Corporate Wellness Market Size, Share, Trends and Forecast by Service, Category, Delivery, Organization Size, and Region, 2026-2034

Global Corporate Wellness Market Size, Share, Trends & Forecast (2026-2034)

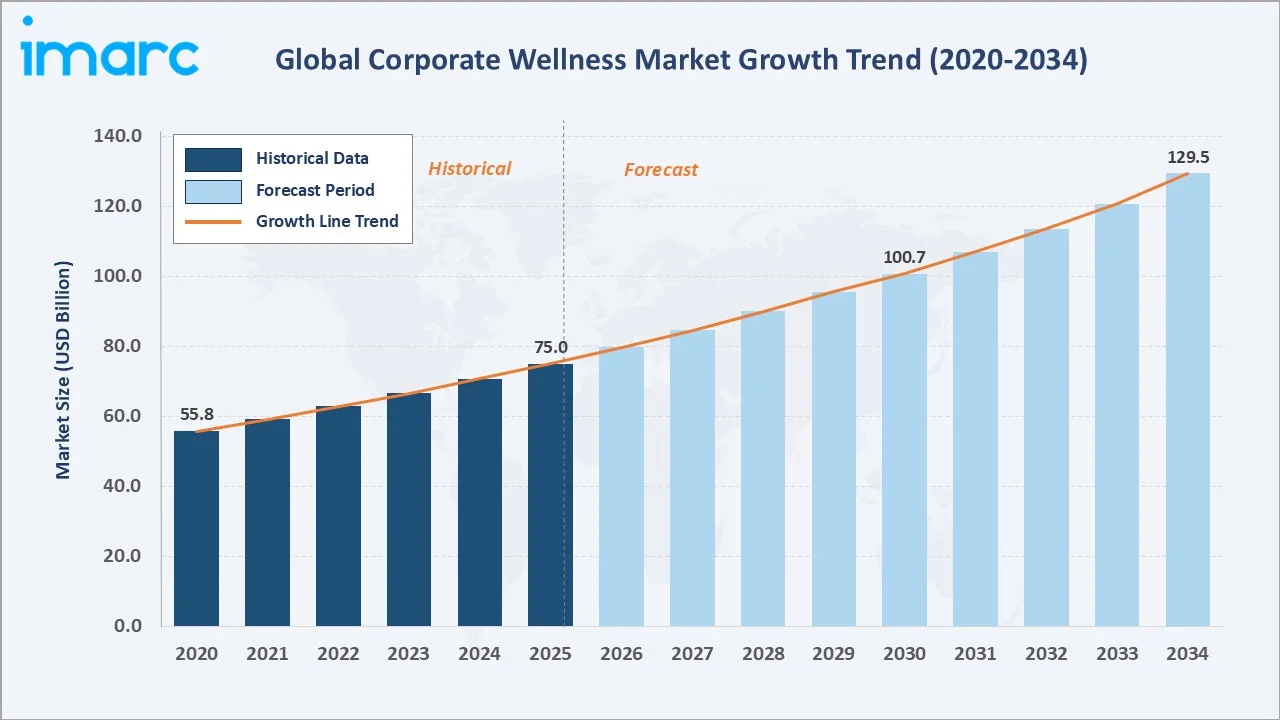

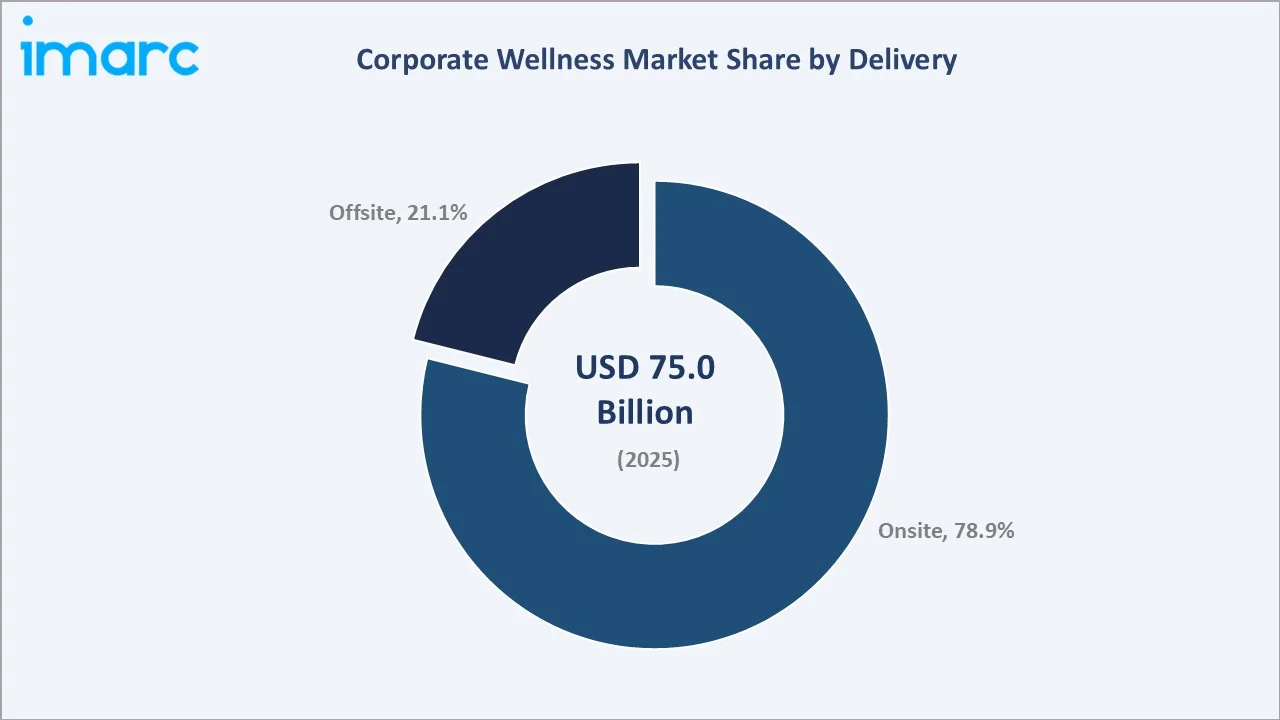

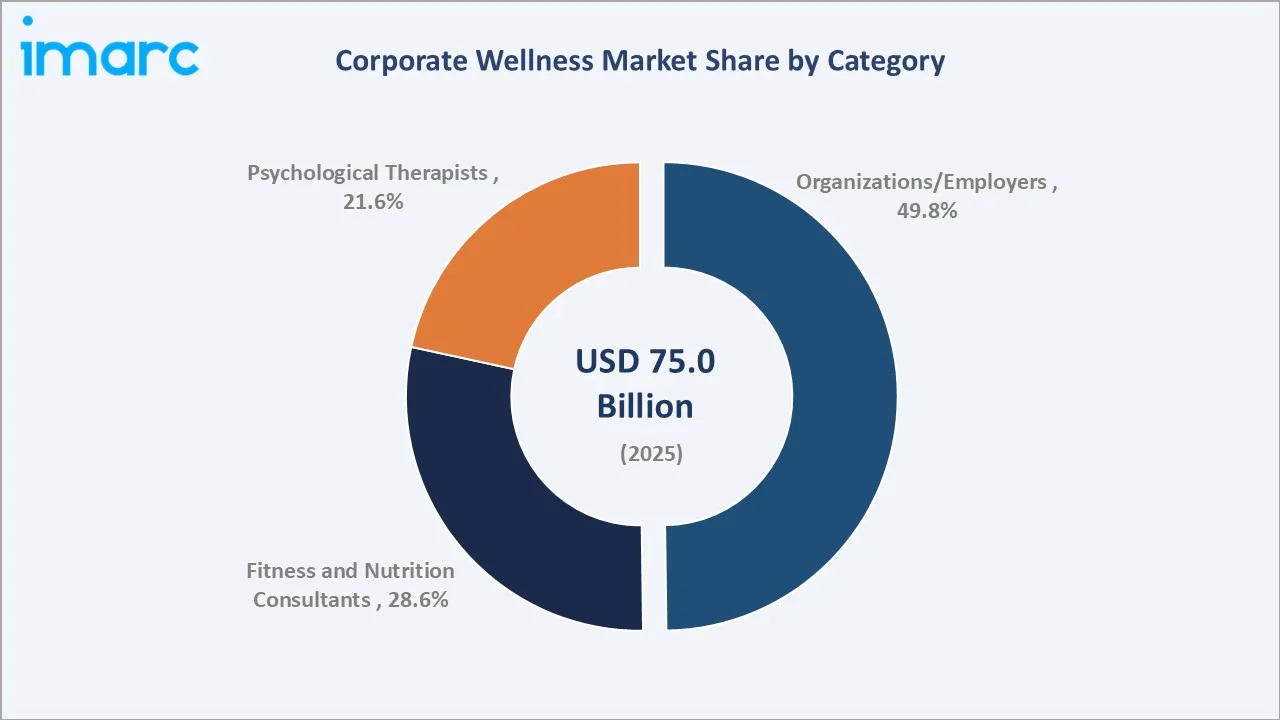

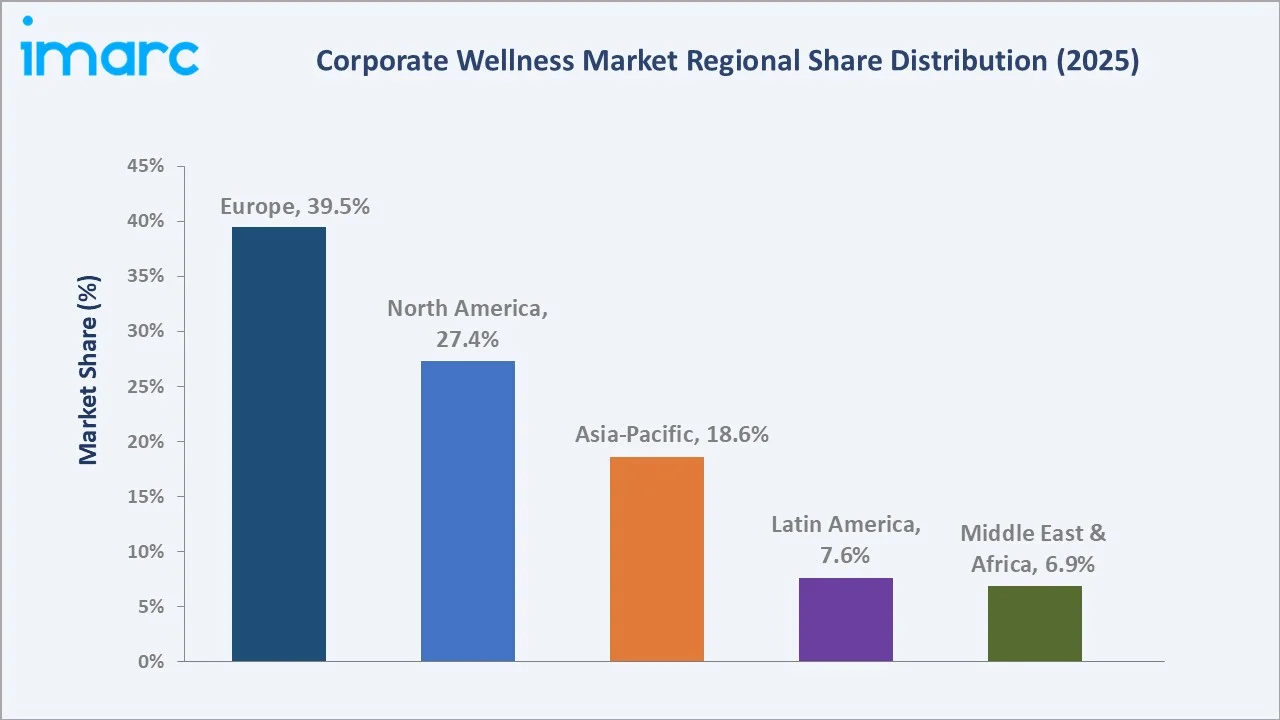

The global corporate wellness market size was valued at USD 75.0 Billion in 2025 and is projected to reach USD 129.5 Billion by 2034, exhibiting a CAGR of 6.07% during the forecast period 2026-2034. Growth is driven by rising employer focus on mental health, increasing healthcare costs, and regulatory pressure around wellness disclosures. Onsite delivery leads at 78.9% in 2025, while Organizations/Employers dominate the category segment at 49.8%. Europe accounts for 39.5% of global revenue in 2025, the world's largest regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 75.0 Billion |

|

Forecast Market Size (2034) |

USD 129.5 Billion |

|

CAGR (2026-2034) |

6.07% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Europe (39.5% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific (CAGR ~8.2%) |

|

Leading Delivery |

Onsite (78.9%, 2025) |

|

Leading Category |

Organizations/Employers (49.8%, 2025) |

The global corporate wellness market growth trajectory from 2020 through 2034, contrasting a consistent historical expansion base against a sustained forecast curve powered by digital health platform adoption, employer-mandated preventive care programs, and the global mental health awareness movement, is gaining regulatory momentum.

To get more information on this market, Request Sample

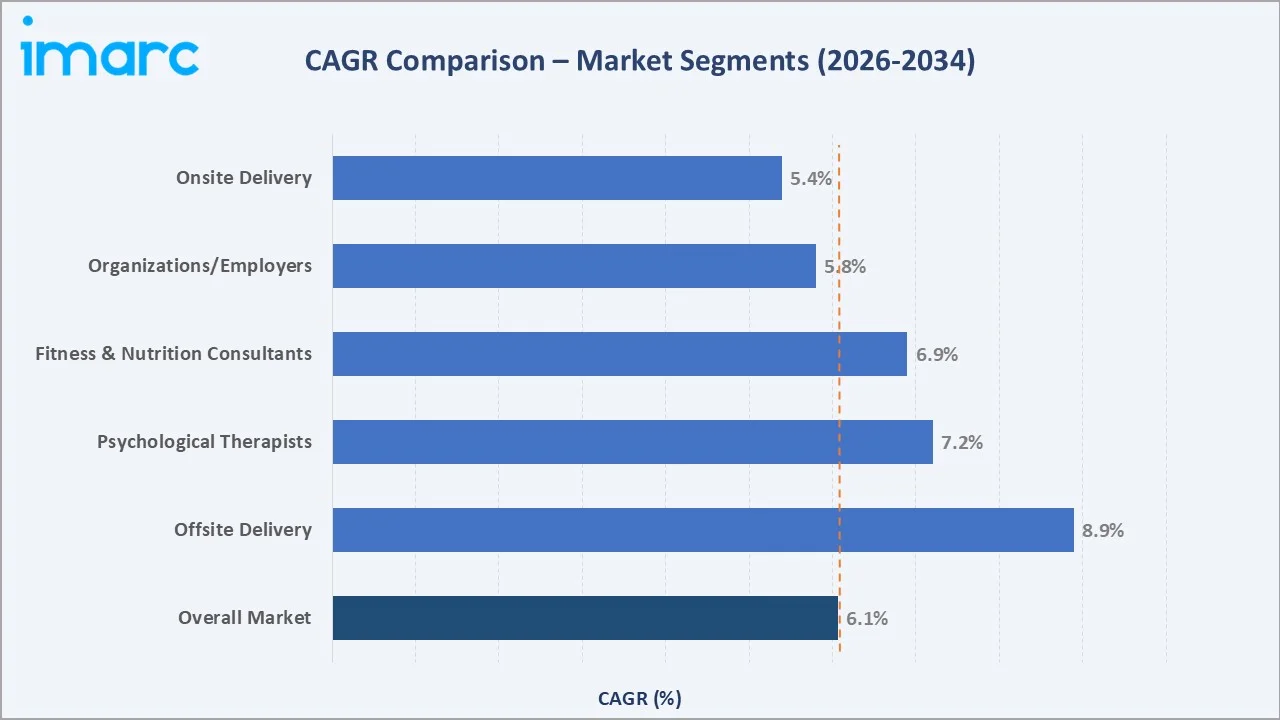

Segment-level CAGR comparisons highlighting offsite delivery and psychological therapists as the two fastest-growing sub-categories within the global corporate wellness industry analysis through 2034, as remote work paradigms and mental health priorities reshape employer wellness investment patterns.

Executive Summary

The global corporate wellness market is undergoing a structural transformation driven by converging forces of rising workforce mental health challenges, escalating employer healthcare expenditures, and regulatory frameworks mandating employee well-being investments. Valued at USD 75.0 Billion in 2025, the market is forecast to reach USD 129.5 Billion by 2034 at a CAGR of 6.07%. The World Health Organization estimates depression, and anxiety cost the global economy approximately USD 1 trillion per year in lost productivity, compelling enterprises to allocate material budgets toward preventive wellness programs rather than reactive healthcare interventions.

Onsite delivery commands 78.9% of the market in 2025, sustained by large enterprise adoption of integrated wellness centers, on-premises fitness facilities, and in-house employee assistance programs (EAPs). However, offsite delivery is the structurally faster-growing mode at an estimated CAGR of 8.9%, fuelled by the remote-first and hybrid workplace transformation accelerated by post-pandemic work model normalization. Organizations/Employers represent 49.8% of the total market share, reflecting corporations' expanding role as direct wellness program administrators driven by cost control and data ownership imperatives.

Europe leads with 39.5% global revenue share in 2025, supported by comprehensive occupational health legislation and high corporate ESG commitments. North America follows at 27.4%, characterized by cost-driven employer wellness investment linked to healthcare premium reduction incentives. Asia-Pacific at 18.6% represents the fastest-growing region as multinational corporations expand wellness programs across APAC operations and domestic enterprises address escalating workplace stress metrics.

Key Market Insights

|

Insight |

Data |

|

Largest Delivery |

Onsite – 78.9% share 2025 |

|

Largest Category |

Organizations/Employers – 49.8% share 2025 |

|

Leading Region |

Europe – 39.5% revenue share 2025 |

|

Second Largest Region |

North America – 27.4% revenue share 2025 |

|

Top Companies |

ComPsych, Optum, Gympass/Wellhub, Vitality Group, Cigna |

|

Market Opportunity |

AI-personalized digital wellness platforms & SME adoption |

Key Analytical Observations Supporting The Above Data:

- Onsite Delivery's 78.9% dominance in 2025 reflects large enterprises' preference for integrated on-campus wellness centers, subsidized fitness facilities, and in-house EAPs that provide measurable engagement and utilization data.

- Organizations/Employers leading at 49.8% reflects corporations' increasing role as direct wellness program administrators rather than passive health insurance purchasers, investing in employee health as a strategic business performance lever.

- Europe's 39.5% regional dominance is underpinned by comprehensive EU occupational health legislation, including Germany's occupational health and safety regulations and France's obligations de sécurité mandates, which create structural employer wellness investment requirements.

- Psychological Therapists growing at ~7.2% CAGR – burnout rates exceeding 40% in several European nations per Eurofound data are driving sustained demand for certified psychological wellness services embedded directly in corporate programs.

- Fitness & Nutrition Consultants at 28.6% benefit from biometric screening mandates embedded in health insurance plan designs, corporate fitness challenge programs, and nutrition counselling tied to health insurance premium reductions.

- Asia-Pacific fastest-growing at ~8.2% CAGR driven by multinational corporations extending global wellness standards into APAC operations and domestic Indian, Chinese, and Southeast Asian enterprises scaling formal employee welfare programs.

Global Corporate Wellness Market Overview

The corporate wellness market comprises programs aimed at improving employee health, productivity, and engagement. Core offerings include physical fitness, mental health support, nutrition counselling, smoking cessation, chronic disease management, and financial wellness.

Adoption spans industries such as financial services, technology, manufacturing, and healthcare, with large enterprises deploying enterprise-wide, digital-first wellness platforms across global workforces. The ecosystem includes wellness platforms, insurers, consultants, fitness providers, digital health apps, and HR teams acting as key orchestrators.

Market growth is driven by strong economic rationale: Harvard Business Review estimates a ~$3.27 reduction in healthcare costs for every $1 invested in wellness programs. Rising absenteeism, talent retention pressures, and ESG mandates are further positioning corporate wellness as a strategic, non-discretionary investment.

Market Dynamics

To evaluate market opportunities, Request Sample

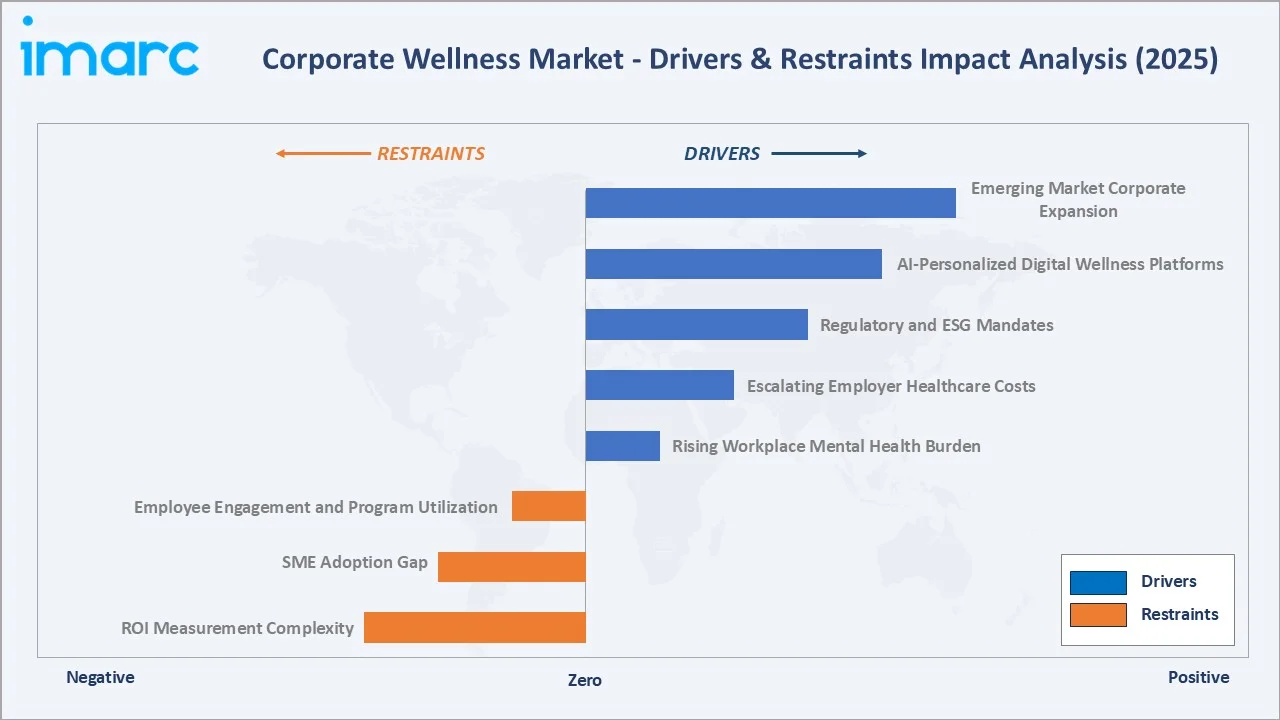

Market Drivers

- Rising Workplace Mental Health Burden: The WHO estimates 15% of working-age adults globally experience a mental disorder, costing USD 1 trillion annually in lost productivity. Enterprises invest in EAPs, counselling services, and stress management programs to mitigate absenteeism and presenteeism.

- Escalating Employer Healthcare Costs: U.S. employer-sponsored healthcare premiums exceeded USD 23,968 per family in 2023 (Kaiser Family Foundation). Preventive wellness programs demonstrably reduce downstream healthcare utilization, creating direct financial incentive for investment.

- Regulatory and ESG Mandates: The EU's Corporate Sustainability Reporting Directive (CSRD), effective 2024, requires large enterprises to disclose employee health and well-being metrics, institutionalizing wellness program investment across European corporate operations.

Market Restraints

- ROI Measurement Complexity: Despite documented aggregate wellness ROI, individual program attribution remains methodologically challenging, limiting CFO-level budget expansion decisions in cost-sensitive business environments.

- SME Adoption Gap: Small and medium enterprises, representing 90%+ of global businesses, face structural budget constraints that limit wellness program adoption, constraining market penetration beyond large enterprise clients.

Market Opportunities

- AI-Personalized Digital Wellness Platforms: Generative AI enables hyper-personalized coaching at scale, analysing biometric data, behavioural patterns, and health risk factors to deliver individualized intervention recommendations cost-effectively at enterprise scale.

- Emerging Market Corporate Expansion: Rapid corporate formalization in Southeast Asia, India, and Latin America is creating structurally new wellness program demand, with multinational employers extending global wellness standards into high-growth emerging markets.

Market Challenges

- Employee Engagement and Program Utilization: Industry data shows 60-70% of eligible employees do not actively participate in corporate wellness programs, limiting ROI and hampering employer budget justification for expanded wellness spending.

- Vendor Fragmentation and Integration Complexity: The highly fragmented wellness vendor landscape, with thousands of point solutions, creates data harmonization and benefits administration complexity for employers seeking integrated wellness ecosystems.

Emerging Market Trends

1. Digital-First Wellness Ecosystem Integration

Corporate wellness programs are migrating from siloed, in-person services toward integrated digital platforms consolidating mental health apps, fitness tracking, nutrition coaching, and biometric monitoring into unified employer-facing dashboards. Vendors such as Virgin Pulse and Gympass/Wellhub are expanding platform aggregation models, connecting employees to thousands of fitness and wellness partners globally through a single digital interface.

2. Mental Health Parity and Psychological Wellness Mainstreaming

Employer mental health investment has escalated from an ancillary EAP benefit to a core wellness pillar. Fortune 500 companies are embedding licensed therapists directly into workplace wellness programs. The global mental health app market, growing at a significant CAGR, is being partially funded through employer wellness budgets as digital mental health tools achieve clinical parity recognition from major insurers.

3. Financial Wellness as the Fourth Pillar

Financial stress is identified as the leading driver of workplace distraction, with 65% of employees reporting that financial concerns affect work performance. Employer-sponsored financial counselling, student debt assistance, and emergency savings programs are expanding the wellness market's total addressable value significantly beyond traditional physical and mental health program categories.

4. Wearable Technology and Biometric Data Integration

Enterprise wearable adoption programs providing subsidized fitness trackers to employees generate continuous biometric data streams, enabling population-level health risk stratification and targeted intervention. Major insurers, including UnitedHealth Group and Aetna, offer premium reduction incentives tied directly to wearable engagement metrics.

5. Outcomes-Based Contracting and ROI Accountability

Progressive employers are shifting from fee-for-service to outcomes-based wellness vendor contracts where pricing is linked to measurable healthcare cost reduction, absenteeism improvement, and productivity metrics. Vendors with analytics capabilities demonstrating clinical and financial outcome evidence are commanding premium contract structures and higher renewal rates.

Industry Value Chain Analysis

The corporate wellness value chain spans five integrated stages from health research and assessment through outcome measurement and reporting. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements.

|

Stage |

Key Players / Examples |

|

Health Research & Assessment |

Johns Hopkins Health System, RAND Corporation, Mercer, Willis Towers Watson |

|

Program Design & Technology |

Optum Health, ComPsych, Vitality Group, Virgin Pulse, Limeade, Gympass/Wellhub |

|

Service Delivery |

Equinox, Lifetime Fitness, nutrition consultants, psychologists, and telehealth EAP providers |

|

Employer HR Integration |

Workday, SAP SuccessFactors, benefits brokers, health insurance carriers (Cigna, Aetna) |

|

Outcome Measurement |

Health analytics platforms, biometric screening companies, and productivity measurement tools |

Program design and technology vendors occupy the highest strategic value position in the corporate wellness value chain, integrating assessment tools, digital engagement platforms, and analytics into turnkey employer solutions. However, direct-to-employer digital platforms are disrupting traditional broker-mediated distribution channels, compressing distribution margins and accelerating program adoption cycles.

Technology Landscape in the Corporate Wellness Industry

AI and Personalized Health Coaching Platforms

AI-powered wellness coaching platforms are transforming program delivery from generic population-level interventions to individualized health journeys. Machine learning algorithms analyse biometric data, behavioural patterns, and health risk assessments to generate personalized nutrition plans, stress management recommendations, and fitness programs. Vendors, including Lark Health and Noom for Business, leverage NLP and large language models to provide 24/7 digital health coaching at per-employee costs well below traditional human-delivered program equivalents.

Digital Mental Health and EAP Technology

The digital mental health technology stack has advanced significantly, encompassing AI-driven triage tools that direct employees to appropriate care levels, asynchronous text-based therapy platforms, live video teletherapy, and self-guided cognitive behavioural therapy (iCBT) applications. ComPsych's GuidanceNow platform and Spring Health's precision mental health model represent the current state of the art in employer-deployed mental health technology, delivering measurable improvements in time-to-treatment and clinical outcome metrics.

Wearables and Biometric Monitoring Integration

Enterprise wearable programs integrating platforms such as Fitbit, Apple Watch, and Garmin enable continuous biometric data collection, supporting population-level health analytics and risk stratification. Insurer-led incentive models—linking rewards or premium adjustments to activity metrics such as step counts—have demonstrated moderate participation levels (typically ~20–40% in large enterprises), while generating rich longitudinal datasets that support wellness program optimization and ROI modelling.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Service |

Health Risk Assessmen |

21.2% |

2025 |

|

Category |

Organizations/Employers |

49.8% |

2025 |

|

Delivery |

Onsite |

78.9% |

2025 |

|

Organization Size |

Large Scale Organizations |

42.7% |

2025 |

|

Region |

Europe |

39.5% |

2025 |

By Delivery

Onsite delivery commands a 78.9% majority share of the global corporate wellness market in 2025, reflecting large enterprise preference for integrated wellness facilities, on-campus medical clinics, and in-house EAPs that provide direct utilization visibility and measurable engagement metrics. The onsite segment benefits from established contractual relationships between wellness program providers and large corporate clients, particularly in manufacturing, financial services, and healthcare sectors, where employee density makes on-premises delivery economically efficient.

To access detailed market analysis, Request Sample

Offsite delivery represents 21.1% of the market in 2025 but is the structurally faster-growing mode driven by the remote and hybrid work transformation. Digital wellness platforms, virtual therapy sessions, community fitness center reimbursements, and telehealth-enabled health coaching constitute the primary offsite program categories experiencing strongest demand growth, with this segment projected to expand its market share to approximately 29-31% by 2034.

By Category

Organizations/Employers lead the category segment at 49.8% in 2025, reflecting corporations' expanding role as direct wellness program commissioners and administrators. Large employers are increasingly building proprietary wellness platforms rather than purchasing generic vendor solutions, investing in employee health as a strategic business performance lever. The direct financial incentive structure – employers bear healthcare premium costs and the productivity cost of workforce health deterioration – reinforces this category's dominance.

Fitness and Nutrition Consultants represent 28.6% of the market in 2025, benefiting from biometric screening mandates embedded in health insurance designs and the measurable absenteeism impact of physical wellness programs. Psychological Therapists account for 21.6%, the fastest-growing category at ~7.2% CAGR – burnout, anxiety, and depression are now the leading drivers of workforce disability claims in developed economies, creating substantial and growing demand for certified psychological wellness services within employer programs.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

Notable Companies |

|

Europe |

39.5% |

EU CSRD mandates, occupational health laws, ESG reporting, and strong trade union welfare mandates |

Vitality Group UK, Benify, Medigold Health, Capita Health & Wellbeing |

|

North America |

27.4% |

Healthcare cost containment, ACA wellness incentive structures, and corporate benefits competition |

ComPsych, Optum, Wellness Corporate Solutions, Spring Health, Noom for Business |

|

Asia-Pacific |

18.6% |

MNC wellness expansion, rising workplace stress, Singapore/Australia occupational health regulations |

Cigna Asia, Medibank, OHC Group, Gympass APAC, StepUp by Mercer |

|

Latin America |

7.6% |

MNC wellness standard adoption, Brazil labour code reform, and rising mental health awareness |

Gympass (founded in Brazil/Wellhub), Conexa Saude, and local EAP providers |

|

Middle East & Africa |

6.9% |

Saudi Vision 2030 worker welfare initiatives, GCC employee well-being mandates |

Cigna Middle East, AXA Gulf, and local telehealth platforms |

Europe leads the corporate wellness market with a 39.5% global revenue share in 2025. Regulatory frameworks—including the EU Corporate Sustainability Reporting Directive, Germany’s Betriebliche Gesundheitsförderung, and the UK’s Health and Safety at Work Act—are driving sustained employer investment. Germany, the UK, and the Netherlands are the top markets, collectively accounting for over 60% of regional revenue.

North America (27.4%) is characterized by a uniquely commercial wellness dynamic where employer healthcare premium costs create direct financial motivation for preventive investment. The U.S. Affordable Care Act permits wellness program incentives of up to 30% of employee health insurance premiums, creating a structured financial incentive architecture sustaining corporate wellness penetration across large employers. Asia-Pacific (18.6%) is the fastest-growing region, driven by multinational corporations extending global wellness standards into APAC operations and government-backed occupational health frameworks in Singapore, Australia, and Japan.

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

ComPsych Corporation |

GuidanceResources |

Leader |

World's largest EAP; 127M employees; 200 countries; AI digital mental health triage |

|

Optum (UnitedHealth Group) |

Optum Wellness |

Leader |

Insurer data integration, chronic disease management, and data-driven personalized wellness |

|

Gympass / Wellhub |

Gympass Platform |

Challenger |

50,000+ partner network; 15,000 corporate clients; 50+ countries; digital platform aggregation |

|

Vitality Group |

Vitality Health |

Leader – Europe |

Behavioural incentive model, insurer partnerships, UK & South Africa market leadership |

|

Virgin Pulse /Personify Health |

Virgin Pulse Platform |

Challenger |

Enterprise digital wellness platform, engagement analytics, wearable integration |

|

Cigna Healthcare |

Cigna Wellbeing Programs |

Leader – Insurance-Led |

Global insurer distribution, integrated health + wellness, APAC & Middle East presence |

|

Aetna (CVS Health) |

Aetna Resources for Living |

Leader – Insurance-Led |

Pharmacy + health integration, CVS MinuteClinic network, population health analytics |

|

Wellness Corporate Solutions |

WCS Wellness Programs |

Emerging |

Biometric screening, health coaching, and customized program design for mid-market employers |

The corporate wellness competitive landscape is moderately fragmented, with established specialist providers competing alongside health insurance giants, HR technology platforms, and emerging digital health startups. ComPsych is the world's largest EAP provider, serving over 56,000 organizations and 127 million employees globally in 2025.

Key Company Profiles

ComPsych Corporation

ComPsych Corporation is the world's largest provider of employee assistance programs, headquartered in Chicago, Illinois, serving 127 million employees across 56,000+ organizations in 200 countries as of 2025.

- Product & Platform Portfolio: GuidanceResources EAP platform; GuidanceNow digital mental health application; WorkLife balance programs; crisis management and critical incident services; substance use and addiction support programs.

- Recent Developments: In June 2025, ComPsych has expanded its digital mental health capabilities, aligning with broader industry adoption of AI-enabled triage and personalized care routing across self-guided, coaching, and clinical support pathways.

- Strategic Focus: ComPsych's strategy centers on digital EAP modernization through AI-driven clinical triage, international market expansion across Asia-Pacific and Latin America, and deepening integration with major HR platforms, including Workday and SAP SuccessFactors, to embed wellness access within daily employee workflows.

Optum (UnitedHealth Group)

Optum is the health services and wellness division of UnitedHealth Group, leveraging one of the world's largest insurers claims databases to deliver population-level wellness program optimization for large employer clients globally.

- Product & Platform Portfolio: Optum Wellness integrated health programs; chronic disease management services; behavioural health and EAP services; digital health coaching platforms; pharmacy care management; population health analytics.

- Recent Developments: In April 2022, Optum has accelerated acquisition-led expansion, including the USD 5.4 billion acquisition of LHC Group and the acquisition of Refresh Mental Health, building an integrated care continuum spanning at-home services, behavioral health, and telehealth.

- Strategic Focus: Optum's differentiated strategy leverages UnitedHealth Group's insurer data ecosystem to demonstrate measurable healthcare cost reduction outcomes from wellness program investment, enabling outcomes-based contract structures that command premium pricing and superior renewal rates.

Gympass / Wellhub

Brazil-founded corporate wellness platform rebranded as Wellhub in 2023, connecting over 15,000 corporate clients to a network of 50,000+ fitness, meditation, therapy, and nutrition partners globally across 50+ countries.

- Product & Platform Portfolio: Corporate wellness subscriptions providing access to gyms, studios, and wellness partners; digital wellness app library; mental health and teletherapy integration; nutrition coaching partnerships; sleep and mindfulness programs.

- Recent Developments: In April 2024, Wellhub (formerly Gympass) rebranded in 2024 to reflect its evolution into a holistic wellbeing platform, serving ~15,000 enterprise clients and ~3 million users, with expanded offerings across mental health, nutrition, and digital wellness.

- Strategic Focus: Wellhub's platform aggregation model targets the structural trend of employers preferring single-vendor wellness solutions over managing multiple point providers. Its growth strategy prioritizes mental health service depth integration, emerging market expansion, and SME-accessible pricing tiers.

Market Concentration Analysis

The global corporate wellness market exhibits moderate fragmentation with the top five players – ComPsych, Optum, Gympass/Wellhub, Vitality Group, and Cigna Healthcare – collectively accounting for approximately 35-40% of global market revenue in 2025. The remaining 60-65% is distributed across hundreds of regional specialists, niche mental health providers, and digital wellness startups, reflecting the market's service diversity and geographic segmentation.

Consolidation trends are accelerating, with large health insurers acquiring specialist wellness vendors to build integrated health-and-wellness propositions. Private equity investment in digital wellness platforms has catalysed mid-tier consolidation, with aggregators such as Gympass/Wellhub building multi-vendor wellness marketplaces that are reshaping competitive dynamics by commoditizing point wellness solutions while adding distribution scale.

The EAP sub-segment, representing the most mature component of the market, exhibits higher concentration, with ComPsych and Optum dominating. Physical wellness and digital mental health remain more fragmented, offering structural opportunity for emerging platform players to capture share through superior user experience and demonstrated clinical outcome evidence.

Investment & Growth Opportunities

Fastest-Growing Segments

Digital mental health platforms are the fastest-growing investment segment, with global venture funding exceeding USD 1.5 billion in 2024. Growth is concentrated in platforms combining AI-driven triage, teletherapy, and self-guided CBT at employer-friendly price points. Within the market, psychological therapy services (~7.2% CAGR) and offsite/digital delivery models (~8.9% CAGR) represent the highest-momentum segments over the forecast period.

Emerging Market Expansion

Asia-Pacific remains underpenetrated relative to North America, creating a significant greenfield opportunity. India and Southeast Asia are key growth markets, driven by workforce expansion and rising adoption of structured wellness programs. Latin America is an emerging market, with growth led by multinational influence and improving workplace health practices.

Venture & Private Investment Trends

Private equity is consolidating the mid-market wellness space, with platform players acquiring point solutions to build integrated ecosystems. Key investment themes include AI-driven personalization, wearable data integration, financial wellness, and SME-focused subscription models, expanding reach beyond large enterprises to the underserved small business segment.

Future Market Outlook (2026-2034)

The global corporate wellness market forecast projects steady value expansion from USD 75.0 Billion in 2025 to USD 129.5 Billion by 2034 at a CAGR of 6.07%, underpinned by digital health platform adoption, AI-driven personalization enabling demonstrated ROI measurement, and regulatory expansion of occupational health mandates into emerging economies through the forecast period.

Three technology shifts will reshape the corporate wellness market through 2034. AI and generative intelligence will automate risk stratification, enable hyper-personalized coaching at near-zero marginal cost, and support predictive absenteeism modelling—shifting competition toward analytics-led platforms. Wearable adoption will expand continuous biometric monitoring, moving programs from reactive to preventive intervention models.

By 2034, the market is expected to evolve from benefits administration to data-driven health performance management. The mental health segment is projected to exceed 28% of total market value (vs. ~21.6% in 2025), driven by rising burnout, anxiety, and depression—positioning psychological wellness as the fastest-growing, structurally critical segment.

Research Methodology

Primary Research

Primary research encompassed over 50 structured interviews conducted in 2024-2025 with corporate wellness industry stakeholders, including CHROs and VP Benefits at large enterprises, corporate wellness program managers, EAP service providers, digital health platform executives, and institutional investors in the health technology sector. Primary insights validated market sizing, segmentation estimates, program adoption trends, and competitive positioning assessments across 25+ countries.

Secondary Research

Secondary sources include WHO mental health workforce reports, ILO occupational health statistics, Kaiser Family Foundation employer health benefits surveys, Eurofound workplace health data, EU CSRD regulatory publications, company annual reports, health insurance industry actuarial data, and trade publications including Business Group on Health, Employee Benefit News, and HRTech Series wellness market analyses.

Forecasting Models

Market sizing and forecasting employ bottom-up segmentation modelling validated against macroeconomic employment data, corporate healthcare expenditure trends, and program adoption rate analysis across company size cohorts and regional regulatory environments. Scenario analysis across base, optimistic, and conservative cases accounts for macroeconomic uncertainty, regulatory developments, and technology adoption pace variables.

Corporate Wellness Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Services Covered | Health Risk Assessment, Fitness, Smoking Cessation, Health Screening, Nutrition and Weight Management, Stress Management, Others |

| Categories Covered | Fitness and Nutrition Consultants, Psychological Therapists, Organizations/Employers |

| Deliveries Covered | Onsite, Offsite |

| Organization Sizes Covered | Small Scale Organizations, Medium Scale Organizations, Large Scale Organizations |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | ComPsych Corporation, Optum (UnitedHealth Group), Gympass / Wellhub, Vitality Group, Virgin Pulse /Personify Health, Cigna Healthcare, Aetna (CVS Health), Wellness Corporate Solutions, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the corporate wellness market from 2020-2034.

- The corporate wellness market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the corporate wellness industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Corporate Wellness Market Report

The global corporate wellness market was valued at USD 75.0 Billion in 2025 and is forecast to reach USD 129.5 Billion by 2034, growing at a CAGR of 6.07%.

The market is projected to reach USD 129.5 Billion by 2034, growing at a CAGR of 6.07% during 2026-2034, driven by digital wellness platform adoption, mental health program expansion, and emerging market growth.

Onsite delivery leads with a 78.9% share in 2025, driven by large enterprise preference for integrated on-campus wellness centers and in-house EAP programs with measurable utilization metrics.

Europe holds the largest regional share at 39.5% in 2025, supported by EU CSRD occupational health legislation and strong corporate ESG wellness investment commitments.

Key drivers include rising workplace mental health burden, escalating employer healthcare costs, regulatory mandates, and growing adoption of digital wellness platforms.

Leading companies include ComPsych Corporation, Optum (UnitedHealth Group), Gympass / Wellhub, Vitality Group, Virgin Pulse /Personify Health, Cigna Healthcare, Aetna (CVS Health), and Wellness Corporate Solutions.

Offsite delivery (CAGR ~8.9%) and Psychological Therapists (CAGR ~7.2%) are the fastest-growing sub-segments, driven by hybrid work normalization and escalating workplace mental health challenges.

North America accounted for 27.4% of the global corporate wellness market revenue in 2025, driven by high employer healthcare costs and ACA wellness program incentive structures.

Key trends include AI-powered digital wellness ecosystem integration, mental health parity mainstreaming, financial wellness as the fourth program pillar, wearable biometric monitoring, and outcomes-based vendor contracting.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)