Depression Drugs Market Size, Share, Trends and Forecast by Drug Class, Disorder Type, Drug Type, Distribution Channel, and Region, 2026-2034

Depression Drugs Market Size, Share, Trends & Forecast (2026-2034)

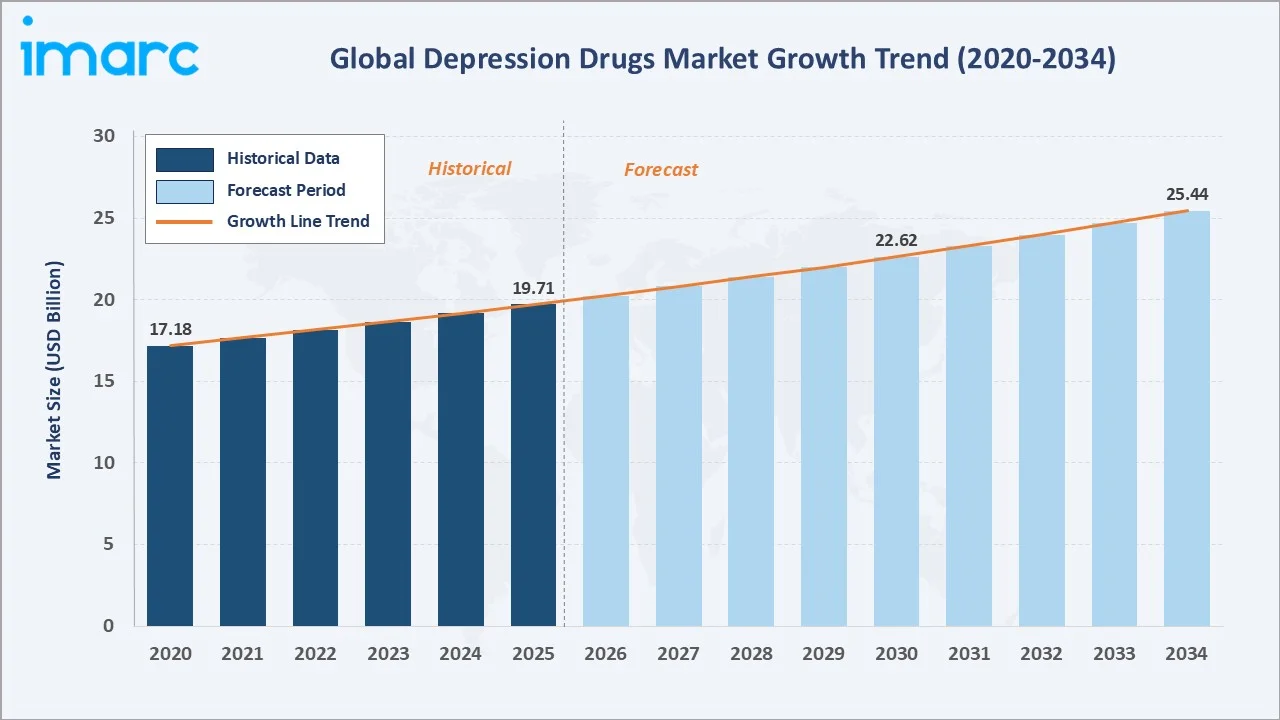

The global depression drugs market reached USD 19.71 Billion in 2025 and is projected to reach USD 25.44 Billion by 2034, exhibiting a CAGR of 2.79% during 2026-2034. Growth is anchored by the rising global prevalence of mental health disorders including major depressive disorder (MDD), generalized anxiety disorder (GAD), and obsessive-compulsive disorder (OCD), an active pipeline of novel mechanism antidepressants, and expanding online pharmacy access to prescription mental health therapies.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 19.71 Billion |

|

Market Forecast (2034) |

USD 25.44 Billion |

|

CAGR (2026-2034) |

2.79% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

The global depression drugs market is expanding as the prevalence of mental health disorders, including major depressive disorder, anxiety, and related conditions, continues to rise worldwide. Increasing awareness of mental health, better diagnostic capabilities, and reduced stigma are driving more patients to seek pharmacological treatment.

To get more information on this market, Request Sample

The market includes a range of antidepressants such as selective serotonin reuptake inhibitors (SSRIs), serotonin-norepinephrine reuptake inhibitors (SNRIs), tricyclic antidepressants, monoamine oxidase inhibitors, and novel rapid-acting therapies.

Executive Summary

The global depression drugs market accounted for USD 19.71 Billion in 2025 and is expected to reach USD 25.44 Billion by 2034. It is a mature, regulated therapeutic category supported by sustained global prevalence of depressive and anxiety disorders, ongoing innovation in novel mechanisms of action including esketamine and dextromethorphan-bupropion combinations, and a robust generic pipeline maintaining patient access.

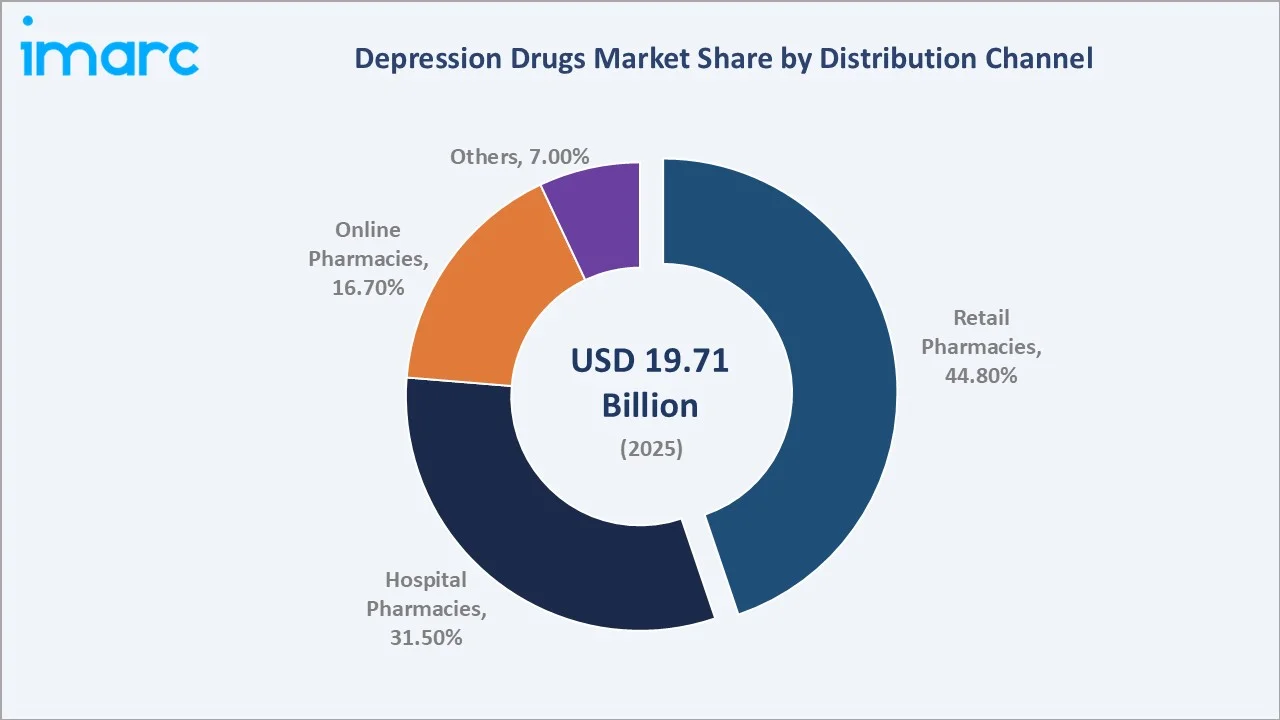

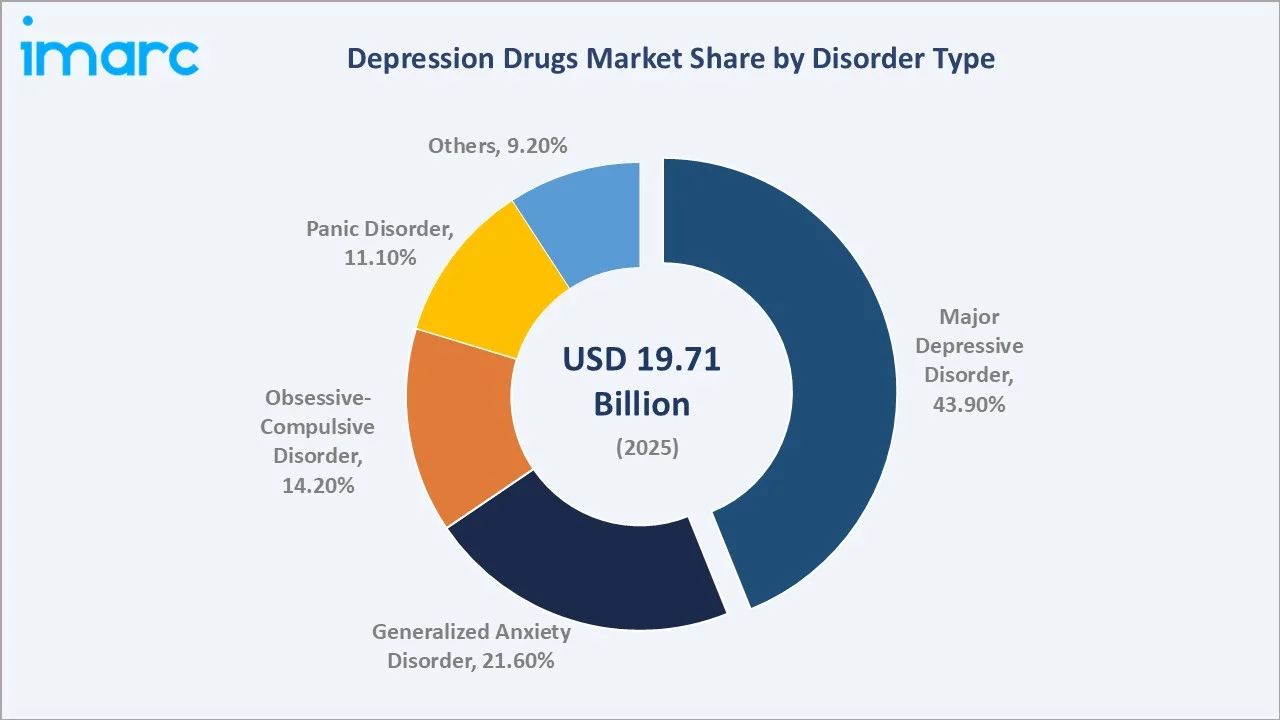

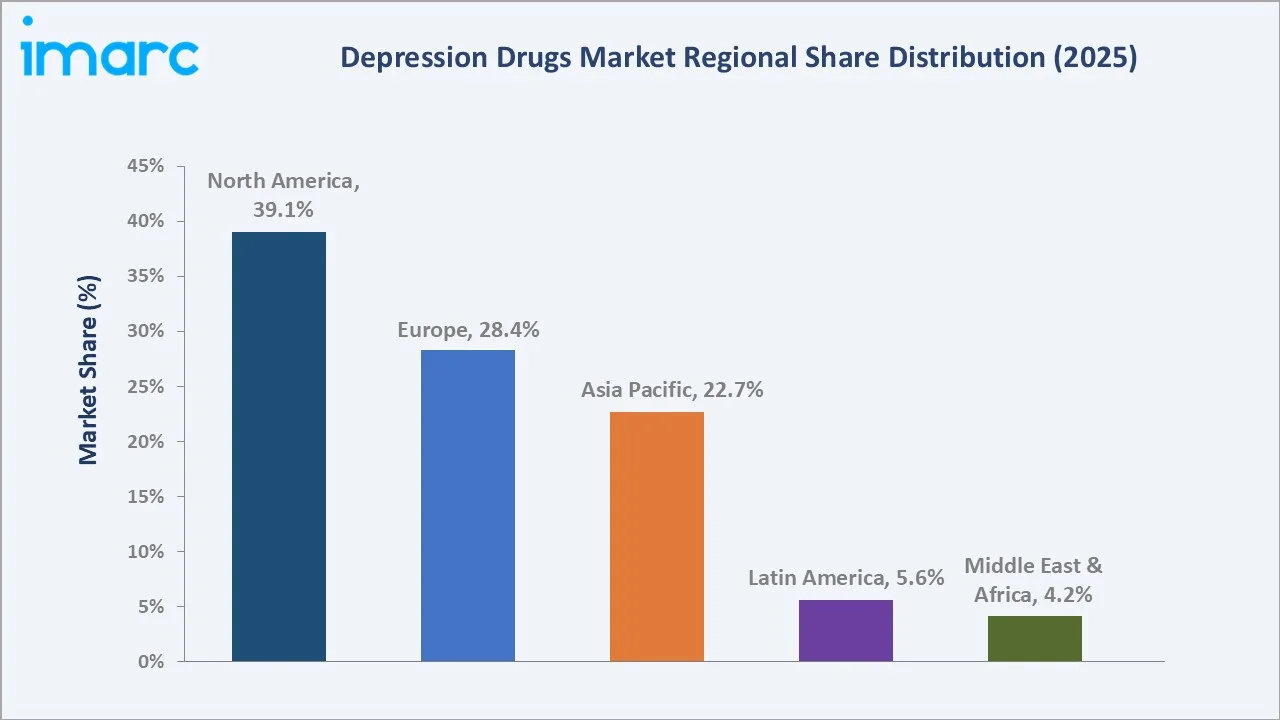

The market is dominated by established multinational pharmaceutical companies including Pfizer Inc., Eli Lilly and Company, Johnson & Johnson, and AbbVie Inc, with SSRIs and SNRIs representing the largest drug classes. Retail pharmacies dominate the distribution mix at 44.8% in 2025, major depressive disorder leads the disorder type segmentation at 43.9%, and North America anchors regional share at 39.1%.

Key milestones include the April 2025 Johnson & Johnson’s acquisition of Intra‑Cellular Therapies, Inc. to strengthen its neuroscience portfolio; Alto Neuroscience’s approximately USD 60 million in additional financing for supporting ongoing development of four Phase 2 clinical programs across multiple central nervous system indications; and Otsuka and H. Lundbeck A/S’s U.S. FDA approval in May 2023 of a supplemental New Drug Application (sNDA) for REXULTI (brexpiprazole), treating agitation associated with dementia due to Alzheimer’s disease.

Key Market Insights

|

Indicator |

Value (2025) |

|

Leading Distribution Channel |

Retail Pharmacies (44.8%) |

|

Leading Disorder Type |

Major Depressive Disorder (43.9%) |

|

Fastest-Growing Distribution Channel |

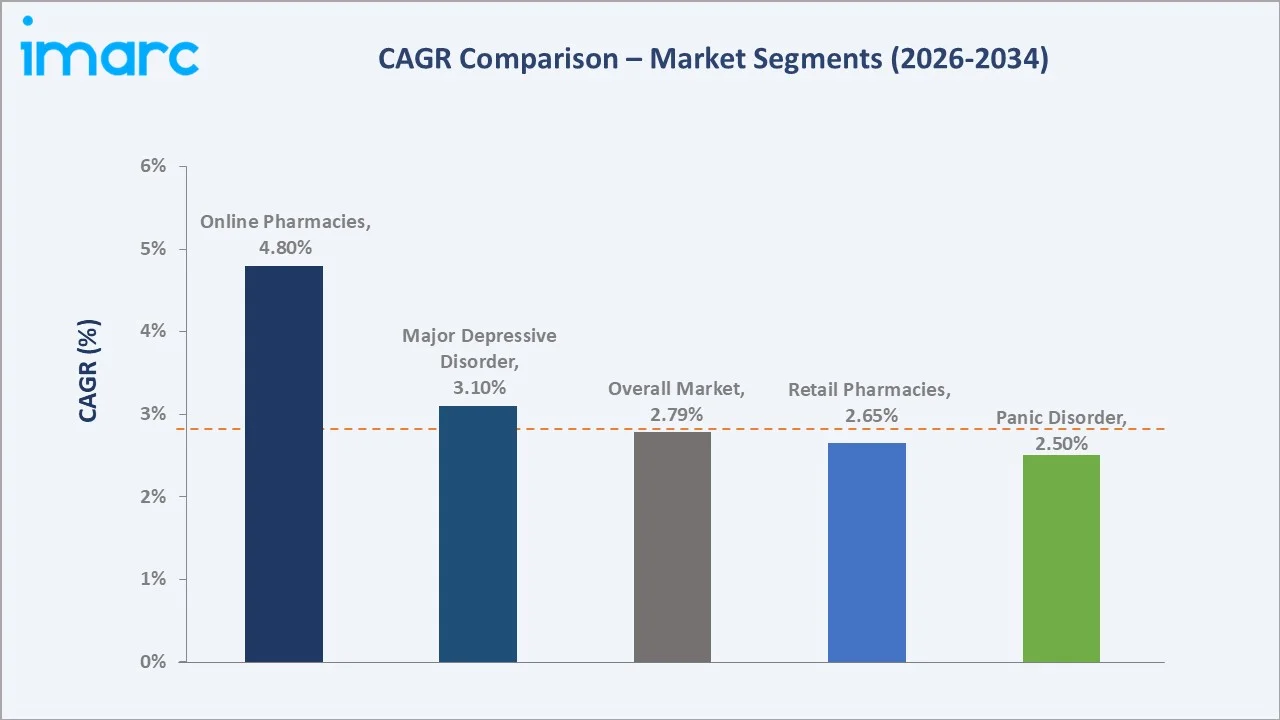

Online Pharmacies (~4.8% CAGR) |

|

Largest Region |

North America (39.1%) |

|

Key Players |

Pfizer Inc., Eli Lilly and Company, Johnson & Johnson, AbbVie Inc. |

Key Analytical Observations Supporting the Above Data:

- Retail pharmacies account for 44.8% of the depression drugs market in 2025, reflecting traditional dispensing dominance for SSRIs, SNRIs, and atypical antidepressants. Hospital pharmacies at 31.5% (2025) serve inpatient psychiatric care and acute treatment-resistant depression therapies including esketamine.

- Online pharmacies at 16.7% (2025) are the fastest-growing distribution channel, projected to grow at approximately 4.8% CAGR through 2034, driven by direct-to-consumer telehealth-pharmacy integrations, refill convenience, and rising acceptance of digital mental health workflows.

- Major depressive disorder leads the disorder type segmentation at 43.9% in 2025, reflecting the World Health Organization estimate that depression affects approximately 332 million people globally and continues to grow as the leading cause of disability worldwide.

- Generalized anxiety disorder at 21.6%, obsessive-compulsive disorder at 14.2%, and panic disorder at 11.1% reflect overlapping pharmacotherapy with SSRIs and SNRIs, while others at 9.2% include post-traumatic stress disorder, seasonal affective disorder, and premenstrual dysphoric disorder.

- North America's 39.1% regional share reflects the United States as the largest single-country market, supported by a sophisticated mental health treatment ecosystem, comprehensive insurance coverage, and the global headquarters of leading depression drug developers including Pfizer Inc., Eli Lilly and Company, and Johnson & Johnson.

Depression Drugs Market Overview

Depression drugs are pharmaceutical agents used to treat major depressive disorder, anxiety disorders, obsessive-compulsive disorder, panic disorder, post-traumatic stress disorder, and related mood and anxiety conditions.

The category spans selective serotonin reuptake inhibitors (SSRIs), serotonin-norepinephrine reuptake inhibitors (SNRIs), tricyclic and tetracyclic antidepressants, monoamine oxidase inhibitors (MAOIs), atypical antidepressants, and emerging novel mechanism therapies including esketamine nasal sprays and rapid-acting oral combinations.

The market is highly regulated, with FDA, EMA, PMDA, and equivalent national agencies overseeing approvals, labelling, and post-market safety. SSRIs and SNRIs remain the largest drug classes, with treatment guidelines from the American Psychiatric Association, NICE, and equivalent bodies positioning them as first-line therapy.

Novel mechanisms targeting treatment-resistant depression, including esketamine, dextromethorphan-bupropion combinations, and emerging psilocybin-based therapeutics, represent the highest-growth innovation frontier.

Market Dynamics

To evaluate market opportunities, Request Sample

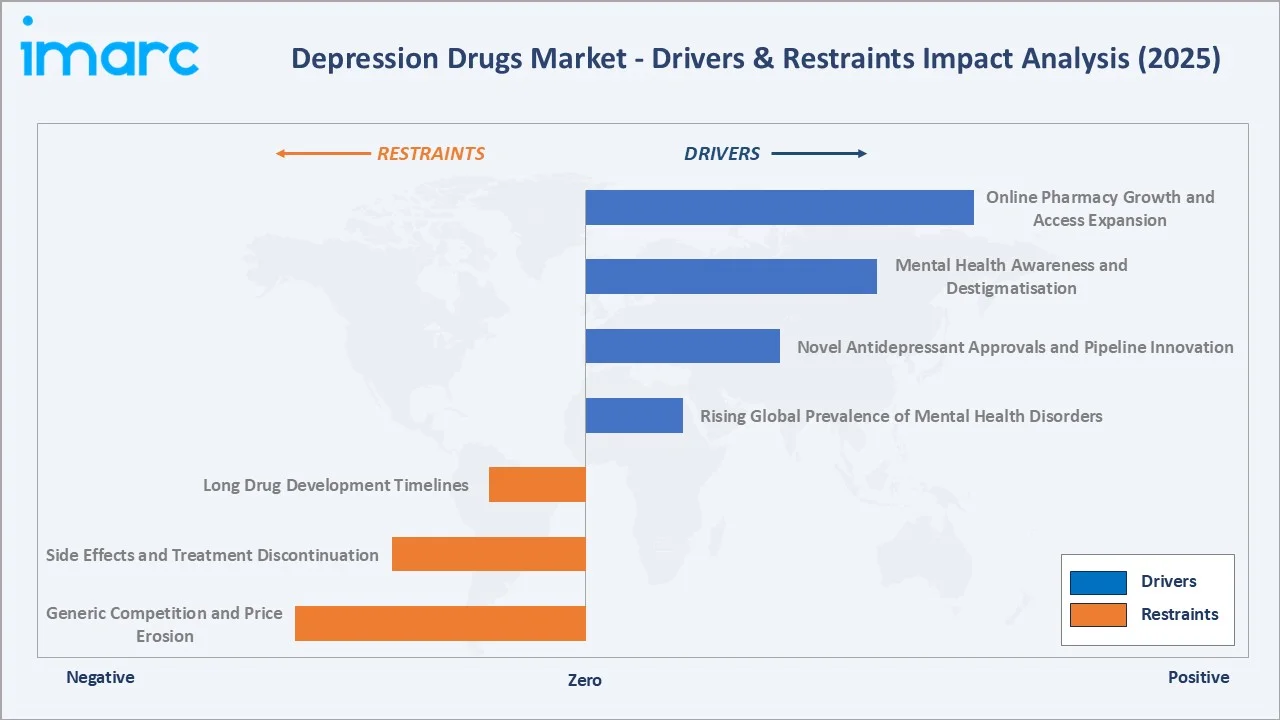

Market Drivers

- Rising Global Prevalence of Mental Health Disorders: The World Health Organization estimates depression affects approximately 332 million people globally, with the COVID-19 pandemic accelerating mental health crisis trajectories.

- Novel Antidepressant Approvals and Pipeline Innovation: In December 2025, Shionogi & Co., Ltd. announced that it has received approval to manufacture and market “ZURZUVAE Capsules 30 mg” in Japan. The capsule is used for the treatment of major depressive disorder based on positive Phase 3 trial results showing rapid symptom improvement.

- Mental Health Awareness and Destigmatisation: Growing public awareness, employer mental health programs, government campaigns, and integration of mental health screening into primary care are expanding diagnosed populations.

- Online Pharmacy Growth and Access Expansion: Direct-to-consumer telehealth-pharmacy integrations are expanding patient access to prescription antidepressants. Online pharmacy channels are projected to grow at approximately 4.8% CAGR through 2034, supported by refill convenience, telemedicine prescribing, and pharmacy benefit manager partnerships.

Market Restraints

- Generic Competition and Price Erosion: Most leading SSRIs and SNRIs are off-patent, with generic alternatives capturing the majority of dispensed volumes at significantly reduced prices. Generic substitution and pharmacy benefit manager formularies continue to compress revenue growth despite rising prescription volumes.

- Side Effects and Treatment Discontinuation: Antidepressants are associated with a range of side effects including weight gain, sexual dysfunction, and discontinuation syndrome. Based on contemporary data from the past decade, roughly 50% of psychiatric patients and 50% of primary care patients discontinue antidepressant therapy prematurely, showing nonadherence when evaluated six months after treatment initiation.

- Long Drug Development Timelines: Novel mechanism antidepressant development typically requires 10-15 years from discovery to approval, with central nervous system clinical trials facing high attrition and placebo response challenges. Regulatory and reimbursement pathways for novel mechanisms remain complex.

Market Opportunities

- Treatment-Resistant Depression and Novel Mechanisms: Treatment-resistant depression affects approximately 30% of major depressive disorder patients, creating significant opportunity for novel mechanism therapies. Esketamine nasal spray, dextromethorphan-bupropion combinations, and emerging psilocybin and neurosteroid-based therapeutics target this high unmet need population.

- Precision Psychiatry and Pharmacogenomics: Alto Neuroscience's precision medicine approach and broader pharmacogenomic-guided prescribing offer opportunity to improve response rates and reduce side effects. Biomarker-guided treatment selection represents a structural shift in mental health pharmacotherapy.

Market Challenges

- Regulatory Complexity for Novel Mechanisms: Approval pathways for novel mechanism antidepressants, including psychedelic-assisted therapies, face complex regulatory requirements across FDA, EMA, and national agencies. REMS programs for esketamine and similar agents add operational complexity for dispensing and clinical administration.

- Stigma and Access Inequalities: Despite progress in destigmatisation, mental health treatment access remains uneven globally. Low-income populations, rural residents, and emerging markets face structural barriers to diagnosis, treatment initiation, and adherence support.

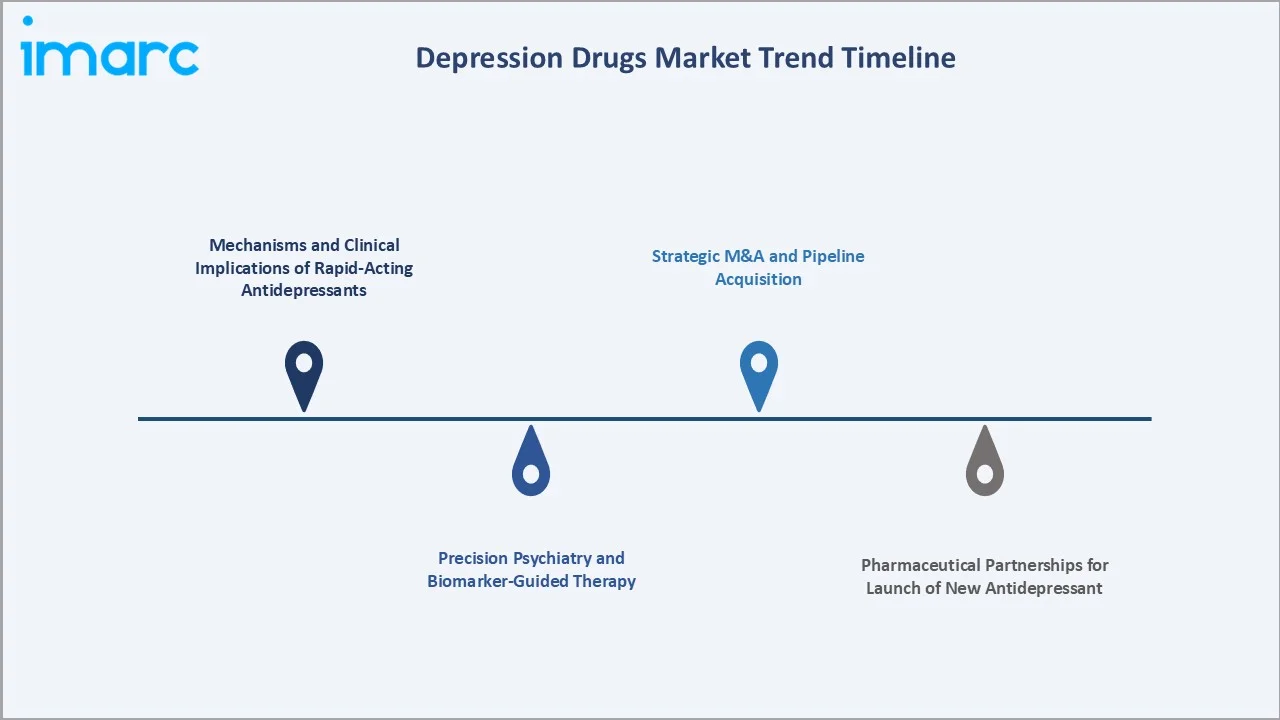

Emerging Market Trends

1. Mechanisms and Clinical Implications of Rapid-Acting Antidepressants

The 2023 study review concluded that ketamine provides rapid antidepressant effects through novel synaptic signaling mechanisms, including NMDA receptor blockade, glutamate surge, BDNF-TrkB activation, and AMPA receptor involvement. These findings highlight a shift from traditional monoamine-based depression models toward targeting synaptic plasticity and circuit-level mechanisms.

2. Strategic M&A and Pipeline Acquisition

In April 2026, Rubicon Research Limited acquired Arinna Lifesciences for about INR 175 crore. This marks its strategic entry into the Indian central nervous system (CNS) formulations market with access to over 60 chronic therapy brands spanning antiepileptics, antidepressants/thymoleptics, antipsychotics, among others. Strategic M&A and pipeline acquisition continue as established pharma companies seek to refresh portfolios facing generic erosion.

3. Pharmaceutical Partnerships for Launch of New Antidepressant

In February 2026, Lupin signed a license and supply agreement with Spektus Pharma to commercialize the novel antidepressant DeslaFlex in Canada. It combines Lupin’s Canadian commercial presence with Spektus’s formulation expertise. The collaboration aims to strengthen Lupin’s central nervous system (CNS) portfolio and offer Canadian patients and clinicians additional options for managing major depressive disorder.

4. Precision Psychiatry and Biomarker-Guided Therapy

Alto Neuroscience raised about USD 60 million in new capital, boosting total equity to roughly USD 100 million since its inception, with strategic backing from Alpha Wave Ventures. This financing, along with a flexible credit line, will enable the company to advance four novel CNS drug candidates through Phase 2 readouts and further refine its biomarker‑driven psychiatry approach.

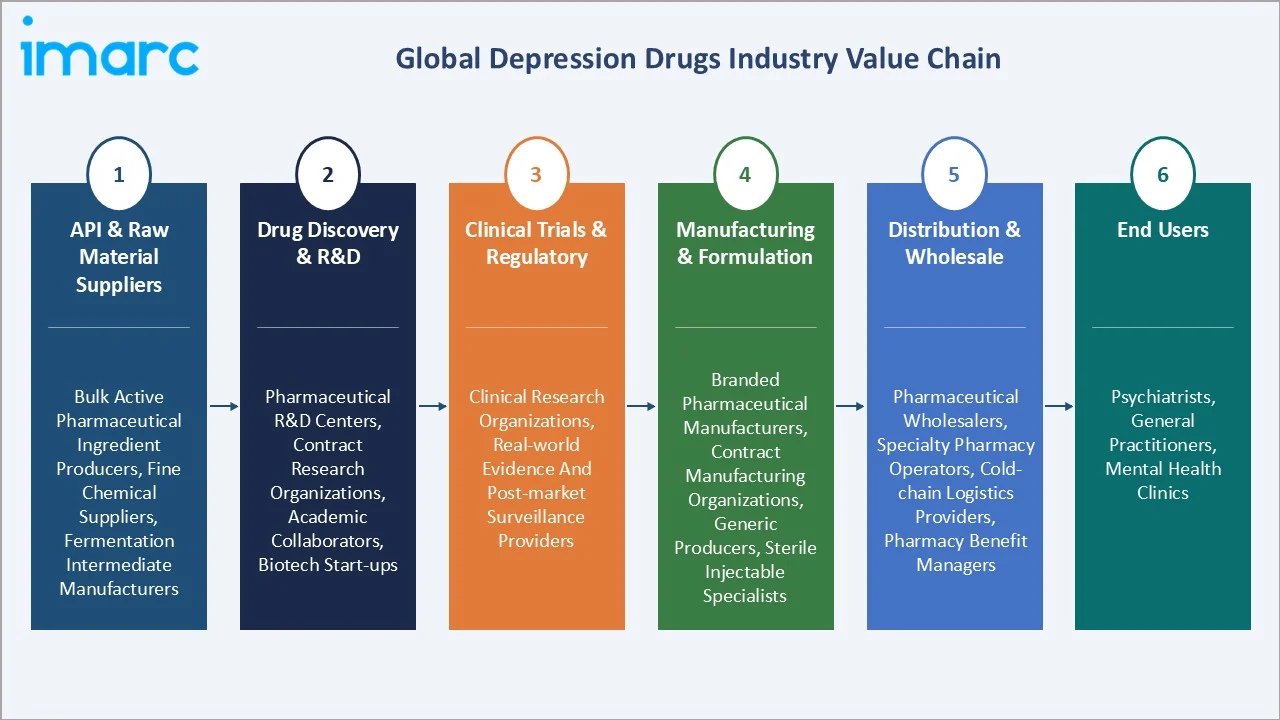

Industry Value Chain Analysis

|

Stage |

Key Players / Activities |

|

API & Raw Material Suppliers |

Bulk active pharmaceutical ingredient producers, fine chemical suppliers, fermentation intermediate manufacturers |

|

Drug Discovery & R&D |

Pharmaceutical R&D centers, contract research organizations, academic collaborators, biotech start-ups |

|

Clinical Trials & Regulatory |

Clinical research organizations, real-world evidence and post-market surveillance providers |

|

Manufacturing & Formulation |

Branded pharmaceutical manufacturers, contract manufacturing organizations, generic producers, sterile injectable specialists |

|

Distribution & Wholesale |

Pharmaceutical wholesalers, specialty pharmacy operators, cold-chain logistics providers, pharmacy benefit managers |

|

End Users |

Psychiatrists, general practitioners, mental health clinics |

Technology Landscape in the Depression Drugs Industry

SSRIs and SNRIs

Selective serotonin reuptake inhibitors and serotonin-norepinephrine reuptake inhibitors remain first-line therapy across major depressive disorder, generalized anxiety disorder, obsessive-compulsive disorder, and panic disorder. SSRIs and SNRIs account for the majority of dispensed volumes, with extensive generic competition and continued reformulation innovation including extended-release and orally disintegrating formats.

Atypical Antidepressants and Augmentation Therapies

Atypical antidepressants including bupropion, mirtazapine, vortioxetine, and vilazodone serve patients with treatment intolerance to SSRIs or specific symptom profiles. Atypical antipsychotics including Rexulti and Abilify serve as adjunctive augmentation therapies. In May 2023, Otsuka and H. Lundbeck A/S announced that the US FDA has approved a supplemental application for REXULTI (brexpiprazole) for Alzheimer's agitation.

Novel Mechanism and Rapid-Acting Therapies

Esketamine nasal spray (Spravato by Johnson & Johnson) anchors the rapid-acting treatment-resistant depression category, administered under REMS programs in healthcare settings. Dextromethorphan-bupropion combinations and emerging psilocybin-based therapeutics from COMPASS Pathways and atai Life Sciences represent the novel mechanism frontier.

Precision Psychiatry and Biomarker-Guided Therapy

Precision psychiatry platforms use EEG biomarkers, pharmacogenomic profiling, and machine learning to guide treatment selection. Alto Neuroscience's biomarker-led approach exemplifies the emerging segment, while pharmacogenomic testing supports SSRI and SNRI prescribing in clinical practice.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Distribution Channel | Retail Pharmacies | 44.8% | 2025 |

| Disorder Type | Major Depressive Disorder | 43.9% | 2025 |

| Drug Class | 🔒 | 🔒 | 2025 |

| Drug Type | 🔒 | 🔒 | 2025 |

| Region | North America | 39.1% | 2025 |

By Distribution Channel

Retail pharmacies dominate with a 44.8% share in 2025, reflecting traditional dispensing dominance for chronic antidepressant therapy. Major retail pharmacy chains across North America, Europe, and Asia-Pacific anchor SSRI, SNRI, and atypical antidepressant fulfilment, supported by deep insurance coverage integration and refill management capability.

To access detailed market analysis, Request Sample

Hospital pharmacies at 31.5% serve inpatient psychiatric care, acute treatment initiation, esketamine and other REMS-program-administered therapies, and integrated mental health treatment programs. Online pharmacies at 16.7% are the fastest-growing channel (~4.8% CAGR), benefiting from telehealth integration and direct-to-consumer prescribing.

By Disorder Type

Major depressive disorder leads with a 43.9% share in 2025, reflecting depression's position as the leading cause of disability worldwide and the WHO estimate of ~332 million affected globally. MDD pharmacotherapy spans first-line SSRIs and SNRIs, augmentation therapies, and emerging rapid-acting novel mechanism agents for treatment-resistant cases.

Generalized anxiety disorder at 21.6%, obsessive-compulsive disorder at 14.2%, and panic disorder at 11.1% reflect overlapping pharmacotherapy with SSRIs and SNRIs as first-line therapies.

Regional Market Insights

North America leads at 39.1% in 2025, supported by the United States as the world's largest single-country market with comprehensive mental health treatment infrastructure, sophisticated insurance coverage, and the global concentration of leading depression drug developers. The region benefits from active pipeline innovation, FDA leadership in novel mechanism approvals, and high diagnosis and treatment initiation rates.

Europe at 28.4% holds the second-largest share, anchored by established treatment guidelines from NICE and equivalent national bodies, aging demographics, and national mental health strategies across the UK, Germany, France, and the Nordics.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

39.1% |

Sophisticated mental health treatment infrastructure; FDA leadership in novel mechanism approvals; major pharma headquarters |

|

Europe |

28.4% |

Established treatment guidelines and reimbursement; aging population; national mental health strategies; EMA novel approvals |

|

Asia Pacific |

22.7% |

Rising mental health awareness; expanding insurance coverage; growing diagnosis rates; large addressable patient base |

|

Latin America |

5.6% |

Rising mental health awareness; expanding insurance access; growing pharmaceutical distribution networks |

|

Middle East and Africa |

4.2% |

Emerging treatment access; gradual destigmatisation; expanding mental health treatment infrastructure |

Asia-Pacific at 22.7% reflects rapid growth across China, Japan, India, and Australia, driven by rising mental health awareness and expanding insurance coverage. Latin America (5.6%) and Middle East and Africa (4.2%) represent emerging-growth markets with rising diagnosis rates.

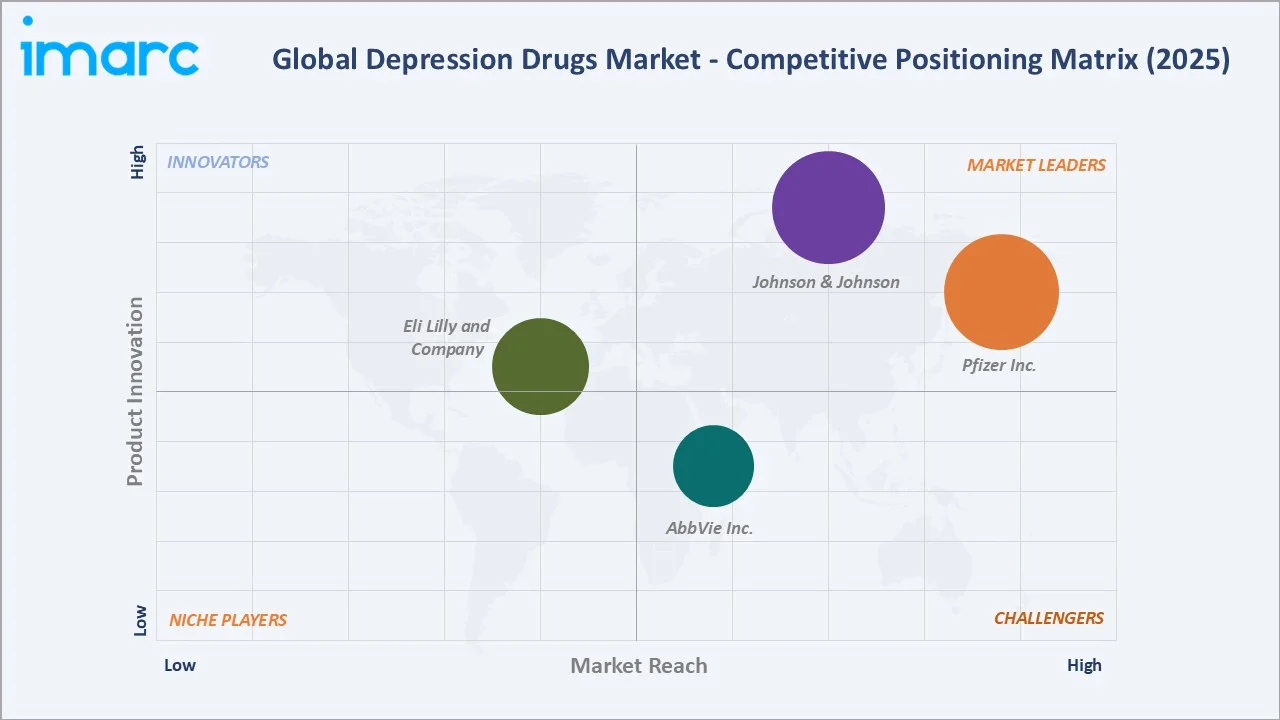

Competitive Landscape

The global depression drugs market is moderately consolidated. Leading players include Pfizer Inc., Eli Lilly and Company, Johnson & Johnson, and AbbVie Inc.

|

Company Name |

Products |

Market Position |

Core Strength |

|

Pfizer Inc. |

EFFEXOR XR, PRISTIQ, NARDIL, ZOLOFT |

Market Leader |

Extensive global distribution; diversified portfolio including Zoloft (sertraline); Q4 2024 USD 150 Million Ireland manufacturing investment; novel formulation launches |

|

Eli Lilly and Company |

Prozac, Cymbalta, Symbyax |

Established Player |

Pioneer in SSRIs (fluoxetine/Prozac legacy); CNS R&D capability; Q1 2025 FDA Fast Track designation for new oral antidepressant |

|

Johnson & Johnson |

SPRAVATO, CAPLYTA |

Market Leader |

Spravato (esketamine) leadership in treatment-resistant depression; integrated mental health portfolio |

|

AbbVie Inc. |

VRAYLAR |

Challenger |

Raising the standards of care through innovative approaches to help patients; exploring novel approaches |

The competitive structure includes large diversified multinationals, CNS-focused specialists, and emerging precision psychiatry biotech companies.

Key Company Profiles

Pfizer Inc.

Pfizer Inc. is one of the world's largest pharmaceutical companies with a long-established presence in the depression drugs market through its legacy and continued SSRI portfolio.

- Product Portfolio: EFFEXOR XR, PRISTIQ, NARDIL, and ZOLOFT.

- Recent Developments: Pfizer Inc. reported USD 14.45 billion in Q1 2026 revenue, up about 5% year‑over‑year, with reported net income of USD 2.69 billion, driven by growth in recently launched and acquired products, reaffirming its full‑year 2026 financial guidance.

- Strategic Focus: Manufacturing capacity expansion for next-generation antidepressants; reformulation innovation for improved adherence; global distribution leadership; defensive portfolio management against generic competition.

Johnson & Johnson

Johnson & Johnson is a global leader in treatment-resistant depression through Spravato (esketamine nasal spray) administered under REMS programs. J&J's neuroscience portfolio represents one of the most differentiated treatment-resistant depression franchises globally.

- Product Portfolio: Spravato (esketamine nasal spray) and CAPLYTA.

- Recent Developments: In January 2026, new analysis of Phase 3 data showed CAPLYTA nearly doubled the likelihood of remission vs. placebo at 6 weeks, with 65% achieving remission and 43% achieving sustained relief through 6 months.

- Strategic Focus: Treatment-resistant depression leadership through Spravato; novel mechanism pipeline expansion via biotech acquisition; REMS program operational excellence; international market expansion.

Market Concentration Analysis

The global depression drugs market is moderately consolidated, with the top players, Pfizer Inc., Eli Lilly and Company, Johnson & Johnson, and AbbVie Inc, holding a substantial portion of branded revenue. Mature SSRI and SNRI patent expirations have driven generic substitution, while novel mechanism therapies create defensible premium-priced segments.

Investment & Growth Opportunities

Fastest Growing Segments

- Online pharmacy distribution is projected to grow at approximately 4.8% CAGR through 2034, supported by direct-to-consumer telehealth-pharmacy integrations and rising acceptance of digital mental health workflows.

- Major depressive disorder therapies are projected to grow at approximately 3.1% CAGR through 2034, driven by novel mechanism approvals targeting treatment-resistant depression and expanding diagnosis rates globally.

Emerging Market Expansion

- Asia-Pacific represents the highest-growth regional opportunity, with rising mental health awareness, expanding insurance coverage, and growing diagnosis rates across China, Japan, India, and Australia.

- Treatment-resistant depression and precision psychiatry novel mechanisms offer premium-priced growth opportunities for vendors with differentiated pipelines.

Venture and Institutional Investment Trends

- Precision psychiatry biotechs are attracting venture capital, exemplified by Alto Neuroscience's USD 60 Million Series B raise to advance EEG biomarker-guided antidepressant therapies.

- Pipeline acquisition and M&A trends are accelerating, with AbbVie's acquisition of Gilgamesh Pharmaceuticals’ novel psychedelic‑based major depressive disorder candidate, bretisilocin, for up to USD 1.2 billion in August 2025.

Future Market Outlook (2026-2034)

The global depression drugs market is positioned for steady, single-digit expansion through 2034. From USD 19.71 Billion in 2025, the market is projected to reach USD 25.44 Billion by 2034, representing incremental value of approximately USD 5.73 Billion at a 2.79% CAGR, increasingly composed of novel mechanism therapies, precision psychiatry platforms, and treatment-resistant depression franchises.

Novel mechanism agents including esketamine, dextromethorphan-bupropion combinations, and emerging psilocybin and neurosteroid therapeutics will capture incremental premium-priced share. Online pharmacy distribution will continue to gain share at approximately 4.8% CAGR. North America will retain regional leadership, with Asia-Pacific closing the gap on rising mental health awareness and expanding diagnosis rates.

Research Methodology

Primary Research

Primary research included structured interviews with over 100 industry participants in 2024–2025, comprising pharmaceutical executives, psychiatry key opinion leaders, payer organizations, pharmacy benefit managers, contract research organization executives, and mental health advocacy organizations across North America, Europe, and Asia-Pacific, validating market sizing, segmentation, regional shares, and pipeline trajectories.

Secondary Research

Secondary research covered WHO mental health publications, FDA and EMA regulatory documentation, company annual reports and SEC filings, alongside government national mental health strategy documents and clinical practice guidelines.

Forecasting Models

Market size estimations used combined top-down and bottom-up forecasting, incorporating country-level mental health prevalence, treatment penetration rates, branded versus generic share dynamics, novel mechanism launch trajectories, and vendor revenue disclosures. The 2.79% CAGR reflects validation against announced pipeline trajectories, generic erosion patterns, and demographic and disease prevalence trends through 2034.

Depression Drugs Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Drug Classes Covered | Atypical Antipsychotics, Serotonin-Norepinephrine Reuptake Inhibitors (SNRIs), Selective Serotonin Reuptake Inhibitors (SSRIs), Central Nervous System (CNS) Stimulants, Tricyclic Antidepressants, Monoamine Oxidase Inhibitors, Others |

| Disorder Types Covered | Major Depressive Disorder, Obsessive-Compulsive Disorder, Generalized Anxiety Disorder, Panic Disorder, Others |

| Drug Types Covered | Generic Drugs, Branded Drugs |

| Distribution Channels Covered | Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Pfizer Inc., Eli Lilly and Company, Johnson & Johnson, AbbVie Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the depression drugs market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the depression drugs industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Depression Drugs Market Report

The global depression drugs market reached USD 19.71 Billion in 2025 and is projected to reach USD 25.44 Billion by 2034.

The market is expected to grow at a CAGR of 2.79% during 2026-2034, driven by rising mental health disorder prevalence, novel antidepressant pipeline, destigmatisation, and online pharmacy growth.

North America leads with a 39.1% share in 2025, supported by the United States as the world's largest single-country market and the global headquarters of leading depression drug developers.

Retail pharmacies dominate with a 44.8% share in 2025, reflecting traditional dispensing dominance for SSRIs, SNRIs, and atypical antidepressants across chronic mental health therapy.

Major depressive disorder leads at 43.9%, reflecting depression's position as the leading cause of disability worldwide and over 280 million people affected globally per the WHO.

Key players include Pfizer Inc., Eli Lilly and Company, Johnson & Johnson, and AbbVie Inc.

Online pharmacies are growing at approximately 4.8% CAGR through 2034 due to direct-to-consumer telehealth-pharmacy integrations, refill convenience, and rising acceptance of digital mental health workflows.

Key challenges include generic competition and price erosion, antidepressant side effects and treatment discontinuation, long drug development timelines for novel mechanisms, regulatory complexity, and stigma and access inequalities.

Treatment-resistant depression therapies, precision psychiatry and pharmacogenomic platforms, pediatric and adolescent depression therapies, and Asia-Pacific market expansion represent the highest-growth investment opportunities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)