Decorative Lighting Market Size, Share, Trends and Forecast by Product Type, Light Source, Distribution Channel, End User, and Region, 2026-2034

Decorative Lighting Market Size, Share, Trends & Forecast (2026-2034)

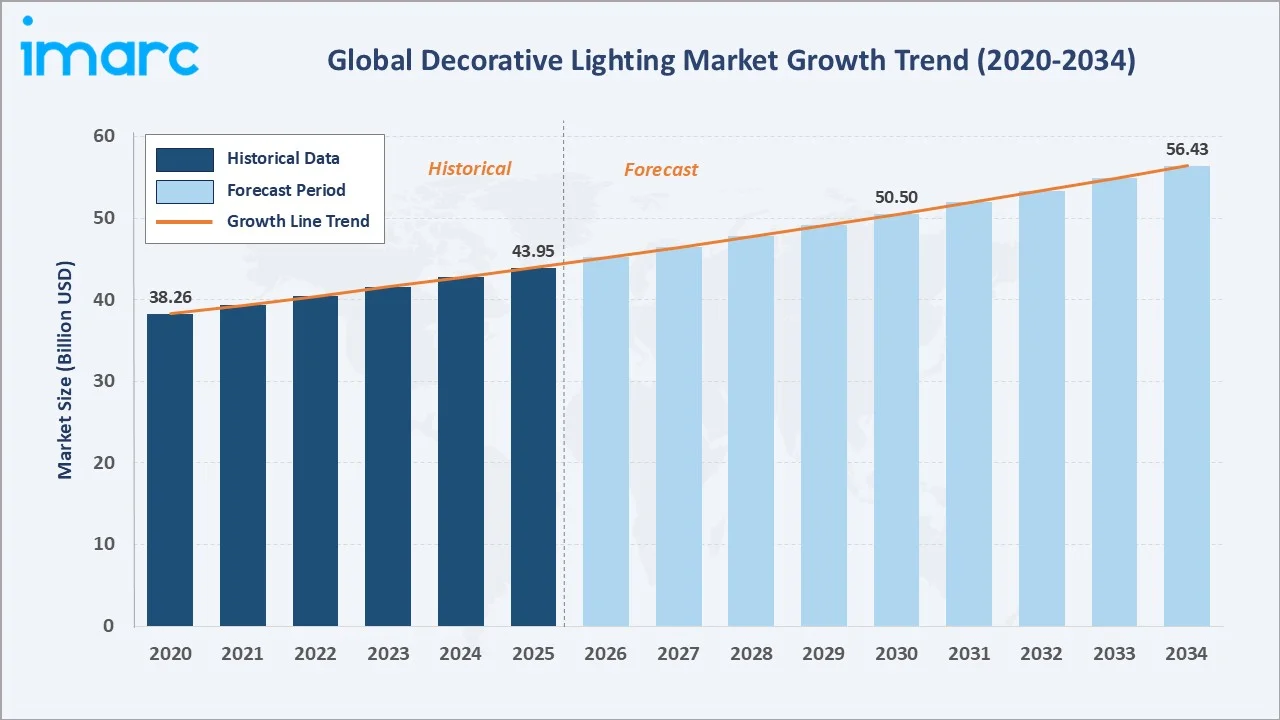

The global decorative lighting market reached USD 43.95 Billion in 2025 and is projected to reach USD 56.43 Billion by 2034, growing at a CAGR of 2.82% during 2026-2034. The market is driven by growing consumer demand for energy-efficient, aesthetically pleasing lighting solutions, as well as the increasing adoption of smart lighting technologies in residential and commercial spaces. By 2050, the global population is projected to grow from 7 billion to 10 billion, necessitating the construction of 13,000 buildings daily over the next 30 years, which drives increased demand for decorative lighting solutions in both residential and commercial sectors. LED light sources dominate at 39.8%. Commercial end users lead at 62.8%. North America commands 37.6% of global market revenues.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 43.95 Billion |

|

Forecast Market Size (2034) |

USD 56.43 Billion |

|

CAGR (2026-2034) |

2.82% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Light Source |

LED (39.8%, 2025) |

|

Largest End User |

Commercial (62.8%, 2025) |

|

Leading Region |

North America (37.6%, 2025) |

The market expanded from USD 38.26 Billion in 2020 to USD 43.95 Billion in 2025, anchored at USD 50.50 Billion in 2030, and forecast to reach USD 56.43 Billion by 2034. The COVID-19 pandemic catalyzed a home renovation surge, permanently increasing decorative lighting upgrade rates as homeowners treated lighting as a cost-effective interior transformation tool. Post-COVID, the hospitality and commercial sector's refurbishment wave sustained commercial decorative lighting demand through 2025.

To get more information on this market, Request Sample

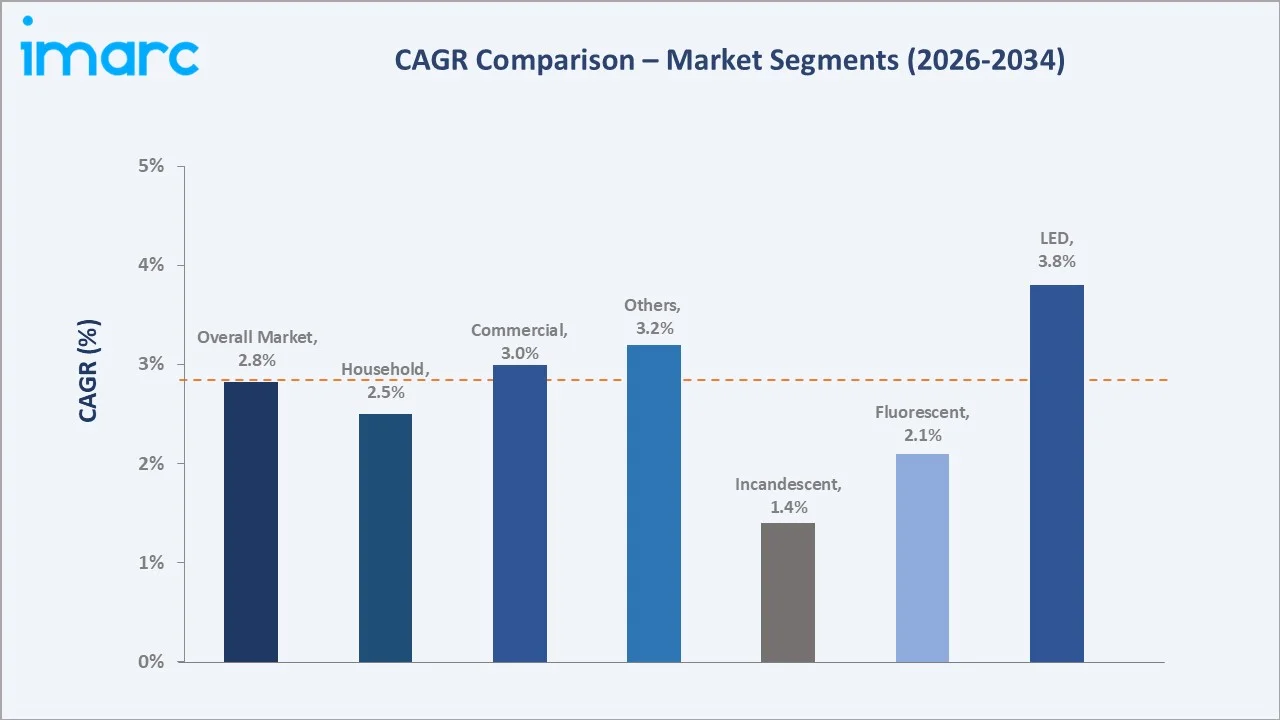

LED grows fastest at ~3.8% CAGR (2026-2034), driven by regulation mandates phasing out fluorescent lamps and LED decorative fixtures achieving aesthetic parity with incandescent through warm-white tunable technology that matches the warm glow previously only achievable with incandescent sources. Commercial end users grow at ~3.0% CAGR, sustained by hospitality sector expansion, luxury retail flagship development, and smart building integration projects.

Executive Summary

The global decorative lighting market reached USD 43.95 Billion in 2025, serving as the intersection of functional electrical infrastructure and decorative interior design elements. Unlike functional lighting (floodlights, task lighting), decorative lighting is purchased primarily for its aesthetic contribution to interior and exterior spaces, including chandeliers, pendant lights, wall sconces, and artisan lamps, which are design statements as much as light sources. This dual functional-aesthetic character gives the decorative lighting market both the stability of a necessary home and commercial building component and the premiumization potential of a luxury goods category. The market is projected to reach USD 56.43 Billion by 2034 at 2.82% CAGR.

LED light sources command 39.8% market share (2025), having crossed the tipping point where LED decorative fixtures equal or exceed incandescent in warmth, color rendering, and aesthetic appeal while delivering energy savings and 15-25 year service lives that eliminate relamping costs for commercial operators. Commercial end users at 62.8% reflect hospitality, retail, office, and restaurant sectors' outsized decorative lighting spending per square foot versus residential. Asia-Pacific at 28.4% is the fastest-growing region as China's interior design industry matures and India's premium residential and hospitality markets adopt global design standards.

Key Market Insights

|

Insight |

Data |

|

Dominant Light Source |

LED - 39.8% share (2025) |

|

Largest End User |

Commercial - 62.8% market share (2025) |

|

Leading Region |

North America - 37.6% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- LED at 39.8% reflecting technology maturation, enabling decorative-quality light output at efficiency economics: Modern LED decorative fixtures achieve Color Rendering Index (CRI) of 90-98 versus traditional incandescent's 100 CRI, while delivering 80-90% energy reduction.

- Commercial at 62.8% driven by hospitality, luxury retail, and restaurant sectors' premium lighting investment: Commercial decorative lighting commands high per fixture in luxury hospitality applications. Major hospitality brands invest heavily per guest room in FF&E (Furniture, Fixtures, and Equipment) during hotel renovations, with lighting representing 8-12% of total FF&E spend.

- North America at 37.6% anchored by home improvement culture and robust commercial real estate market: US home improvement stores collectively generate a market opportunity in decorative lighting sales. The US commercial construction market, office, hospitality, and retail, represents 40%+ of all decorative lighting commercial spending globally, driven by the world's largest commercial real estate market.

Decorative Lighting Market Overview

The decorative lighting market encompasses all luminaires and lighting accessories where aesthetic design intent is primary alongside functional light delivery, including chandeliers, pendant lights, wall sconces, flush mount ceiling fixtures, semi-flush mounts, table lamps, floor lamps, bath lighting, outdoor decorative fixtures, and string lights. The market serves both commercial applications (hospitality, retail, restaurants, offices, entertainment venues) and household applications (living rooms, bedrooms, kitchens, bathrooms, outdoor residential spaces).

The ecosystem integrates raw material suppliers, fixture designers and manufacturers, light source providers, electrical component manufacturers, brand distribution channels, specification networks, and retail channels spanning big-box home improvement stores, specialty lighting showrooms, luxury furniture retailers, and e-commerce platforms. Macroeconomic factors include rapid urbanization, rising disposable incomes, growing demand for energy-efficient and aesthetically pleasing lighting solutions, and increased construction activities in both residential and commercial sectors.

Market Dynamics

To evaluate market opportunities, Request Sample

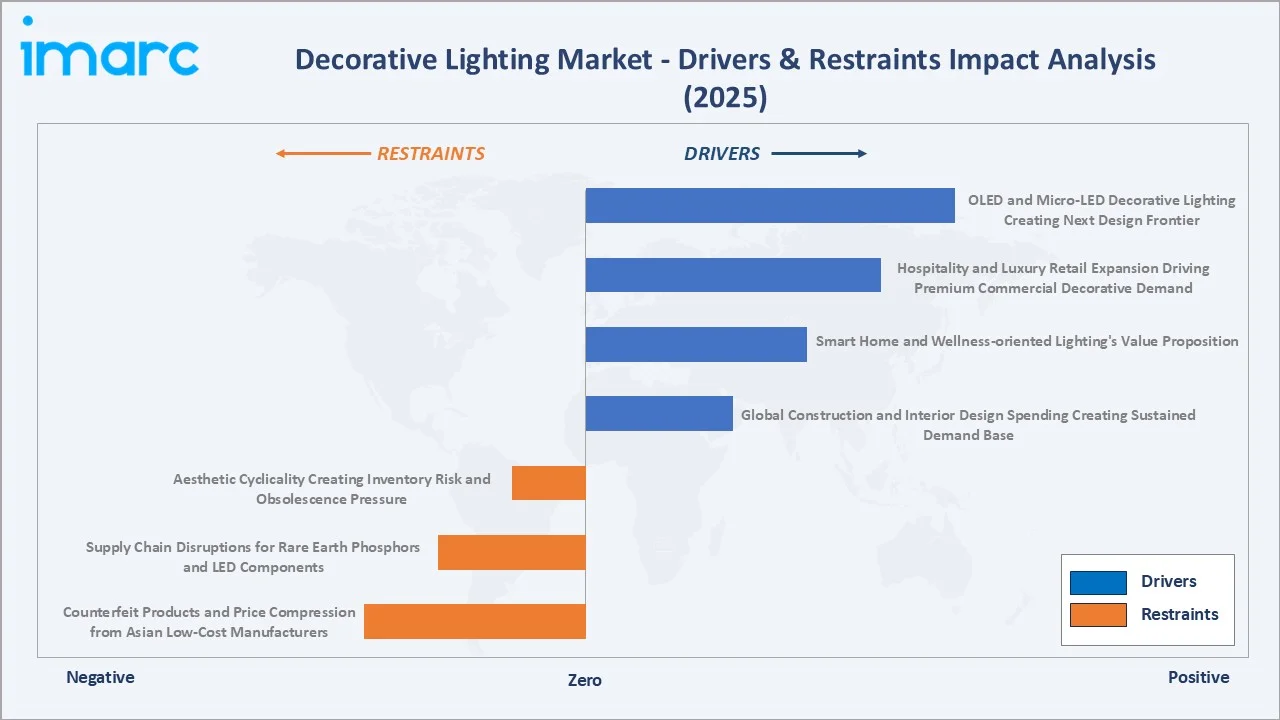

Market Drivers

- Global Construction and Interior Design Spending Creating Sustained Demand Base: Construction spending during January 2026 at a seasonally adjusted annual rate of $2,190.4 billion, with residential and commercial construction generating first-time decorative lighting specification demand for every new building unit.

- Smart Home and Wellness-oriented Lighting's Value Proposition: In June 2024, Signify unveiled NatureConnect, an innovative product designed to improve well-being by simulating natural sunlight indoors. Drawing from biophilic design principles, it supports healthier circadian rhythms, better mood, focus, and sleep quality. This launch is driving the market by meeting the growing demand for wellness-oriented lighting solutions.

- Hospitality and Luxury Retail Expansion Driving Premium Commercial Decorative Demand: Global luxury hotel room supply is expanding, with each luxury hotel room requiring high decorative lighting investment per renovation cycle. Major hotel brands opening new properties generate continuous new commercial decorative specification demand.

Market Restraints

- Counterfeit Products and Price Compression from Asian Low-Cost Manufacturers: The Chinese decorative lighting manufacturing ecosystem produces high-volume imitations of premium Western and European decorative designs at price discounts, available through e-commerce platforms and US/European online retailers. These counterfeit products erode premium brand pricing power, reduce average selling prices across all channels, and create unfair competition for brands investing in design innovation and manufacturing quality.

- Supply Chain Disruptions for Rare Earth Phosphors and LED Components: LED decorative fixtures require rare earth phosphor materials (yttrium, europium, terbium) for white light conversion from blue LED chips, materials primarily sourced from China. Chinese export restrictions on rare earth elements create supply chain vulnerability for LED component manufacturers outside China.

Market Opportunities

- Human-Centric Lighting and Circadian Technology Creating Premium Decorative Segment: Human-Centric Lighting (HCL) commands a premium over conventional LED decorative. Healthcare, education, and senior living facilities are primary commercial HCL adopters, with WELL Building Standard and LEED certification incentivizing HCL investment.

- OLED and Micro-LED Decorative Lighting Creating Next Design Frontier: Organic LED (OLED) panels, providing diffuse, glare-free, ultra-thin light with aesthetic flexibility unavailable from point-source LED, are creating entirely new decorative fixture form factors. OLED panels enable paper-thin luminous ceiling panels, curved decorative surfaces, and transparent light elements that blur the boundary between furniture and lighting.

Market Challenges

- Fragmented Distribution Landscape Creating Channel Management Complexity: Decorative lighting reaches commercial customers through architects' product specifications, interior designers' selections, electrical contractors' installations, hospitality FF&E procurement, and direct-to-contractor dealer programs, each requiring distinct marketing, pricing, and service approaches.

- Aesthetic Cyclicality Creating Inventory Risk and Obsolescence Pressure: Decorative lighting design is subject to interior design trend cycles that make product catalog management challenging.

Emerging Market Trends

1. Smart Decorative Lighting Ecosystems Becoming Mainstream Premium Standard

Smart decorative lighting ecosystems are becoming a mainstream premium standard by integrating advanced technologies such as voice control, automation, and personalized settings. These systems enhance the ambiance and functionality of living and working spaces, appealing to consumers seeking energy-efficient, customizable, and technologically advanced lighting solutions. In February 2026, Govee introduced a new product line designed for home and office spaces. The collection features ceiling lights in multiple colors, gaming lamps, light pillars, and a desk lamp created in partnership with renowned sound company JBL.

2. Designer Collaboration Programs Defining Premium Residential Category

Designer collaboration programs are shaping the premium residential category in the decorative lighting market by offering exclusive, high-quality designs that cater to luxury consumers. These collaborations combine artistic vision with functionality, elevating the aesthetic appeal of lighting fixtures while driving demand for unique, bespoke lighting solutions in upscale residential spaces.

3. Biophilic and Organic Design Aesthetics Driving Material Innovation

Biophilic and organic design aesthetics encourage the use of natural, sustainable materials that promote a connection to nature. This trend is pushing manufacturers to develop eco-friendly, visually appealing lighting solutions that integrate seamlessly into spaces, enhancing well-being and supporting the growing consumer demand for environmentally conscious products.

4. E-Commerce and Digital Visualization Transforming Decorative Lighting Retail

E-commerce and digital visualization are transforming decorative lighting retail by enabling consumers to virtually explore and customize lighting options from the comfort of their homes. This shift enhances the shopping experience, providing convenience, personalized choices, and seamless purchasing, while driving growth in the online lighting market and expanding access to a global customer base.

Industry Value Chain Analysis

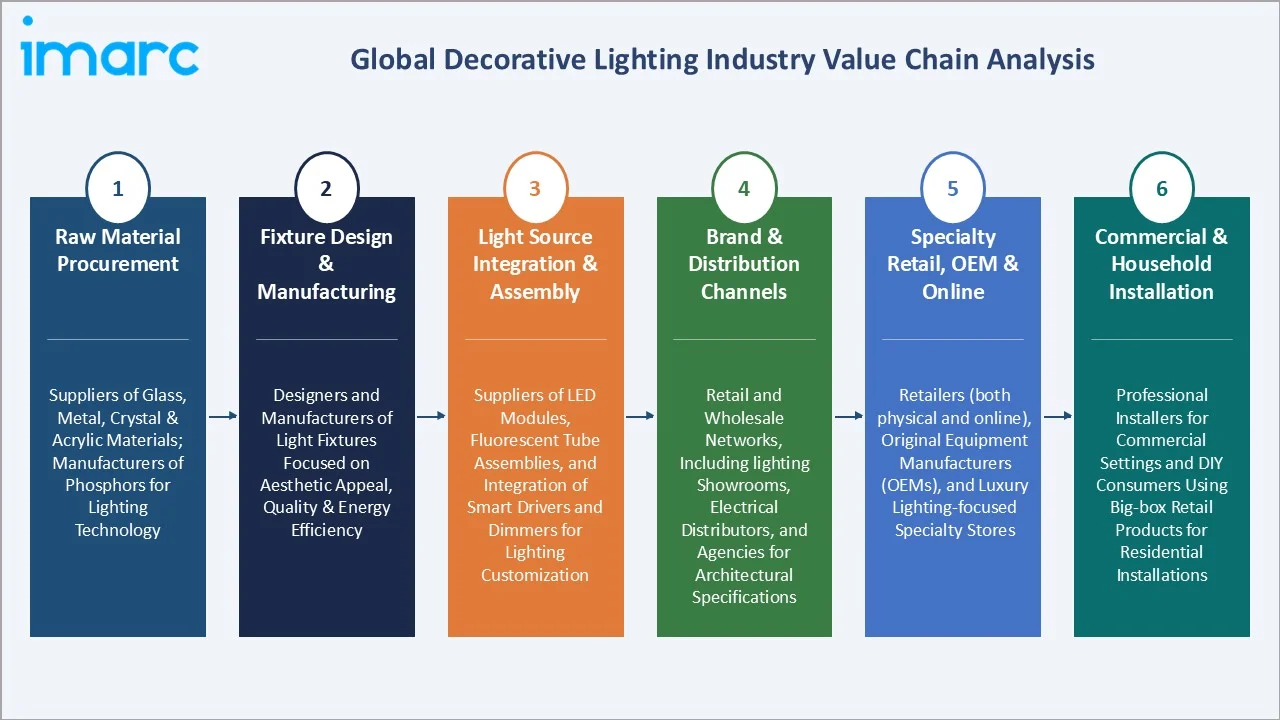

The decorative lighting value chain integrates artisan and industrial raw material processing, fixture design and manufacturing, light source integration, brand distribution through multiple channel types, and commercial or residential installation. Premium decorative manufacturers capture 45-60% gross margins on high-end fixtures; mass-market brands earn 30-40%; and private label offshore production sold through retail captures 20-30% margins. Interior designer specification fees add a 25-35% markup in professional project contexts.

|

Stage |

Key Participants |

|

Raw Material Procurement |

Suppliers of glass, metal, crystal, and acrylic materials; manufacturers of phosphors for lighting technology. |

|

Fixture Design & Manufacturing |

Designers and manufacturers of light fixtures focus on aesthetic appeal, quality, and energy efficiency. |

|

Light Source Integration & Assembly |

Suppliers of LED modules, fluorescent tube assemblies, and integration of smart drivers and dimmers for lighting customization. |

|

Brand & Distribution Channels |

Retail and wholesale networks, including lighting showrooms, electrical distributors, and agencies for architectural specifications. |

|

Specialty Retail, OEM & Online |

Retailers (both physical and online), original equipment manufacturers (OEMs), and luxury lighting-focused specialty stores. |

|

Commercial & Household Installation |

Professional installers for commercial settings and DIY consumers using big-box retail products for residential installations. |

The brand and distribution tier is the decorative lighting value chain's most contested competitive arena. Manufacturers with strong lighting showroom representation gain specification pull from US professional interior designers; those focused on big-box channels sacrifice designer reach for volume.

Technology Landscape in the Decorative Lighting Industry

LED Filament and Warm-Glow Technology Achieving Incandescent Parity

LED filament and warm-glow technology combine the energy efficiency and longevity of LEDs with the aesthetic appeal of traditional incandescent bulbs. These innovations provide a similar warm light output and dimming capabilities, offering consumers a more sustainable, energy-efficient alternative while maintaining the familiar ambiance and aesthetic of incandescent lighting.

Tunable White and Human-Centric LED Systems

Tunable white and human-centric LED systems are transforming the decorative lighting industry by allowing lighting to be adjusted according to the time of day or specific needs, enhancing well-being and productivity. These systems offer customizable color temperatures and brightness levels, promoting healthier circadian rhythms and improving the user experience, making them increasingly popular in both residential and commercial spaces. A recently granted patent from Li presents Artificial Sunlight Lighting, an innovative LED-based system designed to replicate the entire solar spectrum indoors, including the red and infrared wavelengths crucial for mitochondrial function and cellular energy.

Smart Control Integration and Wireless Protocols

Smart control integration and wireless protocols enable seamless connectivity and automation. These technologies allow users to control lighting remotely through apps or voice commands, integrating with smart home systems. Wireless protocols such as Zigbee, Bluetooth, and Wi-Fi offer flexibility, energy efficiency, and enhanced user experience, driving the growth of smart lighting solutions in both residential and commercial markets.

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Sconce |

34,7% |

2025 |

|

Light Source |

LED |

39.8% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

End User |

Commercial |

62.8% |

2025 |

|

Region |

North America |

37.6% |

2025 |

By Light Source

LED leads at 39.8% market share (2025). LED decorative fixtures span the full product range, from LED pendants to custom hotel chandelier LED systems. LED's dominant growth trajectory stems from the convergence of regulatory phase-out of alternatives (fluorescent, halogen, inefficient incandescent), aesthetic maturation achieving incandescent color rendering quality, and economic advantages of energy savings and 15-25 year lamp life, eliminating relamping labor costs. LED grows at ~3.8% CAGR (2026-2034).

Fluorescent at 28.5% is declining under mandatory EU phase-out pressure and US efficiency standard enforcement. Legacy fluorescent decorative installations in offices, schools, and commercial buildings are creating a retrofit market converting to LED, sustaining total market revenues as unit counts decline, but average LED fixture values increase. Incandescent at 21.4% serves a premium residential niche where authenticity justifies efficiency compromise. Others at 10.3% includes halogen decorative, neon, and emerging OLED technologies.

By End User

Commercial end users lead at 62.8% market share (2025). Commercial decorative lighting encompasses hotel guest rooms and public areas, restaurant and café lighting, luxury retail store environments, office reception and common areas, entertainment venues, casinos, places of worship, and healthcare facility public spaces. Commercial buyers are specification-driven through architects, interior designers, and lighting designers whose recommendations create high-value, large-format decorative lighting contracts.

Household at 37.2% is driven by residential construction, renovation, and the growing consumer willingness to invest in premium decorative lighting as a self-expression medium. Online platforms are driving household segment growth by making premium decorative lighting accessible without specialty showroom visits.

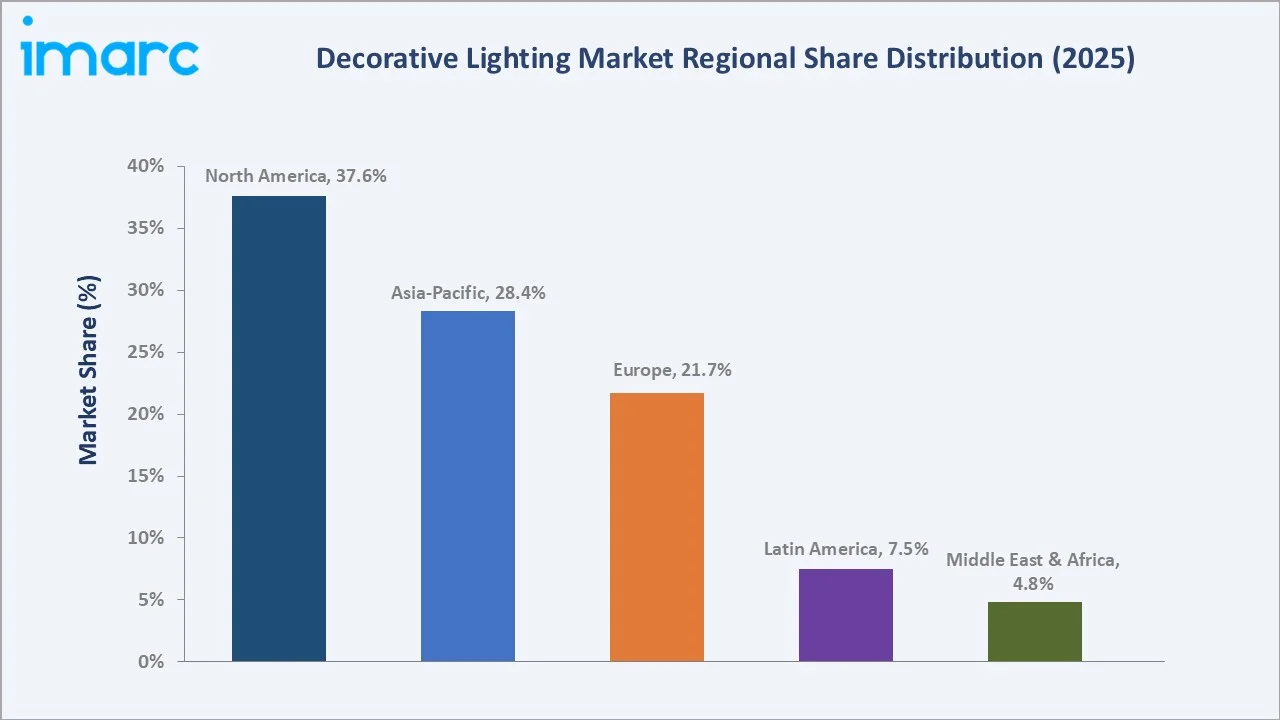

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

North America |

37.6% |

Strong demand driven by housing construction, home renovation, and commercial development. Key drivers include energy-efficient lighting, LED adoption, and premium lighting solutions for residential, commercial, and hospitality sectors. |

|

Asia-Pacific |

28.4% |

Fastest-growing region, driven by rapid urbanization, rising disposable incomes, and the demand for modern lighting solutions in both residential and commercial spaces, particularly in China and India. |

|

Europe |

21.7% |

Growth driven by stringent architectural and hospitality lighting regulations, with a focus on energy-efficient and high-quality lighting solutions for commercial and residential buildings. |

|

Latin America |

7.5% |

Driven by Brazil’s large-scale construction projects, increasing urbanization, and demand for decorative lighting in the hospitality and residential sectors. |

|

Middle East & Africa |

4.8% |

Growth is supported by rapid urbanization and the development of luxury hospitality and commercial spaces, particularly in the UAE and Saudi Arabia. |

North America's 37.6% leadership reflects the US housing market's exceptional breadth and renovation cycle depth. The high number of US housing units undergo on average one decorative lighting upgrade cycle every 8-12 years, creating a perpetual replacement market of fixture replacements independent of new construction activity. This installed base replacement demand provides a resilient revenue foundation that buffers the decorative lighting market against new construction cyclicality.

Asia-Pacific's 28.4% is growing fastest as China's interior design industry elevates domestic decorative lighting quality standards and price points. Indian premium residential and hospitality expansion is specifying global decorative lighting brands rather than domestic low-cost alternatives.

Competitive Landscape

The decorative lighting market is highly fragmented, with thousands of brands operating across premium, mid-market, and value segments across every geographic market. Signify commands the largest individual market share through its global LED technology and distribution infrastructure, but in the premium decorative design segment commands disproportionate value capture despite smaller unit volumes.

|

Company Name |

Brands |

Market Position |

Core Strength |

|

Signify Holding |

Signify Dynalite, Philips Hue, Color Kinetics, EcoLink |

Market Leader |

Signify is the world leader in lighting, providing professional customers and consumers with quality products, systems and services. |

|

Acuity Inc. |

Aculux, Cyclone, Eureka, Gotham, Holophane, Hydrel, Juno, Lithonia Lighting, Luminaire LED, Luminis, Mark Architectural Lighting |

Market Leader |

Acuity’s luminaires deliver exceptional performance and aesthetic appeal, while the electronics portfolio, featuring drivers and a leading controls platform, ensures seamless connectivity and superior functionality. |

|

WAC Group |

WAC LIGHTING, WAC ARCHITECTURAL, MODERN FORMS, SCHONBEK |

Strong Challenger |

As a leader in the lighting industry, WAC Group prioritize innovation and advancing technology in automation and controls to deliver smart, sustainable and beautifully designed products. |

|

Maxim Lighting |

ET2 Contemporary Lighting |

Niche Player |

California-based residential and commercial decorative company |

|

Hinkley, Inc. |

FREDRICK RAMOND, LARK, HINKLEY |

Niche Player |

Hinkley is a 4th-generation family company and has been around for over 100 years, creating thoughtful designs with the same quality and style as its own homes. |

The competitive landscape is bifurcated between technology-led companies competing on LED innovation, smart home integration, and global distribution scale, and design-led companies competing on aesthetic differentiation, designer collaboration, and premium brand positioning.

Key Company Profiles

Signify Holding

Signify is the global leader in lighting, offering high-quality products, systems, and services to both professional customers and consumers. The company’s connected lighting solutions bring light and data to devices, spaces, and people, transforming the way light is used.

- Brands: Signify Dynalite, Philips Hue, Color Kinetics, EcoLink.

- Recent Developments: In October 2025, Signify launched the Philips Aura Floodlight, a market-first innovation that blends professional-grade illumination with cultural and festive aesthetics.

- Strategic Focus: Delivering innovative, energy-efficient, and aesthetically appealing lighting solutions.

Acuity Inc.

Acuity offers a blend of innovative luminaires and advanced electronics. The company’s luminaires provide outstanding performance and visual appeal, while their electronics portfolio, including drivers and a leading controls platform, guarantees seamless connectivity and enhanced functionality. Together, these components create the foundation for all-encompassing lighting solutions.

- Brands: Aculux, Cyclone, Eureka, Gotham, Holophane, Hydrel, Juno, Lithonia Lighting, Luminaire LED, Luminis, Mark Architectural Lighting.

- Recent Developments: In September 2025, Eureka launched its Jarry luminaire. Jarry is a classic ball and seamless tube design, available in dozens of configurations to create many moods and looks.

- Strategic Focus: Integrating innovative design with advanced lighting technology, offering energy-efficient, aesthetically pleasing solutions.

Market Concentration Analysis

The decorative lighting market is highly fragmented compared to functional lighting categories. The top 5 companies identified in this report collectively represent approximately 25-30% of total global market revenues, with the remaining 70-75% distributed among thousands of regional manufacturers, specialty boutique brands, private label producers, and emerging market manufacturers in China, India, and other regions. This extreme fragmentation reflects the decorative lighting category's dual aesthetic-functional character, which supports premium niche brand differentiation that resists the consolidation typical in purely functional product categories.

Design-driven premium segments are highly concentrated among established design brands, while value segments are highly fragmented among Chinese manufacturers exporting through global e-commerce channels. European premium brands command disproportionate value share in their geographic markets and in global luxury specification.

Investment & Growth Opportunities

Fastest Growing Segments

LED light source (~3.8% CAGR), others including OLED/Micro-LED (~3.2% CAGR), commercial end user (~3.0% CAGR), smart decorative lighting (~12%+ CAGR within LED segment from small base), and Asia-Pacific designer decorative collections (~5-6% CAGR in premium tier) represent the global decorative lighting market's highest-growth investment vectors through 2034.

Emerging Market Opportunities

India's premium residential and hospitality decorative lighting market is growing at 8-10% annually, creating a near-term opportunity for international brands establishing local specification relationships with Indian interior designers and hospitality FF&E procurement teams. Southeast Asian luxury hospitality presents similar high-growth premium decorative specification opportunities as the expansion of 5-star hotel pipelines. These markets are currently served primarily by Chinese mid-market imports and indirect European brand distribution.

Investment Themes

- Designer collaboration brand development: Developing designer partnerships with emerging interior design talent in Asia-Pacific and European markets creates locally relevant premium decorative brands with authentic aesthetic credentials, the primary barrier to entry for international brands in culturally distinctive Asian and European residential design markets.

- Smart decorative ecosystem platform investment: The convergence of Matter protocol, voice control, and circadian wellness lighting creates a smart decorative platform opportunity where manufacturers can build recurring software/services revenue alongside hardware.

Future Market Outlook (2026-2034)

The global decorative lighting market is projected to grow from USD 43.95 Billion in 2025 to USD 56.43 Billion by 2034, delivering a 2.82% CAGR over the forecast period. The market's anchor value of USD 50.50 Billion in 2030 reflects a decorative lighting industry at a pivotal technological and aesthetic inflection point, LED having achieved near-complete dominance in new installations and retrofits, smart decorative lighting transitioning from premium niche to mainstream residential standard, and new light source technologies beginning commercial deployments that will define the market's aesthetic possibilities for the 2030-2040 decade.

Three structural forces define the decorative lighting market's trajectory with high certainty through 2034: regulatory phase-out of fluorescent and incandescent technologies creating mandatory LED conversion spending that sustains market revenues even in periods of weak new construction activity; the smart home revolution's intersection with decorative lighting through Matter protocol standardization enabling cross-ecosystem compatibility that will drive smart decorative penetration from premium residential sales; and Asia-Pacific's secular growth in premium interior design spending as China's middle class expands and India's urbanization creates new urban consumers capable of premium decorative lighting purchases.

Research Methodology

Primary Research

Primary research comprised structured interviews with 65+ industry stakeholders (2025), including VP product development executives; interior design principals from American Society of Interior Designers (ASID) member firms; architectural lighting designers from IALD (International Association of Lighting Designers) member practices; buyer category managers from Home Depot and Lowe's lighting departments; and luxury hospitality FF&E procurement directors from Marriott Bonvoy and Hyatt Hotels procurement teams.

Secondary Research

Secondary research encompassed American Lighting Association (ALA) industry data and member surveys 2025, US Census Bureau residential construction and renovation statistics, EU Regulation 2023/826 compliance data, DOE LED lighting facts product database, National Association of Home Builders (NAHB) remodeling market data, IIDA Hospitality Interior Design research, Houzz annual home trends report 2025, Wayfair and Amazon marketplace category data, company investor presentations and annual reports. Over 100 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up light source x end user segmental models calibrated against ALA industry shipment data, US DOE residential and commercial building stock data, LED conversion rate assumptions by segment, and hospitality pipeline construction data from STR Global. Key inputs include US housing starts and renovation spending projections, EU Regulation compliance timeline impacts on fluorescent-to-LED conversion, Asia-Pacific construction output projections, smart decorative lighting adoption S-curve modeling based on smart home platform penetration data, and global luxury hospitality pipeline data.

Decorative Lighting Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Chandelier, Pendant, Sconce, Flush Mount, Ceiling Mount, Wall Mount, Others |

| Light Sources Covered | LED, Fluorescent, Incandescent, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, Online Stores, Others |

| End Users Covered | Commercial, Household |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Signify Holding, Acuity Inc., WAC Group, Maxim Lighting, Hinkley, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the decorative lighting market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global decorative lighting market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the decorative lighting industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Decorative Lighting Market Report

The global decorative lighting market reached USD 43.95 Billion in 2025, driven by residential renovation spending, commercial hospitality refurbishment, LED adoption, and smart home integration creating premium product demand across commercial and household end users.

The market grows at 2.82% CAGR during 2026-2034, reaching USD 56.43 Billion by 2034, driven by LED regulatory conversion mandates, smart decorative mainstream adoption, Asia-Pacific interior design market expansion, and hospitality sector refurbishment cycles.

LED leads at 39.8% (2025) and grows fastest at ~3.8% CAGR, driven by EU fluorescent ban, US DOE efficiency standards, aesthetic maturation with warm-glow filament LED achieving incandescent visual parity, and energy savings compelling commercial operator conversion from incandescent and fluorescent decorative.

Commercial leads at 62.8%, reflecting hospitality, luxury retail, and restaurant sectors' premium decorative spending per fixture for lobby chandeliers, restaurant pendant systems, and retail accent lighting specified by architects and interior designers in multi-fixture project contracts.

North America leads at 37.6%, anchored by US housing units generating high annual fixture replacement demand, the home renovation market, and the world's largest commercial hospitality and luxury retail market specifying premium decorative fixtures.

Leading companies include Signify Holding, Acuity Inc., WAC Group, Maxim Lighting, and Hinkley, Inc., among others.

The market is projected to reach approximately USD 50.50 Billion by 2030, driven by LED completing market light source transition at new installations, matter-enabled smart decorative for US premium residential, and hospitality renovation cycles generating high annual hotel decorative procurement.

LED grows at ~3.8% CAGR driven by general service lamp efficiency standards, warm-glow filament LED achieving incandescent aesthetic parity, energy savings creating commercial operator economic conversion compulsion, and 15-25 year lamp life eliminating commercial relamping costs.

Matter protocol standardization enables cross-ecosystem smart decorative compatibility, removing brand lock-in barriers.

OLED and Micro-LED decorative applications represent the most technically innovative emerging segment, enabling paper-thin luminous ceiling panels, curved decorative surfaces, and transparent light elements commanding high in luxury hospitality and premium residential applications.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)