Emulsifiers Market Size, Share, Trends and Forecast by Product Type, Source, Application, and Region, 2026-2034

Global Emulsifiers Market Size, Share, Trends & Forecast (2026-2034)

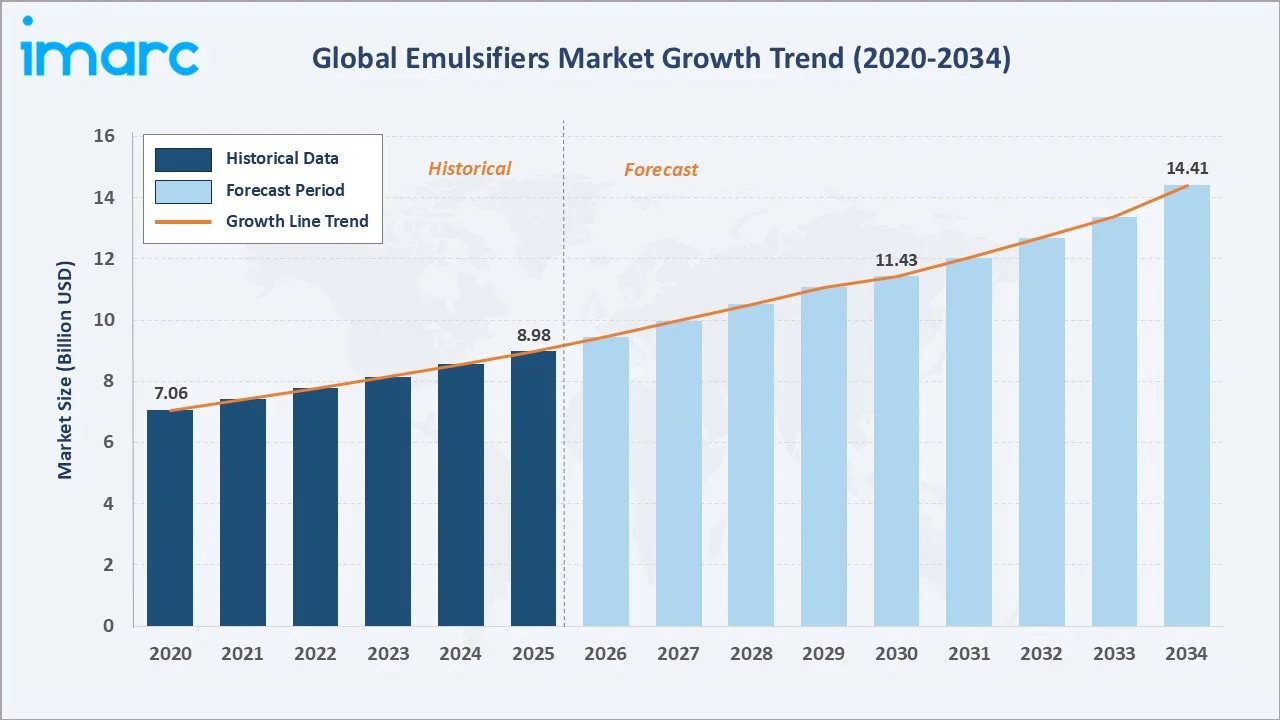

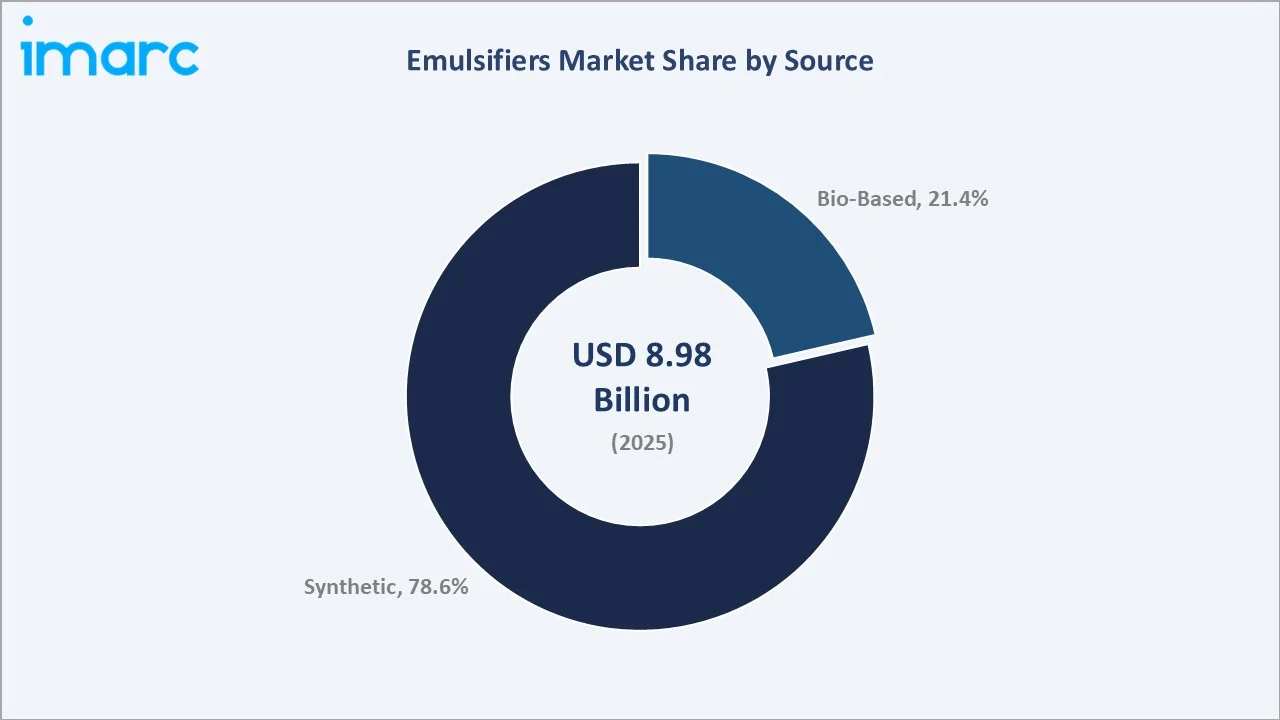

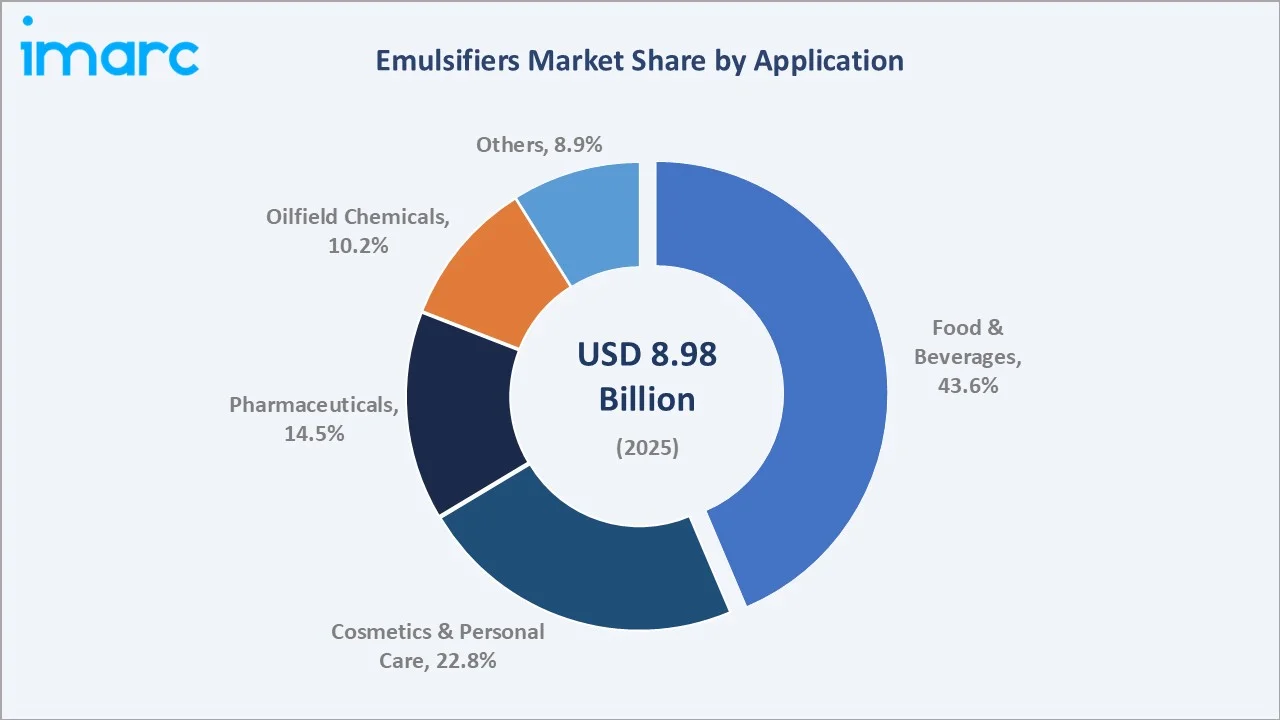

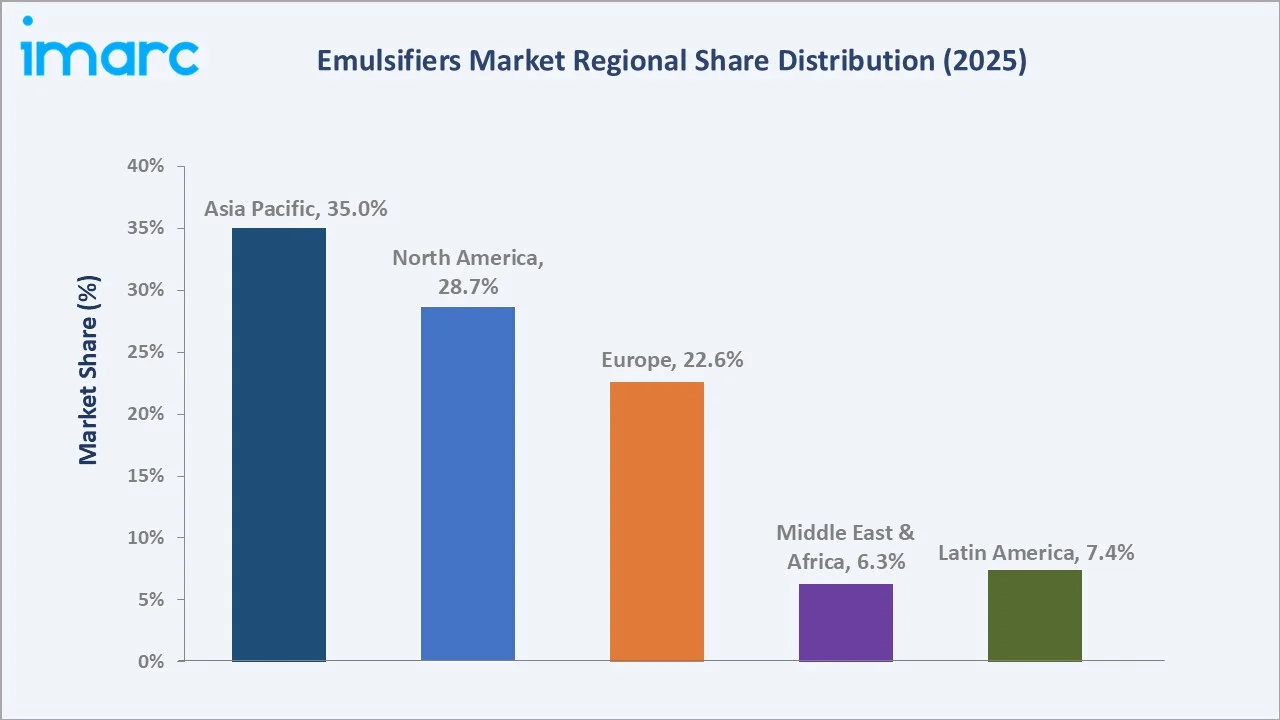

The global emulsifiers market size was valued at USD 8.98 Billion in 2025 and is projected to reach USD 14.41 Billion by 2034, exhibiting a CAGR of 4.94% during the forecast period 2026-2034. Rising demand for processed foods, rapid expansion of the personal care industry, and growing adoption of bio-based ingredients are driving the emulsifiers market growth. Food and beverages applications lead at 43.6% share in 2025, while synthetic emulsifiers account for 78.6% of global source demand. Asia Pacific dominates with 35.0% of global revenue in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 8.98 Billion |

|

Forecast Market Size (2034) |

USD 14.41 Billion |

|

CAGR (2026-2034) |

4.94% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (35.0% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~5.7%) |

|

Leading Source |

Synthetic (78.6%, 2025) |

|

Leading Application |

Food & Beverages (43.6%, 2025) |

The global emulsifiers market growth trajectory from 2020 through 2034 reflects sustained expansion powered by packaged food consumption, personal care premiumization, and the accelerating shift toward bio-based and clean-label ingredient portfolios.

To get more information on this market, Request Sample

Segment-level CAGR comparisons highlight bio-based source adoption and cosmetics application expansion as the fastest-growing sub-categories within the global emulsifiers market forecast through 2034.

Executive Summary

The global emulsifiers market is undergoing sustained transformation. It is driven by packaged food consumption, personal care expansion, and the strategic migration toward bio-based ingredient systems. Valued at USD 8.98 Billion in 2025, the market is forecast to reach USD 14.41 Billion by 2034 at a CAGR of 4.94%.

Synthetic emulsifiers command 78.6% share in 2025, driven by cost efficiency and technical performance in oilfield chemicals and industrial applications. Food and beverages represent 43.6% of global demand, while cosmetics and personal care is the second-largest application at 22.8% and growing at an estimated CAGR of 5.5% through 2030. Bio-based emulsifiers represent the premium growth tier, with increasing adoption across food and personal care as clean-label demand intensifies.

Asia Pacific leads with 35.0% global revenue share in 2025. North America holds 28.7% and Europe 22.6%. The emulsifiers market outlook remains positive as processed food demand, sustainable ingredient sourcing, and pharmaceutical formulation innovation converge across all major markets.

Key Market Insights

|

Insight |

Data |

|

Largest Source |

Synthetic – 78.6% share (2025) |

|

Fastest Growing Source |

Bio-Based – ~6.7% CAGR (2026-2034) |

|

Largest Application |

Food & Beverages – 43.6% share (2025) |

|

Second Application |

Cosmetics & Personal Care – 22.8% share (BaseYear}) |

|

Leading Region |

Asia Pacific – 35.0% revenue share (2025) |

|

Top Companies |

ADM, BASF, Cargill, DSM, Evonik, Kerry, Palsgaard |

Key Analytical Observations Supporting the Above Data:

- Synthetic's 78.6% dominance in 2025 reflects cost advantages and superior technical performance in large-volume applications such as oilfield chemicals, industrial surfactants, and price-sensitive food formulations in emerging markets.

- Bio-Based's 21.4% share is expanding at approximately 6.7% CAGR through 2034, significantly outpacing synthetic growth, driven by clean-label demand and the accelerating reformulation of global consumer-goods portfolios toward plant-derived ingredients.

- Food & Beverages' 43.6% majority is underpinned by global packaged food consumption exceeding USD 3.9 Trillion in 2024, with bakery, dairy, confectionery, and processed meat categories driving the largest share of emulsifier volume demand worldwide.

- Cosmetics & Personal Care's 22.8% share is rising quickly, supported by the global premium skincare market surpassing USD 180 Billion in 2024 and growing demand for natural cream, lotion, and serum formulations across developed and emerging markets.

- Asia Pacific's 35.0% global dominance reflects China's expanding processed food and personal care industries and India's FSSAI-regulated food additive framework, which is lifting structured emulsifier procurement across organized retail channels.

- Pharmaceutical emulsifier demand reached approximately USD 5.4 Billion in 2025, driven by rising injectable biologics, topical formulations, and the growing adoption of lipid-based drug delivery systems for oral and transdermal therapeutics.

Global Emulsifiers Market Overview

Emulsifiers are surface-active agents that stabilize mixtures of two immiscible phases, typically oil and water. The global market spans a broad portfolio including lecithin, mono- and di-glycerides of fatty acids, esters of monoglycerides, polysorbates, polyglycerol esters, polyglycerol polyricinoleate (PGPR), and lactic esters of fatty acids. These ingredients are derived from bio-based feedstocks such as soybean, sunflower, rapeseed, and palm, as well as from synthetic petrochemical routes.

The industry operates at the intersection of consumer goods manufacturing, ingredient sustainability, regulatory compliance, and formulation innovation. Growth is supported by macro drivers such as global processed-food consumption, personal care premiumization, and rising pharmaceutical R&D investment. At the same time, the market is undergoing a structural shift toward plant-based, non-GMO, and enzymatically produced emulsifiers, reshaping procurement and capital investment decisions for global ingredient suppliers.

Market Dynamics

To evaluate market opportunities, Request Sample

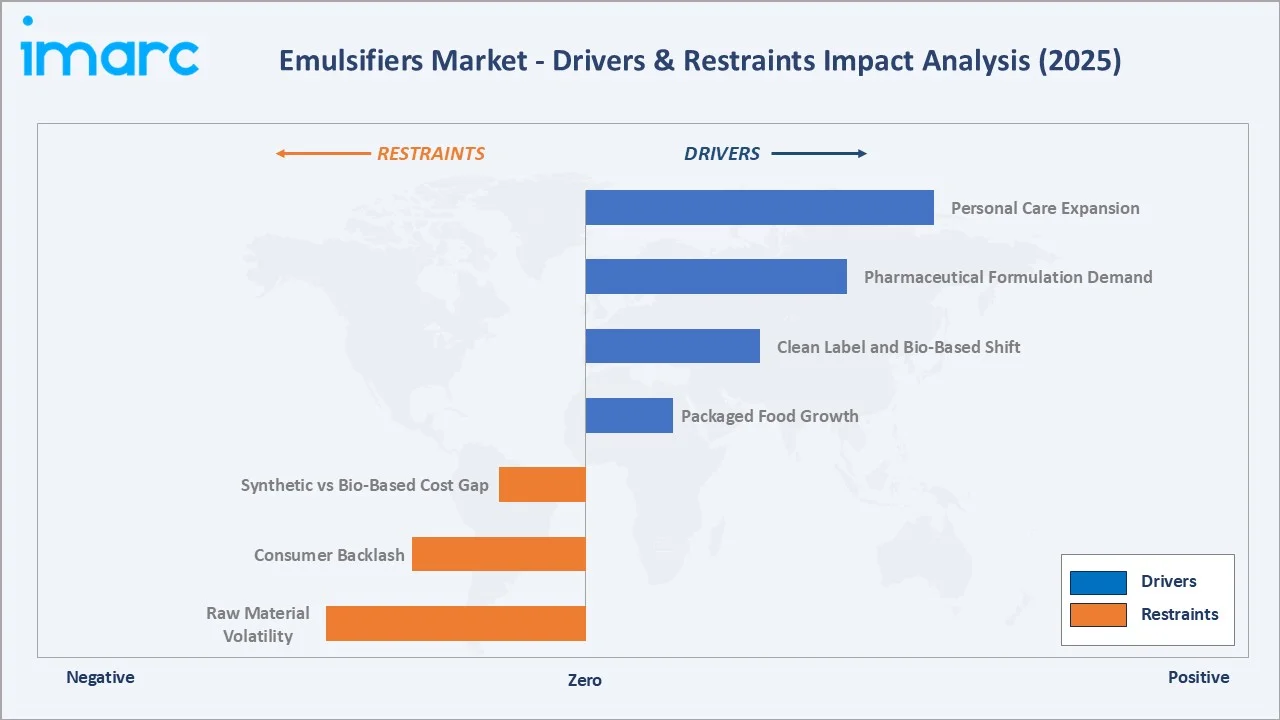

Market Drivers

- Packaged Food Growth: Global packaged food sales exceeded USD 3.9 Trillion in 2024, per Euromonitor, with bakery, dairy, confectionery, and ready meals driving sustained emulsifier volume demand. Rising urbanization and dual-income households across Asia Pacific and Latin America are structurally lifting processed food consumption.

- Clean Label and Bio-Based Shift: Consumer demand for natural, plant-derived, and non-GMO ingredients is reshaping product portfolios. Bio-based emulsifier sales are growing at approximately 6.7% CAGR, with lecithin, mono- and di-glycerides from palm and sunflower, and enzymatically produced variants leading adoption in developed markets.

- Personal Care Expansion: The global cosmetics and personal care market surpassed USD 350 Billion in 2024. Premium skincare, natural cosmetics, and multifunctional formulations require specialized emulsifiers such as polyglycerol esters and PEG-free systems, driving value growth in the segment.

- Pharmaceutical Formulation Demand: Emulsifier use in pharmaceuticals reached approximately USD 1.30 Billion in 2025. Rising injectable biologics, lipid nanoparticles for mRNA vaccines, and topical dermatology formulations are expanding demand for pharma-grade polysorbates, lecithin, and purified PEG derivatives.

Market Restraints

- Synthetic vs Bio-Based Cost Gap: Bio-based emulsifiers remain 25-60% more expensive than synthetic counterparts, limiting adoption in cost-sensitive industrial and emerging-market food applications despite strong consumer preference.

- Raw Material Volatility: Palm oil, soybean oil, and petrochemical feedstock price swings directly inflate production costs. Palm oil prices ranged from USD 700 to USD 1,100 per tonne in 2024, creating margin pressure across bio-based supply chains.

- Consumer Backlash: Negative perception of certain emulsifiers such as polysorbate 80 and carboxymethyl cellulose, fueled by recent gut-health research, is prompting reformulation pressure among major food brands in Europe and North America.

Market Opportunities

- Enzymatic and Fermentation-Derived Emulsifiers: Advances in enzymatic synthesis and precision fermentation are enabling high-purity, non-GMO, and sustainable emulsifier production. Start-ups and incumbents such as Palsgaard and Evonik are scaling these technologies commercially through 2030.

- Pharma and Nutraceutical Applications: Lipid-based drug delivery, mRNA therapeutics, and nutraceutical emulsions are creating premium demand for high-purity emulsifiers. The global lipid nanoparticle market alone is projected to exceed USD 3.70 Billion by 2034.

Market Challenges

- Regulatory Scrutiny: Evolving regulations on certain emulsifiers such as E471 mono- and di-glycerides and E433 polysorbates, particularly in Europe, force reformulation and limit labeling flexibility for multinational food manufacturers.

- Sustainability and RSPO Compliance: Palm-derived emulsifiers face rising pressure for certified sustainable sourcing. Roundtable on Sustainable Palm Oil (RSPO) compliance adds 8-15% to input costs and requires traceability infrastructure investment.

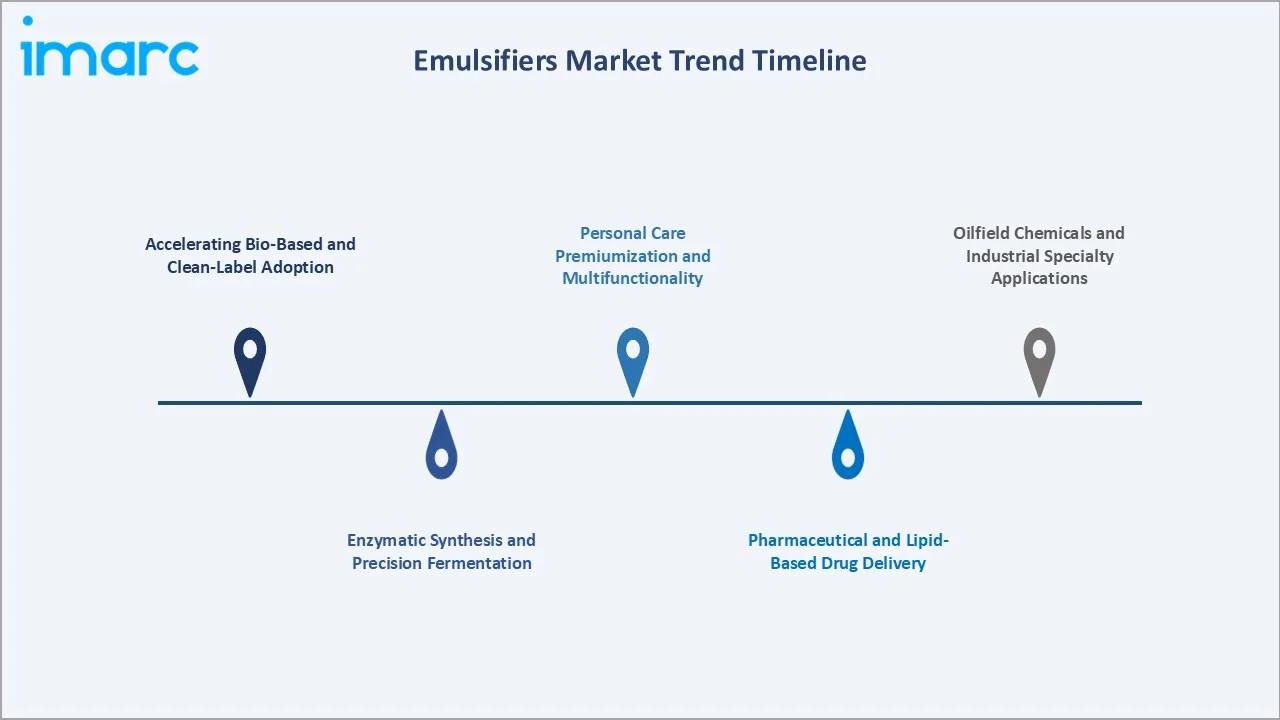

Emerging Market Trends

1. Accelerating Bio-Based and Clean-Label Adoption

Consumer preference for natural and plant-derived ingredients is reshaping procurement. Bio-based emulsifier sales are growing at approximately 6.7% CAGR through 2034, with sunflower lecithin, enzymatically produced mono- and di-glycerides, and PGPR from sustainable palm leading adoption across bakery, confectionery, and dairy categories.

2. Enzymatic Synthesis and Precision Fermentation

Enzymatic interesterification and fermentation-derived emulsifiers are gaining commercial scale. These routes deliver higher purity, lower carbon footprint, and non-GMO positioning. Leading manufacturers such as Palsgaard, Evonik, and Kerry are investing in fermentation-capable sites to serve premium food and personal care portfolios.

3. Personal Care Premiumization and Multifunctionality

The global skincare market exceeded USD 170 billion in 2024, with premium segments contributing a smaller but rapidly growing share, while rising demand for clean-label formulations is driving increased adoption of PEG-free, sulfate-free, and multifunctional emulsifier systems. Manufacturers are launching polyglycerol esters, polymeric emulsifiers, and ECOCERT-compliant variants tailored to natural cosmetics formulators.

4. Pharmaceutical and Lipid-Based Drug Delivery

Pharma-grade emulsifiers are powering the rise of lipid nanoparticles (LNPs) for mRNA therapeutics and vaccines. Polysorbate 80, purified PEG derivatives, and phospholipid-based systems are seeing accelerated demand. Compliance with pharmacopoeial standards and GMP manufacturing is a barrier to entry that favors established suppliers.

5. Oilfield Chemicals and Industrial Specialty Applications

Oilfield emulsifiers play a critical role in drilling fluids, enhanced oil recovery, and crude oil separation processes, with demand strengthening alongside the recovery in upstream oil and gas investment post-2023, particularly in the Middle East and U.S. Permian basin, is sustaining demand for specialty industrial emulsifiers through 2030.

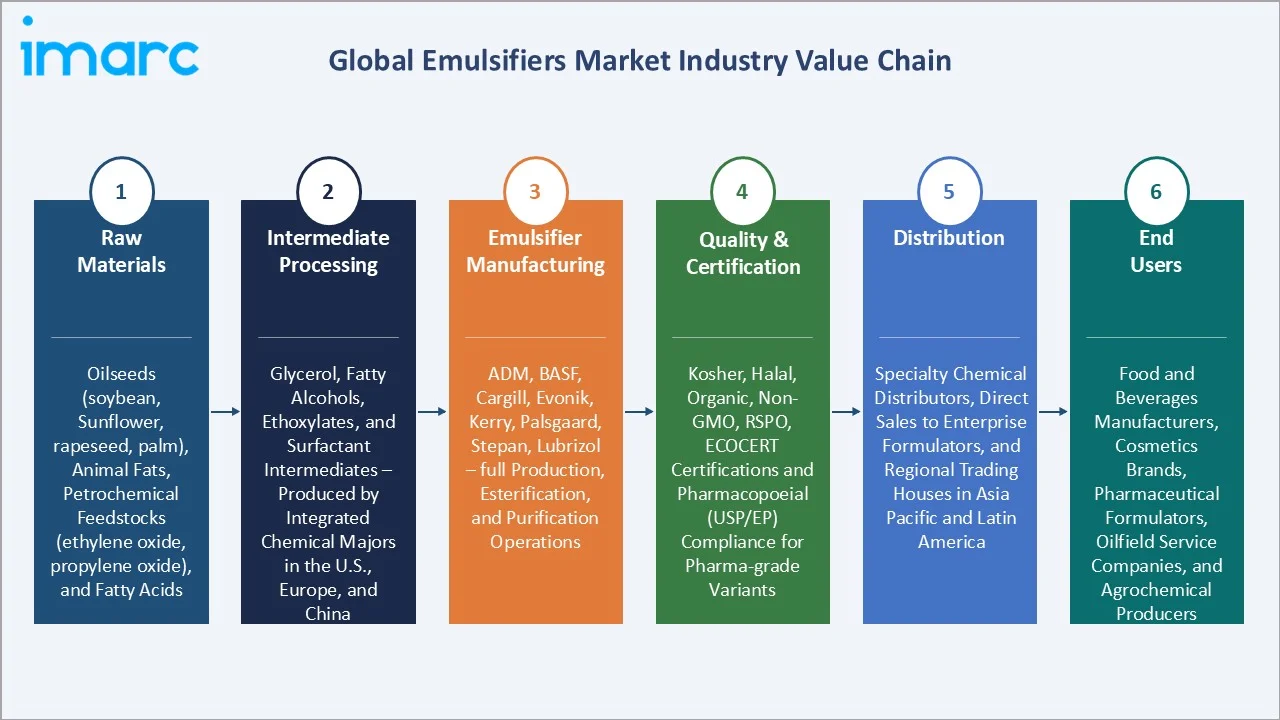

Industry Value Chain Analysis

The global emulsifiers industry value chain spans six integrated stages from raw material supply through end-user application. Each stage presents distinct competitive dynamics, margin profiles, and sustainability investment requirements relevant to the overall emulsifiers market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials |

Oilseeds (soybean, sunflower, rapeseed, palm), animal fats, petrochemical feedstocks (ethylene oxide, propylene oxide), and fatty acids |

|

Intermediate Processing |

Glycerol, fatty alcohols, ethoxylates, and surfactant intermediates – produced by integrated chemical majors in the U.S., Europe, and China |

|

Emulsifier Manufacturing |

ADM, BASF, Cargill, Evonik, Kerry, Palsgaard, Stepan, Lubrizol – full production, esterification, and purification operations |

|

Quality & Certification |

Kosher, halal, organic, non-GMO, RSPO, ECOCERT certifications and pharmacopoeial (USP/EP) compliance for pharma-grade variants |

|

Distribution |

Specialty chemical distributors, direct sales to enterprise formulators, and regional trading houses in Asia Pacific and Latin America |

|

End Users |

Food and beverages manufacturers, cosmetics brands, pharmaceutical formulators, oilfield service companies, and agrochemical producers |

OEM emulsifier manufacturers capture the highest strategic value by integrating upstream raw materials, specialized chemistry, and technical application support into differentiated ingredient solutions. At the same time, distribution partners and formulation specialists are playing an increasingly critical role in helping consumer-goods brands navigate reformulation toward bio-based, clean-label, and sustainability-certified emulsifier systems.

Technology Landscape in the Emulsifiers Industry

Chemical Esterification and Synthesis

Conventional esterification continues to dominate mono- and di-glyceride, polysorbate, and PEG ester production. High-throughput reactor technology, continuous-flow synthesis, and advanced purification are improving yield and consistency. Leading manufacturers such as BASF, Evonik, and Stepan are investing in next-generation process intensification to improve carbon footprint and cost efficiency.

Enzymatic and Fermentation-Derived Routes

Enzymatic interesterification and lipase-catalyzed synthesis enable milder reaction conditions, higher purity, and non-GMO labeling. Palsgaard and Kerry have scaled enzymatic mono- and di-glyceride production. Precision fermentation start-ups are developing microbial-derived lecithin and surfactants, targeting commercial scale through 2027-2030.

Sustainable Sourcing and RSPO Compliance

Sustainable palm oil certification is a strategic imperative. RSPO-certified sourcing, including segregated and mass-balance supply chains, is widely adopted across Europe, supported by strong regulatory and corporate sustainability commitments in palm-based ingredient procurement. Leading suppliers are publishing traceable supply chain disclosures and investing in smallholder programs across Indonesia, Malaysia, and Colombia.

Pharma-Grade Purification and GMP Manufacturing

Pharmaceutical emulsifiers require GMP-compliant facilities, ultra-low endotoxin limits, and pharmacopoeial compliance. Croda, Lubrizol, and NOF Corporation lead high-purity polysorbate, PEG, and phospholipid production. mRNA lipid nanoparticle demand during and after the COVID-19 pandemic has structurally lifted pharma-grade capacity expansion investment.

Market Segmentation Analysis

IMARC Group provides an analysis of the key trends in each segment of the global emulsifiers market, along with forecasts at the global, regional, and country levels from 2026 to 2034. The market has been categorized based on source and application.

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | Mono & Di-glycerides of Fatty Acids | 48.7% | 2025 |

| Source | Synthetic | 78.6% | 2025 |

| Application | Food and Beverages | 43.6% | 2025 |

| Region | Asia Pacific | 35.0% | 2025 |

By Source

Synthetic emulsifiers lead the global market with a 78.6% share in 2025. Demand is driven by cost efficiency, technical performance, and large-volume use in oilfield chemicals, industrial surfactants, and price-sensitive food applications. The global synthetic sub-segment was valued at approximately USD 7.2 Billion in 2025 and is projected to grow at 22% CAGR through 2030. Polysorbates, PEG esters, and synthetic mono- and di-glycerides dominate this tier.

To access detailed market analysis, Request Sample

Bio-Based emulsifiers account for 21.4% of global source demand. This segment is the fastest-growing at an estimated CAGR of 6.7% through 2034, significantly outpacing synthetic growth. Growth is driven by clean-label consumer demand, sustainability mandates, and reformulation commitments from major food and personal care brands. Lecithin from sunflower and soy, enzymatically produced mono- and di-glycerides, and PGPR from certified sustainable palm lead bio-based adoption.

By Application

Food and Beverages leads the global emulsifiers market with a 43.6% share in 2025. Global packaged food sales exceeded USD 3.3 Trillion in 2024, driving emulsifier demand across bakery, dairy, confectionery, processed meat, sauces, and beverage categories. The global food and beverages sub-segment is projected to grow at 5.1% CAGR through 2030. Bakery and dairy represent the largest category-level volume drivers within this application.

Cosmetics and Personal Care Products account for 22.8% of global demand and are among the fastest-growing segments, expanding at approximately 5.5% CAGR through 2030, driven by premium skincare, natural cosmetics, and multifunctional formulation demand. Pharmaceuticals represent 14.5% share, powered by lipid-based drug delivery and injectable biologics. Oilfield Chemicals account for 10.2% share, while the Others segment (8.9%) includes agrochemicals, paints and coatings, and specialty industrial applications.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

35.0% |

China processed food scale, India FSSAI framework, ASEAN personal care growth, Japan pharma innovation |

|

North America |

28.7% |

U.S. packaged food scale, Canada clean-label demand, Mexico cosmetics, pharma LNP expansion |

|

Europe |

22.6% |

EU clean-label regulation, bio-based mandates, Germany and France pharma R&D, RSPO leadership |

|

Latin America |

7.4% |

Brazil processed food expansion, Mexico exports, Argentina personal care, agrochemical demand |

|

Middle East & Africa |

6.3% |

GCC packaged food imports, South Africa cosmetics, oilfield chemical demand, infrastructure growth |

Asia Pacific commands 35.0% global revenue share in 2025. China is the single largest national market, combining rapid processed food growth with a booming personal care industry. India's Food Safety and Standards Authority (FSSAI) framework is structuring food additive procurement across organized retail, creating a large and stable pipeline for certified emulsifier demand. Asia Pacific is also forecast to be the fastest-growing region, advancing at approximately 5.7% CAGR through 2034.

North America holds 28.7% of global revenue, anchored by U.S. packaged food and personal care industries. The U.S. is the world's largest pharma-grade emulsifier market, with lipid nanoparticle demand for mRNA therapeutics sustaining premium pricing. Clean-label reformulation across major CPG brands is lifting bio-based emulsifier demand across Kroger, Walmart, and Whole Foods supplier networks.

Europe holds 22.6%, characterized by strict clean-label regulation, RSPO leadership, and robust pharmaceutical R&D activity in Germany, France, and the UK. The EU's Farm to Fork strategy is accelerating bio-based ingredient adoption across European food brands. Latin America accounts for 7.4%, led by Brazil and Mexico through processed food expansion and personal care growth. The Middle East and Africa represent 6.3%, driven by GCC food imports, oilfield chemical demand, and South African cosmetics consumption.

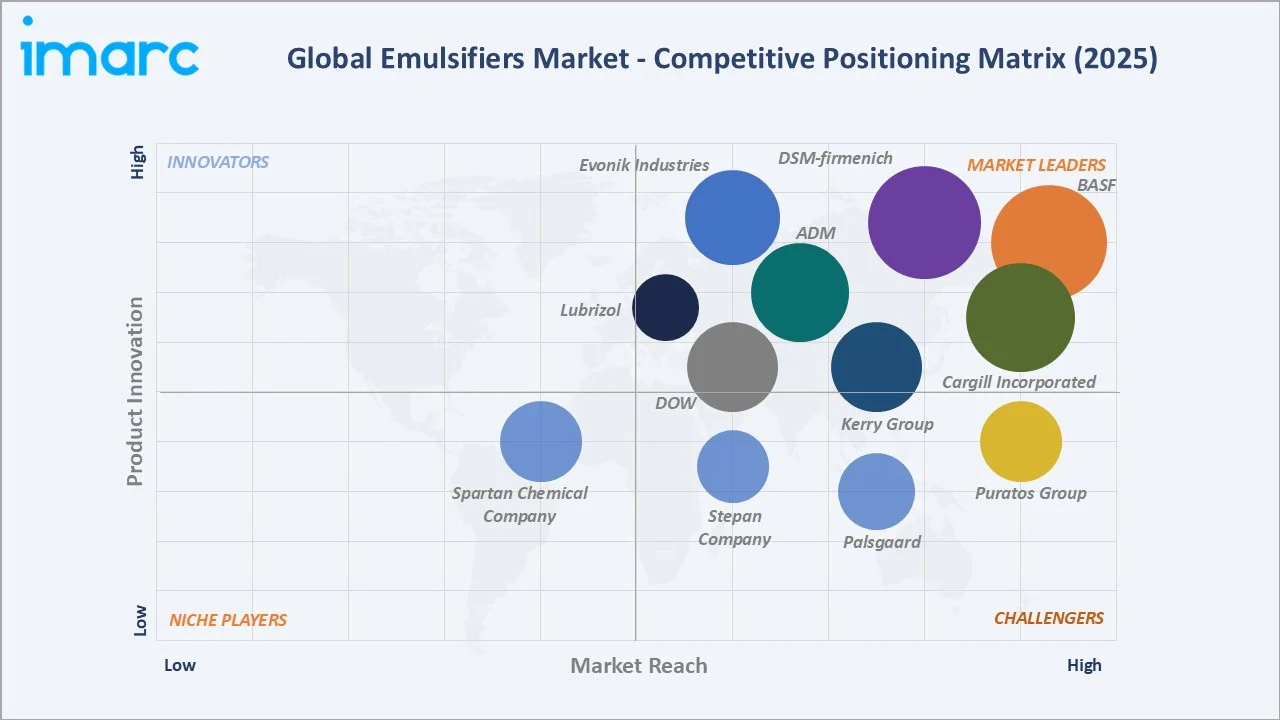

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

BASF |

Emulan, Emulgade, Emulphor |

Leader |

Broad surfactant portfolio, global scale, R&D leadership |

|

Cargill Incorporated |

Topcithin, Star Design Power |

Leader |

Lecithin and plant-based ingredient leadership |

|

ADM |

ADM Emulsifiers |

Leader |

Oilseed integration, food and nutrition scale |

|

DSM-firmenich |

dsm-firmenich |

Leader |

Specialty nutrition, pharma-grade capabilities |

|

Evonik Industries |

Isolan |

Leader |

Personal care surfactants, specialty chemistry |

|

xKerry Group plc |

Admul, Myverol |

Leader |

Taste and nutrition solutions, food industry depth |

|

DOW |

Ecosense, Vorasurf |

Leader |

Industrial surfactants, oilfield chemicals scale |

|

Lubrizol |

Pemulen |

Leader |

Specialty personal care polymers, pharma |

|

Palsgaard |

Palsgaard Emulsifiers |

Challenger |

Sustainable palm, enzymatic leadership |

|

Puratos Group |

Puratos |

Challenger |

Bakery specialty focus, artisanal positioning |

|

Stepan Company |

Polystep |

Challenger |

Global surfactants, agricultural chemicals |

|

Spartan Chemical Company |

Shineline |

Emerging |

Industrial and institutional cleaning specialty |

The global emulsifiers market's competitive landscape is moderately consolidated. Global ingredient majors with integrated surfactant chemistry compete alongside specialty food emulsifier producers and regional specialists. Leading players compete on product breadth, sustainability credentials, technical application support, and bio-based innovation. Strategic acquisitions are a key tool - in 2024, several leading ingredient majors expanded their bio-based emulsifier portfolios through targeted M&A and capacity additions.

Key Company Profiles

Archer Daniels Midland Company

Archer Daniels Midland Company (ADM), headquartered in Chicago, Illinois, is one of the world's largest agricultural processors and ingredient solutions providers. Founded in 1902, ADM operates more than 450 crop procurement facilities and 270 ingredient manufacturing plants across 200 countries.

- Product & Platform Portfolio: ADM's emulsifier portfolio covers lecithin (soy, sunflower, canola), mono- and di-glycerides of fatty acids, and specialty emulsifier blends marketed through its Nutrition business. Brands include Topcithin and ADM Specialty Ingredients targeting food, personal care, and nutrition formulators.

- Recent Developments: In 2024, ADM continued to expand its specialty ingredient portfolio through investments in plant-based protein, flavors, and bio-based emulsifier capacity. The company also advanced its non-GMO sunflower lecithin offering in response to European clean-label demand across its major customer base.

- Strategic Focus: ADM's strategy focuses on scaling its Nutrition segment, expanding bio-based and plant-derived emulsifier capacity, deepening customer co-development partnerships, and leveraging its global oilseed procurement network for supply security and sustainability.

BASF

BASF, headquartered in Ludwigshafen, Germany, is the world's largest chemical company. Founded in 1865, BASF operates six Verbund sites and more than 390 additional production sites worldwide, serving food, personal care, pharmaceutical, and industrial emulsifier markets through its Care Chemicals and Nutrition segments.

- Product & Platform Portfolio: BASF's emulsifier portfolio spans the Lameform, Dehymuls, Emulgade, Tween (polysorbates), and Cremophor product lines, covering O/W and W/O emulsifiers, PEG-free systems, and pharmaceutical-grade surfactants for global formulators.

- Recent Developments: In 2024, BASF advanced its sustainability-aligned product portfolio with expanded MassBal biomass-balance and RSPO-certified emulsifier offerings. The company also invested in process intensification at European Care Chemicals sites to improve carbon footprint and yield.

- Strategic Focus: BASF's strategy centers on sustainability-aligned emulsifier innovation, expanding its Verbund-integrated surfactant platform, deepening personal care and pharma customer relationships, and accelerating biomass-balance certified product offerings globally.

Cargill Incorporated

Cargill Incorporated, headquartered in Minnetonka, Minnesota, is one of the world's largest privately held food, agriculture, and ingredient solutions companies. Founded in 1865, Cargill operates across 70 countries and serves food, pharma, personal care, and industrial customers globally.

- Product & Platform Portfolio: Cargill's emulsifier portfolio includes Topcithin soy and sunflower lecithin, Ingrevita plant-based emulsifiers, mono- and di-glycerides, and specialty emulsifier blends for bakery, confectionery, dairy, and meat processing applications.

- Recent Developments: In 2024, Cargill continued to invest in sustainable palm oil traceability and expand its RSPO-certified emulsifier offerings. The company also advanced plant-based ingredient innovation, including sunflower lecithin capacity expansion to meet European non-GMO demand.

- Strategic Focus: Cargill's strategy focuses on plant-based ingredient leadership, sustainable palm and soy sourcing, bakery and confectionery application depth, and partnership with major food CPG brands on clean-label reformulation programs across regions.

Market Concentration Analysis

The global emulsifiers market exhibits moderate concentration. The top five players - BASF, Cargill, ADM, Evonik, and Kerry - collectively account for 35-42% of global market revenue in 2025. The remaining market share is distributed across Palsgaard, Stepan, Lubrizol, Dow, Puratos, DSM-Firmenich, and a long tail of regional specialty emulsifier producers across Asia Pacific, Europe, and Latin America.

The market is experiencing a bifurcated dynamic. At the global ingredient major tier, consolidation is occurring through capacity additions in bio-based and fermentation-derived emulsifiers. Simultaneously, Chinese and Indian specialty producers such as DuPont Tate & Lyle, Jiangsu Sanmu, and Godrej are scaling cost-competitive synthetic offerings that are reshaping pricing in Asia Pacific and beyond. This dual dynamic is intensifying competition across price tiers and driving portfolio differentiation through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Bio-Based emulsifiers are the highest-growth source sub-segment at an estimated 6.7% CAGR through 2034. Cosmetics and personal care is the fastest-growing application at approximately 5.5% CAGR, driven by natural cosmetics and premium skincare demand. Pharmaceutical emulsifiers represent a premium technology growth opportunity, with lipid nanoparticle demand projected to drive the segment through 2030 at 4.8% CAGR.

Emerging Market Expansion

India represents the highest-potential emerging market, driven by the FSSAI-regulated food additive framework, expanding organized retail, and a fast-growing personal care industry. Southeast Asia's packaged food growth, Latin American cosmetics expansion, and GCC's premium personal care imports collectively represent significant volume opportunities for manufacturers with regional distribution and certification capabilities.

Venture and Strategic Investment Trends

Strategic acquisitions are reshaping the competitive landscape. Major ingredient players are scaling bio-based and fermentation-derived emulsifier capacity through targeted M&A and greenfield plant investments. Venture capital continues to flow into precision fermentation start-ups, sustainable palm alternatives, and enzymatic synthesis platforms. These are the primary focus areas for corporate and venture investment in the emulsifier industry through 2034.

Future Market Outlook (2026-2034)

The global emulsifiers market forecast projects steady value expansion from USD 8.98 Billion in 2025 to USD 14.41 Billion by 2034 at a CAGR of 4.94%. Asia Pacific will retain regional leadership while accelerating structurally. North America and Europe will sustain premium value growth through clean-label reformulation, pharma-grade demand, and bio-based product launches.

Three shifts will reshape the emulsifiers market through 2034. Bio-based and enzymatically produced emulsifiers will continue to gain share structurally, with bio-based penetration rising from 21.4% in 2025 toward 28-30% by 2034. Pharma-grade emulsifiers will become a high-margin growth engine driven by LNP and biologics demand. Meanwhile, Chinese and Indian specialty producers will compress entry-level pricing, intensifying global competition across cost-sensitive applications.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with emulsifier industry stakeholders, including product managers at OEM manufacturers, procurement directors at major food and personal care brands, pharmaceutical formulators, distribution partners, and institutional investors in specialty chemicals. Primary insights validated market sizing, segmentation estimates, and technology adoption timelines.

Secondary Research

Secondary sources include Euromonitor packaged food data, Roundtable on Sustainable Palm Oil (RSPO) publications, EU Farm to Fork strategy documentation, FDA and EFSA regulatory filings, company annual reports, industry publications including Food Ingredients First, Personal Care Products Council reports, and regional chemical association databases.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, packaged food consumption indices, personal care market expansion curves, pharmaceutical formulation demand, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic and regulatory uncertainty.

Global Emulsifiers Market Report Coverage:

|

Report Feature |

Details |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

USD Billion / USD Million |

|

Segments Covered |

|

|

Regions Covered |

Asia Pacific, North America, Europe, Latin America, Middle East & Africa |

|

Countries Covered |

USA, Canada, China, Japan, India, South Korea, Australia, Indonesia, UK, Germany, France, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | BASF, Cargill Incorporated, ADM, DSM-firmenich, Evonik Industries, xKerry Group plc, DOW, Lubrizol, Palsgaard, Puratos Group, Stepan Company, Spartan Chemical Company, etc. |

|

Customization Scope |

10% free customization |

|

Report Delivery |

PDF and Excel through Email (10-12 week support) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, emulsifiers market outlook, and dynamics of the market from 2020-2034.

- The emulsifiers market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the emulsifiers industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Emulsifiers Market Report

The global emulsifiers market was valued at USD 8.98 Billion in 2025, driven by packaged food consumption, personal care expansion, clean-label reformulation demand, and rising pharmaceutical formulation volumes across major global regions.

The market is projected to reach USD 14.41 Billion by 2034, growing at a CAGR of 4.94% during 2026-2034, supported by bio-based adoption, pharma-grade demand, and sustained processed food and personal care consumption worldwide.

Food and beverages applications lead with a 43.6% share in 2025, driven by global packaged food sales exceeding USD 3.1 Trillion and sustained emulsifier volume demand across bakery, dairy, confectionery, and processed meat categories.

Bio-based emulsifiers are the fastest-growing source category, expanding at an estimated CAGR of 6.7% through 2034, driven by clean-label consumer demand, sustainability mandates, and reformulation commitments from major food brands.

Asia Pacific dominates with a 35.0% share in 2025. China's processed food and personal care scale, India's FSSAI food additive framework, and ASEAN consumption growth underpin the region's market leadership globally.

Key drivers include packaged food consumption exceeding USD 3.1 Trillion, personal care expansion, clean-label reformulation, pharmaceutical formulation demand, and sustainability-driven bio-based ingredient adoption across the U.S. and Europe.

Key drivers include packaged food consumption exceeding USD 3.1 Trillion, personal care expansion, clean-label reformulation, pharmaceutical formulation demand, and sustainability-driven bio-based ingredient adoption across the U.S. and Europe.

Major players include BASF, Cargill, ADM, DSM-Firmenich, Evonik, Kerry Group, Palsgaard, Puratos, Stepan, Lubrizol, Dow Chemical, and Spartan Chemical among other regional specialty producers globally.

Cosmetics and personal care is among the fastest-growing application segments, advancing at approximately 5.5% CAGR from 2025 to 2030, driven by premium skincare, natural cosmetics, and multifunctional formulation demand.

Key opportunities include bio-based and enzymatic production, pharma-grade capacity expansion, natural cosmetics ingredient systems, India and Southeast Asia market scaling, and sustainable palm sourcing infrastructure investment worldwide.

Bio-based emulsifiers are growing at approximately 6.7% CAGR, significantly outpacing synthetic counterparts. Their share is expected to rise from 21.4% in 2025 toward 28-30% by 2034 as reformulation and sustainability commitments intensify.

Pharmaceutical emulsifier demand reached USD 1.30 Billion in 2025, driven by lipid nanoparticle formulations for mRNA therapeutics, injectable biologics, and topical dermatology products that require GMP-compliant pharma-grade emulsifier supply.

Key challenges include cost gap between bio-based and synthetic emulsifiers, raw material volatility in palm and soybean feedstocks, regulatory scrutiny on certain additives, and RSPO sustainability compliance costs across global supply chains.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade