Electric Two-Wheeler Market Size, Share, Trends and Forecast by Vehicle Type, Battery Type, Voltage Type, Peak Power, Battery Technology, Motor Placement, and Region, 2026-2034

Global Electric Two-Wheeler Market Size, Share, Trends & Forecast (2026-2034)

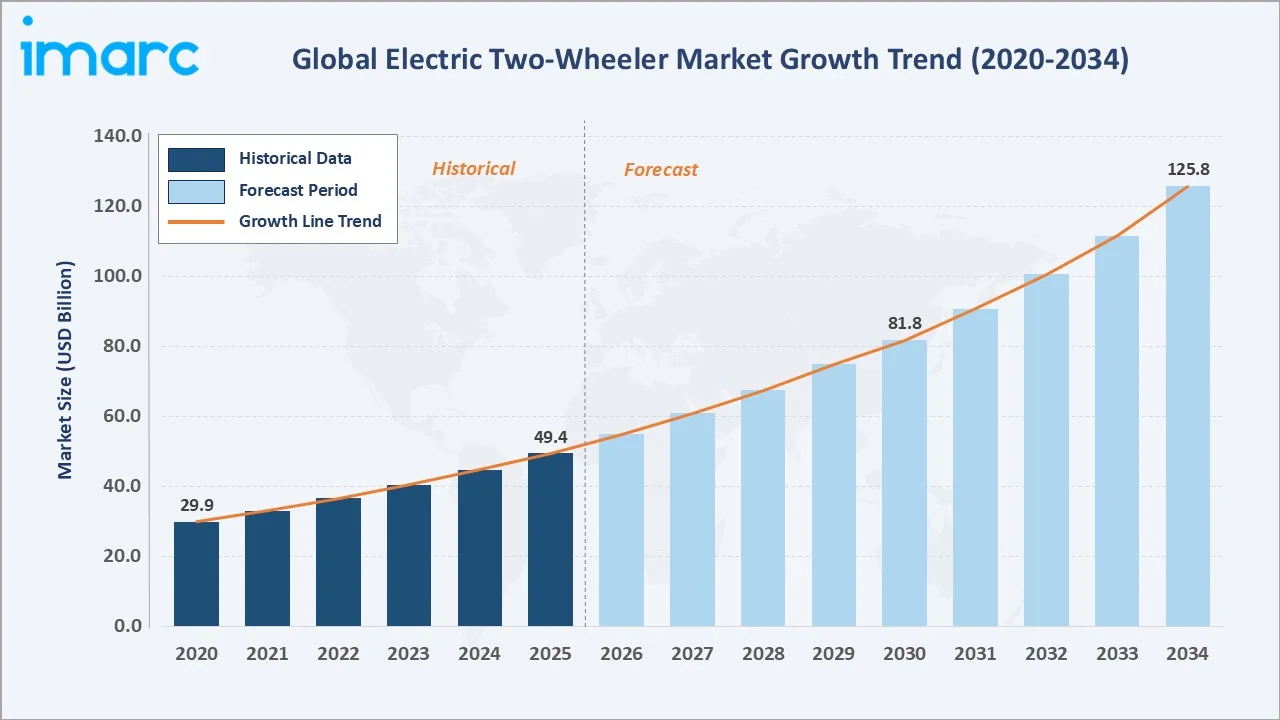

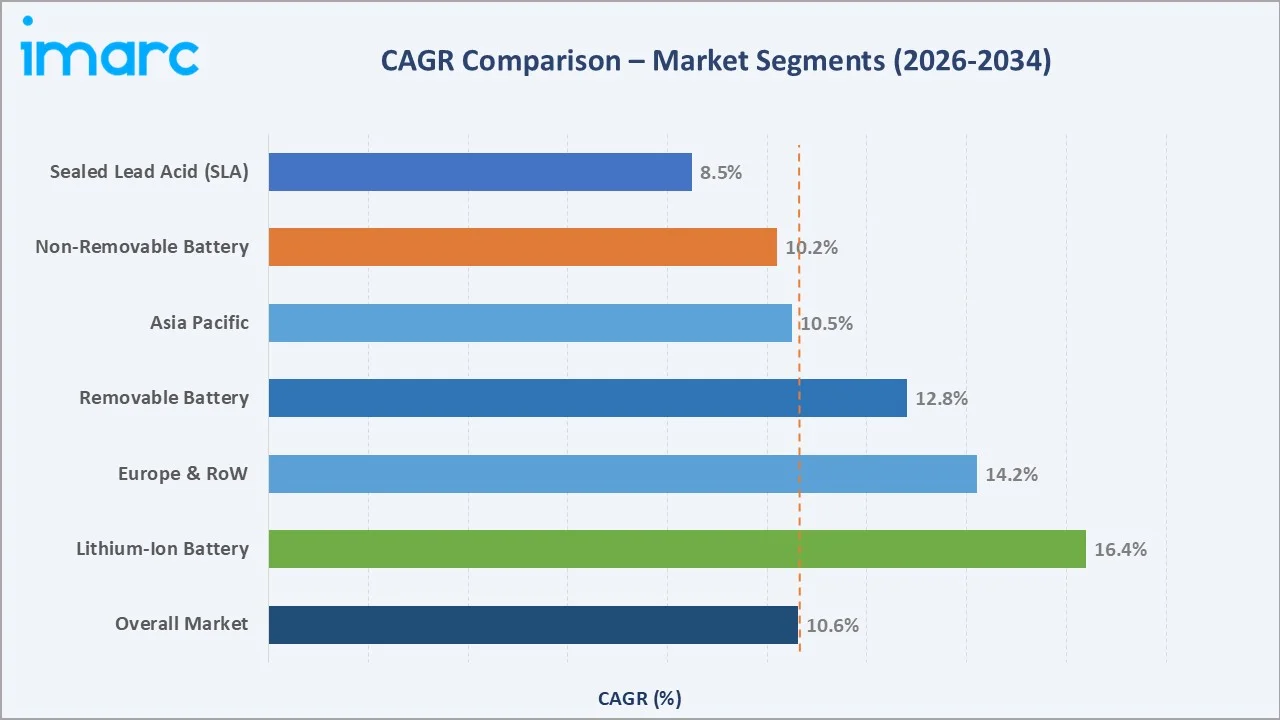

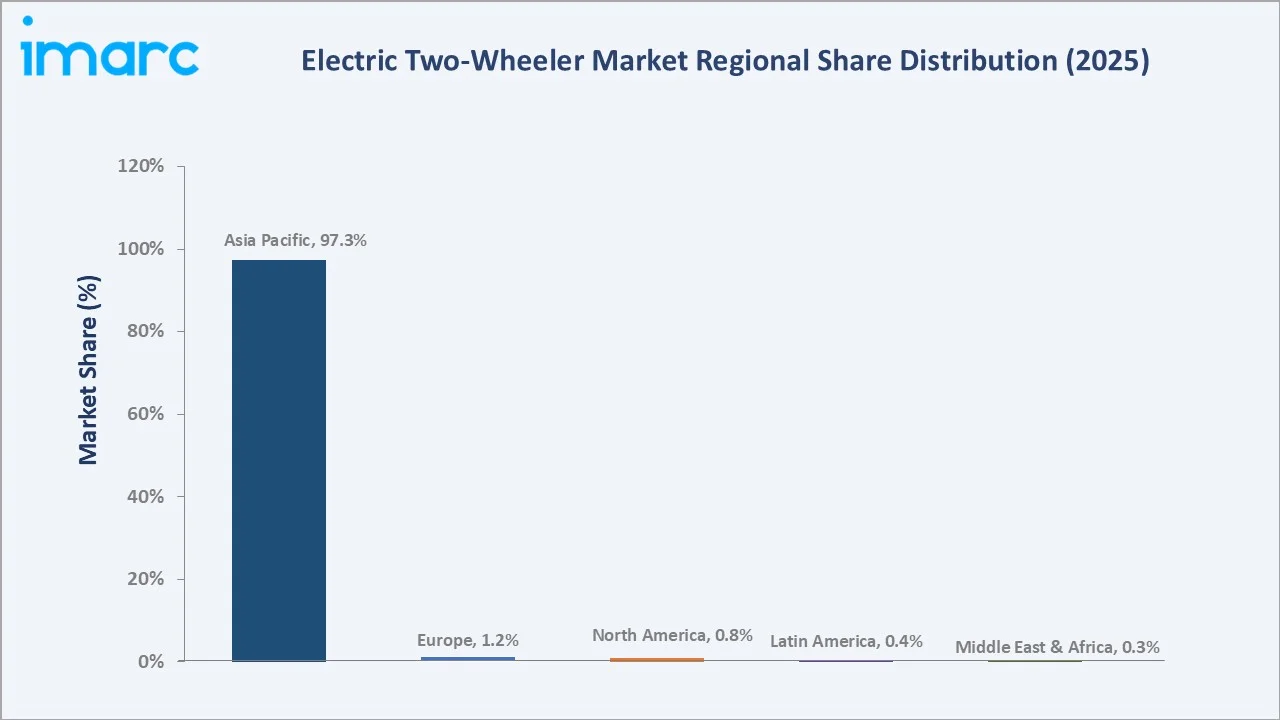

The global electric two-wheeler market was valued at USD 49.42 Billion in 2025 and is projected to reach USD 125.76 Billion by 2034, expanding at a CAGR of 10.61% during 2026-2034. The market’s consistent growth is propelled by rising environmental awareness, rapid urbanization, supportive government incentive frameworks, and growing demand for cost-efficient personal mobility solutions. Asia Pacific remains the dominant region, accounting for approximately 97.3% of global revenue in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 49.42 Billion |

|

Forecast Market Size (2034) |

USD 125.76 Billion |

|

CAGR (2026-2034) |

10.61% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (97.3% share, 2025) |

|

Fastest Growing Region |

Europe & North America |

To get more information on this market, Request Sample

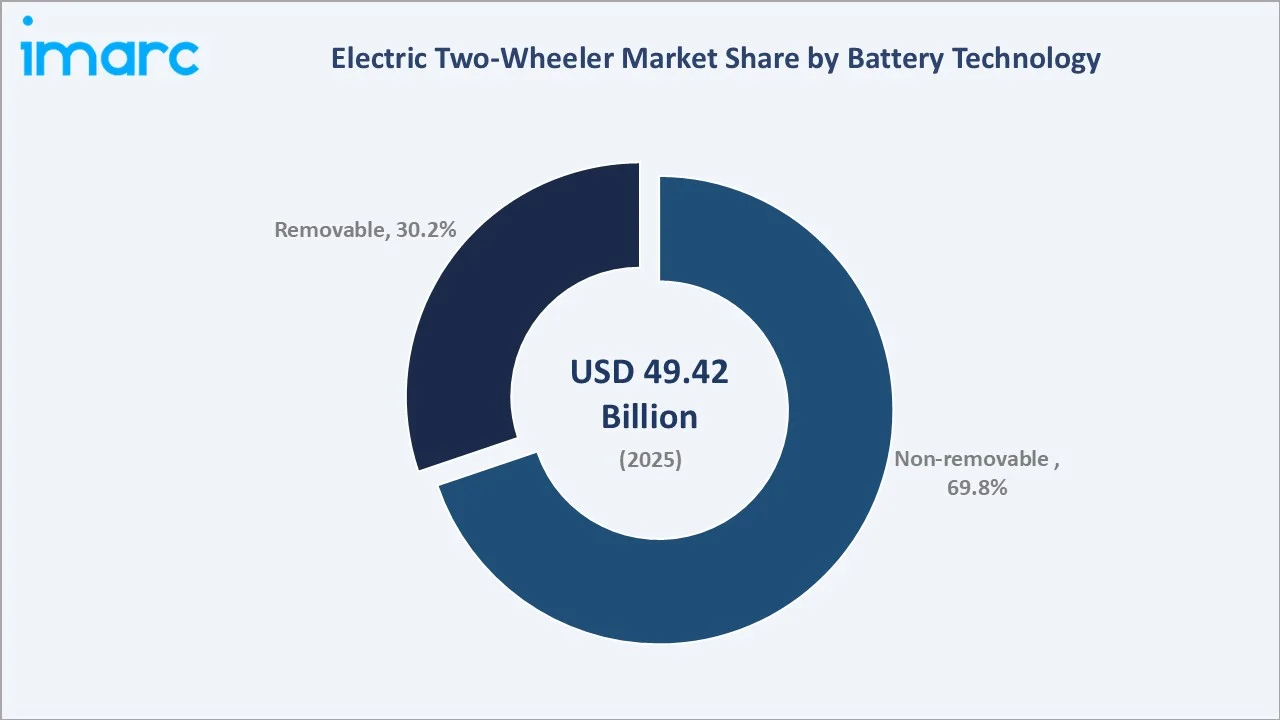

Among battery technologies, the non-removable battery segment leads with the highest revenue share of 69.8%, while the lithium-ion battery type segment exhibits the fastest growth trajectory. Major industry participants include Yadea Group Holdings Ltd., Ola Electric Mobility Ltd., TVS Motor Company, Honda Motor Co., Ltd., Ather Energy Limited, etc.

Executive Summary

The global electric two-wheeler market continues to demonstrate robust expansion, underpinned by shifting environmental priorities, rapid urbanization, and the growing prominence of EV-first mobility policies across major economies. Valued at USD 49.42 Billion in 2025, the market is forecasted to exceed USD 125.76 Billion by 2034, at a steady CAGR of 10.61%.

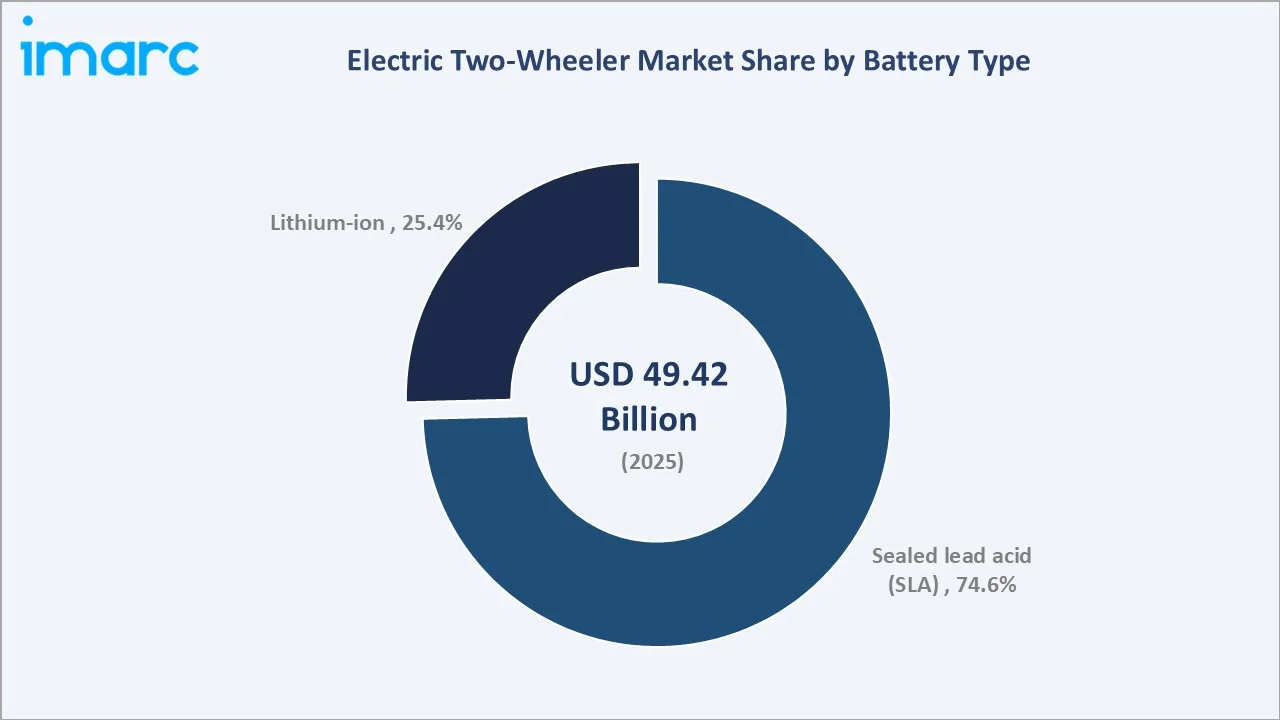

Among the key growth drivers, the increasing inclination toward eco-friendly transportation — particularly among millennial and Gen-Z demographics — remains a primary catalyst. The non-removable battery segment alone represented 69.8% of the global market in 2025, reflecting strong manufacturer preference for integrated, chassis-optimized battery configurations. Sealed lead acid (SLA) continues to dominate the battery type segment with a 74.6% share, primarily due to its cost advantage in price-sensitive markets across Asia Pacific, though lithium-ion variants are rapidly gaining share at an estimated CAGR of 16.4% through 2034.

Asia Pacific retains its market leadership with a 97.3% share (2025), anchored by China and India as the two largest national markets. Europe and North America emerge as the fastest-growing regions in relative terms, registering higher CAGRs driven by tightening emission norms, premium product launches, and evolving urban micro-mobility regulations. Leading market players are investing in battery innovation, direct-to-consumer distribution infrastructure, AI-powered connectivity features, and sustainable manufacturing — all key areas reshaping the competitive landscape through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Battery Technology) |

Non-Removable Battery – 69.8% share (2025) |

|

Largest Segment (Battery Type) |

Sealed Lead Acid (SLA) – 74.6% share (2025) |

|

Leading Region |

Asia Pacific – 97.3% revenue share (2025) |

|

Fastest Growing Segment |

Lithium-Ion Battery – CAGR ~16.4% (2026-2034) |

|

Top Companies |

Yadea, Ola Electric Mobility Ltd., TVS Motor, Honda, Ather Energy |

|

Market Opportunity |

Battery swapping & Li-ion segment projected to reach USD 35B+ by 2034 |

Key Analytical Observations Supporting The Above Data:

- Non-removable battery technology dominates with a 69.8% share (2025), driven by simplified vehicle design, optimized chassis integration, superior range-to-weight ratios, and lower per-unit manufacturing costs for mass-market OEMs.

- Sealed lead acid (SLA) batteries account for 74.6% of market share (2025), favored by cost-conscious consumers and manufacturers in developing economies where battery affordability is the primary purchase driver.

- Asia Pacific generates 97.3% of global revenues (2025), bolstered by China’s mature EV ecosystem and India’s policy-driven electrification wave spanning both urban and semi-urban geographies.

- The lithium-ion battery segment is the fastest growing at a CAGR of approximately 16.4% (2026-2034), supported by declining cell costs, improving energy density, and growing OEM preference for lightweight, high-performance configurations.

- The battery swapping and fleet electrification opportunity is projected to exceed USD 35 Billion by 2034, underpinned by commercial logistics platforms and ride-hailing operators seeking to reduce fuel and maintenance expenditure.

Global Electric Two-Wheeler Market Overview

The electric two-wheeler (e2W) industry is one of the fastest-growing segments within the global mobility ecosystem, with its large-scale adoption originating in China through early government-led electrification initiatives. Today, it spans scooters, motorcycles, mopeds, and e-bikes across developed and emerging markets, supported by a comprehensive value chain including battery suppliers, OEMs, and charging infrastructure providers.

Driven by low operating costs, urban suitability, and rising demand for sustainable mobility, e2Ws have gained strong traction in high-density markets such as China, India, and Southeast Asia, with increasing adoption in Europe and North America. Growth is further accelerated by commercial applications, including last-mile delivery and shared mobility.

Favorable macroeconomic factors—such as urbanization, fuel price volatility, and stringent emission regulations—continue to support expansion. As a result, electric two-wheelers are expected to play a critical role in global vehicle electrification, particularly in urban transport systems.

Market Dynamics

To evaluate market opportunities, Request Sample

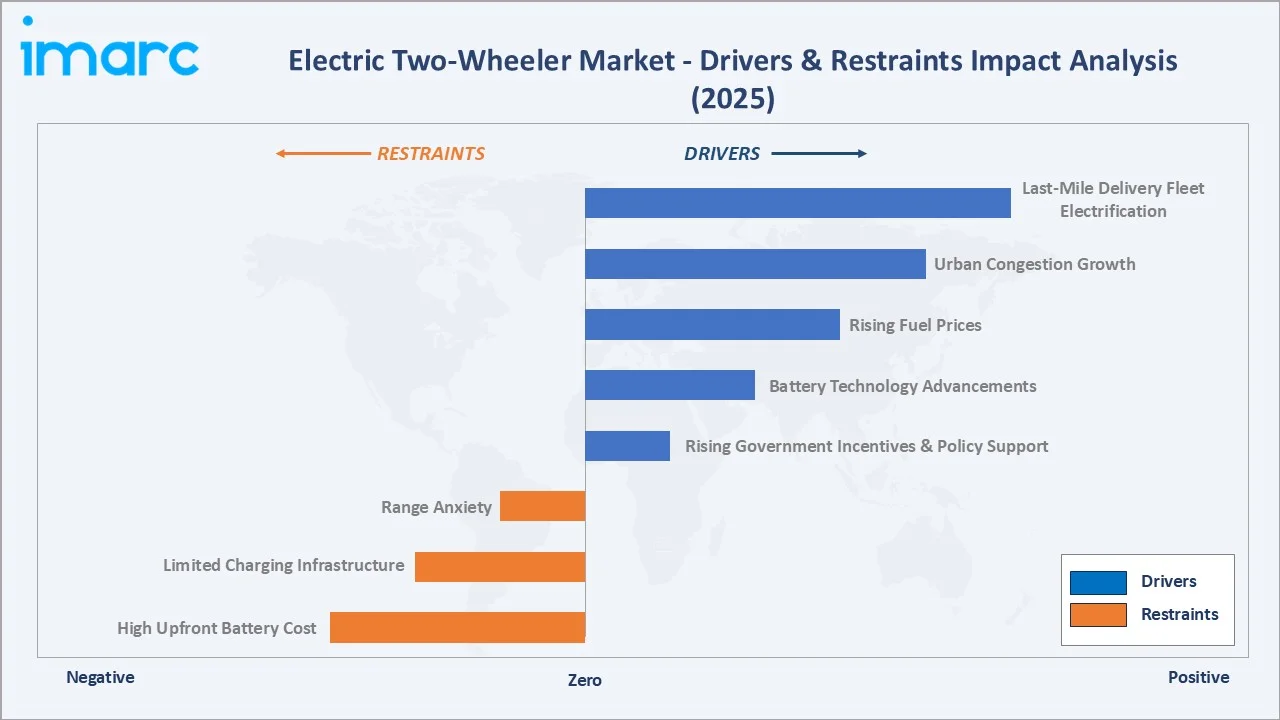

Market Drivers

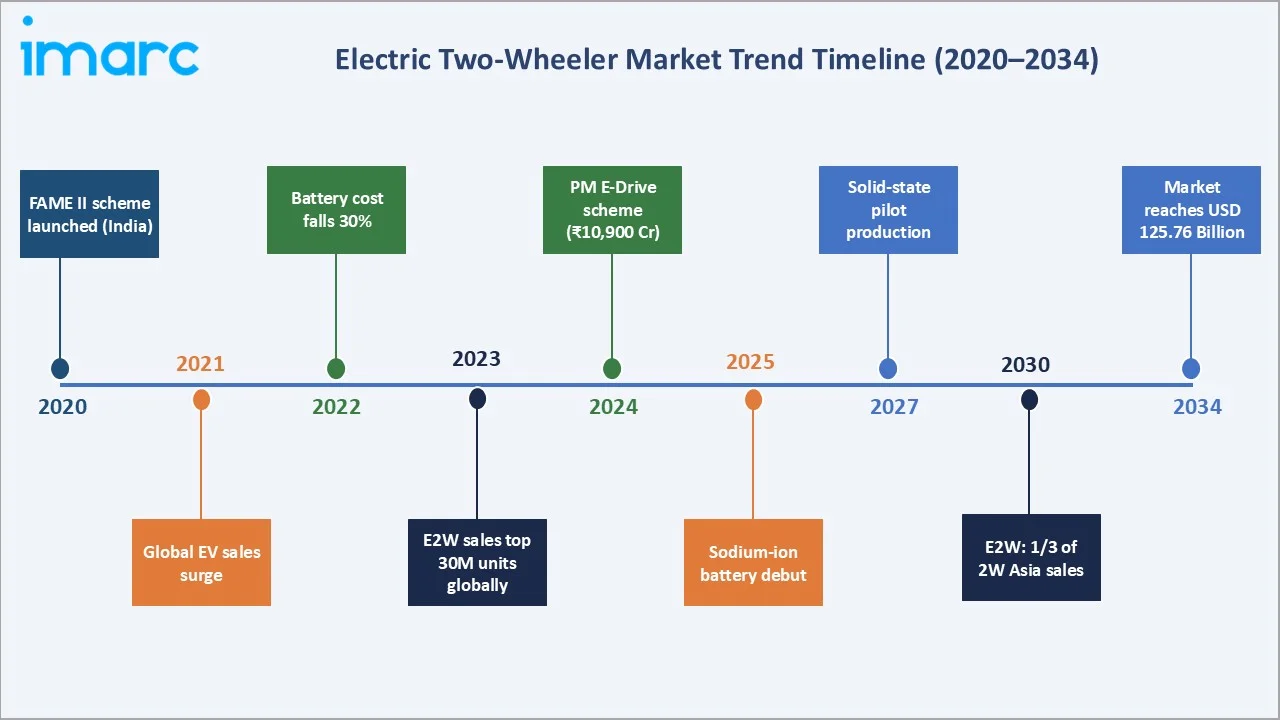

- Rising Government Incentives & Policy Support: Subsidies, tax benefits, and reduced GST are lowering the total cost of ownership. India’s PM E-Drive (2024) and state EV policies (e.g., Delhi EV Policy 2.0) are accelerating adoption.

- Battery Technology Advancements: Improvements in lithium-ion efficiency and emerging sodium-ion/solid-state technologies are increasing range, reducing charging time, and enhancing reliability.

- Rising Fuel Prices: Higher petrol prices are strengthening the cost advantage of e2Ws, which offer ~60–80% lower running costs than ICE vehicles.

- Urban Congestion Growth: Increasing traffic costs (~1% of GDP in urban economies) are driving demand for compact, efficient mobility solutions like e2Ws.

Market Restraints

- High Upfront Battery Cost: Batteries account for ~35–45% of vehicle cost, limiting affordability in price-sensitive markets.

- Limited Charging Infrastructure: Inadequate charging networks beyond major cities constrain adoption in emerging markets.

- Range Anxiety: Concerns over limited range (especially beyond ~100 km) remain a key barrier for semi-urban and long-distance users.

Market Opportunities

- Last-Mile Delivery Fleet Electrification: Rapid e-commerce growth is driving fleet adoption, creating a multi-billion-dollar opportunity by 2034.

- Battery Swapping Infrastructure: Standardized battery swapping networks — pioneered by Gogoro in Taiwan and being scaled across India — offer a compelling solution to charging time and range anxiety, opening a high-margin recurring revenue model for OEMs and energy providers.

- Premium Segment Expansion: Growing disposable incomes in tier-1 Asian cities and rising EV adoption in Europe and North America are driving demand for premium electric motorcycles and high-performance e-scooters with advanced connectivity features.

Market Challenges

- Charging Standardization Gaps: The absence of universal charging standards across markets complicates consumer adoption and OEM product planning, requiring manufacturers to develop multi-standard chargers that add cost and design complexity.

- Commodity Price Volatility: Fluctuating prices of lithium, cobalt, nickel, and copper — key battery and motor components — create cost uncertainty for manufacturers and can delay technology transitions from SLA to lithium-ion configurations.

- Regulatory Complexity: Evolving EV safety standards, battery certification requirements, and vehicle classification rules across different national markets demand significant R&D and compliance investment from manufacturers seeking international scalability.

Emerging Market Trends

1. Transition from SLA to Lithium-Ion and Next-Generation Battery Technologies

The shift from sealed lead-acid (SLA) to lithium-ion batteries is the most critical structural change in the e2W market, driven by higher energy density, longer lifespan, and improved cost efficiency. OEMs are increasingly standardizing lithium-ion across product portfolios, while early-stage commercialization of alternatives such as sodium-ion batteries—demonstrated by Yadea Group Holdings Ltd.—signals a gradual transition toward next-generation chemistries.

2. Government Policy as the Primary Market Accelerant

Government policy remains the primary catalyst for market expansion. National and state-level programs—such as India’s PM E-Drive scheme and Delhi EV Policy 2.0—are improving affordability and accessibility. Globally, regulatory measures, including emission targets, urban mobility reforms, and EV infrastructure investments, are creating a supportive ecosystem for sustained adoption.

3. AI Integration and Smart Connectivity

AI and digital connectivity are becoming core differentiators in electric two-wheelers. OEMs are integrating intelligent dashboards, AI assistants, and cloud-based diagnostics to enhance user experience and vehicle performance. Advanced battery management systems and predictive maintenance capabilities are improving reliability while reducing lifecycle costs, particularly for fleet operators.

4. Commercial Fleet and Last-Mile Delivery Electrification

The rapid expansion of e-commerce and on-demand delivery services is accelerating the adoption of electric two-wheelers in commercial fleets. Their lower operating and maintenance costs, combined with suitability for high-frequency urban usage, make them an efficient solution for last-mile logistics and shared mobility applications.

5. Battery Swapping Ecosystem Expansion

Battery swapping is emerging as a viable alternative to conventional charging, particularly in dense urban environments. Network-led models pioneered by Gogoro Inc. and expanding across Asia are enabling faster turnaround times and improving vehicle utilization, while also creating recurring service-based revenue opportunities.

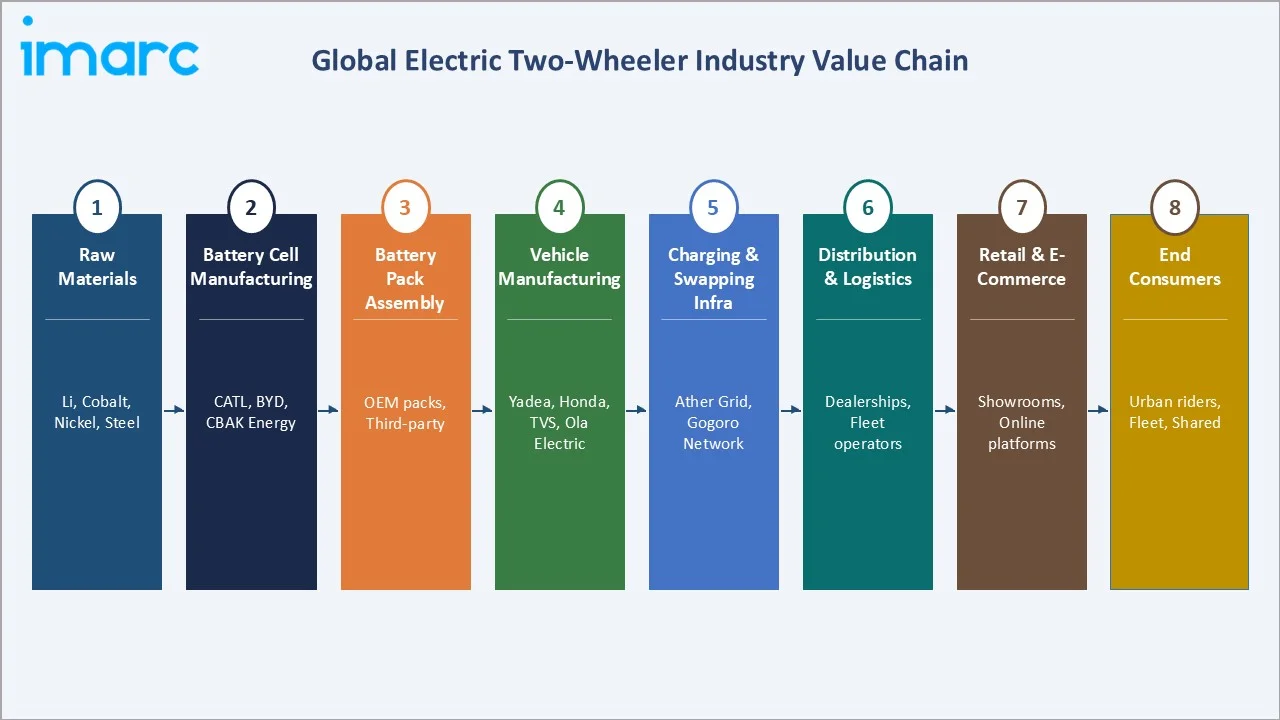

Industry Value Chain Analysis

The electric two-wheeler value chain spans multiple interconnected stages, from raw material procurement to end consumer ownership and aftermarket support. Each stage is populated by specialized operators whose performance directly influences product quality, cost competitiveness, and market responsiveness.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Lithium, cobalt, nickel, steel, copper, and rare-earth materials from global mining operators |

|

Battery Cell Manufacturing |

CATL, BYD, Panasonic, CBAK Energy, Samsung SDI (cylindrical & prismatic cells) |

|

Battery Pack Assembly |

OEM in-house packs (Ola Electric Mobility Ltd., Ather Energy), third-party pack integrators |

|

Vehicle Manufacturing |

Yadea, Jiangsu Xinri, Honda Motor, TVS Motor Company, Bajaj Auto, Hero MotoCorp Ltd. |

|

Distribution & Logistics |

Authorized dealerships, fleet operators, and government procurement agencies |

|

Retail & E-Commerce |

Brand showrooms, online platforms (Amazon, Flipkart), EV-specific marketplaces |

|

Charging & Swapping Infrastructure |

Ather Grid, BPCL EV stations, state networks, Gogoro swapping network |

|

End Consumers |

Urban commuters, delivery fleet operators, shared mobility platforms, and recreational riders. |

Technology Landscape in the Electric Two-Wheeler Industry

Battery Technology Innovation

Battery innovation is the core technological driver in the e2W market. The shift from sealed lead-acid to lithium-ion has significantly improved range, efficiency, and lifespan. Emerging chemistries—such as solid-state, silicon-anode, and sodium-ion—are advancing charging speed, safety, and cost efficiency, with early commercialization initiatives (e.g., by Yadea Group Holdings Ltd.) signaling future scalability.

Smart Connectivity and OTA Updates

Connected technologies are becoming standard across electric two-wheelers. Features such as real-time diagnostics, GPS, remote monitoring, and over-the-air (OTA) updates enhance user experience and enable continuous performance upgrades. Platforms like Ather Energy Pvt. Ltd.’s connected ecosystem highlight the shift toward software-defined vehicles.

Motor and Drivetrain Efficiency

Hub motors dominate due to simplicity and low maintenance, while mid-drive motors are expanding in premium segments for better performance. Brushless DC (BLDC) motors are now industry standard, improving efficiency, durability, and overall cost of ownership.

Charging and Battery Swapping Technology

Advancements in fast-charging and portable charging solutions are reducing downtime and improving convenience. Battery swapping models—pioneered by Gogoro Inc.—are gaining traction, offering instant energy replacement and supporting high-utilization use cases.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Vehicle Type |

Electric Scooter/Moped |

86.4% |

2025 |

|

Battery Type |

Sealed Lead Acid (SLA) |

74.6% |

2025 |

|

Voltage Type |

48-60V |

60.4% |

2025 |

|

Peak Power |

🔒 |

🔒 |

2025 |

| Battery Technology | Non-removable | 69.8% | 2025 |

| Motor Placement | 🔒 | 🔒 | 2025 |

|

Region |

Asia-Pacific |

97.3% |

2025 |

By Battery Technology

The non-removable battery segment dominates the electric two-wheeler market with a 69.8% share (2025), driven by its structural advantages, including simplified vehicle design, optimized chassis integration, and lower per-unit manufacturing costs that make it particularly compelling for price-sensitive mass-market segments across the Asia Pacific.

To access detailed market analysis, Request Sample

Non-removable battery technology’s dominance is reinforced by the large number of mass-market models across China and India that use sealed, chassis-integrated packs optimized for volume production. Despite growing interest in battery-swapping networks in select urban markets, non-removable systems are expected to maintain their majority position through 2034, given significant installed base advantages and OEM product roadmap commitments.

By Battery Type

Sealed lead acid (SLA) batteries hold the leading share within the battery type segment, accounting for 74.6% of the global electric two-wheeler market in 2025. SLA batteries remain the preferred choice for entry-level electric two-wheelers, particularly in markets where affordability is the primary purchase driver, given that their established manufacturing base results in substantially lower per-unit costs compared to lithium-ion alternatives.

However, the lithium-ion segment is projected to be the fastest-growing battery type at approximately 16.4% CAGR through 2034, as declining cell costs narrow the price gap with SLA and growing consumer demand for better range and lighter vehicles drives OEM transitions. Premium-segment manufacturers across India, Taiwan, and Europe have already shifted entirely to lithium-ion configurations, and this trend is expected to gradually permeate mid-market and entry-level models over the forecast period.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

Regulatory Impact |

Major Companies |

|

Asia Pacific |

97.3% |

Urban congestion, govt subsidies, two-wheeler culture, rising fuel costs |

FAME II, PM E-Drive scheme, low-emission zones in Vietnam |

Yadea, Ola Electric Mobility Ltd., Honda, TVS, Ather Energy |

|

Europe |

1.2% |

Emission regulations, cycling culture, and urban micro-mobility growth |

EU emission standards, city-level EV incentive schemes |

Honda, Gogoro, KTM, Piaggio |

|

North America |

0.8% |

EV charging infrastructure expansion, delivery fleet electrification |

Federal EV grants, state purchase rebates |

Zero Motorcycles, Harley-Davidson LiveWire, Rad Power |

|

Latin America |

0.4% |

Rising fuel prices, urban population growth, and affordability |

Nascent national EV policies, import duty reductions |

Regional distributors, Chinese OEM imports |

|

Middle East & Africa |

0.3% |

Fleet electrification, fuel cost savings, and urbanization |

Kenya VAT exemption on e2Ws; GCC clean transport plans |

Local assemblers, Chinese and Indian OEM exports |

Asia Pacific’s market leadership (97.3% share, 2025) is deeply entrenched through China’s world-leading electric two-wheeler manufacturing ecosystem, India’s rapidly expanding EV adoption driven by FAME II and PM E-Drive incentives, and Southeast Asia’s accelerating low-emission zone implementation in major urban centers.

Europe, North America, and emerging markets are the clear growth engines in relative terms. Europe’s tight emission regulations and urban cycling culture are supporting steady e2W adoption, while North America’s USD 521 million EV charging infrastructure grant (August 2024) is laying the foundation for broader consumer market development. In Africa, Kenya’s electric two-wheeler sales are increasing following the government’s VAT exemption policy and motorcycle taxi fleet electrification initiatives, signalling meaningful emerging-market momentum.

Competitive Landscape

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Yadea Group Holdings Ltd. |

Yadea |

Market Leader |

Largest global e2W manufacturer; vertically integrated battery supply |

|

Ola Electric Mobility Ltd. |

Ola Electric |

Market Leader |

Direct-to-consumer model; in-house battery tech; 800+ stores in India |

|

TVS Motor Company |

TVS iQube |

Emerging |

Broad dealer network; strong ICE-to-EV transition pipeline |

|

Honda Motor Co. Ltd. |

EM1 e/ Honda Activa e |

Niche Specialist |

Global brand equity; 400B yen EV investment plan (2026–2030) |

|

Ather Energy Limited |

Ather 450 Series |

Innovation Leader |

AI-enabled OTA updates; Ather Grid fast-charging network |

|

Bajaj Auto Ltd. |

Chetak Electric |

Emerging |

Heritage brand; pan-India dealership; EV export ambitions |

|

Hero MotoCorp Ltd. |

VIDA |

Niche Specialist |

Affordable mass-market positioning; nationwide service network |

|

Gogoro |

Gogoro CrossOver |

Challenger |

Battery-swapping ecosystem leadership; APAC urban mobility focus |

The global electric two-wheeler market exhibits a moderately consolidated competitive structure. The top five players — Yadea, Ola Electric Mobility Ltd., Honda, TVS Motor, and Ather Energy — collectively account for approximately 41% of global market revenues in 2025. The remainder is distributed among dozens of regional manufacturers, emerging start-ups, and private-label brands operating across fragmented national markets.

Key Company Profiles

Yadea Group Holdings Ltd.

Yadea is the electric two-wheeler manufacturer by volume, with a dominant position in the Chinese and Southeast Asian markets. The company’s vertically integrated supply chain — encompassing battery cell sourcing, pack assembly, and vehicle manufacturing — provides high cost and quality control advantages over competitors.

- Product Portfolio: Electric scooters, e-bikes, and electric motorcycles across entry, mid, and premium segments across 100+ countries.

- Recent Developments: In January 2025, Yadea Group Holdings Ltd. unveiled sodium-ion battery-powered electric two-wheelers in Hangzhou, marking a key step toward the commercialization of lithium-free battery technology with improved cost efficiency and charging performance.

- Strategic Focus: International market expansion, premium product development, and proprietary battery technology innovation.

Ather Energy Limited

Ather Energy is India’s premium electric scooter manufacturer, known for its connected vehicle platform, over-the-air (OTA) update capability, and proprietary Ather Grid fast-charging network spanning over 1,000 points across India.

- Product Portfolio: Ather 450S, 450X, and Rizta electric scooters; focused exclusively on the premium smart scooter segment.

- Recent Developments: In January 2025, CBAK Energy Technology, Inc. partnered with Ather Energy Pvt. Ltd. to supply Model 32140 cylindrical lithium-ion battery cells, with integration planned into Ather’s electric two-wheelers—strengthening its advanced battery sourcing strategy.

- Strategic Focus: Premium market positioning, charging infrastructure leadership, and AI-powered ownership experience via the Ather Connect platform.

Honda Motor Co., Ltd.

Honda is the two-wheeler manufacturer overall, accelerating its electric transition with a commitment to invest 400 billion yen (approximately USD 2.6 billion) in electrification from 2026 to 2030, leveraging its global brand equity and distribution network.

- Product Portfolio: Honda EM1 e: (Europe), Activa E (India, planned), multiple electric concept models targeting 2025–2026 commercial releases.

- Recent Developments: In November 2024, launched the EV Fun Concept and EV Urban Concept at EICMA 2024 in Milan, signaling premium EV ambitions in the European market.

- Strategic Focus: Global EV platform standardization, battery technology investment, and competitive entry pricing in high-volume Asian markets.

Market Concentration Analysis

The global electric two-wheeler market exhibits moderate concentration at the top end, with the leading five players holding approximately 41% of total revenues in 2025. However, the presence of hundreds of regional manufacturers globally — particularly in China, India, and Southeast Asia — ensures a highly fragmented competitive long tail, with no single player achieving dominant pricing power across all segments and geographies.

The mass-market consumer scooter segment is notably more fragmented than the premium electric motorcycle segment. In the mass-market scooter category in China, the top three brands command approximately 54% of domestic market value, demonstrating higher concentration in the world’s largest national market compared to international geographies where market development is at earlier stages.

Consolidation activity has been gaining momentum since 2022. The market is expected to see 6–10 significant partnership, investment, and M&A transactions annually through 2034, as incumbent OEMs seek to acquire EV-native technology capabilities and battery-swapping infrastructure operators, while EV start-ups pursue strategic alliances with established global brands to accelerate international market entry.

Investment & Growth Opportunities

Fastest Growing Segments

Lithium-ion–based models, battery swapping infrastructure, and commercial fleet electrification are emerging as the highest-growth segments in the electric two-wheeler market. These areas are attracting strong investment due to their ability to address core adoption barriers—cost efficiency, charging convenience, and high-utilization use cases—making them key strategic entry points for both OEMs and investors.

Emerging Market Expansion

Southeast Asia and Africa represent the most attractive near- to mid-term growth markets, driven by urbanization, policy support, and rising fuel costs. Countries such as Vietnam and Kenya are witnessing accelerated adoption, supported by regulatory initiatives and expanding commercial use cases. Market entry strategies are increasingly focused on local partnerships, dealership network expansion, and participation in government-led fleet electrification programs.

Venture Investment Trends

Venture capital and private equity investment in the electric two-wheeler ecosystem accelerated significantly in 2024, driven by strong interest in battery innovation, AI-enabled connectivity, charging infrastructure, and fleet electrification platforms. Investors are prioritizing next-generation technologies such as sodium-ion and solid-state batteries, along with AI-driven predictive maintenance solutions and scalable battery-swapping networks. ESG-focused funds are increasingly backing electric two-wheeler fleet operators as direct decarbonization plays, particularly in urban logistics. At the same time, institutional private equity continues to pursue multi-market expansion strategies, including franchise roll-ups and cross-border EV brand scaling across high-growth regions such as Southeast Asia, Africa, and the GCC.

Future Market Outlook (2026-2034)

The global electric two-wheeler market is poised for sustained, broad-based growth through 2034, anchored by technology-driven cost reduction, deepening policy support, and geographic expansion into high-growth emerging markets. From a base of USD 49.42 Billion in 2025, the market is forecast to reach USD 125.76 Billion by 2034, representing absolute incremental value addition of USD 76.34 Billion over the nine-year forecast horizon at a steady CAGR of 10.61%.

Technological disruptions—spanning solid-state batteries, AI-driven battery management, advanced safety systems, and high-power charging—are set to reshape cost structures and performance benchmarks across the electric two-wheeler value chain. Manufacturers that achieve meaningful cost efficiencies through battery innovation and automation will gain a clear advantage in mass-market segments over the next decade. At the same time, consumer expectations are rapidly evolving, with connectivity, range, safety, and sustainability shifting from premium features to baseline requirements. OEMs that fail to integrate these capabilities across core product portfolios risk losing market share to EV-native competitors, driving large-scale technology adoption across global markets.

Research Methodology

Primary Research

Primary research for this report included structured interviews and surveys conducted with industry participants comprising electric two-wheeler OEM executives, battery technology specialists, government policy analysts, dealership operators, fleet managers, and end consumers across Asia Pacific, Europe, and North America. Research spanned key geographies including China, India, Vietnam, Germany, the United Kingdom, and the United States.

Secondary Research

Secondary research encompassed a comprehensive review of company annual reports, regulatory filings, trade publications (Economic Times, Autocar Professional, EV Magazine), industry databases (IEA Global EV Outlook 2025, ICCT, Mintel), and publicly available financial data. Government policy documents, EV registration data, and battery technology patent filings were also systematically reviewed and triangulated across over 300 secondary sources.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanization indices, battery cost learning curves, EV policy timelines, and historical market evolution patterns. Scenario analysis across base, optimistic, and conservative cases was performed to account for macroeconomic and policy uncertainty over the 2026–2034 forecast horizon.

Electric Two-wheeler Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Vehicle Types Covered | Electric Scooter/Moped, Electric Motorcycle |

| Battery Types Covered | Lithium-Ion, Sealed Lead Acid (SLA) |

| Voltage Types Covered | <48V, 48-60V, 61-72V, 73-96V, >96V |

| Peak Powers Covered | <3 kW, 3-6 kW, 7-10 kW, >10 kW |

| Battery Technologies Covered | Removable, Non-removable |

| Motor Placements Covered | Hub Type, Chassis Mounted |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Netherlands, Norway, China, Japan, India, South Korea, Australia, Brazil, Mexico,Turkey, Saudi Arabia, Egypt |

| Companies Covered | Yadea Group Holdings Ltd., Ola Electric Mobility Ltd., TVS Motor Company, Honda Motor Co., Ltd., Ather Energy Limited, Bajaj Auto Ltd., Hero MotoCorp Ltd., Gogoro, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the electric two-wheeler market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global electric two-wheeler market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyse the level of competition within the electric two-wheeler industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Electric Two-Wheeler Market Report

The global electric two-wheeler market was valued at USD 49.42 Billion in 2025 and is projected to reach USD 125.76 Billion by 2034, growing at a CAGR of 10.61%.

The electric two-wheeler market is expected to grow at a CAGR of 10.61% during the forecast period from 2026-2034, reflecting strong demand momentum across consumer, commercial, and fleet segments globally.

Asia Pacific is the dominant region, accounting for approximately 97.3% of global electric two-wheeler market revenues in 2025, driven by China and India’s large urban populations, established manufacturing ecosystems, and comprehensive government EV incentive frameworks.

Europe and North America are the fastest-growing regions in relative terms, driven by tightening emission regulations, premium product launches, expanding charging infrastructure, and growing commercial fleet electrification initiatives in major urban centers.

Key drivers include increasing environmental awareness, supportive government incentive programs, rapid advancements in battery technology, rising fuel prices, growing urban congestion, and expanding charging infrastructure networks that collectively lower adoption barriers and accelerate the global shift toward cleaner, cost-effective personal mobility.

Non-removable battery technology is the largest segment, holding a 69.8% market share in 2025, supported by advantages in manufacturing cost efficiency, chassis integration, and energy-to-weight optimization for mass-market electric scooters and motorcycles.

Lithium-ion battery adoption (CAGR ~16.4%), battery swapping network expansion, AI-powered vehicle connectivity, commercial fleet electrification, and sodium-ion battery commercialization are the fastest-growing trends projected through 2034.

The leading companies include Yadea Group Holdings Ltd., Ola Electric Mobility Ltd., TVS Motor Company, Honda Motor Co., Ltd., Ather Energy Limited, Bajaj Auto Ltd., Hero MotoCorp Ltd., and Gogoro.

Sealed lead acid (SLA) batteries dominate the battery type segment with a 74.6% share in 2025, driven by their cost advantages in price-sensitive developing markets. However, lithium-ion is projected to be the fastest-growing type at approximately 16.4% CAGR through 2034.

Government policies — including purchase subsidies, tax credits, EV charging infrastructure grants, GST reductions, and low-emission zone regulations — represent the single most impactful driver of electric two-wheeler adoption globally. India’s PM E-Drive scheme, the U.S. EV charging infrastructure grant, and Vietnam’s planned emission-zone restrictions are recent examples of policies directly catalyzing market expansion.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)