Electronic Design Automation Market Report by Solution Type (Semiconductor IP, CAE (Computer Aided Engineering), IC Physical Design and Verification, PCB & MCM (Printed Circuit Board and Multi-Chip Module), Services), Deployment Type (On-premises, Cloud-based), End-Use Industry (Military/Defense, Aerospace, Telecom, Automotive, Healthcare, and Others), and Region 2026-2034

Electronic Design Automation Market Size:

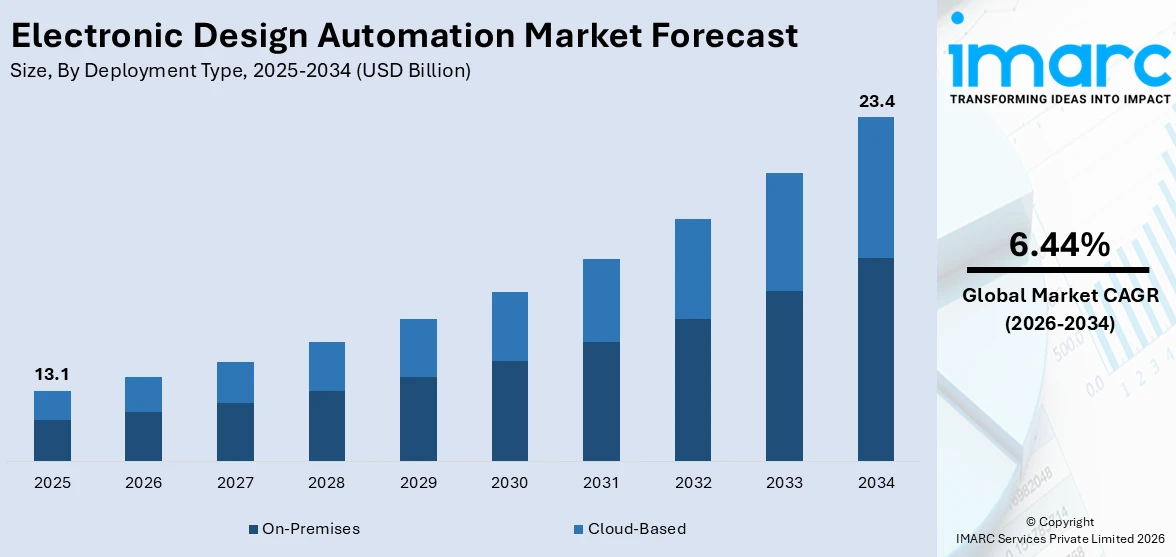

The global electronic design automation market size reached USD 13.1 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 23.4 Billion by 2034, exhibiting a growth rate (CAGR) of 6.44% during 2026-2034. The market is experiencing moderate growth driven by rapid technological advancements, proliferation of IoT devices, 5G technology implementation, increasing complexity of semiconductor designs, and global automotive electronics industry expansion.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 13.1 Billion |

|

Market Forecast in 2034

|

USD 23.4 Billion |

| Market Growth Rate 2026-2034 | 6.44% |

Electronic Design Automation Market Analysis:

- Market Growth and Size: The market is witnessing moderate growth, driven by the increasing demand for semiconductor chips in various industries.

- Technological Advancements: Technological advancements in EDA tools, such as AI and machine learning integration, have improved design efficiency and reduced time-to-market for electronic products. Cloud-based EDA solutions are gaining popularity, enabling remote collaboration and scalability.

- Industry Applications: EDA tools find extensive applications in semiconductor manufacturing, PCB design, and electronic system design across diverse sectors, including automotive, aerospace, consumer electronics, and healthcare.

- Geographical Trends: Asia-Pacific particularly China and Taiwan, has emerged as a dominant player in the EDA market, driven by the robust semiconductor industry in the region. North America remains a key market, with a focus on innovation and R&D in EDA technology.

- Competitive Landscape: Key players are characterized by intense competition, with companies continuously striving to offer cutting-edge solutions.

- Challenges and Opportunities: The EDA market faces challenges related to the complexity of designs and the need for skilled professionals. Opportunities lie in the growing demand for IoT devices, 5G technology, and automotive electronics, driving the need for advanced EDA solutions.

- Future Outlook: The EDA market is poised for growth, driven by emerging technologies and the increasing integration of electronics in various industries. Collaboration and partnerships between EDA companies and semiconductor manufacturers are expected to play a pivotal role in shaping the future of the industry.

To get more information on this market Request Sample

Electronic Design Automation Market Trends:

Rapid Technological Advancements

The EDA market is significantly influenced by rapid technological advancements in the electronics industry. With each passing year, electronic devices become more sophisticated, requiring intricate and efficient designs. EDA tools play a crucial role in meeting these demands. Advancements such as the integration of artificial intelligence (AI) and machine learning have revolutionized the design process, enabling faster and more accurate design iterations. This technology-driven evolution propels the EDA market forward as companies seek cutting-edge solutions to stay competitive.

Proliferation of IoT Devices

The Internet of Things (IoT) has witnessed exponential growth in recent years across various sectors, from smart homes to industrial automation. This rise in IoT applications drives the demand for EDA tools to design efficient and power-efficient microchips and sensors. The EDA market benefits from the expansion of IoT as it requires specialized solutions to address the unique challenges posed by IoT device design, including low power consumption, small form factors, and connectivity requirements.

5G Technology Implementation

The rollout of 5G technology brings enhanced network capabilities, enabling faster data transfer and lower latency. To harness the potential of 5G, there is a growing need for EDA tools that can design complex RF (radio frequency) and mmWave (millimeter-wave) circuits. EDA companies are developing solutions to help manufacturers design 5G-enabled devices, contributing to the growth of the EDA market.

Increasing Complexity of Semiconductor Designs

Semiconductor designs have become increasingly complex, driven by demands for higher performance, lower power consumption, and smaller form factors. This complexity necessitates advanced EDA tools capable of handling intricate designs efficiently. Companies in the semiconductor industry rely on EDA solutions to reduce design cycles and enhance product reliability, which in turn fuels the growth of the EDA market.

Expansion of Automotive Electronics Industry

The automotive electronics industry is undergoing a significant transformation with the proliferation of electric vehicles (EVs) and autonomous driving technologies. These innovations require advanced electronic systems, leading to a rise in automotive electronics. EDA tools are essential in designing the complex electronic components and systems required for EVs and autonomous vehicles. The expansion of automotive electronics is a key driver of the EDA market as it creates opportunities for specialized design solutions tailored to the automotive unique requirements of sectors.

Electronic Design Automation Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on solution type, deployment type, and end-use industry.

Breakup by Solution Type:

- Semiconductor IP

- CAE (Computer Aided Engineering)

- IC Physical Design and Verification

- PCB & MCM (Printed Circuit Board and Multi-Chip Module)

- Services

Semiconductor IP accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the solution type. This includes semiconductor IP, CAE (computer aided engineering), IC physical design and verification, PCB & MCM (printed circuit board and multi-chip module), and services. According to the report, semiconductor IP represented the largest segment.

Semiconductor IP includes pre-designed and pre-verified building blocks of electronic components used in semiconductor chip design. These IP cores serve as the foundational elements for designing integrated circuits (ICs) and system-on-chips (SoCs). As the complexity of ICs continues to grow, semiconductor IP becomes vital for reducing development time and costs. This segment of the EDA market is experiencing moderate growth due to the increasing demand for specialized and reusable IP blocks in various applications, such as consumer electronics, automotive, and IoT devices.

CAE encompasses a range of software tools used for simulating and analyzing electronic systems and components. These tools help engineers assess the performance, reliability, and functionality of electronic designs before physical prototypes are built. CAE software includes simulation tools for electrical, thermal, and mechanical analysis. The CAE segment of the EDA market is expanding as industries seek to minimize design errors, optimize performance, and reduce development costs. It plays a critical role in ensuring the quality and efficiency of electronic products across diverse sectors.

IC physical design and verification involve the process of translating the logical design of a semiconductor chip into a physical layout. This segment includes tools and solutions for floor planning, placement, routing, and verification of ICs. The demand for ICs with higher integration and performance has driven the growth of this segment. EDA companies offer advanced tools that help semiconductor manufacturers design chips with smaller feature sizes, lower power consumption, and improved manufacturability, driving the continued expansion of the IC physical design and verification market.

PCB and MCM design involve creating the layouts and interconnections for electronic components on printed circuit boards and multi-chip modules. This segment of the EDA market is essential for designing complex electronic systems used in various applications, including telecommunications, automotive, and aerospace. With the increasing demand for smaller form factors and higher-density PCBs, EDA tools that aid in PCB and MCM design have become indispensable. They facilitate efficient routing, signal integrity analysis, and thermal management, contributing to the development of high-performance electronic products.

EDA services encompass a range of consulting, training, and support offerings provided by EDA companies to assist consumers in optimizing their electronic design processes. These services help organizations make the most of EDA tools, streamline workflows, and address specific design challenges. The services segment is crucial in ensuring that consumers can leverage EDA technology effectively. It also offers customization options, ensuring that EDA solutions align with the unique needs of different industries and clients.

Breakup by Deployment Type:

- On-Premises

- Cloud-Based

A detailed breakup and analysis of the market based on the deployment type have also been provided in the report. This includes on-premises and cloud-based.

On-premises deployment mode refers to the traditional method of installing and running EDA software and tools directly on own servers and infrastructure of a company within their physical premises. This deployment mode has been the standard for many years and offers certain advantages. One of the key advantages of on-premises deployment is data control and security. Companies have complete control over their data, ensuring that sensitive design and intellectual property remains within their network. This level of control is essential in industries where confidentiality is paramount, such as defense, aerospace, and some areas of semiconductor manufacturing.

Cloud-based deployment mode, on the other hand, involves accessing EDA tools and services over the internet from cloud service providers' data centers. This mode has gained popularity due to its flexibility and scalability. One of the key advantages of cloud-based deployment is agility. Companies can quickly scale their computing resources up or down based on project requirements, paying only for what they use. This flexibility is particularly beneficial in industries with fluctuating design workloads, enabling cost optimization. Additionally, cloud-based EDA tools facilitate collaboration. Design teams can work on projects simultaneously from different locations, accessing a centralized, up-to-date platform. This collaborative environment enhances productivity and reduces design cycle times.

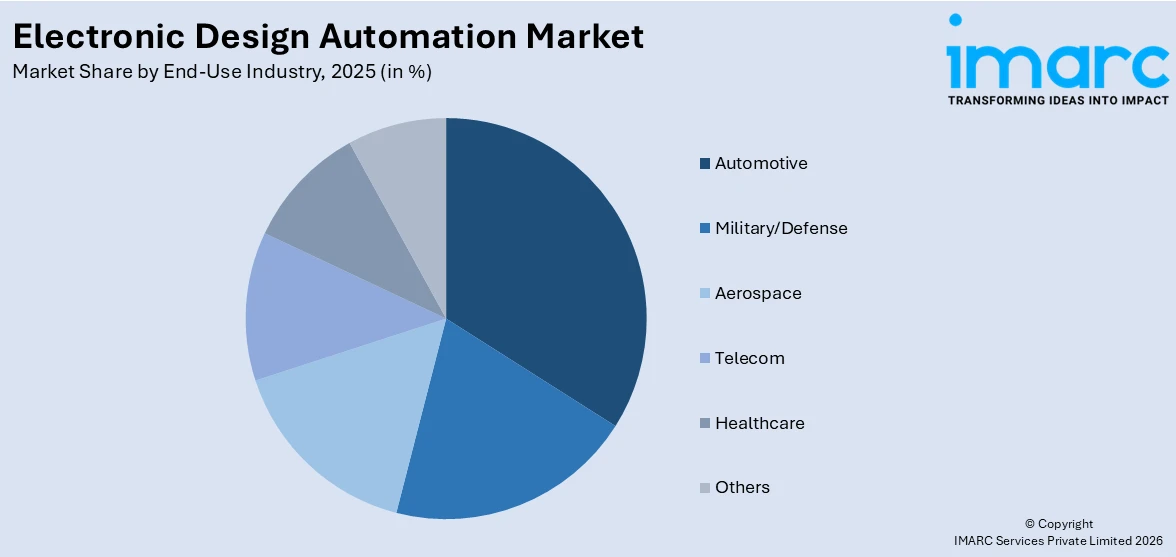

Breakup by End-Use Industry:

Access the comprehensive market breakdown Request Sample

- Military/Defense

- Aerospace

- Telecom

- Automotive

- Healthcare

- Others

Automotive represents the leading market segment

The report has provided a detailed breakup and analysis of the market based on the end use industry. This includes military/defense, aerospace, telecom, automotive, healthcare, and others. According to the report, automotive represented the largest segment.

The automotive industry has witnessed a rapid integration of electronic systems in vehicles, from advanced driver-assistance systems (ADAS) to electric powertrains. EDA tools are essential for designing automotive electronics, including microcontrollers, sensor interfaces, and communication networks. They enable automakers to develop efficient, safe, and connected vehicles while adhering to strict automotive safety standards such as, ISO 26262. With the transition to electric and autonomous vehicles, the demand for EDA solutions in the automotive sector is poised for significant growth.

The military and defense sector relies heavily on advanced electronics for communication, surveillance, navigation, and weaponry. EDA tools play a pivotal role in designing cutting-edge electronic systems for these applications. They aid in developing high-performance, ruggedized components, and ensure compliance with stringent standards for reliability and security. EDA assists in the design of specialized microelectronics for guided missile systems, radar systems, and encrypted communication devices. The emphasis of the defense industry on innovation and rapid development makes EDA solutions indispensable for achieving technological superiority. With evolving threats and the need for modernization, the EDA market within the military and defense sector is poised for continued growth.

In the aerospace industry, safety, reliability, and performance are paramount. EDA tools are essential for designing avionics systems, onboard computing, navigation, and control systems. These tools enable engineers to optimize designs for weight reduction, power efficiency, and durability. EDA plays a crucial role in ensuring compliance with aerospace regulations and standards, such as DO-254 for airborne electronic systems. With the increasing demand for commercial and military aircraft, space exploration, and satellite technology, the aerospace sector represents a significant market for EDA solutions. As the industry advances toward electric propulsion and autonomous flight, EDA tools will continue to drive innovation and efficiency in aerospace electronics.

The telecom industry relies on EDA tools to design complex integrated circuits and communication systems. From the development of 5G infrastructure to the design of high-speed data transmission equipment, EDA plays a crucial role in optimizing performance and power consumption. EDA solutions enable telecom companies to meet the growing demand for faster and more reliable connectivity. Additionally, as the telecom industry explores new technologies such as, optical communication and network virtualization, EDA tools facilitate the design of advanced hardware components and ensure compatibility with evolving standards. The ever-evolving telecom landscape ensures a steady demand for EDA software and services, making it a pivotal market segment.

In healthcare, electronic devices and systems have become instrumental in diagnostics, treatment, and patient care. EDA tools assist in designing medical devices, wearable health technology, and diagnostic equipment. These tools ensure that medical electronics meet stringent regulatory requirements, including FDA standards for safety and effectiveness. EDA solutions enable the development of precise and reliable medical devices such as MRI machines, pacemakers, and insulin pumps. With the increasing demand for telemedicine, remote monitoring, and personalized healthcare, the EDA market in healthcare is experiencing growth. As medical technology continues to advance, EDA will play a critical role in accelerating innovation and improving patient outcomes in the healthcare industry.

Breakup by Region:

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America leads the market, accounting for the largest electronic design automation market share

The market research report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America accounted for the largest market share.

North America is a significant hub for the electronic design automation (EDA) market. The region boasts a strong presence of major EDA companies such as, Synopsys, Cadence Design Systems, and Mentor Graphics. The United States, particularly Silicon Valley, is the epicenter of innovation in the semiconductor and electronics industries. The EDA market of North America is driven by constant technological advancements and heavy investments in research and development. The focus of the region on cutting-edge technologies such as, artificial intelligence, machine learning, and 5G technology fuels the demand for advanced EDA solutions.

Asia Pacific is a dominant force in the global EDA market, particularly driven by China, Taiwan, and South Korea. These countries host major semiconductor manufacturing facilities and are at the forefront of chip production. The rapid economic growth of this region and technological development have led to increased demand for EDA tools in semiconductor design, PCB manufacturing, and electronic system design. China, in particular, has emerged as a key player in the EDA market, with a focus on indigenously developing EDA solutions. The presence of a vast electronics manufacturing ecosystem and a growing consumer electronics market further contributes to the importance of the region.

Europe has a mature and well-established EDA market, with a strong emphasis on automotive and aerospace industries. The region is known for its precision engineering and manufacturing, driving the need for advanced EDA tools to design complex electronic systems in these sectors. Countries such as, Germany, France, and the United Kingdom are leaders in automotive electronics, while aerospace giants such as, Airbus contribute to the demand for cutting-edge EDA solutions. Additionally, Europe is also investing in research and development, particularly in areas such as, autonomous driving and renewable energy, further fueling the EDA growth of the market. The presence of leading universities and research institutions provides a steady pool of talent for the industry.

Latin America represents a growing market for electronic design automation (EDA). While it may not be as large as North America or Asia Pacific, the region is experiencing increased adoption of EDA tools, primarily driven by the expansion of the electronics and automotive industries. Countries such as, Brazil and Mexico have emerging electronics manufacturing sectors, creating a demand for EDA solutions to support product development and innovation. The automotive industry in these countries also contributes to the need for sophisticated electronic systems, further boosting the EDA market.

The Middle East and Africa (MEA) region is gradually emerging as a player in the EDA market. While the market is smaller compared to North America or Asia Pacific, MEA is witnessing growth in various industries, including telecommunications, aerospace, and automotive. Countries such as, the United Arab Emirates (UAE) are investing heavily in technology and innovation hubs, attracting companies in the electronics and semiconductor sectors. The demand for EDA tools is driven by the development of advanced infrastructure and smart cities in the region, which require sophisticated electronic systems. Furthermore, aerospace industry of MEA is gaining momentum with companies such as, Boeing and Airbus establishing a presence in the region. This leads to increased demand for EDA solutions to design intricate avionics systems.

Leading Key Players in the Electronic Design Automation Industry:

The key players in the market are actively investing heavily in research and development to create cutting-edge EDA tools that address the evolving needs of the semiconductor and electronics industries. These companies are integrating artificial intelligence and machine learning into their solutions to enhance design automation and verification processes. Moreover, they are expanding their portfolios to cover areas such as, 5G, IoT, and automotive electronics, catering to the growing demand for specialized EDA solutions in these sectors. Collaboration with semiconductor manufacturers and global expansion efforts are also common strategies among key players to stay at the forefront of the EDA market.

The market research report has provided a comprehensive analysis of the competitive landscape. Detailed profiles of all major companies have also been provided. Some of the key players in the market include:

- Altium Limited

- ANSYS, Inc.

- Autodesk Inc.

- Boldport Limited

- Cadence Design Systems Inc.

- Siemens AG

- Silvaco Inc.

- Synopsys, Inc.

- Vennsa Technologies

- Xilinx, Inc.

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

Latest News:

- February, 2023: Ansys has extended its partnership with Microsoft, aiming to broaden the accessibility of its simulation solutions through integration with the Microsoft Azure cloud-computing platform. This strategic expansion of collaboration seeks to leverage the capabilities of Azure to make Ansys' simulation tools more widely available to users across various industries.

- January, 2023: Siemens AG has introduced Questa, an advanced verification IQ software designed to address the intricate challenges posed by the increasing complexity of integrated circuits (ICs) in the field of logic verification. This software offers a robust solution for logic verification teams, empowering them to effectively navigate and conquer the intricacies that arise during the design process of modern ICs.

- June, 2021: Xilinx Inc. has introduced a groundbreaking product in the field of FPGA Electronic Design Automation (EDA) tools, known as Vivado ML Editions. This innovative tool package harnesses the power of machine learning (ML) optimization techniques and employs advanced team-based design methodologies to significantly enhance design efficiency and reduce costs. In direct comparison with the existing Vivado HLx Editions, the Vivado ML Editions demonstrate remarkable performance improvements.

Electronic Design Automation Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Solution Types Covered | Semiconductor IP, CAE (Computer Aided Engineering), IC Physical Design and Verification, PCB & MCM (Printed, Circuit Board and Multi-Chip Module), Services |

| Deployment Types Covered | On-Premises, Cloud-Based |

| End Use Industries Covered | Military/Defense, Aerospace, Telecom, Automotive, Healthcare, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Altium Limited, ANSYS, Inc., Autodesk Inc., Boldport Limited, Cadence Design Systems, Inc., Siemens AG, Silvaco Inc., Synopsys, Inc., Vennsa Technologies, Xilinx, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the electronic design automation market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global electronic design automation market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the electronic design automation industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Electronic Design Automation Market Forecast Report

The global electronic design automation market was valued at USD 13.1 Billion in 2025.

We expect the global electronic design automation market to exhibit a CAGR of 6.44% during 2026-2034.

The sudden outbreak of the COVID-19 pandemic had led to the implementation of stringent lockdown regulations across several nations, resulting in the temporary closure of numerous end-use industries for electronic design automation solutions.

The emerging trend of miniaturized electronic products, along with the rising adoption of EDA solutions to design advanced electronics with compact designs and high efficiency, is primarily driving the global electronic design automation market.

Based on the solution type, the global electronic design automation market has been segregated into semiconductor IP, CAE (Computer Aided Engineering), IC physical design and verification, PCB & MCM (Printed Circuit Board and Multi-Chip Module), and services. Among these, semiconductor IP currently holds the largest market share.

Based on the end-use industry, the global electronic design automation market can be bifurcated into military/defense, aerospace, telecom, automotive, healthcare, and others. Currently, the automotive industry exhibits a clear dominance in the market.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where North America currently dominates the global market.

Some of the major players in the global electronic design automation market include Altium Limited, ANSYS, Inc., Autodesk Inc., Boldport Limited, Cadence Design Systems, Inc., Siemens AG, Silvaco Inc., Synopsys, Inc., Vennsa Technologies, and Xilinx, Inc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)