Digital Twin Market Size, Share, Trends and Forecast by Type, Technology, End Use, and Region, 2026-2034

Global Digital Twin Market Size, Share, Trends & Forecast (2026-2034)

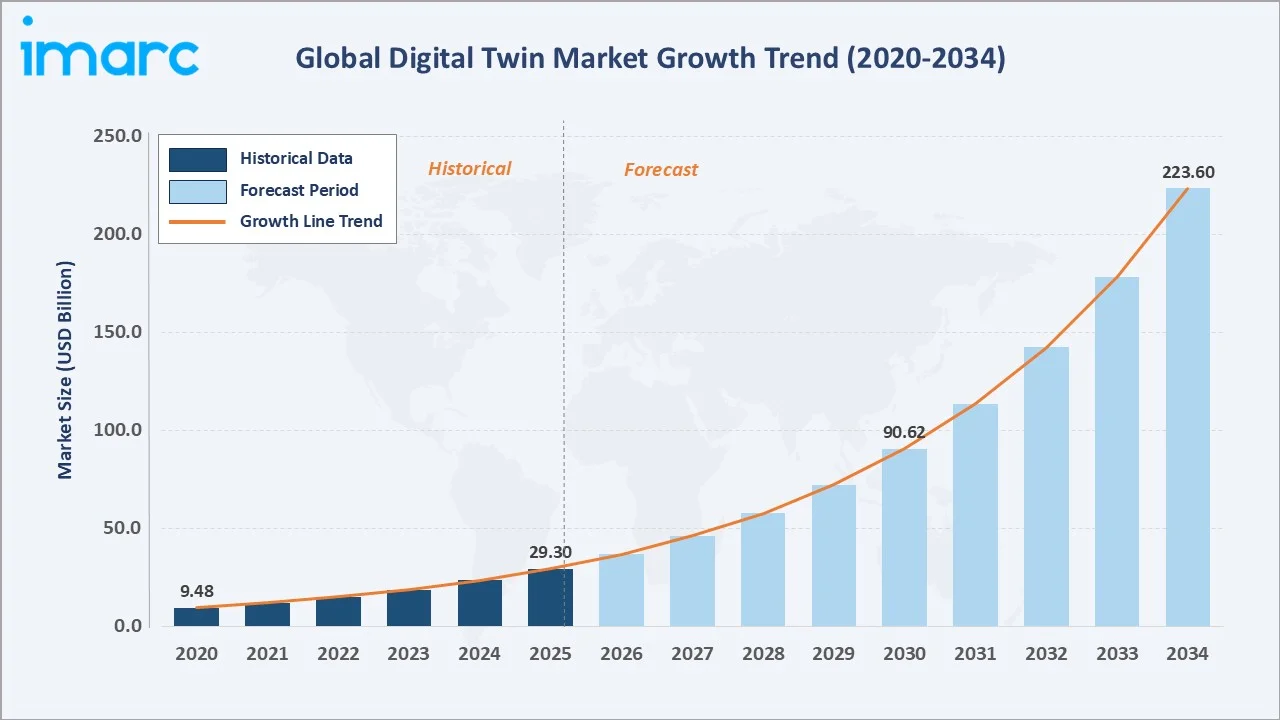

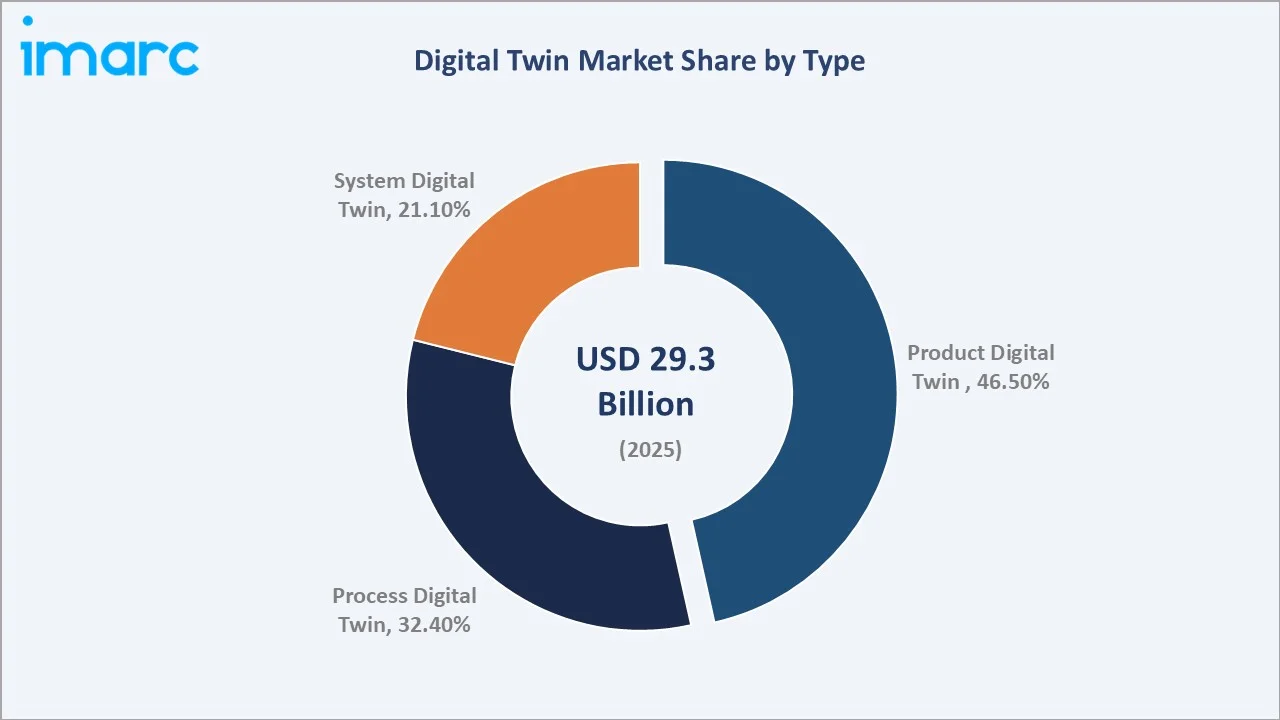

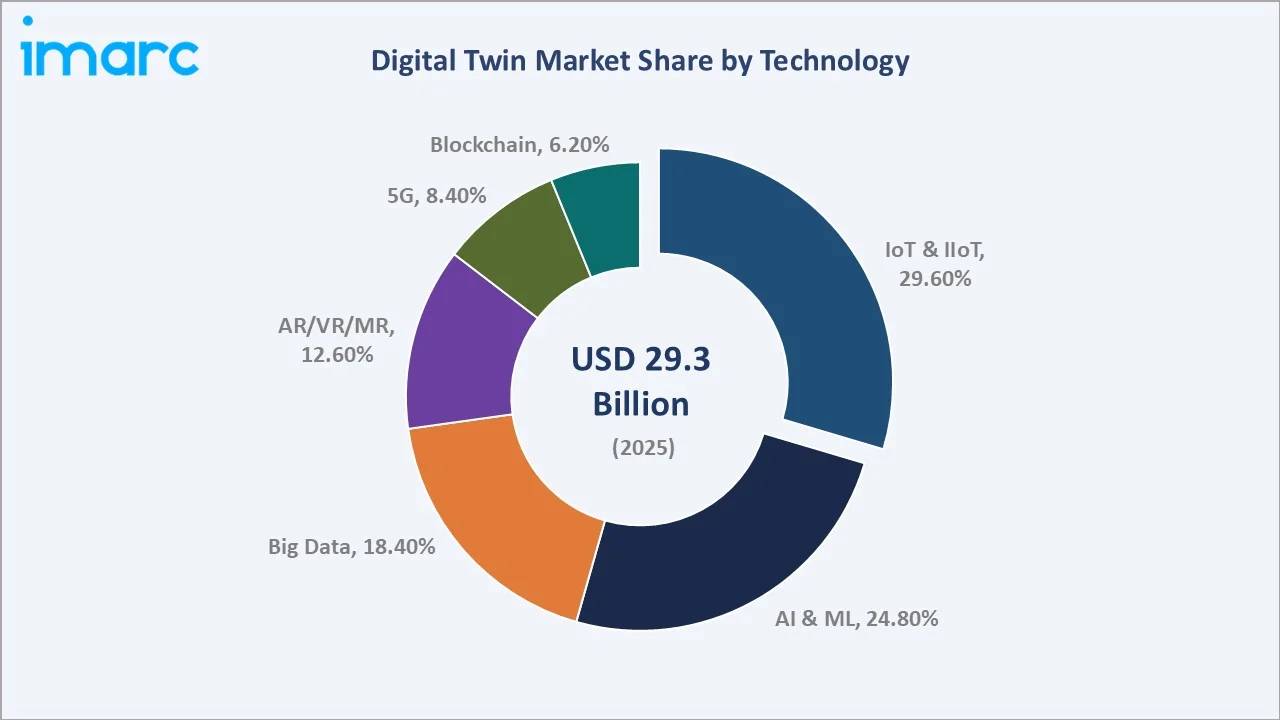

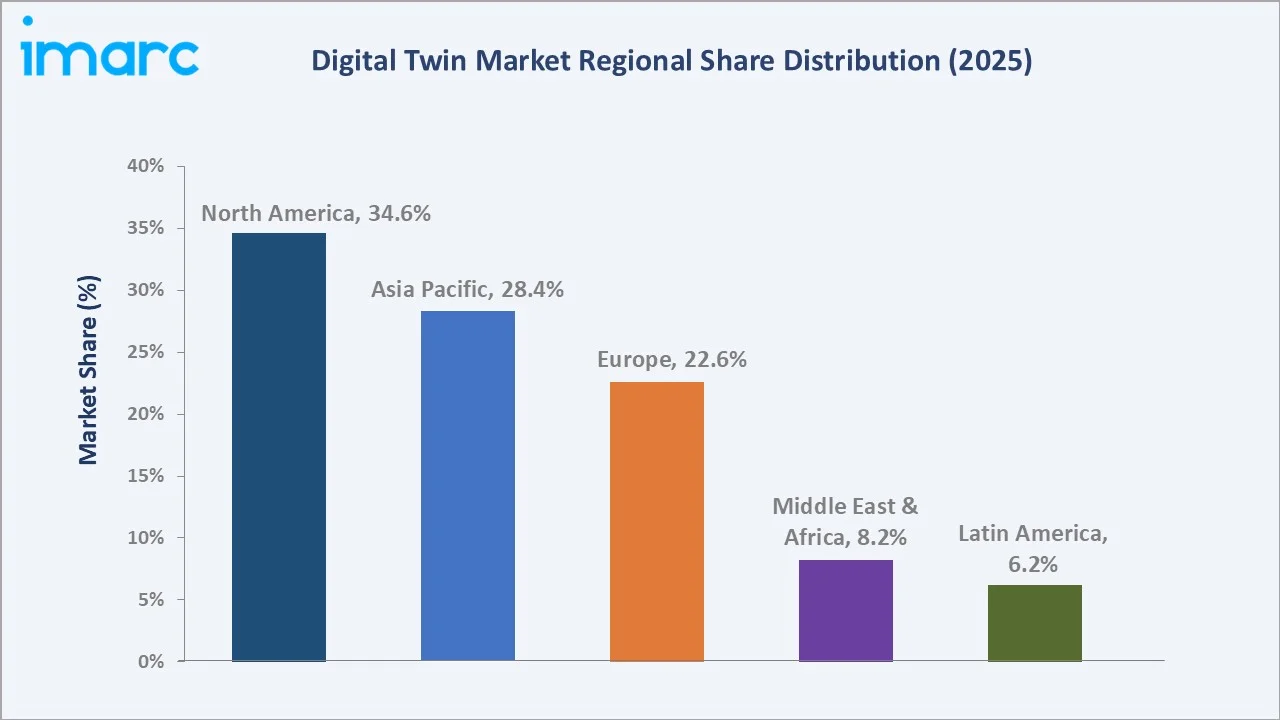

The global digital twin market was valued at USD 29.3 Billion in 2025 and is projected to reach USD 223.6 Billion by 2034, expanding at a CAGR of 25.33% during the forecast period (2026-2034). Rapid Industry 4.0 adoption with manufacturing companies invested $102 billion in Industry 4.0, accounting for 20% of the total manufacturing technology expenditure in 2021, surging demand for predictive maintenance, and the convergence of IoT, AI, and cloud computing are the primary growth catalysts. Product digital twins dominate with a 46.5% share in 2025, while IoT and IIoT technologies underpin 29.6% of the market. North America leads all regions with a 34.6% revenue share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 29.3 Billion |

|

Forecast Market Size (2034) |

USD 223.6 Billion |

|

CAGR (2026-2034) |

25.33% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (34.6%, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~28%, 2026-2034) |

The digital twin market from 2020 through 2034 expanded from USD 9.48 Billion in 2020 to USD 29.3 Billion in 2025, anchored at USD 90.6 Billion in 2030 before reaching USD 223.6 Billion by 2034.

To get more information on this market, Request Sample

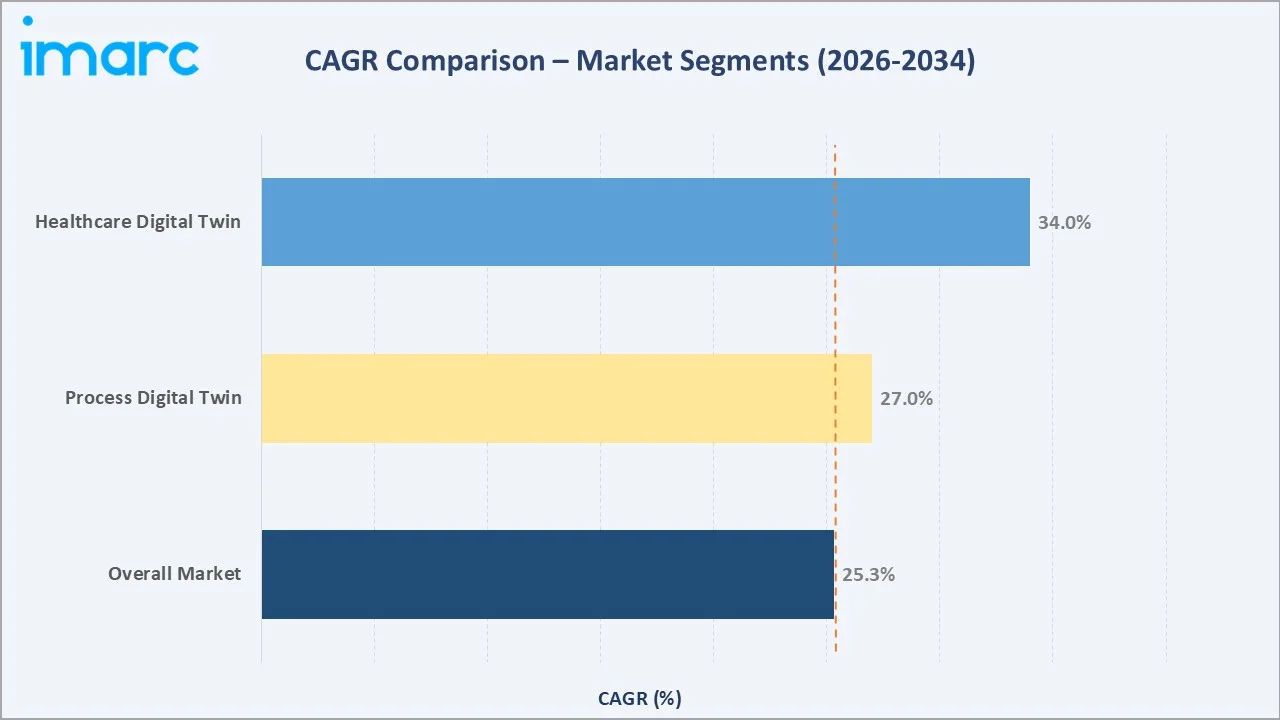

The divergence between the historical period and the forecast trajectory highlights the post-pandemic recovery acceleration. The overall market CAGR is 25.33%, the process digital twin segment is growing at a CAGR of 27.0%, and the healthcare digital twin segment is growing at a CAGR of 34.0%.

Executive Summary

The global digital twin market is experiencing a transformational expansion phase. Valued at USD 29.3 Billion in 2025, it is forecast to surpass USD 223.6 Billion by 2034, a compound annual growth rate of 25.33%. Predictive maintenance typically reduces machine downtime by 30% to 50%, driving rapid deployment across manufacturing, energy, and aerospace sectors globally.

Among the primary growth catalysts, the proliferation of connected industrial devices, with rising global IIoT connections, which created a fertile environment for digital twin deployment. Product digital twins command the largest market share at 46.5% (2025), primarily because they enable lifecycle simulation from design through decommissioning. Process digital twins follow at 32.4%, capturing demand from chemical plants, refineries, and semiconductor fabs seeking real-time process optimization.

Geographically, North America anchors market leadership with a 34.6% revenue share (2025), supported by heavy U.S. federal investment in smart manufacturing under the CHIPS Act. Asia Pacific is the most dynamic region, driven by China's industrial digitization under “Made in China 2025” and India's National Digital Twin initiative. Europe maintains a 22.6% share, underpinned by Germany's Industrie 4.0 framework and the EU Digital Compass 2030 policy agenda.

Key Market Insights

|

Insight |

Data |

|

Largest Type Segment |

Product Digital Twin – 46.5% share (2025) |

|

Leading Technology |

IoT and IIoT – 29.6% share (2025) |

|

Fastest Growing Segment |

Process Digital Twin – CAGR ~27% (2026-2034) |

|

Leading Region |

North America – 34.6% revenue share (2025) |

Key Analytical Observations Supporting The Above Data:

- Product digital twin dominates with a 46.5% share (2025), reflecting broad deployment in automotive, aerospace, and consumer electronics manufacturing for virtual product development and lifecycle management.

- IoT and IIoT lead the technology stack with 29.6% market share (2025), as over 1.4 billion consumer IoT devices and 13.3 billion enterprise IoT devices globally generate the real-time data streams essential for twin synchronization and accuracy.

- North America commands 34.6% revenue share (2025), backed by USD 52.7 billion in federal CHIPS Act funding and strong enterprise cloud infrastructure underpinning twin platform adoption.

Global Digital Twin Market Overview

Digital twin technology creates real-time virtual replicas of physical assets, processes, or entire systems by integrating data from IoT sensors, AI models, and simulation platforms. Originating in aerospace and defense applications, formalized by NASA's mirrored space vehicle concept, digital twins have evolved into a cross-industry strategic capability. The ecosystem spans hardware, connectivity, software, and services.

Applications span product lifecycle management, predictive maintenance, supply chain optimization, smart city planning, and clinical trial simulation in healthcare. Macroeconomic influences are strongly positive with global manufacturing output growth, creating persistent demand for operational efficiency tools. The total enterprise software market, within which digital twins operate, provides a broad commercial foundation for continued twin adoption.

Market Dynamics

To evaluate market opportunities, Request Sample

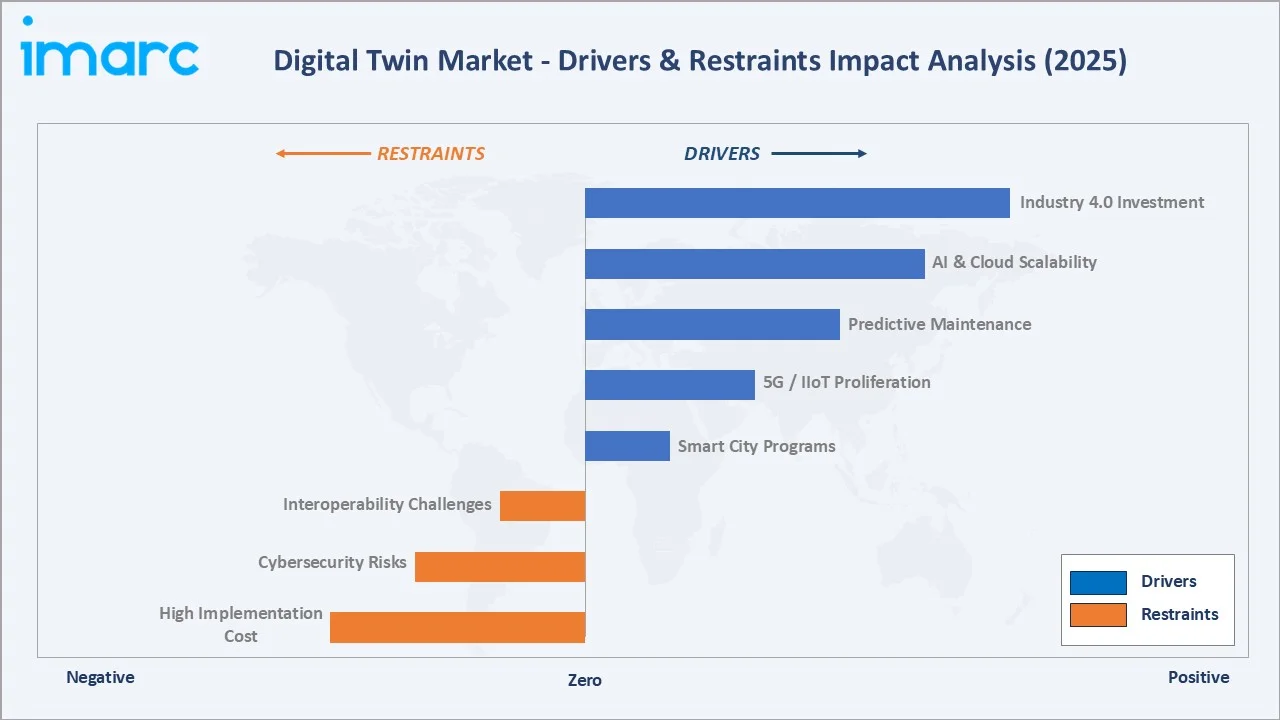

Market Drivers

- Industry 4.0 and Smart Manufacturing Surge: Global smart factory investments growth, directly accelerating digital twin deployments for real-time shop-floor monitoring and autonomous production optimization.

- Predictive Maintenance Demand: Unplanned equipment downtime costs industrial firms approximately USD 50 billion annually (2024). Digital twins reduce unplanned outages by up to 30% by enabling condition-based maintenance across critical assets.

- 5G and IIoT Proliferation: Global 5G connections surpassed 2.7 billion by 2025, enabling ultra-low-latency twin synchronization at scale, a critical technical prerequisite for real-time simulation in high-speed environments.

Market Restraints

- High Implementation Complexity and Cost: Enterprise-wide digital twin deployments typically require USD 5–15 million in initial investment, limiting adoption among mid-sized industrial firms.

- Data Security and Cybersecurity Risks: With digital twins mirroring critical infrastructure, cyberattack exposure is amplified, with over 900 million cyberattacks recorded worldwide between January and December 2025, raising deployment caution.

Market Opportunities

- Healthcare and Life Sciences Expansion: Digital patient twins represent an emerging market, enabling personalized medicine, surgical simulation, and clinical trial acceleration.

- Smart Cities and Urban Infrastructure: Over 1,000 cities globally have initiated smart city programs, with digital twin urban modeling representing one of the highest-value applications in the public sector.

Market Challenges

- Skilled Talent Scarcity: The global shortfall of data scientists and IoT engineers constrains the pace of enterprise twin implementation and optimization.

- Regulatory and Data Sovereignty Complexities: Cross-border data flows critical for global twin deployments face restrictions under GDPR (EU), PIPL (China), and emerging data localization laws in India, raising compliance costs significantly.

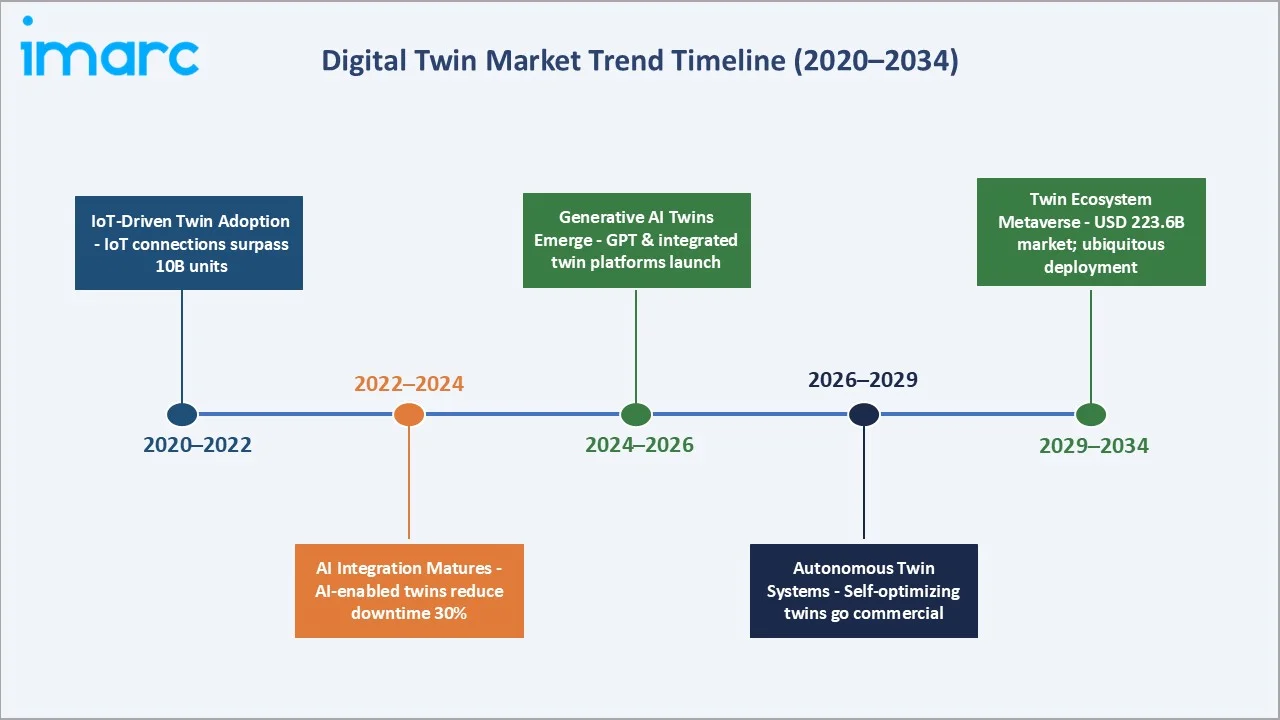

Emerging Market Trends

1. Autonomous Digital Twins Powered by Generative AI

Generative AI is enabling “self-updating” digital twins that autonomously refine simulation models based on new operational data without human intervention. Microsoft's Azure integrated GPT-4 capabilities in 2024, reducing model recalibration time. This trend is particularly transformative for aerospace and energy applications where environmental variables change rapidly.

2. Digital Twin of Organizations (DTO)

Beyond physical assets, enterprises are deploying digital twins of entire organizational structures, modelling supply chains, workforce allocation, and financial flows as interconnected virtual systems.

3. Integration of AR/VR with Digital Twins

Augmented and virtual reality interfaces are being layered onto digital twin platforms to create immersive operator environments. Boeing reduced aircraft wiring assembly time by 25% and error rates by over 40% using AR-assisted twin visualizations.

4. Blockchain-Secured Digital Twin Data Integrity

Blockchain integration with digital twins is gaining traction in pharmaceutical manufacturing and food supply chains where data immutability and regulatory traceability are paramount.

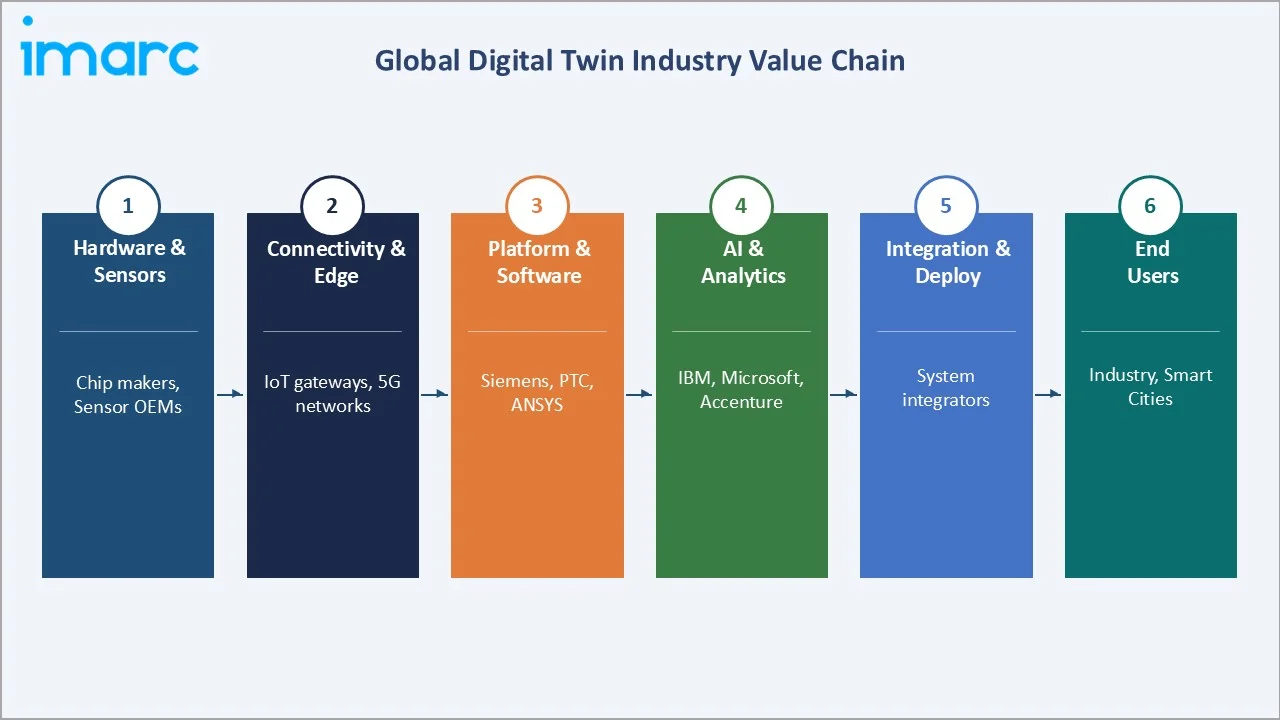

Industry Value Chain Analysis

The digital twin industry value chain is a multi-layered, technology-intensive ecosystem extending from foundational hardware through to end-user applications. Each layer depends on the performance and interoperability of the preceding stage, creating both integration challenges and consolidation opportunities.

|

Stage |

Key Players / Examples |

|

Hardware & Sensors |

Chip makers, sensor OEMs |

|

Connectivity & Edge |

IoT gateways, 5G networks |

|

Platform & Software |

Siemens Xcelerator, PTC ThingWorx, ANSYS Twin Builder |

|

AI & Analytics Layer |

IBM Maximo, Microsoft Azure AI, Accenture AI platforms |

|

Integration & Deployment |

System integrators |

|

End Users |

Aerospace, automotive, energy, healthcare, and smart city operators |

The most value-accretive layer in 2025 is the platform and software development stage, which captures approximately 38% of total market revenue. Platform vendors benefit from high switching costs and recurring subscription revenue models, generating EBIT margins of 22–28% among leading providers.

Technology Landscape in the Digital Twin Industry

IoT and IIoT Connectivity

IoT and IIoT technologies are the foundational data layer for all digital twin implementations, accounting for 29.6% of the technology market. Over 1.4 billion consumer IoT devices and 13.3 billion enterprise IoT devices globally. Industrial protocols enable seamless machine-to-twin data transmission at millisecond latency, forming the nervous system of every operational twin deployment.

Artificial Intelligence and Machine Learning

AI and ML technologies transform raw sensor data into predictive insights, enabling failure prediction in advance across rotating machinery. Reinforcement learning algorithms are increasingly used to optimize digital twin control policies in autonomous systems, reducing energy consumption in pilot deployments.

Big Data Analytics

Big data analytics holds an 18.4% technology market share (2025). Digital twin platforms in large automotive plants process up to 5 terabytes of sensor data per day per facility, requiring enterprise-grade data lakes and stream processing engines.

AR/VR/MR and 5G

AR/VR/MR interfaces (12.6% share, 2025) and 5G connectivity (8.4% share, 2025) are increasingly co-deployed to enable mobile, immersive twin interactions on the factory floor. 5G connections globally surpassed 2.7 billion by 2025. 5G's sub-1ms latency and 10 Gbps throughput eliminate cable tethering constraints of earlier AR/VR deployments.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Product Digital Twin |

46.5% |

2025 |

|

Technology |

IoT and IIoT |

29.6% |

2025 |

|

End Use |

Automotive and Transportation |

17.5% |

2025 |

|

Region |

North America |

34.6% |

2025 |

By Type

Product digital twin is the dominant segment with a 46.5% market share in 2025. These twins replicate individual physical products, from automotive components to consumer electronics, enabling virtual testing, design iteration, and field performance monitoring.

To access detailed market analysis, Request Sample

Process digital twin holds a 32.4% share (2025), with fastest growth potential driven by demand in pharmaceutical manufacturing, where the FDA's Pharma 4.0 initiative explicitly endorses digital twin process validation.

System digital twin accounts for 21.1% of market revenue (2025). These large-scale twins model entire integrated systems, from national power grids to smart city infrastructure. Singapore's Virtual Singapore platform and the UK's National Digital Twin Programme are among the highest-profile system twin deployments, each covering entire urban environments.

By Technology

IoT and IIoT technology dominates with a 29.6% market share (2025). AI and Machine Learning follows at 24.8%, providing the cognitive layer that transforms sensor data into actionable predictions. Big Data Analytics (18.4%) underpins the data management infrastructure critical to twin operation at enterprise scale. AR/VR/MR (12.6%) and 5G (8.4%) enable immersive and mobile deployment scenarios, while Blockchain (6.2%) is primarily applied in regulatory and traceability-intensive verticals.

The technology landscape is consolidating around platform-centric architectures where IoT connectivity, AI analytics, and AR visualization are offered as integrated suites. Vendors offering all five core technologies within a unified platform command a pricing premium over point-solution providers.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

34.6% |

Industry 4.0, CHIPS Act, federal IoT funding |

|

Asia Pacific |

28.4% |

China Made in China 2025, India smart city program |

|

Europe |

22.6% |

Industrie 4.0 (Germany), EU Digital Compass 2030 |

|

Middle East & Africa |

8.2% |

Saudi Vision 2030, NEOM city, oil & gas digitization |

|

Latin America |

6.2% |

Brazil manufacturing digitization, Mexico nearshoring |

North America's 34.6% market share (2025) is deeply entrenched. The US funding to digital twin programs such as the Biden administration announced $285 million in federal funding in May 2024 and inviting applications to create an institute in the U.S. focused on launching digital twin projects for the semiconductor industry. Canada's digital twin adoption in oil sands operations adds incremental regional demand through energy-sector-focused deployments.

Asia Pacific's 28.4% share (2025) masks divergent national dynamics. India's National Digital Twin Program is accelerating infrastructure and urban applications. Japan's Society 5.0 initiative prioritizes twin-enabled human-centered smart manufacturing deployments. Europe's 22.6% share (2025) is anchored by Germany, the continent's largest individual market, where Industrie 4.0 has driven twin adoption of large manufacturers.

Competitive Landscape

The global digital twin market is moderately consolidated at the enterprise platform level. The top five vendors, Siemens, GE Vernova, Microsoft, IBM, and PTC, collectively command approximately 38–42% of the global market revenues in 2025, while hundreds of specialist vendors and regional system integrators populate the remaining share.

|

Company Name |

Brand / Platform/ Products |

Market Position |

Core Strength |

|

Siemens AG |

Siemens Xcelerator |

Market Leader |

End-to-end digital twin portfolio, industrial IoT leadership |

|

GE Vernova |

Asset Digital Twins, Grid Digital Twins, and Process Digital Twins |

Market Leader |

Asset performance management, industrial cloud analytics |

|

Microsoft Corporation |

Azure Digital Twins |

Strong Challenger |

Cloud-native twin platform, AI integration at scale |

|

IBM Corporation |

IBM Maximo |

Strong Challenger |

AI-powered asset management, enterprise-scale deployments |

|

Dassault Systèmes |

3DEXPERIENCE |

Specialist Leader |

3D modeling, PLM, virtual manufacturing simulation |

|

ANSYS Inc. (Synopsys) |

Ansys Twin Builder |

Emerging |

Physics-based simulation twins, engineering-grade fidelity |

|

ABB Ltd |

ABB Ability |

Established |

Energy and automation digital twins, industrial robotics |

|

Accenture Plc |

Accenture Digital Twin |

Integrator |

Consulting-led deployment, cross-industry implementation |

|

AVEVA Group plc (Schneider Electric) |

AVEVA - Connect |

Established |

Process industry twins, operations management at scale |

Platform breadth, AI integration depth, and vertical-specific expertise are the three primary competitive differentiators for the market players.

Key Company Profiles

Siemens AG

Siemens AG is the global market leader in industrial digital twin solutions. Its Siemens Xcelerator platform serves as an open digital business platform integrating digital twin, IoT, and industrial automation capabilities into a unified ecosystem that spans design, simulation, and operations.

- Product Portfolio: Siemens Xcelerator suite, including Teamcenter, NX, and Simcenter platform for industrial twin deployments across automotive, aerospace, and energy sectors globally.

- Recent Developments: In January 2026, Siemens introduced Digital Twin Composer, a new software solution that enables the creation of large-scale Industrial Metaverse environments.

- Strategic Focus: Democratizing digital twin access for mid-market industrial firms through SaaS-based Xcelerator offerings, deepening sustainability-focused twin applications for carbon-neutral factory programs.

Microsoft Corporation

Microsoft is the leading cloud-native digital twin platform provider, leveraging Azure's global infrastructure to deliver scalable twin environments.

- Product Portfolio: Azure Digital Twins forming a complete cloud-native twin deployment stack from sensor connectivity to analytics visualization.

- Recent Developments: In May 2025, Microsoft unveiled the preview of the digital twin builder within Microsoft Fabric Real-Time Intelligence. This new feature is designed to help organizations connect their physical and digital worlds, establishing an AI-ready foundation for their operations.

- Strategic Focus: Expanding into healthcare (digital patient twin), smart buildings, and supply chain twin applications through strategic ISV partnerships and Azure Marketplace ecosystem development.

IBM Corporation

IBM's digital twin strategy centers on Maximo Application Suite, an AI-powered enterprise asset management platform deployed across utilities, transportation, and manufacturing.

- Product Portfolio: IBM Maximo Application Suite with embedded digital twin capabilities.

- Recent Developments: In January 2026, Datavault AI, a leader in instant data monetization and enterprise digital twins, announced its plans to deliver enterprise-grade artificial intelligence performance at the edge in New York and Philadelphia, through an expanded partnership with IBM.

- Strategic Focus: Asset-intensive industries, AI-first twin applications for sustainability compliance, hybrid cloud deployment models for regulated and mission-critical industries.

Dassault Systèmes

Dassault Systèmes is the global leader in 3D simulation and PLM-based digital twins. Its “virtual twin experience” philosophy positions physical-to-virtual fidelity as the company's primary differentiation against platform-oriented competitors.

- Product Portfolio: CATIA, SIMULIA, DELMIA, and ENOVIA, integrated on the 3DEXPERIENCE platform, enabling product design, physics simulation, virtual manufacturing, and collaborative lifecycle twins.

- Recent Developments: In January 2026, Dassault Systèmes opened its Center of Excellence (CoE) for Virtual Twin & Artificial Intelligence and Industry Solutions Lab at the Vietnam National Innovation Center (NIC) in Hanoi.

- Strategic Focus: Life sciences and healthcare virtual twins; expanding cloud-native 3DEXPERIENCE Works for mid-market SMEs; deepening aerospace structural simulation twin capabilities with physics-based fidelity.

Market Concentration Analysis

The global digital twin market exhibits moderate concentration at the enterprise platform tier. The top five vendors, Siemens, GE, Microsoft, IBM, and PTC, collectively generate approximately 38–42% of total market revenues in 2025. This concentration is higher in the industrial manufacturing subsegment and lower in the smart city and healthcare subsegments, where specialized vendors and government entities hold significant market positions.

Market fragmentation is pronounced in the services and integration layer, where regional system integrators and niche consultancies compete globally. The presence of open-source digital twin frameworks is further democratizing market entry, enabling mid-tier industrial software vendors to launch twin products with lower R&D investment requirements.

Investment & Growth Opportunities

Fastest Growing Segments

Process digital twins growing at a CAGR of ~27%, system digital twins for smart cities at a CAGR of ~29%, and healthcare digital patient twins at a CAGR of ~34% represent the three highest-growth investment vectors through 2034. These segments collectively address a total addressable market, with pharma regulatory compliance and urban infrastructure digitization as the most commercially immediate entry points for investors.

Emerging Market Expansion

India, Vietnam, and Saudi Arabia represent the three highest-priority emerging market opportunities within the digital twin landscape. India's National Digital Twin Program targets infrastructure and smart manufacturing deployments. Saudi Arabia's NEOM city project, one of the world's largest active urban digital twin deployments, represents an incremental technology investment opportunity.

Venture Investment Trends

Key investment themes include generative AI-native twin platforms, autonomous digital twin agents, and industry-specific vertical twins for healthcare, agriculture, and retail.

- Key growth bets: generative AI twin co-pilots, digital thread continuity platforms, and cross-border enterprise twin ecosystems enabling supplier-to-OEM virtual collaboration.

- ESG-aligned investors are increasingly targeting sustainability-focused twin applications, carbon accounting, energy optimization, and ethical supply chain traceability, within their digital infrastructure portfolios.

- Institutional PE interest in multi-vertical digital twin platform roll-ups remains elevated, particularly in Southeast Asia and the GCC region, where industrial digitization spending is growing fastest.

Future Market Outlook (2026-2034)

The global digital twin market is poised for one of the most sustained high-growth trajectories of any enterprise technology category through 2034. From a base of USD 29.3 Billion in 2025, the market is forecast to reach USD 223.6 Billion by 2034, representing an absolute value addition of USD 194.3 Billion over the nine-year forecast horizon. This expansion is underpinned by four structural forces: industrial digitization, sustainability mandates, AI-driven autonomy, and infrastructure modernization.

Technological disruptions will reshape market dynamics significantly between 2026 and 2030. Quantum computing integration with digital twin simulation is projected to reduce complex aerodynamic and materials simulation runtimes from hours to seconds by 2028–2030. Autonomous digital twins capable of self-optimization without human input are expected to reach commercial viability in industrial settings by 2027, fundamentally altering the operating model for predictive maintenance programs globally.

Research Methodology

Primary Research

Primary research for this report included structured interviews and surveys conducted with over 180 industry participants in 2025, comprising digital twin platform executives, industrial IoT engineers, procurement managers, end-use industry leaders, and investment professionals across North America, Europe, Asia Pacific, and the Middle East. Primary insights were used to validate quantitative market estimations and assess emerging deployment trends.

Secondary Research

Secondary research encompassed a comprehensive review of company annual reports, regulatory filings, trade publications, industry databases, and government digital strategy documents. Over 320 secondary sources across 28 countries were reviewed, triangulated, and synthesized to construct a consistent global market picture aligned with current deployment realities.

Forecasting Models

Market size estimations and growth projections were derived using a combination of bottom-up and top-down forecasting models. Inputs include GDP growth indices, Industry 4.0 investment trajectories, IoT device proliferation curves, and historical twin vendor revenue growth. Scenario analysis was applied to account for geopolitical and technology adoption uncertainty.

Digital Twin Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Product Digital Twin, Process Digital Twin, System Digital Twin |

| Technologies Covered | IoT and IIoT, Blockchain, Artificial Intelligence and Machine Learning, Augmented Reality, Virtual Reality and Mixed Reality, Big Data Analytics, 5G |

| End Uses Covered | Aerospace and Defense, Automotive and Transportation, Healthcare, Energy and Utilities, Oil and Gas, Agriculture, Residential and Commercial, Retail and Consumer Goods, Telecommunication, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Siemens AG, GE Vernova,Microsoft Corporation, IBM Corporation, Dassault Systèmes, ANSYS Inc. (Synopsys), ABB Ltd, Accenture Plc, AVEVA Group plc (Schneider Electric), etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the digital twin market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global digital twin market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the digital twin industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Digital Twin Market Report

The global digital twin market was valued at USD 29.3 Billion in 2025 and is projected to reach USD 223.6 Billion by 2034, growing at a CAGR of 25.33% during the forecast period.

North America is the dominant region, accounting for 34.6% of global digital twin market revenues in 2025, backed by robust industrial IoT infrastructure and major federal smart manufacturing investments.

Asia Pacific is the fastest-growing region, driven by China's industrial digitization, India's National Digital Twin Program, and Japan's Society 5.0 manufacturing modernization initiatives through 2034.

Key drivers include Industry 4.0 adoption, predictive maintenance demand cutting downtime by up to 30%, 5G proliferation exceeding 2.7 billion connections in 2025, and AI-enabled simulation capabilities.

Product digital twin is the largest segment with a 46.5% market share (2025), driven by applications in automotive, aerospace, and electronics product lifecycle management and virtual prototyping.

IoT and IIoT leads with 29.6% technology market share (2025), providing the real-time data streams essential for digital twin synchronization across all industrial deployment scenarios globally.

The leading companies include Siemens AG, GE Vernova, Microsoft Corporation, IBM Corporation, Dassault Systèmes, ANSYS Inc. (Synopsys), ABB Ltd, Accenture Plc, and AVEVA Group plc (Schneider Electric).

Key trends include generative AI-autonomous twins, Digital Twin of Organizations, AR/VR-immersive interfaces, sustainability-driven ESG twins, and blockchain-secured data integrity frameworks through 2034.

Key challenges include high implementation costs per enterprise deployment, cybersecurity risks rising 28%, talent shortages, and data sovereignty regulatory complexity across geographies.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)