Core Banking Software Market Report by Solution (Deposits, Loans, Enterprise Customer Solutions, and Others), Service (Professional Service, Managed Service), Deployment (Cloud-based, On-premise), End Use (Banks, Financial Institutions, and Others), and Region 2026-2034

Core Banking Software Market Overview:

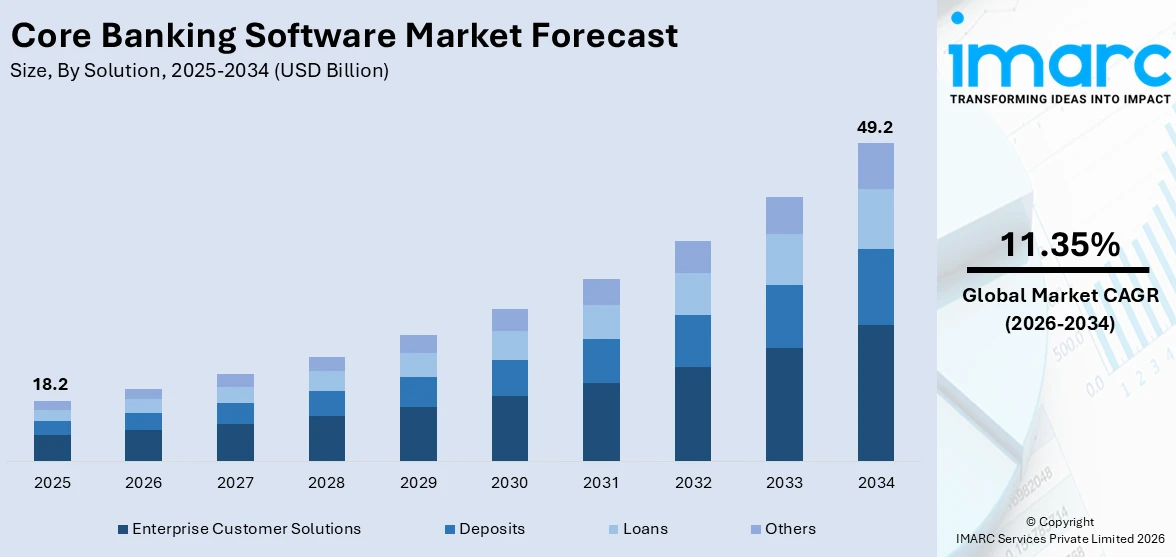

The global core banking software market size reached USD 18.2 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 49.2 Billion by 2034, exhibiting a growth rate (CAGR) of 11.35% during 2026-2034. The increasing digital transformation, the implementation of government regulations, growing need for cost-efficiency, rising fintech services, widespread consumers preference for digital solutions, and the increasing focus on small and medium-sized enterprises (SMEs) are some of the major factors propelling the market.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 18.2 Billion |

|

Market Forecast in 2034

|

USD 49.2 Billion |

| Market Growth Rate 2026-2034 | 11.35% |

Core banking software refers to a centralized system that enables a bank to offer services across all its branches in an integrated manner. It includes retail banking, loan management, and enterprise customer solutions. Core banking software finds applications in account management, real-time transaction processing, customer relationship management, loan origination and management, fraud detection, compliance tracking, financial analytics, mobile and online banking interfaces, and international money transfers. It offers numerous benefits, including improved efficiency, better customer service, enhanced data analysis capabilities, increased scalability, easier compliance with regulations, and better risk management.

To get more information on this market Request Sample

The emergence of fintech companies offering highly efficient and user-friendly financial services is one of the major factors fueling the market growth. Moreover, the increasing consumer preference for online transactions and digital banking services, necessitating the adoption of sophisticated software solutions, is strengthening the market growth. Besides this, the growing need for modern banking solutions that involve various services and applications working in synergy is positively impacting the market growth. In addition to this, the increasing focus of financial institutions on small and medium enterprises (SMEs), requiring a different set of banking solutions that are tailored to meet their unique needs, is stimulating the market growth. Apart from this, the rising demand for advanced analytics and data-driven decision-making, facilitating software adoption, is providing a thrust to the market growth.

Core Banking Software Market Trends/Drivers:

Increasing digital transformation in the banking sector

The sudden shift towards digital transformation in the banking sector is one of the major factors providing a thrust to the market growth. Furthermore, the increasing consumer demand for widespread access to financial information, seamless transaction capabilities, and a user-friendly interface is positively impacting the market growth. In line with this, core banking software enables banks to manage deposits, loans, transactions, and customer data on a unified platform. Besides this, the rising need to modernize the architecture of the banking system and meet the growing demand of the digitally equipped customer base is propelling the market growth. Apart from this, the integration of advanced analytics modules within the software to provide insight into customer behavior and transaction patterns is acting as a growth-inducing factor.

Implementation of complex government regulations

The implementation of complex regulations by the government, prompting financial institutions to adhere to various rules and standards, is stimulating the market growth. In line with this, the introduction of anti-money laundering (AML) laws and data protection regulations encouraging banks to adopt core banking software is creating a positive outlook for the market. Besides this, the failure to meet regulatory standards and non-compliance, leading to fines and penalties, is strengthening the market growth. In confluence with this, the widespread software adoption to simplify the compliance process by integrating features that assist in reporting, data management, and transaction tracking is acting as a growth-inducing factor. Moreover, the growing capabilities of the software to provide financial officers with the necessary information during an audit are anticipated to drive the market growth.

Increasing need for cost-efficiency

The increasing need for cost-efficiency in the banking sector is providing an impetus to the market growth. In line with this, core banking software aids in achieving cost-effectiveness by automating numerous labor-intensive processes like data entry, transaction authentication, and customer service operations. In addition to this, the rising software application to reduce manual intervention, minimize errors, and optimize speed is favoring the market growth. Furthermore, the growing automation of routine processes, enabling employees to focus on complex tasks, thereby adding value to the organization, is acting as a growth-inducing factor. Additionally, the centralized nature of core banking software that implements updates and new feature rollouts across all branches simultaneously, reducing the need for individual training sessions or separate information technology (IT) maintenance efforts, is providing a considerable boost to the market growth.

Core Banking Software Market Opportunities:

Growing Adoption of Cloud Based and API driven Platforms

A key opportunity in the core banking software market is in the increasing uptake of cloud and API-enabled platforms. Banks are shifting away from legacy systems to adopt flexible, scalable solutions that facilitate fast innovation and seamless integration with fintech ecosystems. Cloud-based core banking enables financial institutions to lower infrastructure costs, speed up product launches, and provide personalized digital experiences to customers. The emergence of open banking structures further increases this possibility, with banks now compelled to make data securely available over APIs, providing scope for new business opportunities and partnerships with third-party service providers. The growing needs of real-time payments and data analytics also provide scope for the integration of AI and machine learning, making decision-making more efficient and improving customer insights. This transformation to newer, cloud-native platforms puts core banking providers in a position to take on substantial growth in the changing financial environment.

Core Banking Software Market Challenges:

Complexity of Migrating from Legacy System to Impede the Market Growth

One of the most important challenges facing the core banking software market is legacy system migration complexity. Most financial institutions are still operating on infrastructure that is decades old, hence migration to newer platforms is expensive, time-consuming, and risky. The replacement of core systems entails massive re-engineering of business processes, data migration complications, and possible disruptions in customer services. Additionally, regulatory strictures create an added level of complexity since banks will need to adhere to data protection, cybersecurity, and reporting standards amid the transition. Organizational resistance to change, along with the lack of skilled IT personnel, adds to the difficulty of adoption. Upfront expenses that are prohibitive in nature may also discourage small banks from engaging in sweeping upgrades. Therefore, institutions tend to procrastinate modernization, decelerating innovation and exposing them to the threats of competition from nimble digital-only banks and fintech companies that provide faster, more streamlined services.

Core Banking Software Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on solution, service, deployment, and end user.

Breakup by Solution:

- Deposits

- Loans

- Enterprise Customer Solutions

- Others

Enterprise customer solutions dominates the market

The report has provided a detailed breakup and analysis of the market based on the solution. This includes deposits, loans, enterprise customer solutions, and others. According to the report, enterprise customer solutions represented the largest segment.

Enterprise customer solutions are dominating the market share as large enterprises require a diverse range of financial services, including complex loans, multiple types of deposits, international transactions, and treasury services. In addition to this, they offer modules for different financial products and services, providing the flexibility to cater to specific enterprise needs. Moreover, they provide advanced capabilities, such as real-time analytics, custom reporting, and compliance management tools, which are indispensable for large corporations. Besides this, enterprise customer solutions incorporate sophisticated customer relationship management (CRM) devices designed to enhance customer engagement, deepen relationships, and ultimately improve customer loyalty and retention. Furthermore, they are scalable, allowing financial institutions to expand their offerings as they grow, making it a long-term investment. Besides this, the convenient integration of enterprise customer solutions with other systems like enterprise resource planning (ERP), further streamlining operations and data flow, is driving the market growth.

Breakup by Service:

- Professional Service

- Managed Service

Professional service dominates the market

The report has provided a detailed breakup and analysis of the market based on the service. This includes professional service and managed service. According to the report, professional service represented the largest segment.

Professional services hold the largest market share as the utilization of core banking software requires specialized expertise. In line with this, they help banks assess their specific needs and customize the software, ensuring seamless integration with existing systems. Moreover, professional services include regulatory compliance assistance, ensuring that the software is updated with the latest regulations, mitigating risk and maintaining the institution’s credibility and legal standing. In addition to this, they include initial training and ongoing training of financial experts, ensuring that the bank is fully equipped to leverage the software to its fullest potential. Besides this, the service includes analytics and data interpretation services, helping banks to make data-driven decisions and understand customer behavior. Furthermore, professional service solutions are designed to be scalable to meet the changing needs of the institution, such as expanding to new geographical locations, complying with new regulations, or offering new services.

Breakup by Deployment:

- Cloud-based

- On-premise

On-premise dominates the market

The report has provided a detailed breakup and analysis of the market based on the deployment. This includes cloud-based and on-premise. According to the report, on-premise represented the largest segment.

On-premise solutions dominate the market share as control over data is a primary concern for financial institutions. They provide banks with full control over their data, allowing for the customization of security measures to suit specific organizational needs. Moreover, the increasing preference for performance considerations as on-premise offers faster data retrieval and transaction processing is favoring the market growth. In addition to this, many financial institutions invest in on-premise hardware and software due to its smooth integration with the legacy systems of the financial institutions. Besides this, the widespread customization capabilities of on-premise solutions are providing a thrust to the market growth. Additionally, the establishment of some financial institutions in regions with less reliable internet connectivity, making cloud-based solutions less feasible, is positively impacting the market growth.

Breakup by End Use:

Access the comprehensive market breakdown Request Sample

- Banks

- Financial Institutions

- Others

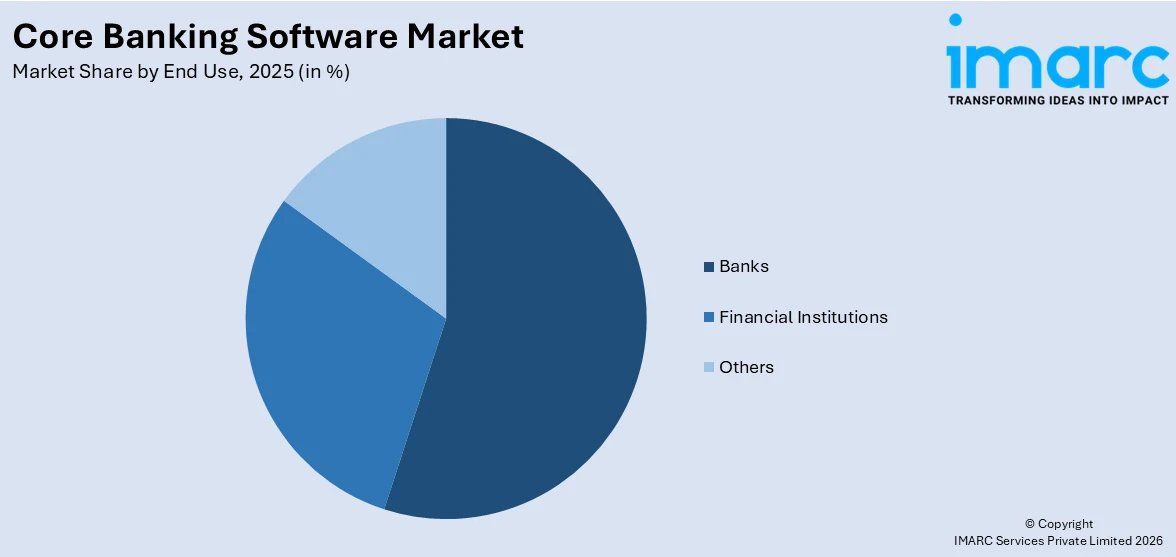

Banks dominate the market

The report has provided a detailed breakup and analysis of the market based on the end use. This includes banks, financial institutions, and others. According to the report, banks represented the largest segment.

Banks dominate the market as they handle an enormous volume of complex transactions involving multiple currencies, regulatory frameworks, and financial products. Core banking software enables these institutions to manage such complexities at scale efficiently. Moreover, the software is designed to assist banks in complying with stringent regulatory requirements by maintaining meticulous records and implementing robust security measures. Besides this, traditional banks serve a large and diverse customer base, offering a wide range of financial services, thus prompting software adoption to meet the varied needs of extensive clientele. In addition to this, core banking software provides banks with the ability to modernize their infrastructure, thereby driving the market growth. Furthermore, it allows for innovations like personalized banking experiences, rapid product launches, and real-time analytics, offering banks a competitive edge.

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Key Regional Takeaways:

United States Core Banking Software Market Analysis

The United States core banking software market is witnessing consistent growth through the digitalization of financial institutions, the uptake of cloud-based solutions, and the demand for improved customer experience. Large banks are making huge investments in transforming legacy systems to enhance operation efficiency, regulatory compliance, and data security. The availability of front-runners in technology provision and fintech partnerships accelerates innovation further by supporting features such as real-time payment, AI analytics, and bespoke banking. Furthermore, the U.S. regulatory environment, prioritizing cybersecurity and customer data protection, is shaping software enhancement. Increasing competition from digital banks is forcing incumbent institutions to adopt agile, scalable platforms supporting omnichannel banking. With heavy investments in research and development as well as the need for integration without impediments from third-party applications, the U.S. market is likely to continue its momentum. Further, with the evolution of open banking architectures, vendors are being compelled to provide more adaptable and API-based core banking solutions.

Europe Core Banking Software Market Analysis

In Europe the market is driven by changing regulatory expectations, cross-border banking requirements, and a massive emphasis on digital transformation. European banks are making proactive investments in modernizing core banking in order to improve client interaction, upgrade payment systems, and comply with PSD2 requirements. Cloud-based as well as SaaS models are picking pace with cost benefits and quicker deployment. Furthermore, the area is also seeing more cooperation between traditional banks and fintech companies in providing customer-centric, data-led banking solutions. The UK, Germany, and France are among the countries at the forefront of implementing open banking systems, driving the need for agile and API-based systems. The quest for green banking and the imperative to enhance operational resilience are also driving investments in next-generation core banking platforms in Europe.

Asia Pacific Core Banking Software Market Analysis

The Asia Pacific core banking software market is growing strongly, fueled by fintech ecosystem promotion by governments, increased adoption of digital banking, and efforts to increase financial inclusion. With an emphasis on cloud-based and mobile-first systems, China, India, and Singapore are leading the way in implementing next-generation core banking technologies. The high demand for innovative digital services from increasingly technology-literate customers and the growing number of digital-only banks in the region are accelerating financial institutions' deployment of scalable and cost-effective solutions. Further driving market expansion are legislative changes that encourage innovation and advancements in cybersecurity.

Latin America Core Banking Software Market Analysis

Latin America core banking software market is expanding as banks see digital transformation as a key priority to respond to changing customers' needs and make banking more accessible. Brazil and Mexico are leading countries investing in cloud-based systems to enable quicker transactions and offer better mobile banking solutions. The push for financial inclusion and the growth of digital wallets are fueling demand for new-generation, scalable platforms. Partnerships with fintech firms are also contributing towards enhancing capabilities to operate in the region.

Middle East and Africa Core Banking Software Market Analysis

Middle East and Africa core banking software market is witnessing steady growth with upgradation of the banking infrastructure and growing digital banking services. Governments in the Gulf region are investing heavily in smart banking efforts, whereas African nations are opting for mobile-first platforms to advance financial inclusion. Bank and fintech provider collaboration is influencing innovation, creating ease of payment solutions and improved customer experiences. Implementation of cloud-based platforms is gaining traction, helping banks boost efficiency and scalability.

Competitive Landscape:

The leading companies in the core banking software market are investing heavily in research and development (R&D) to introduce innovative features and functionalities, such as enhanced security measures, real-time analytics, and artificial intelligence (AI) capabilities to make banking operations more efficient and customer-centric. Moreover, they are actively engaging in mergers and acquisitions to integrate new technologies and expertise into their existing solutions. Furthermore, many companies are partnering with other technology providers or financial institutions to deliver more comprehensive and seamless solutions that address specific market needs or regulatory requirements. Along with this, the major players are increasing their focus on customer service and engagement strategies, including the rollout of self-service portals, educational webinars, and customer support. In addition to this, financial institutions are updating their software to ensure compliance with new financial regulations and standards.

The market research report has provided a comprehensive analysis of the competitive landscape. Detailed profiles of all major companies have also been provided. Some of the key players in the market include:

- Capgemini

- Fidelity Information Services Inc.

- Finastra

- Fiserv Inc.

- HCL Technologies Limited

- Infosys Limited

- Jack Henry & Associates Inc.

- Oracle Corporation

- SAP SE

- Tata Consultancy Services Limited

- Temenos AG

- Unisys Corporation

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

Latest News and Developments:

- In February 2025- Fusion Bank successfully migrated to a next-generation core banking system in just 10 months with Tencent Cloud’s support and WeBank’s digital banking technology. The upgrade integrated over 150 subsystems across key banking areas, reducing costs by 40% and cutting recovery time to 30 minutes. This transformation enhances agility, operational efficiency, and customer experience, setting a new benchmark for Hong Kong’s banking sector.

- In May 2025- Temenos introduced the Product Manager Copilot, a Generative AI tool integrated with Microsoft Azure OpenAI Service, at the Temenos Community Forum ’25. Embedded in Temenos’ retail core banking solution, it enables banks to design, test, and launch financial products faster using conversational AI. Trusted by 950+ banks globally, Temenos aims to enhance product innovation, insights, and operational efficiency through this next-gen AI-powered solution.

- In May 2025- Tietoevry Banking signed a strategic five-year agreement with Lokalbank, a collaboration of 16 banks serving 250,000 customers, to deliver a comprehensive, secure, and compliant banking platform. The solution includes core banking, digital banking, payments, cards, and anti-financial crime tools. This partnership streamlines operations, enhances customer experience, and strengthens Lokalbank’s competitive position, supporting growth within the Frende Group network and fostering future-ready digital banking services.

Core Banking Software Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Solutions Coverage | Deposits, Loans, Enterprise Customer Solutions, Others |

| Services Coverage | Professional Service, Managed Service |

| Deployments Coverage | Cloud-based, On-premise |

| End Uses Coverage | Banks, Financial Institutions, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | Capgemini, Fidelity Information Services Inc., Finastra, Fiserv Inc., HCL Technologies Limited, Infosys Limited, Jack Henry & Associates Inc., Oracle Corporation, SAP SE, Tata Consultancy Services Limited, Temenos AG, Unisys Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the global core banking software market performed so far, and how will it perform in the coming years?

- What are the drivers, restraints, and opportunities in the global core banking software market?

- What is the impact of each driver, restraint, and opportunity on the global core banking software market?

- What are the key regional markets?

- Which countries represent the most attractive core banking software market?

- What is the breakup of the market based on the solution?

- Which is the most attractive solution in the core banking software market?

- What is the breakup of the market based on the service?

- Which is the most attractive service in the core banking software market?

- What is the breakup of the market based on the deployment?

- Which is the most attractive deployment in the core banking software market?

- What is the breakup of the market based on the end use?

- Which is the most attractive end use in the core banking software market?

- What is the competitive structure of the global core banking software market?

- Who are the key players/companies in the global core banking software market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the core banking software market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global core banking software market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the core banking software industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)