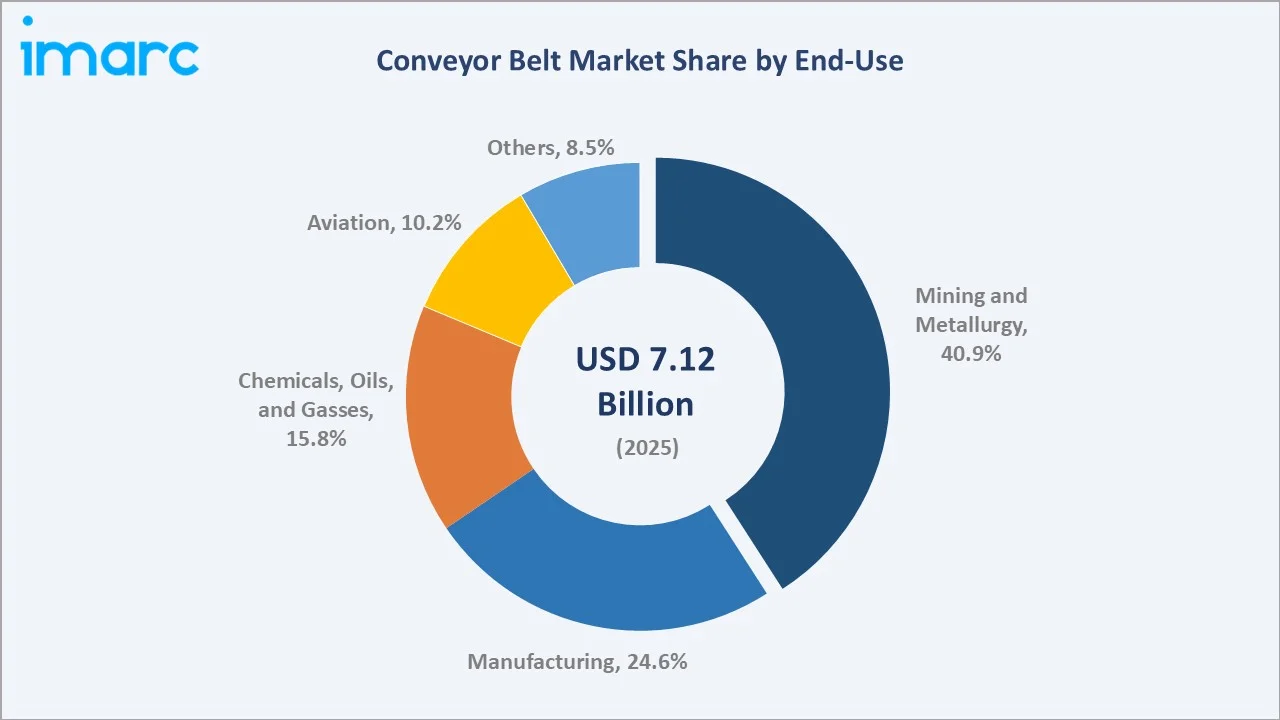

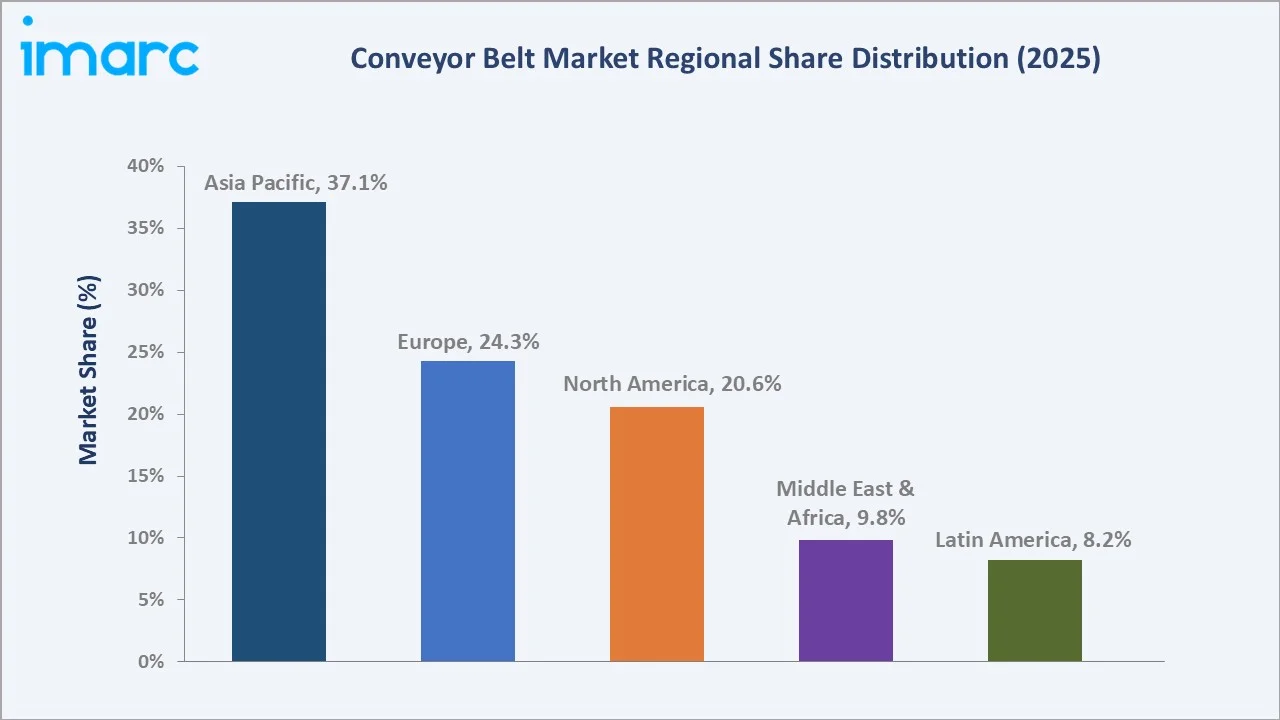

Medium-weight conveyor belt dominates the type segment at 56.9% in 2025, while mining and metallurgy leads the end-use segment at 40.9%. Asia Pacific commands a leading 37.1% regional share in 2025, reflecting the region's role as both the world's largest manufacturing base and a key mining hub.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 7.12 Billion |

|

Forecast Market Size (2034) |

USD 8.90 Billion |

|

CAGR (2026-2034) |

2.51% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (37.1% share, 2025) |

|

Second Largest Region |

Europe (24.3% share, 2025) |

|

Leading Belt Type |

Medium-Weight Conveyor Belt (56.9%, 2025) |

|

Leading End-Use |

Mining and Metallurgy (40.9%, 2025) |

The global conveyor belt market growth trajectory from 2020 through 2034, with historical expansion to USD 7.12 Billion in 2025, reflects consistent infrastructure- and automation-driven demand. The forecast to USD 8.90 Billion captures accelerating e-commerce warehouse buildouts, mining reinvestment cycles, and Asia Pacific industrialization-led demand.

To get more information on this market, Request Sample

The CAGR trajectories across key type, end-use, and regional sub-segments, with light-weight conveyor belts at ~3.1% CAGR and aviation applications at ~2.9% CAGR, represent the fastest-growing categories within the global conveyor belt industry analysis through 2034.

Executive Summary

The global conveyor belt market is on a sustained growth trajectory from USD 7.12 Billion in 2025 to USD 8.90 Billion by 2034. Conveyor belts, essential material handling components deployed across mining, manufacturing, aviation, logistics, and chemical processing, benefit from the non-discretionary, safety-critical nature of industrial demand across global markets.

Medium-weight conveyor belt dominates the type segment at 56.9% in 2025, owing to its versatility across the broadest range of manufacturing, e-commerce distribution, and general industrial applications. Heavy-weight conveyor belt at 26.4% commands premium pricing in mining and bulk material handling where abrasion resistance and high tensile strength are non-negotiable operational requirements.

Light-weight conveyor belt at 16.7% in 2025 is the fastest-growing type segment, driven by exponential e-commerce warehouse automation, food and beverage processing modernization, and pharmaceutical manufacturing requirements for hygienic, modular, and energy-efficient belt solutions.

Asia Pacific dominates at 37.1% in 2025, reflecting China's position as the world's largest manufacturing economy and Australia's role as a top-tier iron ore and coal producing nation with extensive conveyor belt requirements. Europe at 24.3% and North America at 20.6% follow, driven by industrial automation investment and infrastructure maintenance cycles.

Key Market Insights

|

Insight |

Data |

|

Largest Belt Type |

Medium-Weight Conveyor Belt – 56.9% share (2025) |

|

Second Belt Type |

Heavy-Weight Conveyor Belt – 26.4% share (2025) |

|

Leading End-Use |

Mining and Metallurgy – 40.9% share (2025) |

|

Second End-Use |

Manufacturing – 24.6% share (2025) |

|

Leading Region |

Asia Pacific – 37.1% share (2025) |

|

Second Largest Region |

Europe – 24.3% share (2025) |

|

Top Companies |

Bando Chemical Industries, Ltd., Continental AG, Habasit, Intralox, Volta Belting Technology, The Yokohama Rubber Co., Ltd. |

Key Analytical Observations Supporting the Above Data:

- Medium-weight conveyor belt, with 56.9% in 2025, dominates due to its unmatched versatility. Its capacity to handle a wide range of goods across manufacturing lines, airport baggage systems, distribution centres, and food processing facilities makes it the default specification across the broadest array of industrial applications globally.

- Mining and metallurgy, with 40.9% in 2025, leads end-use because of the essential role of heavy-duty conveyor belts in transporting ore, coal, and bulk minerals across often multi-kilometre underground and open-pit mining operations where belt reliability is mission-critical.

- Asia Pacific's 37.1% dominance in 2025 reflects structural forces acting simultaneously: China's manufacturing scale, Australia's mining output, and rapidly industrializing ASEAN economies deploying new conveyor systems across manufacturing, logistics, and food processing.

- Europe's 24.3% share benefits from Germany's highly automated automotive and machinery manufacturing sector, robust food-grade belt demand across European food processors, and growing deployment of conveyor systems in green energy and offshore wind infrastructure.

Global Conveyor Belt Market Overview

A conveyor belt is a continuous loop of material used within a belt conveyor system for transporting goods, raw materials, bulk solids, and products between locations. Available in lightweight, medium-weight, and heavy-weight variants, conveyor belts are manufactured using rubber, polyvinyl chloride (PVC), thermoplastic polyurethane (TPU), steel cord reinforcement, and multi-ply textile fabric constructions to meet diverse industrial load and durability requirements.

The global conveyor belt ecosystem integrates raw material compounders, belt manufacturing facilities, surface finishing and testing operations, industrial distributors, project installation contractors, and end-use industries spanning mining and metallurgy, manufacturing, chemicals and oil & gas, aviation, food processing, and logistics. Belt performance is governed by international standards including ISO 22721, DIN 22102, and ASTM D378, with specialized grades required for fire resistance (ISO 14973), oil resistance, and high-temperature applications.

Market Dynamics

To evaluate market opportunities, Request Sample

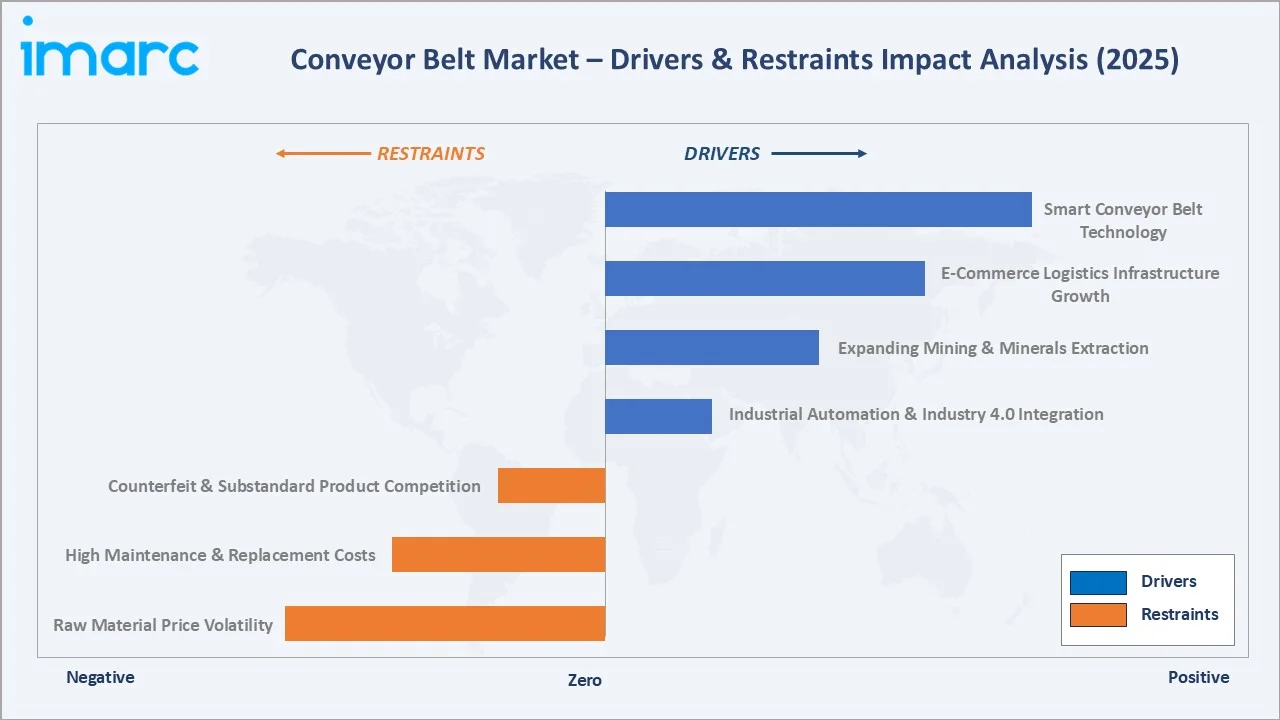

Market Drivers

- Industrial Automation and Industry 4.0 Integration: The global push toward manufacturing and warehouse automation is accelerating conveyor belt system adoption. Automated conveyor systems integrated with robotic picking arms and AI-driven sortation are projected to increase warehouse automation adoption by 45% by 2030, with belt conveyor systems forming the backbone of these automated material flows.

- Expanding Mining and Minerals Extraction: Global mining output reached 17.9 billion tons in 2021, and continued demand for energy transition minerals, including copper, lithium, cobalt, and iron ore, is driving capital expenditure in new mining capacity that fundamentally requires heavy-duty conveyor belt infrastructure for ore transport.

- E-Commerce Logistics Infrastructure Growth: The sustained global expansion of e-commerce fulfilment and last-mile distribution infrastructure, with major operators constructing large-scale automated distribution centres, creates continuous, growing demand for medium-weight and light-weight conveyor belt systems at scale.

Market Restraints

- Raw Material Price Volatility: Fluctuations in natural rubber, synthetic rubber (SBR, NBR), polyester yarn, and steel cord prices create significant margin pressure for conveyor belt manufacturers and procurement cost unpredictability for end users. Global commodity cycles and energy price movements make belt procurement cost planning challenging.

- High Maintenance and Replacement Costs: Conveyor belt systems operating in mining and heavy industrial environments require frequent inspection, tensioning, vulcanized splicing, and periodic section replacement, generating significant ongoing operational expenditure that can delay new system investment by diverting maintenance budgets.

Market Opportunities

- Smart Conveyor Belt Technology: AI-enabled energy management solutions are improving operational efficiency in conveyor systems by optimizing power consumption based on real-time conditions and load requirements. The integration of intelligent technologies is enhancing system performance, safety, and automation capabilities, supporting broader adoption across industries. As a result, the global smart conveyor belt systems market is experiencing steady growth, driven by increasing demand for more efficient, reliable, and intelligent material handling solutions.

- Sustainable and Eco-Friendly Belt Materials: Growing corporate sustainability mandates and regulatory pressure are driving development of recyclable thermoplastic belts, bio-based rubber compounds, and energy-efficient belt constructions that align with global decarbonization targets while delivering lifecycle cost advantages.

Market Challenges

- Counterfeit and Substandard Product Competition: The prevalence of counterfeit and substandard conveyor belt products in price-sensitive markets creates operational safety risks for end users and brand dilution and margin compression challenges for established quality manufacturers competing on value rather than price alone.

- Skilled Installation and Maintenance Workforce Shortage: Conveyor belt installation, vulcanized splicing, and ongoing maintenance require specialized technical skills that are increasingly scarce globally, creating installation bottlenecks that slow new system commissioning and increase service response times for belt failures.

Emerging Market Trends

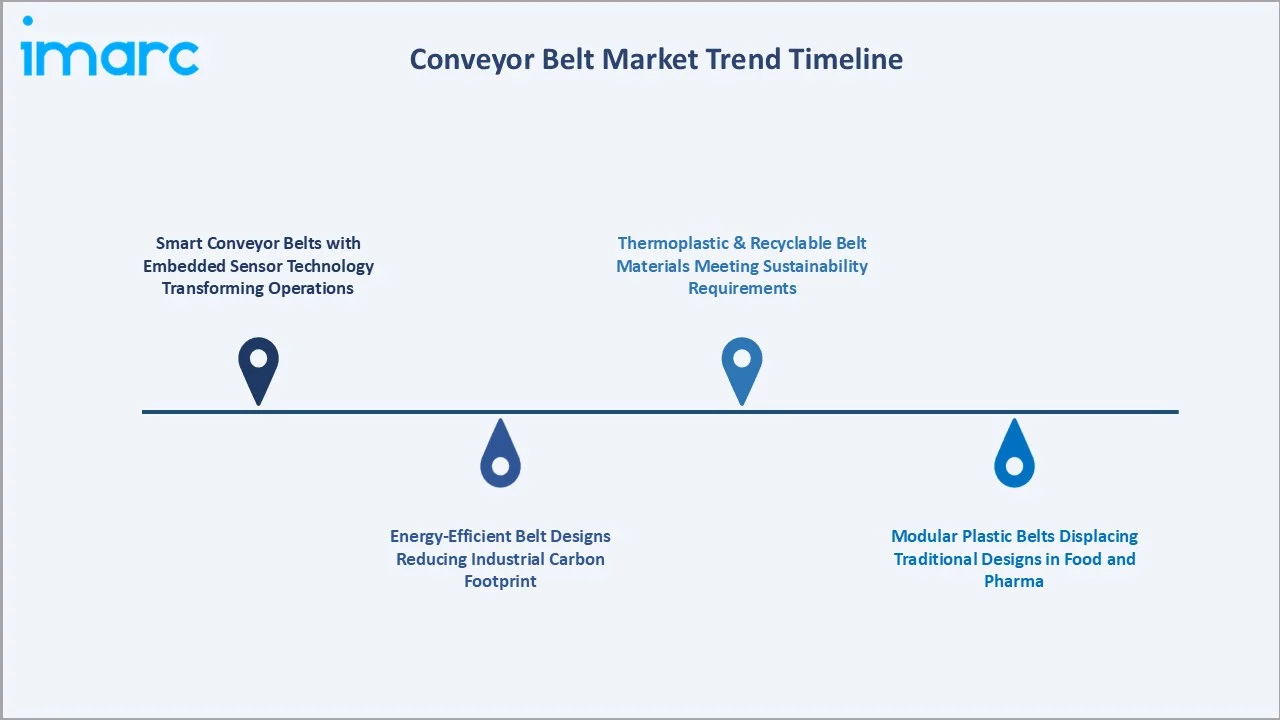

1. Smart Conveyor Belts with Embedded Sensor Technology Transforming Operations

IoT-integrated conveyor belts equipped with wear sensors, temperature monitors, tension gauges, and RFID tracking are enabling real-time predictive maintenance that reduces unplanned downtime by up to 30%. The January 2025 Wuxi Boton and Roy Hill smart monitoring partnership introduced digital management systems and Total Cost of Ownership models as the new standard for premium belt supply agreements.

2. Energy-Efficient Belt Designs Reducing Industrial Carbon Footprint

Advanced rubber compounding and construction innovations reducing conveyor belt rolling resistance are delivering energy savings of 15–25% per installation. This trend is particularly impactful for long-distance overland mining conveyors where energy accounts for 40–60% of total operating cost, making energy efficiency a direct financial driver of belt specification decisions.

3. Modular Plastic Belts Displacing Traditional Designs in Food and Pharma

Modular plastic conveyor belts are rapidly gaining specification in food processing, pharmaceutical, and packaging applications where hygiene compliance, easy piece-by-piece replacement without full system shutdown, and resistance to harsh cleaning chemicals provide decisive operational advantages over traditional rubber belt constructions.

4. Thermoplastic and Recyclable Belt Materials Meeting Sustainability Requirements

BASF's April 2025 launch of GMP-certified Elastollan FC TPU conveyor belt material at CHINAPLAS 2025, meeting global food contact standards (EU Regulation, FDA), exemplifies the accelerating shift toward thermoplastic belt materials offering durability, microbial resistance, and full regulatory compliance alongside reduced environmental impact throughout the product lifecycle.

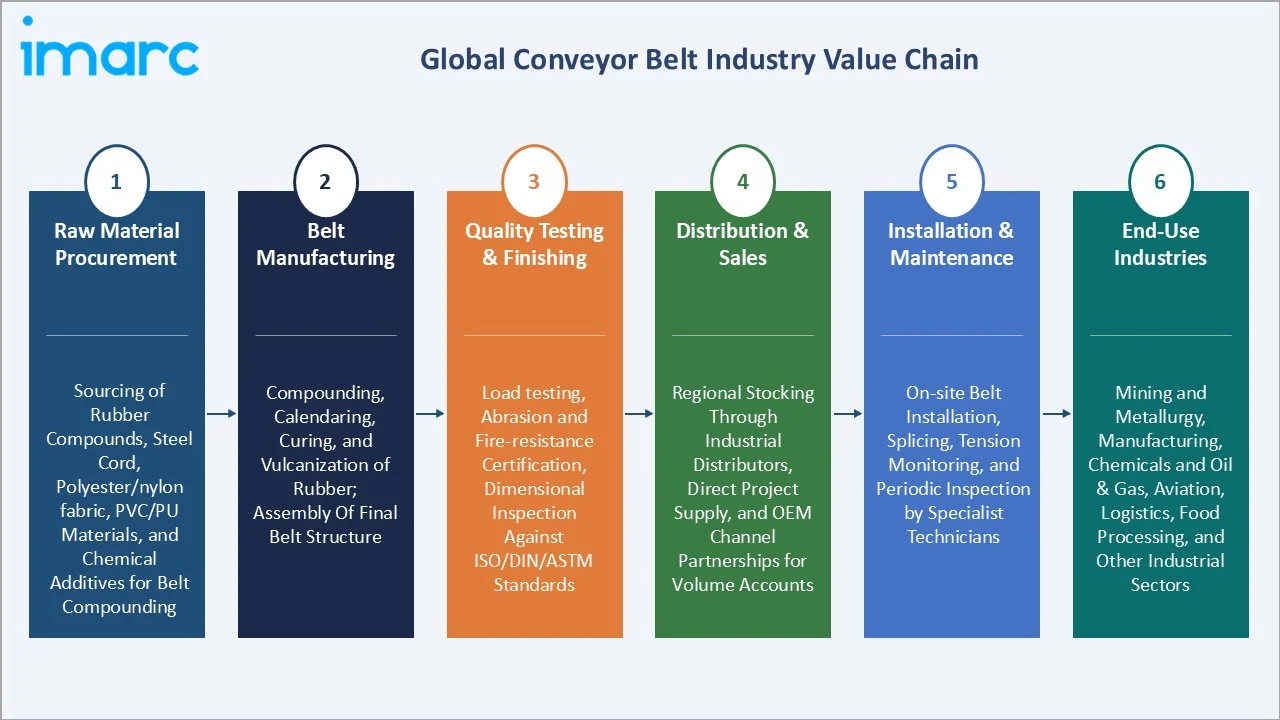

Industry Value Chain Analysis

The conveyor belt value chain spans five primary stages from raw material input through end-use installation and ongoing maintenance. Belt manufacturing and compounding capture the highest value-add margins, while technical installation services and long-term maintenance contracts generate recurring revenue streams for integrated conveyor belt solution providers.

|

Stage |

Key Activities |

|

Raw Material Procurement |

Sourcing of rubber compounds, steel cord, polyester/nylon fabric, PVC/PU materials, and chemical additives for belt compounding |

|

Belt Manufacturing |

Compounding, calendering, curing, and vulcanization of rubber; weaving and embedding of reinforcement layers; assembly of final belt structure |

|

Quality Testing & Finishing |

Load testing, abrasion and fire-resistance certification, dimensional inspection, and surface finishing against ISO/DIN/ASTM standards |

|

Distribution & Sales |

Regional stocking through industrial distributors, direct project supply, and OEM channel partnerships for volume accounts |

|

Installation & Maintenance |

On-site belt installation, splicing and jointing services, tension monitoring, periodic inspection, and belt replacement by specialist field technicians |

|

End-Use Industries |

Mining and metallurgy, manufacturing, chemicals and oil & gas, aviation, logistics, food processing, and other industrial sectors |

Integrated conveyor belt manufacturers with captive rubber compounding operations and in-house quality testing and certification capabilities achieve lower material cost bases and faster new product development cycles than pure assemblers reliant on external material procurement. This vertical integration depth is a meaningful competitive advantage in both commodity and specialty belt market segments.

Technology Landscape in the Conveyor Belt Industry

Belt Construction Technology: From Textile to Steel Cord

Modern conveyor belt construction has evolved from single-ply textile to sophisticated multi-ply fabric-reinforced and steel cord-reinforced designs capable of operating at tensile ratings of up to 10,000 N/mm in ST-grade steel cord classifications across multi-kilometre overland mining installations. Steel cord belt technology enables conveyor spans of 30+ kilometres that are economically viable for remote mining operations as alternatives to truck haulage.

Material Innovation: High-Performance Rubber and Thermoplastic Compounds

Advanced rubber compound developments using EPDM, nitrile (NBR), SBR, and natural rubber blends deliver fire resistance, oil resistance, and extreme temperature performance ranging from -40°C to +200°C. Super abrasion-resistant (SAR) rubber compounds extend belt service life by 50–80% in high-abrasion ore mining environments compared to standard compound grades, fundamentally improving total cost of ownership for mine operators.

Digital Monitoring: Real-Time Belt Intelligence Platforms

Embedded sensor systems enabling real-time monitoring of belt tension, splice integrity, material loading distribution, and wear thickness progression are transforming conveyor maintenance from reactive breakdown repair to fully predictive intervention. Digital service contract models, where belt performance data generates automated maintenance scheduling and predictive replacement recommendations, are creating recurring revenue streams for technology-leading belt manufacturers.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Medium Weight Conveyor Belt | 56.9% | 2025 |

| End Use | Mining and Metallurgy | 40.9% | 2025 |

| Region | Asia Pacific | 37.1% | 2025 |

By Type

Medium-weight conveyor belt commands a 56.9% majority market share in 2025 owing to its fundamental versatility and suitability across the widest range of industrial, manufacturing, and distribution applications. The medium-weight segment serves as the backbone of global manufacturing production lines, e-commerce distribution centres, airport baggage handling systems, and food processing facilities, where its balanced load capacity and operational flexibility make it the default belt specification.

To access detailed market analysis, Request Sample

Heavy-weight conveyor belt at 26.4% in 2025 is irreplaceable in mining, quarrying, steel and cement production, and bulk material handling operations where rubber belt thickness, steel cord tensile strength, and abrasion resistance define operational safety and system reliability requirements.

Light-weight conveyor belt at 16.7% in 2025 is the fastest-growing type segment, driven by e-commerce warehouse automation and food industry belt modernization demanding hygiene-compliant and energy-efficient belt designs.

By End-Use

Mining and metallurgy lead the end-use segment at 40.9% in 2025, reflecting the fundamental reliance on heavy-duty conveyor belts for transporting ore, coal, minerals, and bulk aggregate across complex underground and open-pit mining environments. The mining industry's need for reliable, abrasion-resistant, and often fire-resistant belt grades in continuous high-throughput operations makes it the dominant and most technically demanding demand source globally.

Manufacturing at 24.6% in 2025 represents the broadest application diversity, spanning automotive assembly, electronics production, food and beverage processing, packaging, and general industrial manufacturing lines.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

37.1% |

Rapid industrialization and manufacturing expansion; growing mining and bulk material handling activity; rising logistics and e-commerce infrastructure investment |

|

Europe |

24.3% |

Industrial automation across manufacturing sectors; increasing adoption of energy-efficient belt solutions; expansion of food processing and packaging operations |

|

North America |

20.6% |

Growth in automated warehousing and distribution infrastructure; airport baggage handling system upgrades; active mining and heavy industrial operations |

|

Middle East & Africa |

9.8% |

Industrial diversification and infrastructure development programmes; expansion of mining and natural resource extraction; oil, gas, and petrochemical facility investment |

|

Latin America |

8.2% |

Growth in mining and mineral extraction activities; expanding agricultural and agro-industrial processing; increasing manufacturing investment and industrial capacity build-out |

Asia Pacific's 37.1% market dominance in 2025 is driven by China's position as the world's largest manufacturing economy, Australia's world-class iron ore and coal mining operations generating large-scale belt procurement, and rapidly industrializing ASEAN economies deploying new conveyor systems across manufacturing, food processing, and logistics facilities at an accelerating pace.

Europe's 24.3% share reflects strong demand from Germany's highly automated automotive and manufacturing sector, UK and Nordic region food processing belt requirements, and Eastern Europe's expanding manufacturing base.

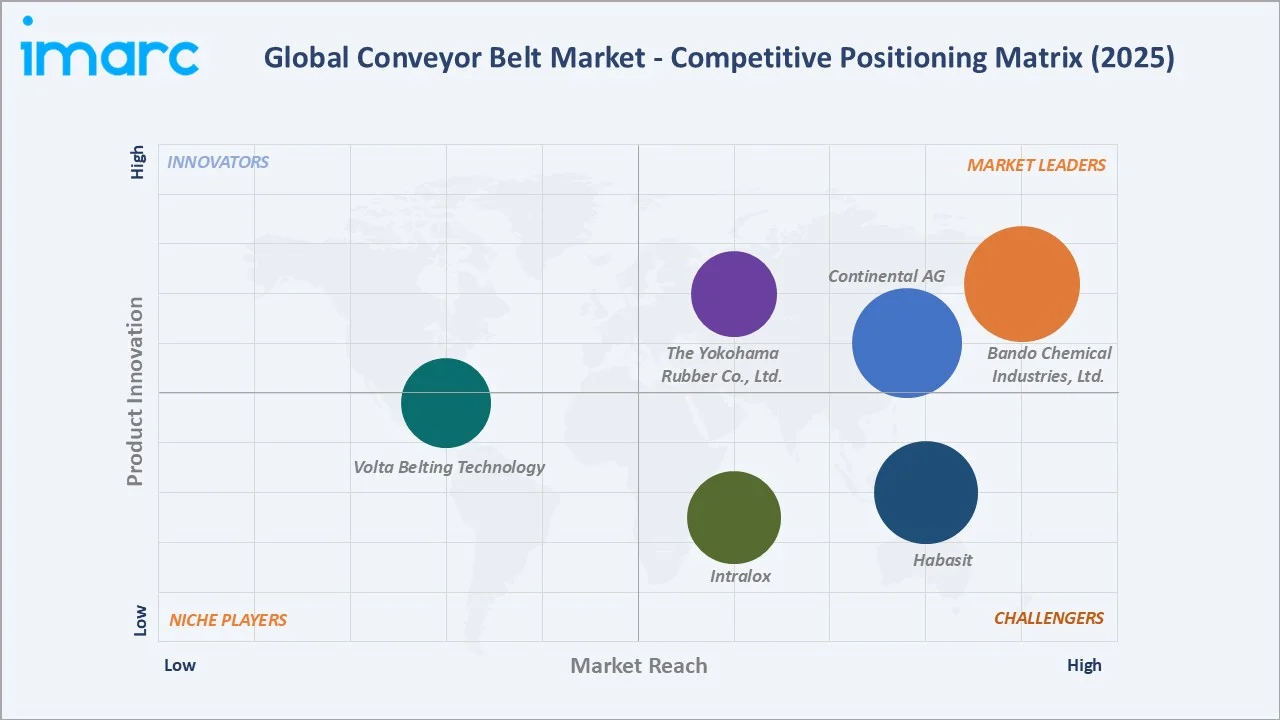

Competitive Landscape

The global conveyor belt market is moderately fragmented, with regional leaders holding strong positions in their home markets while several large global suppliers compete across multiple geographies.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

Bando Chemical Industries, Ltd. |

Conveyor belts |

Leader |

Japan & Asia; eco-friendly and energy-efficient belt innovation; broad industrial portfolio |

|

Continental AG |

Conveyor belts |

Leader |

Europe & global; smart belt systems; sustainability and digitization leadership |

|

Habasit |

Fabric -based conveyor belts |

Challenger |

Food processing, packaging, textile; service-centric model; hygiene-focused solutions |

|

Intralox |

Modular plastic conveyor belts |

Challenger |

Food processing and logistics; modular and hygienic belt solutions; direct-to-customer model |

|

Volta Belting Technology |

Thermoplastic flat belts, food-grade conveyor belts |

Emerging |

Food and pharmaceutical packaging; energy-efficient thermoplastic innovations |

|

The Yokohama Rubber Co., Ltd. |

Steel cord belts, textile conveyor belts, pipe conveyor belts |

Leader |

Asia Pacific & global; mining and heavy industry; record profitability through M&A growth |

Key players include Bando Chemical Industries, Ltd., Continental AG, Habasit, Intralox, Volta Belting Technology, The Yokohama Rubber Co., Ltd., and others.

Key Company Profiles

Bando Chemical Industries, Ltd.

Bando Chemical Industries, Ltd. is Japan's largest manufacturer of power transmission and conveyor belts, serving automotive, industrial machinery, mining, logistics, food processing, and agricultural sectors globally.

- Product Portfolio: Conveyor belts

- Recent Developments: In April 2025, Bando Chemical Industries strengthened its focus on energy-efficient power transmission solutions by expanding its flat belt drive systems, designed to improve operational efficiency and reduce environmental impact.

- Strategic Focus: The company differentiates through advanced rubber compounding, pursuing carbon neutrality by 2050, and accelerating its "Bando Dream Factory" initiative which applies AI and IoT to achieve unmanned, autonomous manufacturing operations across its global production network.

Yokohama Rubber Co., Ltd.

Yokohama Rubber Co., Ltd. is a leading Japanese manufacturer of conveyor belts and industrial rubber products, with strong market presence in Asia Pacific, particularly in Australian mining markets, and growing global distribution built through strategic acquisition investments.

- Product Portfolio: Steel cord belts, textile conveyor belts, pipe conveyor belts, and others

- Recent Developments: In April 2025. Yokohama Rubber launched a new energy-efficient, flame-retardant conveyor belt, FLAME GUARD ECO, aimed at enhancing both operational safety and energy performance in demanding industrial applications such as ports and thermal power plants.

- Strategic Focus: Yokohama's strategy leverages its Asia Pacific manufacturing cost base and premium Japanese quality credentials to build global mining and industrial belt market share, using strategic M&A activity to accelerate geographic coverage expansion beyond Japan's home market.

Market Concentration Analysis

The global conveyor belt market is moderately fragmented at the global level, reflecting significant regional concentration among national and regional leaders, with no single company estimated to hold more than 10–12% of total global market revenue. The Asia Pacific region, representing 37.1% of the market, is served by a mix of Japanese multinationals and Chinese domestic manufacturers, while European and North American markets maintain distinct competitive ecosystems with different leading players.

Consolidation is actively occurring through large industrial conglomerates and private equity firms acquiring regional belt specialists and aftermarket service providers. In July 2022, Continental AG acquired WCCO Belting, Inc. to strengthen its agricultural and specialty belt business, while Motion Industries acquired International Conveyor and Rubber to deepen its aftermarket conveyor belt service and distribution capabilities across North America.

The market is also undergoing consolidation at the distribution and service layer, with industrial distributors and MRO service companies assembling multi-brand conveyor belt stocking and field service capabilities that provide regional customers with single-source supply for a broad range of belt types and maintenance services, creating competitive pressure on manufacturer-direct sales channels.

Investment & Growth Opportunities

Fastest-Growing Segments

Light-weight conveyor belt at ~3.1% CAGR through 2034 is the highest-growth type segment, driven by the structural expansion of e-commerce warehouse automation and food processing modernization globally. Aviation at ~2.9% CAGR through 2034 represents the fastest-growing end-use segment, fuelled by rising air passenger traffic volumes and major airport infrastructure investment programmes across Asia Pacific, the Middle East, and North America.

Emerging Markets

Middle East and Africa at ~2.8% CAGR represents an emerging priority region for conveyor belt manufacturers. African copper, lithium, gold, and cobalt mining expansion driven by energy transition metal demand, combined with GCC industrial diversification mega-projects, are creating large-scale belt procurement opportunities in a region with limited domestic belt manufacturing capacity, requiring imports from global suppliers.

Venture & Investment Trends

Private equity interest in consolidating regional belt distribution, aftermarket service, and specialty belt manufacturing markets is increasing. Smart belt technology investment is accelerating, with AI-enabled monitoring, IoT sensor integration, and digital service platform development creating new recurring revenue models that structurally improve customer retention and reduce the price sensitivity that characterises commodity belt procurement in mature markets.

Future Market Outlook (2026-2034)

The global conveyor belt market is forecast to expand from USD 7.12 Billion in 2025 to USD 8.90 Billion by 2034 at a CAGR of 2.51%, adding USD 1.78 Billion in cumulative incremental annual market value over the forecast period. This consistent and sustained growth reflects the market's infrastructure-linked, operationally non-discretionary demand characteristics across all major end-use industries.

Three primary technological forces will most significantly shape the conveyor belt industry landscape through 2034. Smart belt monitoring and predictive maintenance platforms will transition from premium differentiators to standard expectations across mining and large industrial customers, compelling manufacturers to invest in digital service capabilities or risk commoditization of their belt product revenue. Eco-friendly thermoplastic and recyclable belt materials will gain growing specification share as sustainability-driven procurement requirements filter through supply chains globally.

Asia Pacific will maintain its dominant regional position through 2034, with China's manufacturing sector evolution toward higher-value industrial automation and Australia's sustained mining output sustaining large-scale demand. Middle East and Africa will exhibit above-average growth as mining infrastructure investment accelerates, while e-commerce logistics automation and food industry belt modernization will sustain steady demand across North American and European markets throughout the forecast period.

Research Methodology

Primary Research

Primary research encompassed structured interviews with conveyor belt industry stakeholders, including senior commercial managers at belt manufacturers, mining procurement specialists, materials handling engineers, aviation infrastructure specialists, and industrial distribution professionals across key geographies. Primary data validated market sizing estimates, type and end-use segment shares, regional demand estimates, key player positioning, and technology adoption timelines across the global conveyor belt industry.

Secondary Research

Key secondary sources include World Mining Congress output data, IEA World Energy Investment Report (2024), GWEC Global Wind Report (2024), industry trade publications including Bulk Solids Handling, Mining Magazine, Materials Handling and Logistics, and company annual reports and investor presentations from Bridgestone, Continental AG, Michelin Group (Fenner), and Yokohama Rubber Co., Ltd. Standards bodies including ISO, DIN, and ASTM provided product specification and classification frameworks.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, industrial production indices, mining capital expenditure cycles, logistics infrastructure investment data, and historical market evolution patterns. Scenario analysis including base, optimistic, and conservative cases was performed to account for macroeconomic and commodity price uncertainty throughout the 2026–2034 forecast horizon.

Conveyor Belt Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Medium-Weight Conveyor Belt, Light-Weight Conveyor Belt, Heavy-Weight Conveyor Belt |

| End-Uses Covered | Mining and Metallurgy, Manufacturing, Chemicals, Oils and Gases, Aviation, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Bando Chemical Industries, Ltd., Continental AG, Habasit, Intralox, Volta Belting Technology, The Yokohama Rubber Co., Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the conveyor belt market from 2020-2034.

- The conveyor belt market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the conveyor belt industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Conveyor Belt Market Report

The global conveyor belt market reached USD 7.12 Billion in 2025, reflecting consistent demand growth from industrial automation investment, expanding mining operations, e-commerce logistics infrastructure build-out, and growing aviation baggage handling system deployment globally.

The market is projected to reach USD 8.90 Billion by 2034, growing at a CAGR of 2.51% during 2026-2034, driven by sustained industrial automation expansion, mining capital investment cycles, e-commerce logistics growth, and technology adoption of smart conveyor belt monitoring systems across major end-use industries.

Medium-weight conveyor belt leads the type segment with a 56.9% share in 2025, valued for its unmatched versatility across manufacturing, distribution, aviation, and general industrial applications. Its capacity to handle a broad range of materials and load requirements while offering energy efficiency and operational flexibility makes it the dominant specification globally.

Mining and metallurgy lead the end-use segment with a 40.9% share in 2025, driven by the critical dependence of global mining operations on heavy-duty conveyor belt systems for the safe and efficient transport of ore, coal, and bulk minerals across long-distance underground and surface mining environments.

Asia Pacific commands a leading 37.1% market share in 2025, driven by China's position as the world's largest manufacturing economy, Australia's extensive iron ore and coal mining belt requirements, and rapidly growing ASEAN manufacturing and distribution sectors deploying new conveyor infrastructure at scale.

Light-weight conveyor belt is the fastest-growing type segment at ~3.1% CAGR through 2034, driven by the structural expansion of e-commerce warehouse automation globally, growing food and beverage processing modernization requiring hygienic belt solutions, and pharmaceutical manufacturing adoption of modular and thermoplastic belt constructions.

Leading companies include Bando Chemical Industries, Ltd., Continental AG, Habasit, Intralox, Volta Belting Technology, The Yokohama Rubber Co., Ltd., and others.

Key applications include ore and mineral transport in underground and open-pit mining, automotive and electronics manufacturing assembly lines, airport baggage handling systems, e-commerce distribution centre sortation, food and beverage processing lines, pharmaceutical manufacturing, bulk cement and aggregate transport in construction, and chemical plant material handling across a wide range of industries globally.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)