Dialysis Market Size, Share, Trends and Forecast by Type, Product and Services, End User, and Region, 2026-2034

Global Dialysis Market Size, Share, Trends & Forecast (2026-2034)

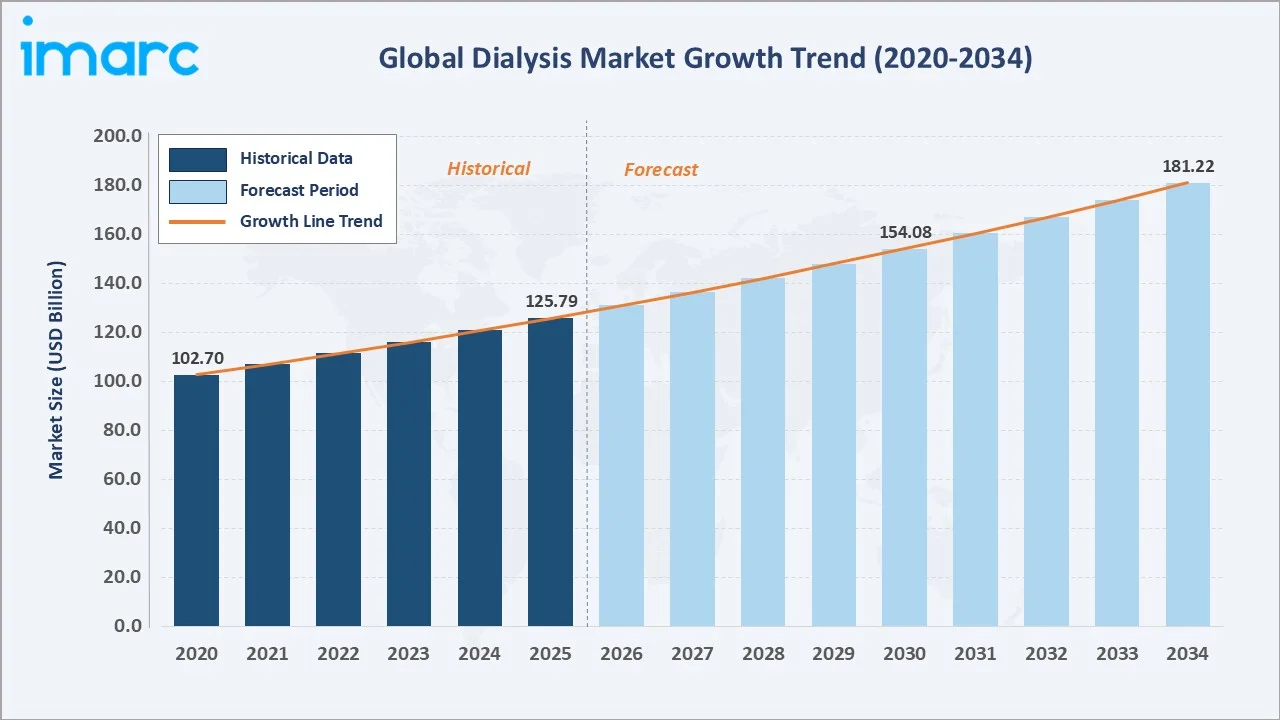

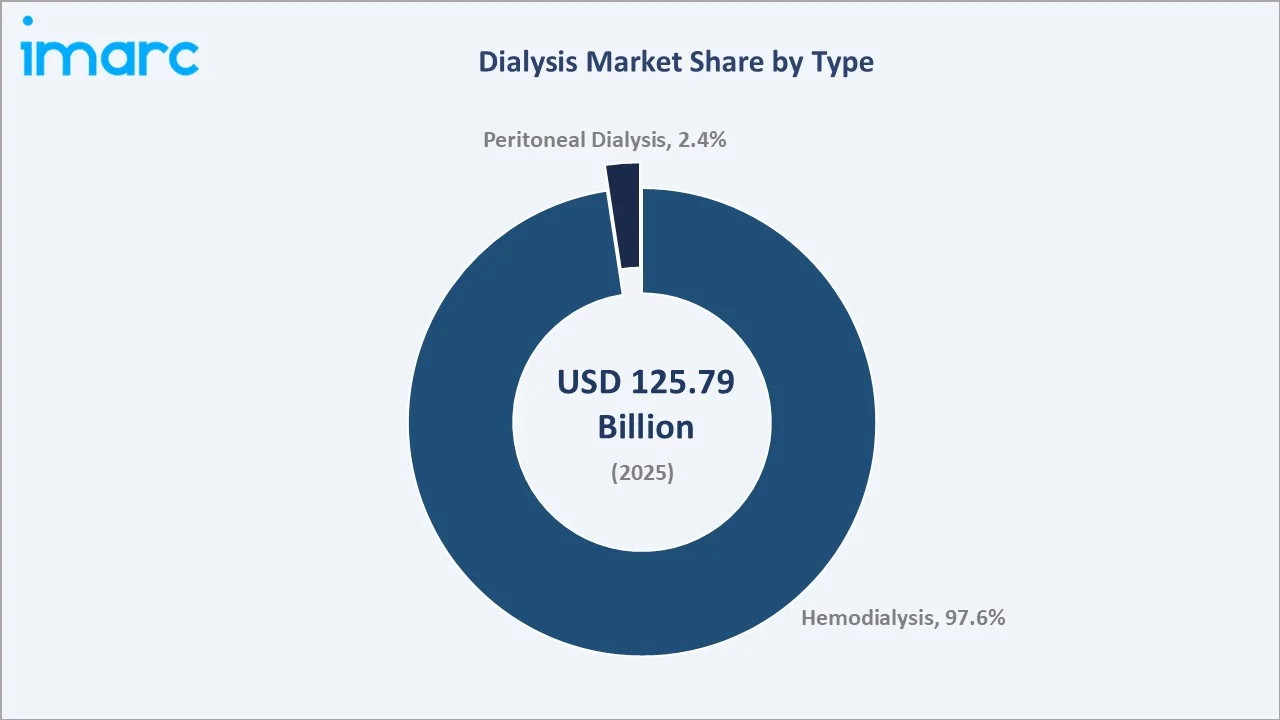

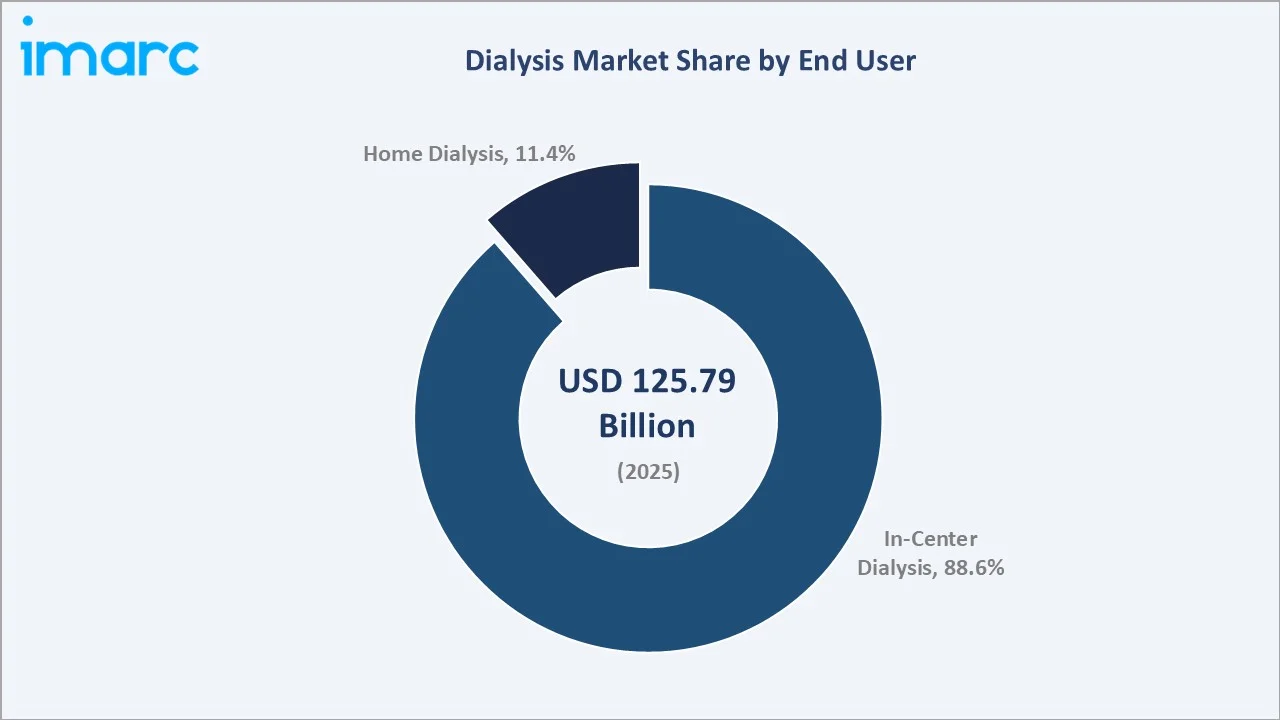

The global dialysis market reached USD 125.79 Billion in 2025 and is projected to reach USD 181.22 Billion by 2034, exhibiting a CAGR of 4.14% during 2026-2034. Growth is primarily driven by the rising global burden of chronic kidney disease (CKD), an aging population, and expanding access to renal replacement therapy.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 125.79 Billion |

|

Forecast Market Size (2034) |

USD 181.22 Billion |

|

CAGR (2026-2034) |

4.14% |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2020-2025 |

|

Largest Region |

North America (41.0%) |

|

Fastest Growing Region |

Asia-Pacific (28.5%) |

|

Leading Type |

Hemodialysis (97.6%, 2025) |

|

Leading End User |

In-Center Dialysis (88.6%, 2025) |

Global dialysis market exhibited steady expansion driven by the rising incidence of chronic kidney disease (CKD) and end-stage renal disease (ESRD) globally. Healthcare infrastructure improvements in developed regions and growing access to renal care in emerging economies accelerated market penetration.

To get more information on this market, Request Sample

Global dialysis market is expected to see differential growth across key segments, with the fastest‑growing sub‑categories through 2034.

Executive Summary

The global dialysis market stood at USD 102.70 Billion in 2020 and expanded steadily to USD 125.79 Billion by 2025, reflecting consistent demand growth fueled by the worldwide surge in end-stage renal disease (ESRD). The market is forecast to reach USD 154.08 Billion by 2030 and USD 181.22 Billion by 2034.

Hemodialysis remains the cornerstone of the market, commanding a 97.6% share in 2025. In-Center Dialysis accounts for 88.6% of end-user revenues, underpinned by specialist clinical supervision requirements. However, Home Dialysis is witnessing accelerated uptake, benefiting from advances in portable equipment, remote patient monitoring, and shifting patient preference for home-based care.

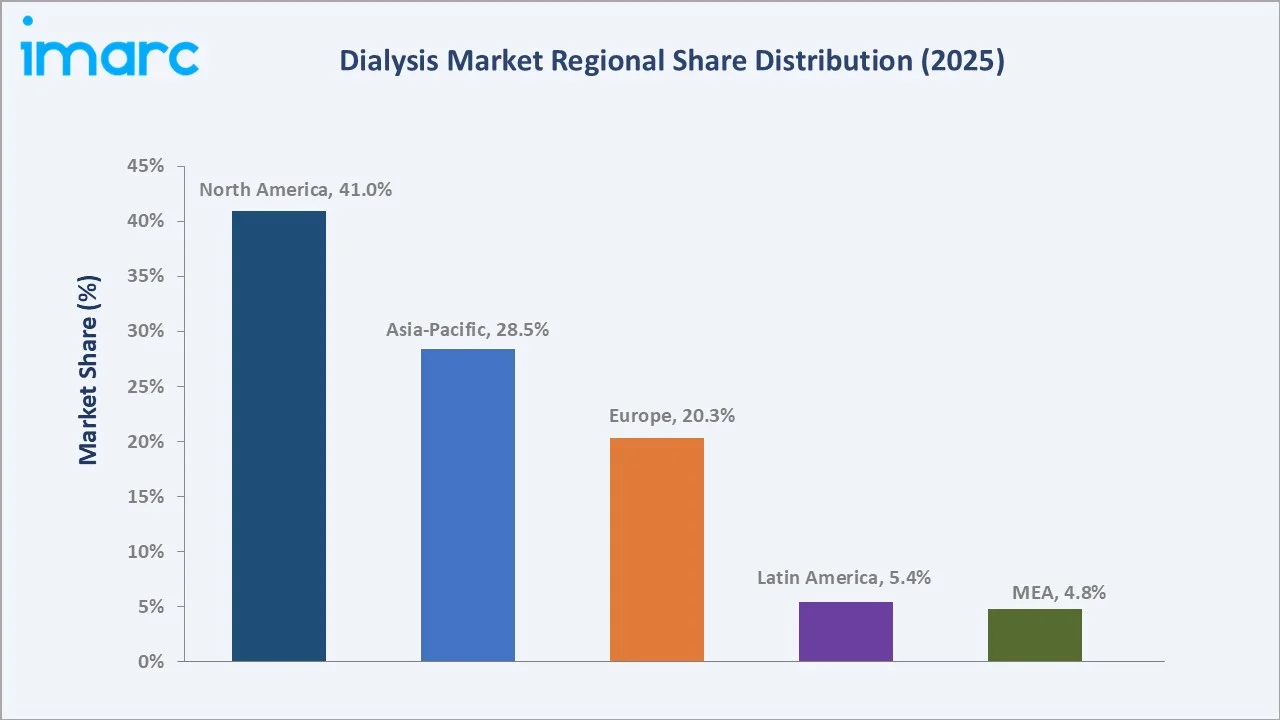

North America accounts for 41.0% of global revenue in 2025, with Asia-Pacific at 28.5% and Europe at 20.3%. Emerging regions such as Latin America (5.4%) and the Middle East and Africa (4.8%) present significant untapped opportunities.

Key Market Insights

|

Insight |

Data |

|

Largest Type |

Hemodialysis – 97.6% share (2025) |

|

Second Type |

Peritoneal Dialysis– 2.4% market share (2025) |

|

Largest End User |

In-Center Dialysis– 88.6% market share (2025) |

|

Leading Region |

North America – 41.0% (2025) |

|

Fastest Growing Region |

Asia-Pacific – 28.5%, highest growth potential |

|

Top Companies |

Fresenius Medical Care AG, B. Braun SE., NIPRO, BD, Asahi Kasei Medical Co., Ltd., TORAY MEDICAL CO., LTD., Teleflex Incorporated., Vantive Health LLC |

|

Market Opportunity |

Emerging markets in Asia-Pacific and home dialysis expansion |

Key Analytical Observations Supporting The Above Data:

- Hemodialysis held a dominant 97.6% share in 2025, driven by widespread clinical adoption, established infrastructure, and superior patient outcomes in ESRD management.

- North America commanded 41.0% of global dialysis revenues in 2025 - supported by the high prevalence of diabetes-induced CKD and comprehensive reimbursement structures under Medicare.

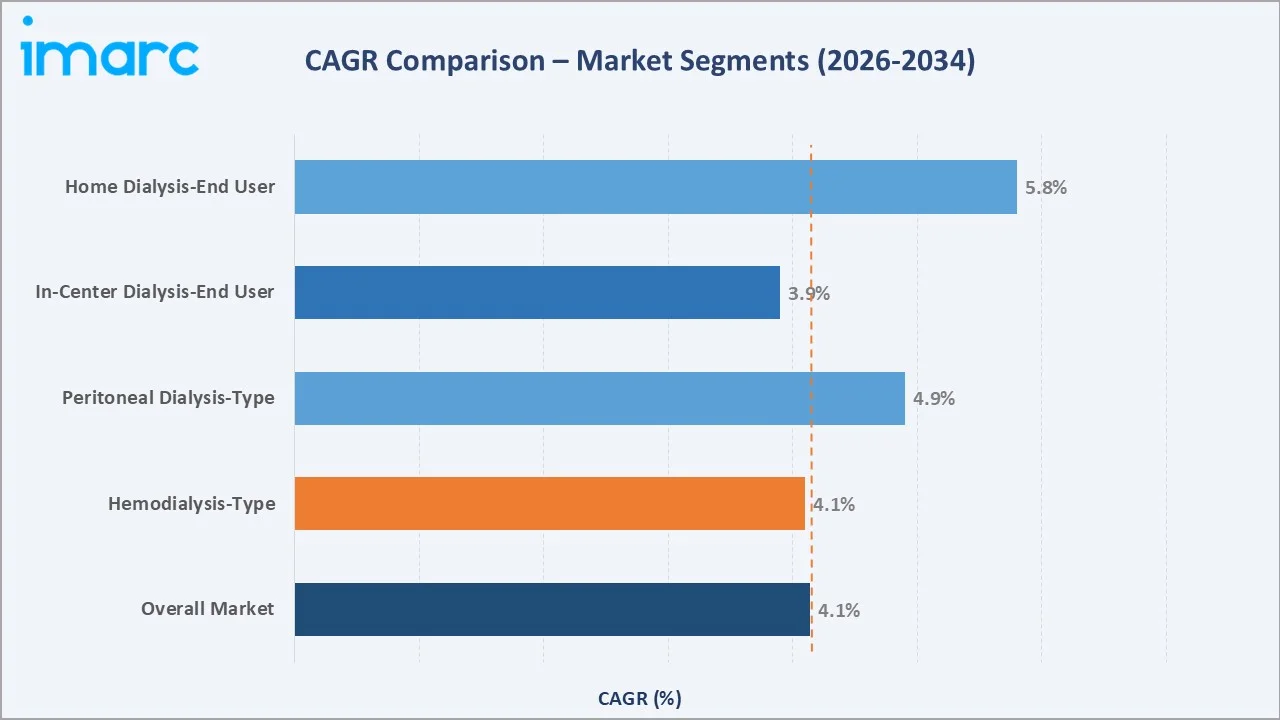

- Home Dialysis is the fastest-growing end-user segment with an estimated CAGR of ~5.8% during 2026-2034, propelled by telemedicine, wearable monitoring, and patient empowerment programs.

- Peritoneal Dialysis, though representing only 2.4% share in 2025, is gaining traction in Asia-Pacific and Latin America where home-based care costs are substantially lower than in-center alternatives.

- Asia-Pacific, the second-largest region at 28.5% share in 2025, is projected to be the fastest growing regional market, led by China, India, and Japan with rising ESRD diagnosis rates.

- The global dialysis patient population exceeded 4.9 million in 2025, creating sustained long-term market demand.

Global Dialysis Market Overview

Dialysis is a life-sustaining medical procedure that artificially replicates kidney function by removing waste, toxins, and excess fluid from the blood. It serves as the primary renal replacement therapy for patients with Stage 5 CKD or acute kidney injury. The industry ecosystem encompasses equipment manufacturers, consumable producers, pharmaceutical companies, service providers, and integrated dialysis clinic operators.

Macroeconomic forces shaping the market include rising prevalence of hypertension and type-2 diabetes - the two leading causes of CKD alongside aging demographics in high-income nations. Government-funded universal healthcare programs in Europe and North America sustain demand, while developing nations are rapidly expanding dialysis access through public-private partnerships.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

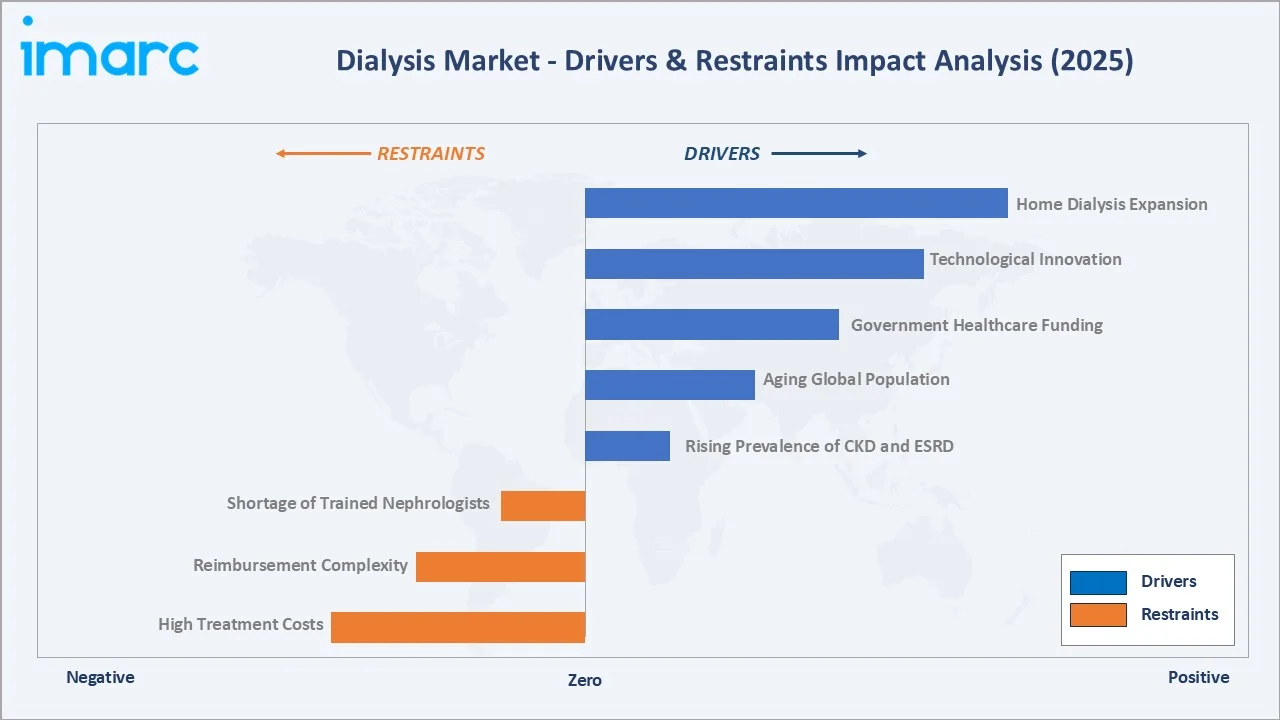

- Rising Prevalence of CKD and ESRD: Over 850 million people globally suffered from kidney disease in 2025, directly expanding the dialysis patient base.

- Aging Global Population: Older adults particularly those aged 65 and above ace a significantly higher risk of developing chronic kidney disease (CKD) compared to younger populations. As this age group continues to expand across developed regions, it plays a critical role in sustaining long-term demand for dialysis and related renal care services.

- Government Healthcare Funding: Publicly funded dialysis programs in the United States support a substantial patient population, serving as a critical reimbursement backbone and providing strong, sustained financial support for the dialysis market.

- Technological Innovation: The integration of AI-based fluid management systems, advanced biocompatible membranes, and portable hemodialysis machines has contributed to measurable improvements in patient outcomes, enhancing treatment efficiency, safety, and overall quality of care in recent years.

Market Restraints

- High Treatment Costs: Annual per-patient dialysis costs range from USD 60,000 to USD 100,000 in 2025, limiting access in lower-income nations and creating payer sustainability challenges.

- Reimbursement Complexity: Fragmented reimbursement policies across Asia, Latin America, and Africa restrict market expansion, with many patients unable to access therapies despite clinical eligibility.

- Shortage of Trained Nephrologists: A significant global shortage of skilled nephrology professionals continues to constrain the scalability of in-center dialysis programs, limiting the ability of healthcare systems to expand capacity and meet growing patient demand.

Market Opportunities

- Home Dialysis Expansion: A relatively small share of patients currently utilize home-based dialysis therapies, indicating substantial untapped potential. Expanding adoption through supportive policies and technology enablement presents a significant incremental market opportunity while improving accessibility and patient convenience.

- Emerging Market Penetration: Dialysis access in regions such as Sub-Saharan Africa and South Asia remains limited relative to the eligible patient population, highlighting a substantial unmet need. This gap creates a strong opportunity for expanding care delivery through cost-effective solutions, particularly peritoneal dialysis models that are better suited for low-resource settings.

- Digital Health Integration: The adoption of remote monitoring platforms, AI-driven treatment optimization, and telehealth-based nephrology consultations is expected to significantly lower per-patient dialysis costs, improving efficiency while enhancing access to continuous and personalized care.

Market Challenges

- Patient Adherence: Non-adherence to prescribed dialysis schedules remains a significant challenge globally, contributing to increased risk of clinical complications and placing additional financial strain on healthcare systems.

- Equipment Maintenance & Supply Chain: Disruptions in raw material supply chains—particularly for polymer-based dialyzer membranes—have led to increased manufacturing costs in recent years, creating pricing pressures and impacting overall supply stability in the dialysis market.

- Regulatory Approval Timelines: Lengthy regulatory approval processes in major markets such as the United States and Europe continue to delay the commercialization of new dialysis technologies, slowing the pace at which innovative solutions reach patients.

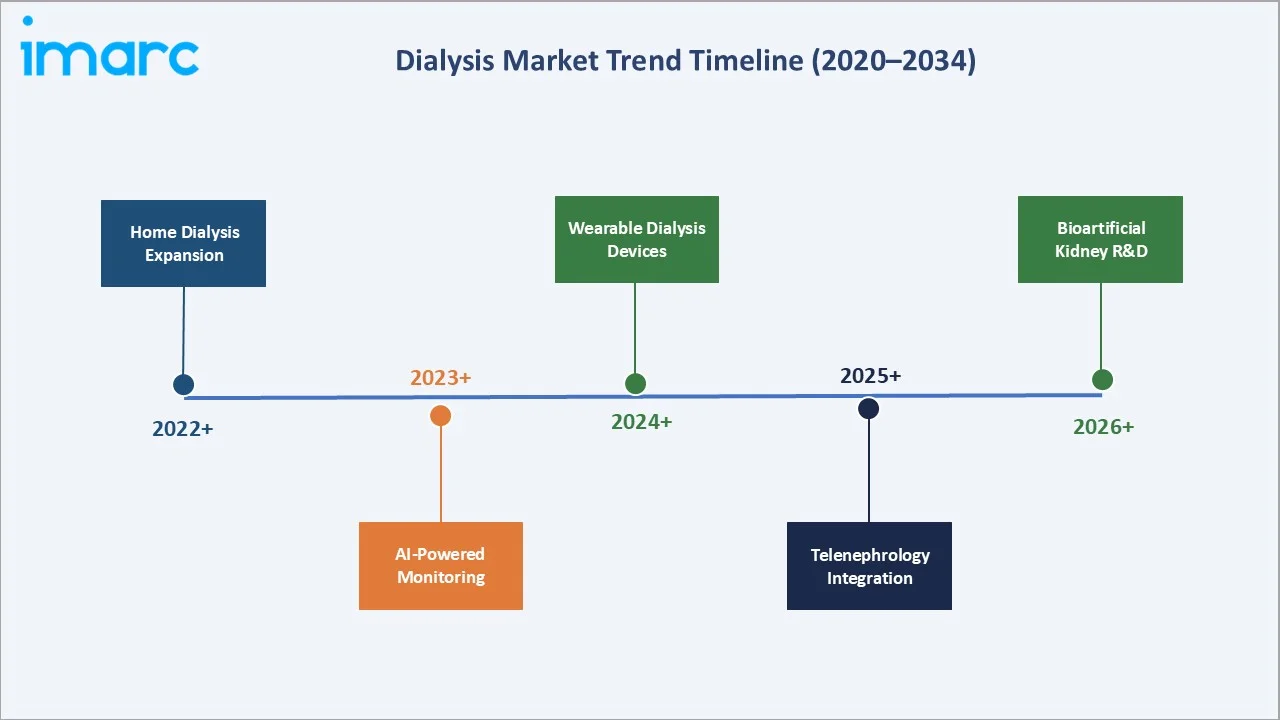

Emerging Market Trends

1. Acceleration of Home Dialysis Adoption

Home dialysis adoption has been steadily increasing in recent years, supported by favorable policy frameworks and a growing emphasis on patient-centric care models. Initiatives such as the Advancing American Kidney Health Initiative have played a key role in encouraging the shift toward home-based therapies in the United States.

2. AI and Digital Health Integration

Artificial intelligence–enabled tools for fluid management, treatment adequacy monitoring, and early complication detection have increasingly moved into mainstream clinical practice in recent years. Leading providers such as Fresenius Medical Care have introduced AI-integrated dialysis platforms, demonstrating the potential to enhance clinical decision-making, improve patient stability, and reduce the risk of hospitalization in real-world care settings.

3. Wearable and Portable Dialysis Devices

Prototype wearable artificial kidney (WAK) devices have advanced into late-stage clinical development, marking a significant step toward more patient-friendly renal replacement solutions. These compact, lightweight systems are designed to deliver continuous, low-flow dialysis, shifting away from the conventional intermittent treatment mode.

4. High-Flux and Biocompatible Membrane Innovation

Advanced synthetic membranes such as polysulfone, polyethersulfone, and polyarylethersulfone composites have become widely adopted in high-flux dialyzers. These materials offer superior performance compared to traditional cellulose-based membranes, particularly in removing larger molecular toxins, and contribute to improved clinical outcomes and reduced long-term complications for patients undergoing dialysis.

5. Telenephrology and Remote Patient Monitoring

Advanced synthetic membranes, including polysulfone, polyethersulfone, and polyarylethersulfone composites, are now widely utilized in high-flux dialyzers. Compared to conventional cellulose-based materials, they deliver enhanced filtration performance particularly in clearing larger molecular toxins thereby supporting better treatment effectiveness and improved long-term patient outcomes.

Industry Value Chain Analysis

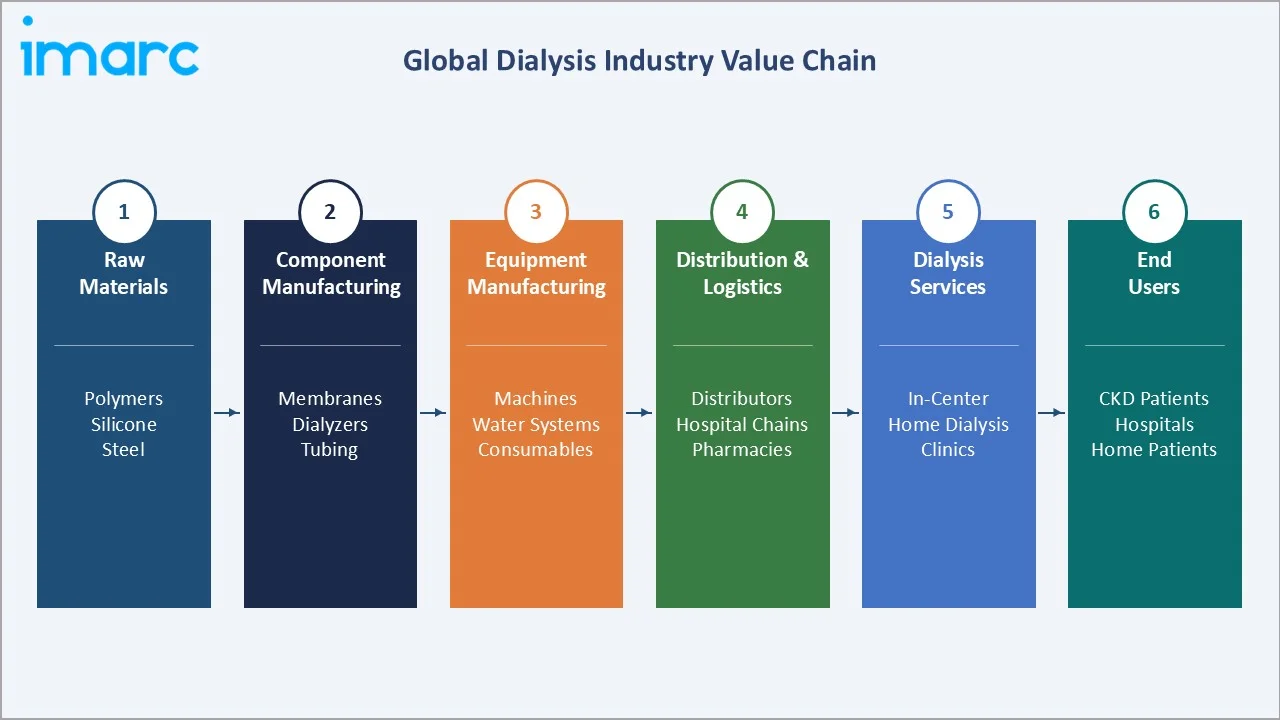

The global dialysis value chain begins with raw material suppliers providing specialized polymers, metals, and medical-grade components, followed by manufacturers producing membranes, catheters, tubing, and integrated dialysis equipment and consumables.

|

Stage |

Key Players / Activities |

|

Raw Materials |

Polymer suppliers, silicone manufacturers, medical-grade steel producers |

|

Component Manufacturing |

Dialyzer membrane makers, catheter producers, tubing fabricators |

|

Equipment Manufacturing |

OEMs – dialysis machines, water treatment systems, consumables |

|

Distribution & Logistics |

Medical device distributors, hospital procurement teams, GPOs |

|

Dialysis Service Providers |

In-center clinics, home therapy programs |

|

End Users |

CKD patients, hospital nephrology departments, home patients |

It extends through distributors and procurement networks to dialysis service providers, including clinic operators and home care programs, ultimately serving chronic kidney disease patients across hospital settings and home-based treatment environments.

Technology Landscape in the Dialysis Industry

Membrane Technology Innovations

High-flux synthetic membranes, particularly polysulfone and polyacrylonitrile variants, dominate global dialyzer usage. Ongoing innovations in membrane design, nanocomposite structures, and biocompatible coatings have enhanced durability, efficiency, and reuse potential in dialysis treatments.

Smart Connectivity and Remote Monitoring

IoT-enabled dialysis machines with integrated sensors for real-time monitoring of blood flow, conductivity, and transmembrane pressure are increasingly being adopted in advanced healthcare settings. These connected systems transmit treatment data to centralized platforms, enabling proactive clinical intervention, improved treatment oversight, and more personalized patient care.

Automation and Robotics

Automated peritoneal dialysis (APD) cyclers equipped with intuitive interfaces and self-diagnostic capabilities have become the dominant modality for home-based peritoneal dialysis in advanced healthcare markets, improving ease of use and patient adherence.

Bioartificial Kidney Research

The Kidney Health Initiative and NIH-funded Wearable Artificial Kidney Consortium advanced implantable silicon nanopore membrane-based bioartificial kidneys to Phase II clinical testing by 2025. If approved, these devices could eliminate the need for conventional dialysis by 2035, representing a disruptive technology threat to the current market structure.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Hemodialysis |

97.6% |

2025 |

|

Product and Services |

Services |

79.0% |

2025 |

|

End User |

In-Center Dialysis |

88.6% |

2025 |

|

Region |

North America |

41.0% |

2025 |

By Type

The dialysis market is segmented by therapy type into Hemodialysis and Peritoneal Dialysis. Hemodialysis accounted for 97.6% of global revenue in 2025, valued at approximately USD 122.8 Billion. This dominance reflects the therapy's clinical efficacy, established infrastructure in dialysis centers, and physician familiarity with HD protocols.

To access detailed market analysis, Request Sample

By End User

In-Center Dialysis dominated end-user revenues in 2025, accounting for 88.6% - approximately USD 111.4 Billion. These facilities provide professionally supervised HD sessions typically 3 times per week, with structured nutritional, psychological, and social support.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

41.0% |

CKD prevalence, insurance coverage, advanced infrastructure |

|

Asia-Pacific |

28.5% |

Diabetic nephropathy surge, government health schemes, urbanization |

|

Europe |

20.3% |

Universal healthcare, aging demographics, strong regulatory frameworks |

|

Latin America |

5.4% |

Rising diabetes burden, expanding hospital networks, healthcare reforms |

|

Middle East & Africa |

4.8% |

Government dialysis funding programs, increasing CKD awareness |

North America

North America held a 41.0% revenue share in 2025, equivalent to approximately USD 51.6 Billion. The United States alone accounts for nearly 90% of this regional total, supported by Medicare ESRD coverage. Over 540,000 patients in the U.S. received dialysis in 2025. The Advancing American Kidney Health Initiative has further stimulated home therapy investment..

Asia-Pacific

Asia-Pacific accounted for 28.5% of global revenues in 2025 - approximately USD 35.9 Billion - and is the fastest-growing regional market. China has the world's largest CKD patient population (estimated 132 million in 2025), with dialysis penetration below 30% of eligible patients. Japan, with the world's highest dialysis rate per capita (~3,200 per million population in 2025), represents a mature yet technology-intensive market. India presents enormous growth potential with dialysis penetration below 10% of ESRD patients.

Competitive Landscape

|

Company Name |

Brand / Product |

Market Position |

Strategic Focus |

|

Fresenius Medical Care AG |

NxStage |

Leader |

Global dialysis services & equipment |

|

B. Braun SE |

Dialog+ System |

Major Player |

Hemodialysis machines & consumables |

|

NIPRO |

ELISIO Dialyzers |

Major Player |

Hollow fiber dialyzers, blood tubing |

|

BD |

BD Peripheral IV Catheter (PIVC) |

Challenger |

Vascular access and catheter systems |

|

Asahi Kasei Medical Co., Ltd. |

Rexeed |

Challenger |

High-performance membrane dialyzers |

|

TORAY MEDICAL CO, LTD. |

Toraylight NV |

Challenger |

Synthetic membrane dialyzers |

|

Teleflex Incorporated |

Arrow Catheters |

Emerging |

Vascular access solutions for dialysis |

|

Vantive Health LLC |

PrisMax System |

Emerging |

CRRT and peritoneal dialysis systems |

The global dialysis market is moderately consolidated, characterized by the presence of a few large, vertically integrated players alongside several regional and product-focused companies.

Key Company Profiles

Fresenius Medical Care AG

Fresenius Medical Care AG is a Germany-based global healthcare company and the world’s leading provider of dialysis products and services for patients with chronic kidney failure. Headquartered in Bad Homburg, Germany, the company operates a highly integrated business model that combines dialysis services, equipment manufacturing, and consumables production.

- Product Portfolio: Dialysis machines, high-flux dialyzers, renal pharmaceuticals, and home dialysis systems.

- Recent Developments: In 2023, Fresenius Medical Care has developed a predictive model using machine learning and cloud computing to help proactively identify when kidney dialysis patients might be suffering a potentially life-threatening complication.

- Strategic Focus: Vertical integration across services, products, and pharmaceuticals; expansion of home dialysis programs in Asia and North America; digital health ecosystem development.

NIPRO Corporation

NIPRO Corporation is a Japan-based global healthcare and medical device manufacturer headquartered in Osaka, founded in 1954. The company is publicly listed on the Tokyo Stock Exchange and has grown into a diversified multinational organization with a strong presence across medical devices, pharmaceuticals, and pharmaceutical packaging.

- Product Portfolio: NIPRO cellulose triacetate and polysulfone dialyzers, blood circuit sets, peritoneal dialysis accessories.

- Recent Developments: In 2025, NIPRO Corporation announced the launch of its LiniXia next-generation reverse-osmosis (RO) water treatment system at the European Renal Association Congress 2025, strengthening its dialysis portfolio. The LiniXia system is designed to deliver high-quality water essential for dialysis treatment, offering improved reliability, efficiency, and resource optimization for dialysis clinics.

- Strategic Focus: Dialyzer quality leadership, emerging market penetration, and co-development agreements with hospital networks.

BD

Becton, Dickinson and Company is a U.S.–based multinational medical technology company that develops, manufactures, and sells a broad range of medical devices, instrument systems, and laboratory equipment. Founded in 1897 and headquartered in Franklin Lakes, New Jersey, BD operates through key segments including BD Medical, BD Life Sciences, and BD Interventional.

- Product Portfolio: BD’s offerings include Hemodialysis Catheters, GlidePath Long‑Term Hemodialysis Catheter, Pristine Long‑Term Hemodialysis Catheter, and DuoGlide Dialysis Catheters

- Recent Developments: In 2021, BD announced FDA 510(k) clearance for its Pristine Long-Term Hemodialysis Catheter, featuring a unique side-hole free symmetric Y-Tip design. Developed by Pristine Access Technologies (Israel) and acquired by BD in 2020, the catheter became available in the U.S. in May 2021, aligning with BD’s strategy to enhance chronic disease treatment through targeted acquisitions and R&D.

- Strategic Focus: BD’s focus within renal care centers on improving vascular access and dialysis delivery through innovative catheter designs that enhance flow, reduce complications.

Market Concentration Analysis

The global dialysis market demonstrates moderate-to-high concentration at the services level and moderate concentration at the products/equipment level.

At the product and equipment level, the top 5 manufacturers - Fresenius Medical Care AG., Asahi Kasei Medical Co., Ltd., B. Braun SE., NIPRO, and BD. - collectively held approximately 55-60% of the global dialyzer market in 2025. The remaining 40-45% is fragmented among regional manufacturers in Asia, Europe, and Latin America.

Investment & Growth Opportunities

Home Dialysis Segment: The shift from in-center to home dialysis presents a significant investment opportunity. With a relatively small share of patients currently receiving home-based care, increasing adoption over the coming years is expected to substantially expand the addressable market. Companies developing portable hemodialysis systems, patient training programs, and telehealth infrastructure are well-positioned to benefit from this transition and capture strong growth potential.

Asia-Pacific Market Expansion: With a large and rapidly growing population and rising rates of chronic kidney disease (CKD), the Asia-Pacific region offers strong growth potential in the dialysis market through the coming years. Expanding dialysis demand across key countries is creating significant opportunities for market participants.

Digital Health and Remote Monitoring Platforms: AI-powered dialysis optimization platforms, IoT-connected machines, and remote patient monitoring solutions are attracting strong venture and strategic investment interest. The growing adoption of digital health technologies in dialysis care is driving increased funding activity, as stakeholders focus on improving treatment efficiency, patient outcomes, and real-time care management.

Future Market Outlook (2026-2034)

The global dialysis market is projected to grow from USD 125.79 Billion in 2025 to USD 181.22 Billion by 2034, at a CAGR of 4.14%. This trajectory reflects both the structural inelasticity of ESRD treatment demand and incremental growth from technology upgrades, home therapy expansion, and emerging market penetration.

By 2030, the market is expected to reach USD 154.08 Billion, with Asia-Pacific emerging as a near-equivalent competitor to North America in absolute revenue terms. Technological disruptions on the horizon include bioartificial kidney commercialization (anticipated 2032-2035), which could fundamentally reshape the treatment landscape.

From an industry transformation standpoint, value-based care contracting - where dialysis providers are compensated based on patient outcomes rather than procedure volumes - is gaining traction in the United States and Europe. This model incentivizes investment in preventive nephrology, slowing CKD progression and ultimately reshaping the market's long-term demand profile.

Research Methodology

Primary Research

Primary data collection involved structured interviews with 120+ industry stakeholders including nephrologists, dialysis center administrators, device manufacturers, procurement managers, and policy-makers across 18 countries. Interviews were conducted between Q3 2024 and Q1 2025, providing current insights on market dynamics, technology trends, and competitive strategies.

Secondary Research

Secondary sources included peer-reviewed medical journals (JASN, Kidney International), regulatory databases (FDA, EMA), company annual reports, government health statistics, WHO and ISN publications, trade association databases, and proprietary market intelligence repositories. Over 450 secondary sources were reviewed and triangulated.

Forecasting Models

Market sizing utilized a bottom-up approach - estimating the dialysis patient population by region, multiplying by average annual per-patient treatment costs, and validating against top-down macroeconomic and healthcare expenditure models. Forecasts were further refined using regression analysis of historical CAGR trends, policy impact modeling, and scenario-based sensitivity analysis for three growth trajectories: base, optimistic, and conservative.

Dialysis Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered |

|

| Product and Services Covered |

|

| End Users Covered | In-center Dialysis, Home Dialysis |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Fresenius Medical Care AG, B. Braun SE, NIPRO, BD, Asahi Kasei Medical Co., Ltd., TORAY MEDICAL CO, LTD., Teleflex Incorporated, Vantive Health LLC, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the dialysis market from 2020-2034.

- The dialysis market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the dialysis industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Dialysis Market Report

The global dialysis market was valued at USD 125.79 Billion in 2025, reflecting steady growth from USD 102.70 Billion in 2020, driven by increasing CKD prevalence worldwide.

The market is forecast to reach USD 181.22 Billion by 2034, supported by aging populations and rising ESRD diagnosis rates.

The global dialysis market is projected to expand at a CAGR of 4.14% during the 2026-2034 forecast period, with home dialysis sub-segments growing at a faster ~5.8% CAGR.

Hemodialysis dominates with a 97.6% market share in 2025, driven by its clinical efficacy, widespread infrastructure, and established reimbursement coverage in key markets.

North America holds the largest regional share at 41.0% in 2025, supported by Medicare ESRD coverage, high CKD prevalence, and advanced dialysis infrastructure across the United States.

Asia-Pacific is the fastest growing region, driven by rising diabetic CKD in China and India, low dialysis penetration rates, and expanding government healthcare investment programs.

Key drivers include the global rise in CKD and ESRD cases, aging demographics, government-funded renal care programs, and continuous innovations in dialysis technology and monitoring solutions.

Leading players include Fresenius Medical Care AG, B. Braun SE., NIPRO, BD, Asahi Kasei Medical Co., Ltd., TORAY MEDICAL CO., LTD., Teleflex Incorporated., and Vantive Health LLC.

In-Center Dialysis commands 88.6% of end-user revenues in 2025, while Home Dialysis accounts for 11.4%. Home dialysis is the faster-growing segment at an estimated ~5.8% CAGR through 2034.

Key trends include home dialysis expansion, AI-powered monitoring, wearable kidney devices, telenephrology integration, and advanced biocompatible membrane innovations for improved patient outcomes.

The Asia-Pacific dialysis market was valued at approximately USD 35.9 Billion in 2025, representing 28.5% of global revenues, with China, Japan, and India as the primary growth contributors.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)