Data Center Cooling Market Size, Share, Trends and Forecast by Solution, Services, Type of Cooling, Cooling Technology, Type of Data Center, Vertical, and Region, 2026-2034

Global Data Center Cooling Market Size, Share, Trends & Forecast (2026-2034)

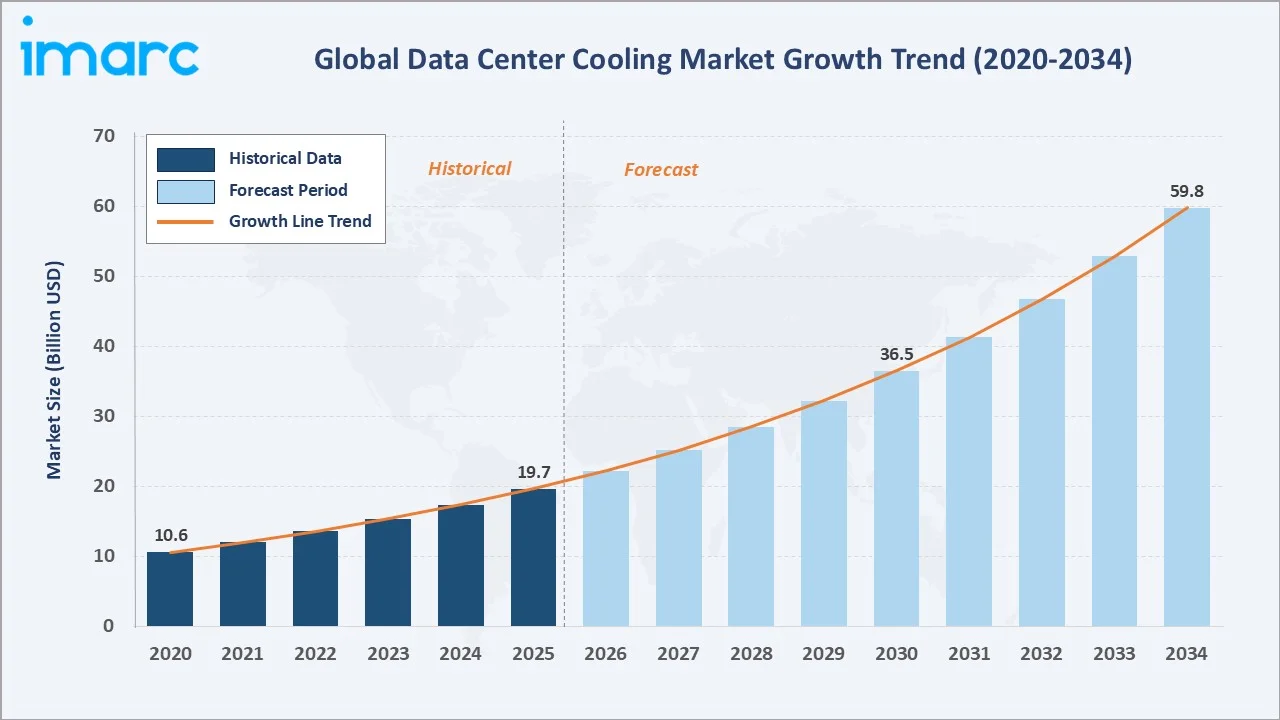

The global data center cooling market size was valued at USD 19.7 Billion in 2025 and is projected to reach USD 59.8 Billion by 2034, exhibiting a CAGR of 13.17% during the forecast period 2026-2034. Surging cloud workloads, AI-driven GPU densities, hyperscale capex, and tightening energy-efficiency rules are fuelling the data center cooling market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 19.7 Billion |

|

Forecast Market Size (2034) |

USD 59.8 Billion |

|

CAGR (2026-2034) |

13.17% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

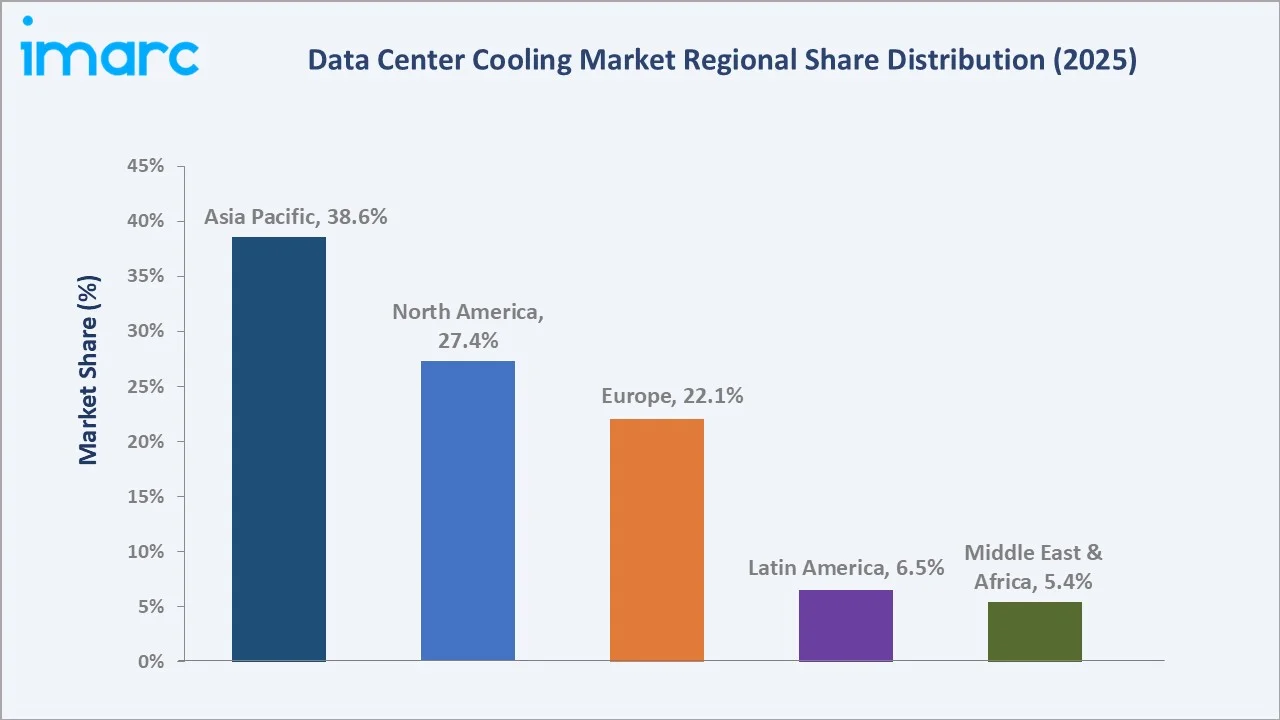

Asia Pacific (38.6% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~14.3%) |

|

Leading Type of Cooling |

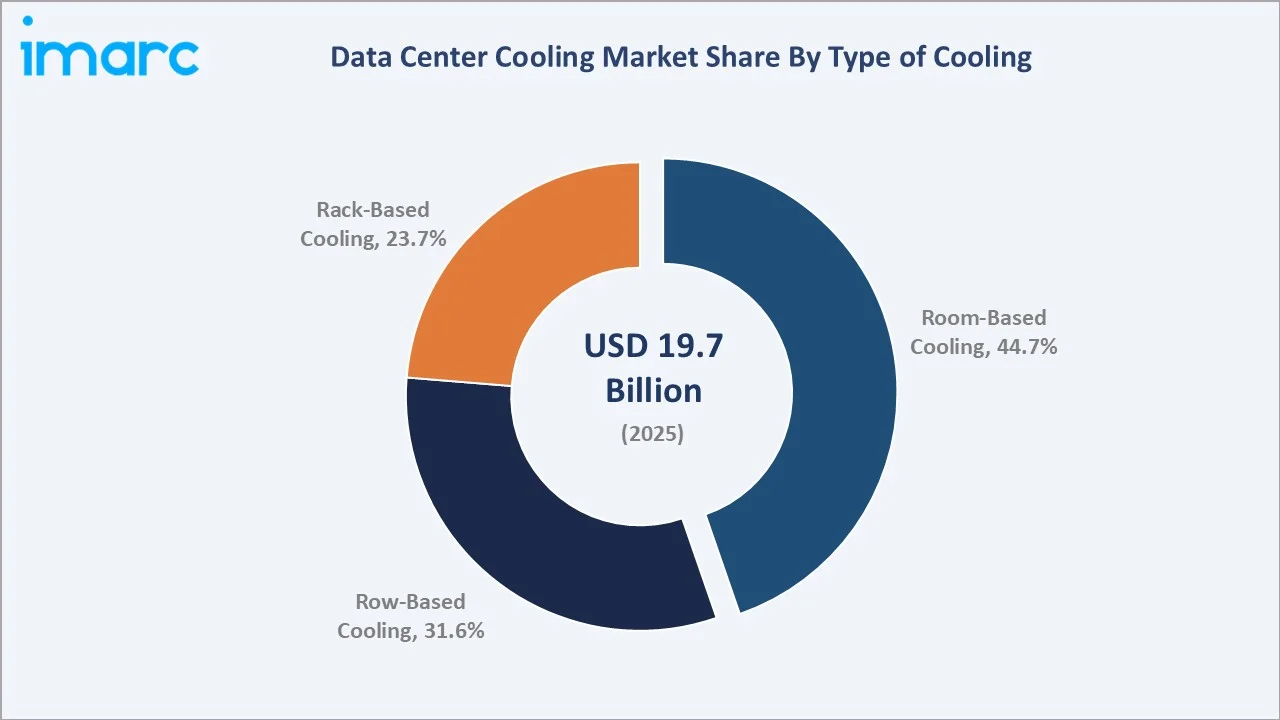

Room-Based Cooling (44.7%, 2025) |

|

Leading Type of Data Center |

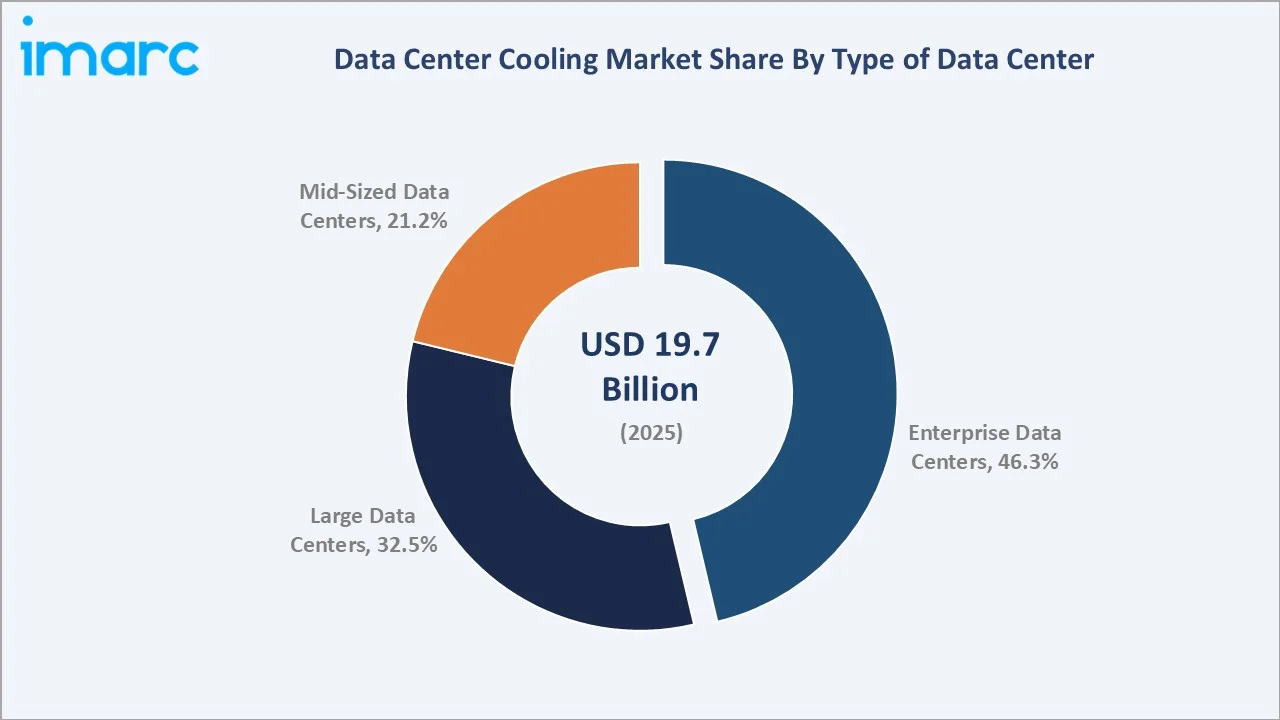

Enterprise Data Centers (46.3%, 2025) |

The global data center cooling market growth trajectory from 2020 through 2034 contrasts historical expansion against a sustained forecast curve. Hyperscale capex, AI workload heat loads, and sustainability-driven retrofits reinforce this upward curve across enterprise and colocation facilities worldwide.

To get more information on this market, Request Sample

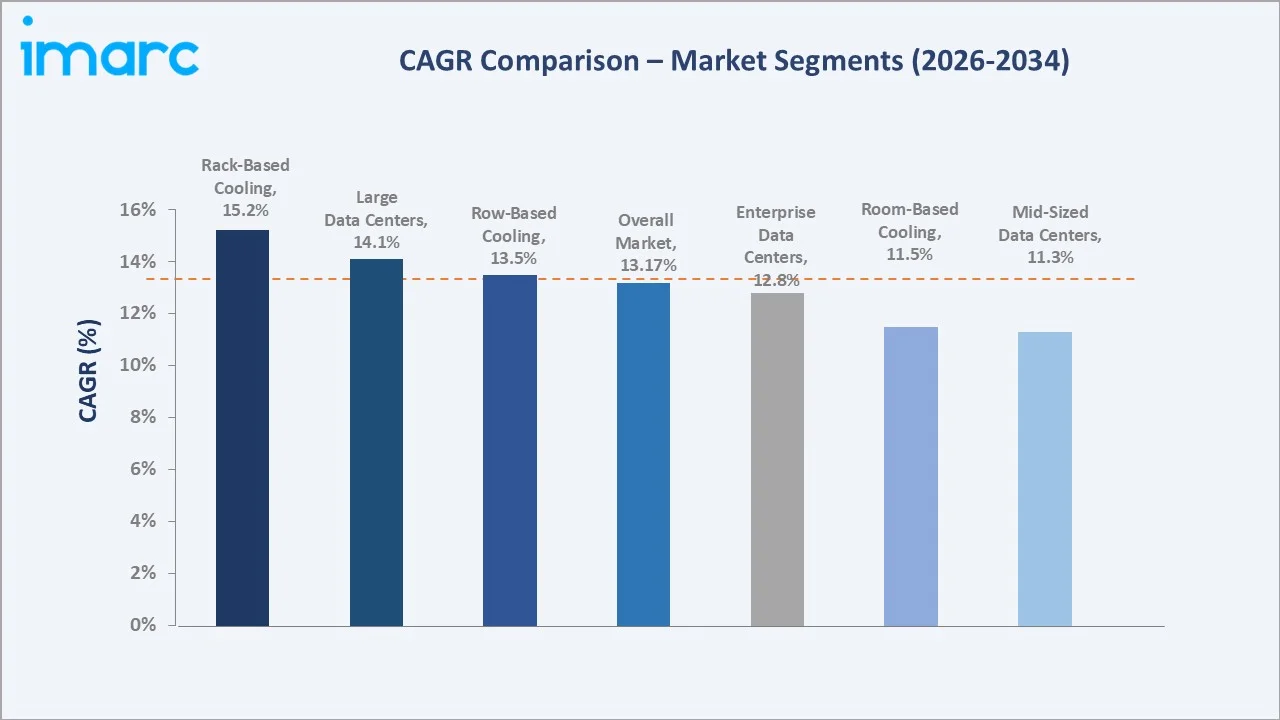

Segment-level CAGR comparisons highlight liquid-based cooling, rack-based cooling, and large data centers as the fastest-growing sub-categories within the global data center cooling market forecast through 2034.

Executive Summary

The global data center cooling market is undergoing a structural upshift. Growth is driven by cloud consolidation, AI compute expansion, and stricter energy-efficiency mandates. Valued at USD 19.7 Billion in 2025, the market is forecast to reach USD 59.8 Billion by 2034 at a CAGR of 13.17%.

Room-based cooling commands 44.7% share in 2025, anchored by legacy enterprise halls and colocation facilities. Row-based and rack-based systems are gaining ground as rack-power densities climb beyond 30 kW.

Asia Pacific leads with 38.6% global revenue share in 2025. North America holds 27.4% and Europe 22.1%. The data center cooling market outlook stays positive as hyperscale expansion, liquid-cooling adoption, and net-zero commitments converge across all major markets through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Type of Cooling |

Room-Based Cooling - 44.7% share (2025) |

|

Second-Largest Cooling Type |

Row-Based Cooling - 31.6% share (2025) |

|

Largest Type of Data Center |

Enterprise Data Centers - 46.3% share (2025) |

|

Fastest Growing Type of Data Center |

Large Data Centers - ~14.1% CAGR (2026-2034) |

|

Leading Region |

Asia Pacific - 38.6% revenue share (2025) |

|

Top Companies |

Schneider Electric, Vertiv Group Corp., STULZ GmbH, Rittal Pvt. Ltd., Fujitsu Limited, AIREDALE INTERNATIONAL AIR CONDITIONING LTD. |

|

AI Rack Heat Load |

AI workloads are significantly increasing rack-level heat density in data centers |

Key Analytical Observations Supporting The Above Data:

- Room-based cooling's 44.7% dominance in 2025 reflects its entrenched use in traditional enterprise halls and mid-density colocation facilities, where CRAC and CRAH units remain the default infrastructure.

- Row-based systems at 31.6% share are gaining ground in modular and containerized deployments. The configuration offers higher energy efficiency than room-based alternatives, making it a preferred retrofit choice.

- Enterprise data centers at 46.3% remain the backbone of corporate IT, with BFSI, IT & telecom, and healthcare verticals driving demand. On-premises workloads expand as hybrid-cloud strategies mature through 2026.

- Asia Pacific's 38.6% global dominance reflects China's data-sovereignty investments, India's Digital India push, and ASEAN colocation expansion. In April 2024, GDS and Gaw Capital Partners committed to a 40 MW campus in Tokyo, Japan.

- AI and GPU heat densities are a structural tailwind. NVIDIA H100-class racks exceed 40 kW, forcing a shift toward direct-to-chip and immersion cooling, the premium-growth sub-segment through 2030.

Global Data Center Cooling Market Overview

Data center cooling encompasses systems and services that regulate temperature, humidity, and airflow across server environments. The global market spans air conditioning, chilling units, cooling towers, economizer systems, liquid cooling, and control platforms, along with consulting, installation, and maintenance services.

The industry sits at the intersection of digital infrastructure, energy policy, and sustainability mandates. Growth is supported by strong hyperscale investment in data center expansion, rising cloud adoption as enterprises shift workloads to cloud environments, and the rapid rise of AI-driven applications that are significantly increasing rack-power densities across the sector.

Market Dynamics

To evaluate market opportunities, Request Sample

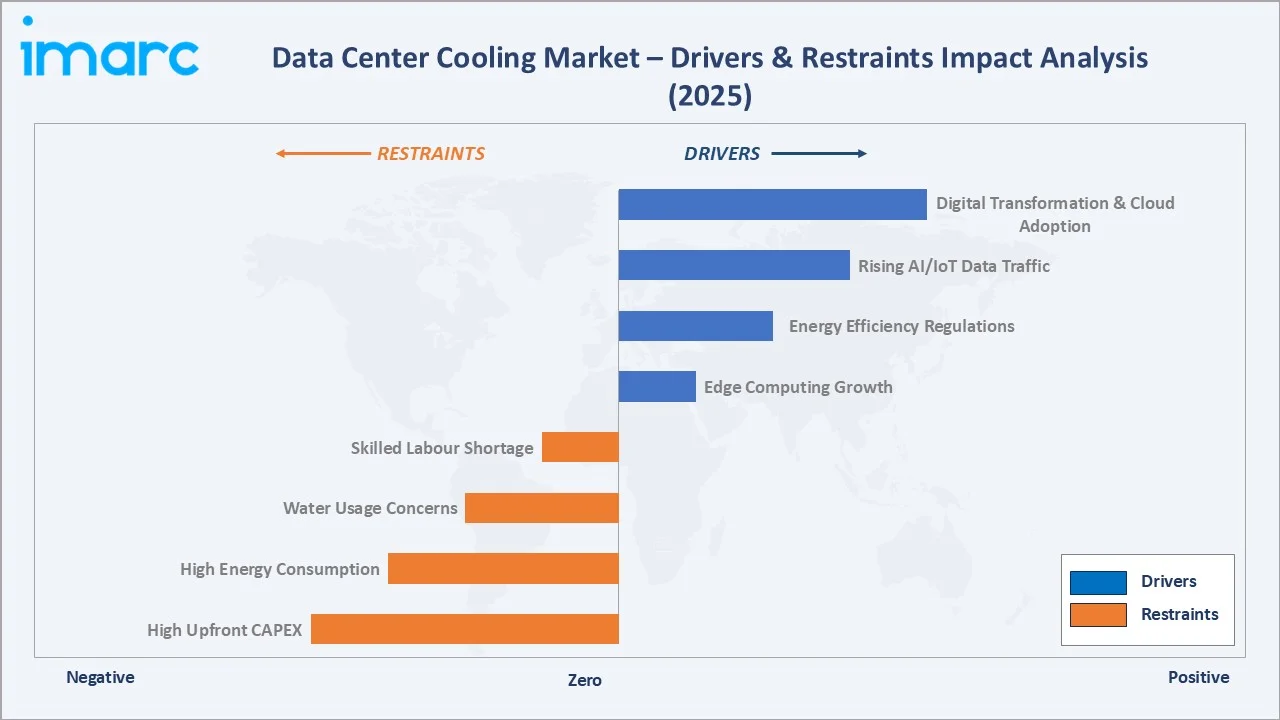

Market Drivers

- Hyperscale and Cloud Expansion: Cloud data centers now store about 60% of global corporate data, according to industry benchmarks. Hyperscalers such as AWS, Microsoft, Google, and Alibaba continue to expand capacity, creating sustained demand for high-capacity precision cooling across new and retrofit builds.

- Rising AI and GPU Workloads: AI training clusters and GPU-dense racks are significantly increasing rack-level thermal loads compared to traditional environments. This shift is accelerating the adoption of advanced cooling technologies, including liquid-based systems and rear-door heat exchangers, across both hyperscale and enterprise data center facilities.

- Energy-Efficiency Regulations: Regulatory frameworks such as the EU Energy Efficiency Directive (2023), Singapore's Green Data Centre Roadmap, and California's SB 253 mandate PUE disclosure and efficiency targets, accelerating replacement of legacy CRAC units with free-cooling and economizer-based systems.

- Edge and IoT Proliferation: In 2025, Number of connected IoT devices growing 14% to 21.1 billion globally according to IoT Analytics. Edge micro-data-centers require compact, modular cooling, generating a high-growth niche for rack-based and row-based configurations.

Market Restraints

- High Upfront CAPEX: Advanced cooling platforms, particularly liquid and immersion systems, require significant upfront investment and plumbing retrofits, slowing adoption among mid-sized data-center operators with constrained budgets.

- High Energy Consumption: Rising electricity tariffs and grid-capacity constraints in markets such as Northern Virginia, Dublin, and Singapore are adding operational pressure on facility owners.

- Water Usage Concerns: Evaporative cooling towers face scrutiny in water-stressed regions. Regulators in parts of the western United States, Spain, and Australia are restricting water-intensive cooling, nudging operators toward dry and hybrid alternatives.

Market Opportunities

- Liquid and Immersion Cooling: Liquid cooling is transitioning from a niche HPC technology into a mainstream data center requirement. Direct-to-chip cold-plate systems are being specified as standard for AI training clusters. Single-phase and two-phase immersion cooling are moving beyond pilot deployments into broader commercial rollouts by vendors. Leading hyperscalers are designing new halls for native liquid-cooling operation by 2026–2027.

- AI-Driven Cooling Optimization: AI and ML platforms can significantly improve cooling efficiency by dynamically optimizing airflow, temperature setpoints, and chiller performance. This creates a strong software-driven upsell opportunity for OEMs and data-center operators, enabling smarter energy management and reduced operational costs.

- Emerging Market Buildouts: Countries such as India, Indonesia, and Vietnam, along with the Gulf Cooperation Council, are rapidly expanding digital infrastructure. Investments by players like GDS Holdings and Gaw Capital Partners highlight strong pan-Asian demand for advanced, high-performance cooling platforms to support next-generation data centers.

Market Challenges

- Refrigerant Transition: Global phase-down of HFC refrigerants under the Kigali Amendment is forcing OEMs to reformulate chiller and CRAC product lines, adding material costs and certification complexity through 2030.

- Skilled Labour Shortage: The shift to liquid and immersion platforms requires new plumbing, chemistry, and controls skills. Shortages of certified data-center technicians are extending project timelines in North America and Europe.

- Grid and Permitting Constraints: Data-center power moratoriums in markets such as Dublin and Amsterdam, combined with slow transmission buildouts, are delaying cooling-system commissioning alongside overall facility ramp-ups.

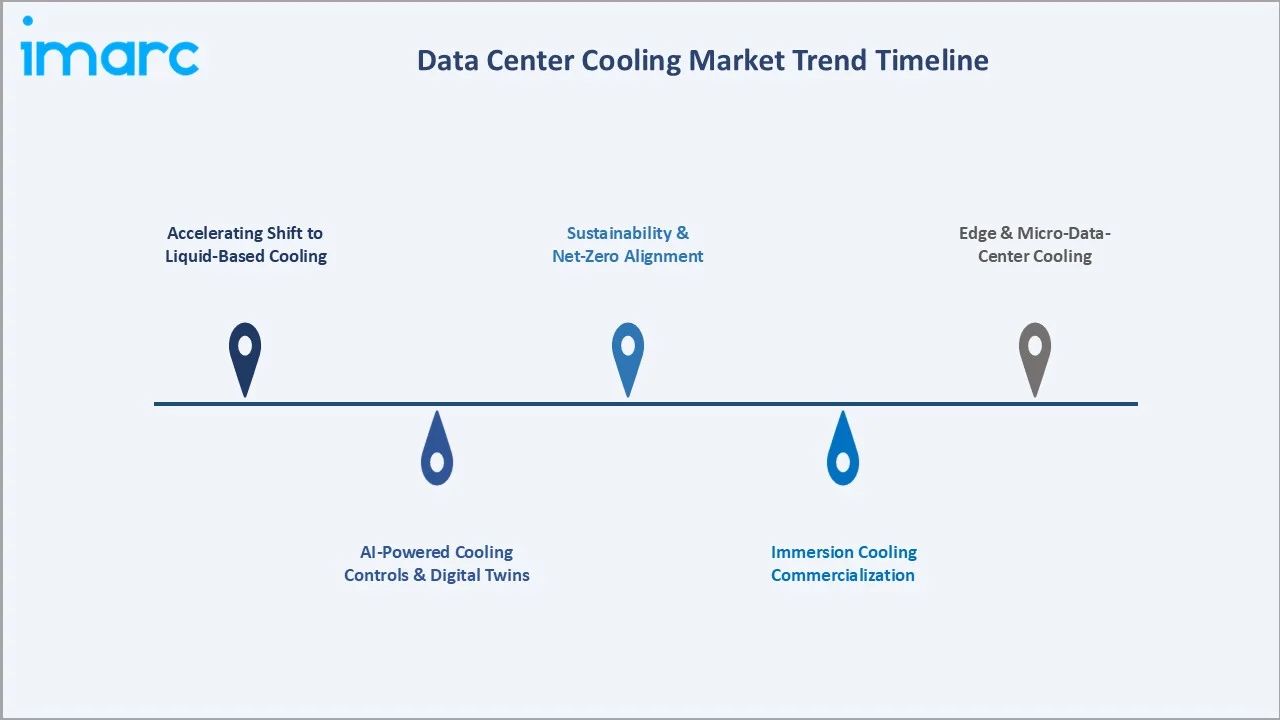

Emerging Market Trends

1. Accelerating Shift to Liquid-Based Cooling

Liquid cooling is transitioning from a niche HPC technology into a mainstream requirement. Direct-to-chip and rear-door heat-exchanger architectures are being specified as standard for AI training clusters. Leading hyperscalers are designing new halls for hybrid air-liquid operation by 2026-2027.

2. AI-Powered Cooling Controls and Digital Twins

Operators are increasingly embedding AI and ML into building-management systems to reduce cooling energy consumption through real-time optimization. Digital twin platforms from Schneider Electric, Vertiv, and Siemens enable continuous PUE optimization, with early deployments demonstrating notable efficiency gains.

3. Immersion Cooling Commercialization

Two-phase and single-phase immersion cooling are moving beyond pilot stages into broader deployment across advanced data centers. Global rollouts by Submer, GRC (Green Revolution Cooling), and LiquidStack—alongside innovations from Petronas Lubricants International and Iceotope—are enabling next-generation AI campuses to achieve ultra-efficient cooling performance with significantly lower PUE levels.

4. Sustainability and Net-Zero Alignment

Net-zero commitments from Microsoft (2030), Google (2030), and Equinix (2030) are driving adoption of free cooling, heat reuse, and renewable-powered chillers. European operators are piping waste heat into district systems, notably in Stockholm and Helsinki.

5. Edge and Micro-Data-Center Cooling

5G and IoT rollouts are proliferating edge sites near cell towers, factories, and retail hubs. Compact prefabricated cooling modules from Schneider and Vertiv are becoming the default choice, supporting fast deployment in under-conditioned environments.

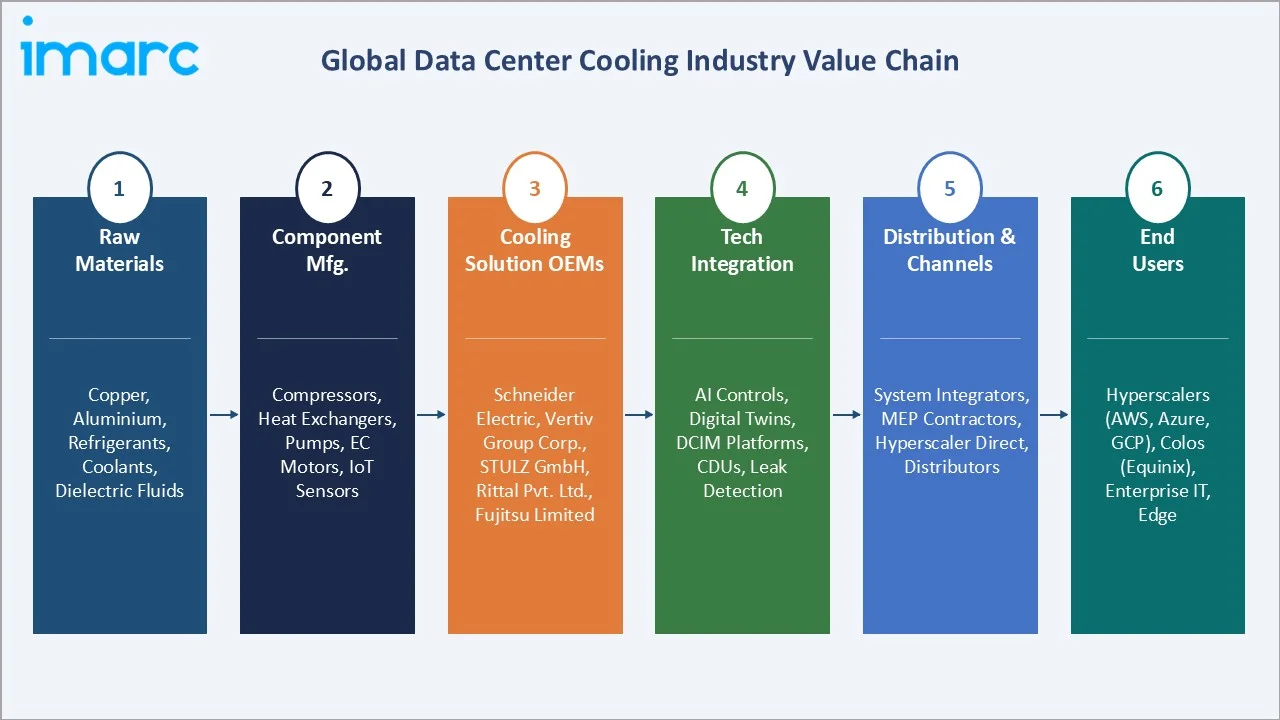

Industry Value Chain Analysis

The global data center cooling value chain spans six integrated stages, from raw-material supply through end-customer operation. Each stage exhibits distinct margin profiles, technology investments, and competitive dynamics relevant to the overall data center cooling market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials |

Copper, aluminium, steel, low-GWP refrigerants (R-1234ze, R-513A), dielectric coolants, glycol mixtures |

|

Component Manufacturing |

Compressors, heat exchangers, pumps, fans, EC motors, IoT sensors - produced by Tier-2 suppliers across China, Germany, Italy, and Japan |

|

OEM Manufacturing |

Schneider Electric, Vertiv Group Corp., STULZ GmbH, Rittal Pvt. Ltd - CRAC/CRAH units, chillers, in-row coolers, immersion tanks |

|

Technology Integration |

AI-based controls, digital twins, DCIM platforms, liquid-cooling distribution units (CDUs), leak-detection systems |

|

Distribution Channels |

System integrators, MEP contractors, direct-to-hyperscaler sales, regional distributors, online B2B procurement |

|

End Users |

Hyperscalers (AWS, Azure, GCP), colocation operators (Equinix, Digital Realty), enterprise IT, edge/telco, BFSI, government |

OEMs hold the highest strategic value by bundling components, advanced refrigerants, and AI-driven controls into turnkey platforms. Meanwhile, systems integrators and hyperscaler-direct sales channels are reshaping distribution, enabling vendors to capture higher lifetime service revenue.

Technology Landscape in the Data Center Cooling Industry

Air-Based Cooling and Free Cooling Innovation

Air-based systems continue to serve the majority of installed data center capacity. Economizer-based free cooling—leveraging outside air in cooler climates is becoming standard practice in regions such as the Nordics, Canada, and the northern United States. Indirect evaporative cooling units are also gaining traction in temperate zones, helping operators achieve significantly improved energy efficiency with lower PUE levels.

Liquid and Immersion Cooling

Air-based systems continue to dominate the installed data center base. Economizer-based free cooling—using outside air in cooler climates is becoming standard across regions such as the Nordics, Canada, and the northern United States. Indirect evaporative cooling is also gaining adoption in temperate regions, supporting improved energy efficiency and lower PUE levels.

Smart Controls and AI Optimization

DCIM (data-center infrastructure management) and AI-based control layers are now embedded in most new chiller and CRAH deployments. Airedale's 2024 Cooling System Optimizer, launched in the United States, is an example of intelligent control layers bridging chiller controls with building management systems.

Sustainable Refrigerants and Heat Reuse

OEMs are migrating to low-GWP refrigerants such as R-1234ze and R-513A ahead of Kigali Amendment phasedowns. Heat-reuse systems that route waste heat to district networks are increasingly deployed in Europe, notably by operators in Stockholm, Helsinki, and Frankfurt.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Solution | Air Conditioning | 🔒 | 2025 |

| Services | Installation and Deployment | 🔒 | 2025 |

| Type of Cooling | Room-Based Cooling | 44.7% | 2025 |

| Cooling Technology | Liquid-Based Cooling | 🔒 | 2025 |

| Type of Data Center | Enterprise Data Centers | 46.3% | 2025 |

| Vertical | IT and Telecom | 🔒 | 2025 |

| Region | Asia Pacific | 38.6% | 2025 |

By Type of Cooling

To access detailed market analysis, Request Sample

Room-based cooling leads the global data center cooling market with a 44.7% share in 2025. Demand is anchored by legacy enterprise halls and traditional colocation facilities that rely on CRAC and CRAH units. The segment benefits from familiar operating models, large installed bases, and widespread maintenance expertise across North America, Europe, and Asia Pacific.

By Type of Data Center

Enterprise data centers dominate the end-user mix at 46.3% of global revenue in 2025. Demand is sustained by BFSI, IT & telecom, government, and healthcare workloads that remain on-premises for regulatory, latency, or security reasons. Hybrid-cloud strategies are extending the life of enterprise halls through 2026, reinforcing steady cooling capex.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

38.6% |

China data-sovereignty capex, India Digital India, Japan/Singapore hyperscale, ASEAN colocation boom |

|

North America |

27.4% |

Hyperscale expansion (AWS, Azure, GCP), AI training capex, SB 253 disclosure, Texas and Virginia clusters |

|

Europe |

22.1% |

EU Energy Efficiency Directive, Nordic free cooling, heat-reuse regulations, German/UK colocation |

|

Latin America |

6.5% |

Brazil/Mexico colocation, nearshoring to Mexico, fintech cloud demand, Sao Paulo metro clusters |

|

Middle East & Africa |

5.4% |

UAE and Saudi digital-economy programs, Vision 2030 data-residency, South Africa cloud zones |

Asia Pacific commands 38.6% global revenue share in 2025. China is the single most important national market, combining data-sovereignty investments with rapidly scaling hyperscale builds from Alibaba, Tencent, and Baidu. India's Digital India mission is driving colocation expansion by CtrlS, NTT, and ST Telemedia. In April 2024, GDS and Gaw Capital announced a 40 MW data-center campus in Tokyo, Japan. The region is forecast to remain the fastest-growing geography at approximately 14.3% CAGR through 2034.

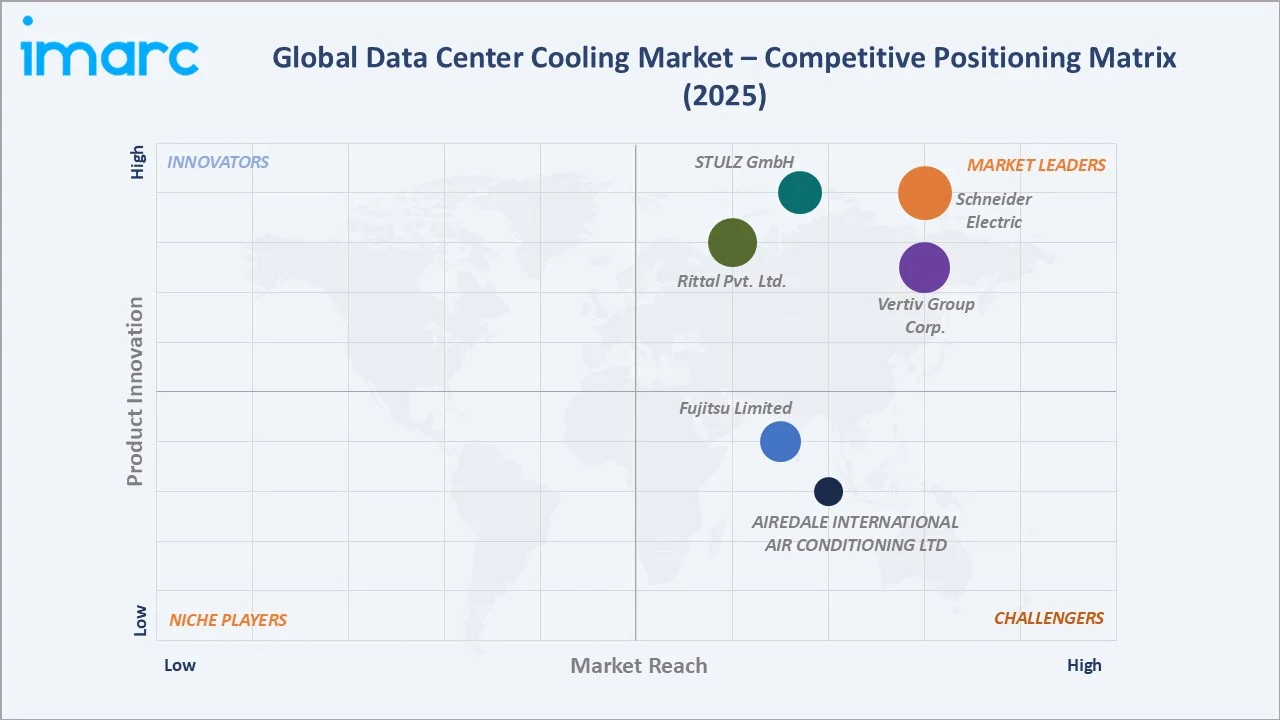

Competitive Landscape

|

Company |

Brand |

Position |

Core Strength |

|

Schneider Electric |

EcoStruxure, Uniflair, APC, Motivair |

Leader |

DCIM integration, modular cooling, global distribution |

|

Vertiv Group Corp. |

Liebert, CoolPhase |

Leader |

Broad CRAC/chiller portfolio, AI-ready cooling |

|

STULZ GmbH |

CyberAir, CyberRow, CyberHandler |

Leader |

German engineering, precision cooling, CRAH expertise |

|

Rittal Pvt. Ltd. |

LCP, Liquid Cooling Package |

Leader |

Modular racks, liquid cooling, data-center containers |

|

Fujitsu Limited |

PRIMERGY Liquid Immersion Cooling System |

Challenger |

Liquid immersion pilots, Japan and Asia hyperscale |

|

AIREDALE INTERNATIONAL AIR CONDITIONING LTD. |

TurboChill, Cooling System Optimizer (rebranded Airedale by Modine) |

Challenger |

UK engineering, 2024 US Cooling System Optimizer |

The global data center cooling market is moderately consolidated. Global powerhouses compete with regional specialists and emerging liquid-cooling vendors. Leading players compete on PUE performance, AI-driven controls, liquid-cooling capability, and sustainability credentials. Strategic moves are frequent.

Key Company Profiles

Schneider Electric

Schneider Electric is a global leader in energy management and industrial automation, headquartered in France. The company provides integrated solutions across power distribution, data centers, infrastructure, and industrial processes, combining hardware, software, and digital services.

- Product & Platform Portfolio: Schneider Electric’s cooling portfolio spans the EcoStruxure Data Center platform, Uniflair precision cooling, APC InRow RP/RC, Motivair liquid cooling, and modular prefabricated data-center solutions, covering air, liquid, and hybrid architectures.

- Recent Developments: In 2025, Schneider Electric unveiled a comprehensive liquid cooling portfolio integrated with Motivair, aimed at supporting high-performance computing (HPC) and AI workloads. The offering combines hardware, software, and services including coolant distribution units, cold plates, and thermal management systems to address rising heat densities in next-generation data centers while improving scalability and energy efficiency.

- Strategic Focus: Schneider Electric’s strategy centers on integrated DCIM, liquid-cooling leadership, and net-zero data-center solutions, with particular emphasis on hyperscale wins in North America, Europe, and Asia Pacific through 2030.

Vertiv Group Corp.

Vertiv Group Corp. is a U.S.-based provider of critical digital infrastructure and continuity solutions, primarily serving data centers, communication networks, and commercial and industrial facilities. Headquartered in Columbus, Ohio.

- Product & Platform Portfolio: Vertiv Group Corp.’s cooling portfolio includes the Liebert CRV and DS precision cooling families, CoolPhase immersion systems, rear-door heat exchangers, chillers, and the XDU coolant distribution unit line optimized for AI and HPC workloads.

- Recent Developments: In 2025, Vertiv Group Corp. unveiled new liquid cooling solutions at Data Centre World (DCW) 2025 in London, aimed at addressing the growing thermal demands of AI and high-density computing environments. The portfolio highlights advanced cooling technologies and integrated services designed to improve efficiency, scalability, and reliability, while supporting next-generation data center architectures.

- Strategic Focus: Vertiv Group Corp.’s focus is on scaling AI-ready liquid and hybrid cooling, expanding its modular prefabricated data-center business, and deepening OEM partnerships with hyperscalers building GPU-dense clusters across the Americas and Asia Pacific.

STULZ GmbH

STULZ GmbH is a Germany-based, family-owned company specializing in precision cooling and climate control solutions for mission-critical applications such as data centers and telecommunications infrastructure. Founded in 1947 and headquartered in Hamburg.

- Product & Platform Portfolio: STULZ GmbH’s portfolio includes CyberAir CRAH units, CyberRow in-row cooling, CyberHandler air-handling units, chillers, and the Micro DC edge-cooling range. The company is also scaling direct-to-chip cold-plate systems for AI workloads.

- Recent Developments: In 2025, STULZ GmbH has invested in a new production facility at its Hamburg headquarters focused on liquid cooling solutions, reinforcing its strategy to meet rising demand from AI and high-performance computing data centers. The expansion integrates R&D, product, and service teams to accelerate innovation, improve efficiency, and enhance global customer support, while increasing production of advanced cooling systems such as its CyberCool CMU units.

- Strategic Focus: STULZ GmbH’s strategy targets precision cooling leadership in Germany, the UK, and North America, supported by expanded liquid-cooling capability and a stronger service footprint across Asia Pacific and the Middle East.

Market Concentration Analysis

The global data center cooling market is moderately concentrated. The top five players - Schneider Electric, Vertiv Group Corp., STULZ GmbH, Rittal Pvt. Ltd., Fujitsu Limited - collectively account for an estimated 35-42% of global market revenue in 2025.

The market shows a bifurcated dynamic. At the premium OEM tier, consolidation is accelerating around AI-ready liquid cooling, DCIM software, and sustainability credentials. Meanwhile, immersion and direct-to-chip specialists are scaling rapidly, attracting strategic investment from hyperscalers and industrial conglomerates. This dual dynamic is intensifying competition across price tiers through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Liquid-based cooling is the fastest-growing sub-segment, driven by rising thermal demands from advanced computing workloads. Rack-based cooling is also expanding steadily, while large data centers continue to lead among end-user segments. AI-ready direct-to-chip and immersion platforms represent a premium technology opportunity, with ultra-high rack densities becoming increasingly commercially viable in next-generation deployments.

Emerging Market Expansion

India is the highest-potential emerging market, driven by Digital India, PLI-backed IT investment, and rapid hyperscale buildouts. Indonesia, Vietnam, the GCC, and Mexico represent secondary high-growth opportunities, supported by nearshoring, data-residency rules, and structural digital-economy expansion through 2030.

Venture and Strategic Investment Trends

Strategic investment is flowing into liquid and immersion cooling. Petronas Lubricants and Iceotope launched a new data-center cooling fluid in June 2024. In September 2024, Gates introduced the Data Master Data Center Cooling Hose. Investments in AI-driven cooling software, low-GWP refrigerants, and heat-reuse systems are the primary focus areas for venture and corporate capital in the sector through 2034.

Future Market Outlook (2026-2034)

The global data center cooling market forecast projects steady expansion from USD 19.7 Billion in 2025 to USD 59.8 Billion by 2034 at a CAGR of 13.17%. Asia Pacific will retain regional leadership while scaling structurally. North America and Europe will sustain premium value growth through AI capex, regulatory compliance, and sustainability-driven retrofit cycles.

Three shifts will reshape the market over the next decade. First, rising AI-driven GPU densities will make liquid cooling a default requirement, with hybrid air–liquid data halls emerging as the standard. Second, tightening energy and water regulations will push operators toward ultra-efficient designs and accelerate adoption of closed-loop water systems. Third, AI-native control platforms from OEMs will unlock a new layer of efficiency gains, shifting cooling from a one-time capital investment to a more outcome-based, service-driven model.

Research Methodology

Primary Research

Primary research included structured interviews conducted in 2024-2025 with data-center stakeholders: cooling-platform product directors at OEMs, facility and energy managers at hyperscale and colocation operators, MEP consulting engineers, and procurement leads at BFSI and IT & telecom enterprises. Primary insights validated market sizing, segment shares, and technology adoption timelines.

Secondary Research

Secondary sources include IEA data-center energy reports, Uptime Institute's Global Data Center Survey, EU Energy Efficiency Directive documentation, US DOE Better Buildings data-center program, company annual reports, hyperscaler capex disclosures, trade publications such as Data Center Knowledge and Data Center Dynamics, and regional digital-infrastructure association data.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models. Inputs included hyperscale capex trajectories, rack-power density assumptions, PUE improvement curves, and historical cooling-revenue elasticity. Scenario analysis (base, optimistic, conservative) was applied to account for macroeconomic and regulatory uncertainty.

Data Center Cooling Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Solutions Covered | Air Conditioning, Chilling Units, Cooling Towers, Economizer Systems, Liquid Cooling Systems, Control Systems, Others |

| Services Covered | Consulting, Installation and Deployment, Maintenance and Support |

| Type of Coolings Covered | Room-Based Cooling, Row-Based Cooling, Rack-Based Cooling |

| Cooling Technologies Covered | Liquid-Based Cooling, Air-Based Cooling |

| Types of Data Centers Covered | Mid-Sized Data Centers, Enterprise Data Centers, Large Data Centers |

| Verticals Covered | BFSI, IT and Telecom, Research and Educational Institutes, Government and Defense, Retail, Energy, Healthcare, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Schneider Electric, Vertiv Group Corp., STULZ GmbH, Rittal Pvt. Ltd., Fujitsu Limited, AIREDALE INTERNATIONAL AIR CONDITIONING LTD., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the data center cooling market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global data center cooling market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the data center cooling industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Data Center Cooling Market Report

The global data center cooling market was valued at USD 19.7 Billion in 2025, driven by hyperscale capex, AI heat densities, cloud migration, and stricter energy-efficiency mandates worldwide.

The market is projected to reach USD 59.8 Billion by 2034, growing at a CAGR of 13.17% during 2026-2034, supported by liquid-cooling adoption, AI workloads, and sustainability-driven retrofits.

Room-based cooling leads with a 44.7% share in 2025, reflecting its entrenched use across legacy enterprise halls and traditional colocation facilities that rely on CRAC and CRAH platforms.

Enterprise data centers lead with a 46.3% share in 2025, sustained by on-premise BFSI, IT & telecom, healthcare, and government workloads across hybrid-cloud architectures through 2026.

Asia Pacific dominates with a 38.6% share in 2025. China's data-sovereignty capex, India's Digital India mission, and hyperscale expansion in Japan and Singapore underpin its leadership.

Key drivers include hyperscale and cloud expansion, AI and GPU workloads, energy-efficiency regulations such as the EU EED, rising IoT connections, and sustainability-driven retrofit activity.

Major players include Schneider Electric, Vertiv Group Corp., STULZ GmbH, Rittal Pvt. Ltd., Fujitsu Limited, and AIREDALE INTERNATIONAL AIR CONDITIONING LTD.

Liquid-based cooling is the fastest-growing technology, driven by rising AI rack densities and the commercialization of immersion cooling solutions, which are accelerating adoption across next-generation data centers.

Key opportunities include liquid and immersion cooling platforms, AI-driven cooling optimization, emerging-market hyperscale builds in India and Indonesia, low-GWP refrigerants, and heat-reuse systems.

AI workloads are significantly increasing rack densities compared to traditional environments. This shift is accelerating the adoption of direct-to-chip liquid cooling and rear-door heat exchanger technologies to manage rising thermal demands.

Sustainability is central. Net-zero commitments, EU Energy Efficiency Directive, and Kigali Amendment phase-downs are driving low-GWP refrigerants, free cooling, and heat-reuse deployments globally.

IT & telecom lead demand, followed by BFSI, government & defense, healthcare, and energy. These verticals require precision cooling for high-availability, high-density computing environments.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)