East Africa Cement Market Size, Share, Trends and Forecast by Type, Application, and Region, 2026-2034

East Africa Cement Market Size, Share, Trends & Forecast (2026-2034)

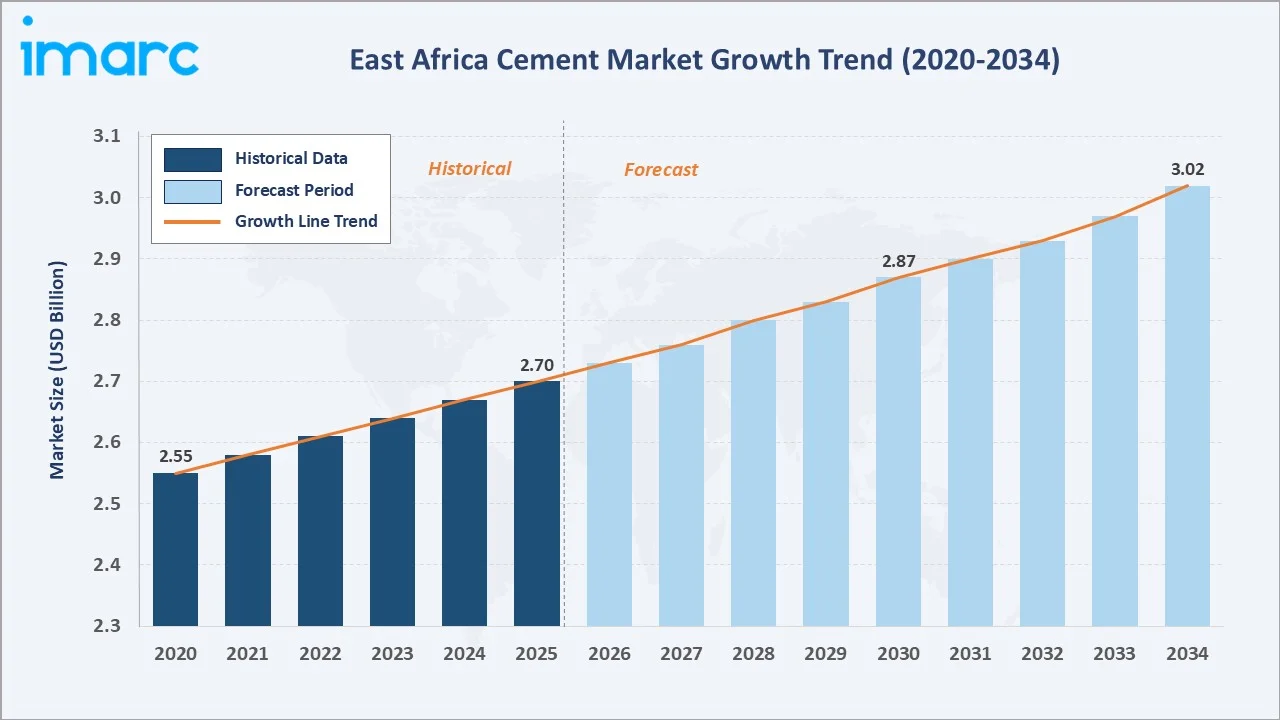

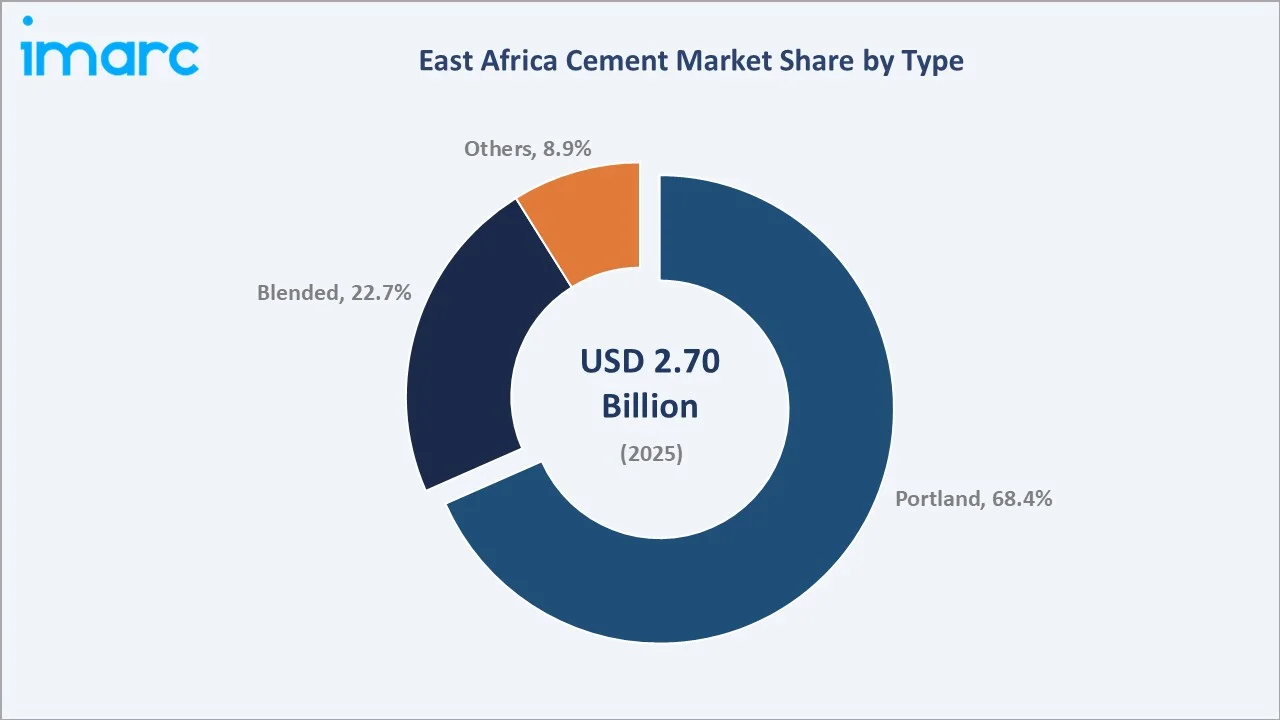

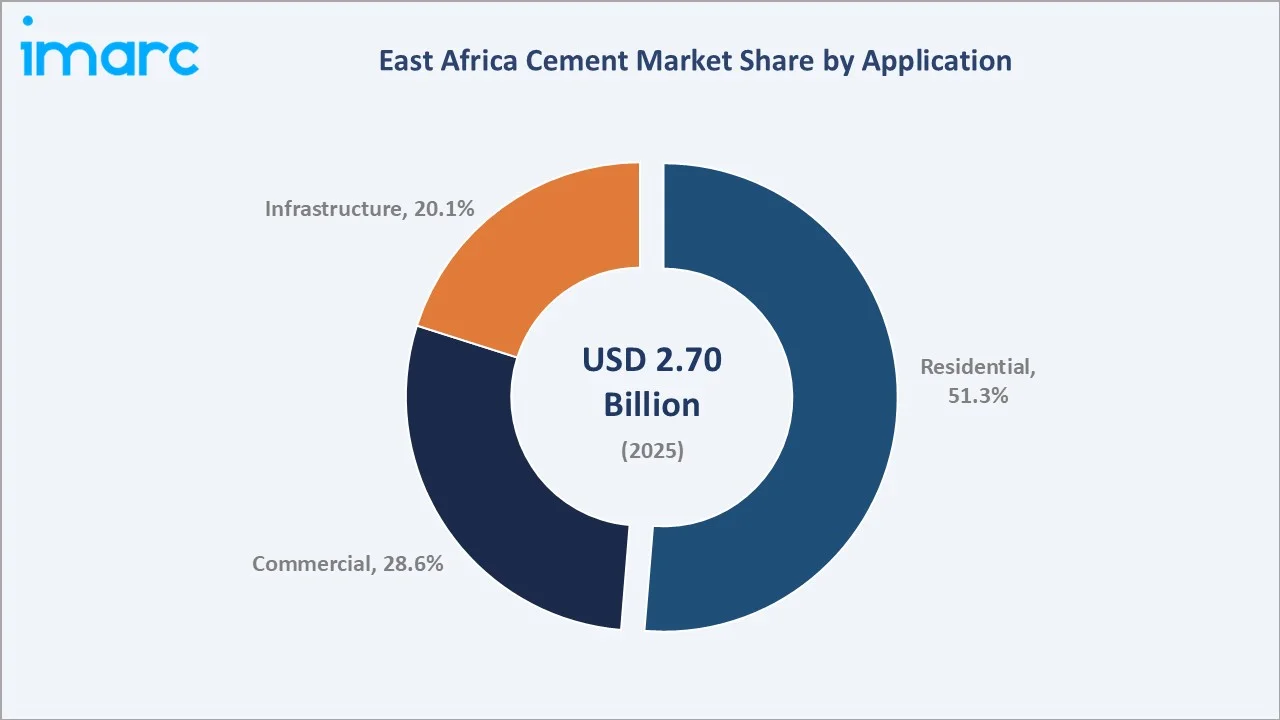

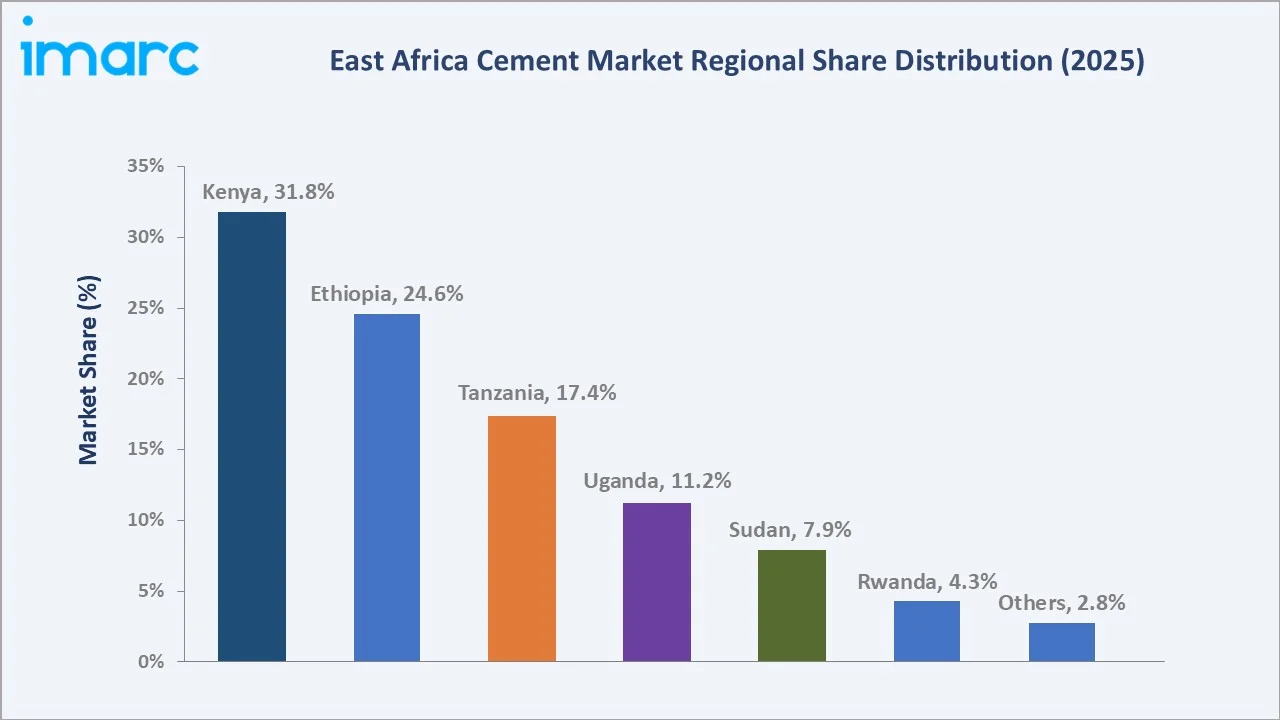

The East Africa cement market size was valued at USD 2.70 Billion in 2025 and is projected to reach USD 3.02 Billion by 2034, exhibiting a CAGR of 1.20% during 2026-2034. Rising urban housing demand, infrastructure pipelines under Vision 2030 frameworks, cross-border trade corridors linking Kenya, Ethiopia, Tanzania and Uganda, and the shift toward blended cement are driving market growth. Portland cement leads the product type segment at 68.4% in 2025, while Residential construction dominates the application segment at 51.3%. Kenya accounts for 31.8% of regional revenue in 2025, the largest country market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.70 Billion |

|

Forecast Market Size (2034) |

USD 3.02 Billion |

|

CAGR (2026-2034) |

1.20% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country Market |

Kenya (31.8% share, 2025) |

|

Fastest Growing Country |

Rwanda (CAGR ~2.4%) |

|

Leading Type |

Portland (68.4%, 2025) |

|

Leading Application |

Residential (51.3%, 2025) |

The East Africa cement market growth trajectory from 2020 through 2034 reflects steady historical expansion supported by post-pandemic recovery, sustained public infrastructure delivery, and a forecast curve anchored by urban housing demand and cross-border trade integration under AfCFTA.

To get more information on this market, Request Sample

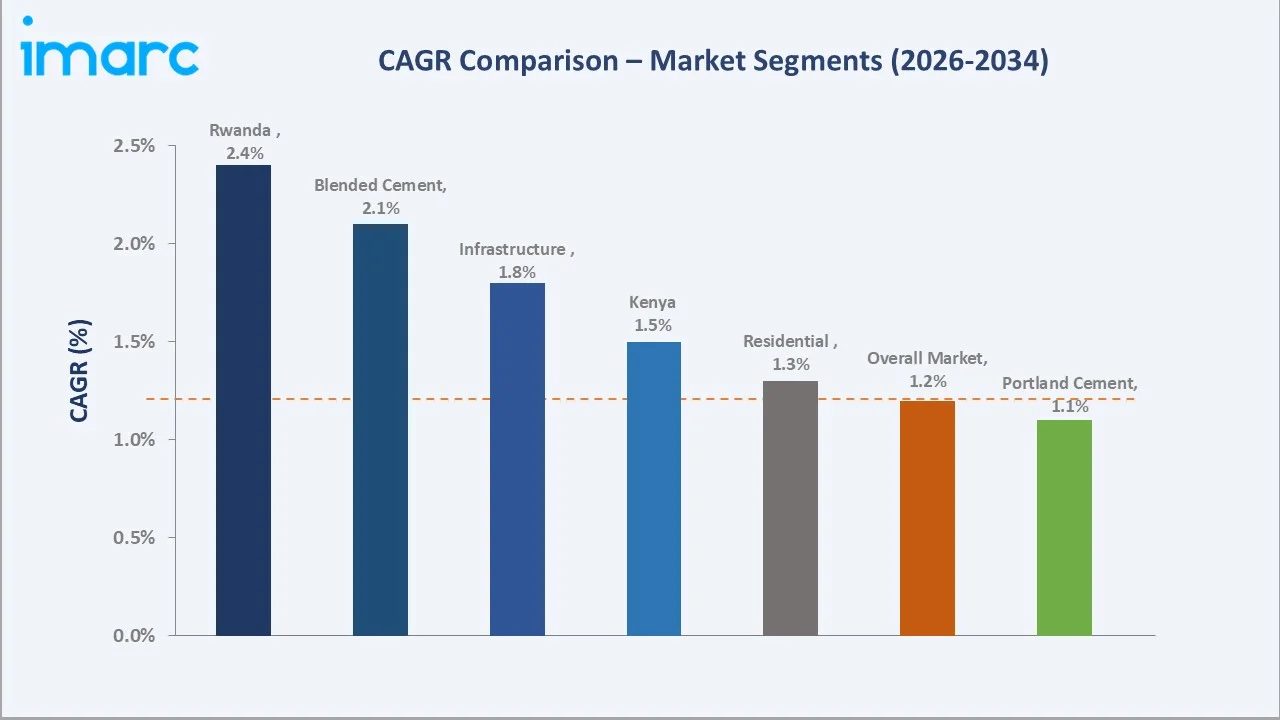

Segment-level CAGR comparison through 2034 highlights Rwanda and blended cement as the two fastest-growing sub-segments within the East Africa cement industry analysis, supported by new capacity and low-carbon formulation uptake.

Executive Summary

The East Africa cement market is in a phase of steady, infrastructure-led expansion, shaped by urbanisation, public capital spending, and a gradual shift toward lower-carbon production. Valued at USD 2.70 Billion in 2025, the market is forecast to reach USD 3.02 Billion by 2034 at a CAGR of 1.20%. Urban populations across Sub-Saharan Africa are expanding at approximately 3.5–4.0% annually, reinforcing sustained demand for residential and commercial cement.

Portland cement commands the dominant product type share at 68.4% in 2025, driven by OEM-standard strength grades, contractor familiarity, and universal applicability. Blended cement at 22.7% is the faster-growing type, fuelled by lower production cost, improved carbon profile, and donor-funded project preferences for sustainable materials.

Kenya dominates with a 31.8% regional revenue share in 2025, led by the Affordable Housing Programme targeting 250,000 units annually, followed by Ethiopia at 24.6% and Tanzania at 17.4%. Uganda holds 11.2% and Sudan 7.9%, characterised by reconstruction activity and cross-border flows. Rwanda (4.3%) shows the fastest relative growth trajectory through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Type |

Portland Cement - 68.4% share (2025) |

|

Largest Application |

Residential Construction - 51.3% share (2025) |

|

Leading Country |

Kenya - 31.8% revenue share (2025) |

|

Second Country |

Ethiopia - 24.6% revenue share (2025) |

|

Top Companies |

Bamburi Group PLC, Dangote Cement Plc., Tororo Cement Limited, Tanzania Portland Cement Public Limited (Twiga), Mugher Cement, Habesha Cement, Simba Cement Factory LTD, Cimerwa |

Key Analytical Observations Supporting the Above Data:

- Portland's 68.4% dominance in 2025 reflects the standardisation around 32.5 and 42.5 strength grades, consistent contractor demand, and the lowest per-bag cost point in the regional product mix.

- Residential's 51.3% demand anchor in 2025 reflects 4.2% annual urban population growth, 9-11% mortgage book expansion in Kenya, and government programmes targeting 400,000+ affordable homes by 2030.

- Kenya's 31.8% regional dominance in 2025 reflects its role as both the region's largest construction market and most diversified cement producer ecosystem across Mombasa, Athi River, and Emali.

East Africa Cement Market Overview

Cement in East Africa is an integrated industrial platform combining limestone quarrying, clinker manufacturing, grinding, blending, bagging, and organised distribution across Kenya, Ethiopia, Tanzania, Uganda, Sudan, Rwanda and smaller neighbouring economies. Producers increasingly serve as single-point suppliers for residential, commercial and infrastructure projects.

Applications span residential buildings, commercial real estate, transport infrastructure, water conveyance, and industrial plants. Export activity is growing toward landlocked neighbours, including DRC, South Sudan and Burundi, where domestic production remains limited.

Macroeconomic enablers include sustained regional economic growth, a rebound in public capital expenditure, rising remittance-supported residential construction, and ongoing EAC trade harmonisation, collectively supporting cement demand across East Africa. In Kenya, cement consumption reached approximately 4.76 million tonnes in H1 2025, reflecting strong year-on-year growth driven by housing and infrastructure activity.

Market Dynamics

To evaluate market opportunities, Request Sample

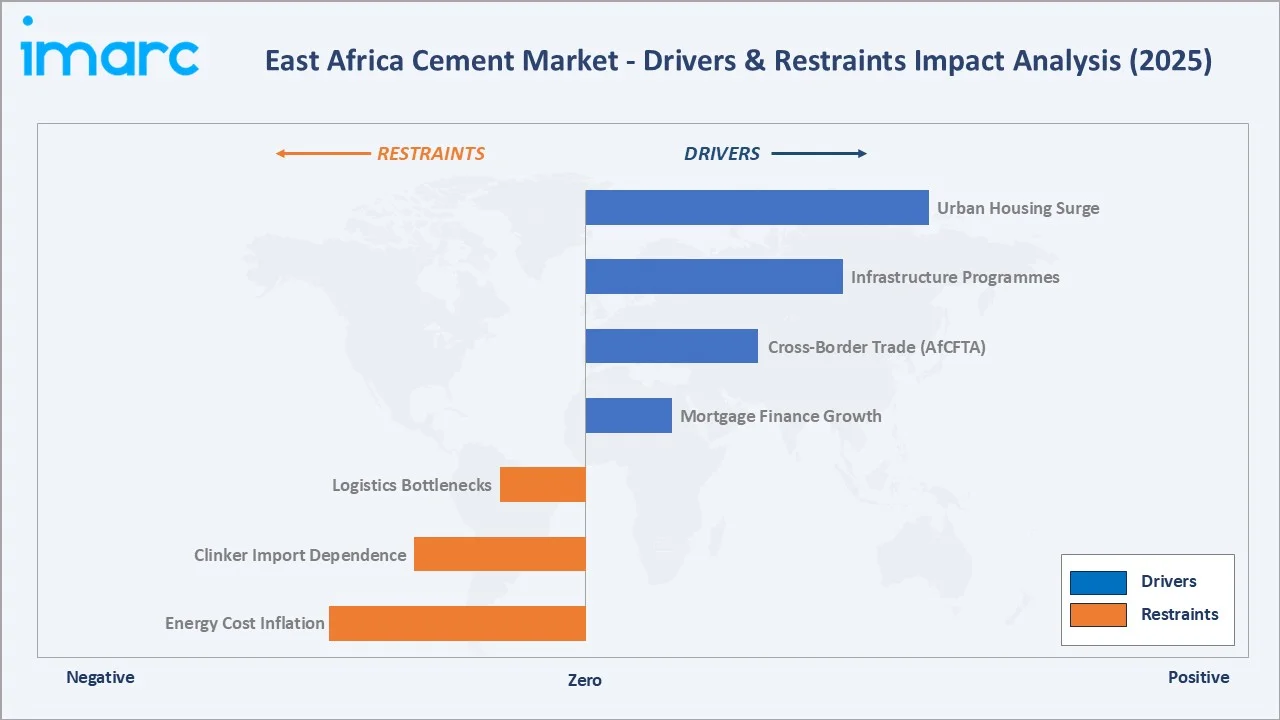

Market Drivers

- Urban Housing Surge: Urban housing demand remains a core growth driver, supported by rapid urbanisation across East Africa, where rising population migration to cities is accelerating residential construction and sustaining cement consumption.

- Infrastructure Programmes: Infrastructure investment across East Africa is led by large-scale transport and energy projects in Kenya, Ethiopia, and Tanzania, including the LAPSSET corridor and renewable energy developments. In Kenya, SGR extensions linked to the LAPSSET corridor alone are estimated at approximately USD 16 billion, underscoring the scale of ongoing infrastructure expansion in the region.

- Cross-Border Trade (AfCFTA): AfCFTA implementation is facilitating reduced cement tariffs and improved intra-African trade flows, enabling Kenyan and Tanzanian surplus capacity to serve DRC, South Sudan and Burundi at competitive delivered prices.

- Mortgage Finance Growth: Kenya’s mortgage market continues to expand gradually, supported by growth in outstanding mortgage portfolios and increased participation in housing finance, alongside emerging mortgage ecosystems in Rwanda and Ethiopia, improving end-user purchasing power for formal home construction.

Market Restraints

- Energy Cost Inflation: Thermal and electricity costs account for a significant share of clinker production cost, exposing producer margins to fuel price swings, grid reliability issues, and FX volatility on imported coal and heavy fuel oil.

- Clinker Import Dependence: Uganda, Rwanda and parts of Tanzania import clinker, creating FX exposure, port-congestion cost pass-through, and vulnerability to shipping market cycles.

- Logistics Bottlenecks: Poor last-mile roads, seasonal port congestion at Mombasa and Dar es Salaam, and limited rail capacity inflated inland cement delivery costs and reduced supply chain efficiency.

Market Opportunities

- Green and Blended Cement: The share of blended cement is increasing steadily, indicating strong growth potential for pozzolana, fly ash, and limestone-based formulations, particularly in donor-funded and sustainability-linked infrastructure projects.

- Affordable Housing Partnerships: Government-led housing initiatives across Kenya, Rwanda, and Ethiopia are creating sustained demand visibility and enabling long-term supply partnerships with institutional stakeholders.

- Waste Heat Recovery and Alternative Fuels: Adoption of waste heat recovery systems and alternative fuels such as biomass and refuse-derived fuel is improving energy efficiency and reducing production costs, with increasing uptake across cement plants in the region.

Market Challenges

- Capacity Utilisation Pressure: Regional average capacity utilisation remained moderate, constraining fixed-cost absorption and investment economics for greenfield expansion.

- Regulatory and Tax Volatility: Frequent excise duty revisions and cement-specific levies introduced uncertainty for capex decisions, particularly for plant modernisation and alternative fuel retrofits.

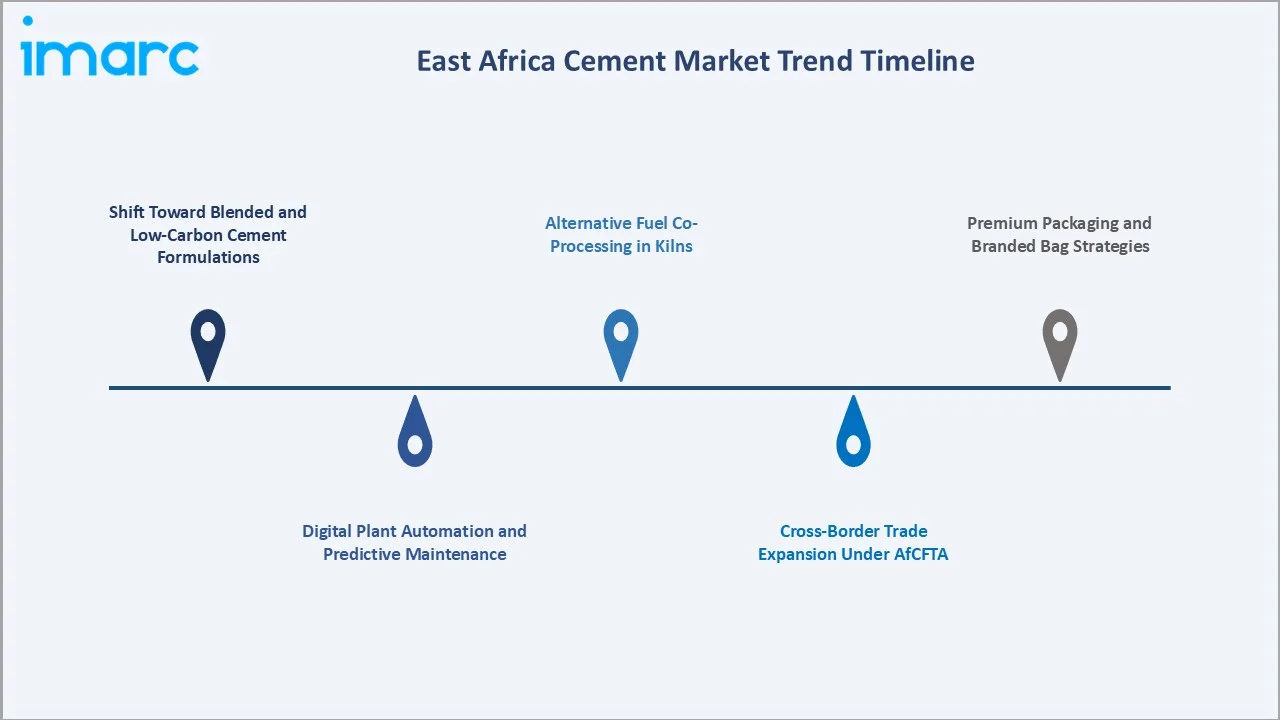

Emerging Market Trends

1. Shift Toward Blended and Low-Carbon Cement Formulations

Manufacturers across East Africa are increasingly adopting blended cement formulations using materials such as pozzolana and limestone to reduce clinker intensity, lower emissions, and improve cost efficiency.

2. Digital Plant Automation and Predictive Maintenance

Leading producers are gradually implementing kiln optimisation and predictive maintenance solutions to improve operational efficiency, reduce downtime, and stabilise production performance.

3. Cross-Border Trade Expansion Under AfCFTA

Intra-regional cement trade flows increased as AfCFTA implementation lowered tariffs. Kenyan and Tanzanian exporters now serve DRC border towns and South Sudan at competitive delivered prices, while Ugandan producers push into Rwanda and eastern DRC markets.

4. Alternative Fuel Co-Processing in Kilns

Co-processing of biomass and waste-derived fuels is gaining traction in cement plants across East Africa, with studies indicating thermal substitution potential in the range of 15–30% under favourable operating and policy conditions.

5. Premium Packaging and Branded Bag Strategies

Retail buyers showed rising willingness to pay for branded bags with tamper-proof seals, strength guarantees and moisture protection. Producers in Kenya, Uganda and Rwanda accelerated repackaging line investments to capture brand loyalty in the retail channel.

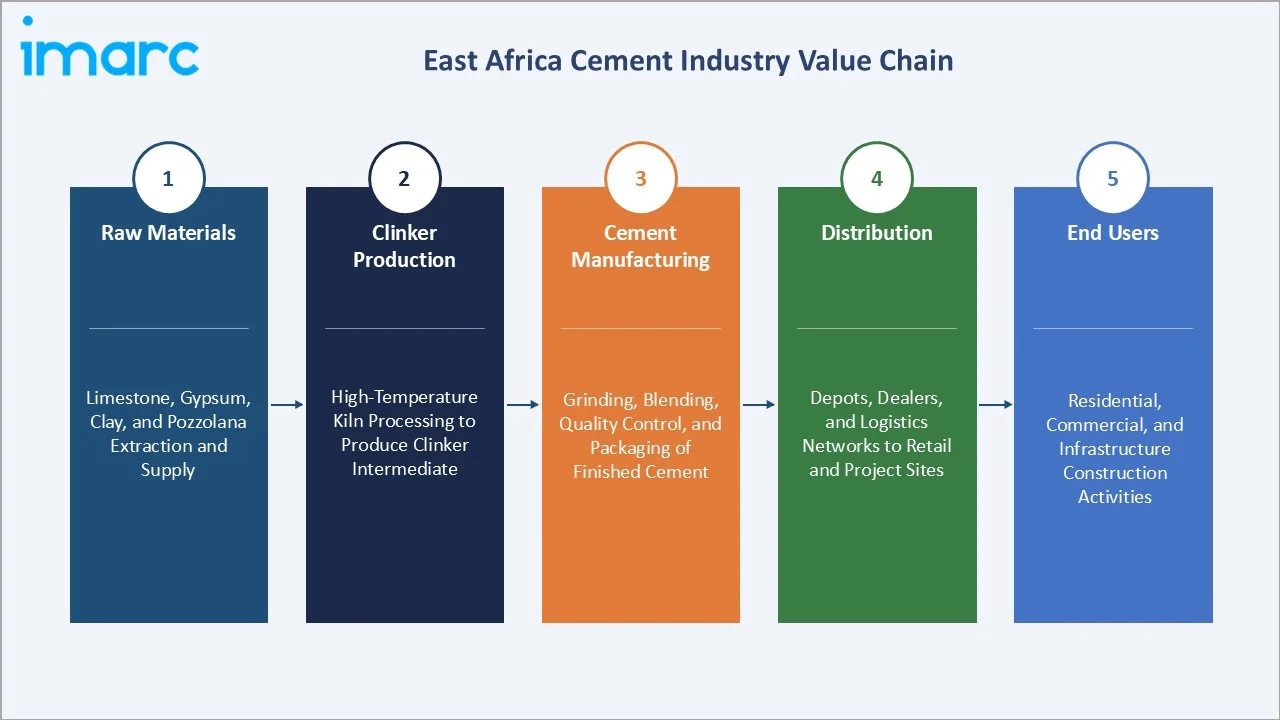

Industry Value Chain Analysis

The East Africa cement value chain spans five integrated stages from raw material extraction through end-consumer delivery. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Extraction and supply of core inputs such as limestone, gypsum, clay, and pozzolana are required for cement production. |

|

Clinker Production |

High-temperature processing of raw materials in kilns to produce clinker, the primary intermediate in cement manufacturing. |

|

Cement Manufacturing |

Grinding clinker with additives, followed by blending, quality control, and packaging into finished cement products. |

|

Distribution |

Movement of cement through depots, dealers, and logistics networks to reach retail and project sites across regions. |

|

End Users |

Final consumption of cement across residential, commercial, and infrastructure construction activities. |

Integrated producers occupy the highest strategic value position in the regional cement value chain, combining limestone quarry ownership, clinker manufacturing, grinding, and organised distribution into turnkey supply solutions. This vertical integration, however, is under competitive pressure from standalone grinding units that can procure imported clinker and serve niche regional markets with lower fixed-cost exposure.

Technology Landscape in the East Africa Cement Industry

Alternative Raw Materials and Green Cement

The industry is shifting toward low-clinker formulations. Calcined clay (LC3) and natural pozzolana substitution gained traction across East Africa through pilot projects and institutional research initiatives. In Kenya, the Institute of Cement & Concrete at Meru University of Science and Technology is advancing LC3, a blended cement type that can reduce CO₂ emissions by up to 40%.

Energy Efficiency and Waste Heat Recovery

Waste heat recovery systems are being adopted across cement plants to generate on-site power, with studies indicating the potential to meet a meaningful share of plant electricity demand while improving cost efficiency and energy resilience.

Automation and Robotics in Packaging

Automated palletising systems are increasingly being adopted in cement plants, improving loading efficiency, reducing manual handling, and enabling continuous, round-the-clock dispatch operations at major distribution hubs.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Portland | 68.4% | 2025 |

| Application | Residential | 51.3% | 2025 |

| Region | Kenya | 31.8% | 2025 |

By Type

Portland cement commands a 68.4% majority share in 2025, reflecting its position as the industry-standard binder across residential, commercial and basic infrastructure projects. The segment benefits from established supply chains, price consistency, and widely recognised quality certification across the EAC bloc.

To access detailed market analysis, Request Sample

Blended cement at 22.7% in 2025 is the faster-growing product type, driven by pozzolana and fly ash substitution of clinker, cost savings per tonne, and rising contractor acceptance for non-structural applications. Others (8.9%) include specialty binders such as oil-well cement, white cement and rapid-hardening variants, serving niche demand from finishing, decorative, and industrial use cases.

By Application

Residential construction dominates at 51.3% in 2025, benefitting from annual urban population growth, individual home builds, plotted developments, and government-backed affordable housing schemes across Kenya, Rwanda and Ethiopia. The segment enjoys demand stickiness due to demographic tailwinds and remittance-funded private builds.

Commercial applications at 28.6% in 2025 cover retail, office, hospitality, and mixed-use developments. Nairobi, Addis Ababa, and Kampala accounted for the bulk of commercial cement consumption. Infrastructure applications (20.1%) include roads, bridges, railways, dams and port facilities, with outlook strengthening through 2030 as multilateral-financed programmes progress.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

Kenya |

31.8% |

Affordable Housing Programme, road network upgrades, Nairobi commercial real estate hub |

|

Ethiopia |

24.6% |

Addis Ababa expansion, industrial parks, renewable energy projects, urbanisation |

|

Tanzania |

17.4% |

SGR extension, Dar es Salaam real estate growth, LNG projects, port expansion |

|

Uganda |

11.2% |

Oil pipeline works, Kampala housing, cross-border trade with DRC and South Sudan |

|

Sudan |

7.9% |

Post-conflict reconstruction, Nile irrigation infrastructure, housing recovery |

|

Rwanda |

4.3% |

Kigali master plan, tourism infrastructure, fastest-growth trajectory |

|

Others |

2.8% |

Burundi, South Sudan, Somalia - mainly import-driven cement demand |

Kenya commands a 31.8% regional revenue share in 2025, the most dominant country position in the East Africa cement market. Kenya combines the region's most diversified producer ecosystem across Mombasa, Athi River, and Emali, with the most ambitious affordable housing programme targeting 250,000 units annually. Ethiopia (24.6%) follows, anchored by Addis Ababa's expansion and industrial park construction.

Tanzania holds 17.4% in 2025, supported by SGR works, Dar es Salaam real estate, and LNG development. Uganda (11.2%) benefits from oil pipeline construction and cross-border demand. Sudan (7.9%) is entering reconstruction driven by Nile irrigation and housing recovery, while Rwanda (4.3%) shows the fastest growth pace through 2034 on Kigali master plan delivery.

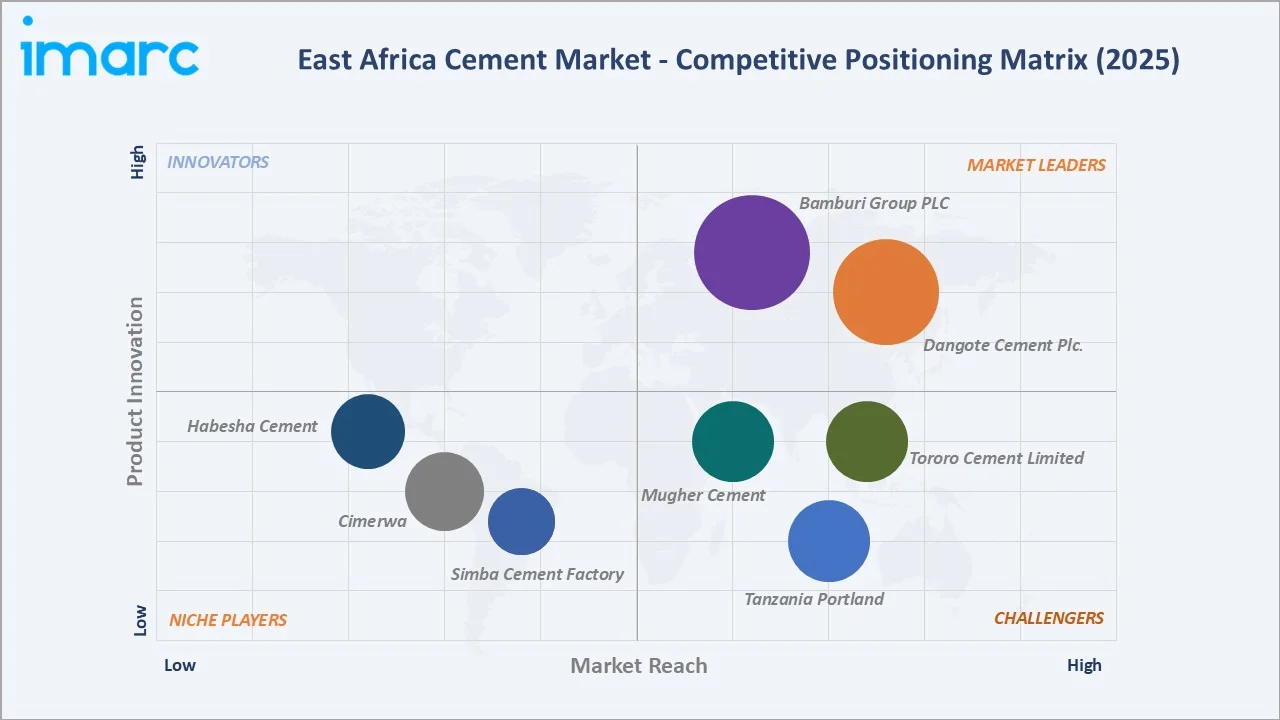

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Bamburi Group PLC |

Bamburi Power Plus, Tembo |

Leader |

Integrated Kenyan plants, retail brand recall, blended cement |

|

Dangote Cement Plc. |

Dangote 3X |

Leader |

Pan-African scale, cost leadership, Ethiopia & Tanzania plants |

|

Tororo Cement Limited |

Portland Cement |

Challenger |

Uganda leader, cross-border exports to DRC and South Sudan |

|

Tanzania Portland Cement Public Limited (Twiga) |

Twiga Plus |

Challenger |

Heidelberg Materials backing, Wazo Hill plant, dealer network |

|

Mugher Cement |

Mugher |

Challenger |

Ethiopian Portland leader, government-backed project supply |

|

Habesha Cement |

Portland Pozzolana Cement |

Emerging |

Ethiopia modern plant, Addis Ababa corridor brand play |

|

Simba Cement Factory LTD |

Simba Cement |

Emerging |

Kenya-Uganda cross-border operations, retail channel |

|

Cimerwa |

Surecem, Surebuild |

Emerging |

Rwanda domestic leader, PPC Group ownership |

The East Africa cement competitive landscape is characterised by a small number of regional integrated producers commanding substantial OEM and government relationships, alongside smaller domestic operators challenging the established hierarchy through retail branding and niche geographies. Market leaders differentiate through integrated clinker capacity, strong brand recall, wide distribution networks, and increasing investment in blended cement and alternative fuel infrastructure.

Key Company Profiles

Bamburi Group PLC

Bamburi Cement, majority-owned by Amsons Industries since 2024, is one of the oldest integrated cement producers in East Africa, operating plants in Mombasa and Nairobi.

- Product & Platform Portfolio: Bamburi Power Plus, Tembo, Nguvu, Supaset specialty, and Duracem blended variants.

- Recent Developments: In 2024, Bamburi Cement underwent a strategic transition following its acquisition by Tanzania-based Amsons Group for approximately USD 180 million, strengthening its regional positioning and enabling future capacity expansion and investment in East Africa.

- Strategic Focus: Bamburi's strategy centres on blended cement capacity expansion, alternative fuel and WHR adoption to cut thermal costs, and retail brand leverage through Power Plus and Tembo across Kenya and export markets.

Dangote Cement PLC.

Dangote Cement operates major East African plants in Mugher, Ethiopia, and Mtwara, Tanzania, with combined regional capacity above 5.0 million tonnes, part of a broader pan-African footprint.

- Product & Platform Portfolio: Dangote 3X branded Portland cement, blended pozzolana variants, bulk and bagged product lines.

- Recent Developments: Dangote Cement is advancing its pan-African expansion strategy through significant capacity investments, including a planned USD 400 million expansion of its Ethiopia plant to increase production and meet rising regional demand.

- Strategic Focus: Dangote prioritises cost leadership through scale, vertical integration from quarry to bag, aggressive retail pricing, and capital discipline to fund capacity expansion in volatile FX environments.

Tororo Cement Limited

Tororo Cement is Uganda's largest integrated producer, serving domestic demand and cross-border markets in Rwanda, DRC, and South Sudan from eastern Uganda limestone reserves.

- Product & Platform Portfolio: Tororo branded Portland cement, blended pozzolana cement, rapid-hardening specialty variants.

- Recent Developments: In 2025,

- Strategic Focus: Tororo combines vertical integration of limestone reserves, cost-competitive Portland production, and opportunistic expansion into landlocked neighbours where road-accessed Ugandan cement competes with coastal imports.

Market Concentration Analysis

The East Africa cement market exhibits moderate concentration among the top regional integrated producers, with Bamburi, Dangote, Tororo, Twiga and Mugher collectively accounting for approximately 62-66% of regional installed capacity in 2025 and a slightly larger share of revenue.

The market is experiencing a bifurcated dynamic. Among integrated producers, consolidation is gradually occurring: modern kiln lines, alternative fuel systems, and digital plant control require capital commitments only the largest producers can sustain, limiting mid-sized competitors to niche geographies or blending operations.

Country-level fragmentation persists. Ethiopia hosts 10+ domestic producers of meaningful scale, creating local pricing pressure. Kenya and Uganda display a higher concentration, with the top three players holding above 70% of local capacity in 2025. Consolidation is expected to continue through 2030, driven by capacity rationalisation and ESG-led capex differentiation.

Investment & Growth Opportunities

Fastest-Growing Segments

Blended cement is the highest-growth product sub-segment at approximately 2.1% CAGR through 2034, supported by pozzolana and limestone-filler formulation scaling. Rwanda is the fastest-growing country at approximately 2.4% CAGR, driven by Kigali master plan delivery and low-base growth dynamics.

Emerging Market Expansion

Alternative fuel co-processing and waste heat recovery are the emerging capex sub-markets, transitioning from flagship pilots to mainstream adoption. Green cement capacity expansion represents the highest-potential allocation opportunity, offering both cost savings and ESG-linked financing access.

Venture & Private Investment Trends

Notable regional transactions include Amsons Industries' acquisition of Bamburi stake in 2024, Heidelberg Materials investments in Tanzania, and PPC Group's activity in Rwanda. Private infrastructure funds increasingly co-invest with DFIs on alternative fuel retrofits and blended cement capacity additions.

Future Market Outlook (2026-2034)

The East Africa cement market forecast projects steady value expansion from USD 2.70 Billion in 2025 to USD 3.02 Billion by 2034 at a CAGR of 1.20%, supported by urban housing demand, infrastructure delivery, and the gradual shift toward blended cement.

Two technology discontinuities are most likely to reshape the market through 2034. Blended cement scaling is expected to reshape industry cost structures and carbon intensity, while increased adoption of alternative fuel co-processing will help reduce thermal cost exposure and support alignment with sustainability and ESG requirements for early adopters.

By 2034, the East Africa cement industry is forecast to have transitioned from a pure Portland commodity market to a differentiated product portfolio economy. Competitive dynamics will feature regional integrated leaders (Bamburi, Dangote, Tororo), country-champion producers (Mugher, Twiga, Cimerwa), and emerging blended-cement specialists targeting ESG-linked procurement channels.

Research Methodology

Primary Research

Primary research encompassed over 40 structured interviews conducted in 2024-2025 with East African cement stakeholders including plant managers at integrated producers, distributor principals, government housing agency officials, contractors, and DFI programme leads. Primary insights validated market sizing, segmentation, capacity utilisation, pricing, and competitive positioning.

Secondary Research

Secondary sources include Kenya National Bureau of Statistics, Central Bank of Kenya, Ethiopia CSA industrial data, Tanzania Cement Association reports, Uganda Bureau of Statistics, AfDB infrastructure publications, World Bank project documents, cement producer annual reports, EAC trade statistics, and regional chambers of commerce.

Forecasting Models

Market size estimations were derived using a combination of top-down and bottom-up models, incorporating GDP growth, urbanisation, housing starts, public capex, and historical evolution patterns. Scenario analysis (base, optimistic, conservative) was performed to account for macroeconomic uncertainty and policy shifts.

East Africa Cement Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Portland, Blended, Others |

| Applications Covered | Residential, Commercial, Infrastructure |

| Countries Covered | Ethiopia, Kenya, Tanzania, Uganda, Sudan, Rwanda, Others |

| Companies Covered | Bamburi Group PLC, Dangote Cement Plc., Tororo Cement Limited, Tanzania Portland Cement Public Limited (Twiga), Mugher Cement, Habesha Cement, Simba Cement Factory LTD, Cimerwa, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the East Africa cement market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the East Africa cement market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the East Africa cement industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the East Africa Cement Market Report

The East Africa cement market was valued at USD 2.70 Billion in 2025, driven by residential housing demand, government infrastructure spending, and cross-border trade activity across Kenya, Ethiopia and Tanzania.

The market is projected to reach USD 3.02 Billion by 2034, growing at a CAGR of 1.20% during 2026-2034, driven by urban housing demand, affordable housing programmes, and blended cement adoption.

Portland cement leads with a 68.4% share in 2025, driven by universal applicability across residential, commercial and infrastructure projects, broad contractor acceptance, and established supply chain maturity.

Residential construction leads with a 51.3% share in 2025, driven by 4.2% annual urban population growth, affordable housing programmes, and remittance-funded home construction across the six-country bloc.

Kenya leads with a 31.8% share in 2025, driven by the Affordable Housing Programme, Nairobi commercial real estate growth, road network upgrades, and a diversified domestic cement producer base.

Key drivers include urbanisation (4.2% annual growth), infrastructure programmes (USD 18B budgets 2024-2025), AfCFTA-led cross-border trade integration, mortgage finance expansion, and affordable housing programme delivery.

Rwanda is the fastest-growing country at approximately 2.4% CAGR through 2034, driven by Kigali urban master plan delivery, tourism-led construction, and favourable low-base growth dynamics.

Leading companies include Bamburi Group PLC, Dangote Cement Plc., Tororo Cement Limited, Tanzania Portland Cement Public Limited (Twiga), Mugher Cement, Habesha Cement, Simba Cement Factory LTD, and Cimerwa across the six-country East African market.

Blended cement grew from 18.4% share in 2021 to 22.7% in 2025, cutting production cost by 12-18% and specific CO2 emissions by 18-22% per tonne, attracting ESG-linked procurement demand.

AfCFTA lowered cross-border cement tariffs from 2024, enabling Kenyan and Tanzanian producers to serve DRC, South Sudan and Burundi competitively, with intra-regional trade growing approximately 9% in 2025.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)