Engineering Services Outsourcing Market Size, Share, Trends and Forecast by Service, Location, Application, and Region, 2026-2034

Global Engineering Services Outsourcing Market Size, Share, Trends & Forecast (2026-2034)

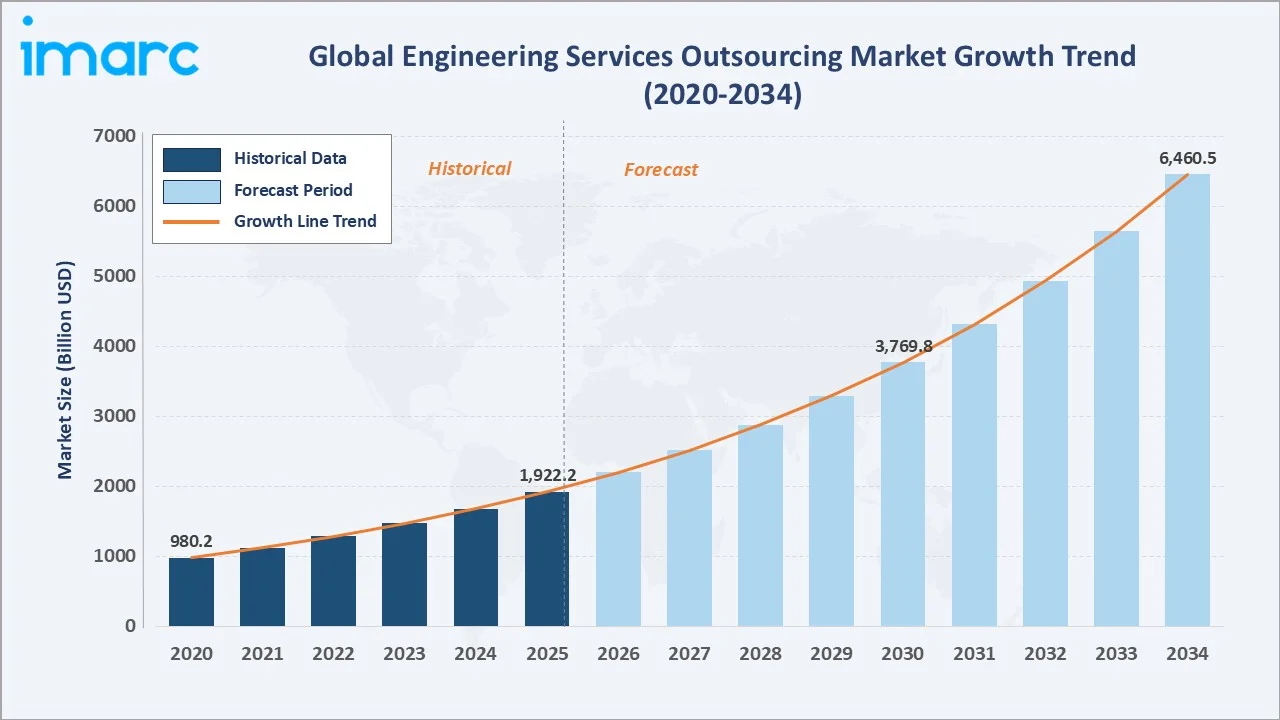

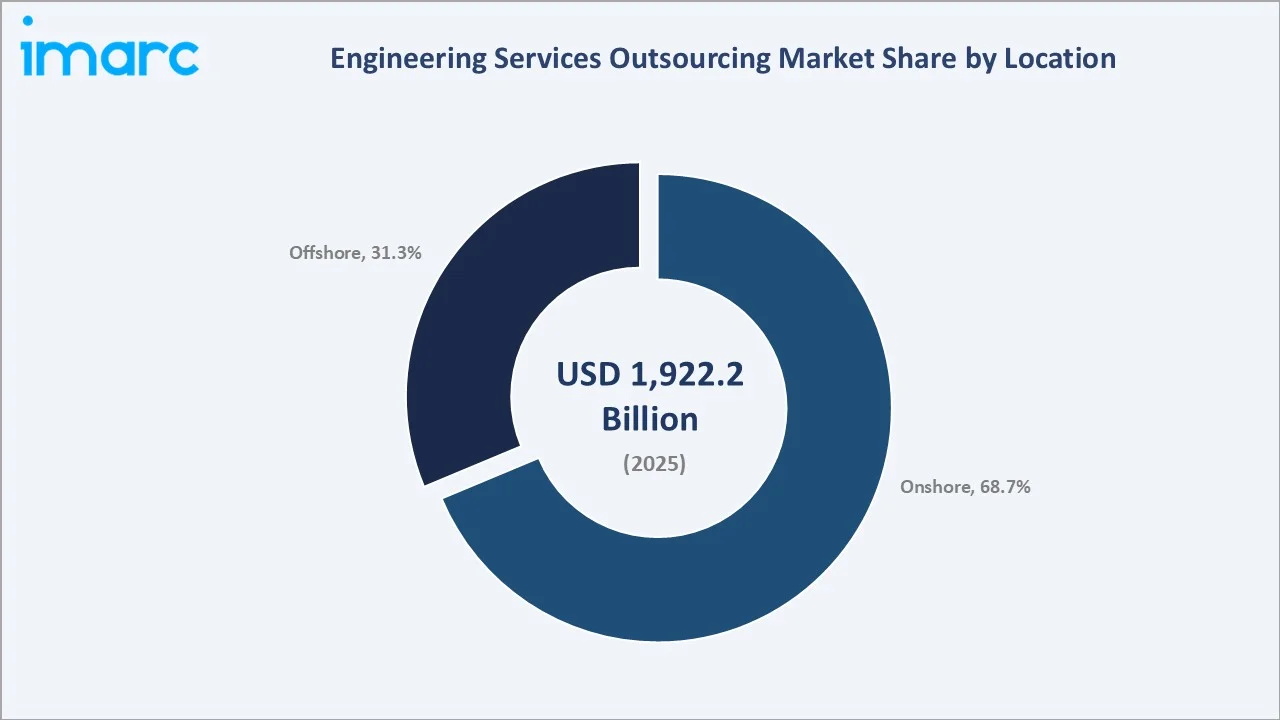

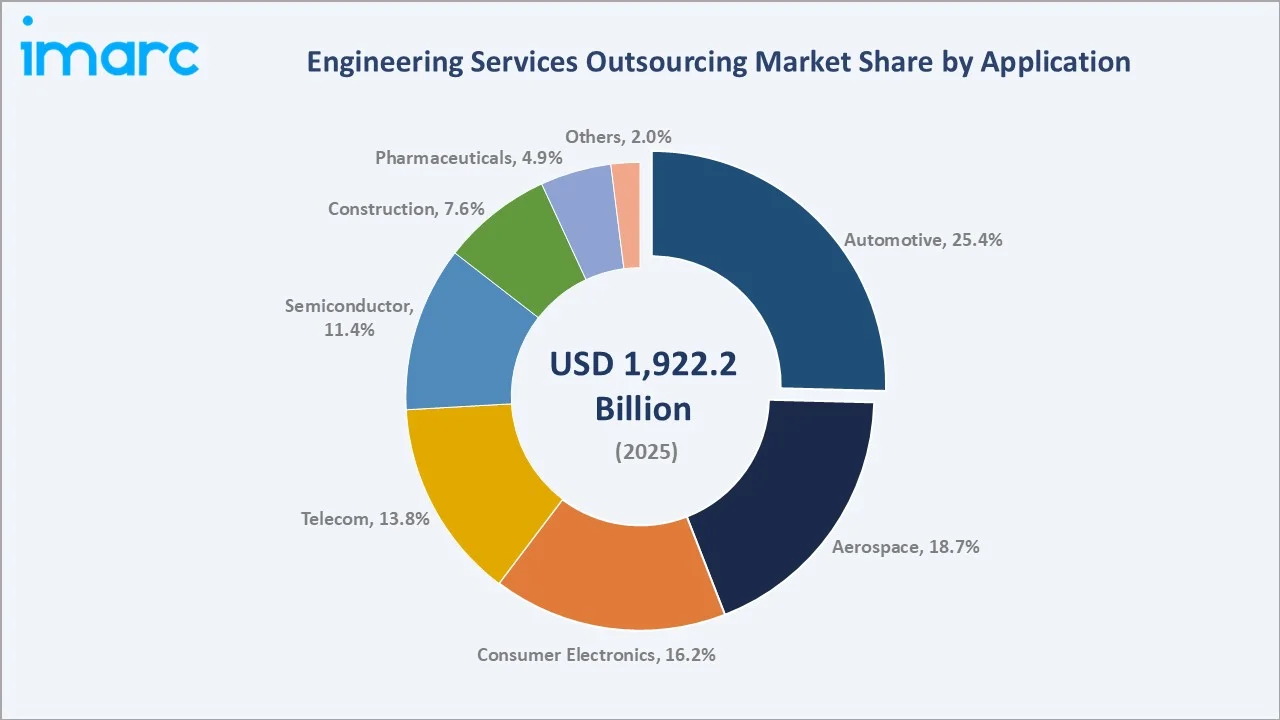

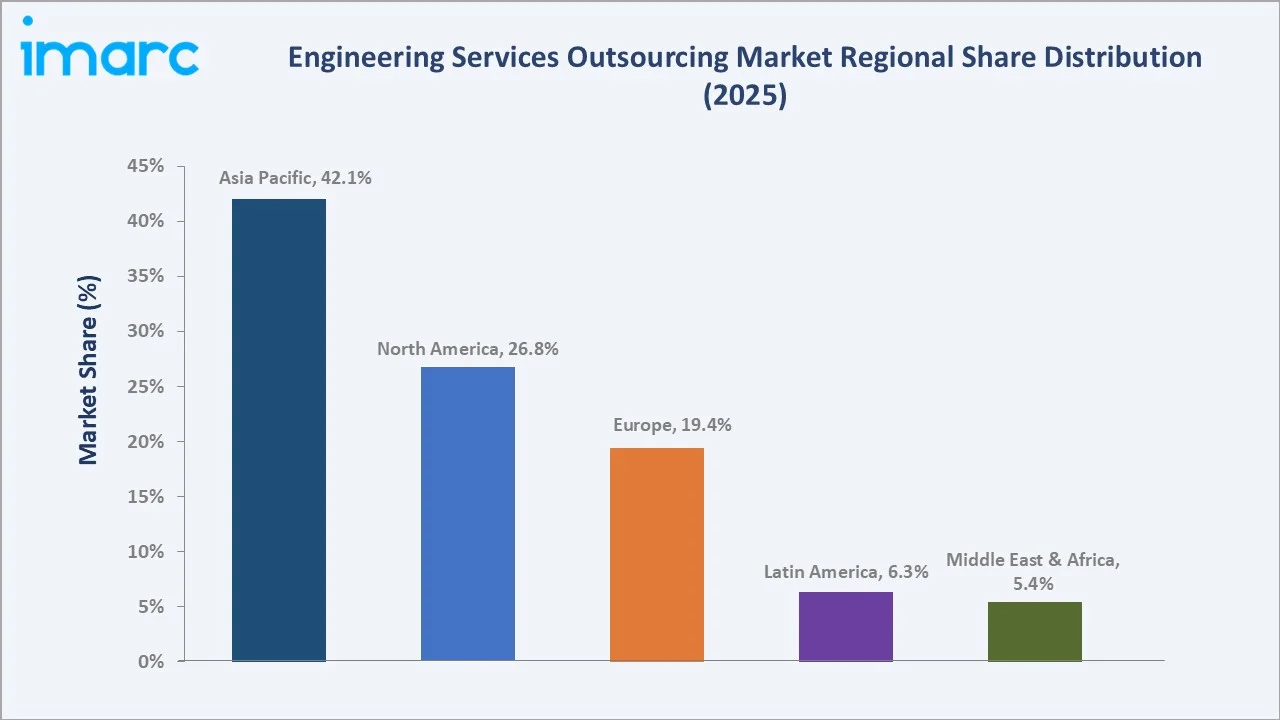

The global engineering services outsourcing (ESO) market reached USD 1,922.2 Billion in 2025 and is projected to reach USD 6,460.5 Billion by 2034, growing at a CAGR of 14.42% during 2026-2034. The market is driven by the need for cost reduction, access to specialized skills, and the increasing demand for innovation in product design and development across industries such as automotive, aerospace, and manufacturing. Electric vehicle engineering complexity, AI-augmented design tools, India's 2.55 million and China’s 3.57 million annual STEM graduates (2025), and semiconductor proliferation anchor the market's sustained double-digit CAGR. Onshore location leads at 68.7%. Automotive dominates applications at 25.4%. Asia Pacific commands 42.1% of global market revenues.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1,922.2 Billion |

|

Forecast Market Size (2034) |

USD 6,460.5 Billion |

|

CAGR (2026-2034) |

14.42% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Location |

Onshore (68.7%, 2025) |

|

Largest Application |

Automotive (25.4%, 2025) |

|

Leading Region |

Asia Pacific (42.1%, 2025) |

The market expanded from USD 980.2 Billion in 2020 to USD 1,922.2 Billion in 2025, anchored at USD 3,769.8 Billion in 2030, and forecast to reach USD 6,460.5 Billion by 2034. COVID-19 normalized remote engineering delivery globally, and companies that had never outsourced engineering work discovered that offshore teams delivered equivalent quality at lower cost, permanently shifting ESO from tactical cost management to strategic R&D capability sourcing that compounds market growth well above pre-pandemic trajectory rates.

To get more information on this market, Request Sample

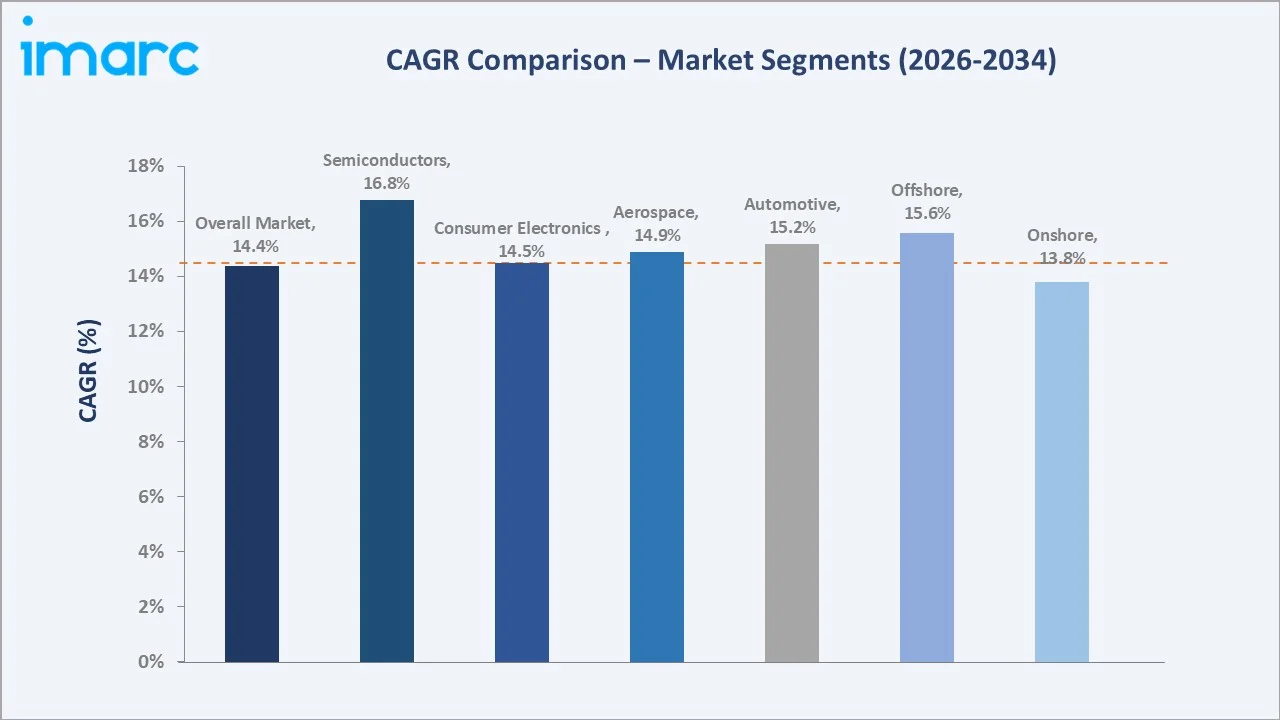

Offshore grows fastest at ~15.6% CAGR (2026-2034), driven by India's Global Capability Center (GCC) expansion and the maturing quality of offshore engineering delivery that is reducing client reluctance to offshore complex, IP-sensitive design work. Semiconductors grow at ~16.8% CAGR among applications, driven by generative AI chip complexity requiring more engineering per SoC design, CHIPS Act-driven US semiconductor fab expansion requiring engineering services.

Executive Summary

The global engineering services outsourcing (ESO) market reached USD 1,922.2 Billion in 2025, making engineering services outsourcing the world's largest professional services category by annual revenue. The market's extraordinary scale reflects the engineering intensity of global manufacturing; every automobile, aircraft, semiconductor, smartphone, and pharmaceutical product requires thousands of engineering person-years of design, testing, and certification work that global OEMs increasingly source from specialized ESO providers rather than maintain as internal engineering headcount. The market is projected to reach USD 6,460.5 Billion by 2034 at 14.42% CAGR, representing the largest absolute revenue addition in any professional services market globally.

Onshore ESO commands 68.7% of market revenues, reflecting the substantial engineering work performed by engineering service providers working at or near client facilities in high-cost countries. The automotive application segment leads with 25.4%. Asia Pacific at 42.1% leads regionally through India's dominant offshore delivery infrastructure.

Key Market Insights

|

Insight |

Data |

|

Dominant Location |

Onshore - 68.7% share (2025) |

|

Largest Application |

Automotive - 25.4% share (2025) |

|

Leading Region |

Asia Pacific - 42.1% share () |

Key Analytical Observations Supporting the Above Data:

- Onshore at 68.7% driven by client proximity requirements for complex, regulated, and IP-sensitive engineering: Onshore ESO is not simply a legacy delivery model; it reflects genuine engineering work that requires physical co-location with clients. Automotive ADAS development requires engineers embedded with OEM testing teams in proving ground environments; aerospace structural analysis requires facility access to physical prototype hardware; pharmaceutical device engineering requires regulatory affairs specialists co-located with FDA submission teams.

- Automotive at 25.4% anchored by EV/ADAS engineering complexity requiring massive, outsourced talent: The global automotive industry is undergoing its largest engineering transition since the combustion engine, with electrification, software-defined vehicles, ADAS, and autonomous driving requiring 10-15x more software engineering per vehicle than traditional ICE development.

- Asia Pacific at 42.1% reflecting India's structural dominance as the world's ESO delivery hub: India's IT-ESO export revenue target places engineering services as the sector's highest-growth component. Bengaluru hosts most of the GCC engineering headcount.

Global Engineering Services Outsourcing Market Overview

The global engineering services outsourcing market encompasses all contracted engineering services performed by third-party providers, including product design and engineering, prototype development, system integration, testing and validation, simulation, manufacturing engineering support, and embedded software development. The market spans service delivery from full-time engineers on-site embedding at client facilities (onshore/nearshore) to offshore centers performing autonomous design work under client oversight at significant cost advantages.

The ecosystem integrates client organizations, ESO providers across Tier-1, Tier-2, and niche engineering boutiques, engineering talent pools across India, Central and Eastern Europe, the Philippines, Mexico, and the Americas, technology platforms, and regulatory frameworks governing IP protection and export controls. Macroeconomic factors include rising labor costs in developed economies, the need for companies to focus on core competencies, global talent availability, technological advancements, and increased demand for cost-effective, scalable solutions across various industries.

Market Dynamics

To evaluate market opportunities, Request Sample

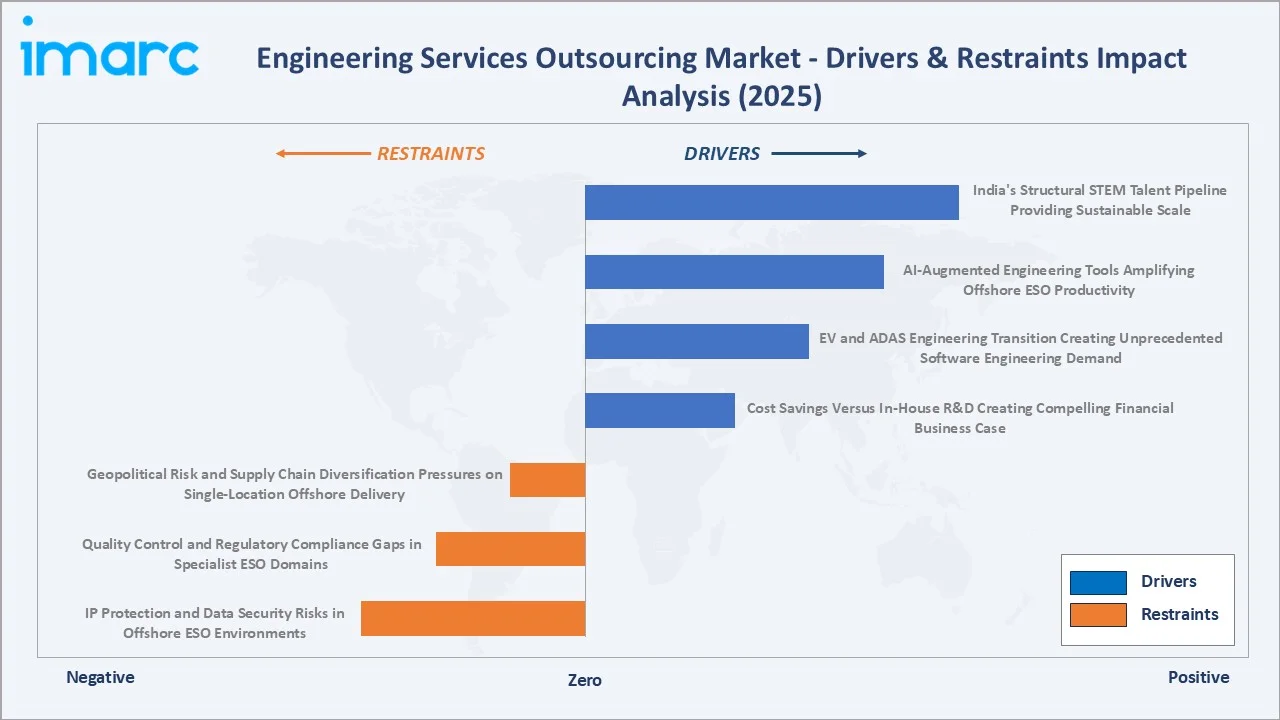

Market Drivers

- Cost Savings Versus In-House R&D Creating Compelling Financial Business Case: Engineering talent costs in high-income countries create powerful financial incentives for outsourcing to India, Eastern Europe, or Mexico.

- EV and ADAS Engineering Transition Creating Unprecedented Software Engineering Demand: Electric car sales topped 17 million worldwide in 2024, rising by more than 25%. The automotive industry's software content explosion has created an engineering talent demand that no single OEM can staff internally.

- AI-Augmented Engineering Tools Amplifying Offshore ESO Productivity: Generative AI design tools are multiplying the productivity of offshore engineering teams. An engineer using AI-assisted design can complete 3-5x more design iterations per day than without AI assistance. This AI productivity multiplier increases the effective output of India and Eastern Europe's engineering talent pools, improving value delivery at existing offshore cost structures and making offshore ESO even more attractive relative to onshore alternatives.

- India’s Structural STEM Talent Pipeline Providing Sustainable Scale: India produces 2.55 million STEM graduates annually, the world's second-largest producer of STEM graduates. These structural talent pipelines provide ESO delivery ecosystems that cannot be quickly replicated by competing regions, ensuring Asia Pacific delivery hubs maintain structural cost and scale advantages throughout the 2026-2034 forecast period.

Market Restraints

- IP Protection and Data Security Risks in Offshore ESO Environments: Engineering IP, such as product designs, simulation models, material specifications, and manufacturing processes, represents billions of dollars in competitive advantage for OEM clients. Data breach risks, insider threat from offshore engineering staff, and jurisdictional uncertainty around IP ownership in multi-country ESO arrangements create client hesitation around offshoring complex, proprietary design work.

- Quality Control and Regulatory Compliance Gaps in Specialist ESO Domains: Automotive functional safety, aerospace software certification, and pharmaceutical device software regulation require specialized regulatory expertise that not all ESO providers have developed. Quality lapses in regulated-domain ESO can result in product recalls, certification failures, or regulatory penalties, creating risk aversion among regulated industry clients and limiting offshore ESO addressable market in the highest-value regulated application segments.

Market Opportunities

- Semiconductor Engineering Services Entering Hyper-Growth Phase from CHIPS Act Manufacturing Build-Out: The CHIPS Act and European CHIPS Act are funding new semiconductor fabs globally, each requiring high investment in facility engineering services for cleanroom design, process equipment qualification, utility systems engineering, and safety systems integration. This fab construction wave creates a one-time engineering services demand surge in semiconductor facility engineering, representing the largest single-project ESO opportunity in market history.

- Autonomous Vehicle and Robotics Engineering Creating New High-Value Outsourcing Domain: Level 3-5 autonomous vehicle development requires integration of computer vision, sensor fusion, deep learning, safety validation, and functional safety certification expertise that no single company can staff internally at the required scale. The emerging humanoid robotics industry requires similar multi-disciplinary engineering outsourcing.

Market Challenges

- Geopolitical Risk and Supply Chain Diversification Pressures on Single-Location Offshore Delivery: US-China trade tensions, India-Pakistan geopolitical risks, and Eastern European conflict proximity are prompting clients to implement multi-location offshore ESO strategies rather than single-country concentration.

- Talent Retention and Engineering Wage Inflation in Mature ESO Delivery Markets: Bengaluru and Hyderabad engineering talent markets experienced 20-30% annual wage inflation as demand for skilled engineers in digital, AI, and specialized engineering domains significantly exceeded supply.

Emerging Market Trends

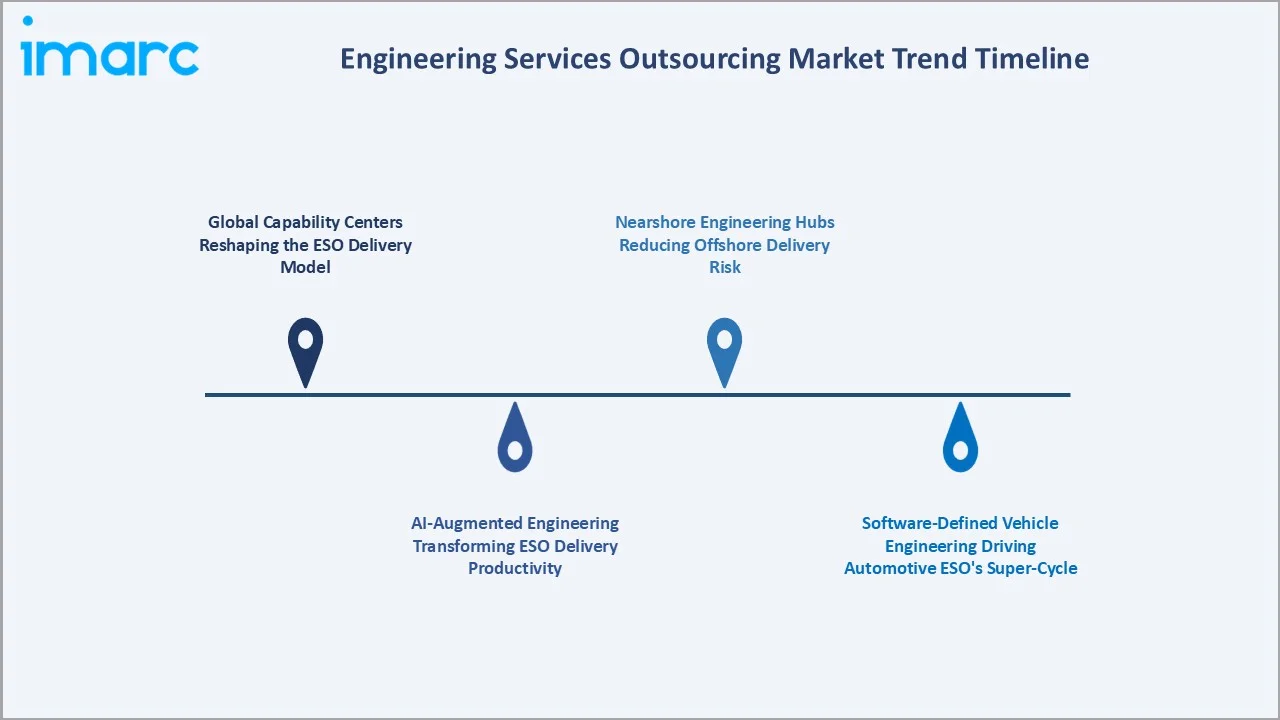

1. Global Capability Centers Reshaping the ESO Delivery Model

The GCC (Global Capability Center) model, where global OEMs establish captive offshore engineering centers rather than contracting with external ESO providers, is blurring the traditional ESO industry boundary. In FY24, India hosted nearly 1,700 GCCs. Traditional ESO providers are responding by offering 'GCC-as-a-Service' models where they build, operate, and transition GCC operations to clients, creating a new hybrid delivery model.

2. AI-Augmented Engineering Transforming ESO Delivery Productivity

Generative AI's application to engineering, not just code generation but physical system simulation, materials selection, structural topology optimization, and failure mode prediction, is transforming ESO provider productivity and capability. ESO providers investing in AI-augmented engineering tools are achieving high productivity improvements that they are sharing with clients through lower project costs, enabling ESO to compete even more effectively against in-house engineering alternatives.

3. Software-Defined Vehicle Engineering Driving Automotive ESO's Super-Cycle

The automotive industry's Software-Defined Vehicle (SDV) transition, where vehicle functionality is defined by software upgradable over-the-air rather than hardware, is creating an unprecedented software engineering demand surge in automotive ESO.

4. Nearshore Engineering Hubs Reducing Offshore Delivery Risk

Nearshore engineering hubs are reducing offshore delivery risks by offering geographically closer, culturally aligned, and time zone-synchronized solutions. These hubs provide companies with faster communication, reduced logistical challenges, and enhanced collaboration, making them an attractive alternative to traditional offshore outsourcing. This trend is boosting the adoption of nearshore outsourcing models, especially in industries requiring rapid innovation and seamless integration with in-house teams, while mitigating the risks associated with long-distance offshore engagements.

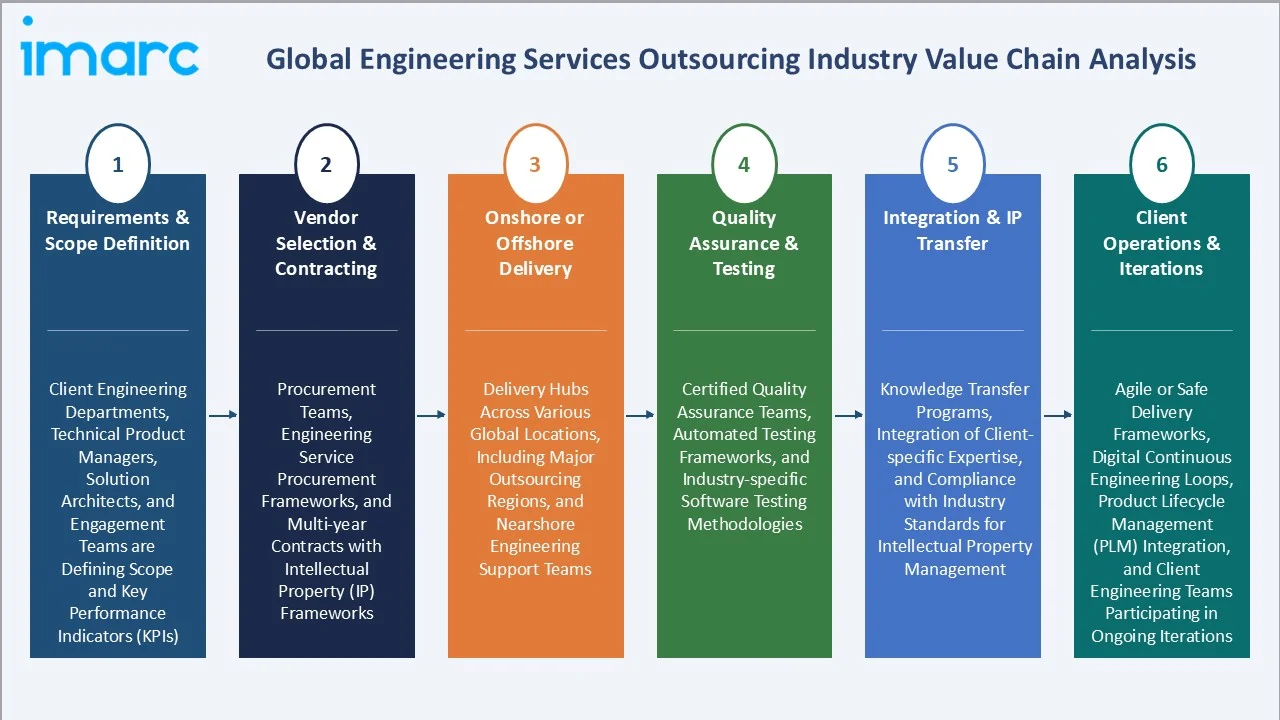

Industry Value Chain Analysis

The global engineering services outsourcing value chain integrates requirements definition, vendor selection, delivery execution (onshore or offshore), quality assurance, IP integration, and client operational support serving global OEM clients across automotive, aerospace, semiconductor, telecom, consumer electronics, and pharmaceutical sectors. Tier-1 ESO providers capture 25-35% gross margins on complex, multi-year strategic engagements; niche domain specialists earn 35-50% margins on regulated-domain engineering where expertise scarcity commands premium pricing.

|

Stage |

Key Participants |

|

Requirements & Scope Definition |

Client engineering departments, technical product managers, solution architects, and engagement teams are defining scope and key performance indicators (KPIs). |

|

Vendor Selection & Contracting |

Procurement teams, engineering service procurement frameworks, and multi-year contracts with intellectual property (IP) frameworks. |

|

Onshore or Offshore Delivery |

Delivery hubs across various global locations, including major outsourcing regions, and nearshore engineering support teams. |

|

Quality Assurance & Testing |

Certified quality assurance teams, automated testing frameworks, and industry-specific software testing methodologies. |

|

Integration & IP Transfer |

Knowledge transfer programs, integration of client-specific expertise, and compliance with industry standards for intellectual property management. |

|

Client Operations & Iterations |

Agile or safe delivery frameworks, digital continuous engineering loops, product lifecycle management (PLM) integration, and client engineering teams participating in ongoing iterations. |

The vendor selection and contracting tier is experiencing increasing sophistication; clients are moving from transactional engineering staff augmentation to multi-year engineering center-of-excellence contracts with outcome-based pricing and shared IP ownership arrangements. This shift from FTE-rate billing to outcome pricing is the single most important commercial evolution in ESO, transferring risk from clients to providers and creating differentiation between ESO providers with sufficient scale and quality to accept outcome-based commitments versus those reliant on time-and-materials staff augmentation.

Technology Landscape in the Global Engineering Services Outsourcing Industry

AI-Augmented Design and Simulation Platforms

AI-augmented design and simulation platforms are enhancing the speed, accuracy, and efficiency of product development. These platforms leverage artificial intelligence to optimize design processes, simulate real-world conditions, and automate repetitive tasks, allowing engineers to focus on innovation. The integration of AI in design and simulation enables faster iterations, reduces errors, and lowers costs, helping companies achieve more advanced and customized solutions while improving time-to-market for complex engineering projects.

Digital Twin Engineering Enabling Virtual Product Development

Digital twin engineering enabling virtual product development. By creating a digital replica of physical assets, processes, or systems, digital twin technology allows engineers to simulate, monitor, and analyze products in real-time without the need for physical prototypes. This enhances the design and testing phases, reduces time-to-market, improves product performance, and helps identify potential issues before they arise. The ability to iterate and optimize virtually leads to more efficient and cost-effective product development, driving innovation across industries like automotive, aerospace, and manufacturing.

PLM and Cloud-Based Collaboration Infrastructure

Product Lifecycle Management (PLM) platforms are the operational backbone of distributed ESO delivery, enabling globally dispersed engineering teams to work concurrently on shared design data with version control, change management, and IP access control. Cloud migration of PLM infrastructure has dramatically improved offshore engineering team productivity by eliminating the latency and VPN performance issues that previously degraded offshore CAD workstation experience.

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Service |

Testing |

🔒 |

2025 |

|

Location |

Onshore |

68.7% |

2025 |

|

Application |

Automotive |

25.4% |

2025 |

|

Region |

Asia Pacific |

42.1% |

2025 |

By Location

Onshore ESO leads at 68.7% market share (2025). This encompasses domestic engineering service firms working at or near client facilities, multinational ESO providers' onshore operations, and ESO delivery from nearshore locations within less flight time of client headquarters. Onshore ESO commands premium pricing but is sustained by genuine client requirements for physical co-location, regulatory jurisdiction mandates, security clearances, and the collaboration quality advantages of same-location teams for iterative design work. Onshore grows at ~13.8% CAGR (2026-2034).

To access detailed market analysis, Request Sample

Offshore ESO at 31.3% grows fastest at ~15.6% CAGR as India's GCC ecosystem matures and Eastern European engineering hubs achieve quality parity with onshore delivery for complex engineering work. India's offshore engineering delivery has evolved from documentation and drafting support through software-driven design assistance to full autonomous engineering center operations where GCCs in Bengaluru and Hyderabad independently design, simulate, and validate complex automotive, semiconductor, and aerospace subsystems with no day-to-day client oversight required.

By Application

Automotive leads at 25.4% market share (2025). The EV, ADAS, and SDV engineering transition has created a decade-long super-cycle of automotive ESO demand as OEMs outsource 40-60% of software engineering, simulation, validation, and electrification system design. Aerospace at 18.7% is driven by Boeing and Airbus next-generation aircraft development, satellite constellations, and MRO (Maintenance, Repair, Overhaul) engineering services. Consumer electronics at 16.2% serves Apple, Samsung, Sony, and Chinese OEMs with product design and manufacturing engineering.

Telecom at 13.8% is driven by 5G network engineering and Open RAN architecture deployment. Semiconductors at 11.4% grow fastest at ~16.8% CAGR as AI chip design complexity and CHIPS Act manufacturing build-out create exceptional engineering services demand. Construction at 7.6% serves NEOM, mega-infrastructure, and green building engineering. Pharmaceuticals at 4.9% is driven by medical device engineering, drug-device combination products, and regulatory compliance engineering.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

Asia Pacific |

42.1% |

Strong availability of STEM talent, global capability centers, and competitive delivery models. |

|

North America |

26.8% |

Growth driven by demand from the automotive, aerospace, and technology sectors, with an emphasis on advanced engineering and IT outsourcing. |

|

Europe |

19.4% |

Significant outsourcing demand from automotive, aerospace, and defense sectors, with contributions from Eastern European markets. |

|

Latin America |

6.3% |

Growth driven by automotive and aerospace engineering services, supported by trade agreements and proximity to major markets |

|

Middle East & Africa |

5.4% |

Increasing outsourcing is driven by infrastructure development, energy projects, and the growth of engineering services in emerging markets. |

Asia Pacific's 42.1% dominance reflects India's structural position as the world's engineering services delivery hub, a position built over 40 years of IIT/NIT engineering education investment, English-language proficiency, compatible time zones with both US and European clients, and a regulatory environment accommodating complex IP-protected engineering work.

North America's 26.8% is demand-driven rather than supply-driven. The US is the world's largest ESO client market, procuring engineering services from domestic providers, India-based GCCs, and Mexican nearshore suppliers. North America's ESO demand growth is accelerating from semiconductor fab engineering (CHIPS Act), automotive EV transition, and space economy engineering.

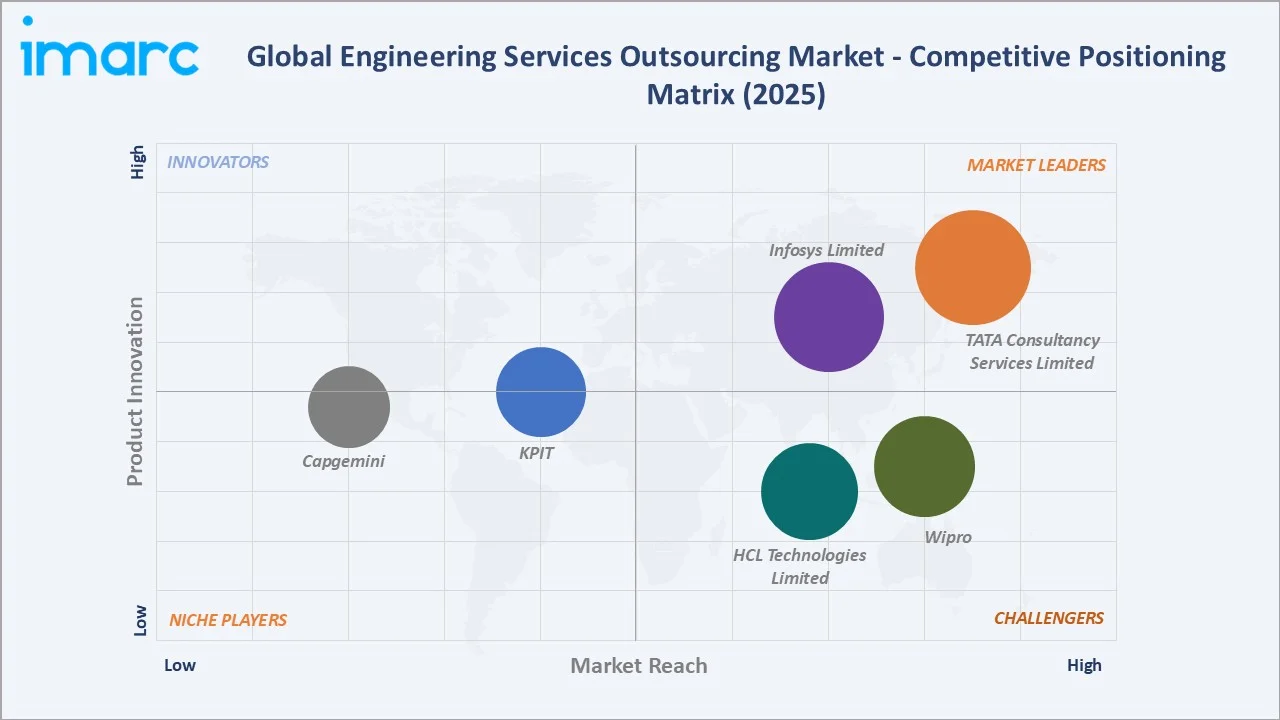

Competitive Landscape

The global engineering services outsourcing market is moderately fragmented with high concentration among Tier-1 providers. India's IT majors collectively command approximately 35-40% of global offshore ESO revenue through their scale, client relationships, and multi-vertical engineering capability. However, the market fragments significantly in domain-specialized segments where specialist providers with deep domain IP compete effectively against generalist large providers.

|

Company Name |

Brand / Services |

Market Position |

Core Strength |

|

TATA Consultancy Services Limited |

TCS Engineering Services |

Market Leader |

World's largest engineering services outsourcer by revenue |

|

Infosys Limited |

Infosys Engineering Services |

Market Leader |

At Infosys Engineering Services, products can functionally enable humans to better understand their lives and interactions. |

|

Wipro |

Wipro Engineering Edge |

Strong Challenger |

Wipro has led engineering services for over 35 years, empowering 500+ clients across industries to innovate and engineer market-changing products and platforms with deep expertise. |

|

HCL Technologies Limited |

Engineering and R&D Services (ERS) |

Strong Challenger |

HCL is delivering high-performance, future-ready engineering solutions, shaping the mobility of tomorrow |

|

KPIT |

Vehicle Engineering & Design |

Established Player |

KPIT is offering comprehensive product development support for vehicle electrification, Autonomous & Infotainment and Hardware Packaging through new-age design & simulation |

|

Capgemini |

Capgemini Engineering |

Established Player |

Capgemini is recognized as a Leader in the IDC MarketScape: Worldwide IT and Engineering Services for Software Defined Vehicles 2025 report. |

The competitive landscape is being reshaped by strategic acquisitions that signal domain specialization as the primary competitive differentiator: Cognizant's USD 1.3 Billion Belcan acquisition (2024). ESO providers that combine talent scale with proprietary engineering IP, specialized domain certifications, and outcome-based delivery models are commanding the highest revenue growth and operating margin profiles.

Key Company Profiles

TATA Consultancy Services Limited

Tata Consultancy Services is a digital transformation and technology partner of choice for industry-leading organizations worldwide and is the world's largest engineering services outsourcing company by revenue.

- Service Portfolio: TCS Engineering Services

- Recent Developments: In September 2025, Tata Consultancy Services launched its Chiplet-based System Engineering Services, designed to help semiconductor companies push the boundaries of traditional chip design.

- Strategic Focus: AI-first engineering delivery amplifying offshore engineer productivity.

Infosys Limited

Infosys is a global leader in next-generation digital services and consulting. Infosys Engineering Services is strategically positioned to respond to real-time customer needs and proactively propose disruptive solutions to help enterprises stay ahead.

- Service Portfolio: Infosys Engineering Services

- Recent Developments: In April 2026, Infosys announced a strategic collaboration with OpenAI to help enterprises transform software development and modernization with OpenAI's frontier AI models and products like Codex.

- Strategic Focus: Leveraging its deep engineering expertise, advanced technologies, and strong digital capabilities to cater to industries such as automotive, aerospace, and high-tech sectors.

Market Concentration Analysis

The global engineering services outsourcing market exhibits moderate concentration among the top providers and high fragmentation across the remaining engineering service firms that collectively serve the majority of SME and specialized OEM clients. India's top 4 IT majors (TCS, Infosys, Wipro, HCL Technologies) collectively generate approximately USD 25-30 Billion in engineering services revenues, representing only 1.5% of the USD 1,922.2 Billion total market. This suggests the ESO market is far more fragmented than the concentration of marquee providers suggests, with the vast majority of ESO revenues generated by regional engineering service firms, domestic ESO providers, and the internal engineering functions of large IT consultancies.

Domain-specialized ESO segments exhibit higher concentration; automotive software ESO and aerospace engineering feature dominant specialized players with 10-20% market shares in their specific application verticals. The semiconductor ESO segment is bifurcated between offshore VLSI design service firms and onshore US semiconductor engineering consultancies serving TSMC, Intel, and NVIDIA.

Investment & Growth Opportunities

Fastest Growing Segments

Offshore ESO (~15.6% CAGR), semiconductors (~16.8% CAGR), AI-augmented engineering platforms (~25%+ CAGR from current small base), automotive SDV engineering (~20%+ CAGR), and aerospace MRO digital services (~18% CAGR) represent the global ESO market's highest-growth investment vectors through 2034. The semiconductor ESO opportunity represents the single largest near-term engineering services opportunity in market history.

Emerging Market Opportunities

Latin America's nearshore engineering hubs represent the most underpenetrated high-growth ESO delivery market. Colombia, Brazil, and Argentina are growing IT-engineering hybrid ESO markets serving US and European technology companies.

Investment Themes

- Domain-specialized ESO acquisition: Pure-play domain specialists command 15-25x EBITDA valuations versus 8-12x for generalist ESO providers, reflecting premium pricing power and client stickiness in regulated domains. Private equity acquisition of 20-500 engineer niche ESO firms at scale creates diversified specialized portfolios that command premium multiples upon strategic exit.

- India GCC-as-a-Service platform development: GCCs in India employing a high number of engineers create a growing transition management market as OEMs build captive centers.

Future Market Outlook (2026-2034)

The global engineering services outsourcing market is projected to grow from USD 1,922.2 Billion in 2025 to USD 6,460.5 Billion by 2034, delivering a 14.42% CAGR over the forecast period. The market's anchor value of USD 3,769.8 Billion in 2030 represents a transformed global engineering delivery landscape where offshore engineering quality is indistinguishable from onshore for the majority of engineering work types, AI-augmented engineering tools have multiplied effective engineering output per professional by 3-5x, and specialized ESO providers have become genuine R&D partners rather than cost-reduction service vendors.

Three structural forces define the global ESO market's growth trajectory with exceptional certainty through 2034: the irreversible engineering complexity explosion across automotive, semiconductor, aerospace, and telecom that simultaneously increases demand for specialized engineering talent and accelerates the rate of in-house talent shortfalls; the structural competitiveness of India's and Eastern Europe's engineering talent pipelines creating durable offshore delivery economics that will persist regardless of AI productivity improvements; and the AI-augmented engineering productivity revolution that multiplies the effective output of existing ESO delivery teams, reducing per-unit engineering cost while expanding total market revenues as clients outsource higher volumes of increasingly complex work at improving economics.

Research Methodology

Primary Research

Primary research comprised structured interviews with 85+ industry stakeholders (2025), including VP-Engineering and Chief Engineering Officers from Fortune 500 automotive OEMs, aerospace primes, and semiconductor companies; ESO provider commercial leaders from TCS Engineering, Infosys Engineering, Wipro, KPIT Technologies, and Capgemini Engineering; NASSCOM Engineering R&D Committee members; India GCC Association executives; and buy-side engineering procurement specialists at global OEMs managing annual ESO contracts.

Secondary Research

Secondary research encompassed NASSCOM Engineering R&D Report 2025, India Brand Equity Foundation IT-BPM Export Statistics 2024, Everest Group Engineering Research and Development Annual Report 2025, Nelson Hall ESO Market Assessment 2025, company investor presentations and annual reports, M&A transaction databases for ESO acquisitions (2020-2025), and CHIPS Act and European CHIPS Act engineering services demand analyses from Gartner and IDC. Over 160 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using a bottom-up application vertical x location model, calibrated against NASSCOM engineering export revenue data, Everest Group engineering services market sizing, and individual company engineering revenue disclosures. Key inputs include global R&D spending growth rates by industry, offshore ESO penetration rate trajectory models by application vertical, CHIPS Act and automotive EV investment-to-engineering-services conversion ratios, AI productivity multiplier adoption curves by 2034, and Latin America nearshore growth assumptions from USMCA economic data.

Engineering Services Outsourcing Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Services Covered | Designing, Prototyping, System Integration, Testing, Others |

| Locations Covered | Onshore, Offshore |

| Applications Covered | Aerospace, Automotive, Construction, Consumer Electronics, Semiconductors, Pharmaceuticals, Telecom, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | TATA Consultancy Services Limited, Infosys Limited, Wipro, HCL Technologies Limited, KPIT, Capgemini, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the engineering services outsourcing market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global engineering services outsourcing market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the engineering services outsourcing industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Engineering Services Outsourcing Market Report

The global engineering services outsourcing market reached USD 1,922.2 Billion in 2025, driven by automotive EV/SDV engineering demand, semiconductor complexity, and India's 2.55 million annual STEM graduates, enabling offshore delivery at a cost advantage.

The market grows at 14.42% CAGR during 2026-2034, reaching USD 6,460.5 Billion by 2034, driven by automotive SDV engineering outsourcing, CHIPS Act semiconductor engineering demand, AI-augmented offshore productivity, and GCC ecosystem maturation in India and Eastern Europe.

Onshore leads at 68.7% due to client proximity requirements, regulatory mandates, and IP protection needs for complex engineering.

Automotive leads at 25.4%, driven by EV, ADAS, and SDV engineering complexity requiring 40-60% outsourcing of software engineering by major OEMs.

Asia Pacific leads at 42.1%, anchored by India's dominant position with GCCs employing a high number of engineering professionals, 2.55 million annual STEM graduates, and IT-ESO export revenue, representing the world's largest and most competitive engineering services delivery ecosystem.

Leading companies include TATA Consultancy Services Limited, Infosys Limited, Wipro, HCL Technologies Limited, KPIT, and Capgemini, among others.

The market is projected to reach approximately USD 3,769.8 Billion by 2030, with automotive SDV engineering, semiconductor ESO, India offshore delivery achieving quality parity with onshore for most work types, and AI-augmented engineering platforms achieving 3-5x per-engineer productivity.

Cognizant's USD 1.3 Billion Belcan acquisition (2024) integrated aerospace and defense engineers, creating a combined entity targeting revenue synergies. It signals domain specialization as the primary ESO competitive differentiator, accelerating M&A consolidation among ESO providers seeking regulated-domain engineering depth.

Global Capability Centers (GCCs) are captive offshore engineering centers established by Fortune 500 OEMs in India. GCCs employ a high number of engineers in India, creating demand for GCC-as-a-Service models where TCS, Infosys, and Wipro establish and manage centers transitioning to client ownership within 3-5 years.

AI-augmented engineering tools multiply offshore engineer productivity by 3-5x per engineer for design iteration, simulation, and validation tasks. ESO providers with proprietary AI engineering platforms are commanding 30-50% productivity improvements that improve both project economics and competitive differentiation.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)