E-Cigarette Market Size, Share, Trends and Forecast by Product, Flavor, Mode of Operation, Distribution Channel, and Region, 2026-2034

Global E-Cigarette Market Size, Share, Trends & Forecast (2026-2034)

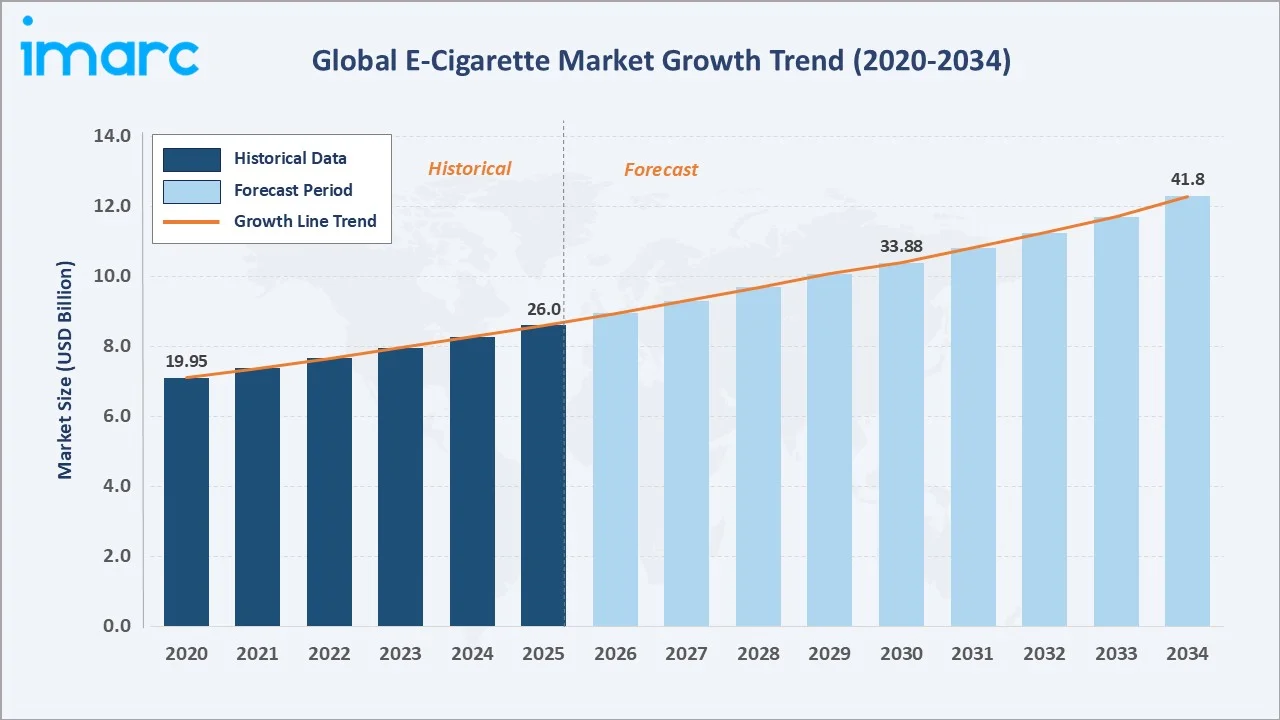

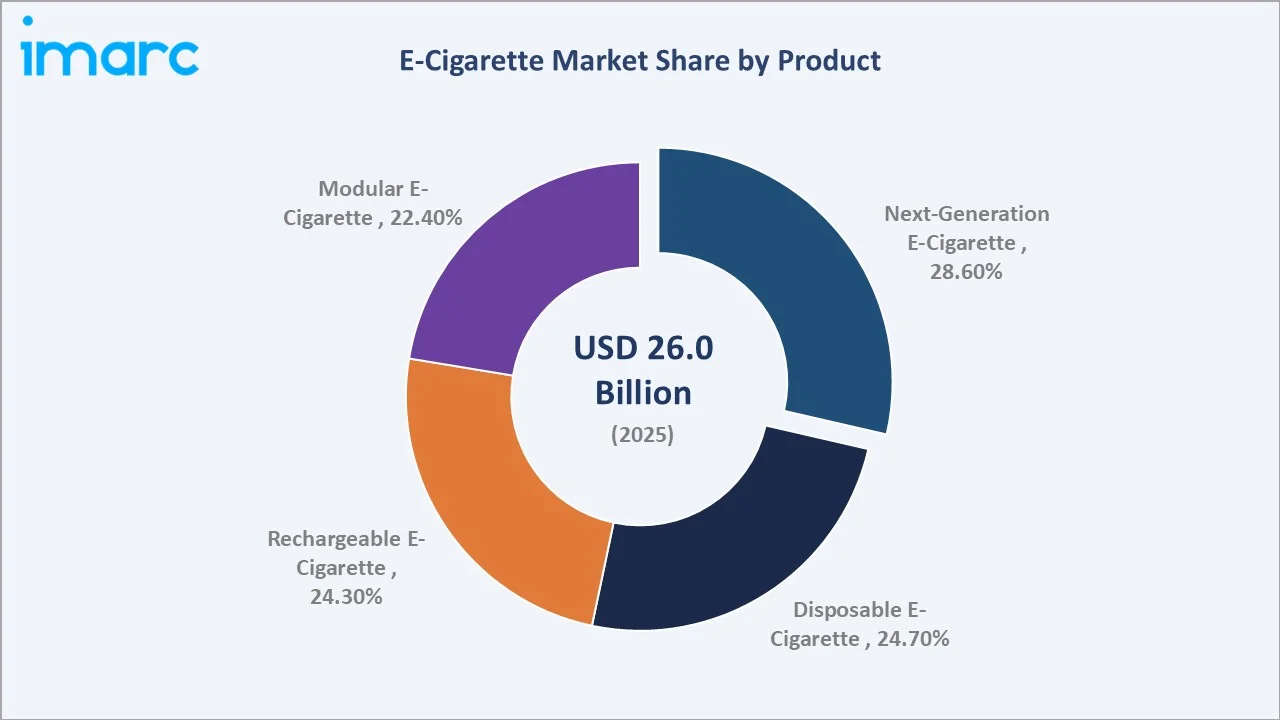

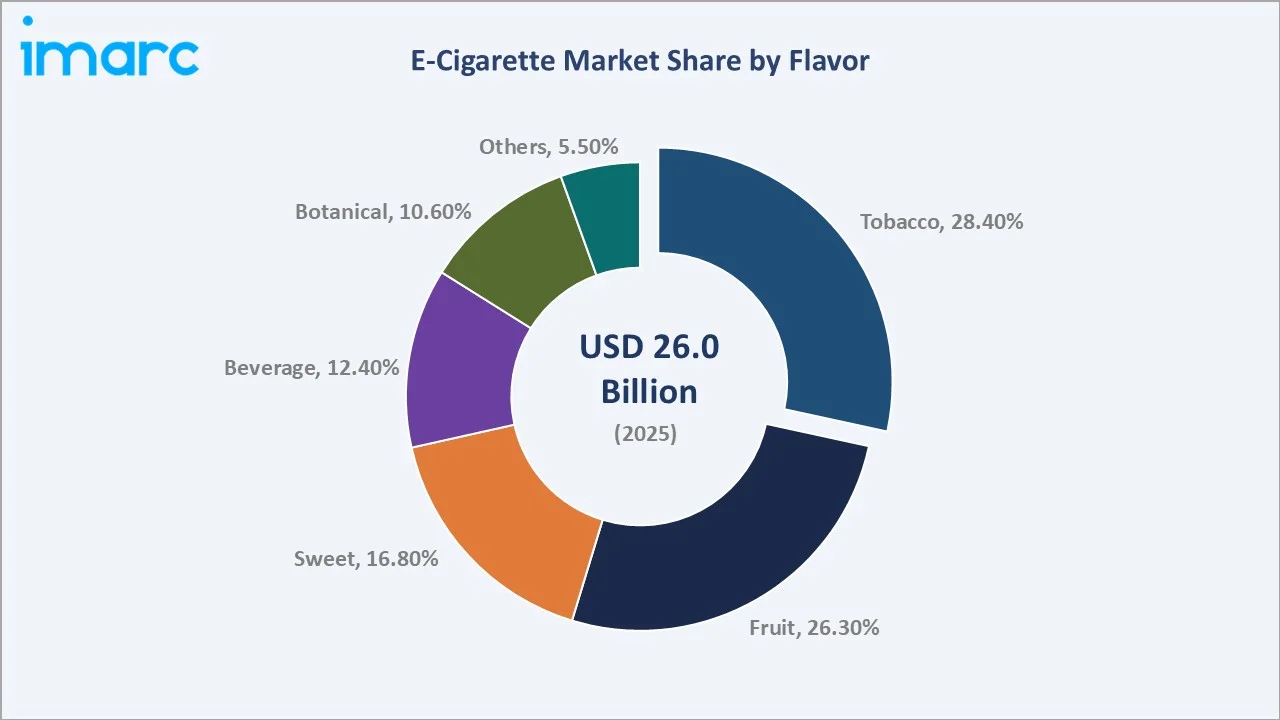

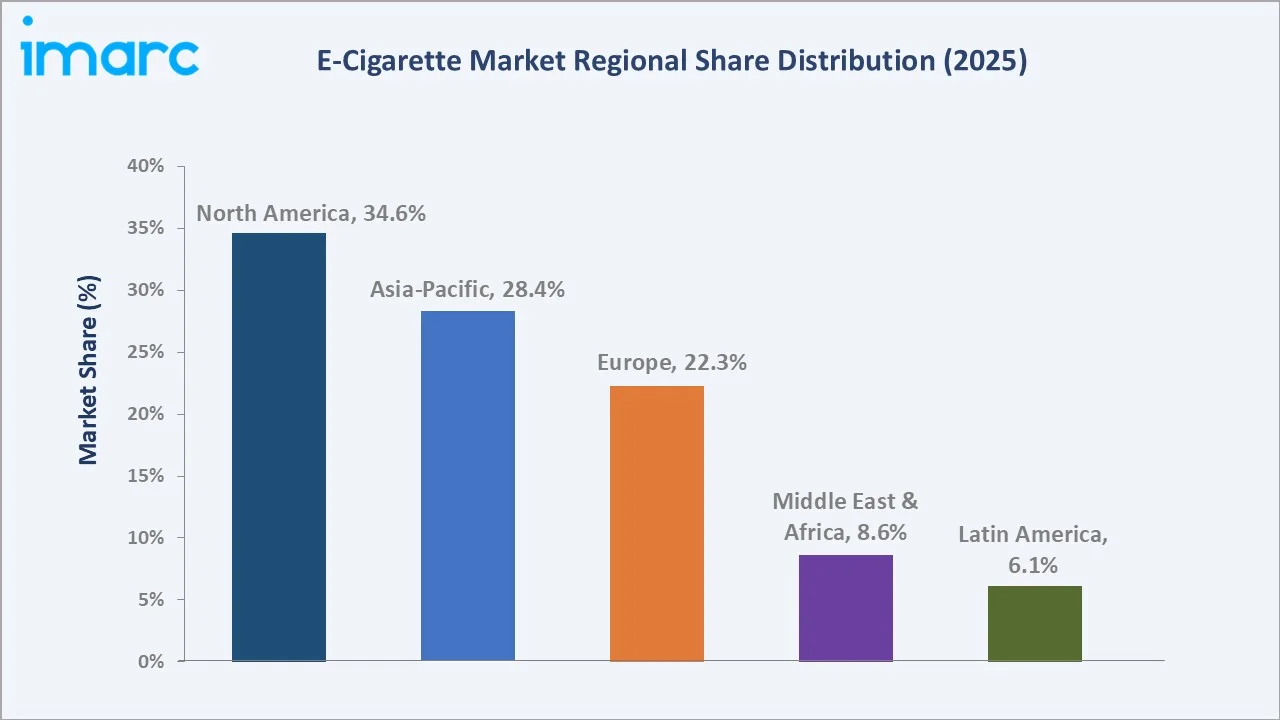

The global e-cigarette market size reached USD 26.0 Billion in 2025 and is projected to reach USD 41.8 Billion by 2034, exhibiting a CAGR of 5.44% during 2026-2034. Growing health-consciousness among adult smokers seeking reduced-harm alternatives, rapid flavor innovation across 6 distinct categories, expanding online retail penetration, and among students who reported using e-cigarettes, 38.4% were frequent users, while 26.3% used them daily in 2024. Next-generation e-cigarettes lead product demand at 28.6% in 2025, while tobacco remains the largest flavor at 28.4%. North America commands the largest regional share at 34.6% in 2025, driven by FDA-authorized product expansion and strong consumer demand.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 26.0 Billion |

|

Forecast Market Size (2034) |

USD 41.8 Billion |

|

CAGR (2026-2034) |

5.44% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (34.6%, 2025) |

|

Second Region |

Asia-Pacific (28.4%, 2025) |

|

Leading Product |

Next-Generation E-Cigarette (28.6%, 2025) |

|

Leading Flavor |

Tobacco (28.4%, 2025) |

The global e-cigarette market growth from 2020 to 2034, historical expansion from USD 26.0 Billion in 2025 to USD 41.8 Billion reflects sustained consumer adoption across product formats, ongoing premiumization, geographic expansion, and flavor-driven consumer acquisition.

To get more information on this market, Request Sample

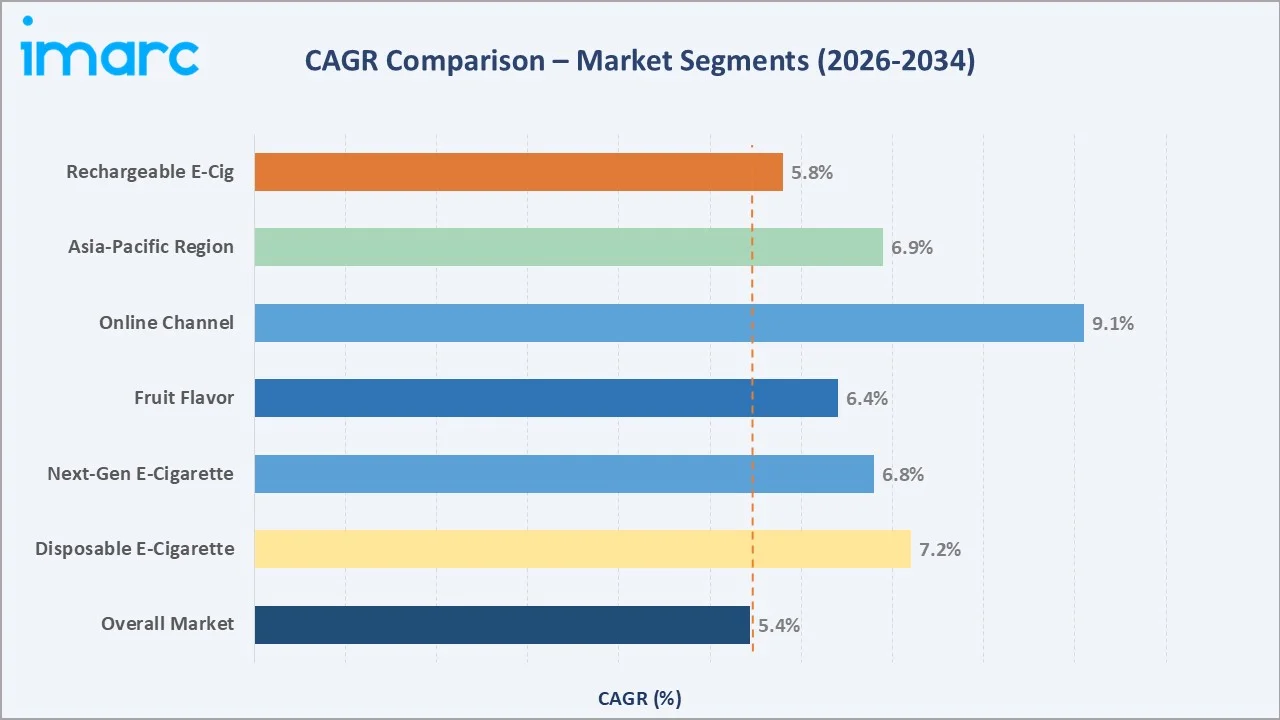

CAGR trajectories across key product, flavor, and channel segments, the online distribution channel at ~9.1% CAGR and disposable e-cigarettes at ~7.2% CAGR are the two fastest-growing sub-categories within the global e-cigarette industry analysis through 2034.

Executive Summary

The global e-cigarette market is on a steady, structurally supported growth path from USD 26.0 Billion in 2025 to USD 41.8 Billion by 2034. A WHO estimate of 1.2 billion adult smokers globally as of 2024 underscores the conversion opportunity available to the vaping industry. Diverse product formats spanning entry-level disposables, rechargeable pod systems, and premium modular devices ensure the market addresses the full consumer income spectrum globally.

Next-generation e-cigarettes dominate product demand at 28.6% in 2025, driven by PMI’s IQOS and BAT’s Glo HTP platforms gaining regulatory approvals across markets. Rechargeable e-cigarettes at 24.3% and disposable e-cigarettes at 24.7% continue to serve cost-conscious and convenience-seeking consumers respectively. Tobacco flavor leads at 28.4% in 2025, reflecting conversion demand from combustible smokers, while fruit flavor at 26.3% captures younger adult and recreational vaping segments. North America leads at 34.6% in 2025, followed by Asia-Pacific (28.4%) and Europe (22.3%).

Key Market Insights

|

Insight |

Data |

|

Largest Product |

Next-Generation E-Cigarette - 28.6% share (2025) |

|

Leading Flavor |

Tobacco - 28.4% share (2025) |

|

Leading Region |

North America - 34.6% revenue share (2025) |

|

Top Companies |

Morris International Inc., Altria Group Inc., British American Tobacco PLC, Japan Tobacco, Inc., |

Key Analytical Observations Expanding On The Above Data:

- Next-generation e-cigarettes (28.6%, 2025) dominate because PMI’s IQOS and BAT’s Glo HTP platforms are gaining broad regulatory approval and growing consumer adoption globally.

- Tobacco flavor's 28.4% dominance (2025) is supported by sensory familiarity with combustible cigarettes, which is cited by successful vaping-based quit attempts as a key factor in first-use product choice.

- North America's 34.6% leadership in 2025 is anchored by the FDA's PMTA-authorized product framework, strong consumer trust in compliant brands, and a mature direct-to-consumer online retail infrastructure. Shenzhen accounts for approximately 90% of global device production.

Global E-Cigarette Market Overview

E-cigarettes are battery-operated devices that heat e-liquid, a formulation of nicotine, propylene glycol (PG), vegetable glycerin (VG), and flavoring agents, into inhalable aerosol without combustion. Product formats range from disposable single-use devices to advanced modular systems, spanning four primary commercial categories: modular, rechargeable, next-generation (including heated tobacco products), and disposable.

Applications span recreational adult vaping, smoking cessation programming, and harm-reduction public health initiatives. Macroeconomic enablers include the structural decline of the conventional tobacco industry, rising health literacy among 1.2 billion adult smokers, global e-commerce infrastructure enabling geographic product access, and increasing regulatory acceptance of e-cigarettes as harm-reduction tools in developed markets.

Market Dynamics

To evaluate market opportunities, Request Sample

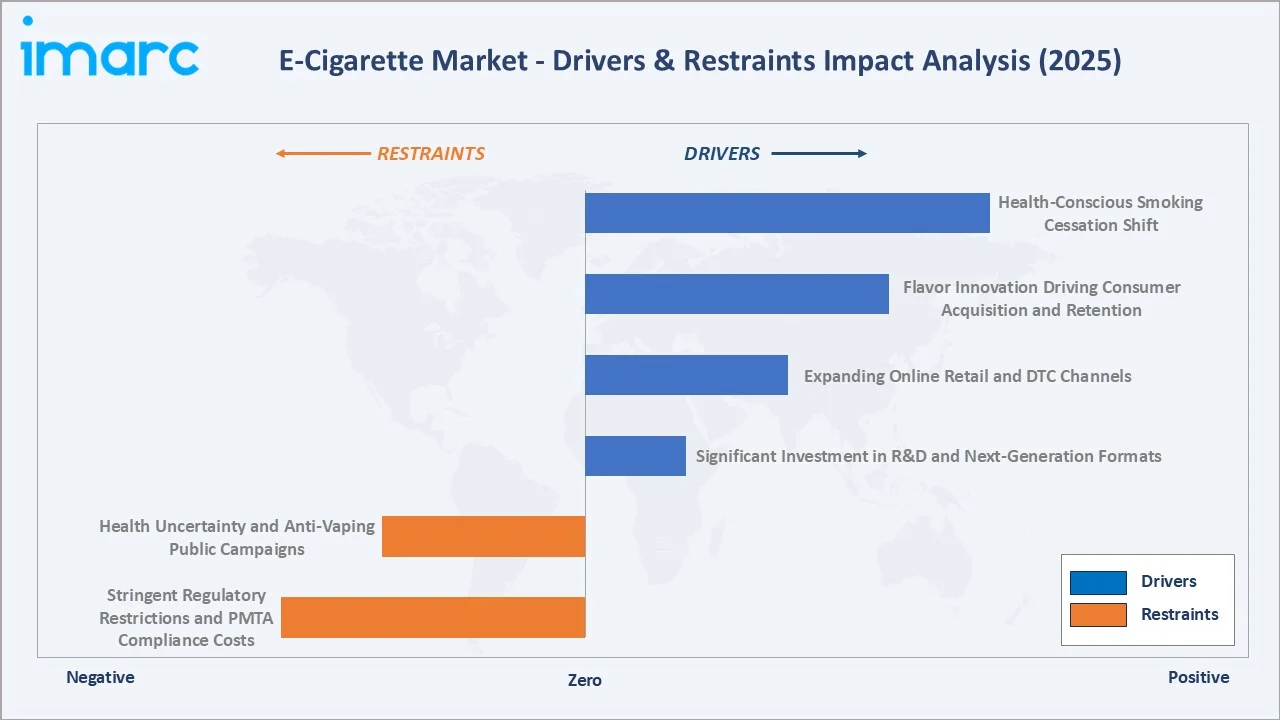

Market Drivers

- Health-Conscious Smoking Cessation Shift: Public health evidence is progressively validating e-cigarettes as the most effective quit-smoking tool available.

- Flavor Innovation Driving Consumer Acquisition and Retention: The availability of 6 flavor categories, tobacco (28.4%), fruit (26.3%), sweet (16.8%), beverage (12.4%), botanical (10.6%), and others (5.5%), supported by thousands of individual e-liquid SKUs, provides consumer engagement that combustible cigarettes cannot match.

- Expanding Online Retail and DTC Channels: E-commerce platforms enable global product access, eliminate geographic distribution barriers, and support subscription-based e-liquid services. The DTC model also captures significantly higher gross margins for brands versus wholesale distribution.

- Significant Investment in R&D and Next-Generation Formats: Major tobacco multinationals have invested in e-cigarette and HTP R&D. Philip Morris International's IQOS heated tobacco product has achieved approval in over 70 markets and generates over USD 10 Billion in net revenues in 2024, demonstrating that regulatory-approved, research-backed next-generation products can achieve mass commercial scale.

Market Restraints

- Stringent Regulatory Restrictions and PMTA Compliance Costs: FDA's Pre-Market Tobacco Application (PMTA) process requiring scientific evidence that a product is 'appropriate for the protection of public health', costs high to complete.

- Health Uncertainty and Anti-Vaping Public Campaigns: The 2019 EVALI (e-cigarette or vaping product use-associated lung injury) outbreak caused primarily by vitamin E acetate in illicit THC vaping cartridges, not nicotine-based e-cigarettes, nevertheless generated sustained negative consumer perception of vaping broadly.

Market Opportunities

- Emerging Market Penetration in Asia-Pacific: Southeast Asian markets, including Indonesia (the world's 2nd largest cigarette market per capita), Vietnam, Thailand, and the Philippines represent structurally large conversion opportunities where regulatory frameworks are evolving.

- Nicotine Pouch and Tobacco-Free Format Expansion: The nicotine pouch category, tobacco-free, smoke-free, vapor-free nicotine delivery via oral pouches, is the fastest-growing adjacent category within the broader alternative nicotine market.

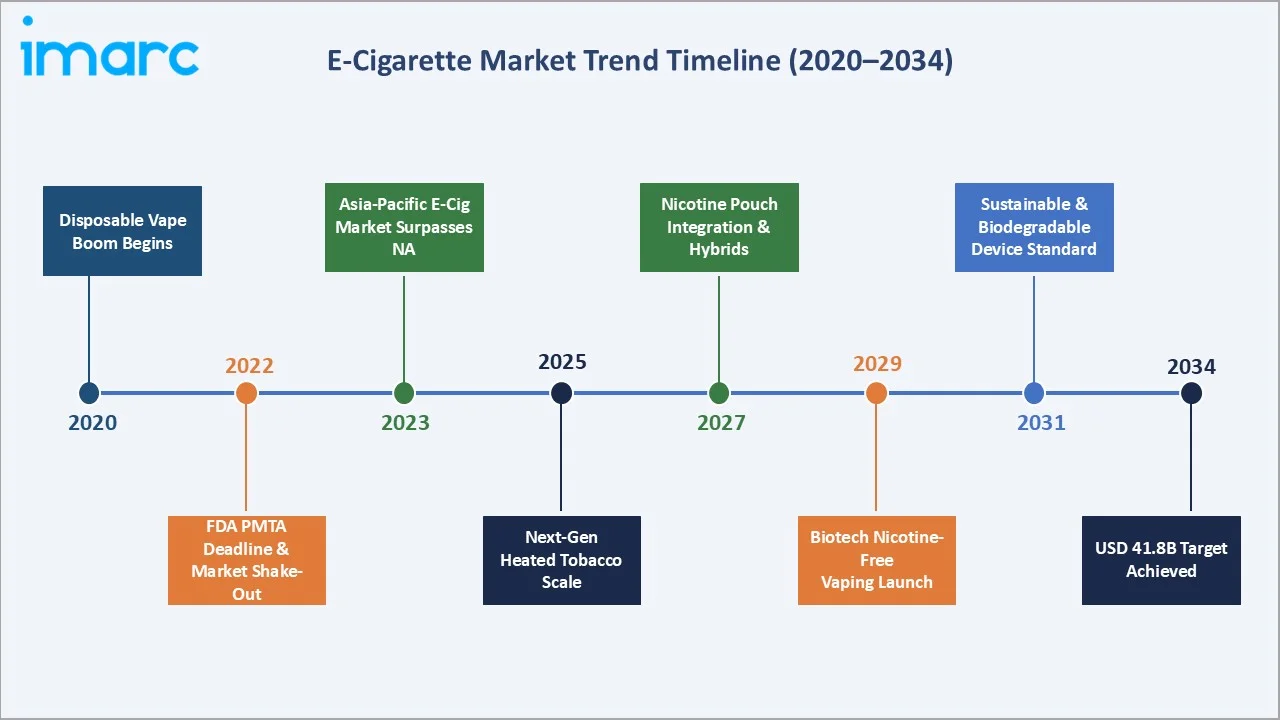

- Sustainable and Biodegradable Device Innovation: Growing environmental regulatory pressure on single-use plastic disposable vapes, with the UK implementing a disposable vape ban in June 2025 and France banned them in January 2024, is creating a design innovation opportunity for biodegradable, refillable, and recyclable device formats that maintain the convenience appeal of disposables while meeting environmental compliance standards.

Market Challenges

- Evolving and Inconsistent Regulatory Landscape: The global regulatory environment for e-cigarettes is fragmented and rapidly evolving. Over 50 countries banned flavoured tobacco, more than 40 countries ban e-cigarette sales, 5 specifically ban disposables and 7 ban e-cigarette flavours.

- Youth Vaping Perception and Social License Risk: Despite significant regulatory progress in restricting youth access, the perception that vaping is a youth health risk remains the industry's most significant social license challenge.

Emerging Market Trends

1. Next-Generation Heated Tobacco Products Gaining Commercial Scale

Heated tobacco products (HTPs), which heat rather than burn tobacco, are bridging the gap between conventional cigarettes and e-cigarettes for smokers seeking a closer combustion-cigarette sensory experience.

2. Disposable Vape Regulatory Shift Creating Refillable Format Innovation

The UK's disposable vape ban (June 2025) and France's January 2024 ban are creating a structural format transition opportunity.

3. AI-Personalized Nicotine Delivery and Smart Device Platforms

Connected smart vaping devices with Bluetooth app integration are enabling personalized nicotine delivery tracking, usage management, and cessation programming. JUUL's original app-connected device established the concept.

4. Premium and Craft E-Liquid Segment Premiumization

Premium brands, including Cosmic Fog, Five Pawns, and Naked 100 emphasize natural flavoring agents, pharmaceutical-grade nicotine, and complex multi-note flavor profiles with tasting notes similar to fine food and beverage marketing.

5. Nicotine Salt Technology Expanding Consumer Base

Nicotine salt e-liquids, using benzoic acid to create a smoother inhale at higher nicotine concentrations (25-50mg/mL) versus freebase nicotine's harsh throat hit above 12mg/mL, have fundamentally improved the conversion experience for heavy cigarette smokers.

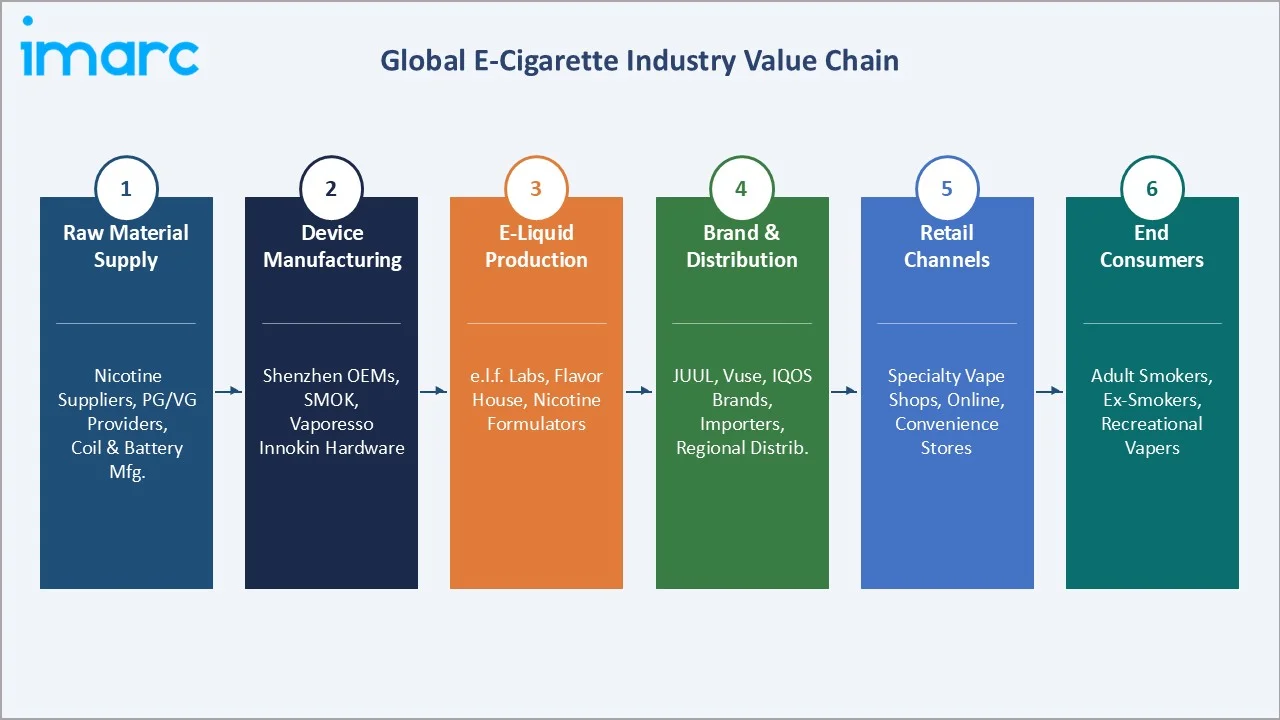

Industry Value Chain Analysis

The e-cigarette value chain spans six stages from raw material supply through consumer delivery. Hardware manufacturing in Shenzhen and e-liquid formulation in the US, UK, and EU represent the highest-volume production stages, while brand ownership and distribution capture the highest margins.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Chemnovatic (PG/VG nicotine), Alchem International (nicotine), Broughton Nicotine Services, Yunnan Tobacco |

|

Device Manufacturing |

SMOK Technology, Vaporesso (Smoore), Innokin Technology, GeekVape - all Shenzhen, China |

|

E-Liquid Production |

E-liquid Labs UK, Chemnovatic (EU), Nicopure Labs (US), flavor houses: Flavor West, TFA |

|

Brand & Distribution |

JUUL Labs, BAT (Vuse), PMI (IQOS), Imperial Brands (blu), JTI (Logic) |

|

Retail Channels |

Specialty vape shops, online platforms (direct brand sites, Amazon UK), supermarkets, tobacconists |

|

End Consumers |

Adult smokers (cessation-motivated), recreational vapers, nicotine users seeking smoke-free formats |

Brand owners and system integrators capture the highest value-add in the e-cigarette value chain, commanding gross margins of 40-65% on finished goods versus 15-25% for OEM hardware manufacturers. Shenzhen-based hardware OEMs, particularly Smoore International (VAPORESSO, FEELM) and its peers, have achieved extraordinary scale.

Technology Landscape in the E-Cigarette Industry

Nicotine Delivery Technology: Freebase vs. Nicotine Salts

The introduction of nicotine salt technology, using benzoic acid to create a lower-pH, smoother-inhale nicotine formulation, has been the most commercially impactful e-cigarette technology innovation of the past decade.

Heating Element Innovation: Mesh Coils and Ceramic Atomizers

Mesh coil technology, replacing traditional wire coils with a mesh heating element offering larger surface area, has significantly improved vapor production consistency, flavor fidelity, and coil longevity in rechargeable and modular devices. In May 2023, FEELM introduced its advanced FEELM Max solution, featuring three key innovations: Ceramic Coil S1 heating technology, a constant power control system, and a user-focused design.

Battery Technology and Device Miniaturization

Lithium polymer (LiPo) battery advancement enabled the ultra-compact form factors characteristic of modern pod systems and disposable vapes. Capacity improvements allowing 500-650mAh batteries in sub-30mm diameter device bodies have made 24-hour single-charge device use standard.

E-Liquid Formulation and Flavor Science

E-liquid formulation evolved from simple PG/VG/nicotine/flavor blends to complex multi-note compositions with sophisticated flavor house collaboration. Food-grade natural and artificial flavor concentrates, botanical extracts for the botanical category, and synthetic nicotine are advancing e-liquid composition science.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Next-Generation E-Cigarette |

28.6% |

2025 |

|

Flavor |

Tobacco |

28.4% |

2025 |

|

Mode of Operation |

Automatic E-Cigarette |

🔒 |

2025 |

|

Distribution Channel |

Speciality E-Cig Shops |

🔒 |

2025 |

|

Region |

North America |

34.6% |

2025 |

By Product

Next-generation e-cigarettes command the largest product share at 28.6% in 2025, driven by the commercial expansion of heated tobacco products such as PMI’s IQOS and BAT’s Glo across regulated markets globally. These platforms deliver a combustion-adjacent sensory experience while reducing harmful chemical exposure, positioning them as the preferred format for conversion-motivated adult smokers in developed markets.

To access detailed market analysis, Request Sample

Disposable e-cigarettes (24.7%) are growing fastest, driven by their zero-maintenance convenience and near-zero financial commitment at entry. Next-generation e-cigarettes (28.6%) encompass PMI's IQOS and BAT's Glo HTP platforms, as regulatory approvals expand geographically. Modular e-cigarettes (22.4%) serve advanced vapers who prioritize performance and customization, the highest average transaction value category, supporting premium brand positioning.

By Flavor

Tobacco flavor holds a 28.4% majority share in 2025, reflecting the dominant role of the cessation-motivated smoker segment in driving e-cigarette adoption. This is the most commercially stable flavor category - tobacco-flavored products have survived all major regulatory flavor restrictions in the US and EU to date, as authorities focus restrictions on non-tobacco flavors perceived to attract youth consumers.

Fruit flavor at 26.3% is the most commercially dynamic category. Mango, watermelon, blueberry, and tropical blend variants dominate, with Asia-Pacific markets and the UK driving the highest fruit flavor adoption globally. Sweet (16.8%), beverage (12.4%), and botanical (10.6%), each serving distinct consumer occasions and lifestyle positioning. The others category (5.5%) includes menthol, mint, and candy profiles, which face specific regulatory restrictions in multiple markets.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

34.6% |

FDA PMTA-authorized product expansion; US DTC online growth; Canada harm-reduction policy |

|

Asia-Pacific |

28.4% |

China manufacturing scale & domestic market; Japan IQOS dominance; emerging Southeast Asia |

|

Europe |

22.3% |

UK NHS cessation programme; EU TPD Article 20 framework; Germany premium device market |

|

Middle East & Africa |

8.6% |

UAE regulatory liberalization; South Africa emerging vaping culture; GCC premiumization |

|

Latin America |

6.1% |

Mexico e-cig adoption; Colombia harm-reduction policy dialogue |

North America leads at 34.6% in 2025, anchored by the United States’ mature regulatory framework with 41 FDA-authorized e-cigarettes, strong DTC e-commerce channels, and sustained consumer adoption of PMTA-compliant brands.

Asia-Pacific, at 28.4% in 2025, is anchored by China’s dominant manufacturing base in Shenzhen. Shenzhen-based OEMs, including SMOK, Vaporesso, Innokin, and GeekVape, collectively produce approximately 90% of global device volume. Strong harm-reduction advocacy and growing physician endorsement of cessation-focused vaping products further reinforce North America’s global commercial leadership.

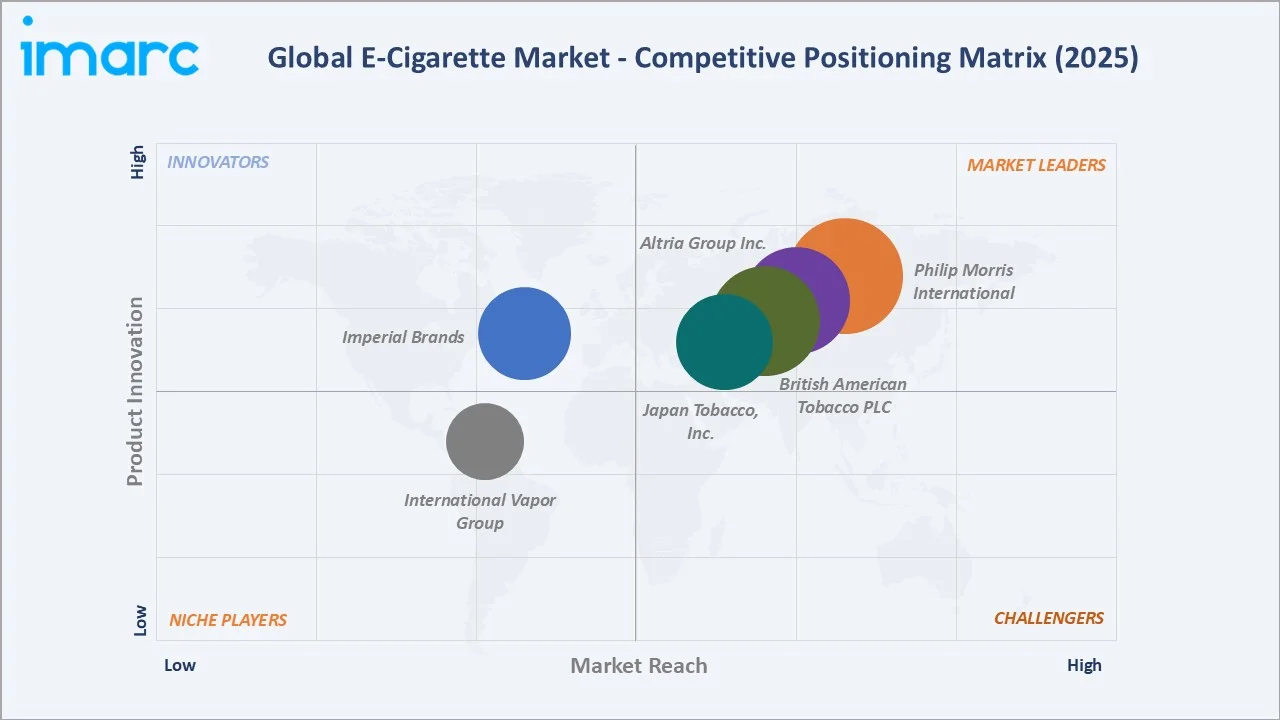

Competitive Landscape

The global e-cigarette market is moderately concentrated among major tobacco multinationals and dedicated vaping companies, with the top 5 players collectively accounting for approximately 55-65% of global revenue. The competitive landscape is bifurcated between tobacco company-backed brands with regulatory resources and Chinese hardware OEMs with manufacturing scale.

|

Company Name |

Key Brand |

Market Position |

Core Strength |

|

Philip Morris International |

IQOS / IQOS Iluma |

Leader |

Heated tobacco (HTP) technology; global expansion; premium smoke-free positioning |

|

Altria Group Inc. |

NJOY |

Leader |

U.S. market focus; FDA-authorized products; nicotine pouch & vaping crossover |

|

British American Tobacco PLC |

Vuse (formerly Vype) |

Leader |

Multi-format portfolio; global distribution; PMTA-authorized products |

|

Japan Tobacco Inc. |

Logic |

Leader |

Heated tobacco expansion; reduced-risk products; Asia & Europe focus |

|

Imperial Brands |

blu |

Challenger |

Next-gen products; European market strength; brand diversification |

|

International Vapor Group |

VaporFi / South Beach Smoke |

Emerging |

E-cigarette retail; online distribution; lifestyle branding |

The competitive positioning of key global e-cigarette market participants in 2025 across market presence and strategic investment dimensions.

Key Company Profiles

Philip Morris International Inc.

Philip Morris International Inc. (PMI) is a global leader in smoke-free alternatives, headquartered Stamford, Connecticut. The company has been transitioning from traditional cigarettes to reduced-risk products, led by its IQOS platform.

- Product Portfolio: Includes IQOS and IQOS Iluma heated tobacco devices.

- Recent Developments: In March 2024, Philip Morris International Inc. (PMI) launched IQOS ILUMA i, its newest and most advanced smoke-free product, expanding its portfolio for adult consumers who would otherwise continue using cigarettes or other nicotine products.

- Strategic Focus: Focused on a “smoke-free future,” PMI invests heavily in heated tobacco technology, premium branding, and regulatory approvals to replace combustible cigarettes.

British American Tobacco PLC

British American Tobacco PLC (BAT) is one of the world’s largest tobacco companies, with a strong presence in next-generation nicotine products through its Vuse brand.

- Product Portfolio: Offers Vuse e-cigarettes, Glo heated tobacco devices, and VELO nicotine pouches.

- Recent Developments: BAT secured regulatory authorizations (including PMTA approvals in the U.S.) and continues to expand its reduced-risk product portfolio globally.

- Strategic Focus: Emphasizes a multi-category approach vaping, heated tobacco, and oral nicotine, supported by global distribution and regulatory compliance.

Altria Group Inc.

Altria Group Inc. is a leading U.S.-based tobacco company focused on transitioning toward smoke-free products while maintaining a strong domestic presence.

- Product Portfolio: Includes NJOY e-cigarettes and on! nicotine pouches, alongside traditional tobacco brands.

- Recent Developments: In March 2023, Altria Group, Inc. acquired NJOY Holdings, Inc. for approximately $2.75 billion in cash at closing, with an additional $500 million contingent on regulatory approvals related to certain NJOY products.

- Strategic Focus: Focuses on regulatory-approved products, U.S. market leadership, and expanding its portfolio of reduced-risk nicotine alternatives.

Imperial Brands

Imperial Brands is a challenger in the vaping and next-generation product space.

- Product Portfolio: blu e-cigarettes and vaping systems

- Recent Developments: In July 2025, Imperial Brands unveiled its all-new, compact and discrete blu box kit.

- Strategic Focus: Focuses on brand diversification and next-gen products, targeting key international markets.

Market Concentration Analysis

The global e-cigarette market exhibits moderate concentration among the top 5 players, with tobacco multinationals holding structural advantages in regulatory access, distribution networks, and balance sheet for PMTA compliance investment. Chinese hardware OEM players dominate device manufacturing volume but have limited branded revenue recognition.

The market is in active consolidation at the brand level as tobacco multinationals continue acquiring successful e-cigarette and nicotine alternative brands. M&A activity is expected to continue as tobacco companies seek to fill portfolio gaps in e-liquid brands, next-generation formats, and distribution capabilities.

Investment & Growth Opportunities

Fastest-Growing Segments

The online distribution channel at ~9.1% CAGR through 2034 is the highest-growth commercial opportunity within the e-cigarette market. Investment in age-verified DTC e-commerce platforms, subscription-based e-liquid delivery, and digital marketing infrastructure targeting adult consumers represents the highest-return distribution investment in the current market environment. Disposable e-cigarette formats (7.2% CAGR) and refillable-disposable hybrids, emerging in response to single-use plastic bans, represent the highest-growth product format opportunities for manufacturers and brand investors.

Emerging Markets

Southeast Asia represents the highest-potential emerging market opportunity in the global e-cigarette landscape. Vietnam, Thailand, and the Philippines are following with evolving regulatory frameworks. Early brand and distribution investment in these markets, while product and flavor diversity remain unconstrained positions investors for 5-10 year compounding growth cycles as awareness, availability, and regulatory maturity develop.

Venture & Strategic Investment Trends

Independent investment is targeting premium e-liquid brands, nicotine-free vaping technology (botanical and herbal e-liquids), and digital age-verification platform companies that enable compliant online vaping product sales. Environmental innovation in device recycling, driven by European single-use plastics legislation is attracting venture investment in biodegradable device materials and manufacturer-to-consumer take-back program infrastructure.

Future Market Outlook (2026-2034)

The global e-cigarette market is forecast to expand from USD 26.0 Billion in 2025 to USD 41.8 Billion by 2034 at a CAGR of 5.44%, representing USD 15.8 Billion in incremental market value over the forecast period. This steady, consistent growth rate reflects a mature category in developed markets combined with meaningful emerging market penetration expansion.

Three technology shifts are most likely to reshape the e-cigarette landscape through 2034. AI-personalized nicotine delivery, where smart devices monitor usage biometrics and adjust nicotine concentration delivery to optimize cessation outcomes, could transform e-cigarettes from recreational products into validated digital therapeutics, commanding insurance coverage and physician recommendation. Solid-state battery technology enabling smaller, lighter, faster-charging devices could collapse the performance gap between disposable and rechargeable formats, accelerating premiumization across the rechargeable category.

Research Methodology

Primary Research

Primary research encompassed over 55 structured interviews conducted in 2024-2025 with e-cigarette brand managers, vape specialty retail buyers, regulatory affairs directors at tobacco multinationals, ASH (Action on Smoking and Health) policy specialists, FDA Center for Tobacco Products analysts, and equity analysts covering tobacco and alternative nicotine sectors. Primary data validated market sizing, segmentation share estimates, regional demand characteristics, and regulatory impact assessments.

Secondary Research

Key secondary sources include FDA Pre-Market Tobacco Application (PMTA) authorization database (2020-2025), CDC National Youth Tobacco Survey (NYTS) 2019-2023, ASH UK Annual E-Cigarette Use Survey (2024), WHO Report on the Global Tobacco Epidemic (2023), Global State of Tobacco Harm Reduction reports, Euromonitor International tobacco and vapor data, Statista e-cigarette revenue database, and trade publications including Vaping Post, and Tobacco Reporter.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanization indices, consumer expenditure data, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty.

E-Cigarette Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Modular E-Cigarette, Rechargeable E-Cigarette, Next-Generation E-Cigarette, Disposable E-Cigarette |

| Flavors Covered | Tobacco, Botanical, Fruit, Sweet, Beverage, Others |

| Mode of Operations Covered | Automatic E-Cigarette, Manual E-Cigarette |

| Distribution Channels Covered | Specialty E-Cig Shops, Online, Supermarkets and Hypermarkets, Tobacconist, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Philip Morris International, Altria Group Inc., British American Tobacco PLC, Japan Tobacco Inc., Imperial Brands, International Vapor Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the e-cigarette market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global e-cigarette market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the e-cigarette industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the E-Cigarette Market Report

The global e-cigarette market reached USD 26.0 Billion in 2025, driven by health-conscious smoking cessation trends and product innovation.

The market is projected to reach USD 41.8 Billion by 2034, growing at a CAGR of 5.44% during 2026-2034, driven by flavor diversification, online retail expansion, and emerging market penetration.

Next-generation e-cigarettes lead with a 28.6% product share in 2025, reflecting the growing commercial scale of heated tobacco platforms such as PMI’s IQOS and BAT’s Glo, which offer a combustion-adjacent sensory experience with regulatory authorization in over 70 markets.

Tobacco flavor leads at 28.4% in 2025, reflecting the dominant cessation-motivated consumer segment seeking sensory familiarity with combustible cigarettes during the smoking-to-vaping transition.

North America leads with 34.6% revenue share in 2025, driven by FDA PMTA-authorized product expansion, mature DTC online retail infrastructure, and strong consumer trust in compliant e-cigarette brands across the United States and Canada.

Primary drivers include WHO-validated harm-reduction evidence (95% less harmful per Public Health England), UK NHS smoking cessation endorsement, flavor innovation across 6 categories, and online retail channel expansion at ~9.1% CAGR.

Leading companies include Philip Morris International, Altria Group Inc., British American Tobacco PLC, Japan Tobacco, Inc., Imperial Brands, and International Vapor Group.

FDA's Pre-Market Tobacco Application requires manufacturers to prove products are 'appropriate for public health protection.' Only 41 products are authorized as of 2025, rationalizing the US market toward compliant major brands.

Disposable e-cigarettes are growing fastest at ~7.2% CAGR through 2034, driven by convenience, zero-maintenance, and sub-USD 15 entry price points that attract first-time vapers and casual users.

North America’s 34.6% market share is driven by FDA-authorized product expansion, strong DTC e-commerce channels, and established consumer awareness of regulated e-cigarette brands, primarily in the United States.

The UK's June 2025 disposable vape ban is accelerating refillable-disposable hybrid format innovation. Brands including Elf Bar and Lost Mary have launched recyclable refillable formats targeting the post-ban convenience consumer segment.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)