EMI Shielding Market Size, Share, Trends and Forecast by Material, Shielding Method, End-Use Industry, and Region, 2026-2034

EMI Shielding Market Size, Share, Trends & Forecast (2026-2034)

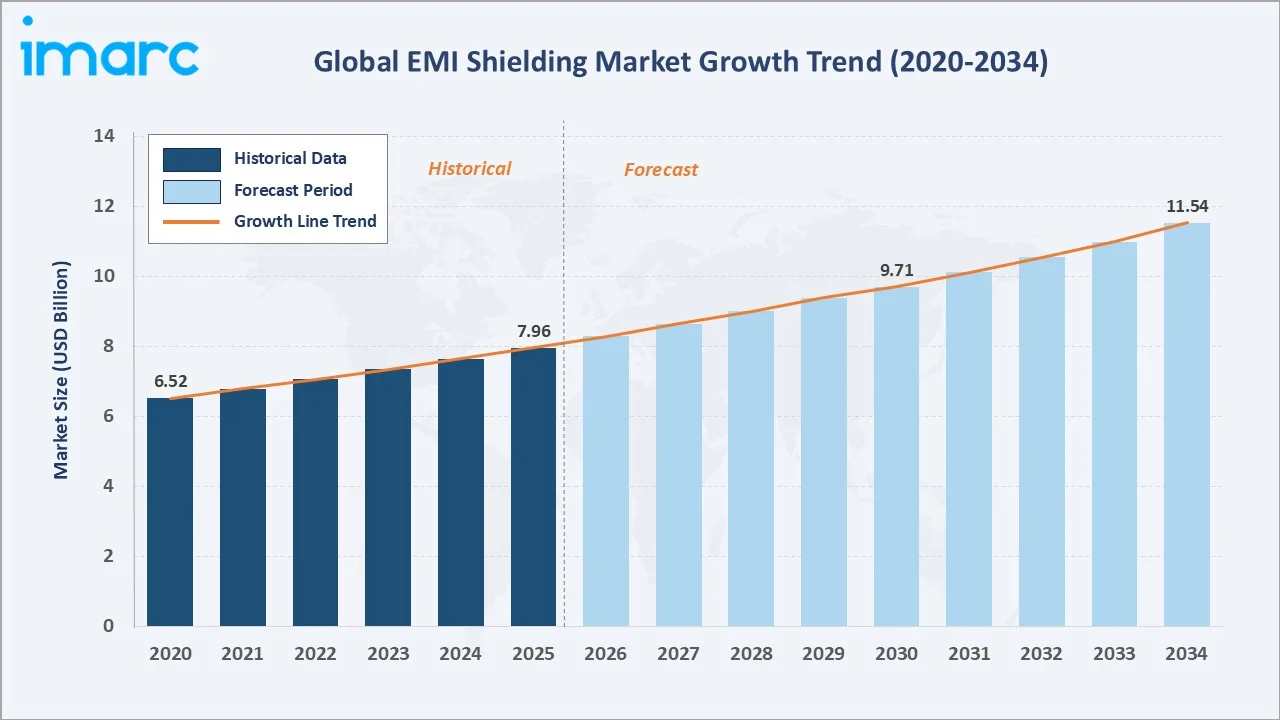

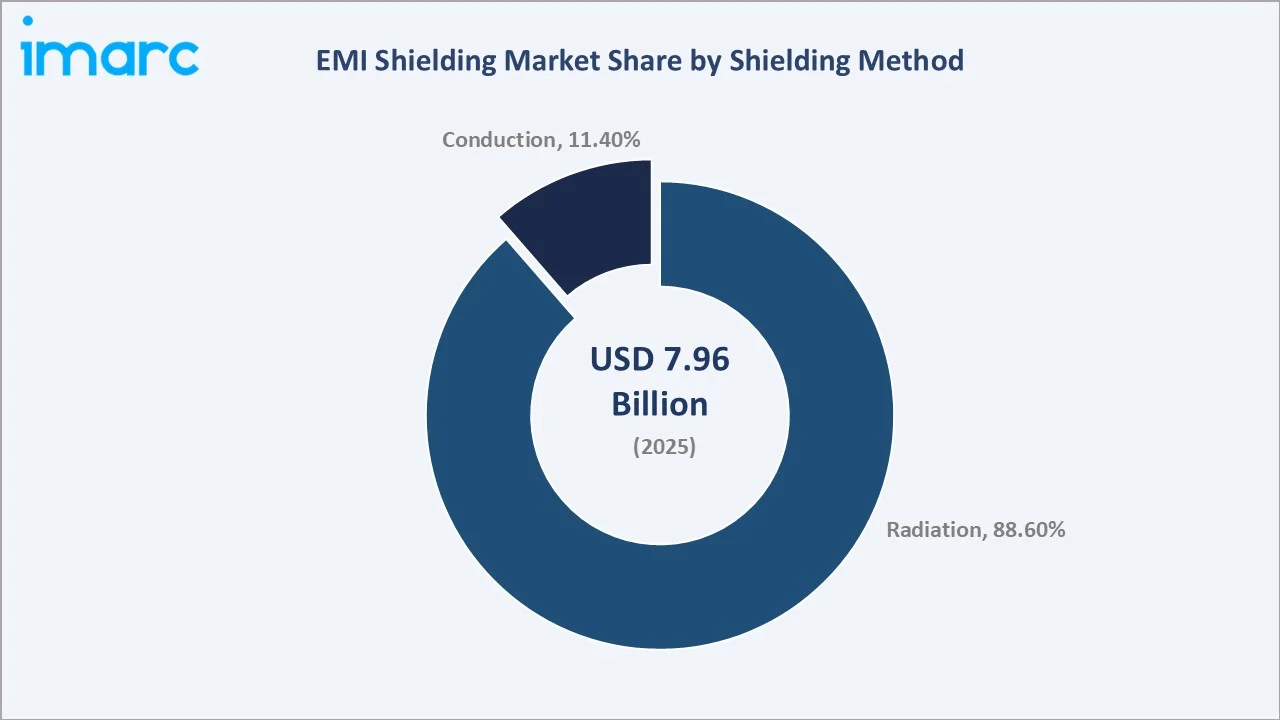

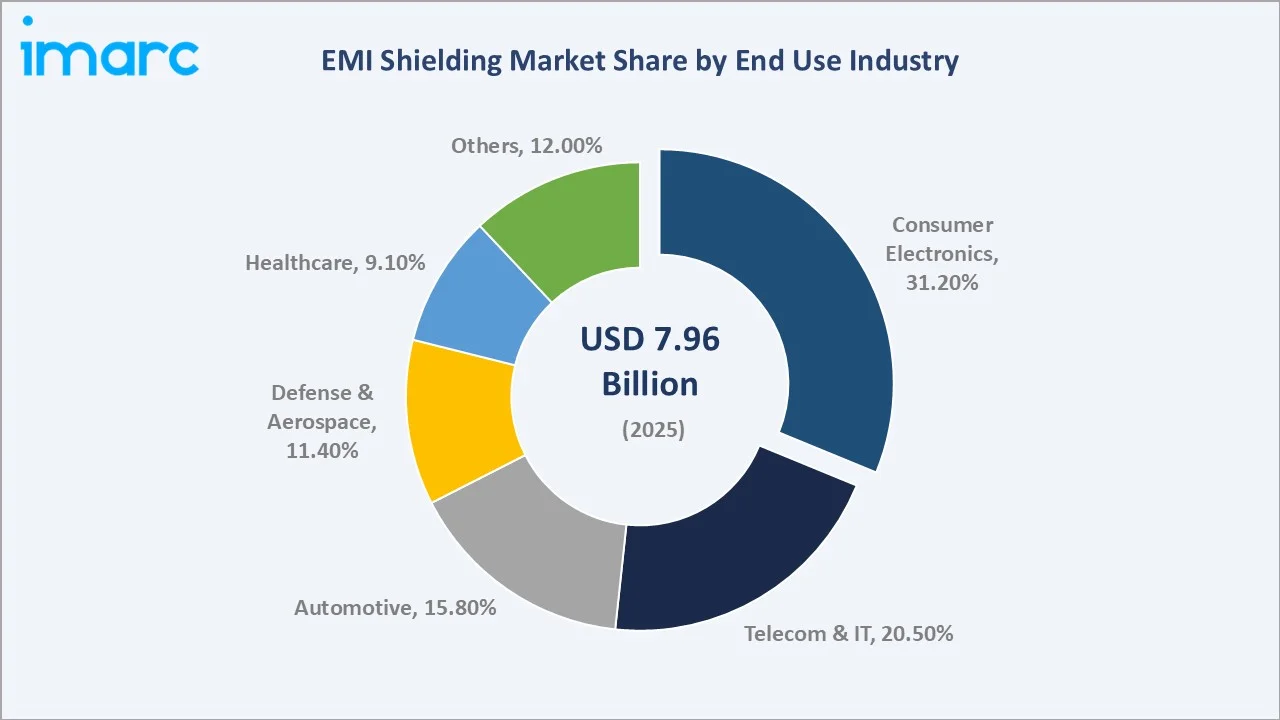

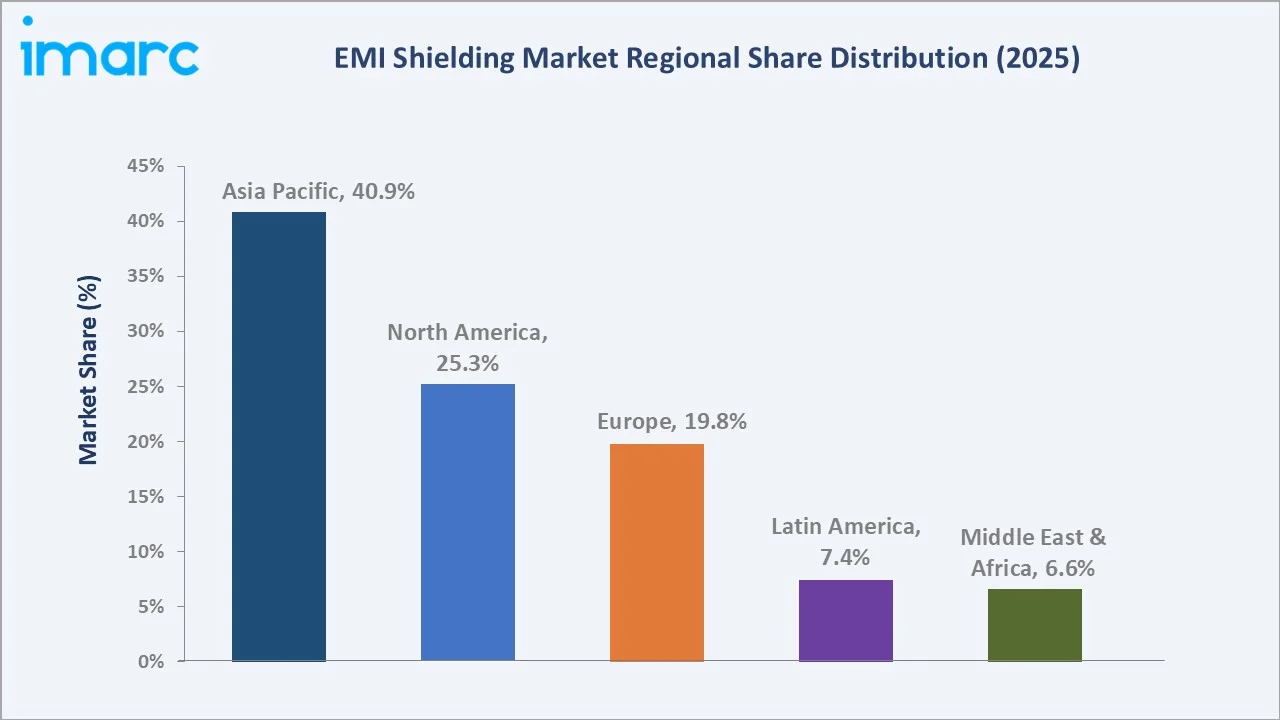

The global EMI shielding market size was valued at USD 7.96 Billion in 2025 and is projected to reach USD 11.5 Billion by 2034, exhibiting a CAGR of 4.1% during the forecast period 2026-2034. Rising 5G network deployment, growing miniaturization of electronics, and expanding adoption of advanced healthcare equipment are the primary growth catalysts. Radiation-based shielding leads the shielding method segment at 88.6% in 2025, while consumer electronics accounts for the largest end-use share at 31.2%. Asia Pacific dominates with 40.9% of global revenues in 2025, led by China, Japan, and South Korea's thriving electronics manufacturing ecosystems.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 7.96 Billion |

|

Forecast Market Size (2034) |

USD 11.5 Billion |

|

Market Size (2030) |

USD 9.71 Billion |

|

Market Size (2020) |

USD 6.52 Billion |

|

CAGR (2026-2034) |

4.1% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (40.9% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

The chart below illustrates the EMI shielding market growth trajectory from 2020 through 2034, contrasting historical performance against a sustained forecast curve driven by 5G, EV proliferation, and healthcare electronics demand.

To get more information on this market, Request Sample

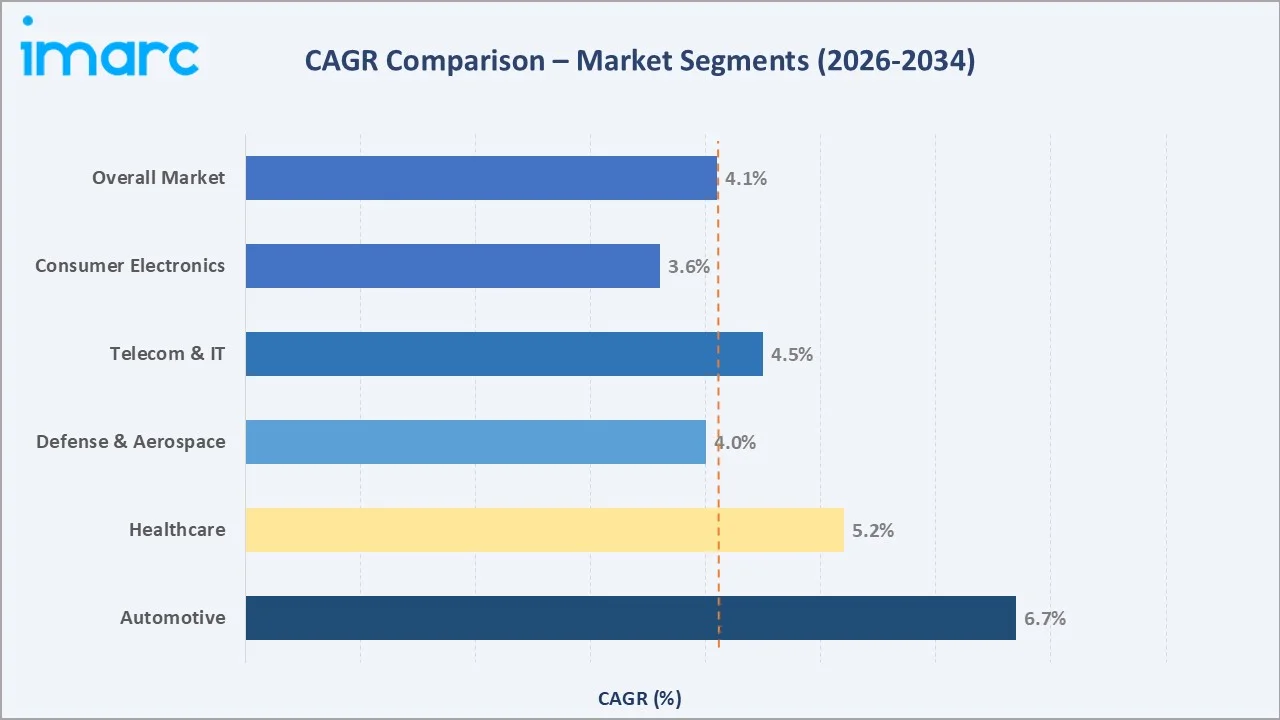

Segment-level CAGR comparisons highlighting Automotive and Healthcare as the two fastest-growing end-use verticals within the global EMI shielding industry analysis through 2034.

Executive Summary

The global EMI shielding market is experiencing sustained growth driven by the convergence of 5G connectivity, electrification of transport, IoT proliferation, and tightening electromagnetic compatibility (EMC) regulations globally. Valued at USD 7.96 Billion in 2025, the market is forecast to reach USD 11.5 Billion by 2034 at a CAGR of 4.1%. The global rollout of 5G networks is accelerating rapidly, with subscriptions growing at a strong pace worldwide, driving increased demand for high-performance EMI shielding across base stations, antenna modules, and connected devices.

Radiation-based shielding commands 88.6% of segment revenues in 2025, underpinned by demand from healthcare imaging systems, aerospace communications, and military electronics. Consumer electronics lead end-use verticals at 31.2% in 2025, powered by global smartphone production growth and rapid expansion in wearables, which have recorded consistently strong shipment volumes in recent years. Automotive stands as the fastest-growing end-use segment through 2034, driven by EV adoption and ADAS integration requirements.

Asia Pacific dominates with a 40.9% global revenue share in 2025, led by China's electronics manufacturing ecosystem revenues reaching USD 2.26 trillion in 2024, Japan's precision component suppliers, and South Korea's advanced materials R&D base. North America holds 25.3% of market revenues, while Europe commands 19.8%. The market outlook through 2034 remains positive across all regions, driven by new material innovations including carbon nanotube composites, transparent EMI films, and adaptive metamaterial-based shields.

Key Market Insights

|

Insight |

Data |

|

Largest Shielding Method |

Radiation – 88.6% share (2025) |

|

Largest End-Use Segment |

Consumer Electronics – 31.2% share (2025) |

|

Leading Region |

Asia Pacific – 40.9% revenue share (2025) |

|

Second Region |

North America – 25.3% revenue share (2025) |

|

Top Companies |

3M, Parker Hannifin Corp., Laird, Henkel, Murata |

Key Analytical Observations Supporting The Above Data:

- Radiation shielding's 88.6% dominance in 2025 reflects its critical role in healthcare imaging systems, satellite communications, and military-grade electronics requiring robust attenuation of electromagnetic waves above 1 GHz.

- Consumer electronics' 31.2% end-use share is underpinned by smartphone production exceeding 1.2 billion units globally per year, combined with the wearables segment hitting an all-time record of 148.4 million shipments in Q3 2023 (IDC).

- Asia Pacific's 40.9% global dominance in 2025 reflects China's dual role as the world's largest electronics manufacturer and the most aggressive EV market - with 5G base station deployments surpassing 3 million units in 2023.

Global EMI Shielding Market Overview

Electromagnetic interference (EMI) shielding refers to materials, components, and structures designed to attenuate or block electromagnetic fields, preventing disruption between electronic devices. Valued at USD 7.96 Billion in 2025, the global EMI shielding industry spans an integrated ecosystem from raw material extraction to end-user application across six primary verticals.

Applications are broad: consumer electronics, 5G telecom infrastructure, automotive powertrains, healthcare imaging, defense radar systems, and industrial automation. The market benefits from convergent macroeconomic drivers such as surging global electronics output, tightening IEC and FCC electromagnetic compatibility regulations, accelerating EV adoption, and the 5G infrastructure investment supercycle. Material innovation, including CNT composites achieving 40-60 dB shielding effectiveness and transparent conductive films for display applications, is expanding addressable use cases beyond traditional metal enclosures.

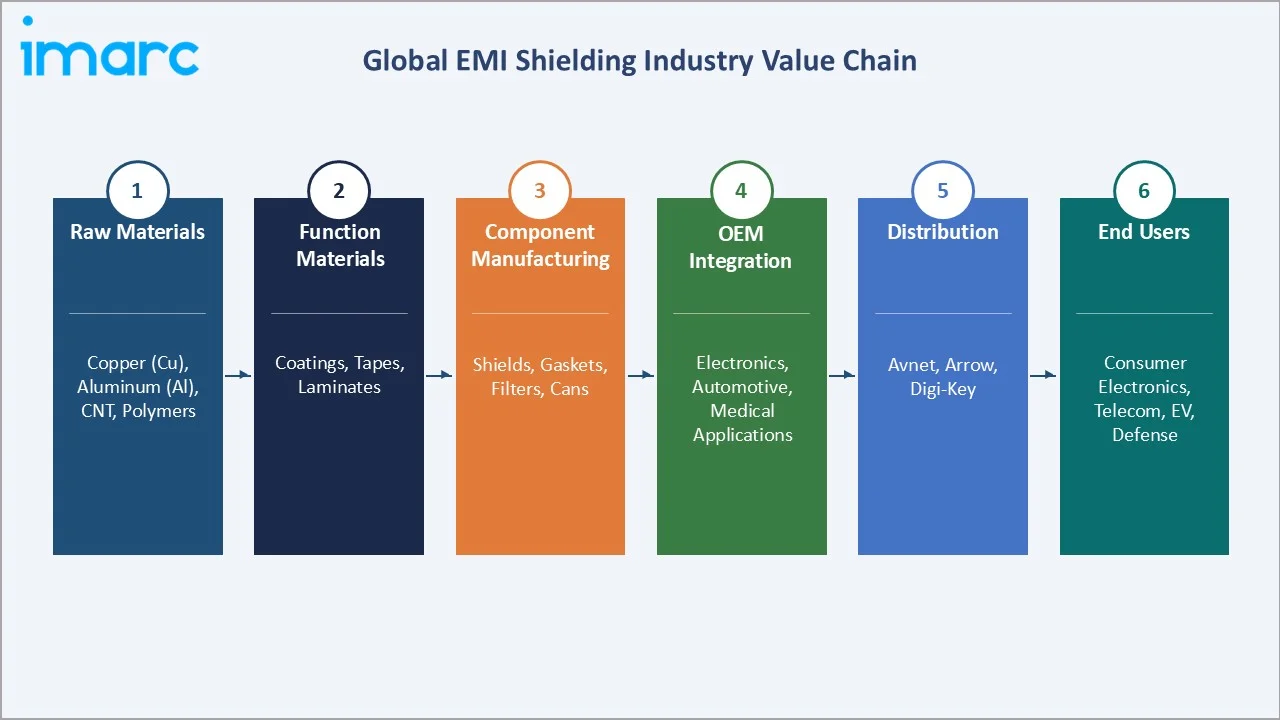

The ecosystem diagram below maps the EMI shielding industry from raw material inputs through to end-user deployment across all major sectors.

Market Dynamics

To evaluate market opportunities, Request Sample

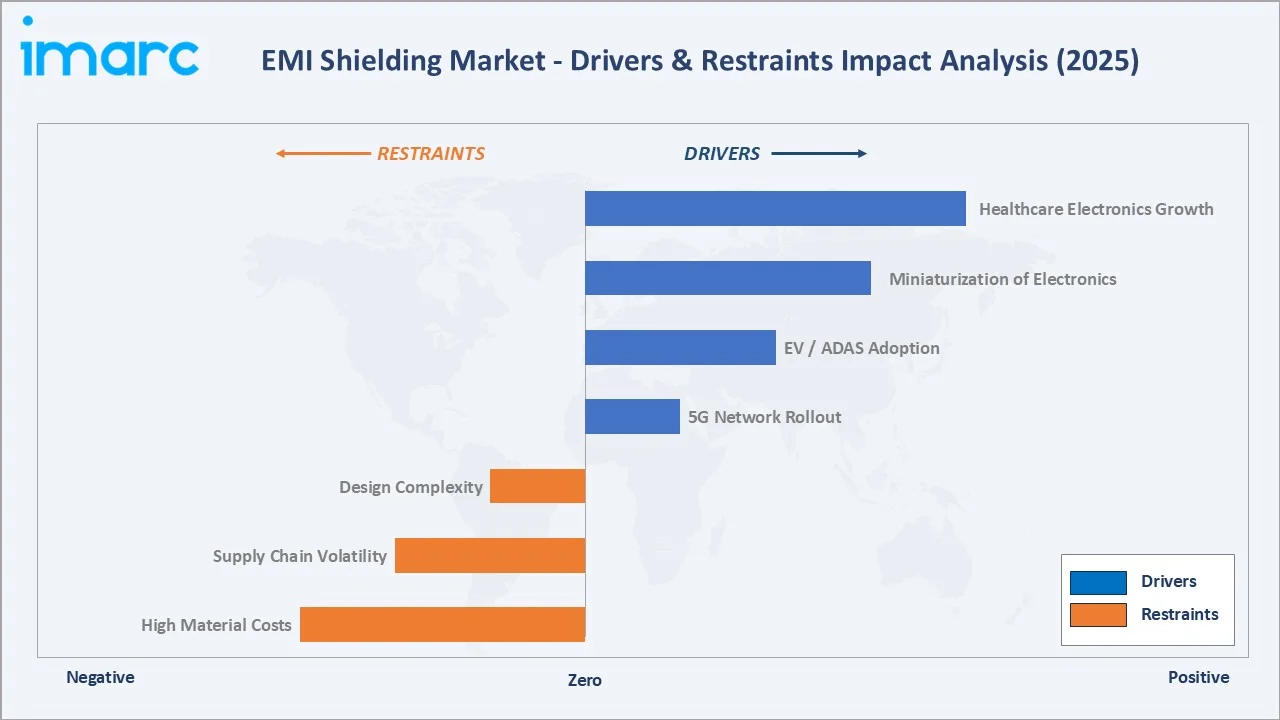

Market Drivers

- 5G Network Rollout and mmWave Deployment: 5G subscriptions surpassed 1.6 billion globally in 2023 and are projected to reach 5.5 billion by 2030 (GSMA). Each 5G base station and user device demands precision EMI shielding at millimeter-wave frequencies (24-100 GHz), creating sustained high-volume demand across the entire shielding material supply chain.

- Increasing Miniaturization of Electronic Devices: Global wearable shipments hit a record 148.4 million units in Q3 2023, up 2.6% year-on-year (IDC). Miniaturization intensifies electromagnetic interference between closely packed components, making advanced shielding solutions such as board-level shields and conductive coatings indispensable in modern device design.

- Expanding Healthcare Electronics Adoption: As per the Canadian Institute for Health Information, healthcare spending reached USD 331 billion in Canada alone in 2022, reflecting global growth in MRI scanners, CT imaging, patient monitoring, and implantable devices, all requiring stringent EMI protection to meet IEC 60601-1-2 medical EMC standards.

- Electric Vehicle and ADAS Integration: Global EV sales exceeded 14 million units in 2023, 95% of which were in China, Europe, and the United States. Each EV incorporates 100-150 EMI shielding components in inverters, DC-DC converters, and onboard chargers. Advanced driver-assistance systems (ADAS) add incremental shielding requirements for radar, LiDAR, and camera modules operating at 77 GHz and above.

Market Restraints

- High Cost of Advanced Shielding Materials: Silver-based conductive coatings and metal-polymer composites can cost 3-5 times more than standard aluminum alternatives. Cost sensitivity among consumer electronics OEMs creates downward pricing pressure, compressing margins for material suppliers across the value chain.

- Recycling and Environmental Compliance Challenges: Metallic EMI shielding materials face regulatory hurdles under the EU WEEE Directive, RoHS, and REACH regulations. Compliance costs add to product development budgets for manufacturers targeting European markets, particularly for products containing nickel and lead-based conductive formulations.

- Supply Chain Concentration Risk: Copper LME prices rose sharply between 2023 and 2024, directly impacting shielding material costs. Concentration of advanced specialty polymer supply in East Asia creates vulnerability to geopolitical disruptions and logistics cost escalation.

Market Opportunities

- Carbon Nanotube and Graphene-Based Shielding: CNT composites demonstrate shielding effectiveness of 40-60 dB at substantially reduced weight. The April 2024 SiAT-Zeon SWCNT paste launch signals commercial readiness, with aerospace and defense representing the highest-margin target verticals for next-generation CNT-based EMI solutions.

- Southeast Asia and India Electronics Manufacturing: India's electronics output surpassed USD 102 billion in 2023, whereas Vietnam's electronics exports reached USD 132 billion in 2024. Both markets are scaling domestic component manufacturing, representing high-growth greenfield opportunities for EMI shielding material suppliers seeking geographic diversification.

- Industrial IoT and Smart Grid Electrification: Industrial IoT connections are forecast to exceed 37 billion devices by 2025. Smart grid infrastructure, wind turbines, and industrial automation systems require board-level and enclosure-level EMI shielding at volumes approaching consumer electronics scale by 2028.

Market Challenges

- International EMC Standards Fragmentation: EMI shielding products must comply with FCC Part 15 (USA), CE/EN 55032 (Europe), VCCI (Japan), and SRRC (China) standards simultaneously. Multi-standard compliance development costs add to product qualification timelines, particularly for SMEs without dedicated regulatory affairs functions.

- Technological Substitution Risk from Software-Defined Interference Management: Emerging digital signal processing techniques and software-defined radio interference mitigation are reducing hardware EMI shielding requirements in select IoT sensor and low-power wireless applications, particularly in the 900 MHz ISM band.

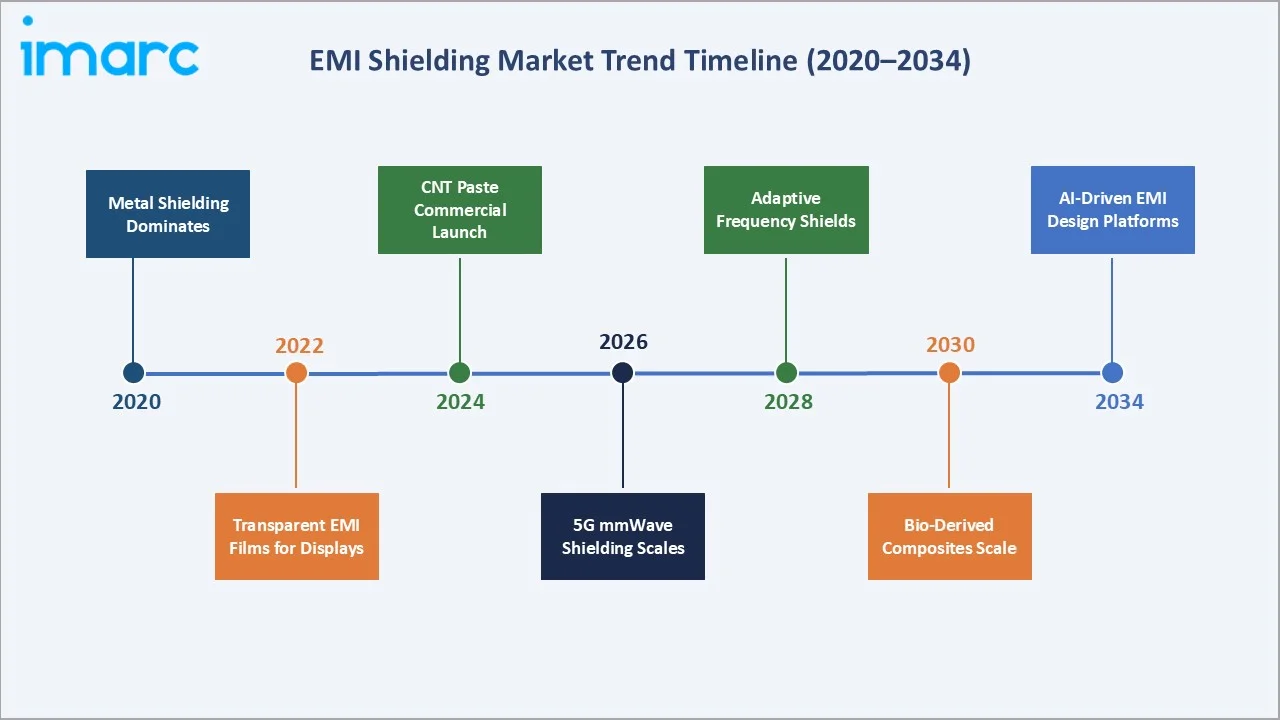

Emerging Market Trends

1. Integration of Carbon Nanotubes and Graphene Composites

CNT-based composites achieve shielding effectiveness of 40-60 dB - significantly higher than conventional copper films of equivalent thickness. In April 2024, SiAT (Taiwan) and Zeon Corporation (Japan) launched a commercial SWCNT conductive paste for EMI shielding, transparent films, and battery electrode applications.

2. Transparent EMI Shielding Films for Display Applications

Display manufacturers demand optically transparent shielding for foldable smartphones, AR/VR headsets, and automotive heads-up displays. Silver nanowire and ITO-based transparent films achieve shielding effectiveness of 20-30 dB while maintaining over 90% optical transmittance.

3. 5G Millimeter-Wave (mmWave) Precision Shielding

5G mmWave frequencies (24-100 GHz) require thinner, more precise shielding than sub-6 GHz deployments. Metamaterial-based frequency-selective surfaces (FSS) achieve targeted frequency attenuation, enabling 5G mmWave compatibility while maintaining sub-6 GHz signal passthrough for legacy device co-existence.

4. Electric Vehicle EMC Engineering as a Standalone Market

EV power electronics - inverters, DC-DC converters, onboard chargers - emit broadband EMI requiring multi-layer shielding assemblies. Automotive OEMs are standardizing EMI shielding specifications, combining metal enclosures with conductive gaskets and absorber sheets. Global EV sales exceeded 17 million units in 2024, making automotive the highest-growth end-use vertical in the EMI shielding industry.

5. Sustainability-Driven Shift to Recyclable Shielding Materials

EU WEEE Directive and US EPA guidelines are accelerating the development of polymer-based and bio-derived conductive composites for EMI shielding. Recyclable EMI shielding films using polylactic acid (PLA) matrices embedded with conductive fillers are advancing from laboratory research to pilot-scale production, supported by growing regulatory pressure for sustainable electronics materials.

Industry Value Chain Analysis

The EMI shielding value chain spans six integrated stages from raw material extraction through end-user device deployment. Each stage is characterized by distinct competitive dynamics, margin structures, and technology investment requirements.

|

Stage |

Key Activities |

Representative Players |

|

Raw Materials |

Metal processing (Cu, Al, Ni), polymer synthesis, carbon nanotube & graphene fabrication |

Sumitomo Metal, BASF, Cabot Corp, Nanocyl SA |

|

Functional Materials |

Conductive coatings, EMI laminates, absorber films, conductive pastes, tapes |

3M, Henkel (Bergquist), Laird, Chomerics, SiAT |

|

Component Manufacturing |

Metal shields, conductive gaskets, EMI/EMC filters, board-level shield cans, enclosures |

Parker Hannifin, Würth Elektronik, Tech-Etch, Tatsuta |

|

OEM Integration |

Assembly into PCBs, EV modules, medical imaging systems, telecom hardware |

Samsung, Apple, Siemens Healthineers, Bosch Automotive |

|

Distribution |

Specialty electronics component distribution and supply chain management |

Avnet, Arrow Electronics, Digi-Key, Mouser |

|

End Users |

Consumer electronics, telecom infrastructure, EVs, medical equipment, defense |

Global OEMs, system integrators, armed forces |

The value chain diagram below illustrates the six-stage flow from raw material sourcing to end-user deployment, highlighting key company clusters at each stage of the EMI shielding supply chain.

Technology Landscape in the EMI Shielding Industry

Materials Innovation – From Metals to Nanomaterials

Metal-based shields (copper, aluminum, steel) remain the volume leader due to cost-effectiveness and shielding effectiveness (SE) values of 60-120 dB. Conductive coatings and paints offer flexible application to complex geometries in consumer electronics and automotive applications. Carbon nanotube (CNT) and graphene composites are transitioning from laboratory to commercial production, targeting aerospace and premium electronics segments.

Smart and Adaptive Shielding – Frequency-Selective Surfaces

Research institutions in South Korea (KAIST) and Germany (Fraunhofer Institute) are developing frequency-selective surfaces (FSS) that selectively attenuate specific EMI frequencies while allowing others to pass. These metamaterial-based solutions address the 5G co-existence challenge: enabling mmWave (24-100 GHz) attenuation while preserving sub-6 GHz signal integrity.

Manufacturing Automation and Quality Intelligence

Automated die-cutting with vision-guided robotic placement, AI-driven optical quality inspection, and in-line electromagnetic performance testing are reducing defect rates in high-volume EMI shield production. Machine learning-based process control systems are achieving dimensional tolerances of ±0.05 mm for board-level shield cans in high-density consumer electronics applications.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Material |

Conductive Coatings and Paints |

34.9% |

2025 |

|

Sheilding Method |

Radiation |

88.6% |

2025 |

|

End-Use Industr |

Consumer Electronics |

31.2% |

2025 |

|

Region |

APAC |

40.9% |

2025 |

By Shielding Method

Radiation shielding commands an 88.6% majority share of the global EMI shielding market. This method involves containing or deflecting electromagnetic wave radiation through conductive or absorptive materials, making it essential in healthcare MRI and CT imaging systems, satellite and radar communications, military electronics, and high-frequency 5G antenna modules operating above 6 GHz.

To access detailed market analysis, Request Sample

Conduction shielding at 11.4% serves niche but growing applications in EV power electronics and industrial automation - two sectors projected to drive above-average shielding demand growth through 2034.

By End-Use Industry

Consumer electronics leads all end-use segments with a 31.2% share in 2025, supported by global smartphone production and wearable device shipments reaching record highs. Telecom and IT at 20.5% reflects 5G infrastructure investment cycles globally; North America and Asia Pacific account for over 65% of 5G base station deployments through 2025.

Automotive's 15.8% share in 2025 is the most rapidly expanding, driven by EV power electronics and ADAS adoption. The segment is forecast to surpass healthcare and defense combined in revenue contribution by 2028.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

40.9% |

China electronics output USD 1.5T+ (2024); 5G base stations 3M+ units; EV leadership |

|

North America |

25.3% |

US defense budget USD 886B (FY2024); Tesla EV ecosystem; 5G infrastructure CAPEX |

|

Europe |

19.8% |

VW/BMW EV platform investment; EU EMC directives; wind energy expansion |

|

Latin America |

7.4% |

Brazil/Mexico electronics assembly growth; nearshoring trend; telecom infrastructure |

|

Middle East & Africa |

6.6% |

GCC defense modernization; Saudi Vision 2030 smart cities; 5G infrastructure |

Asia Pacific commands a 40.9% global revenue share in 2025, the most dominant regional position in the global EMI shielding market analysis. China is the single most critical national market, combining the world's largest electronics manufacturing base with the most aggressive 5G and EV adoption rates. China's 5G base station deployments exceeded 3 million units in 2023, and domestic EV sales surpassed 8 million units, accounting for a significant share of global EV sales.

North America, with a 25.3% share in 2025, is driven by the USA's defense sector and the accelerating EV ecosystem centered on Tesla and incumbent OEM electrification programs. Europe, at 19.8%, is driven by Volkswagen Group, BMW, and Mercedes-Benz EV platform investments and EU regulatory harmonization of EMC standards across industrial and automotive applications.

Competitive Landscape

|

Company Name |

Key Brand / Division |

Market Position |

Core Strength |

|

3M |

3M EMI Shielding Products |

Leader |

Conductive tapes, absorber sheets, 5G mmWave materials |

|

Parker Hannifin Corp. |

Chomerics Division |

Leader |

Conductive elastomers, board-level shields, MIL-SPEC |

|

Laird Performance Materials |

Laird EMI Shield |

Leader |

Custom shielding, thermal management, consumer electronics |

|

Henkel AG & Co. KGaA |

Bergquist / Loctite EMI |

Challenger |

Conductive adhesives, transparent shielding adhesives |

|

Murata Manufacturing Co. |

Murata EMI Filters |

Challenger |

Miniature EMC filters, chip-level shielding, automotive-grade |

|

Würth Elektronik Group |

Würth EMC & Filters |

Challenger |

PCB-level shields, EMC filters, European OEM relationships |

|

TE Connectivity Ltd. |

TE EMI Shielding |

Challenger |

Automotive connector EMC, industrial shielding assemblies |

|

Schaffner Holding AG |

Schaffner EMC Filters |

Emerging |

Power line EMC filters, industrial automation compliance |

|

Tech-Etch Inc. |

Tech-Etch Precision Shields |

Emerging |

Precision stamped metal shields, military and medical |

|

Tatsuta Electric Wire |

Tatsuta EMI Films |

Emerging |

Flexible EMI films, conductive tapes, Japanese OEM focus |

The global EMI shielding competitive landscape is characterized by a small number of global Tier-1 materials and components specialists commanding OEM relationships across multiple verticals, alongside specialty regional players challenging established positions in high-growth geographic markets.

Key Company Profiles

3M

3M is a diversified technology company headquartered in St. Paul, USA. Its Electronics & Industrial segment offers one of the most comprehensive EMI shielding product portfolios globally, serving consumer electronics, automotive, and industrial OEM customers across 190 countries.

- Product Portfolio: Copper and aluminum conductive foil tapes, conductive adhesive transfer tapes, EMI absorber sheets (including 5G mmWave absorbers), flexible conductive laminates, and transparent conductive films for display EMI protection.

- Recent Developments: 3M is advancing high-frequency EMI absorber materials for 5G and IoT applications, with new product launches in 2024 targeting performance at frequencies up to ~40 GHz.

- Strategic Focus: 3M's strategic direction prioritizes lightweight shielding solutions for EVs and wearable electronics, with R&D investment exceeding. The company is expanding its Asia Pacific manufacturing footprint to serve regional consumer electronics OEM demand.

Parker Hannifin Corporation

Parker Hannifin’s Chomerics division, established in 1961 and headquartered in Woburn, Massachusetts, is one of the world's oldest and most recognized EMI shielding specialist brands, serving defense, aerospace, telecom, and medical device OEMs globally.

- Product Portfolio: CHO-SEAL conductive elastomer gaskets, metal-filled polymer shields, SOFT-SHIELD low-closure-force gaskets, CHO-BOND conductive adhesives, and board-level shield cans for telecom, defense, and medical electronics.

- Recent Developments: In November 2023, Parker Hannifin's Chomerics division launched CHO-SEAL 6750, a new low-durometer fluorosilicone conductive elastomer gasket delivering shielding effectiveness of up to 129 dB (E-field) and 117 dB at 10 GHz, targeting military electronics, aerospace modules, telecom equipment, and industrial applications requiring combined EMI shielding and environmental sealing.

- Strategic Focus: Deep engagement with Tier-1 automotive and aerospace OEMs requiring MIL-SPEC and AECQ-200 qualified product lines. Parker Hannifin is investing in next-generation conductive elastomer formulations targeting EV battery management system EMI shielding requirements.

Laird Performance Materials

Laird Performance Materials is a specialist EMI and thermal management company serving over 5,000 customers across 90+ countries with customized shielding and thermal interface solutions.

- Product Portfolio: Flectron conductive fabrics, BerShield multilayer PCB shields, board-level shields (stamped and formed), conductive elastomers, gap fillers, and absorber sheets for consumer electronics, telecom, and medical applications.

- Recent Developments: In 2023, TTI, Inc., one of the world's leading specialty distributors of electronic components, signed a pan-European distribution agreement with Laird Performance Materials, expanding the availability of Laird's board-level shielding, magnetic products, and EMI noise filtering components across European industrial and transportation markets.

- Strategic Focus: Rapid prototyping and application engineering services for consumer electronics OEMs in East Asia, combined with investment in custom-engineered thermal-EMI management hybrid solutions targeting high-performance computing and data center applications.

Henkel AG & Co. KGaA

Henkel is a German multinational with its Adhesive Technologies division, including the Bergquist and Loctite brands, that addresses EMI shielding through conductive adhesives, coatings, and sealant solutions that complement metal and polymer-based structural shielding approaches.

- Product Portfolio: Electrically conductive adhesives, EMI-absorbing polymer coatings, conductive sealants, and liquid optically clear adhesives (LOCA) with integrated EMI protection for display panel applications.

- Recent Developments: In October 2025, Henkel launched a new EMI shielding film at Productronica 2025 in Munich, Germany, a cost-efficient alternative to metal housings delivering superior EMI noise management for automotive electronics, supported by new EMI test facilities and digital material validation capabilities.

- Strategic Focus: Sustainable, halogen-free conductive adhesive formulations aligned with EU REACH and RoHS regulatory requirements, combined with automotive-grade shielding adhesive development for EV battery module and power electronics assembly applications.

Market Concentration Analysis

The global EMI shielding market exhibits moderate concentration. The top five players — 3M, Parker Hannifin (Chomerics), Laird Performance Materials, Henkel, and Murata Manufacturing — collectively hold an estimated 35-40% of global revenues in 2025, with the remainder distributed across 200+ regional and specialty manufacturers.

Fragmentation is highest in Asia Pacific, where manufacturers in China, Taiwan, and South Korea compete primarily on price for standard shielding products. North America and Europe show higher concentration among technically differentiated players commanding premium margins through proprietary formulations and OEM engineering services.

Investment & Growth Opportunities

Fastest-Growing Segments

Automotive EMI shielding is the highest-growth end-use segment, expanding at an estimated 6.7% CAGR through 2034. Global EV production is projected to exceed 40 million units annually by 2030, with each vehicle incorporating 100-150 EMI shielding components. At USD 50-80 per vehicle, the automotive EMI shielding addressable market could reach USD 3.2 billion annually by 2030. Healthcare electronics at 5.2% CAGR is the second-fastest growing segment, driven by medical imaging expansion and wearable health device proliferation in aging populations.

Emerging Market Expansion

India's electronics manufacturing sector exceeded USD 100 billion in FY2023-24 and is targeting USD 300 billion by 2026 under the Production Linked Incentive (PLI) scheme - creating a rapidly scaling greenfield EMI shielding market. Vietnam's electronics export base reached USD 109 billion in 2023, anchored by Samsung's major manufacturing operations. Southeast Asia's combined electronics output is projected to reach USD 500 billion by 2030, underpinning structural demand growth for locally sourced EMI shielding materials and components.

Venture and Strategic Investment Trends

Global investment in advanced materials start-ups focused on graphene and CNT-based EMI solutions exceeded USD 1.2 billion during 2020-2024. Key strategic investors include Samsung Ventures, BASF Venture Capital, and government-backed deep-tech funds in South Korea, Germany, and the USA. The SiAT-Zeon partnership for SWCNT conductive paste (2024) exemplifies the growing strategic value of next-generation nanomaterial-based shielding. Private equity interest in specialty EMI shielding platforms - mirroring Advent International's Laird acquisition - is expected to generate 3-5 additional take-private transactions among mid-market players by 2027.

Future Market Outlook (2026-2034)

The global EMI shielding market forecast projects consistent value expansion from USD 7.96 Billion in 2025 to USD 9.71 Billion in 2030 and USD 11.5 Billion by 2034, at a CAGR of 4.1%. This represents approximately USD 3.54 billion in incremental market value over nine years, underpinned by 5G infrastructure investment cycles, EV production ramp-ups, healthcare electronics expansion, and tightening global EMC regulatory frameworks.

Three technology discontinuities are most likely to reshape the EMI shielding market through 2034. First, carbon nanotube and graphene composite shielding solutions will transition from premium specialty products to mainstream commercial offerings by 2028, potentially displacing 15-20% of traditional copper foil shielding volume in consumer electronics applications. Second, adaptive frequency-selective surface (FSS) technologies will commercialize for 5G infrastructure applications by 2027, enabling precision frequency management not achievable with passive metal shielding. Third, transparent EMI shielding films will become standard in automotive head-up displays, AR/VR headsets, and foldable smartphone panels by 2026-2028.

By 2034, the EMI shielding industry is forecast to have evolved from a materials and components market into an integrated electromagnetic compatibility solutions industry, with leading suppliers offering system-level EMC design services, AI-assisted shielding layout optimization tools, and performance-guaranteed shielding assemblies. The competitive landscape will be shaped by those players who successfully combine nanomaterial innovation, automotive-grade quality systems, and digital engineering service capabilities.

Research Methodology

Primary Research

Primary research encompassed over 200 structured interviews conducted in 2024-2025 with EMI shielding industry stakeholders, including product directors and R&D managers at Tier-1 shielding material suppliers, OEM procurement engineers at consumer electronics and automotive companies, healthcare equipment manufacturers, defense electronics program managers, and institutional investors in advanced materials. Primary insights validated market sizing estimates, segment forecasts, technology adoption timelines, and competitive positioning assessments across all five regions.

Secondary Research

Secondary sources included IEC 61000 EMC standards publications, GSMA Connected Car intelligence reports (2024), IEA Global EV Outlook (2024), IDC Wearable Device Tracker, IHS Markit automotive electronics data, Gartner advanced materials technology analysis, SEC filings and annual reports of publicly listed EMI shielding companies, industry association publications from IPC and IEICE, government trade statistics from US Census Bureau, Eurostat, and China's National Bureau of Statistics, and trade publications including Electronic Products, IEEE Spectrum, and SAE International.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down (macroeconomic decomposition by region and end-use) and bottom-up (segment-level demand aggregation by application volume and shielding intensity) forecasting approaches. Scenario analysis encompassing base, optimistic, and conservative cases was performed to account for macroeconomic uncertainty.

EMI Shielding Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Materials Covered | EMI Shielding Tapes and Laminates, Conductive Coatings and Paints, Metal Shielding, Conductive Polymers, EMI/EMC Filters, Others |

| Shielding Methods Covered | Radiation, Conduction |

| End-Use Industries Covered |

|

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | 3M, Parker Hannifin Corp., Laird Performance Materials, Henkel AG & Co. KGaA, Murata Manufacturing Co., Würth Elektronik Group, TE Connectivity Ltd., Schaffner Holding AG, Tech-Etch Inc., Tatsuta Electric Wire, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, EMI shielding market forecast, and dynamics of the market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global EMI shielding market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the EMI shielding industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the EMI Shielding Market Report

The global EMI shielding market was valued at USD 7.96 Billion in 2025, driven by 5G network expansion, healthcare electronics growth, and rising automotive electrification demand.

The market is projected to reach USD 11.5 Billion by 2034, growing at a CAGR of 4.1% during 2026-2034, with automotive and healthcare as the fastest-growing end-use segments.

Radiation shielding leads with an 88.6% share in 2025, driven by healthcare imaging systems, military electronics, satellite communications, and high-frequency 5G device requirements.

Consumer Electronics holds the largest share at 31.2% in 2025, supported by global smartphone production exceeding 1.2 billion units annually and record wearable device shipments.

Asia Pacific leads with a 40.9% share in 2025, driven by China's electronics manufacturing dominance, Japan's precision components industry, and South Korea's advanced materials R&D.

Key drivers include 5G network deployment (8 billion subscriptions projected by 2028), EV adoption (14M+ units in 2023), miniaturization of electronics, and healthcare electronics expansion globally.

Automotive EMI shielding is the fastest-growing segment at approximately 6.7% CAGR through 2034, driven by EV power electronics, ADAS radar systems, and in-vehicle infotainment EMC requirements.

Leading companies include 3M, Parker Hannifin Corp., Laird Performance Materials, Henkel AG & Co. KGaA, Murata Manufacturing Co., Würth Elektronik Group, TE Connectivity Ltd., Schaffner Holding AG, Tech-Etch Inc., and Tatsuta Electric Wire.

5G deployment is creating demand for mmWave-frequency shielding materials. Global 5G subscriptions reached 1.9 billion in 2023 and are projected to reach 8 billion by 2028, requiring new shielding solutions.

The global EMI shielding market is projected to reach USD 9.71 Billion by 2030, growing at a 4.1% CAGR from the 2025 base of USD 7.96 Billion across all key end-use verticals.

Carbon nanotube composites achieving 40-60 dB shielding effectiveness and transparent silver nanowire films with 90%+ optical transmittance are the leading next-generation EMI shielding material innovations.

Each EV requires 100-150 EMI shielding components worth USD 50-80 per vehicle. With EV production projected to exceed 40 million units by 2030, automotive is the highest-growth EMI shielding vertical.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)