Engineering Insurance Market Report by Insurance Type (Project Insurance, Operational Machineries Insurance, Business Interruption Insurance), Application (Production and Processing Enterprises, Oil and Gas, Power and Utilities, Heavy Industries, Transportation Systems, Heavy Civil Engineering Projects, and Others), and Region 2026-2034

Market Overview:

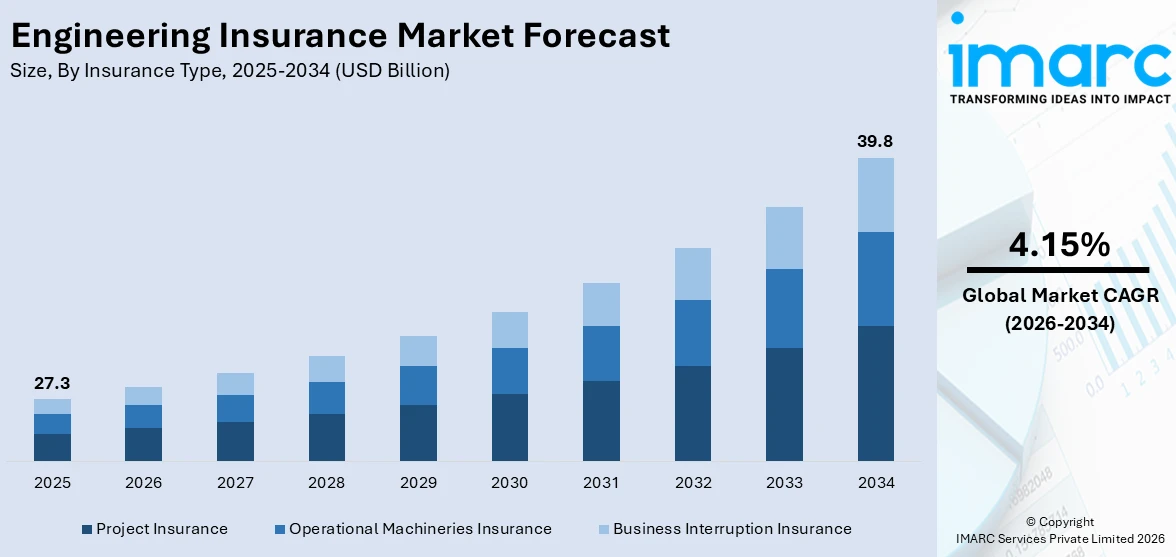

The global engineering insurance market size reached USD 27.3 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 39.8 Billion by 2034, exhibiting a growth rate (CAGR) of 4.15% during 2026-2034. The expanding infrastructural development, the increasing complexity of engineering projects, the escalating awareness about risk management, and the emergence of new technologies and industrial practices are some of the major factors propelling the market.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 27.3 Billion |

| Market Forecast in 2034 | USD 39.8 Billion |

| Market Growth Rate 2026-2034 | 4.15% |

Engineering insurance is a specialized type of insurance that provides coverage for risks and liabilities associated with construction, engineering, and infrastructure projects. It is designed to protect project owners, contractors, and stakeholders from potential financial losses arising from various perils and uncertainties such as property damage, machinery breakdown, construction delays, third-party liabilities, natural disasters, and other unforeseen events throughout the project lifecycle. These insurance policies can be tailored to the specific needs of different types of projects, such as buildings, bridges, roads, power plants, and industrial facilities. These policies help mitigate financial risks, protect investments, and ensure the successful completion of projects.

To get more information on this market Request Sample

The rapid expansion of infrastructure development projects across the globe is primarily driving the engineering insurance market. Besides this, extensive investments by governments and private enterprises in large-scale construction and engineering ventures are fueling the need for comprehensive insurance coverage to protect against unforeseen events and losses, thus favoring the market growth. Moreover, the increasing complexity and scale of engineering projects, including the use of advanced technologies and innovative construction methods, have heightened the risks involved, positively impacting the market growth. In addition to this, the growing awareness of risk management practices in the thriving construction sector is contributing to the market expansion. Furthermore, favorable regulatory requirements and contractual obligations mandating the inclusion of engineering insurance in construction projects are presenting remunerative growth opportunities for the market. Apart from this, with the emergence of new technologies and innovative industrial practices, such as renewable energy, smart infrastructure, and autonomous vehicles, there is a surging need for specialized insurance products tailored to these sectors, further creating a positive outlook for the market.

Engineering Insurance Market Trends/Drivers:

Increasing infrastructure development

One of the primary drivers of the market is the surge in infrastructure development projects across the globe. In line with this, extensive investments in constructing transportation networks, energy facilities, commercial complexes, and residential buildings by governments and private entities across the globe are aiding in market expansion. In addition to this, the widespread product demand to provide protection against these risks, including property damage, construction delays, equipment breakdown, and third-party liabilities, is presenting remunerative growth opportunities for the market. With the growing demand for robust risk management strategies and financial security, engineering insurance has become an essential component of infrastructure development projects to safeguard investments, manage potential losses, and ensure the successful completion of projects.

Technological advancements and complex projects

With the rapid advancement of technology and the resulting complexity of projects, there is a rising demand for engineering insurance. The expanding integration of advanced and innovative technologies, such as smart infrastructure, renewable energy systems, the Internet of Things (IoT) devices, and artificial intelligence (AI), in modern construction and engineering projects is creating a favorable outlook for the market growth. While these technologies offer significant benefits, they also introduce new risks and challenges. Engineering insurance plays a vital role in mitigating these risks by providing coverage for technology-related issues, including system failures, cyber-attacks, data breaches, and design flaws. In addition to this, the increasing complexity of projects, coupled with the need for specialized coverage tailored to emerging technologies, is propelling the market forward.

Regulatory compliance and risk management

The growing emphasis on regulatory compliance and risk management practices in the construction and engineering industries is one of the key factors impelling the market growth. Governments and regulatory bodies worldwide are implementing stringent regulations and standards to ensure safety, environmental protection, and financial accountability in engineering projects. As a result, there is a surging inclusion of engineering insurance to ensure compliance with these regulations. In addition to this, stakeholders in the construction industry are increasingly recognizing the importance of risk management to protect their investments and minimize potential losses, which is strengthening the market growth. Furthermore, the growing need for legal and financial protection, coupled with the focus on risk mitigation, is fueling the growth of the global engineering insurance market.

Engineering Insurance Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global engineering insurance market report, along with forecasts at the global, regional, and country levels from 2026-2034. Our report has categorized the market based on insurance type and application.

Breakup by Insurance Type:

- Project Insurance

- Operational Machineries Insurance

- Business Interruption Insurance

Project insurance is dominating the market

The report has provided a detailed breakup and analysis of the market based on the insurance type. This includes project insurance, operational machineries insurance, and business interruption insurance. According to the report, project insurance represented the largest segment.

The increasing complexity and scale of construction and infrastructure projects worldwide are creating a surging demand for engineering insurance. As projects become larger and involve multiple stakeholders, the risks associated with them also amplify, creating a favorable outlook for the market growth. Besides this, the widespread demand for operational machinery insurance to safeguard businesses against the risks associated with their machinery and equipment, such as damage or breakdown resulting in substantial financial losses and operational disruptions, is aiding in market expansion. In addition to this, the increasing use of business interruption insurance to offer coverage for lost income, additional expenses, and ongoing fixed costs incurred due to an unpredicted occurrence, such as a natural disaster, fire, or other covered perils, is presenting remunerative growth opportunities for the market.

Breakup by Application:

Access the comprehensive market breakdown Request Sample

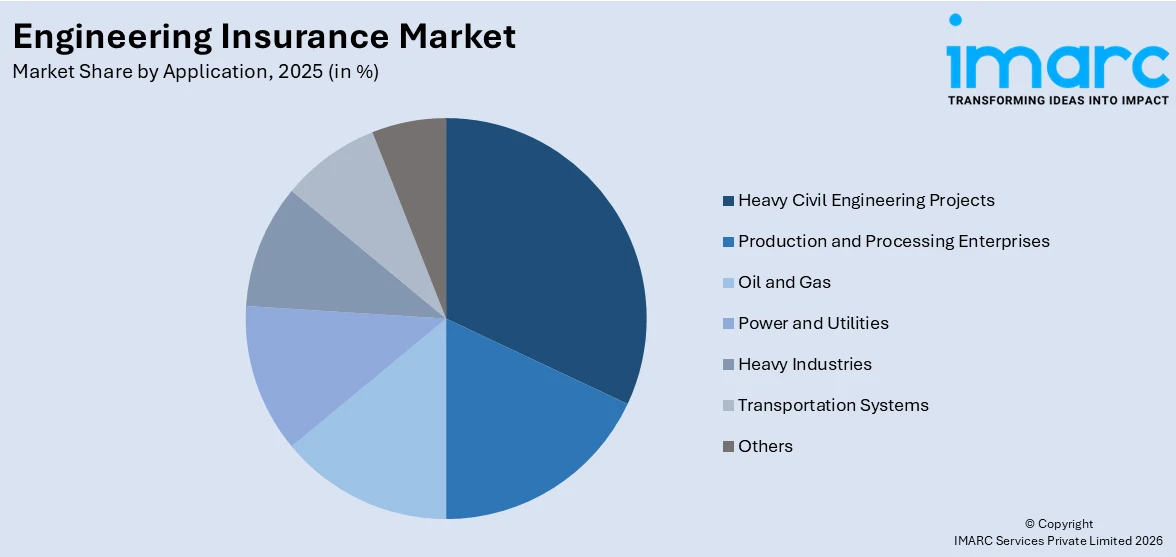

- Production and Processing Enterprises

- Oil and Gas

- Power and Utilities

- Heavy Industries

- Transportation Systems

- Heavy Civil Engineering Projects

- Others

Heavy civil engineering projects hold a larger share in market

A detailed breakup and analysis of the market based on the application has also been provided in the report. This includes production and processing enterprises, oil and gas, power and utilities, heavy industries, transportation systems, heavy civil engineering projects, and others. According to the report, heavy civil engineering projects accounted for the largest market share.

The large-scale demand for engineering insurance in production and processing enterprises, due to the rising reliance on complex machinery and equipment that can break down, fail, and damage, is influencing the market growth. In addition to this, widespread product adoption across the flourishing oil and gas industry, on account of the unique risks, such as potential accidents, environmental liabilities, and property damage involved in exploration, production, and refining activities, is contributing to the market growth. Moreover, the rising need for engineering insurance across the power and utilities sector to safeguard companies from the critical nature of their infrastructure and the risks associated with power generation, transmission, and distribution is propelling the market forward. Concurrent with this, the expanding transportation systems, including railways, ports, and airports, require engineering insurance to protect against potential accidents, property damage, and disruptions to transportation services, which, in turn, is aiding in market expansion.

Breakup by Region:

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Asia Pacific exhibits a clear dominance in the market, accounting for the largest engineering insurance market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa.

Asia Pacific is experiencing rapid industrialization and infrastructure development, leading to an increasing need for insurance cover to mitigate potential risks. Countries like China and India are at the forefront of this growth, with numerous large-scale projects in the pipeline. Additionally, the increasing adoption of advanced technologies in the construction sector is driving the demand for specialized insurance policies to cover equipment and systems. Furthermore, rising awareness about insurance benefits among contractors and construction firms, coupled with regulatory policies encouraging or mandating insurance coverage for certain types of projects, is also contributing to the region's dominant position in the market.

The extensive infrastructure development projects in North America are primarily driving the market. In line with this, the expanding construction of transportation networks, energy facilities, and commercial complexes in the region necessitates comprehensive coverage against risks, such as property damage, construction delays, and third-party liabilities, creating a positive outlook. Moreover, the rising focus on risk management and regulatory compliance in North America reinforces the product demand as businesses aim to mitigate potential losses and ensure project success.

In addition to this, the implementation of rigid regulations and standards governing construction and engineering projects in Europe has mandated the need for engineering insurance to comply with legal obligations and protect against potential liabilities. Furthermore, the region's advanced infrastructure and technological advancements in sectors, such as renewable energy and smart cities, increases the complexity of projects, thus driving the need for specialized coverage provided by engineering insurance.

Competitive Landscape:

The market exhibits a competitive landscape characterized by the presence of several key players striving to gain a significant market share. These players compete based on various factors, including the range of insurance products offered, geographical coverage, industry expertise, client relationships, and service quality. The leading insurance companies leverage their extensive networks, financial stability, and established brand reputation to attract clients and offer comprehensive coverage for a wide range of engineering risks. In addition to this, to maintain a competitive edge, these companies invest in technological advancements to enhance underwriting processes, claims management, and client servicing. The evolving nature of engineering risks and the need for comprehensive coverage ensure that competition in this market remains robust and focused on delivering value-added solutions to clients.

The report has provided a comprehensive analysis of the competitive landscape in the market. Detailed profiles of all major companies have also been provided. Some of the key players in the market include:

- Allianz Insurance plc

- Assicurazioni Generali

- Aviva plc

- HDI Global SE (Talanx)

- Munich Re Group

- Prudential Guarantee and Assurance Inc.

- Royal & Sun Alliance Insurance Ltd (Intact Financial Corporation)

- Swiss Re

- Zurich Insurance Group Ltd

Recent Developments:

- In June 2023, Assicurazioni Generali collaborated with four other insurance companies - namely Allianz, Intesa Sanpaolo Vita, Poste Vita, and Unipol SAI - in the agreements aimed at implementing a collective operation to protect Eurovita policyholders.

- In May 2023, Aviva plc announced the completion of a £ 900 million bulk annuity buy-in transaction with the Trustees of the Thomas Cook Pension Plan.

- In April 2023, Swiss Re Reinsurance Solutions announced its strategic partnership with Benekiva to create an end-to-end digital claims management solution.

Engineering Insurance Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Insurance Types Covered | Project Insurance, Operational Machineries Insurance, Business Interruption Insurance |

| Applications Covered | Production and Processing Enterprises, Oil and Gas, Power and Utilities, Heavy Industries, Transportation Systems, Heavy Civil Engineering Projects, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Allianz Insurance plc, Assicurazioni Generali, Aviva plc, HDI Global SE (Talanx), Munich Re Group, Prudential Guarantee and Assurance Inc., Royal & Sun Alliance Insurance Ltd (Intact Financial Corporation), Swiss Re, Zurich Insurance Group Ltd, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the global engineering insurance market performed so far, and how will it perform in the coming years?

- What are the drivers, restraints, and opportunities in the global engineering insurance market?

- What is the impact of each driver, restraint, and opportunity on the global engineering insurance market?

- What are the key regional markets?

- Which countries represent the most attractive engineering insurance market?

- What is the breakup of the market based on the insurance type?

- Which is the most attractive insurance type in the engineering insurance market?

- What is the breakup of the market based on the application?

- Which is the most attractive application in the engineering insurance market?

- What is the competitive structure of the global engineering insurance market?

- Who are the key players/companies in the global engineering insurance market?

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the engineering insurance market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global engineering insurance market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the engineering insurance industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)