Electric Vehicle Charging Station Market Size, Share, Trends and Forecast by Charging Station Type, Vehicle Type, Installation Type, Charging Level, Connector Type, Application, and Region, 2026-2034

Electric Vehicle Charging Station Market Size, Share, Trends & Forecast (2026-2034)

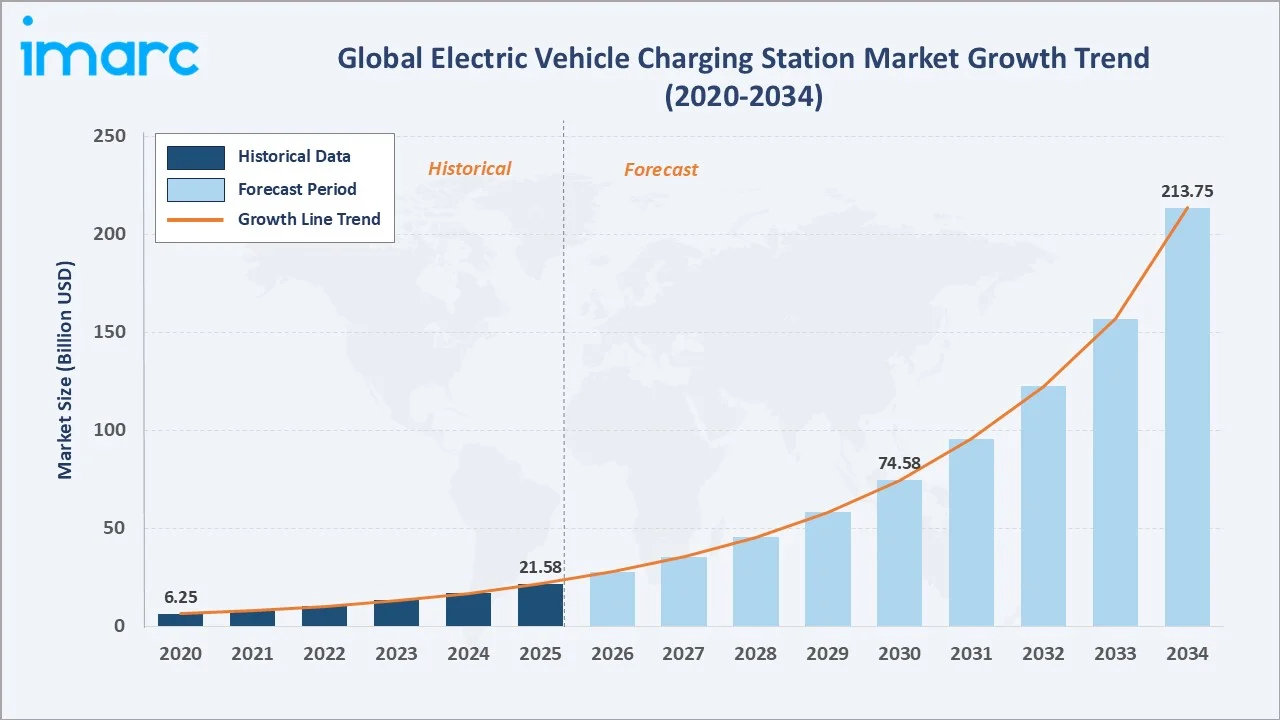

The global electric vehicle (EV) charging station market reached USD 21.58 Billion in 2025 and is projected to reach USD 213.75 Billion by 2034, growing at a CAGR of 28.15% during 2026-2034. The accelerating global adoption of battery electric vehicles (BEVs), sweeping government mandates to phase out internal combustion engines, and massive public and private investment in charging infrastructure are the primary forces driving extraordinary market expansion throughout the forecast period.

Market Snapshot

|

Metric |

Value |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Market Size (2025) |

USD 21.58 Billion |

|

Market Size (2034) |

USD 213.75 Billion |

|

CAGR (2026-2034) |

28.15% |

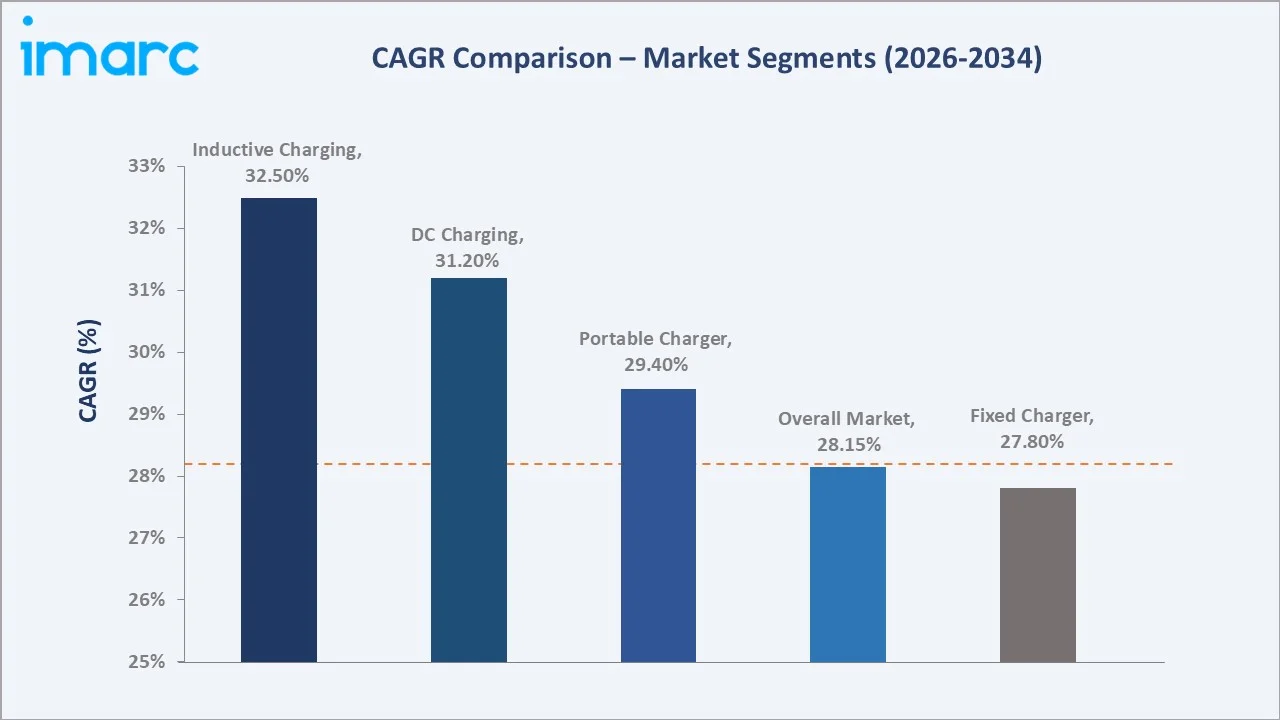

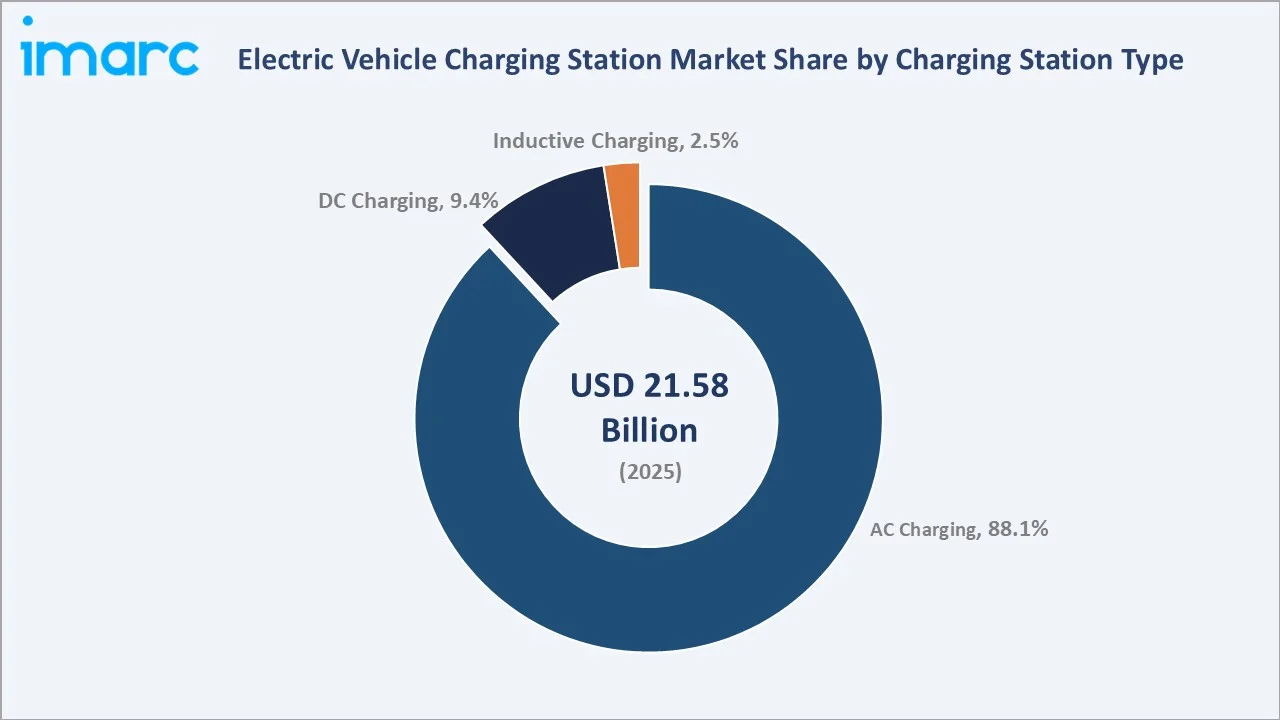

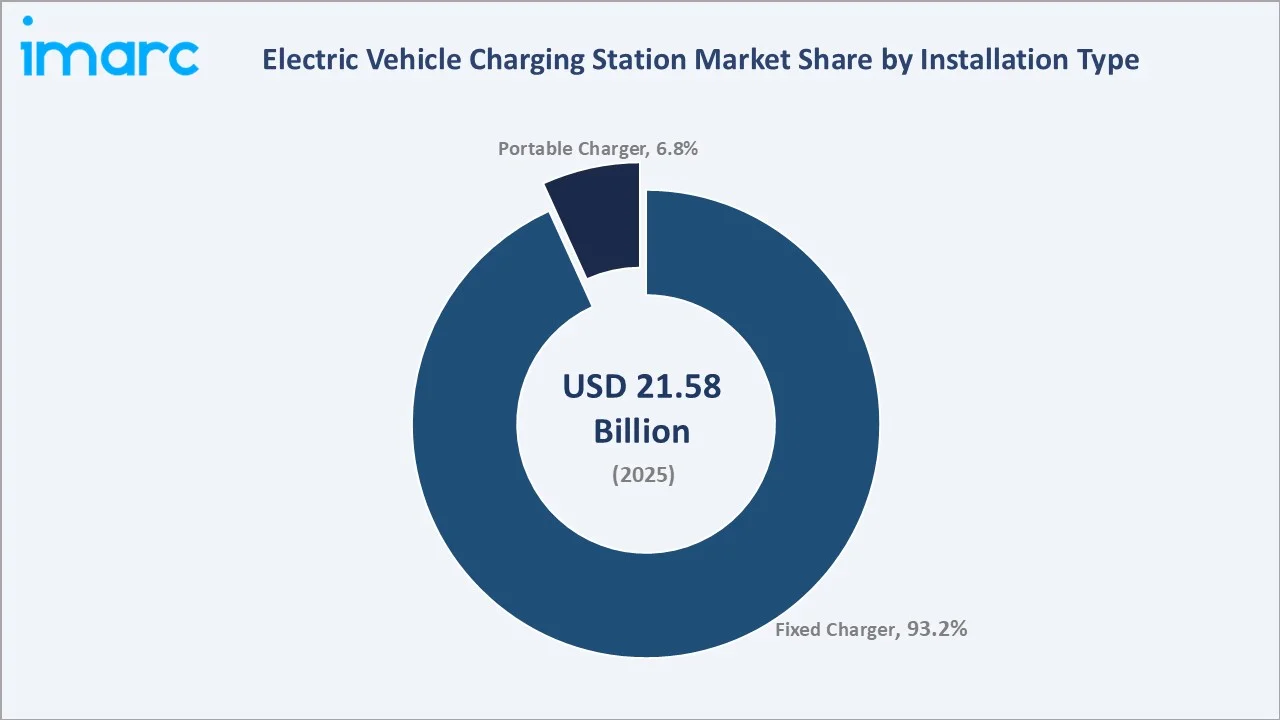

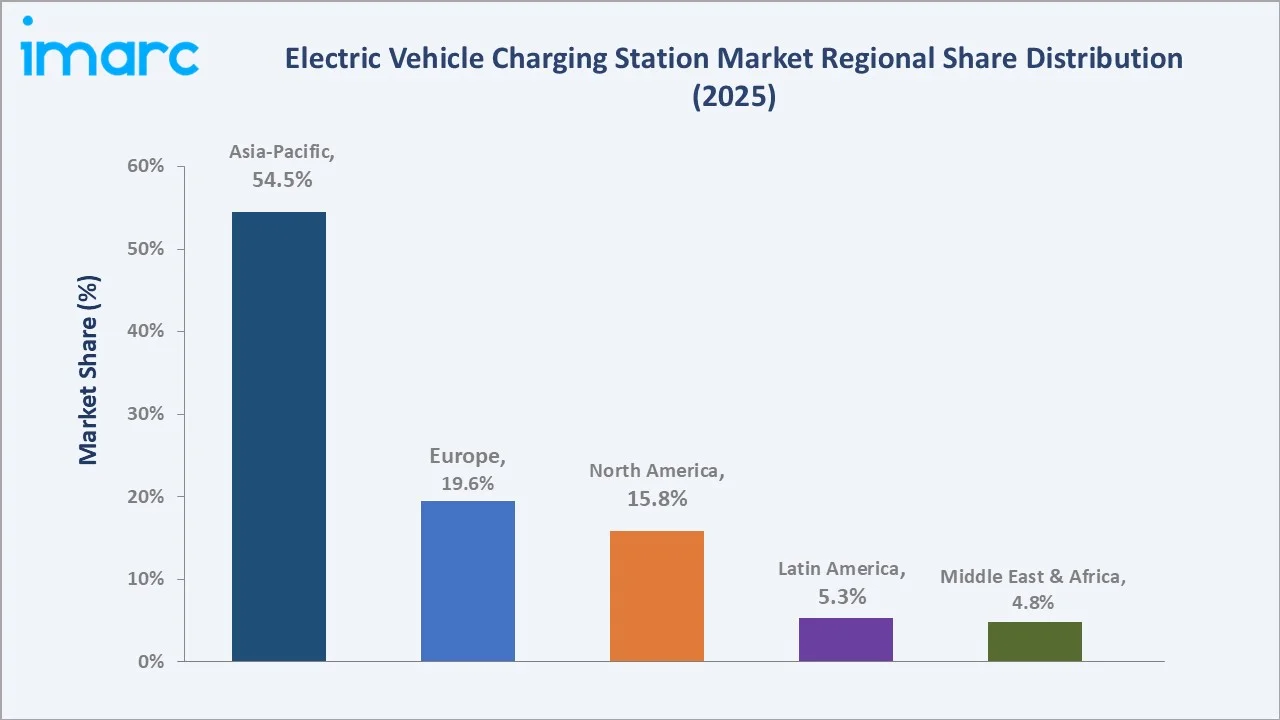

Asia-Pacific leads regionally with a 54.5% market share in 2025, anchored by China’s world-leading EV adoption rate and the addition of 1.3 million public charging points within the country in 2025. AC charging dominates the station type segment at 88.1%, driven by the ubiquity of Level 1 and Level 2 home and workplace chargers, while Fixed charger leads installation type at 93.2%. Inductive charging is the fastest-growing station type at ~32.5% CAGR, as automotive OEMs integrate wireless charging capability into premium EV platforms.

To get more information on this market, Request Sample

The market grew from USD 6.25 Billion in 2020 to USD 21.58 Billion in 2025, driven by COVID-19-accelerated EV adoption as urban consumers sought private transport alternatives, the deployment of national charging infrastructure programs across China, the US, EU member states, and Japan, and the rapid maturation of DC fast charging technology enabling practical long-distance EV travel. The market is forecast to reach USD 213.75 Billion by 2034, driven by the global EV transition’s structural inevitability and the massive infrastructure investment required to support growing global EV fleet sizes.

Executive Summary

The global EV charging station market is experiencing transformational expansion, representing one of the fastest-growing infrastructure investment markets globally. The market stood at USD 21.58 Billion in 2025 and is forecast to reach USD 213.75 Billion by 2034 at a 28.15% CAGR, underpinned by 65 countries linked to gas-powered car phaseout pathways, zero-emission vehicle targets, electric vehicle adoption goals, or international zero-emission vehicle commitments.

AC charging dominates with an 88.1% share in 2025, reflecting the dominance of Level 1 (3–7 kW) and Level 2 (7–22 kW) chargers in home, workplace, retail, and public parking charging scenarios. Fixed charger leads installation type at 93.2%, reflecting the fundamental economics of charging infrastructure, high utilization fixed installations offer the most favorable return on investment for charging point operators (CPOs) and property owners.

Asia-Pacific commands 54.5% of the global market, driven by China’s state-directed EV adoption and infrastructure investment, Japan’s mature EV culture, South Korea’s aggressive hydrogen and battery EV programs, and India’s rapidly growing two-wheel and four-wheel EV market. Europe at 19.6% reflects the EU’s 2035 ICE vehicle ban and the deployment of the pan-European AFIR (Alternative Fuels Infrastructure Regulation) fast-charging network.

Key Market Insights

|

Insight |

Data |

|

Largest Charging Station Type |

AC Charging – 88.1% share (2025) |

|

Fastest Growing Charging Station Type |

Inductive Charging – ~32.5% CAGR (2026-2034) |

|

Largest Installation Type |

Fixed Charger – 93.2% share (2025) |

|

Fastest Growing Installation Type |

Portable Charger – ~29.4% CAGR (2026-2034) |

|

Leading Region |

Asia-Pacific – 54.5% share (2025) |

|

Key Players |

Tesla, ChargePoint, Inc., ABB, Schneider Electric |

Key Analytical Observations Supporting The Above Data:

- AC charging at 88.1% (2025) reflects the fundamental charging behavior of EV owners: AC charging through Level 1 and Level 2 chargers is expected to handle 80% of U.S. EV charging needs by 2030, mainly at homes, multifamily buildings, workplaces, and public destinations.

- Fixed charger at 93.2% (2025) dominates because the business model of charging point operators (CPOs) is fundamentally built around fixed location assets that generate revenue through per-kWh energy delivery fees, subscription memberships, and commercial real estate partnerships.

- Inductive charging at ~32.5% CAGR is the fastest-growing technology, driven by BMW, Mercedes-Benz, Genesis, and Toyota integrating inductive charging pads into premium EV platforms, enabling hands-free charging at home parking pads without cable handling.

- Asia-Pacific’s 54.5% (2025) market share reflects China’s structural dominance: Preliminary data for April 2026 indicates that electric car sales in China reached a monthly record, accounting for more than 60% of total car sales, and operates the world’s largest public charging network.

Electric Vehicle Charging Station Market Overview

The global electric vehicle charging station market encompasses hardware (charging unit, cables, connectors, enclosures), software (charging management systems, OCPP-based network platforms, payment systems, energy management), and services (installation, maintenance, CPO operations, roaming) for Level 1, Level 2, Level 3/DC Fast Charging, and inductive (wireless) charging systems serving battery electric vehicles (BEVs), plug-in hybrid electric vehicles (PHEVs), and hybrid electric vehicles (HEVs) across residential, commercial, fleet, and public infrastructure applications.

The EV charging station value chain is characterized by the convergence of energy infrastructure, automotive technology, real estate, and digital services. The rapid commoditization of Level 2 AC charging hardware is driving consolidation in the hardware manufacturing layer, while the software and network management layer is emerging as the primary source of long-term competitive differentiation and recurring revenue for charging network operators.

Market Dynamics

To evaluate market opportunities, Request Sample

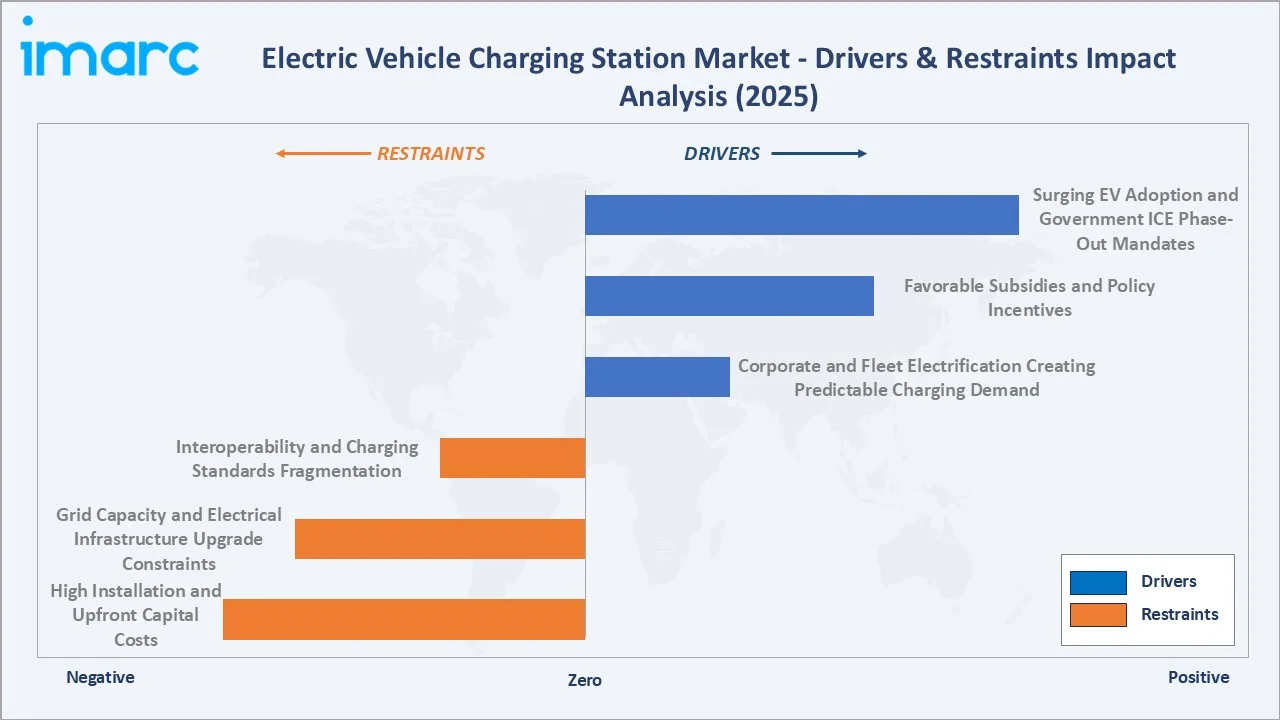

Market Drivers

- Surging EV Adoption and Government ICE Phase-Out Mandates: In 2025, global electric car sales increased by 20%, surpassing 20 million units. Additionally, global electric car sales are projected to increase again in 2026, reaching 23 million units and accounting for nearly 30% of total car sales worldwide, according to the latest edition of the IEA’s annual Global EV Outlook.

- Favorable Subsidies and Policy Incentives: Favorable subsidies and policy incentives are supporting EV charging adoption in India, with schemes such as PM E-DRIVE and state-level programs offering financial support for charging infrastructure. Delhi, for instance, offers up to 100% subsidy capped at INR 6,000 per charging point for homes and apartments, helping reduce installation costs and improve charger accessibility.

- Corporate and Fleet Electrification Creating Predictable Charging Demand: Amazon’s commitment to 100,000 Rivian electric delivery vehicles and equivalent fleet electrification, and municipal bus fleet electrification programs across China, Europe, and North America are creating large, predictable charging infrastructure demand that is more fundable and contractually secure than public retail charging, enabling depot charging infrastructure at scale.

Market Restraints

- High Installation and Upfront Capital Costs: DC fast charging stations require USD 50,000–150,000 per unit capital investment, including hardware, electrical infrastructure upgrades, civil works, and permitting. These high upfront costs require access to patient capital, government subsidies, or utility cost-sharing arrangements to achieve acceptable investment returns within a 5–7 year payback target.

- Grid Capacity and Electrical Infrastructure Upgrade Constraints: The deployment of DC fast charging at scale requires significant grid infrastructure upgrades, including local distribution transformer capacity expansion, medium-voltage cable installation, and, in some cases, transmission-level reinforcement.

- Interoperability and Charging Standards Fragmentation: The co-existence of multiple charging standards across global markets creates consumer confusion, limits cross-network charging compatibility, and increases CPO hardware inventory complexity.

Market Opportunities

- Vehicle-to-Grid (V2G) and Bidirectional Charging: Vehicle-to-grid technology, enabling EVs to discharge stored electricity back to the grid during peak demand periods, creates a new revenue model for EV owners and charging operators that transforms EVs from energy consumers into distributed energy storage assets.

- Highway Fast Charging Network Buildout: The intercity fast charging corridor represents the highest-revenue-density opportunity in charging infrastructure, with DCFC stations on major motorways consistently achieving 25–40% utilization rates versus 10–15% for urban public chargers.

Market Challenges

- Charging Reliability and Uptime Consistency: Industry surveys consistently identify charging station reliability as the primary barrier to EV consideration among non-EV drivers. Moreover, poor uptime undermines consumer confidence in EV long-distance travel capability, representing a critical adoption barrier that charging operators must address through improved hardware quality, proactive maintenance programs, and real-time status monitoring.

- Business Model Viability and Payback Period Uncertainty: The emergence of bundled charging subscription models, dynamic pricing, advertising revenue, and V2G grid services revenue is gradually improving CPO economics, but many charging network operators remain dependent on government subsidies and OEM charging guarantees for financial viability.

Emerging Market Trends

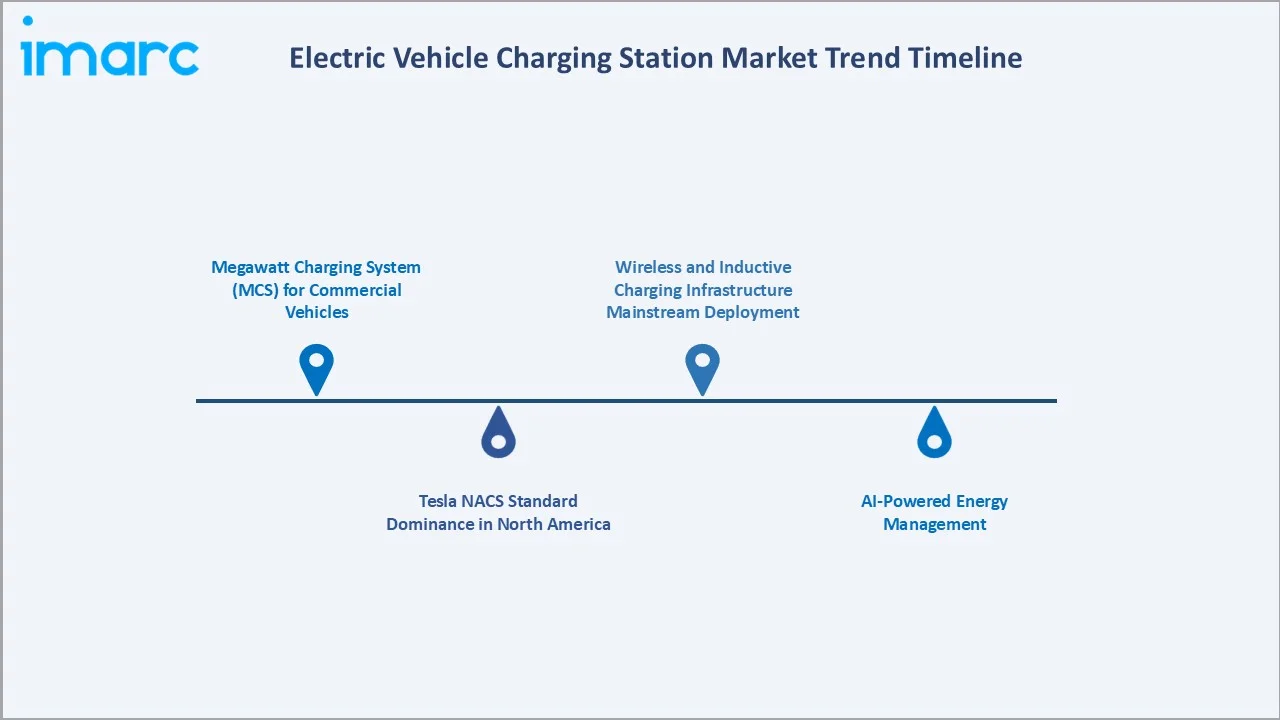

1. Megawatt Charging System (MCS) for Commercial Vehicles

In February 2026, CharIN announced the official publication of IEC TS 63379, a technical specification standardizing connectors, vehicle inlets, and cable assemblies for Megawatt Charging System (MCS) hardware. The standard supports high-power DC charging of up to 1,500 V and 3,000 A, enabling faster charging and interoperability for heavy-duty electric trucks, buses, off-highway machinery, marine, mining, and industrial applications.

2. Tesla NACS Standard Dominance in North America

Tesla’s North American Charging Specification (NACS) is helping standardize EV charging in the U.S. by opening Tesla’s connector design to other charging providers and automakers. Tesla planned to make 7,500 chargers accessible to non-Tesla EVs by the end of 2024, while automakers such as Ford and General Motors agreed to equip new BEVs with NACS inlets from 2025.

3. AI-Powered Energy Management

Delta launched DeltaGrid EVM, an AI-powered EV charging management system that integrates EV chargers with solar energy and energy storage to improve charging-site power stability, safety, and operating efficiency. The platform supports smart charging, energy scheduling, charger management, and digital O&M, using real-time load management to distribute charging peaks and prevent grid overload.

4. Wireless and Inductive Charging Infrastructure Mainstream Deployment

EV wireless charging uses resonant electromagnetic induction to charge vehicles without a plug, with future applications ranging from home and fleet charging to dynamic charging roads that power EVs while driving. The technology can reduce range anxiety and improve charging convenience, but wider adoption still depends on lower installation costs, faster charging speeds, common standards, and more compatible EV models.

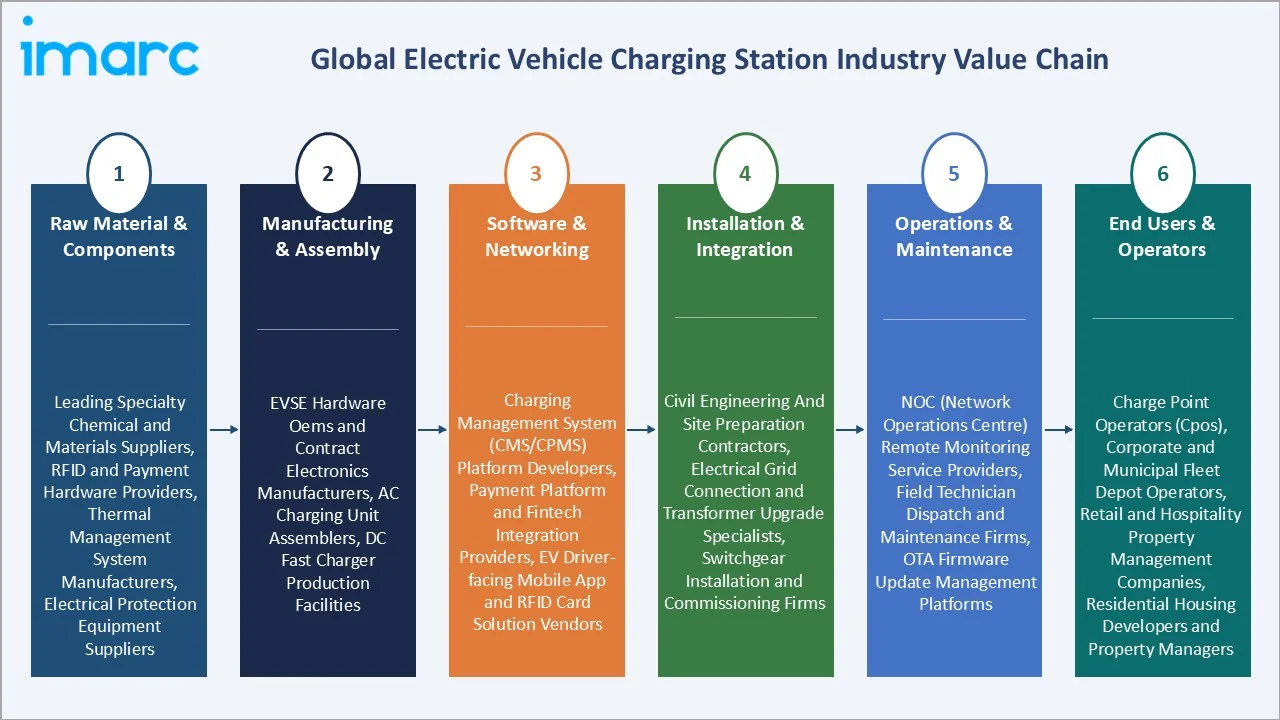

Industry Value Chain Analysis

The EV charging station value chain is distinguished by the rapid entry of utilities, energy retailers, automotive OEMs, and real estate operators into the middle and downstream stages, transforming charging infrastructure from a pure technology manufacturing market into a diversified services and infrastructure asset class.

|

Stage |

Key Players/Examples |

|

Raw Material & Components |

Leading specialty chemical and materials suppliers, RFID and payment hardware providers, thermal management system manufacturers, electrical protection equipment suppliers |

|

Manufacturing & Assembly |

EVSE hardware OEMs and contract electronics manufacturers, AC charging unit assemblers, DC fast charger production facilities |

|

Software & Networking |

Charging Management System (CMS/CPMS) platform developers, payment platform and fintech integration providers, EV driver-facing mobile app and RFID card solution vendors |

|

Installation & Integration |

Civil engineering and site preparation contractors, electrical grid connection and transformer upgrade specialists, switchgear installation and commissioning firms |

|

Operations & Maintenance |

NOC (Network Operations Centre) remote monitoring service providers, field technician dispatch and maintenance firms, OTA firmware update management platforms |

|

End Users & Operators |

Charge Point Operators (CPOs), corporate and municipal fleet depot operators, retail and hospitality property management companies, residential housing developers and property managers |

Technology Landscape in the Electric Vehicle Charging Station Industry

DC Fast Charging and Ultra-Fast Charging Technology

DC fast charging technology has advanced from 50 kW first-generation systems to 350 kW ultra-fast charging systems. The adoption of silicon carbide (SiC) power semiconductors has reduced DCFC charger size and weight by approximately 50% while improving energy conversion efficiency from 92–94% to 96–98%, directly reducing operating costs and enabling higher-density multi-charger site configurations.

Open Protocols, Interoperability, and Smart Charging Platforms

The adoption of OCPP 2.0.1 (Open Charge Point Protocol) as the dominant communication standard between charging hardware and network management systems is enabling multi-vendor interoperability, allowing CPOs to mix charging hardware from different manufacturers within a single network management platform.

Energy Storage Integration and Grid Services

The integration of battery energy storage systems (BESS) with EV charging infrastructure is enabling high-power DCFC deployment in locations with inadequate grid connection capacity, at demand charge-intensive commercial tariffs, and in remote locations off the main distribution grid.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Charging Station Type |

AC Charging |

88.1% |

2025 |

|

Installation Type |

Fixed Charger |

93.2% |

2025 |

|

Vehicle Type |

Battery Electric Vehicle (BEV) |

78.8% |

2025 |

|

Charging Level |

Level 2 |

69.7% |

2025 |

|

Connector Type |

CHAdeMO |

30.3% |

2025 |

|

Application |

Residential |

61.1% |

2025 |

|

Region |

Asia-Pacific |

54.5% |

2025 |

By Charging Station Type

AC charging dominates with an 88.1% share in 2025. This segment encompasses Level 1 (3–7.4 kW single-phase) and Level 2 (7.4–22 kW three-phase) charging equipment serving residential home chargers, workplace charging, retail and parking destination charging, and public street-side charging.

To access detailed market analysis, Request Sample

DC charging at 9.4% serves the intercity travel and rapid urban top-up use cases across dedicated fast charging networks on highways, fuel stations, and high-traffic urban locations. Despite its minority share in total installed units, DC Charging represents a disproportionate share of total market revenue due to the significantly higher hardware costs.

By Installation Type

Fixed charger commands a 93.2% share in 2025. Fixed chargers are the standard deployment model for home, workplace, retail, and public charging across all power levels from Level 1 to ultra-fast DC. The fixed installation model enables permanent grid connections, building management system integrations, and signage that maximize utilization rates and revenue generation potential of charging assets.

Portable charger at 6.8% serves fleet operators requiring flexible depot charging configurations, EV drivers in multi-family residential settings without dedicated parking, emergency roadside charging services, and markets with immature fixed charging infrastructure where portable units provide an interim solution.

Regional Market Insights

Asia-Pacific’s market leadership (54.5%, 2025) is defined by China’s structural dominance of the global EV ecosystem. The Chinese government’s integrated policy approach, combining mandatory NEV quotas for automotive manufacturers, direct subsidies for both EV purchase and charging infrastructure, and state grid investment in charging-ready distribution network upgrades, has created the world’s most mature and comprehensive EV charging ecosystem.

Europe at 19.6%, benefits from the EU’s most comprehensive regulatory framework for EV charging, creating a legally enforceable demand signal for charging infrastructure investment. North America, at 15.8%, is experiencing a step-change in public DCFC deployment through the NEVI Program, while the Tesla Supercharger network’s opening to non-Tesla EVs with NACS adapters is significantly expanding its contribution to the overall public charging ecosystem.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

54.5% |

World's largest EV fleet and most extensive public charging network; rapid two-wheel and commercial vehicle electrification; strong government-directed charging infrastructure investment and EV adoption mandates across all major regional economies |

|

Europe |

19.6% |

National EV charging infrastructure programs across major economies; growing EV platform rollouts by domestic and international automotive OEMs; highway and urban fast charging network expansion by energy majors and independent CPOs |

|

North America |

15.8% |

Federal government infrastructure funding programs; tax credit incentives driving commercial EV charging investment; accelerating EV platform launches by major domestic automakers |

|

Latin America |

5.3% |

Growing hybrid and battery EV adoption among urban consumers; automotive manufacturing sector EV transition creating fleet charging demand; rising middle-class EV awareness in key markets |

|

Middle East & Africa |

4.8% |

Government EV adoption incentive programs; growing urban premium EV consumer market; public sector fleet electrification initiatives; expanding charging infrastructure investment by energy companies and real estate developers |

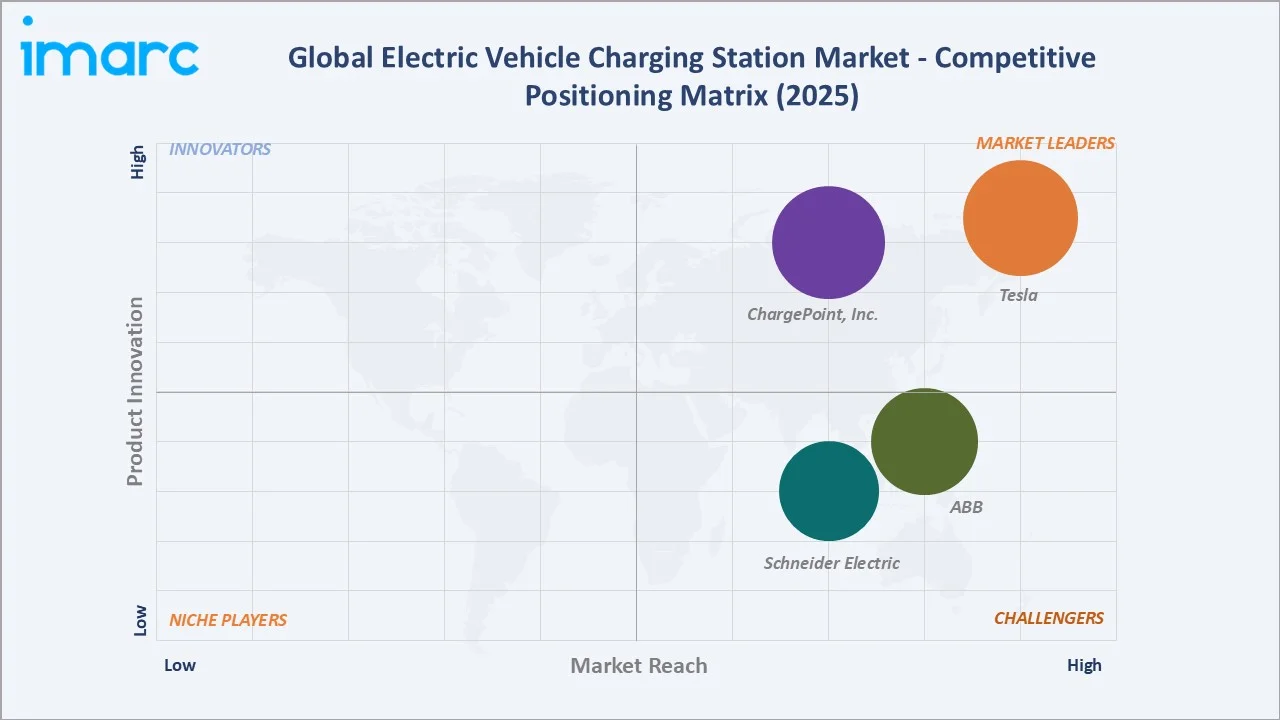

Competitive Landscape

The global EV charging station market exhibits moderate concentration in the network software and premium DCFC hardware layers, with Tesla, ChargePoint, Inc., ABB, and Schneider Electric commanding strong positions.

|

Company Name |

Key Product/Solution |

Market Position |

Core Strength |

|

Tesla |

Charging, Home Charging, Supercharging, Wall Connector for Business, Supercharger for Business, Semi Charging for Business |

Market Leader |

One of the world’s largest and highest-utilization DCFC networks; vertically integrated hardware-software-network ecosystem |

|

ChargePoint, Inc. |

Next-gen Express, Express 280, Express Plus, CP6000, ChargePoint Home Flex |

Market Leader |

One of the world’s largest open CPO networks by port count; strong enterprise and fleet B2B segment; North America and Europe dual-market presence |

|

ABB |

OM X-Series, OM M-Series |

Strong Challenger |

Broadest charging technology portfolio from AC to ultra-fast DC and wireless; strong utility and highway CPO client base |

|

Schneider Electric |

EVlink Home, EVlink Pro AC, EcoStruxure EV Charging Expert |

Strong Challenger |

Strong commercial building and industrial site charging management; AI-powered demand charge management; global service and installation network |

The hardware manufacturing layer is highly competitive and rapidly commoditizing for Level 2 AC chargers, with Chinese manufacturers offering units at 30–50% below Western equivalent pricing and capturing growing share in cost-sensitive markets.

Key Company Profiles

ABB

ABB’s division ABB E-mobility is one of the world’s leading providers of EV charging technology, offering one of the broadest portfolios of AC and DC charging solutions for residential, commercial, and industrial applications.

- Product Portfolio: Charging, home charging, supercharging, wall connector for business, supercharger for business, and semi charging for business.

- Recent Developments: In May 2026, ABB E-mobility launched the OM X-Series, a distributed DC charging system designed for continuous, high-duty fleet use at transit depots, logistics hubs, and public charging corridors. The platform can scale from 800 kW to over 10 MW across 100+ charge points, using liquid-cooled architecture, coordinated site-level power management, and direct energy storage integration.

- Strategic Focus: Ultra-fast AC and DC charging hardware leadership; Halo wireless charging platform for premium OEM integration; global CPO and utility partnership expansion; AI-powered uptime and predictive maintenance.

ChargePoint, Inc.

ChargePoint, Inc. is one of the world’s largest EV charging network operators by number of ports. The company operates as a hardware manufacturer, network software platform provider, and CPO services company, offering an end-to-end white-label CPO platform.

- Product Portfolio: Next-gen Express, Express 280, Express Plus, CP6000, and ChargePoint Home Flex.

- Recent Developments: In April 2026, ChargePoint, Inc. launched Express Solo, a next-generation standalone DC fast charger for mass-market EVs, capable of delivering up to 600 kW to a single vehicle. It can charge two EVs simultaneously, or up to four vehicles when paired with an additional dispenser, while addressing grid constraints, speed, reliability, and deployment cost challenges.

- Strategic Focus: ChargePoint Assure CaaS model to accelerate commercial site deployment; fleet management platform enhancement for autonomous and last-mile electric delivery; ChargePoint Cloud platform API ecosystem for third-party integration.

Market Concentration Analysis

The global EV charging station market exhibits moderate concentration in the network operation and DC fast charging hardware layers, with Tesla, ChargePoint, Inc., and the energy majors commanding significant positions in high-traffic public charging networks.

The AC Level 2 hardware manufacturing segment is highly fragmented and commoditized, with hundreds of manufacturers across China, Europe, and North America competing primarily on price, with Chinese manufacturers increasingly displacing Western incumbents in cost-sensitive residential and fleet depot applications.

Investment & Growth Opportunities

Fastest Growing Segments

Inductive charging (~32.5% CAGR), portable charger (~29.4% CAGR), DC fast charging (~31.2% CAGR), and commercial fleet depot charging (~30%+ CAGR) represent the primary high-growth investment vectors through 2034. The emerging Megawatt Charging System (MCS) for heavy trucks is expected to grow from virtually zero to a USD 8–15 Billion market by 2034, representing one of the single largest new sub-segment opportunities in the entire EV ecosystem.

Emerging Market Expansion

The India electric vehicle charging station market size was valued at USD 589.1 Million in 2025 and is projected to reach USD 1,078.8 Million by 2034, exhibiting a CAGR of 6.82% during 2026-2034. This is attributed to the country’s electric two-wheeler and three-wheeler markets driving unprecedented low-power charging infrastructure demand. Southeast Asia’s EV transition, led by Thailand, Indonesia, and Vietnam adopting Chinese EV brands and building domestic charging networks, represents a USD 5–10 Billion incremental market by 2034.

Venture and Institutional Investment Trends

- Infrastructure funds have established dedicated EV charging infrastructure investment vehicles, treating CPO networks as regulated infrastructure assets with long-term contracted revenue streams comparable to toll roads and utility assets.

- Strategic corporate investors, for instance, in April 2026, Walmart and ABB E-mobility launched ABB’s A400 All-in-One fast chargers at seven Walmart locations in the Phoenix metro area, marking the start of a nationwide retail EV charging rollout.

Future Market Outlook (2026-2034)

The global EV charging station market is positioned for a structural decade of extraordinary expansion, with the 28.15% CAGR representing the most sustained high-growth period in the market’s history. From a base of USD 21.58 Billion in 2025, the market will reach USD 74.58 Billion by 2030 and USD 213.75 Billion by 2034.

Asia-Pacific will retain absolute market leadership throughout the forecast period, while Europe and North America will grow faster than the global average from 2026–2030 as mandated charging infrastructure deployment accelerates ahead of ICE vehicle phase-out dates.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 90 industry participants in 2024–2025, including CPO executives, charging hardware manufacturers, automotive OEM charging strategy teams, utility EV charging program managers, government EV policy officials, and industry association representatives from CharIN, OCPI Forum, and AVERE.

Secondary Research

Secondary research encompassed company annual reports and investor presentations; IEA Global EV Outlook 2025; BNEF Electric Vehicle Outlook 2025; European Automobile Manufacturers Association (ACEA) charging data; US DOE Alternative Fuels Station Locator database; China EVCIPA charging infrastructure statistics; and SAE, CharIN, and OCPP technical standards documentation.

Forecasting Models

Market size estimations were derived using bottom-up charging point deployment modelling combined with top-down EV fleet growth projections and average revenue per charging session analysis. A CAGR of 28.15% reflects the convergence of EV fleet expansion, regulatory mandates, and infrastructure investment, validated against IEA and BNEF charging infrastructure investment forecasts and IMARC’s primary expert panel review.

Electric Vehicle Charging Station Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Charging Station Types Covered | AC Charging, DC Charging, Inductive Charging |

| Vehicle Types Covered | Battery Electric Vehicle (BEV), Plug-in Hybrid Electric Vehicle (PHEV), Hybrid Electric Vehicle (HEV) |

| Installation Types Covered | Portable Charger, Fixed Charger |

| Charging Levels Covered | Level 1, Level 2, Level 3 |

| Connector Types Covered | Combines Charging Station (CCS), CHAdeMO, Normal Charging, Tesla Supercharger, Type-2 (IEC 621196), Others |

| Applications Covered | Residential, Commercial |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Tesla, ChargePoint, Inc., ABB, Schneider Electric, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the electric vehicle charging station market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global electric vehicle charging station market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the electric vehicle charging station industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Electric Vehicle Charging Station Market Report

The global EV charging station market reached USD 21.58 Billion in 2025 and is forecast to reach USD 213.75 Billion by 2034.

The market is expected to grow at a CAGR of 28.15% during 2026-2034, driven by EV adoption mandates, government infrastructure incentives, energy major CPO investment, and the electrification of commercial vehicle and fleet segments.

Asia-Pacific leads with a 54.5% share in 2025, anchored by China’s world-leading EV fleet and the country’s addition of 1.3 million public charging points in 2025, further supported by Japan, South Korea, and India’s rapidly growing EV markets.

AC Charging dominates with an 88.1% share in 2025, driven by the prevalence of Level 1 and Level 2 home, workplace, and destination chargers that serve the daily charging behavior of the global EV owner base.

Fixed Charger leads with a 93.2% share in 2025, reflecting the CPO business model’s dependence on permanently installed assets at high-traffic locations for revenue generation through energy delivery fees.

Some of the key players in the market include Tesla, ChargePoint, Inc., ABB, and Schneider Electric.

Inductive charging is growing at approximately 32.5% CAGR as the premium automotive OEMs are integrating SAE J2954-compliant wireless receivers into EV platforms, enabling hands-free charging that eliminates the cable-handling friction of conventional charging.

Key challenges include high DC fast charger installation costs, grid infrastructure upgrade constraints creating 12–24 month utility connection timelines, and connector standard fragmentation between CCS, NACS, and CHAdeMO.

Highway Megawatt Charging for heavy trucks, inductive wireless charging infrastructure for premium EV platforms, fleet depot electrification charging, India and Southeast Asia first-mover EV charging deployment, and AI-powered energy management CMS platforms represent the highest-growth investment opportunities through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)