Dimethyl Ether Market Size, Share, Trends and Forecast by Raw Material, Application, End-Use Industry, and Region, 2026-2034

Global Dimethyl Ether Market Size, Share, Trends & Forecast (2026-2034)

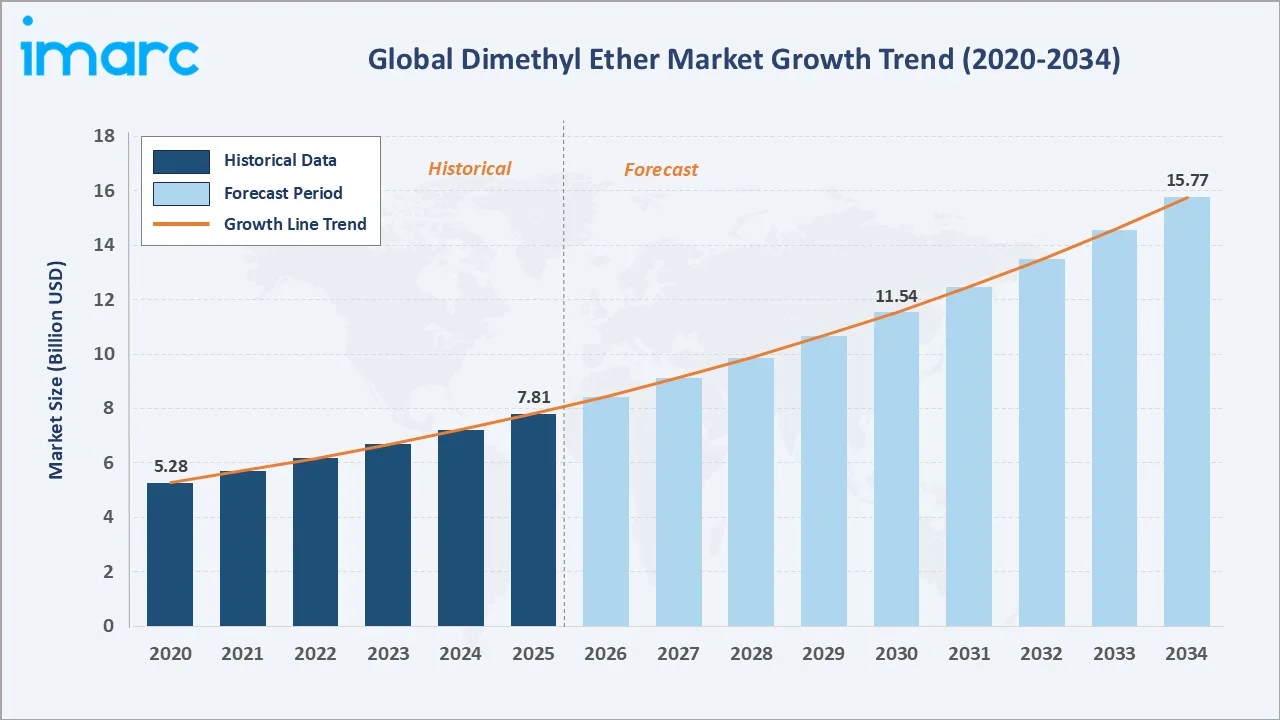

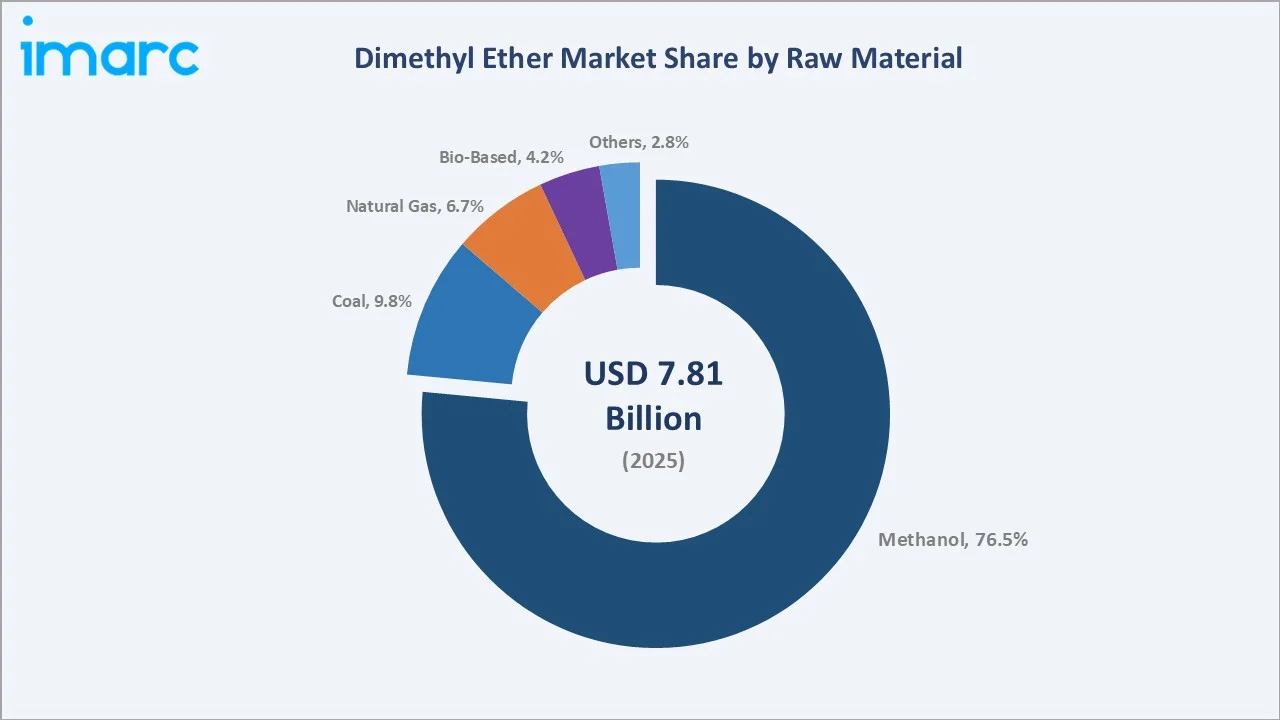

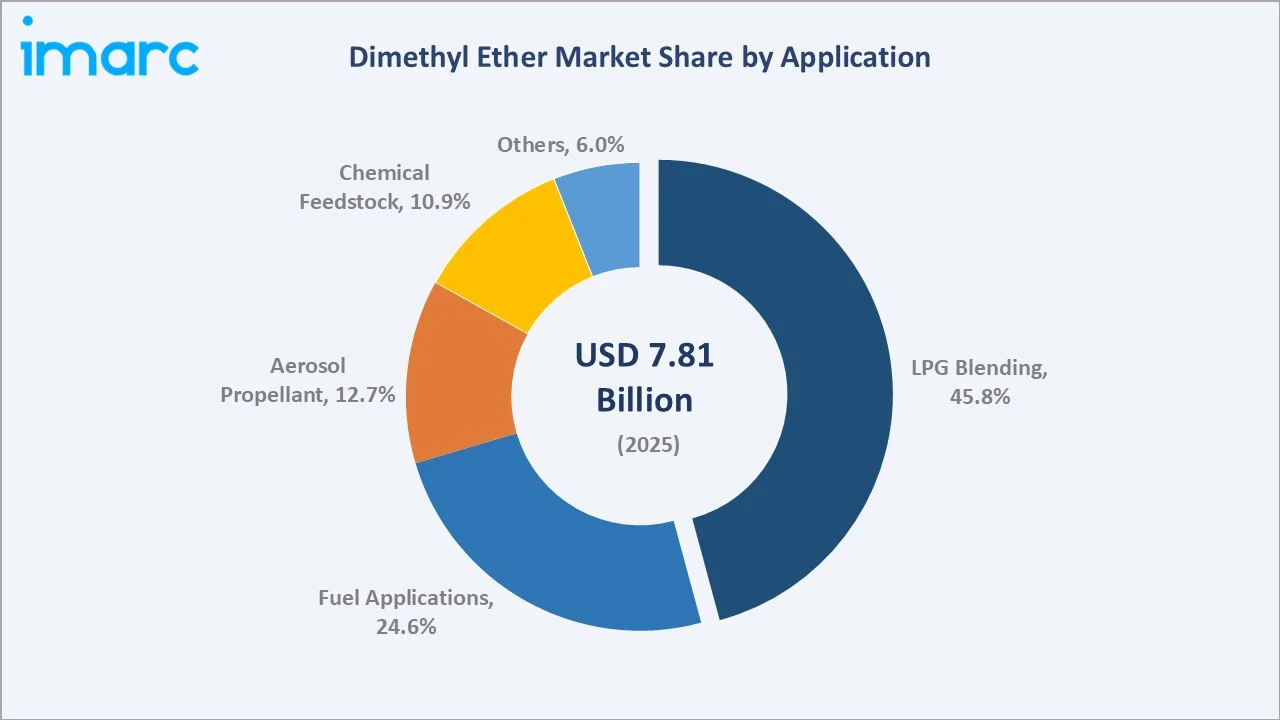

The global dimethyl ether market size reached USD 7.81 Billion in 2025 and is projected to reach USD 15.77 Billion by 2034, exhibiting a CAGR of 8.12% during 2026-2034. Surging demand for clean-burning LPG substitute fuels, robust expansion of aerosol propellant applications, and Asia-Pacific's coal-to-DME energy programs are the primary forces driving dimethyl ether market growth.

Methanol-derived DME dominates the raw material mix at 76.5% in 2025, while LPG blending leads the application segment at 45.8%.

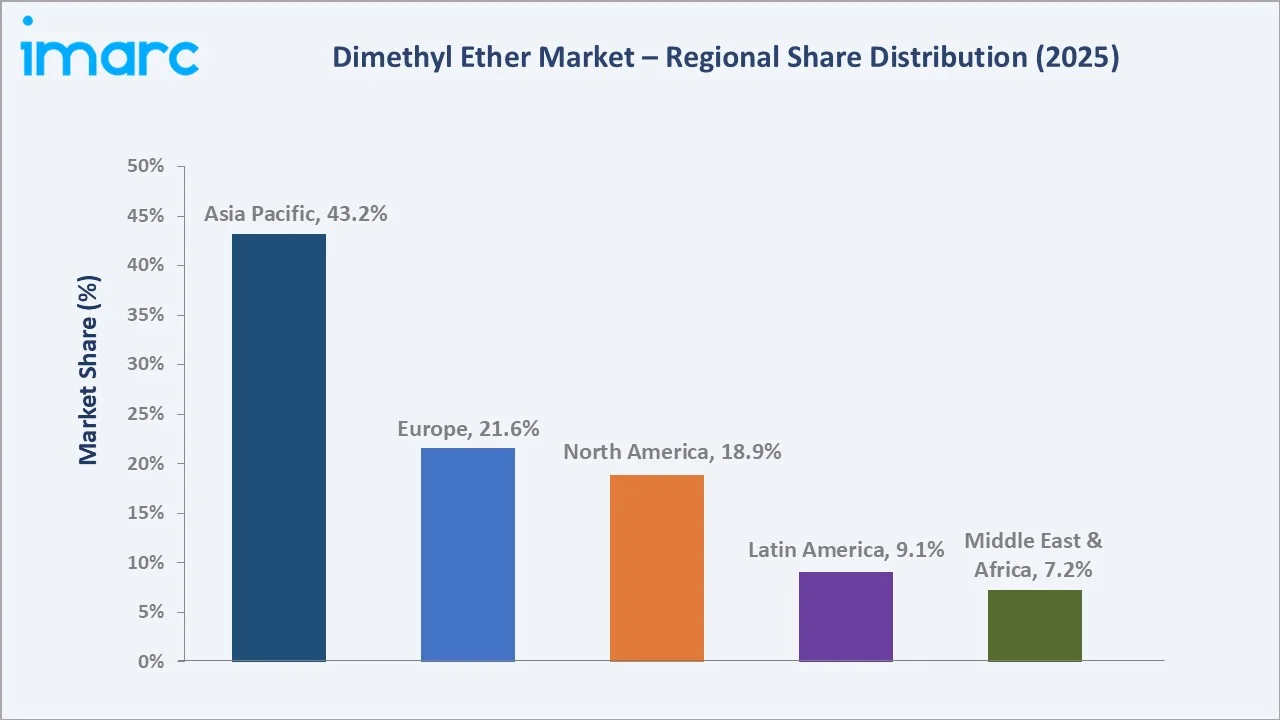

Asia Pacific commands a dominant 43.2% regional share in 2025, reflecting China and India's unparalleled production capacity and policy-driven demand.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 7.81 Billion |

|

Forecast Market Size (2034) |

USD 15.77 Billion |

|

CAGR (2026-2034) |

8.12% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (43.2% share, 2025) |

|

Second Largest Region |

Europe (21.6% share, 2025) |

|

Leading Raw Material |

Methanol (76.5%, 2025) |

|

Leading Application |

LPG Blending (45.8%, 2025) |

The global dimethyl ether market growth trajectory from 2020 through 2034, with historical expansion to USD 7.81 Billion in 2025, reflects consistent energy transition-driven demand, while the forecast to USD 15.77 Billion captures accelerating clean fuel adoption, LPG blending mandates across Asia-Pacific, and bio-based DME commercialization.

To get more information on this market, Request Sample

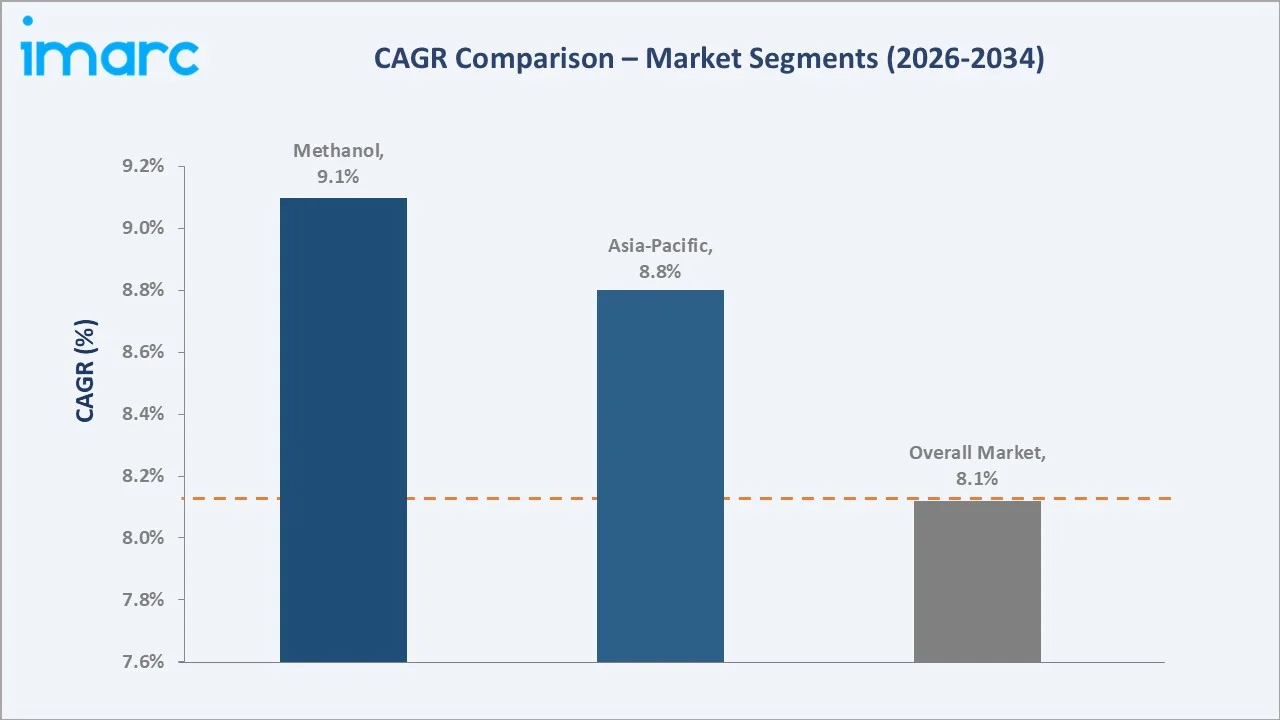

The CAGR trajectories across key raw material, application, and regional sub-segments, with bio-based DME at ~11.2% CAGR and Asia Pacific at ~8.8% CAGR, represent the fastest-growing categories within the global dimethyl ether industry analysis through 2034.

Executive Summary

The global dimethyl ether market is on a sustained growth trajectory from USD 7.81 Billion in 2025 to USD 15.77 Billion by 2034. DME, a clean-burning chemical intermediate and fuel substitute with near-zero particulate emissions, benefits from the global energy transition and environmental regulatory pressure across multiple end-use applications.

Methanol dominates raw material sourcing at 76.5% in 2025, owing to the commercial maturity of catalytic dehydration of methanol processes and lower capital requirements compared to coal- or gas-to-DME routes. Coal-derived DME at 9.8% remains significant in China through large-scale coal-to-DME projects supported by national energy security policy.

LPG blending leads application demand at 45.8% in 2025, reflecting government mandates across India, Indonesia, and South Korea to blend DME into LPG cylinders for household cooking fuel. Fuel applications at 24.6% capture commercial vehicle and power generation DME demand, while aerosol propellant at 12.7% benefits from F-Gas regulatory phase-down.

Asia Pacific dominates at 43.2% in 2025, driven by China's coal-to-DME infrastructure and India's LPG-DME blending program. Europe at 21.6% and North America at 18.9% follow, driven by aerosol propellant demand and clean transportation fuel mandates respectively.

Key Market Insights

|

Insight |

Data |

|

Largest Raw Material |

Methanol - 76.5% share (2025) |

|

Leading Application |

LPG Blending - 45.8% share (2025) |

|

Leading Region |

Asia Pacific - 43.2% share (2025) |

|

Second Largest Region |

Europe - 21.6% share (2025) |

|

Top Companies |

Nouryon, Mitsubishi Gas Chemical Company, Inc., Grillo-Werke AG, Oberon Fuels, Inc. |

Key Analytical Observations Expanding on the Above Data:

- Methanol at 76.5% in 2025 dominates because catalytic dehydration of methanol is the lowest-capital-cost DME production route. Established methanol production infrastructure globally supplies the DME synthesis chain at competitive economics, making it the default feedstock choice across all major DME-producing regions.

- LPG blending at 45.8% in 2025 leads because regulatory mandates make it the most volume-scalable application. Government-backed blending programs across India and Southeast Asia create assured demand at national scale, providing offtake visibility that supports large DME capacity investments.

- Asia Pacific's 43.2% dominance reflects China's unparalleled coal-to-DME production capacity and India's rapidly scaling LPG-DME blending program under national energy policy, creating the world's largest combined DME supply and demand concentration in a single region.

- Europe at 21.6% benefits from DME's classification as a low-GWP aerosol propellant substitute for HFCs, with EU F-Gas Regulation phase-down driving aerosol industry conversion toward DME across personal care, household, and industrial spray product categories.

Global Dimethyl Ether Market Overview

Dimethyl ether (CH₃-O-CH₃) is the simplest ether, existing as a colorless gas at standard conditions with a low boiling point, making it storable and transportable in liquid form under moderate pressure. DME is produced via methanol dehydration, coal gasification, natural gas reforming, or biomass conversion, offering broad feedstock flexibility.

The global ecosystem integrates feedstock producers, DME synthesis operators, pressurized storage and transport infrastructure providers, downstream blenders and formulators, and diverse end-use industries spanning energy, automotive, aerosol, and specialty chemicals. DME's physical properties closely resemble LPG, enabling it to leverage existing LPG infrastructure with limited modification.

Market Dynamics

To evaluate market opportunities, Request Sample

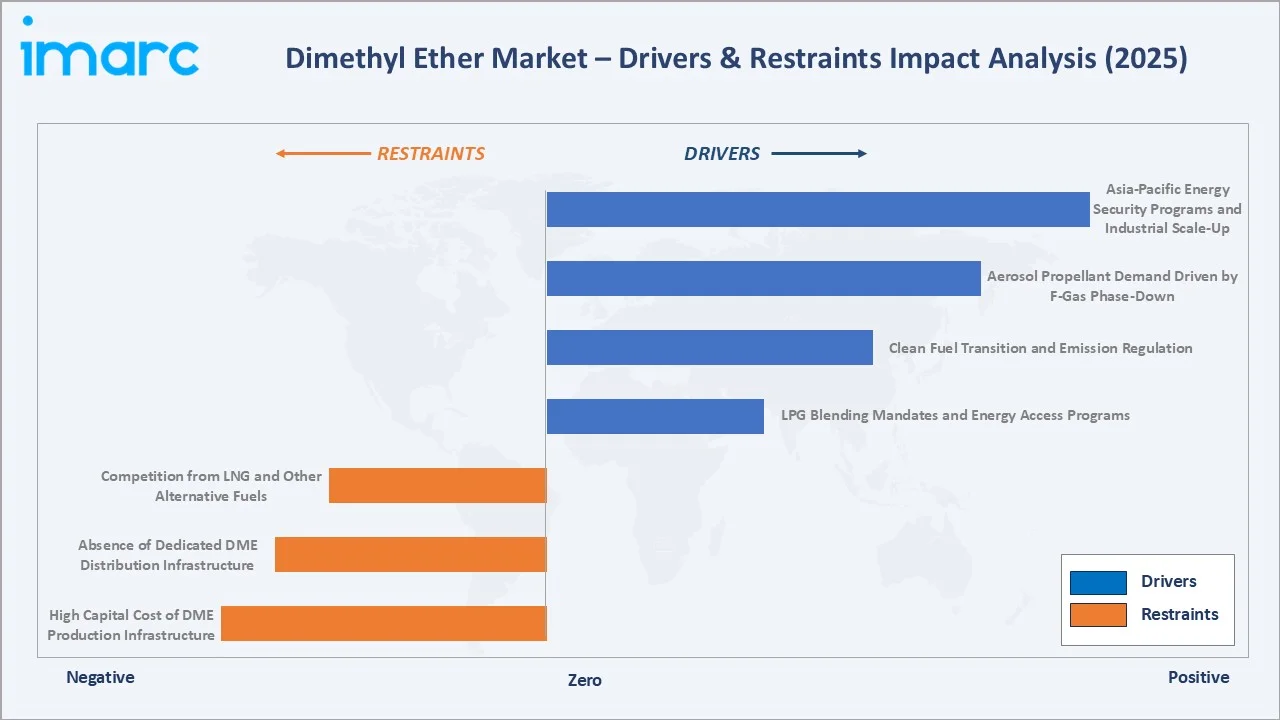

Market Drivers

- LPG Blending Mandates and Energy Access Programs: Government mandates across India, Indonesia, and South Korea requiring DME blending into LPG cylinders create large, policy-assured demand. National blending programs targeting a significant DME share in household cooking fuel represent a multi-million tonne annual demand driver.

- Clean Fuel Transition and Emission Regulation: DME's near-zero particulate matter and SOx emissions, high cetane number, and compatibility with modified diesel engines position it as a preferred clean transportation fuel under tightening emission norms globally across road transport and maritime applications.

- Aerosol Propellant Demand Driven by F-Gas Phase-Down: The EU F-Gas Regulation's progressive phase-down of HFC propellants in aerosol applications is driving aerosol formulators toward DME as a cost-effective, low-GWP substitute across personal care, household cleaning, and industrial spray product categories.

- Asia-Pacific Energy Security Programs and Industrial Scale-Up: China's coal-to-DME programs leverage domestic coal reserves to produce a clean-burning energy carrier, reducing import dependency. India's Methanol Economy Mission and IOCL-led DME blending initiative support domestic DME production capacity development.

Market Restraints

- High Capital Cost of DME Production Infrastructure: Greenfield DME plants require significant capital expenditure for integrated methanol-to-DME or coal-to-DME capacity at commercial scale, limiting new entrants and restricting the pace of capacity expansion to meet growing demand.

- Absence of Dedicated DME Distribution Infrastructure: DME requires specialized pressurized distribution equipment, largely separate from existing LPG or natural gas infrastructure, generating incremental last-mile distribution costs that limit market penetration in regions with underdeveloped energy logistics networks.

- Competition from LNG and Other Alternative Fuels: LNG, biogas, and hydrogen are increasingly competing with DME in the commercial vehicle and power generation clean fuel segments, particularly in markets where LNG infrastructure is already established and benefit from more advanced regulatory support.

Market Opportunities

- Bio-Based DME from Renewable Methanol and Biomass: Bio-DME produced from forestry residues, municipal waste, or green hydrogen-derived renewable methanol qualifies as a sustainable fuel under EU renewable energy directives, attracting premium pricing from decarbonization-committed industries and government incentive programs.

- DME as a Hydrogen Energy Carrier: DME's high hydrogen content and relative ease of liquid-phase storage make it a competitive hydrogen carrier. Chemical looping DME reforming for distributed hydrogen production is gaining research and commercial traction as a supply solution for emerging hydrogen fuel cell applications.

Market Challenges

- Material Compatibility and Engine Modification Requirements: DME's lower energy density compared to diesel necessitates engine modifications including larger fuel tanks, DME-compatible seals and elastomers, and adjusted fuel injection systems, adding original equipment manufacturer adoption cost and complexity.

- Feedstock Price Volatility Affecting Production Economics: DME production costs are directly linked to methanol and coal feedstock prices, which are subject to significant volatility driven by energy market cycles, trade policy changes, and supply chain disruptions, creating margin uncertainty for DME producers.

Emerging Market Trends

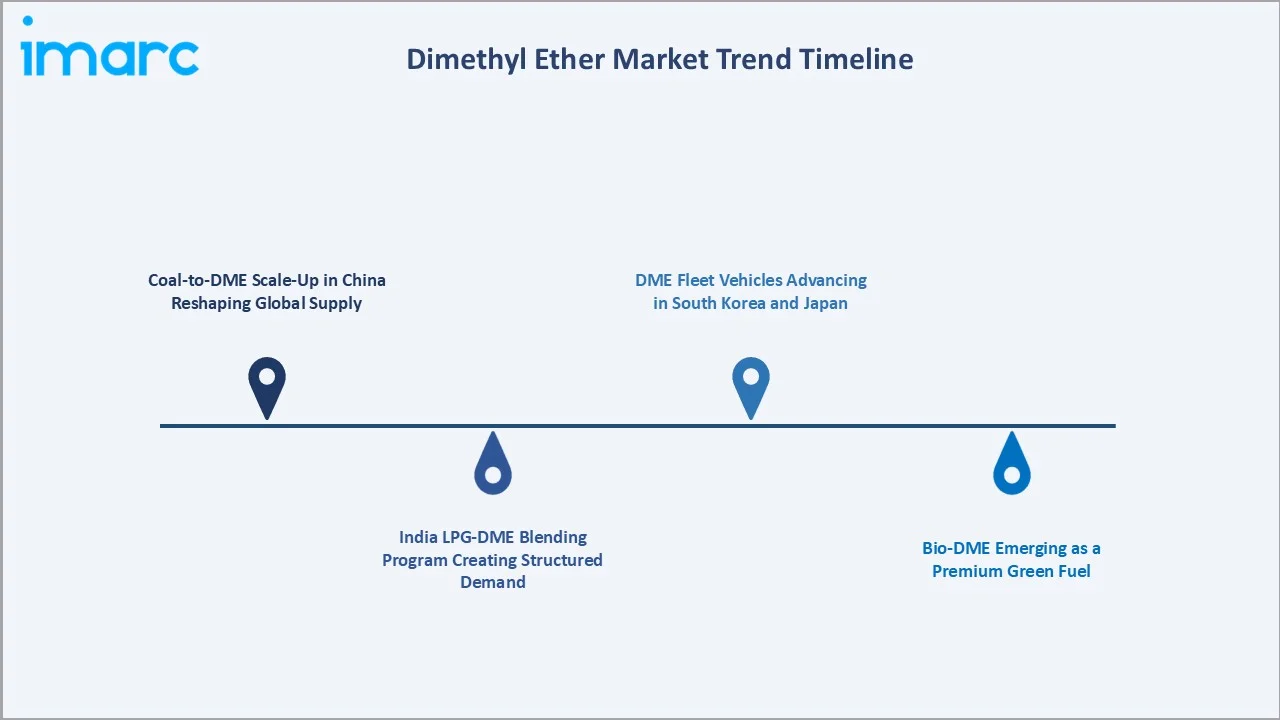

1. Coal-to-DME Scale-Up in China Reshaping Global Supply

China's coal-to-DME infrastructure represents the world's largest DME manufacturing base, with numerous large-scale plants operating across Inner Mongolia, Shaanxi, and Shanxi provinces. Ongoing capacity expansions driven by national energy security policy and air quality improvement targets are progressively strengthening China's position as the global DME supply anchor.

2. India LPG-DME Blending Program Creating Structured Demand

India's government-led LPG-DME blending initiative under national oil companies’ targets displacing a significant share of LPG annually with blended DME, creating assured domestic demand. Domestic DME synthesis units targeting commercial commissioning in the near term are being developed in partnership with industrial and engineering companies.

3. Bio-DME Emerging as a Premium Green Fuel

European and North American bio-DME projects utilizing black liquor, municipal solid waste, and agricultural residues are scaling from pilot to commercial stage. Bio-DME commands a premium over conventional DME in markets qualifying for renewable energy obligation certificates and low-carbon fuel standard credits.

4. DME Fleet Vehicles Advancing in South Korea and Japan

National gas utilities and automotive OEM partnerships in South Korea and Japan have completed commercial truck demonstration programs, establishing DME as a viable bridge fuel in East Asian transportation decarbonization strategy. Commercial fleet deployment is scheduled for broader rollout pending refueling infrastructure expansion.

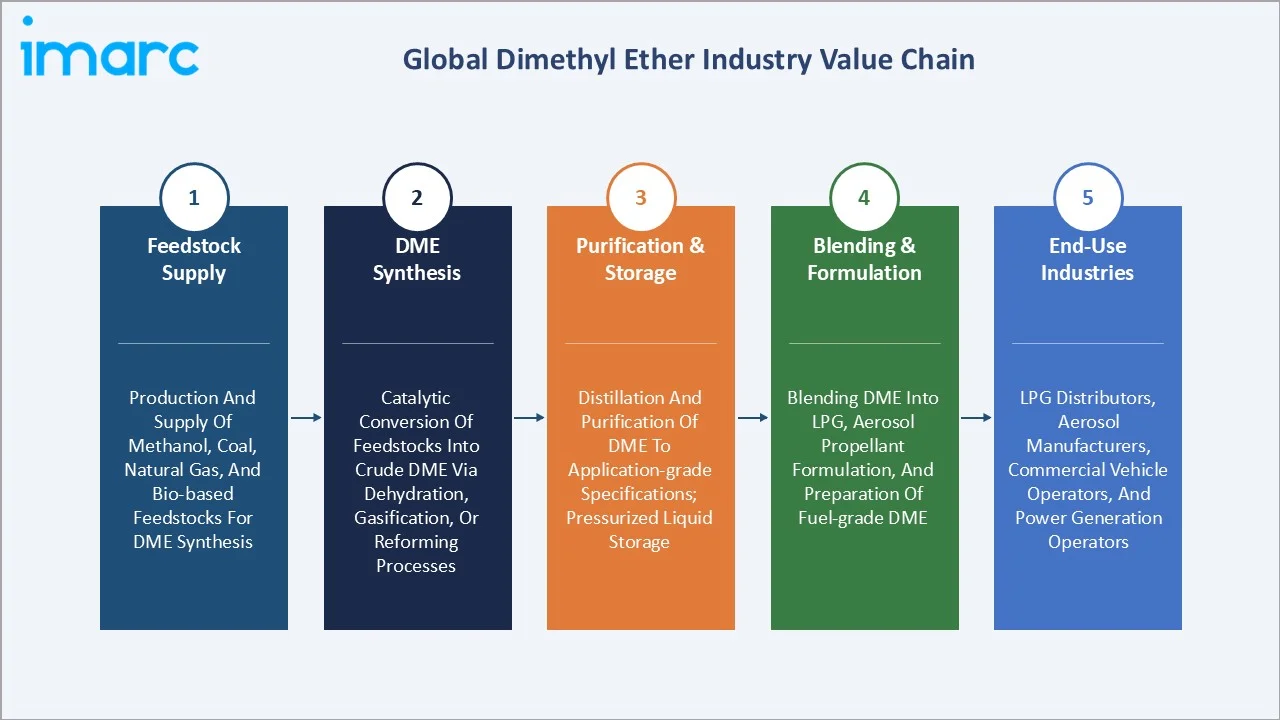

Industry Value Chain Analysis

The dimethyl ether value chain spans five stages from feedstock production through end-use application. DME synthesis and purification capture the highest value-add margins, while distribution logistics and application-specific formulation generate significant infrastructure investment requirements that favor integrated operators.

Integrated DME producers with captive feedstock sourcing and in-house purification capabilities achieve lower delivered cost structures than processors relying entirely on spot market feedstock procurement, providing a meaningful competitive advantage in commodity market segments where price competition is intense.

|

Stage |

Description |

|

Feedstock Supply |

Production and supply of primary feedstocks including methanol, coal, natural gas, and bio-based materials for DME synthesis |

|

DME Synthesis |

Catalytic conversion of feedstocks into crude DME via dehydration, gasification, or reforming processes at commercial-scale facilities |

|

Purification & Storage |

Distillation and purification of DME to application-grade specifications, followed by pressurized liquid storage and terminal operations |

|

Blending & Formulation |

Blending of DME into LPG, aerosol propellant formulation, and preparation of fuel-grade or chemical-grade DME for specific end-use requirements |

|

End-Use Industries |

Consumption by LPG distributors, aerosol manufacturers, commercial vehicle operators, chemical processors, and power generation operators |

Technology Landscape in the Dimethyl Ether Industry

DME Synthesis Technology: CDM vs. Direct Synthesis

The dominant commercial pathway is two-step catalytic dehydration of methanol using gamma-alumina catalysts, achieving high DME selectivity. Single-step direct synthesis via hybrid catalysts co-producing methanol and DME from syngas is gaining commercial traction, offering a meaningful energy efficiency advantage over the two-step route.

Coal and Natural Gas Gasification Routes

Coal-to-DME via entrained flow gasification followed by methanol synthesis and dehydration is the dominant production route in China, supported by government policy and domestic coal availability. Natural gas steam methane reforming to syngas-to-methanol-to-DME provides lower carbon intensity than the coal route, preferred where gas feedstock is competitively priced.

Bio-Based DME Production Technology

Biomass gasification from black liquor, municipal solid waste, or agricultural residues to syngas, followed by methanol synthesis and DME conversion, achieves low lifecycle carbon intensity qualifying under EU Renewable Energy Directive sustainability criteria. Bio-DME routes are attracting increasing investment as carbon pricing and low-carbon fuel mandates expand.

Catalyst Innovation and Process Intensification

Advanced zeolite-based catalysts are achieving higher DME selectivity in single-pass reactors compared to conventional alumina catalysts. Membrane reactor technology integrating separation and reaction stages is reducing DME production costs at pilot scale, with commercial deployment expected progressively through the forecast period.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Raw Material |

Methanol |

76.5% |

2025 |

|

Application |

LPG Blending |

45.8% |

2025 |

|

End-Use Industry |

🔒 |

🔒 |

2025 |

|

Region |

Asia Pacific |

43.2% |

2025 |

By Raw Material

Methanol commands a majority share of 76.5% in 2025, owing to the commercial maturity of catalytic dehydration processes, methanol's global commodity availability, and the lower capital cost of methanol-to-DME versus direct coal or gas routes. Established methanol supply chains globally support the DME synthesis industry at competitive feedstock economics.

To access detailed market analysis, Request Sample

Coal-derived DME at 9.8% in 2025 remains significant in China, where coal gasification infrastructure and domestic energy security policy maintain coal as an economically viable DME feedstock despite higher carbon intensity compared to methanol routes. Natural gas at 6.7% serves markets where pipeline gas availability ensures competitive feedstock economics.

By Application

LPG blending dominates at 45.8% in 2025, representing the largest single application for DME globally. Government mandates across key Asian markets requiring DME inclusion in LPG cylinder blends create policy-secured demand at scale. DME blending into LPG reduces cylinder costs while maintaining clean-burning performance for household cooking applications.

Fuel applications at 24.6% in 2025 capture commercial vehicle diesel substitute demand, power generation auxiliary fuel, and marine fuel applications where DME's zero particulate and near-zero SOx emission profile qualifies under international marine sulfur cap requirements. Growing DME fleet vehicle programs in Asia are expanding this segment.

Regional Market Insights

Asia Pacific's 43.2% market dominance in 2025 is driven by China's world-leading DME production capacity, India's rapidly scaling LPG-DME blending program, and South Korea and Japan's advanced DME vehicle fuel commercialization programs, creating an unparalleled concentration of both DME supply and demand in the region.

Europe at 21.6% in 2025 benefits from the EU F-Gas Regulation's HFC propellant phase-down, making DME the preferred low-GWP aerosol propellant replacement across personal care and household product categories. Bio-DME certification under EU renewable energy directives positions European bio-based producers for green fuel premium markets with dedicated offtake agreements.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

43.2% |

Largest production base; LPG blending policy; DME vehicle programs in South Korea and Japan |

|

Europe |

21.6% |

F-Gas aerosol propellant substitution; bio-DME green fuel premiums; EU clean energy policy |

|

North America |

18.9% |

Aerosol industry demand; renewable bio-DME scaling; clean fuel incentive programs |

|

Latin America |

9.1% |

LPG substitution programs; industrial fuel demand; domestic energy diversification initiatives |

|

Middle East & Africa |

7.2% |

Large-scale DME production capacity; petrochemical integration; LPG cooking fuel blend programs |

Competitive Landscape

The global dimethyl ether market is moderately fragmented, with regional leaders holding strong positions in their home markets while several large integrated energy and chemical companies compete across multiple geographies. Asia Pacific is dominated by Chinese production-side operators and Japanese conglomerates, while North American and European markets are served by specialty chemical and integrated energy companies.

|

Company |

Key Products |

Market Position |

Strategic Focus |

|

Nouryon |

Demeon D, Demeon ReNu100, Demeon Green DME |

Leader |

European and global specialty chemicals; high-purity DME for aerosol propellant applications; bio-based DME development via ReNu100 renewable grade |

|

Mitsubishi Gas Chemical Company, Inc. |

Dimethyl ether |

Leader |

Global DME trading and project investment; Japan clean transportation fuel programs |

|

Grillo-Werke AG |

Dimethyl ether (DME): GRILLO-one |

Challenger |

European specialty chemicals and industrial markets; high-purity GRILLO-one DME for aerosol, pharmaceutical, and specialty industrial applications |

|

Oberon Fuels, Inc. |

Renewable DME (rDME) |

Emerging |

North American bio-DME; renewable fuel certification and clean fuel incentive program access |

Key players include Nouryon, Mitsubishi Gas Chemical Company, Inc., Grillo-Werke AG, Oberon Fuels, Inc., and others

Key Company Profiles

Mitsubishi Gas Chemical Company, Inc.

Mitsubishi Gas Chemical Company, Inc. (MGC) is a leading Japanese chemical manufacturer and one of the world's only comprehensive methanol producers, operating DME production at its Niigata Plant primarily for aerosol propellant and specialty chemical applications. The company produces high-purity DME from methanol at its Niigata Plant, serving aerosol, chemical feedstock, and emerging bio-fuel markets.

- Product Portfolio: Dimethyl ether

- Recent Developments: In December 2023, Mitsubishi acquired International Sustainability and Carbon Certification (ISCC) PLUS for Bio-methanol and dimethyl ether (DME) produced at its Niigata Plant. The company signed a Basic Agreement with Niigata Prefecture on the Purchase and Sales of Biogas to ensure the effective utilization of unused biogas generated from its sewage treatment plants.

- Strategic Focus: MGC's DME strategy focuses on high-purity aerosol-grade DME production, the integration of bio-methanol from waste biogas into its Niigata manufacturing base, and obtaining international sustainability certifications to serve customers seeking low-carbon chemical feedstocks and propellants.

Grillo-Werke AG

Grillo-Werke AG is a leading European manufacturer of dimethyl ether (DME) and dimethyl sulphate, producing DME using methanol as a raw material in a state-of-the-art plant. The company produces DME based on a license from the Japanese group MGC.

- Product Portfolio: Dimethyl ether (DME): GRILLO-one

- Strategic Focus: Grillo-Werke's DME strategy focuses on maintaining a leading European supply position for high-purity aerosol and specialty-grade DME, differentiating through green biomethanol-based production, REDcert² and ISO sustainability certifications, and serving the aerosol industry's ongoing transition away from HFC propellants toward low-GWP alternatives.

Market Concentration Analysis

The global dimethyl ether market is moderately fragmented at the global level, reflecting significant regional concentration among national or regional leaders, with no single company holding a dominant share of total global market revenue. Asia Pacific, representing the largest regional share, is served primarily by domestic producers, while North American and European markets have distinct competitive ecosystems.

Consolidation at the regional level is more advanced than global consolidation suggests. State-backed energy utilities in South Korea, Japan, and India are leading DME commercialization through program investment and infrastructure development, while private integrated producers compete on cost and scale in China and the Middle East.

Investment & Growth Opportunities

Fastest-Growing Segments

Bio-based DME at ~11.2% CAGR through 2034 is the highest-growth raw material segment, driven by EU renewable fuel mandates, sustainable aviation fuel precursor qualification, and premium pricing for carbon-negative DME produced from waste biomass and renewable methanol feedstocks.

Emerging Markets

India is the fastest-growing country market for DME through 2034. India's LPG-DME blending program, scale-up of domestic methanol production under the Methanol Economy Mission, and growing aerosol and specialty chemicals industry are creating multi-application DME demand from the world's most populous LPG user base.

Venture & Investment Trends

Venture capital investment in bio-DME startups has grown significantly, with North American and European renewable DME producers attracting capital linked to clean fuel incentive programs. Strategic investment in DME distribution infrastructure, particularly pressurized terminal and cylinder handling networks, is growing as LPG-DME blending mandates create infrastructure development requirements across Asian markets.

Future Market Outlook (2026-2034)

The global dimethyl ether market is forecast to expand from USD 7.81 Billion in 2025 to USD 15.77 Billion by 2034 at a CAGR of 8.12%, adding significant incremental annual market value over the forecast period. This consistent, sustained growth reflects DME's accelerating role across fuel, aerosol, and chemical feedstock applications driven by energy transition policy.

Three structural forces will shape the DME industry landscape through 2034. India's LPG-DME blending scale-up from pilot to national deployment will create the world's second-largest DME demand center. Bio-DME's qualification under EU renewable fuel mandates will drive new European production capacity investment with green premium pricing.

South Korea and Japan's commercial DME vehicle fleet programs, supported by national gas utilities and automotive OEM partnerships, will establish the first scalable DME transportation fuel markets outside niche demonstration, creating replicable program models for Southeast Asian and Latin American clean fuel policy adoption through 2034.

Research Methodology

Primary Research

Primary research encompassed structured interviews with DME industry stakeholders including senior commercial managers at DME producers, procurement specialists at LPG distributors, aerosol formulation chemists, and policy advisors at national energy ministries. Primary data validated market sizing, segment shares, regional demand estimates, and technology adoption timelines across all major DME-consuming regions.

Secondary Research

Key secondary sources include IEA Energy Technology Perspectives, International DME Association market reports, World LPG Association blending data, EU F-Gas Regulation compliance tracking, national energy ministry capacity data, and trade publications including ICIS Chemical Business, Chemical Week, and Hydrocarbon Processing.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating energy transition policy calendars, feedstock price trajectory modeling, capacity expansion pipelines, and LPG blending mandate adoption rates by country. Scenario analysis was performed to account for feedstock price volatility and regulatory uncertainty.

Dimethyl Ether Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Raw Materials Covered | Methanol, Coal, Natural Gas, Bio-Based, Others |

| Applications Covered | Fuel, Aerosol Propellent, LPG Blending, Chemical Feedstock, Others |

| End-Use Industries Covered | Oil and Gas, Automotive, Power Generation, Cosmetics, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Nouryon, Mitsubishi Gas Chemical Company, Inc., Grillo-Werke AG, Oberon Fuels, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the dimethyl ether market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global dimethyl ether market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the dimethyl ether industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Dimethyl Ether Market Report

The global dimethyl ether market reached USD 7.81 Billion in 2025, reflecting consistent demand from LPG blending mandates, aerosol propellant applications, and Asia-Pacific industrial fuel programs.

The market is projected to reach USD 15.77 Billion by 2034, growing at a CAGR of 8.12% during 2026-2034, driven by India LPG-DME blending scale-up, bio-DME investment, and aerosol industry HFC substitution.

Methanol leads with a 76.5% raw material share in 2025, owing to the commercial maturity and lowest capital cost of catalytic dehydration of methanol processes compared to coal or natural gas routes.

LPG blending leads at 45.8% in 2025, driven by government-mandated LPG-DME blending programs in India, Indonesia, and South Korea creating policy-assured large-volume demand for DME as an LPG extender and clean cooking fuel.

Asia Pacific commands a dominant 43.2% market share in 2025, driven by China's world-leading DME production capacity, India's LPG-DME blending program, and South Korea and Japan's DME vehicle fuel commercialization initiative.

Bio-based DME is the fastest-growing raw material at approximately 11.2% CAGR through 2034, driven by EU renewable fuel mandates, sustainable aviation fuel precursor qualification, and carbon-negative lifecycle certification premium pricing.

Leading companies include Nouryon, Mitsubishi Gas Chemical Company, Inc., Grillo-Werke AG, Oberon Fuels, Inc., and others.

Key applications include LPG blending for household cooking fuel, transportation fuel as a diesel substitute, aerosol propellant in personal care and industrial products, chemical feedstock for specialty chemicals, and emerging power generation auxiliary fuel applications.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)