Europe Bancassurance Market Size, Share, Trends and Forecast by Product Type, Model Type, and Country, 2026-2034

Europe Bancassurance Market Size, Share, Trends & Forecast (2026-2034)

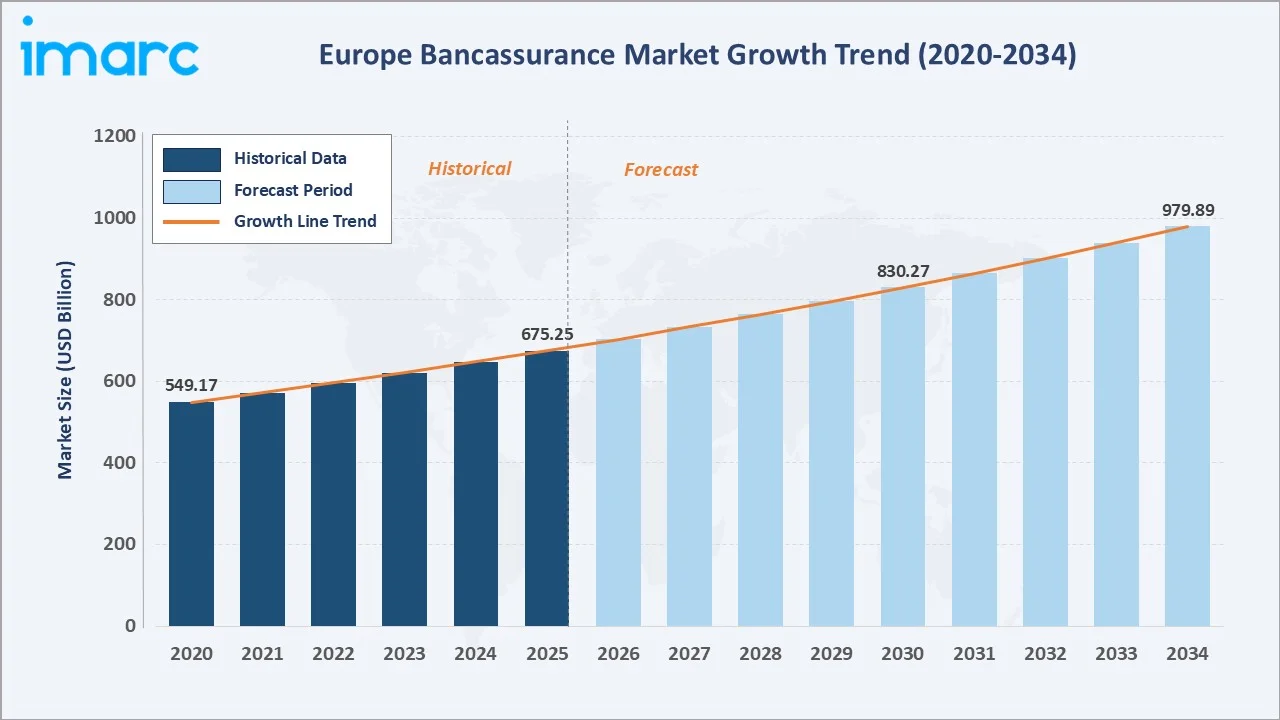

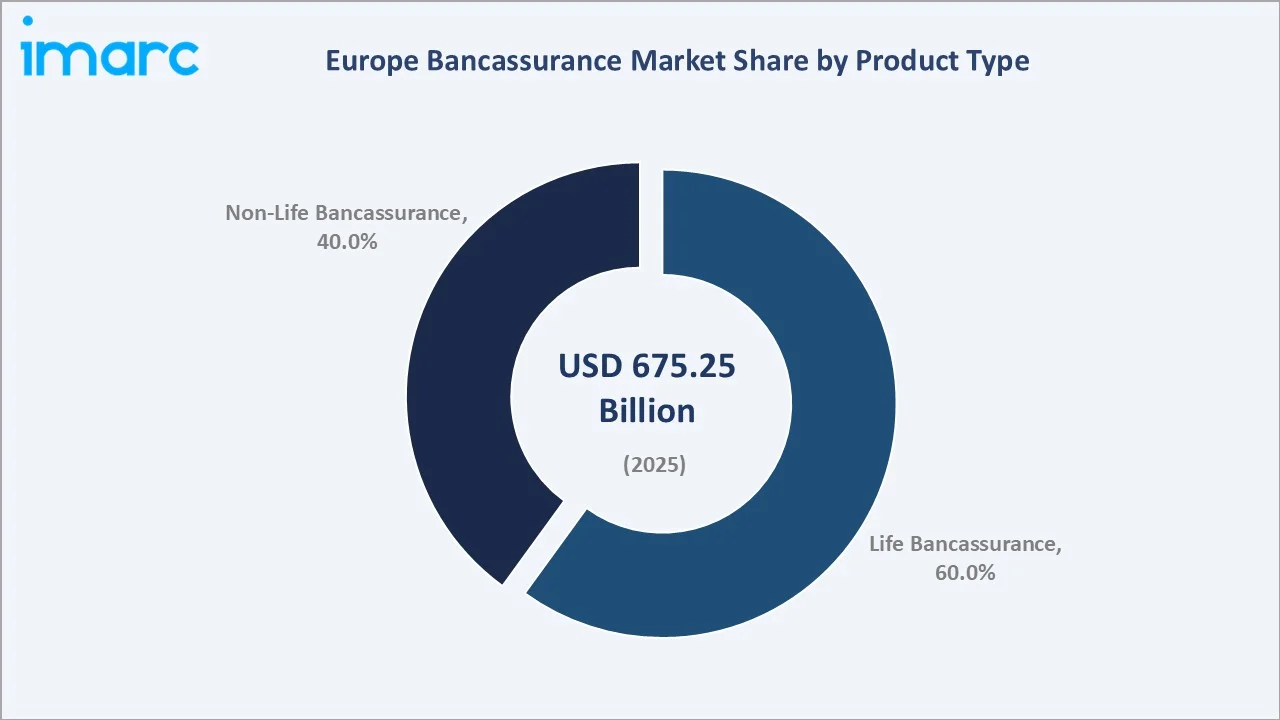

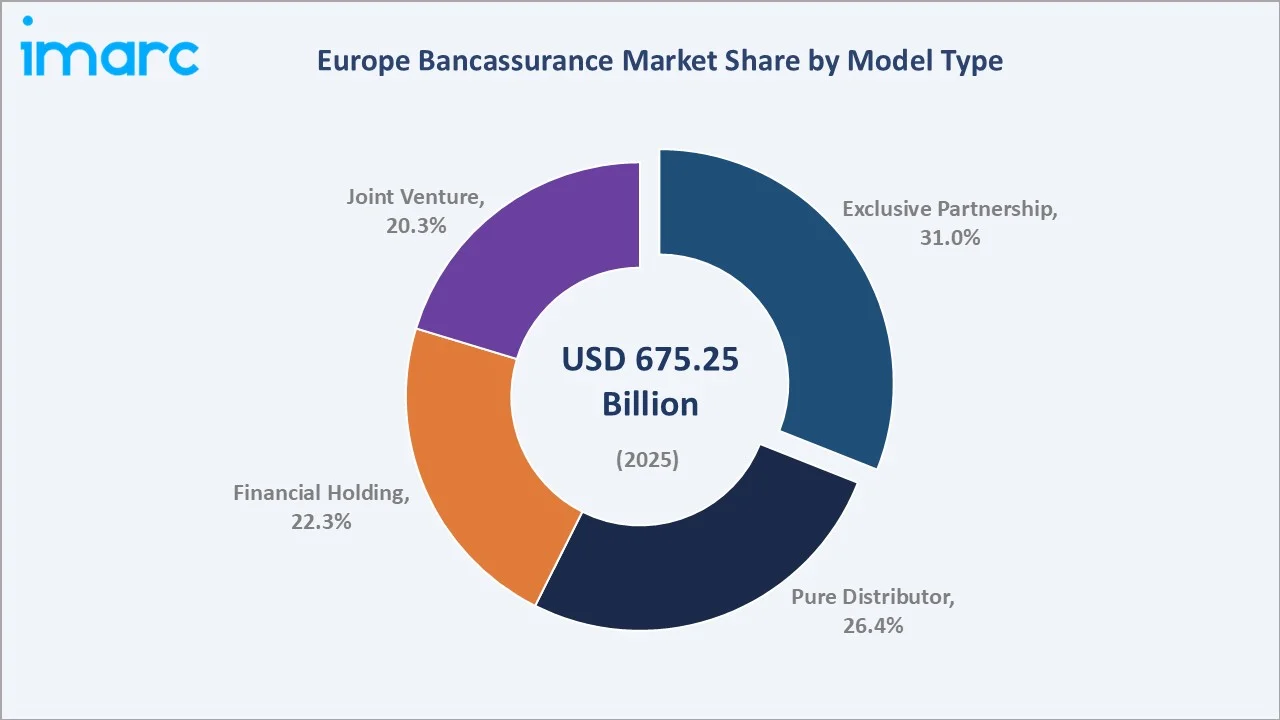

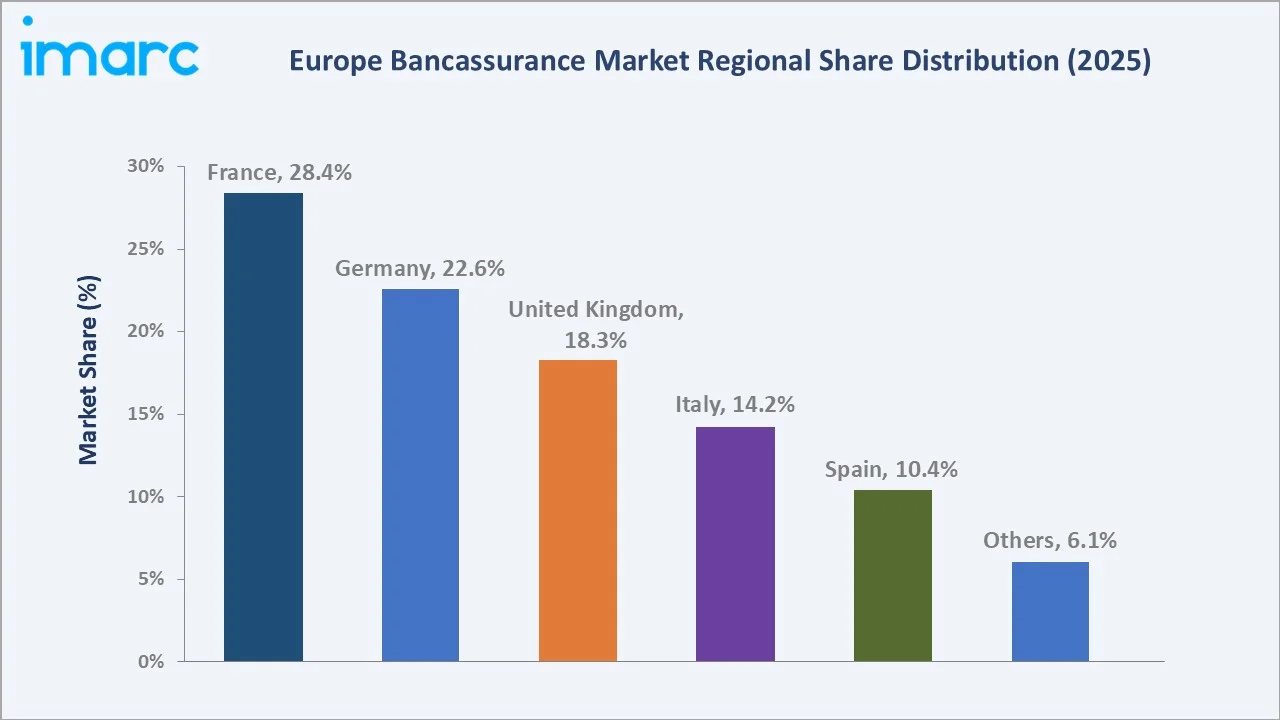

The Europe bancassurance market was valued at USD 675.25 Billion in 2025 and is projected to reach USD 979.89 Billion by 2034, expanding at a CAGR of 4.22% during the forecast period (2026-2034). Growth is driven by Europe’s rapidly ageing demographic, with the population aged 60 and above in WHO European Region increasing from 215 million in 2021 to an estimated 247 million by 2030, and surpassing 300 million by 2050, requiring pension and life protection products, digital banking integration enabling frictionless insurance embedding, post-COVID elevation of protection awareness, and rising mortgage markets fuelling creditor insurance demand. Life bancassurance dominates at 60.0% of market share, while exclusive partnership leads model types at 31.0%. France commands the largest country share at 28.4%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 675.25 Billion |

|

Forecast Market Size (2034) |

USD 979.89 Billion |

|

CAGR (2026-2034) |

4.22% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

France (28.4%, 2025) |

|

Fastest Growing Country |

Spain (CAGR ~4.6%, 2026-2034) |

To get more information on this market, Request Sample

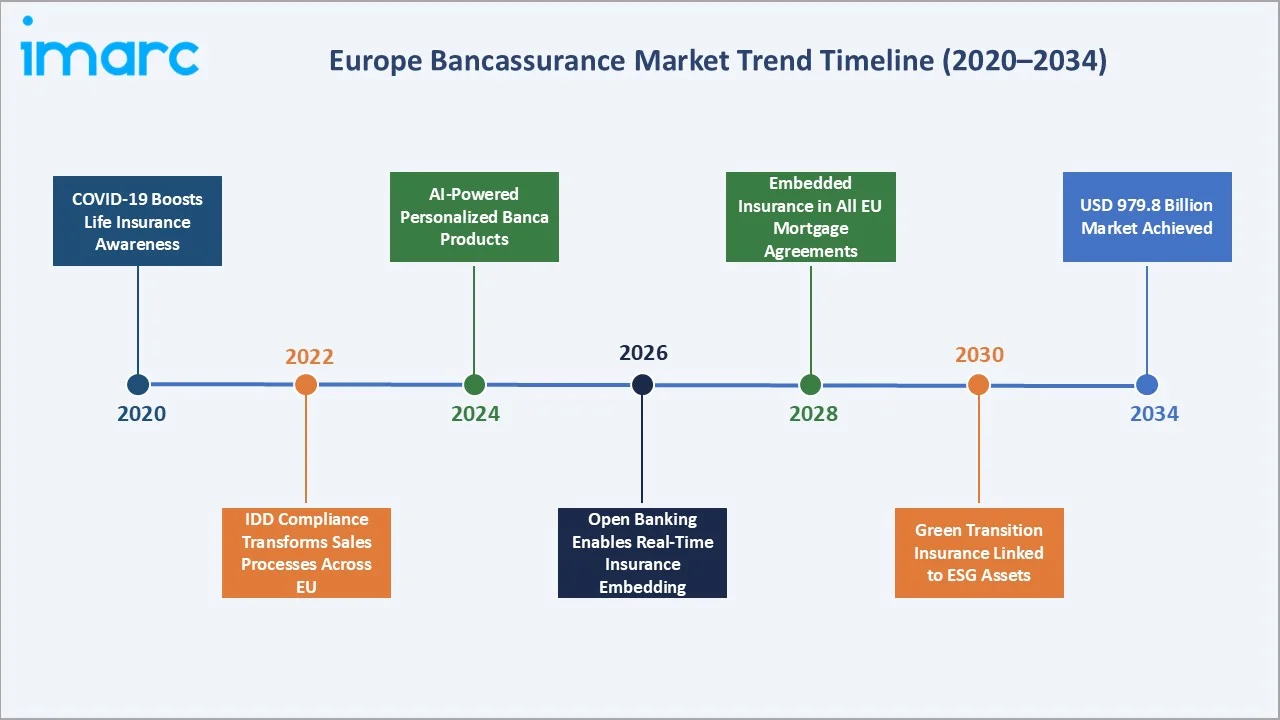

The Europe bancassurance market growth expanded from USD 549.17 Billion in 2020 to USD 675.25 Billion in 2025. Anchored at USD 830.27 Billion in 2030, the forecast to USD 979.89 Billion by 2034, supported by demographic-driven insurance demand and regulatory frameworks promoting integrated financial product distribution across Europe’s retail banking customers.

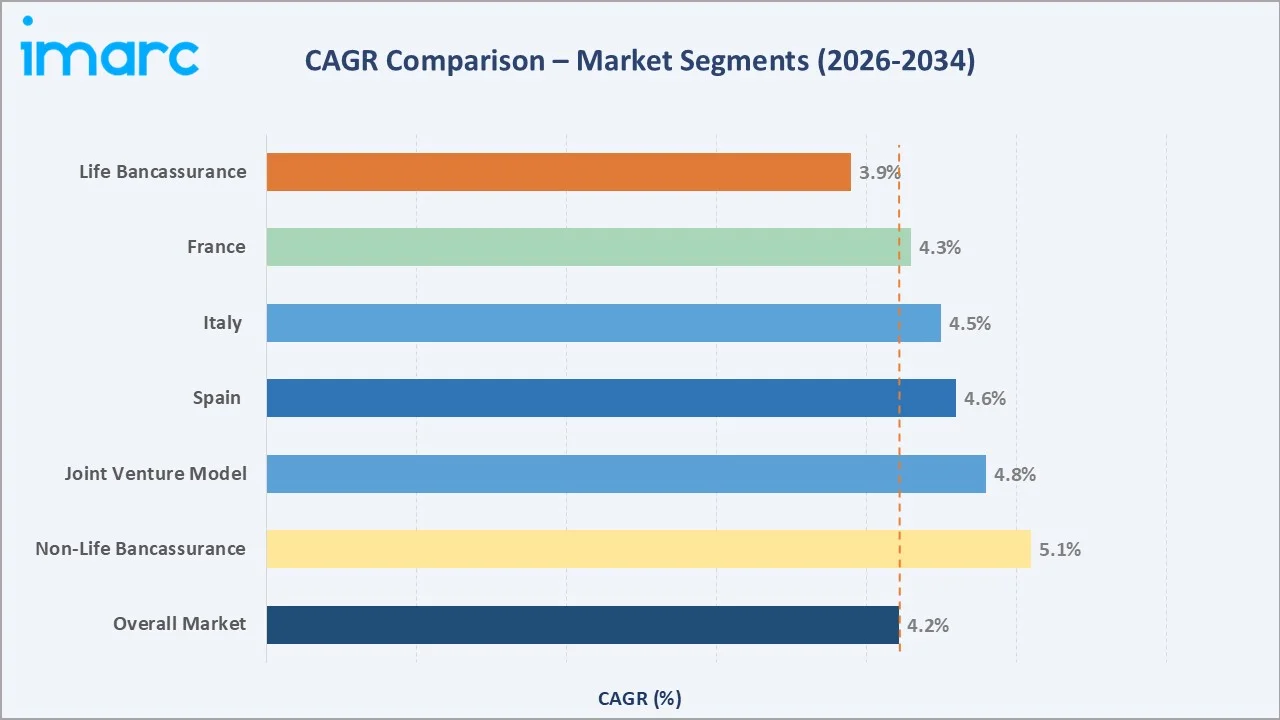

The CAGR across key segments with non-life bancassurance leads growth at ~5.1% CAGR, reflecting rising demand for home, motor, and health insurance products distributed through bank networks. Spain at ~4.6% CAGR outpaces the overall 4.22% market rate, driven by structural deepening of bancassurance penetration among Spanish banking groups including CaixaBank and BBVA.

Executive Summary

The Europe bancassurance market has grown steadily from USD 549.17 Billion in 2020 to USD 675.25 Billion in 2025, achieved through a period that included COVID-19’s disruption, rising interest rate cycles, and fundamental regulatory reform under the Insurance Distribution Directive (IDD). Europe pioneered the bancassurance concept and continues to operate the world’s most mature and institutionally embedded bank-insurance integration model. The forecast trajectory to USD 979.89 Billion by 2034 is anchored by two structural mega-trends: Europe’s demographic challenge and the digital banking revolution, enabling insurance products to be embedded within every significant financial life event, mortgage completion, pension contribution, savings account opening, and cross-border fund transfer.

Life bancassurance at 60.0% (2025) encompasses individual life insurance, endowment policies, unit-linked savings products, pension annuities, and creditor life insurance tied to mortgages and personal loans. Non-Life at 40.0% is the faster-growing segment at ~5.1% CAGR, driven by bancassurance expansion into home insurance (tied to mortgage origination), payment protection insurance, health supplementary insurance, and travel insurance embedded in premium debit card products.

France’s 28.4% leadership reflects the country’s unique bancassurance heritage. Germany’s 22.6% share is driven by Germany’s insurance market growth and the Sparkassen savings bank network’s retail banking market share, enabling systematic insurance cross-sell at local bank branches. Italy’s 14.2% market is uniquely concentrated through Intesa Sanpaolo Vita’s dominance as Italy’s largest life insurer, underscoring bancassurance’s structural penetration in Southern European markets.

Key Market Insights

|

Insight |

Data |

|

Dominant Product Type |

Life Bancassurance – 60.0% revenue share (2025) |

|

Dominant Model Type |

Exclusive Partnership – 31.0% revenue share (2025) |

|

Leading Country |

France – 28.4% revenue share (2025) |

|

Fastest Growing Country |

Spain (CAGR ~4.6%, 2026-2034) |

Key Analytical Observations Supporting The Above Data:

- Life Bancassurance dominates at 60.0% (2025): European banks distributed approximately EUR 400 billion in life insurance premiums, driven by unit-linked savings products, mortgage protection life insurance, and pension savings products that are systematically cross-sold at the point of home purchase, retirement planning, and inheritance management.

- Exclusive Partnership leads at 31.0% (2025): The exclusive partnership model, where a bank distributes products from a single insurance partner exclusively, generates the highest cross-sell intensity and brand consistency, with penetration rates higher than non-exclusive arrangements.

- France leads at 28.4% (2025): France’s bancassurance market is unique globally, banks control high life insurance distribution nationally.

Europe Bancassurance Market Overview

Bancassurance is the integrated distribution of insurance products through banking channels, leveraging the bank’s customer relationship, branch network, digital platform, and financial data to offer complementary insurance protection, savings, and investment products alongside core banking services. The European bancassurance ecosystem encompasses four distinct structural models: pure distributor, exclusive partnership, financial holding, and joint venture.

Applications span life protection, pension and retirement savings, creditor insurance, property and casualty, and health supplementary insurance. Macroeconomic influences include ECB interest rate policy, EU capital markets union development, demographic aging, and digital banking penetration rates that determine the frequency and depth of bancassurance customer engagement.

Market Dynamics

To evaluate market opportunities, Request Sample

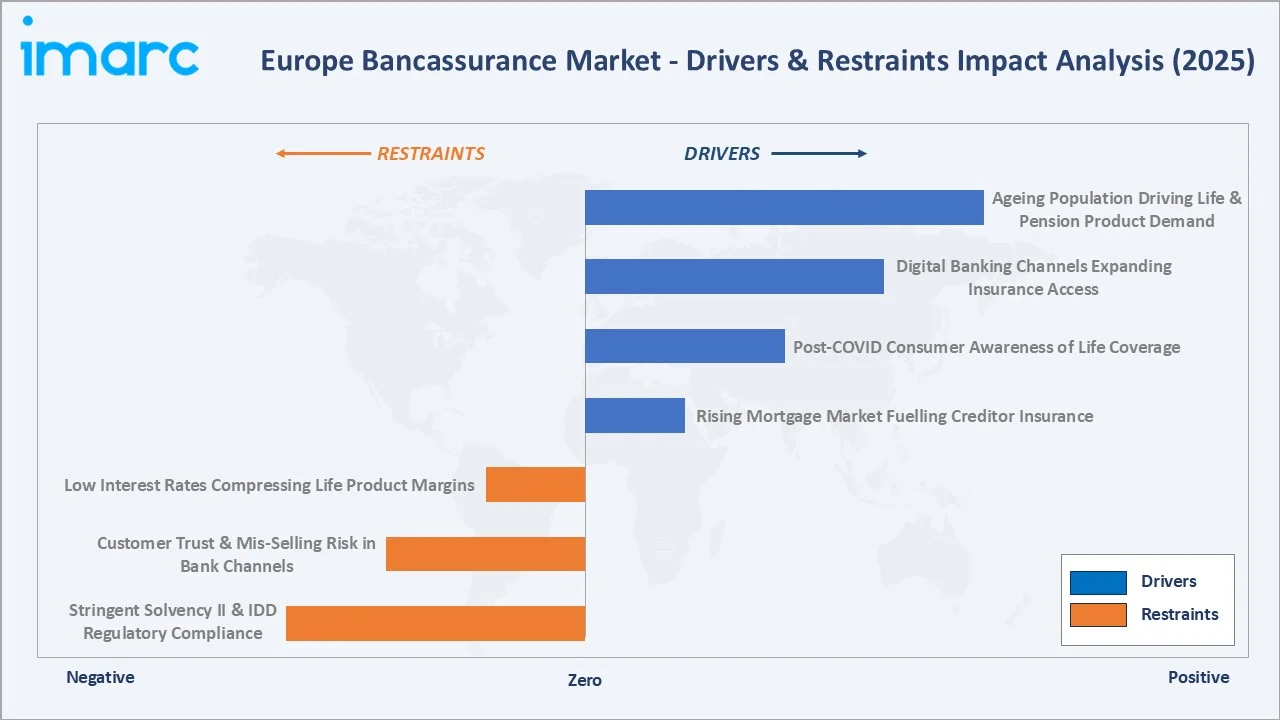

Market Drivers

- Europe’s Ageing Population Creating Structural Protection Demand: The population aged 60 and above in the WHO European Region is expanding quickly, increasing from 215 million in 2021 to an estimated 247 million by 2030, and surpassing 300 million by 2050, creating the largest per-capita concentration of retirement savings and protection product demand ever seen in European financial services.

- Digital Banking Integration Exponentially Expanding Insurance Touchpoints: Online, 46% of adults frequently use payment cards, 25% use mobile apps, and 17% prefer bank transfers. The digital engagement transformation enables bancassurance to be embedded at precise moments of financial need, when a customer checks their mortgage statement, transfers money abroad (travel insurance), or receives a salary.

- Consumer Protection Awareness Permanently Elevated Post-COVID: The structural shift in protection awareness is converting latent insurance demand into active purchasing behavior, benefiting bancassurance’s trusted bank relationship as the primary insurance recommendation channel over independent agents and direct insurers for consumers who were previously uninsured or under-insured.

Market Restraints

- Solvency II and IDD Compliance Creating Substantial Cost Burden: The Insurance Distribution Directive (IDD), transposed into national law across 27 EU member states, mandates IPID/KID documentation for all bancassurance distribution.

- Persistent Low-Yield Environment Compressing Life Product Attractiveness: European life bancassurance products, particularly guaranteed-return traditional life savings policies, face structural margin compression from the 2012–2022 decade of near-zero interest rates that forced insurers to guarantee returns that became unprofitable as yields declined.

Market Opportunities

- ESG-Linked Bancassurance Products for European Green Transition: The EU’s EUR 1 trillion European Green Deal investment program is creating a new category of ESG-linked bancassurance products, green mortgage payment protection linked to energy-efficient home improvements, renewable energy equipment insurance, and sustainable investment-linked life savings products with verified ESG credentials.

- Open Banking and Embedded Finance Creating Real-Time Insurance Moments: The EU’s Financial Data Access regulation (FiDA), expected from 2026, will enable insurance providers to access bank customer financial data with consent to deliver hyper-personalised insurance recommendations in real time.

Market Challenges

- Technology Modernisation Debt in Legacy Core Banking Systems: Bancassurance platform integration requires real-time data connectivity between the bank’s core banking system and the insurance partner’s underwriting and policy administration system, a technical integration that many European banks still execute through batch file transfers rather than real-time APIs.

- InsurTech Competition and Disintermediation Risk: Direct-to-consumer digital insurance platforms are growing in Europe, targeting the under-35 customer segment that represents bancassurance’s future customer base.

Emerging Market Trends

1. AI-Powered Personalised Bancassurance Recommendations

Artificial intelligence platforms analysing banking transaction history, mortgage holding, family status, and financial profile are enabling European banks to deliver precisely timed, individually personalised insurance recommendations.

2. Embedded Insurance at Every Financial Life Event

The convergence of open banking APIs, real-time underwriting, and digital customer journeys is enabling insurance to be embedded invisibly within every significant financial transaction, mortgage completion, car finance drawdown, foreign exchange transfer, and savings account opening.

3. Health and Wellness Bancassurance Emerging as New Growth Category

Post-COVID consumer health consciousness is driving European banks into supplementary health insurance, dental, vision, mental health, and digital GP access. products that complement national health systems with private coverage.

4. Sustainability-Linked Life Products Under EU Green Finance Agenda

The EU’s Sustainable Finance Action Plan is cascading into bancassurance product design, with SFDR Article 8 and 9 classifications being applied to unit-linked life savings products and the EU Taxonomy creating new standards for sustainable underwriting in non-life bancassurance.

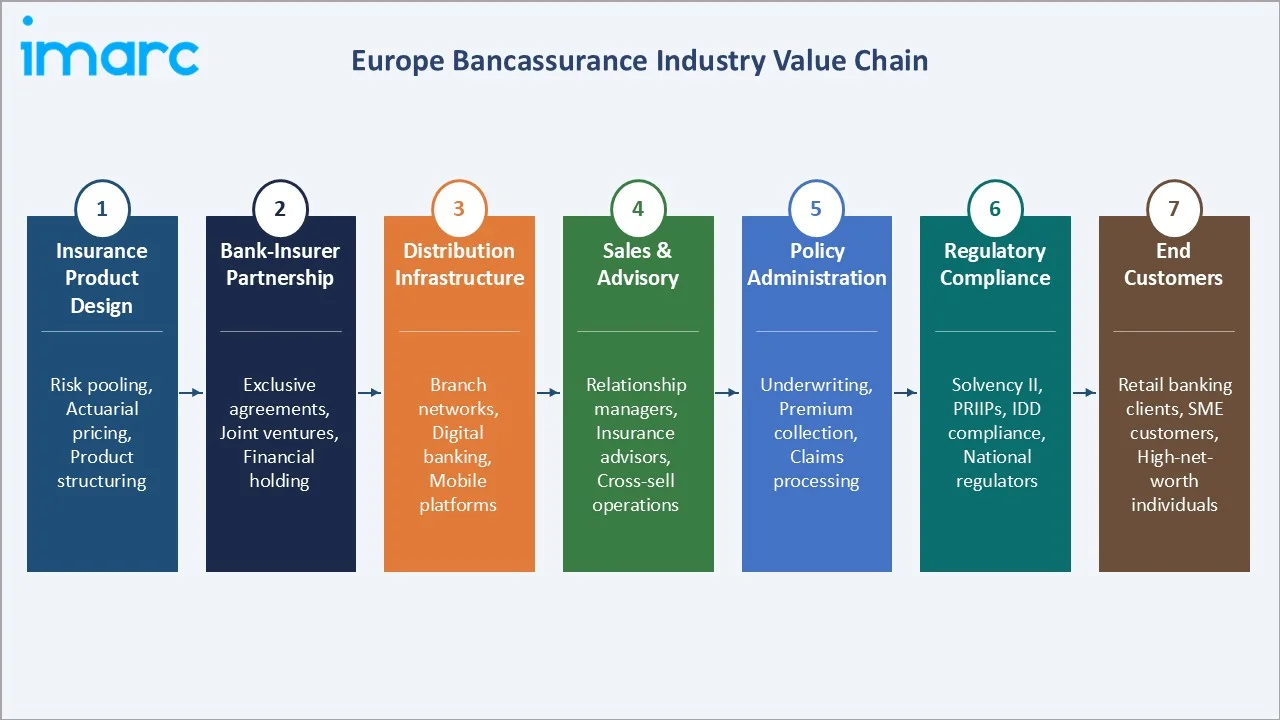

Industry Value Chain Analysis

The Europe bancassurance value chain spans insurance product design and underwriting through partnership structuring, multi-channel distribution, policy servicing, and regulatory compliance, with value captured at each stage by specialist participants operating under rigorous dual financial services supervision.

|

Stage |

Key Participants |

|

Insurance Product Manufacturing & Underwriting |

Underwriting life, health, property, creditor, and pension products for bank distribution |

|

Bancassurance Partnership Agreement |

Defining product scope, commission structures, and compliance frameworks |

|

Sales & Distribution (Bank Branch Network) |

Point-of-sale insurance recommendation at the moment of financial product need |

|

Digital & Mobile Bancassurance Channels |

Enabling self-service insurance purchase embedded within digital financial journeys |

|

Customer Service & Claims Management |

Back-office claims teams, call centres, digital claims portals are managed by the insurance partner under the bank’s SLA commitments and brand promise |

|

Regulatory Compliance & Conduct Oversight |

European Central Bank (ECB), EIOPA, national supervisory authorities, monitoring IDD compliance, Solvency II capital adequacy, and PRIIPs KID obligations |

|

End Clients (Insurance Policyholders) |

Retail banking customers (mortgage, personal loan, savings), private banking clients, SME business owners, corporate treasury clients purchasing creditor and liability products through banks |

Insurance product manufacturers capture 40-50% of bancassurance value chain economics through underwriting spread and asset management fees, while banks retain 20–35% through distribution commissions, which typically range from 15-25% of first-year premium for life products and 8-18% for non-life products. Under financial holding and joint venture models, the bank captures an additional 30-40% through ownership of the insurance entity’s profits, creating the highest total economic return of any bancassurance model structure.

Technology Landscape in the Europe Bancassurance Industry

AI and Machine Learning for Needs Analysis and Propensity Scoring

Leading European bancassurers are deploying AI-powered customer analytics that analyse 50-200 data points, banking product holdings, transaction behaviour, life stage signals, and financial vulnerability indicators, to generate real-time insurance coverage gap assessments and next-best-action recommendations. BNP Paribas' 900 APIs handle 700 million transactions monthly across the Group's platforms. The company is fully committed to artificial intelligence (AI), with over 750 use cases in development and more than 300 currently being explored or tested.

Digital Claims Management and Straight-Through Processing

Bancassurance customer satisfaction is heavily dependent on claims experience, the moment of truth that validates or destroys the bank-insurance relationship. AI-powered claims automation is reducing claims settlement times from 15–30 days to 24–48 hours for straightforward payment protection and home insurance claims.

Regulatory Technology (RegTech) for IDD and Solvency II Compliance

IDD compliance, requiring pre-sale suitability assessment, conflict of interest disclosure, and product oversight and governance documentation for every bancassurance sale, created a substantial RegTech adoption wave in European banking.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Life Bancassurance |

60.0% |

2025 |

|

Model Type |

Exclusive Partnership |

31.0% |

2025 |

|

Country |

France |

28.4% |

2025 |

By Product Type

To access detailed market analysis, Request Sample

Life bancassurance dominates at 60.0% market share (2025). This segment encompasses individual term life insurance, whole life policies, endowment savings products, unit-linked investment-linked products, pension annuities, group life insurance distributed through corporate banking relationships, and mortgage payment protection life insurance.

Non-Life bancassurance at 40.0% is significantly faster than life, as European banks systematically expand into property insurance, payment protection insurance, health supplementary insurance, travel insurance, and cyber protection products for SME banking clients.

By Model Type

Exclusive Partnership leads at 31.0% market share (2025), representing the arrangement where the bank distributes insurance from a single designated partner exclusively across all distribution channels. This model achieves the highest cross-sell intensity and operational efficiency, as bank advisors are trained on a single product range, digital systems are deeply integrated with a single insurance partner, and marketing investment is concentrated on one joint brand.

Pure distributor at 26.4% represents banks acting as multi-product insurance agents selling policies from multiple insurers as a distribution intermediary without exclusive commitment. Financial holding at 22.3% covers banks owning insurance subsidiaries as fully consolidated group entities, exemplifying this structure. Joint venture at 20.3% represents co-owned entities where bank and insurer share capital, governance, and profits seek the middle path between agency distribution and full ownership.

Country Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

France |

28.4% |

French Loi Hamon enabling consumer switching of bancassurance tied to mortgage loans |

|

Germany |

22.6% |

Commerzbank non-life expansion under regulatory pressure; Allianz bank subsidiary direct bancassurance |

|

United Kingdom |

18.3% |

Lloyds Banking Group’s Scottish Widows insurance division; Barclays insurance products via Barclays Insurance; HSBC bancassurance expansion post-Brexit |

|

Italy |

14.2% |

UniCredit CreditRas bancassurance partnership; Italian bancassurance channel distributes 75%+ of life insurance premiums nationally |

|

Spain |

10.4% |

Spanish bancassurance distributes 80%+ of all life insurance sold nationally, among EU’s highest penetration rates |

|

Others |

6.1% |

Netherlands (ING’s NN Group spin-off model); Belgium (KBC Groupe integrated bancassurance model); Switzerland (UBS, Credit Suisse bancassurance); Poland (PKO BP, mBank bancassurance growth) |

France’s 28.4% market dominance (2025) reflects the country’s five-decade history as the global birthplace and capital of bancassurance. The French bancassurance ecosystem is uniquely deep; banks distribute 65% of all life insurance nationally, creating a structural market position for bank-distributed insurance that independent agents and direct insurers have been unable to dismantle despite 50 years of competition.

Germany’s 22.6% share reflects a bancassurance market that is large in absolute terms but relatively less bank-dominated than France, with independent brokers and tied agents maintaining good share of life insurance distribution. The UK’s 18.3% share is shaped by the aftermath of the PPI mis-selling scandal, the largest consumer financial services mis-selling case in history, which imposed significant structural caution on UK bancassurance product development and sales practices.

Competitive Landscape

The Europe bancassurance market is moderately concentrated among the largest universal banking groups, with BNP Paribas, Crédit Agricole, and The Intesa Sanpaolo Assicurazioni Group collectively representing approximately 35–40% of European bancassurance premium volume.

|

Company Name |

Brand / Insurance Services |

Market Position |

Core Strength |

|

BNP Paribas Cardif |

Creditor/Loan Protection Insurance, Life Savings, Personal Protection (Death, Disability, Health), and Affinity Insurance |

Market Leader |

One of Europe’s largest bancassurer by premium volume; life savings and creditor insurance as primary product engines |

|

Crédit Agricole |

Predica, Pacifica, Crédit Agricole Creditor Insurance, Spirica. |

Market Leader |

France’s largest life insurer with huge policyholders; Crédit Agricole’s Predica subsidiary managing high assets |

|

Intesa Sanpaolo Assicurazioni S.p.A. |

Insurance solutions for People, Properties, and Wealth |

Strong Challenger |

Italy’s largest bancassurer, financial holding model with full insurance ownership |

|

UniCredit S.p.A. |

UniCredit Life Insurance (ULI), UniCredit Vita Assicurazioni (UVA) |

Established |

Bancassurance operations in Italy |

|

Barclays Bank PLC |

Life insurance, Tech insurance, Travel and breakdown insurance |

Established |

UK bancassurance across personal lines |

|

NN Group |

ABN AMRO Levensverzekering N.V. |

Established |

ABN AMRO Bank N.V. sold ABN AMRO Levensverzekering N.V. to NN Group in November 2022. |

The top five bancassurers account for approximately 50–55% of total European bancassurance market value. However, the remaining 45–50% is distributed across national and regional banks operating bancassurance partnerships across Europe’s 27 EU member states, plus the UK and Switzerland, creating a fundamentally fragmented mid-market.

Key Company Profiles

BNP Paribas Cardif

BNP Paribas is Europe’s largest bancassurer and the world’s leading bank-distributed insurance group, which operates in 30+ countries.

- Product Portfolio: Insurance and Services for the Automotive Industry, Retailers, Financial advisors & brokers.

- Recent Developments: In December 2025, BNP Paribas and Ageas Groups signed a framework agreement covering savings, protection and property & casualty insurance, and brought together BNP Paribas Fortis and AG Insurance’s expertise, as the leading insurer in Belgium, to serve their clients.

- Strategic Focus: Cardif as standalone bancassurance manufacturing global leader serving 3rd-party banks; digital API-enabled embedded insurance for mobile banking integration globally; ESG product development under SFDR Article 8/9 for European sustainable finance compliance; CEE expansion through new bank distribution partnerships in Poland, Czech Republic, and Romania.

Intesa Sanpaolo Assicurazioni S.p.A.

Intesa Sanpaolo is Italy’s largest bank and Europe’s most profitable integrated bancassurer, operating Intesa Sanpaolo Vita and RBM Assicurazione (health) as fully consolidated insurance entities within the financial holding structure.

- Product Portfolio: Insurance solutions for People, Properties, and Wealth.

- Recent Developments: In February 2026, Intesa Sanpaolo Assicurazioni announced its membership in the Conference of European Bancassurers (CEB), becoming the first operator in the Italian bancassurance market to join the CEB.

- Strategic Focus: Insurance as strategic profit diversification from net interest income compression; financial holding model maximising economic profit capture across underwriting, asset management, and distribution; ESG product range under EU sustainable finance disclosure rules; digital bancassurance portal reducing servicing costs 30–40% versus branch-based model; health bancassurance expansion as supplementary care market grows with Italian ageing demographics.

Barclays Bank PLC

Barclays operates a focused non-life bancassurance model in the UK, distributing home and travel insurance products through its UK retail banking customers.

- Product Portfolio: Life insurance, Tech insurance, Travel and breakdown insurance.

- Recent Developments: Barclays partnered with Nimbla, a pioneer of single invoice insurance in January 2020.

- Strategic Focus: Consumer Duty compliance as brand trust rebuilding strategy; digital-first home insurance at mortgage completion as non-life bancassurance anchor; premium current account insurance bundles as switching incentive and revenue diversification; workplace pension SME distribution as B2B bancassurance growth avenue; transparent opt-in digital insurance sales as differentiation from legacy PPI-era practices.

Market Concentration Analysis

The Europe bancassurance market exhibits moderate concentration at the distribution tier and moderate-to-high fragmentation at the country and product level. BNP Paribas Cardif’s represents approximately 4–5% of total European bancassurance market value, while the top five bancassurers combined account for an estimated 40–45% of European bancassurance premium volume.

Market fragmentation is pronounced at the national level, where 20–30 national banking groups in each major European market operate bancassurance partnerships, creating competitive dynamics unique to each country’s banking market structure. France’s six major banking groups collectively dominate national bancassurance, creating high national concentration. The UK’s post-PPI recovery opened market share for digital and transparent bancassurance entrants. Italian bancassurance’s concentration around Intesa Sanpaolo Vita creates a quasi-monopoly in individual life bancassurance that smaller Italian banks are unable to challenge.

Investment & Growth Opportunities

Fastest Growing Segments

Non-Life bancassurance (~5.1% CAGR), Health bancassurance (~10–12% CAGR), Digital-embedded insurance (~15–20% CAGR), and ESG-linked life savings (~8–10% CAGR) represent the four highest-growth investment vectors in the Europe bancassurance market through 2034. CEE market bancassurance penetration growth at 7–10% CAGR represents the highest-growth geographic opportunity for established Western European bancassurers seeking new distribution markets.

Emerging Market Opportunities

Poland’s PKO BP and mBank bancassurance markets growth transitions toward bank-channel dominance. Romania’s Bancpost, BCR, and BRD represent a growth opportunity in the bancassurance market. Baltic states’ Scandinavian-owned banking groups are building bancassurance capabilities across Estonia, Latvia, and Lithuania’s combined insurance markets.

Investment and Partnership Themes

The primary investment themes driving European bancassurance capital flows include digital platform build-out, ESG product development under SFDR Article 8/9 frameworks, InsurTech partnerships for digital product distribution, and regulatory technology investment for IDD and Consumer Duty compliance automation.

- Key digital investment themes: AI-powered personalisation platforms, open banking API insurance embedding, digital claims automation, and mobile app insurance marketplace development are the four highest-priority technology investment categories in European bancassurance through 2028.

- Partnership and M&A activity: CNP Assurances’ equity stake acquisitions in bank insurance subsidiaries, BNP Paribas Cardif’s 3rd-party bank partnership expansion, and Generali’s Cattolica Assicurazioni bancassurance integration represent the 2024–2026 consolidation wave.

Future Market Outlook (2026-2034)

The Europe bancassurance market is positioned for sustained, structurally anchored growth through 2034. From USD 675.25 Billion in 2025, the market is forecast to reach USD 979.89 Billion by 2034, growing at a 4.22% CAGR. This growth is underpinned by three irreversible megatrends: Europe’s demographic destiny with documented retirement savings gaps requiring systematic private provision through bancassurance; the digital banking revolution permanently multiplying insurance cross-sell occasions from annual branch events to daily digital touchpoints; and the EU regulatory framework’s progressive requirement for personal pension and long-term savings adequacy that designates bancassurance as the primary accessible delivery channel for most European retail banking customers.

Between 2026 and 2030, the defining transformation will be the mainstream adoption of embedded insurance, where insurance coverage is purchased invisibly and automatically within financial product journeys rather than through separate insurance sales processes. The 2030–2034 period will be defined by the maturation of health and wellness bancassurance as a major new revenue category, as supplementary health insurance becomes systematically distributed through the banking relationships that already serve Europe’s population. The green transition will have produced a significant new category of climate-linked bancassurance, renewable energy equipment insurance, EV fleet insurance through bank auto finance, and green mortgage protection linked to energy efficiency improvements.

Research Methodology

Primary Research

Primary research included structured interviews with 130+ industry stakeholders in 2025, including bancassurance product managers at major European banks, insurance company distribution directors, EIOPA policy officers, national supervisory authority representatives, bancassurance technology vendors, and independent financial advisors. Geographic coverage spanned France, Germany, the UK, Italy, Spain, the Netherlands, Belgium, and Poland.

Secondary Research

Secondary research encompassed Insurance Europe annual statistics, EIOPA Annual Report and Consumer Trends Reports, ECB Banking Supervision Annual Reports, national insurance association data, company annual reports and investor presentations, KPMG and McKinsey European bancassurance benchmarking studies, and European Commission financial services regulatory publications. Over 220 secondary sources were reviewed.

Forecasting Models

Market size forecasts were developed using a bottom-up product-country matrix validated against top-down. Key inputs include ECB interest rate forward curves, European mortgage market recovery projections, demographic ageing models (Eurostat), open banking adoption timelines, and IDD regulatory implementation assessment by country.

Europe Bancassurance Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Life Bancassurance, Non-Life Bancassurance |

| Model Types Covered | Pure Distributor, Exclusive Partnership, Financial Holding, Joint Venture |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | BNP Paribas Cardif, Crédit Agricole, Intesa Sanpaolo Assicurazioni S.p.A., UniCredit S.p.A., Barclays Bank PLC, NN Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe bancassurance Market Report

The Europe bancassurance market was valued at USD 675.25 billion in 2025 and is projected to reach USD 979.89 billion by 2034.

The Europe bancassurance market is forecast to grow at a CAGR of 4.22% during 2026-2034, driven by demographic ageing, digital banking expansion, mortgage market recovery, and open banking enabling embedded insurance.

Life bancassurance leads with 60.0% market share (2025), driven by pension, endowment, creditor life, and unit-linked savings products cross-sold through banks’ retail and mortgage lending relationships.

Exclusive Partnership leads at 31.0% market share (2025), delivering the highest cross-sell intensity.

France leads with 28.4% market share (2025), with banks distributing 65%+ of all national life insurance. BNP Paribas Cardif and CNP Assurances anchor France’s globally unparalleled bancassurance penetration.

Key market players include BNP Paribas Cardif, Crédit Agricole, Intesa Sanpaolo Assicurazioni S.p.A., UniCredit S.p.A., Barclays Bank PLC, and NN Group.

Key drivers include Europe’s ageing demographic creating pension demand, digital banking expanding insurance touchpoints, mortgage market recovery boosting creditor insurance, and post-COVID protection awareness elevation.

Key trends include AI personalised insurance recommendations, open banking embedded insurance, health and wellness bancassurance expansion, ESG-linked life savings products, and CEE market penetration growth at 7–10% CAGR.

Solvency II governs insurance capital adequacy; Insurance Distribution Directive (IDD) governs bancassurance sales conduct; PRIIPs regulation governs product disclosure; MiFID II applies to investment-linked bancassurance products.

Top opportunities include digital embedded insurance platforms, health bancassurance expansion, ESG-linked life savings, CEE market penetration, open banking-powered real-time insurance, and AI-driven personalisation technology.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)