E-Bike Market Size, Share, Trends and Forecast by Mode, Motor Type, Battery Type, Class, Design, Application, and Region, 2026-2034

Global E-Bike Market Size, Share, Trends & Forecast (2026-2034)

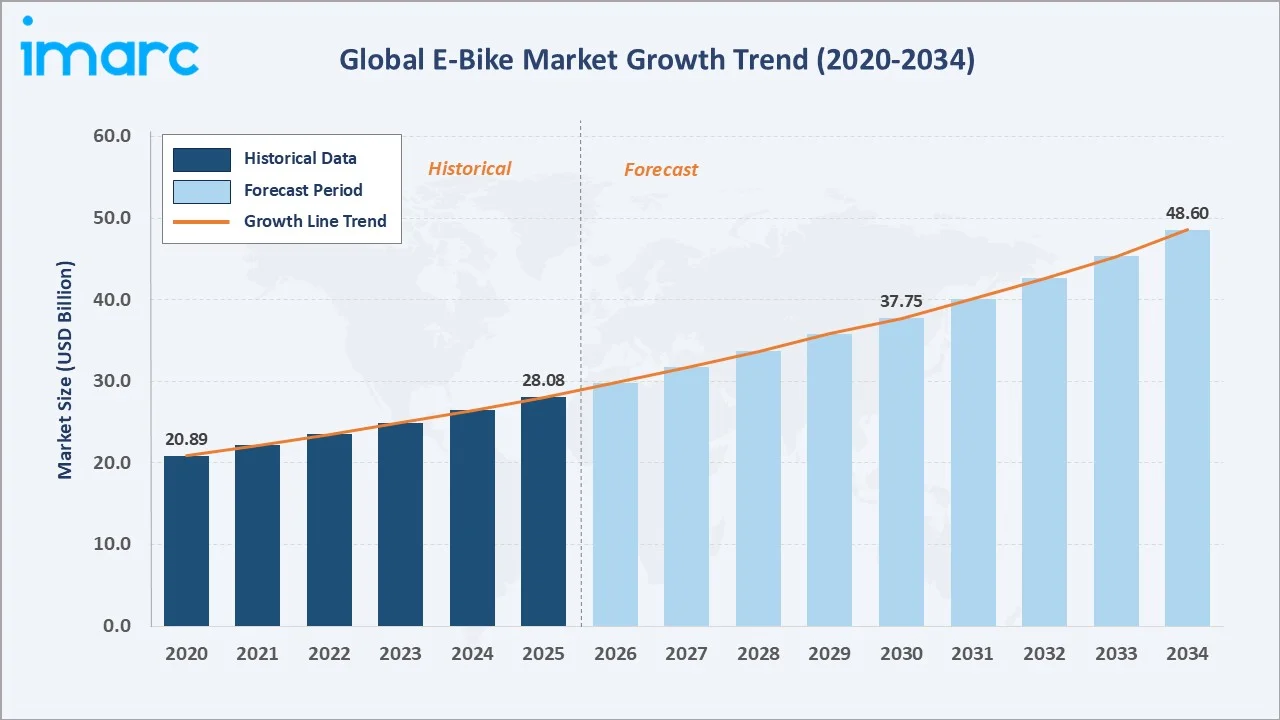

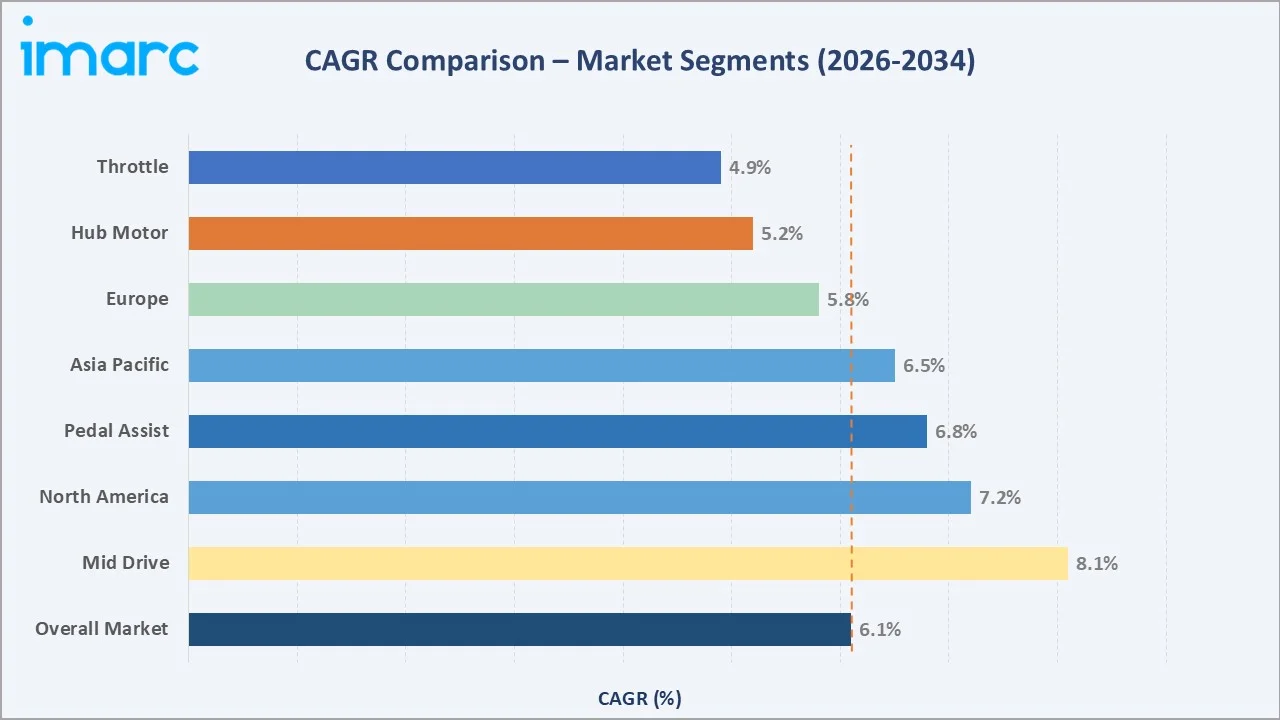

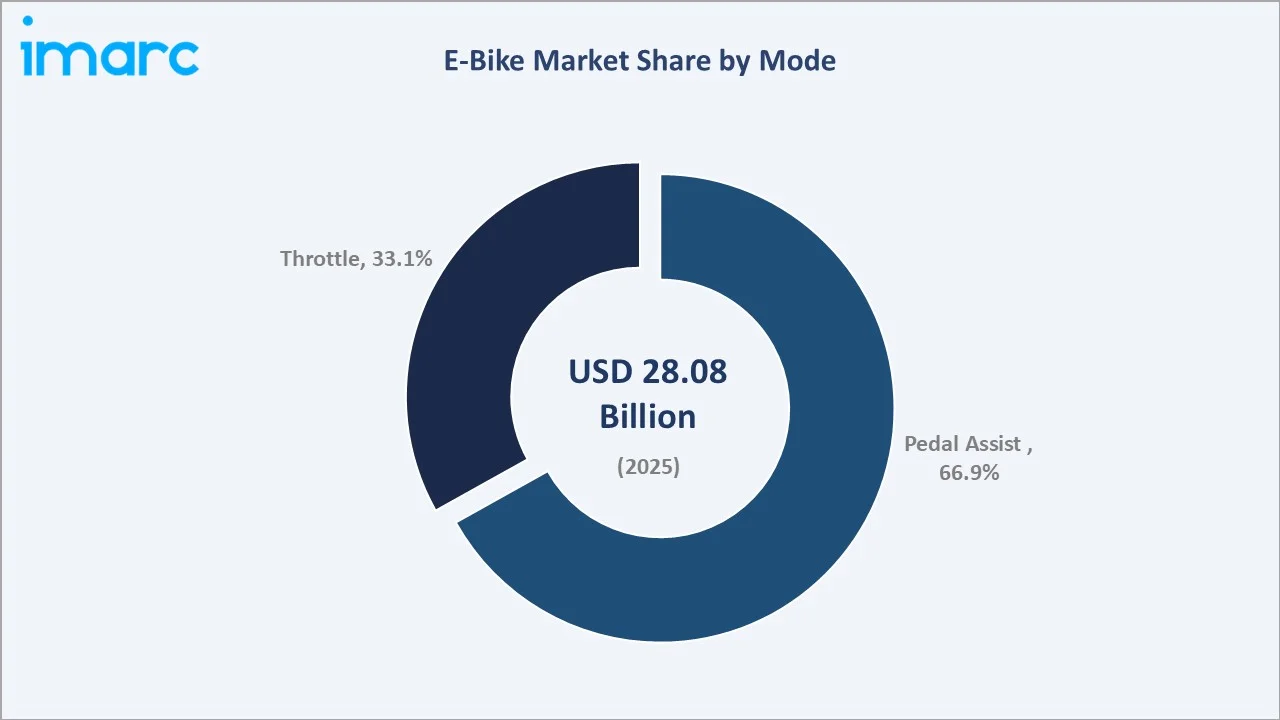

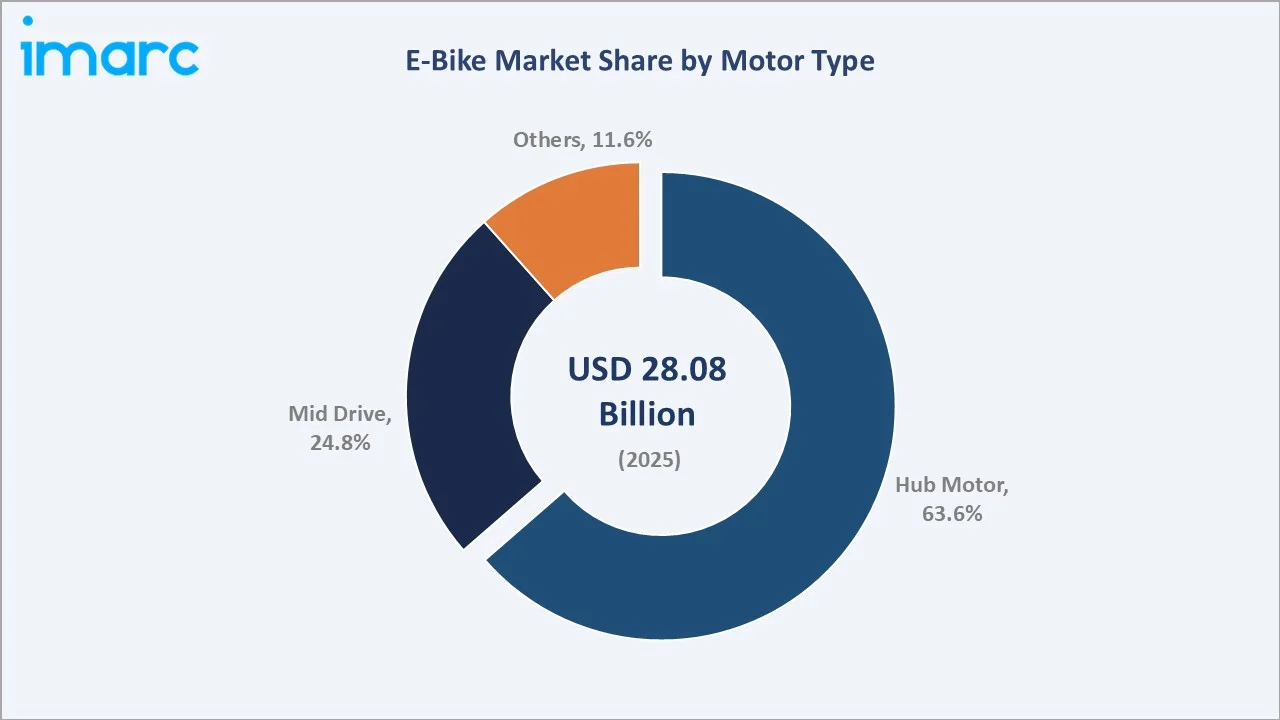

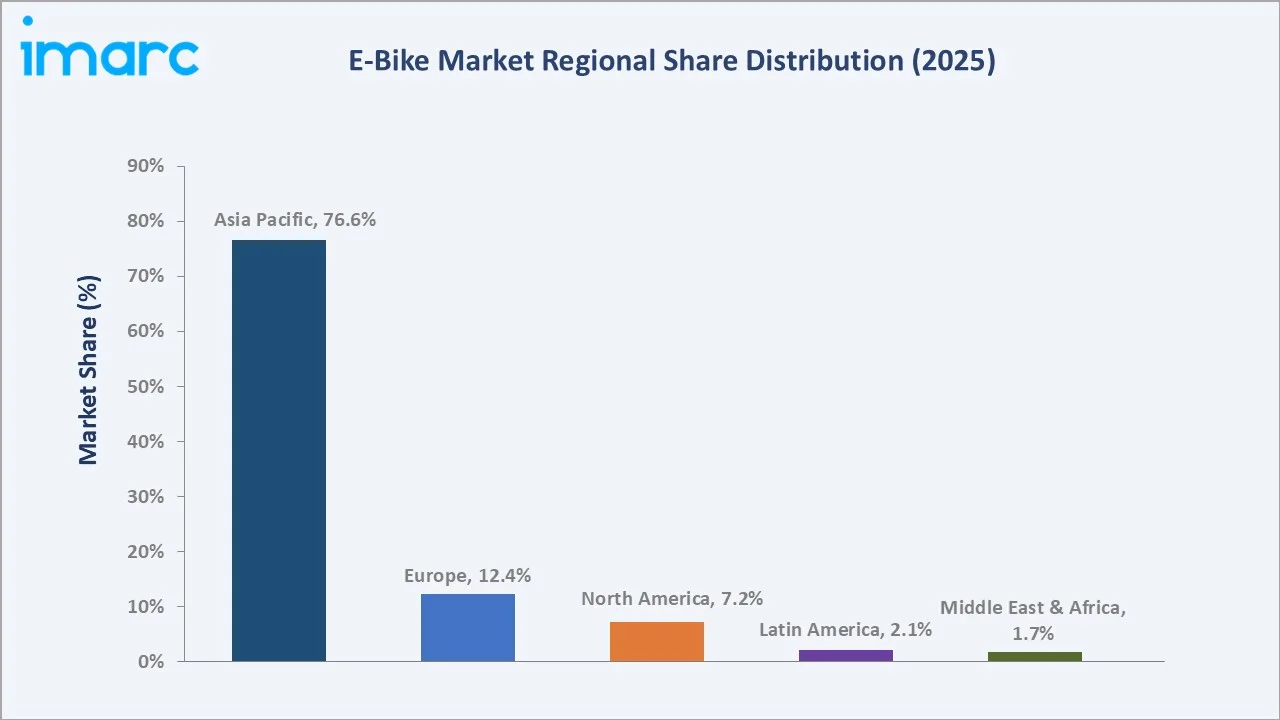

The global e-bike market was valued at USD 28.08 Billion in 2025 and is projected to reach USD 48.60 Billion by 2034, expanding at a CAGR of 6.1% during the forecast period (2026-2034). The market’s consistent growth is propelled by rising urbanization, mounting traffic congestion, accelerating government support for clean transportation, and increasing environmental consciousness among consumers worldwide. Asia Pacific dominates the global e-bike market, accounting for 76.6% of market revenues in 2025, driven by China’s unrivalled manufacturing scale, rapid urbanization across emerging economies, and deep consumer familiarity with two-wheeled mobility. Among modes, the pedal assist segment leads with 66.9% share in 2025, while hub motors command 63.6% of the motor type segment. Major industry participants include AIMA Inc., Giant Bicycles, MERIDA BIKES, Pedego, and Yadea Technology Group Co., Ltd.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 28.08 Billion |

|

Forecast Market Size (2034) |

USD 48.60 Billion |

|

CAGR (2026-2034) |

6.1% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Region |

Asia Pacific (76.6% share, 2025) |

|

Dominant Mode |

Pedal Assist (66.9% share, 2025) |

|

Dominant Motor Type |

Hub Motor (63.6% share, 2025) |

|

Fastest Growing Motor |

Mid Drive (CAGR ~8.1%, 2026-2034) |

To get more information on this market, Request Sample

Executive Summary

The global e-bike market continues to demonstrate robust expansion, underpinned by shifting urban mobility patterns, rapid urbanization, and the convergence of environmental policy with technological innovation. Valued at USD 28.08 Billion in 2025, the market is forecasted to exceed USD 48.60 Billion by 2034, at a steady CAGR of 6.1%.

Among the key growth drivers, the increasing inclination toward sustainable, cost-effective urban commuting — particularly among working-age demographics in major metropolitan areas — remains a primary catalyst. The pedal assist segment alone represented 66.9% of the global e-bike market in 2025, reflecting strong consumer and regulatory preference for pedelec-class e-bikes that align with existing cycling infrastructure access rules. Mid-drive motor adoption is gaining rapid momentum at a CAGR of approximately 8.1%, driven by superior torque delivery and performance characteristics suited to cargo and performance-oriented applications.

Asia Pacific retains its market leadership with a 76.6% share in 2025, while North America and Europe emerge as strategically important high-growth markets, underpinned by expanding cycling infrastructure, favorable policy environments, and rising consumer awareness of e-bikes as a credible alternative to conventional motorized transport. Leading market players are investing in proprietary motor ecosystems, smart connectivity platforms, and lightweight design innovations — all key areas reshaping the competitive landscape through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Mode) |

Pedal Assist – 66.9% share (2025) |

|

Second Segment (Mode) |

Throttle – 33.1% share (2025) |

|

Largest Segment (Motor Type) |

Hub Motor – 63.6% share (2025) |

|

Fastest Growing Motor |

Mid Drive – CAGR ~8.1% (2026-2034) |

|

Dominant Region |

Asia Pacific – 76.6% revenue share (2025) |

|

Fastest Growing Region |

North America – CAGR ~7.2% (2026-2034) |

|

Top Companies |

AIMA Inc., Giant Bicycles, Pedego, Trek Bicycle Corporation, and Yadea Technology Group Co., Ltd. |

|

Market Opportunity |

The cargo e-bike commercial segment is projected at a high single-digit CAGR through 2034 |

Key Analytical Observations Supporting The Above Data:

- Pedal assist dominates with a 66.9% share (2025), driven by regulatory alignment, health appeal, and broad demographic suitability for urban and recreational cycling segments globally.

- Throttle-mode e-bikes hold a 33.1% share, particularly favored in North America, where consumers value motor engagement without mandatory pedaling effort.

- Hub motors command 63.6% of the motor type segment in 2025, valued for minimal maintenance, silent operation, and cost competitiveness in price-sensitive markets.

- Mid-drive motors, holding a 24.8% share, are the fastest-growing motor type at a CAGR of approximately 8.1%, driven by superior torque delivery and terrain adaptability.

- Asia Pacific generates 76.6% of global revenues (2025), supported by China’s manufacturing scale, strong government EV mandates, and deep consumer familiarity with two-wheeled transportation.

- North America is the fastest-growing regional market at a CAGR of approximately 7.2% (2026-2034), driven by expanding cycling infrastructure, federal and state incentive programs, and commercial last-mile delivery adoption.

Global E-Bike Market Overview

The e-bike industry is one of the fastest-growing segments in sustainable mobility, evolving from a niche Asian market into a global solution for urban commuting, recreation, cargo transport, and shared mobility. Its value chain spans battery manufacturers, motor suppliers, OEMs, and distribution networks across regions.

E-bikes serve a wide spectrum of users—from budget commuters to premium cyclists—making demand broad and resilient. Regulatory adaptability across key markets (U.S., EU, and Asia Pacific) has supported widespread adoption, while emerging use cases such as cargo delivery, fleet electrification, and shared mobility are reshaping the market. Supported by urbanization, rising incomes, environmental regulations, and shifting mobility preferences, e-bikes are poised to become a core element of global urban transport systems by 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

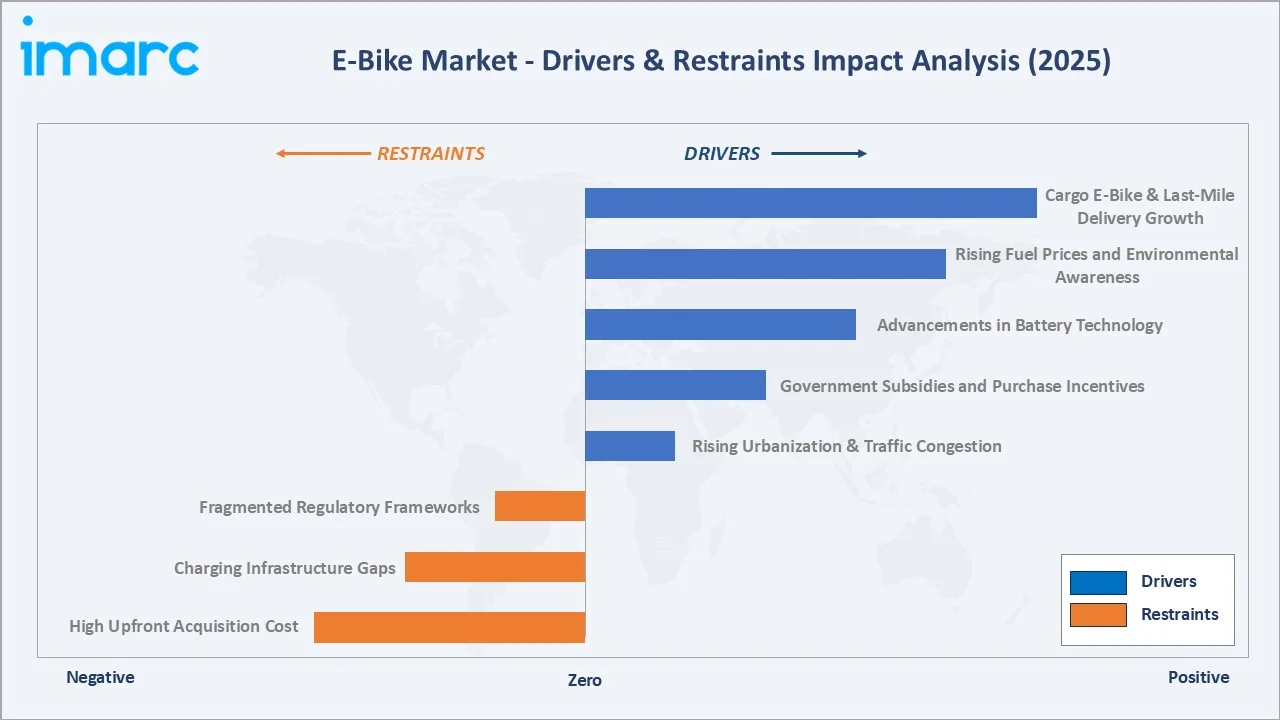

Market Drivers

- Rising Urbanization & Traffic Congestion: Rapid urbanization and increasing congestion are key structural drivers for e-bike adoption. Urban mobility systems are under pressure from rising vehicle density, making e-bikes an efficient solution for short-distance travel by reducing commute time, cost, and congestion impact.

- Government Subsidies and Purchase Incentives: Public policy support—including purchase incentives, tax rebates, and large-scale investments in cycling infrastructure—is significantly lowering adoption barriers. Governments across North America and Europe are actively promoting e-bikes through subsidies and dedicated infrastructure funding, accelerating market penetration.

- Advancements in Battery Technology: Continuous improvements in lithium-ion battery technology—particularly declining costs, higher energy density, and better lifecycle performance—are enhancing e-bike affordability and usability. These advancements are enabling longer ranges, faster charging, and integration of smart battery management systems.

- Rising Fuel Prices and Environmental Awareness: Increasing fuel costs and growing environmental consciousness are reinforcing the shift toward low-emission mobility. E-bikes offer a cost-efficient alternative to fuel-powered transport while supporting decarbonization goals, especially in urban environments.

Market Restraints

- High Upfront Acquisition Cost: E-bikes remain significantly more expensive than conventional bicycles, limiting adoption in price-sensitive markets despite long-term cost savings from lower fuel and maintenance expenses.

- Charging Infrastructure Gaps: While urban charging ecosystems are improving, limited infrastructure in suburban and rural areas contributes to range anxiety and restricts broader adoption, particularly among first-time users.

- Fragmented Regulatory Frameworks: Variations in e-bike classifications, speed limits, and usage permissions across regions create compliance complexity for manufacturers and confusion for consumers.

Market Opportunities

- Cargo E-Bike & Last-Mile Delivery Growth: Rapid expansion in e-commerce and urban logistics is driving strong demand for cargo e-bikes, which offer a cost-efficient and low-emission alternative for last-mile delivery operations.

- Emerging Market Expansion: Regions such as India, Southeast Asia, Latin America, and the Middle East present significant growth potential, supported by rising urbanization, increasing fuel costs, and evolving government sustainability initiatives.

- Smart & Connected E-Bikes: Integration of IoT, AI-based pedal assist, GPS tracking, and anti-theft technologies is enabling a premium, high-margin segment and unlocking recurring revenue opportunities through digital ecosystems.

Market Challenges

- Supply Chain Vulnerability: Dependence on battery cells, rare earth materials, and semiconductors exposes manufacturers to supply disruptions and price volatility, with geographic concentration adding geopolitical risk.

- Safety & Infrastructure Readiness: Higher speeds of e-bikes versus traditional bicycles raise safety concerns in cities lacking dedicated infrastructure, while insurance and regulatory frameworks are still evolving.

- Competition from Alternative Micro-Mobility: Shared e-scooters and e-mopeds are emerging as strong substitutes, particularly in dense urban areas and among younger consumers favoring access-over-ownership models.

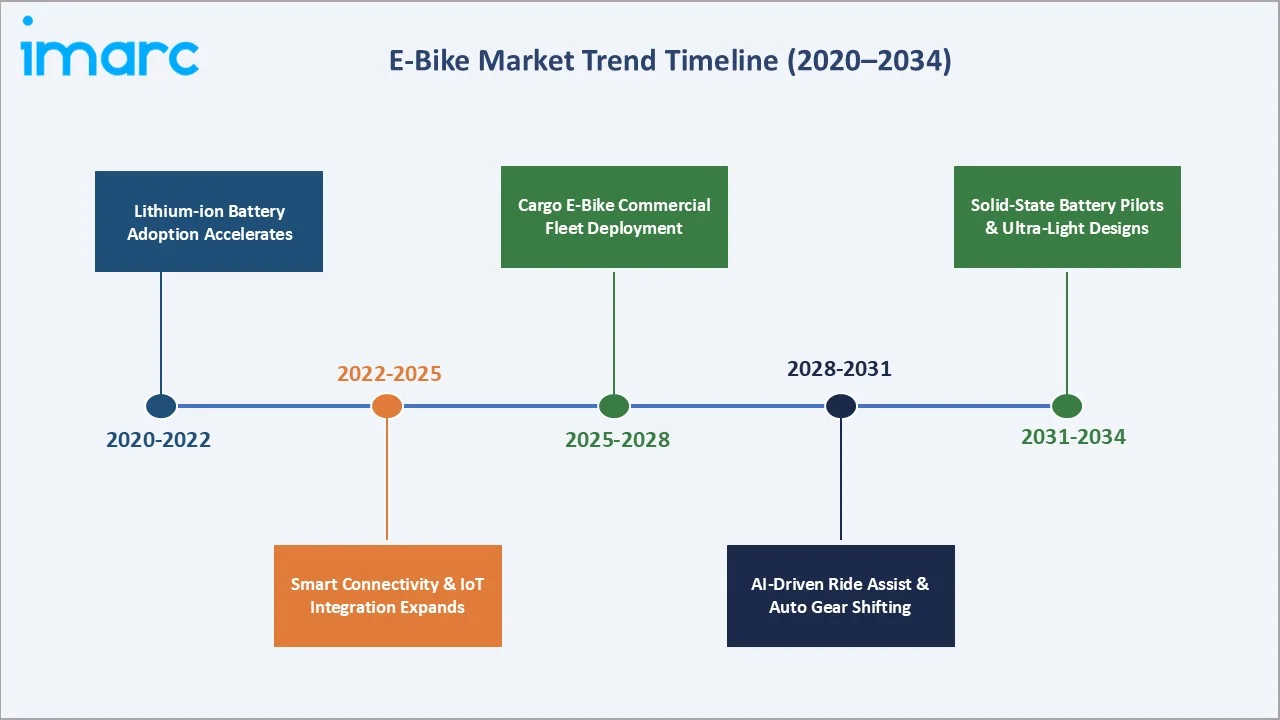

Emerging Market Trends

1. Rising Smart Connectivity and Digital Integration

E-bikes are increasingly equipped with IoT, GPS, and app-based controls, enabling real-time monitoring, enhanced security, and personalized riding experiences—driving premiumization and recurring digital revenue opportunities.

2. Accelerating Adoption for Urban Commuting and Last-Mile Delivery

Rising congestion and e-commerce expansion are accelerating the adoption of e-bikes—especially cargo models—as cost-efficient, low-emission solutions for urban mobility and logistics.

3. Advancements in Pedal-Assist Systems and Battery Technology

Improved torque-sensing systems and lithium-ion batteries are enhancing performance, extending range, and reducing costs, making e-bikes more efficient and appealing across consumer segments.

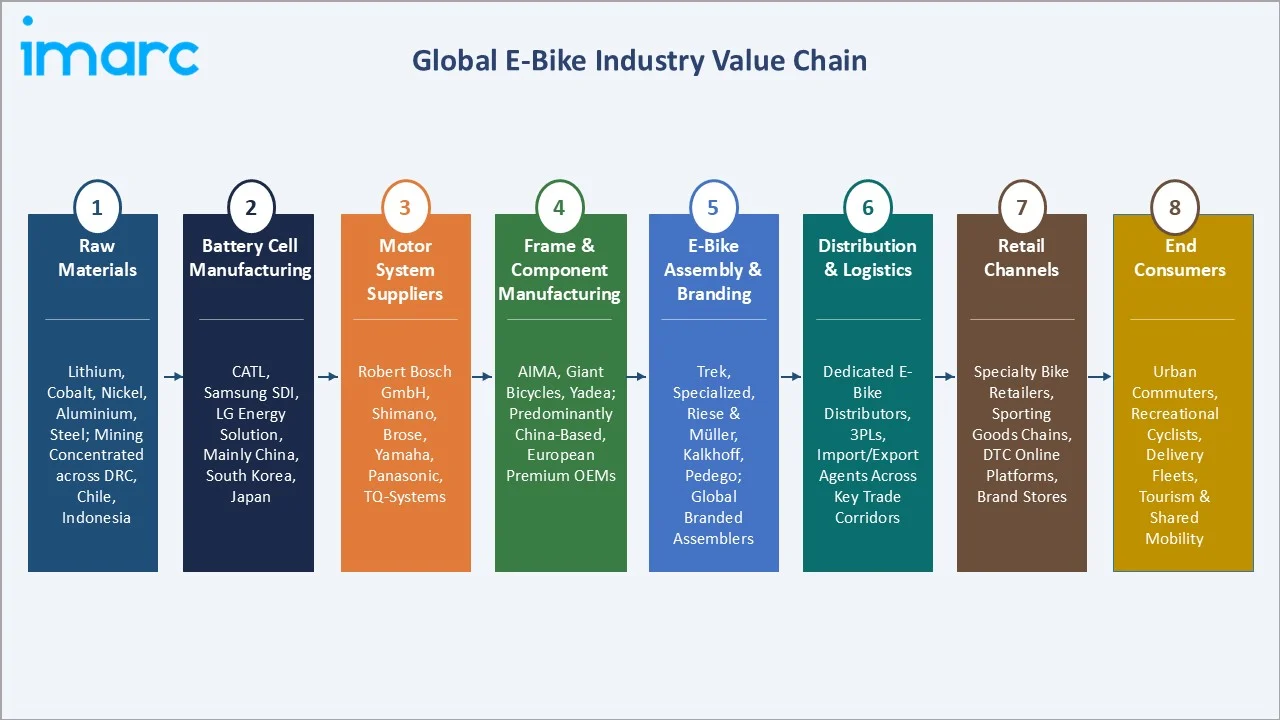

Industry Value Chain Analysis

|

Stage |

Key Players / Examples |

|

Raw Materials |

Lithium, cobalt, nickel, aluminum, steel; mining companies across DRC, Chile, and Indonesia |

|

Battery Cell Manufacturing |

CATL, Samsung SDI, LG Energy Solution, concentrated in China, South Korea, and Japan |

|

Motor System Suppliers |

Robert Bosch GmbH, Shimano, Brose, Yamaha, Panasonic, TQ-Systems |

|

Frame & Component Manufacturing |

AIMA Technology Group Co., Ltd., Giant Bicycles, MERIDA BIKES, and Yadea Technology Group Co., Ltd., predominantly China-based, with European premium OEMs |

|

E-Bike Assembly & Branding |

Trek, Specialized, Riese & Müller, Kalkhoff, Pedego; global branded assemblers |

|

Distribution & Logistics |

Dedicated e-bike distributors, 3PLs, import/export agents across key trade corridors |

|

Retail Channels |

Specialty bike retailers, sporting goods chains, direct-to-consumer online platforms, brand-owned stores |

|

End Consumers |

Urban commuters, recreational cyclists, delivery fleet operators, tourism providers, and shared mobility platforms. |

The global e-bike industry value chain spans multiple interconnected stages, from raw material procurement and battery cell manufacturing to end-consumer delivery and post-sale servicing. Each stage is populated by specialized operators whose performance directly influences product quality, cost competitiveness, and market responsiveness.

Technology Landscape in the E-Bike Industry

Motor System Innovation

Advances in mid-drive and hub motor engineering are delivering higher torque, improved efficiency, and better power-to-weight ratios. Compact motor designs are also enabling lighter, more seamless e-bike form factors without compromising performance.

Smart Connectivity & IoT Integration

E-bikes are evolving into connected mobility platforms with IoT-enabled features such as real-time diagnostics, GPS tracking, anti-theft systems, and app-based customization—enhancing user experience and enabling data-driven services.

Battery Technology & Energy Management

Continued improvements in lithium-ion batteries—along with emerging silicon-anode and solid-state innovations—are increasing range, reducing weight, and improving safety. Advanced battery management systems are further enhancing lifecycle and reliability.

Lightweight Materials & Design Innovation

Adoption of carbon fiber, titanium, and advanced composites is reducing overall weight while maintaining strength. Integrated designs and segment-specific innovations (ultra-light commuters vs. high-payload cargo bikes) are expanding performance and use-case diversity.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Mode |

Pedal Assist |

66.9% |

2025 |

|

Motor Type |

Hub Motor |

63.6% |

2025 |

|

Battery Type |

Lithium Ion |

68.6% |

2025 |

|

Class |

Class I |

72.2% |

2025 |

| Design | Non-Foldable | 90.5% | 2025 |

| Application | City/Urban | 63.7% | 2025 |

|

Region |

Asia Pacific |

76.6% |

2025 |

By Mode

Pedal Assist dominates the mode segment with a 66.9% share in 2025. The pedal assist category combines the physical benefits of cycling with motor assistance, appealing across a wide demographic spectrum, including commuters, fitness enthusiasts, older adults, and recreational cyclists. Pedal-assist e-bikes are favorably positioned within regulatory frameworks across Europe and North America, where Class 1 pedelec classifications allow access to a broader range of cycling paths without requiring rider licensing. Manufacturers are investing in refining assist algorithms to deliver intuitive, terrain-responsive power delivery. The throttle segment, holding a 33.1% share, remains significant, particularly within the North American market, where consumers favor convenient throttle-activated motor engagement.

To access detailed market analysis, Request Sample

By Motor Type

Hub Motor holds the dominant position in the motor type segmentation with a 63.6% share in 2025. Hub motors are embedded directly within the wheel hub, providing a simple, self-contained drive system requiring minimal interaction with the bicycle’s existing drivetrain. This results in lower maintenance requirements, reduced mechanical complexity, and competitive pricing accessible across price-sensitive markets. Mid-drive motors, holding a 24.8% share, are gaining adoption at the fastest rate due to superior torque delivery and gear-system compatibility suited to performance, mountain, and cargo e-bike segments. The others category accounts for 11.6% of the motor type segment.

Regional Market Insights

Asia Pacific’s market leadership (76.6% share, 2025) is deeply entrenched. China alone commands over 90% of volume within the region, leveraging unrivalled production infrastructure. Rapid urbanization across India, Indonesia, Vietnam, and the Philippines; strong government EV mandates; and rising consumer aspirations for cost-efficient mobility sustain a structurally favorable demand environment. Japan’s high penetration rate and stable domestic production capacity support steady growth, while South Korea’s smart e-bike adoption, driven by IoT features, positions it as a premium sub-market within the region.

Europe’s market (12.4% share, 2025) is anchored by a mature cycling culture and ambitious carbon neutrality commitments, making the Europe e-bike Market one of the most progressive mobility sectors globally. London’s ULEZ expansion, combined with scrappage grants, is driving e-bike adoption among couriers and urban commuters. The cargo e-bike segment is experiencing particularly strong growth across European cities where road access restrictions favor low-emission delivery vehicles.

|

Region |

Share (2025) |

Key Growth Drivers |

Regulatory Context |

Leading Dynamics |

|

Asia Pacific |

76.6% |

Urbanization, govt. EV mandates, manufacturing scale, low-cost models |

National EV promotion policies in China, India, and Japan |

China >90% regional volume; India fastest-growing sub-market |

|

Europe |

12.4% |

Cycling culture, sustainability policy, and premium leisure demand |

EU EN 15194 pedelec standard; ULEZ expansions across UK cities |

Germany, the Netherlands, and France lead; cargo e-bikes are accelerating |

|

North America |

7.2% |

Infrastructure expansion, state incentives, and last-mile delivery growth |

Class I-III federal and state classification system |

US dominates; rebates up to USD 1,000 in CA and CO |

|

Latin America |

2.1% |

Urbanization, rising fuel costs, and shared e-bike programs |

Varies by country; limited formal e-bike regulations |

Brazil and Mexico are the primary markets; early-stage adoption |

|

Middle East & Africa |

1.7% |

Urban mobility demand and the sustainability agenda in the Gulf states |

Nascent regulatory frameworks; UAE and Saudi Arabia leading |

GCC states are emerging as high-income urban consumer segments |

North America holds a 7.2% share in 2025 and is projected to grow at the fastest regional CAGR of approximately 7.2% through 2026-2034. The United States benefits from approximately 17,000 miles of designated bicycle routes and state-level incentive programs providing rebates. The commercial last-mile delivery segment is an increasingly important demand driver, with logistics providers seeking to reduce urban delivery costs simultaneously.

Competitive Landscape

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

AIMA Technology Group Co., Ltd. |

AIMA |

Volume Leader |

Mass-market hub motor e-bikes; dominant China domestic share |

|

Giant Bicycles |

Giant / Liv |

Global Leader |

Vertically integrated manufacturing; broad portfolio across all segments |

|

MERIDA BIKES |

Merida |

Global Challenger |

OEM manufacturing capability; strong mountain e-bike portfolio |

|

Pedego |

Pedego |

North America Leader |

Direct-to-consumer premium; strong dealer network |

|

Riese & Müller GmbH |

Riese & Müller |

Premium Cargo Leader |

High-end cargo and urban e-bikes; fleet and family specialist |

|

Jiangsu Xinri E-Vehicle Co., Ltd |

SUNRA |

Asia Volume Player |

Mass-market e-bikes; large domestic distribution network |

|

Trek Bicycle Corporation |

Trek / Electra |

Global Premium Brand |

Full-range premium lineup |

|

Yadea Technology Group Co., Ltd. |

Yadea |

Volume & Export Leader |

Largest global e-bike unit seller; strong export growth across SE Asia |

The global e-bike market exhibits a moderately fragmented competitive structure where established bicycle manufacturers, dedicated electric mobility specialists, and vertically integrated technology companies compete across geographic markets and product tiers. Key competitive strategies include geographic expansion, proprietary motor ecosystem development, exclusive dealer network cultivation, and sustained R&D investment in battery range, motor efficiency, and digital rider experience.

Key Company Profiles

AIMA Technology Group Co., Ltd.

AIMA Technology Group Co., Ltd. is an e-bike manufacturer with a dominant position in the domestic mass-market segment. The company operates an extensive dealer and distribution network spanning all major Chinese provinces and has been expanding its presence across Southeast Asian markets.

- Product Portfolio: Urban commuter e-bikes, electric mopeds, and smart e-bike platforms across entry to mid-range price tiers.

- Recent Developments: In January 2025, AIMA Technology Group Co., Ltd. expanded its smart e-bike portfolio, integrating app-based diagnostics, GPS tracking, and anti-theft connectivity across key product lines.

- Strategic Focus: Domestic volume leadership, Southeast Asia market expansion, and transition toward higher-value connected e-bike models.

Trek Bicycle Corporation

Trek is a U.S.-headquartered premium bicycle and e-bike brand with a global distribution network spanning over 100 countries. Trek’s e-bike portfolio is anchored by the Domane, Marlin, and Rail platforms across road, mountain, and urban segments.

- Product Portfolio: Domane+ for electric road cycling; Rail e-MTB for performance trail riding; Verve+ and FX+ for urban commuting and fitness.

- Recent Developments: In September 2025, Trek Bicycle Corporation launched the Checkpoint+ SL, its first electric gravel bike, strengthening its position in the performance and mixed-terrain segment.

- Strategic Focus: Premium segment leadership, performance product innovation, and deepening dealer relationships in North America and European markets.

Yadea Technology Group Co., Ltd.

Yadea is the electric two-wheeler brand by global unit sales, with a strong position across China and rapidly expanding international distribution across Southeast Asia, Europe, and Latin America.

- Product Portfolio: Urban commuter e-bikes and electric mopeds spanning entry-level to mid-premium price tiers with integrated smart features.

- Recent Developments: In January 2026, Yadea Technology Group Co., Ltd. showcased its connected e-bike platform at CES 2026, highlighting IoT-enabled features and enhancing global brand visibility.

- Strategic Focus: International market expansion, product premiumization, and integration of IoT connectivity into mass-market models.

Market Concentration Analysis

The global e-bike market shows moderate concentration at the top and high fragmentation at the mass level, operating through a dual structure. The premium segment, particularly in Europe and North America, is relatively consolidated and led by brands such as Giant Bicycles, Riese & Müller GmbH, and Trek Bicycle Corporation, which leverage strong branding and proprietary technology ecosystems.

In contrast, the mass-market urban segment in Asia Pacific remains highly fragmented, with players like AIMA Technology Group Co., Ltd., Jiangsu Xinri E-Vehicle Co., Ltd, and Yadea Technology Group Co., Ltd. competing alongside numerous smaller manufacturers on price and volume.

Industry consolidation is gradually accelerating, highlighted by the formation of New Pedego Holdings Inc. following a strategic move by Pedego Electric Bikes in November 2025, alongside rising private equity interest in premium brands. This trend is expected to continue through 2034 as companies pursue scale, innovation, and leadership in high-margin markets.

Investment & Growth Opportunities

Fastest Growing Segments

Cargo e-bikes, performance mid-drive e-bikes, and smart connected platforms represent the highest-growth segments through 2034, driven by fleet electrification and premium consumer demand. Cargo e-bikes benefit from recurring fleet demand and strong unit economics in last-mile delivery, while performance e-bikes—particularly in Europe and North America—are seeing rapid growth. Meanwhile, smart connectivity platforms are unlocking recurring revenue streams via subscriptions, diagnostics, and digital services layered on hardware sales.

Emerging Market Expansion

Asia Pacific secondary markets (India, Vietnam, Indonesia, Philippines) and Latin America are key growth frontiers beyond China. Rising fuel costs, urbanization, and supportive EV policies—particularly in India—are driving adoption, while Brazil and Mexico present strong incremental opportunities. Successful market entry is typically driven by localized product strategies, partnerships with domestic distributors, and government subsidy alignment, with shared mobility platforms offering a capital-efficient entry route.

Technology Investment Themes

Key investment themes include solid-state batteries, which promise 30–50% higher energy density and were showcased in early prototypes at CES 2026, indicating future commercialization potential; AI-powered ride assist systems, leveraging machine learning for adaptive performance and predictive maintenance while enabling proprietary software ecosystems; and ultra-lightweight materials, where carbon fiber, titanium, and advanced composites are driving the development of sub-10 kg high-performance e-bikes, significantly enhancing efficiency and user experience.

Future Market Outlook (2026-2034)

The global e-bike market is poised for sustained, broad-based growth through 2034, anchored by digital transformation, product premiumization, and geographic expansion into high-growth emerging markets. From a base of USD 28.08 Billion in 2025, the market is forecast to reach USD 48.60 Billion by 2034, representing absolute incremental value addition of approximately USD 20.5 Billion over the decade at a CAGR of 6.1%.

Technological disruptions—including AI-driven adaptive assist systems, solid-state battery advancements, ultra-lightweight design platforms, and emerging digital solutions for battery lifecycle management—are expected to significantly reshape the e-bike product landscape and consumer expectations. Manufacturers that successfully enhance range, efficiency, and system integration through next-generation technologies will gain a strong competitive edge, particularly in premium segments.

At the same time, e-bike usage is evolving beyond personal ownership toward integrated urban mobility solutions. The growth of commercial fleet electrification, shared micro-mobility, and multi-modal transport ecosystems is positioning e-bikes as a core component of urban infrastructure. Companies that effectively address both consumer and commercial use cases—while embedding connectivity, sustainability, and personalized riding experiences—will be best positioned to capture long-term market leadership.

Research Methodology

Primary Research

Primary research for this report involved structured consultation with industry participants, including e-bike manufacturers, component suppliers, retail distributors, fleet operators, and regulatory bodies across key markets in Asia Pacific, Europe, and North America. Expert interviews provided qualitative validation of market sizing estimates, competitive dynamics, and technology roadmap assessments conducted throughout 2024 and 2025.

Secondary Research

Secondary research encompassed a comprehensive review of company annual reports, regulatory filings, industry association publications (Confederation of the European Bicycle Industry, People for Bikes), trade databases, government transportation statistics, and publicly available financial data. Key secondary sources included IMARC Group’s proprietary market intelligence database, Statista, and international energy and transport agencies across 40+ countries.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanization indices, government EV adoption policy strength indices, historical e-bike penetration curves, and consumer expenditure data. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty and technology adoption pace variability through the 2026–2034 forecast period.

E-Bike Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Modes Covered | Throttle, Pedal Assist |

| Motor Types Covered | Hub Motor, Mid Drive, Others |

| Battery Types Covered | Lead Acid, Lithium Ion, Nickel-Metal Hydride (NiMH), Others |

| Classes Covered | Class I, Class II, Class III |

| Designs Covered | Foldable, Non-Foldable |

| Applications Covered | Mountain/Trekking Bikes, City/Urban, Cargo, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | AIMA Technology Group Co., Ltd., Giant Bicycles, MERIDA BIKES, Pedego, Riese & Müller GmbH, Jiangsu Xinri E-Vehicle Co., Ltd, Trek Bicycle Corporation, Yadea Technology Group Co., Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the e-bike market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global e-bike market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the e-bike industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the E-Bike Market Report

The global e-bike market was valued at USD 28.08 Billion in 2025 and is projected to reach USD 48.60 Billion by 2034, growing at a CAGR of 6.1% during 2026-2034.

The e-bike market is expected to grow at a CAGR of 6.1% during 2026-2034, reflecting sustained demand growth across both personal and commercial end-use segments globally.

Asia Pacific is the dominant region, accounting for 76.6% of global e-bike market revenues in 2025, driven primarily by China’s manufacturing scale, government EV mandates, and deep consumer familiarity with two-wheeled personal mobility.

North America is the fastest-growing region, projected at a CAGR of approximately 7.2% (2026–2034), led by expanding cycling infrastructure, state-level purchase incentives, and growing commercial last-mile delivery adoption.

Key drivers include rising urbanization and traffic congestion, government subsidies and purchase incentive programs, advancements in lithium-ion battery technology, rising fuel prices reinforcing cost competitiveness, and growing adoption of commercial last-mile delivery operations.

Pedal assist is the largest mode segment, holding a 66.9% market share in 2025, supported by broad regulatory access advantages, health and fitness appeal, and a natural pedaling experience that attracts a wide demographic range of riders.

Smart connectivity and IoT integration, cargo e-bike commercial fleet expansion (~45% growth in 2025), mid-drive motor adoption (CAGR ~8.1%), and ultra-lightweight solid-state battery designs are the fastest-growing trends through 2034.

The leading companies include AIMA Technology Group Co., Ltd., Giant Bicycles, MERIDA BIKES, Pedego, Riese & Müller GmbH, Jiangsu Xinri E-Vehicle Co., Ltd, Trek Bicycle Corporation, and Yadea Technology Group Co., Ltd.

Hub motors dominate the motor type segment with a 63.6% share in 2025, valued for minimal maintenance and cost competitiveness. Mid-drive motors, holding a 24.8% share, are the fastest-growing motor type at a CAGR of approximately 8.1%.

High-growth investment opportunities exist in cargo e-bikes for commercial fleet electrification, solid-state battery technology, AI-driven adaptive assist systems, premium performance e-bikes in Europe and North America, and emerging market expansion in India, Southeast Asia, Brazil, and GCC countries.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)