Diamond Coating Market Report by Technology (Chemical Vapour Deposition (CVD), Physical Vapour Deposition (PVD)), Substrate (Metal, Ceramic, Composite, and Others), End Use Industry (Electrical and Electronics, Medical, Industrial, Automotive, and Others), and Region 2026-2034

Diamond Coating Market Size:

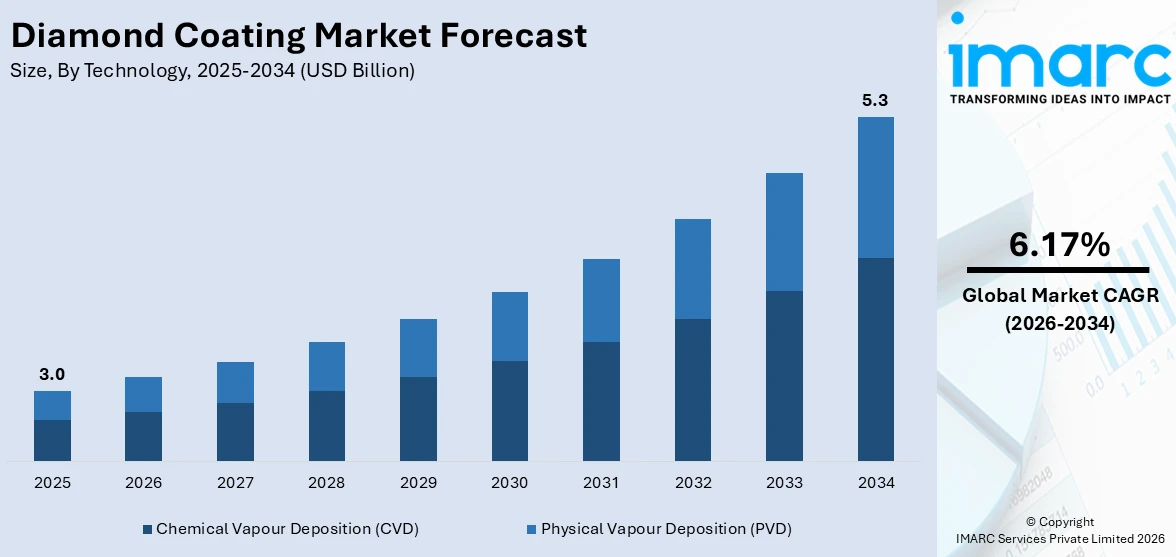

The global diamond coating market size reached USD 3.0 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 5.3 Billion by 2034, exhibiting a growth rate (CAGR) of 6.17% during 2026-2034. The market is propelled by the increasing demand for diamond-coated tools in machining and cutting applications, rapid expansion in the electronics industry, significant advancements in medical device technology, expansion of the automotive sector, substantial investment in research and development of novel diamond coating applications, and increased adoption of chemical vapour deposition (CVD) diamond technology.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 3.0 Billion |

| Market Forecast in 2034 | USD 5.3 Billion |

| Market Growth Rate 2026-2034 | 6.17% |

Diamond Coating Market Analysis:

- Major Market Drivers: The increasing demand for diamond-coated tools in machining and cutting applications, rapid expansion in the electronics industry, and significant advancements in medical device technology are some of the major market drivers.

- Key Market Trends: Improvement of diamond coating techniques in order to enhance adhesion and quality, rising adoption of chemical vapor deposition (CVD), and rising focus on sustainable and environmentally friendly manufacturing procedures are some key market trends responsible for a positive diamond coating market outlook.

- Geographical Trends: Rapid industrialization and manufacturing growth, increasing investments in automotive and electronics industries, and the expanding research and development (R&D) activities are driving the Asia Pacific diamond coating market.

- Competitive Landscape: Some of the major market players in the diamond coating industry include Blue Wave Semiconductors Inc., Diamond Product Solutions, Endura Coatings LLC, JCS Technologies Pte Ltd., NeoCoat SA, OC Oerlikon Management AG, RobbJack Corporation, sp3 Diamond Technologies, and Surface Technology Inc., among many others.

- Challenges and Opportunities: Challenges of the industry include the high production cost of diamond coatings, issues including acheiveing uniform thicjeness and quality, and restricted awareness among potential users about the benefits of diamond coatings and its adoption rates. Whereas, significant innovations in technology, expansion into untapped industries, and rising demand for durable and efficient tools are positively contributing to the diamond coating market revenue.

To get more information on this market Request Sample

Diamond Coating Market Trends:

Increasing Demand for Diamond-Coated Tools in Machining and Cutting Applications

The increasing demand for diamond-coated tools in machining and cutting applications is a significant driver of the global diamond coating market. Diamond coatings are renowned for their exceptional hardness and wear resistance, making them ideal for cutting, grinding, and drilling applications in industries such as automotive, aerospace, and electronics, thus leading to a higher diamond coating demand in the market. The coating enhances the lifespan and performance of tools, reducing the need for frequent replacements and thus lowering operational costs. The longevity is critical in high-precision industries where the cost of downtime and maintenance is significant. Manufacturers are increasingly adopting diamond-coated tools to leverage these benefits, fostering growth in the diamond coating market.

Rapid Growth in the Electronics Industry

The expansion of the electronics industry significantly influences the diamond coating market, particularly in thermal management applications. According to a report published by GITNUX, the global consumer electronics market size reached USD 729.11 Billion in 2022. Diamond has the highest thermal conductivity of any material, making it an excellent choice for managing heat in electronic devices such as semiconductors, LEDs, and high-power electronics. As devices become smaller and more powerful, effective heat dissipation becomes crucial to ensure performance and longevity. With the ongoing innovation in electronics, such as the development of 5G technology and advanced computing systems, the demand for efficient thermal management solutions is expected to rise, further creating a positive diamond coating market overview. Diamond coatings offer a viable solution to meet these requirements, thereby driving the market growth.

Significant Advanced in Medical Device Technology

Advances in medical device technology is one of the major diamond coatings market trends, particularly in the development of more durable and biocompatible implants. Diamond coatings are utilized in various medical applications, including dental implants and orthopedic joints, due to their excellent biocompatibility, non-toxicity, and resistance to wear and corrosion. The aging global population and increasing prevalence of chronic diseases have led to higher demand for medical implants and devices, further bolstering the market for diamond coatings. According to the WORLD HEALTH ORGANIZATION (WHO), the proportion of the global population above the age of 60 will almost double from 12% to 22% during 2015-2050. The ability of diamond coatings to extend the life of medical devices and improve patient outcomes is particularly valuable in the healthcare environment today, where cost-effectiveness and patient safety are paramount, thereby leading to a positive diamond coating market growth.

Diamond Coating Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on technology, substrate, and end-use industry.

Breakup by Technology:

- Chemical Vapour Deposition (CVD)

- Physical Vapour Deposition (PVD)

Chemical vapour deposition (CVD) accounts for the majority of the market share

The diamond coating research report has provided a detailed breakup and analysis of the market based on technology. This includes chemical vapour deposition (CVD), and physical vapour deposition (PVD). According to the report, chemical vapour deposition (CVD) represented the largest segment.

Chemical Vapor Deposition (CVD) dominates the market breakup by technology in the diamond coating industry primarily due to its versatility, efficiency, and the superior quality of coatings it produces. The CVD process allows for the deposition of pure, dense, and uniformly thick diamond films over large areas and on various substrates. This method is highly controllable, enabling the precise adjustment of gas mixtures, temperature, and pressure to tailor the physical properties of the diamond coatings according to specific application needs. Moreover, CVD technology has made significant advancements over the years, enhancing its scalability and reducing operational costs. This has made it increasingly accessible for industrial applications, thereby positively impacting the diamond coatings market value.

Breakup by Substrate:

- Metal

- Ceramic

- Composite

- Others

Metal holds the largest share of the industry

A detailed breakup and analysis of the market based on the substrate have also been provided in the report. This includes metal, ceramic, composite, and others. According to the report, metal accounted for the largest market share.

Metal substrates dominate the largest segment in the market breakup by substrate for diamond coatings due to their widespread applications across multiple industries, including automotive, aerospace, and manufacturing. Metals are the preferred choice because they provide an excellent foundation for diamond coatings, offering the necessary hardness and durability that these applications demand. The intrinsic properties of metals, such as high mechanical strength and thermal conductivity, make them ideal for enhancing with diamond coatings to extend tool life and improve performance in harsh environments.

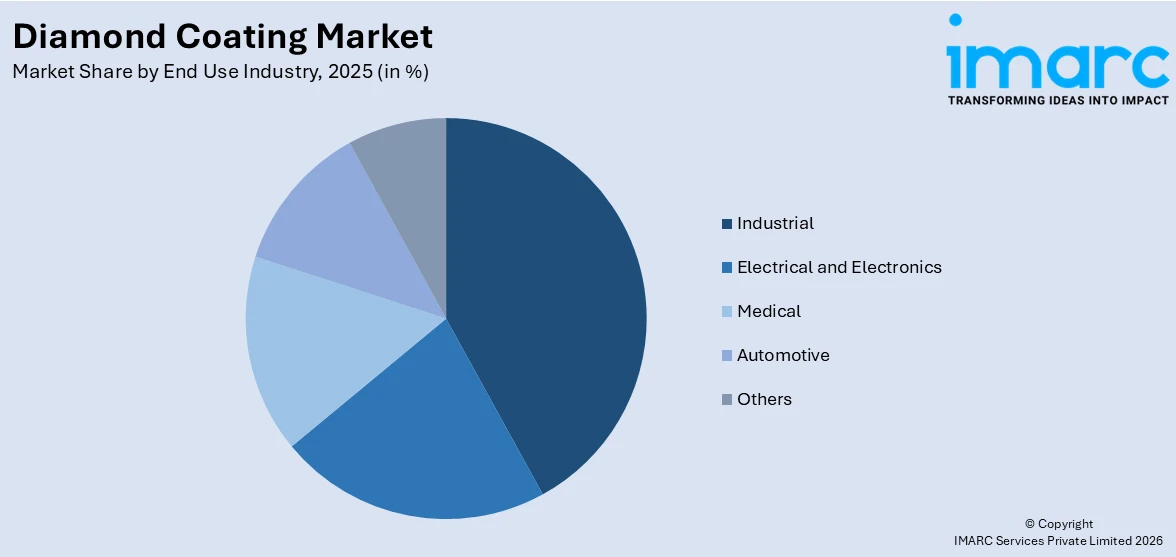

Breakup by End Use Industry:

Access the comprehensive market breakdown Request Sample

- Electrical and Electronics

- Medical

- Industrial

- Automotive

- Others

Industrial represents the leading market segment

The diamond coating market report has provided a detailed breakup and analysis of the market based on the end use industry. This includes electrical and electronics, medical, industrial, automotive, and others. According to the report, industrial represented the largest segment.

The industrial sector emerges as the largest segment in the market breakup by end-use industry for diamond coatings primarily due to the extensive and varied applications of diamond-coated tools and components across numerous manufacturing and processing industries. Diamond coatings are integral in enhancing the durability, efficiency, and performance of cutting, grinding, and drilling tools, which are crucial in industries such as automotive, aerospace, and heavy machinery. These sectors demand tools that can withstand harsh conditions and deliver precision, qualities that diamond coatings provide effectively. The unique properties of diamond, such as high thermal conductivity, exceptional hardness, and resistance to wear and corrosion, make it ideal for applications subjected to extreme environments and continuous use, leading to a significant growth in the diamond coating industry.

Breakup by Region:

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Asia Pacific leads the market, accounting for the largest diamond coating market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, Asia Pacific was the largest regional market for diamond coating.

Asia Pacific holds the distinction of being the largest segment in the market breakup by region for diamond coatings due to several compelling factors. The region is home to rapidly growing economies such as China and India, which have witnessed significant industrial growth and expansion in manufacturing sectors. These countries have become global hubs for automotive, electronics, and machinery manufacturing, all of which are key industries that extensively utilize diamond-coated tools and components for enhanced durability and performance. Additionally, the commitment of the region to advancing technology and increasing investments in research and development have fostered innovation in material science, including advanced coatings such as diamond coatings.

Competitive Landscape:

- The market research report has also provided a comprehensive analysis of the competitive landscape in the market. Detailed profiles of all major companies have also been provided. Some of the major diamond coating companies include Blue Wave Semiconductors Inc., Diamond Product Solutions, Endura Coatings LLC, JCS Technologies Pte Ltd., NeoCoat SA, OC Oerlikon Management AG, RobbJack Corporation, sp3 Diamond Technologies, and Surface Technology Inc.

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

- Key players in the diamond coating market are driving growth through several strategic initiatives aimed at enhancing product offerings and expanding their market reach. These efforts include significant investments in research and development (R&D) to innovate and improve the quality and application range of diamond coatings. By focusing on advancing coating technologies such as Chemical Vapor Deposition (CVD) and Physical Vapor Deposition (PVD), they are able to cater to a broader spectrum of industries, including automotive, aerospace, medical, and electronics, with more efficient and customized solutions. Moreover, according to the diamond coating market forecast, these players are actively engaging in partnerships and collaborations with other technology firms and research institutions to leverage collective expertise and drive technological advancements. These collaborations often lead to the development of new applications and the optimization of existing ones, enhancing market penetration and consumer satisfaction.

Diamond Coating Market News:

- October 3, 2023: HOYA VISION CARE launched Hi-Vision Meiryo Diamond, a premium coating with exceptional clarity and extended durability, offering protection against scratches, smudges, glare, and UV.

- December 2023: Ultrananocrystalline diamond (UNCD™) coating offers a promising solution for enhancing the performance and biocompatibility of implantable medical devices. The use of UNCD™ coatings can potentially reduce the risk of infections and improve the long-term stability of prostheses within the human body.

Diamond Coating Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| USDScope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technologies Covered | Chemical Vapour Deposition (CVD), Physical Vapour Deposition (PVD) |

| Substrates Covered | Metal, Ceramic, Composite, Others |

| End Use Industries Covered | Electrical and Electronics, Medical, Industrial, Automotive, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Blue Wave Semiconductors Inc., Diamond Product Solutions, Endura Coatings LLC, JCS Technologies Pte Ltd, NeoCoat SA, OC Oerlikon Management AG, RobbJack Corporation, sp3 Diamond Technologies, Surface Technology Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the global diamond coating market performed so far, and how will it perform in the coming years?

- What are the drivers, restraints, and opportunities in the global diamond coating market?

- What is the impact of each driver, restraint, and opportunity on the global diamond coating market?

- What are the key regional markets?

- Which countries represent the most attractive diamond coating market?

- What is the breakup of the market based on technology?

- Which is the most attractive technology in the diamond coating market?

- What is the breakup of the market based on the substrate?

- Which is the most attractive substrate in the diamond coating market?

- What is the breakup of the market based on the end use industry?

- Which is the most attractive end use industry in the diamond coating market?

- What is the competitive structure of the market?

- Who are the key players/companies in the global diamond coating market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the diamond coating market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global diamond coating market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the diamond coating industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)