Europe Cosmetics Market Size, Share, Trends and Forecast by Product Type, Category, Gender, Distribution Channel, and Country, 2026-2034

Europe Cosmetics Market Size, Share, Trends & Forecast (2026-2034

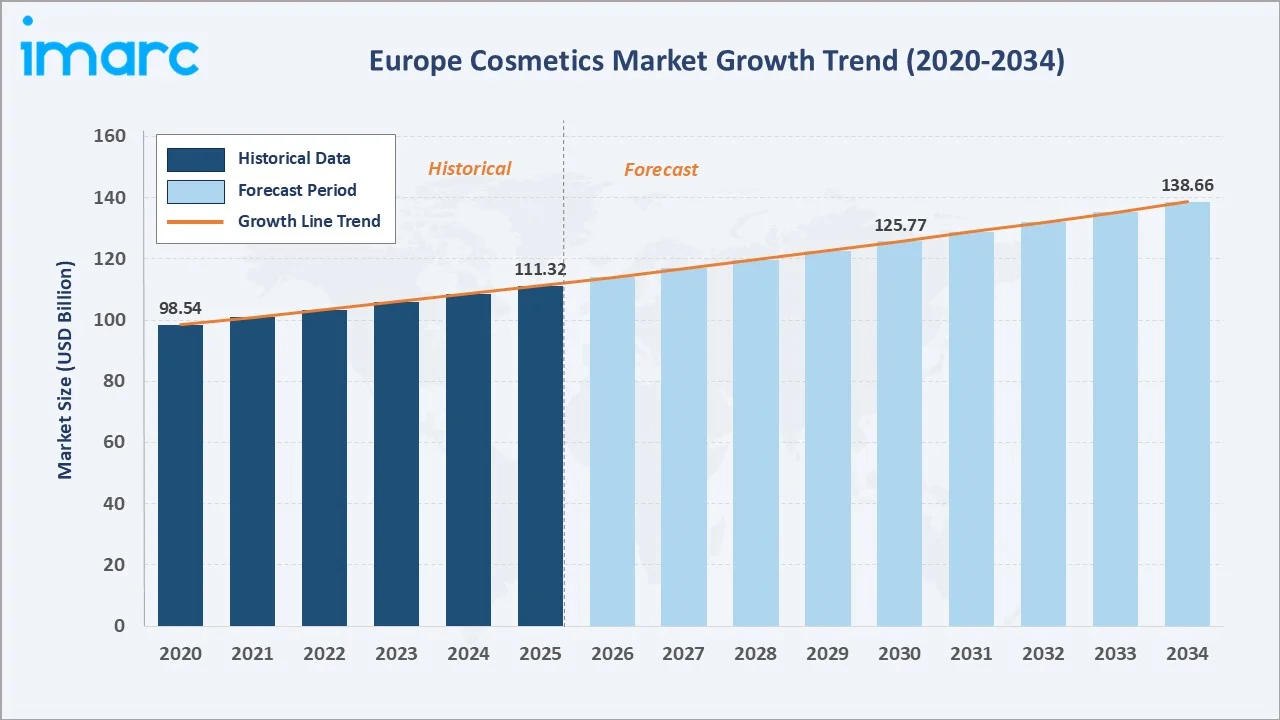

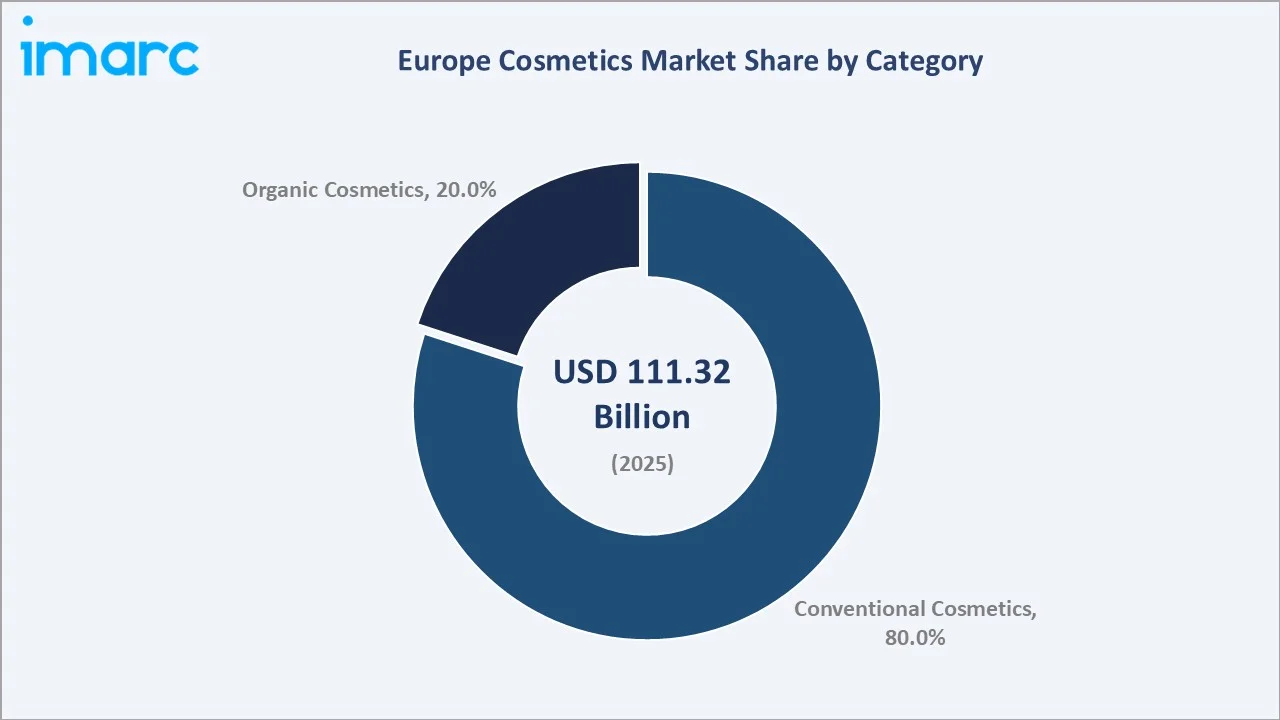

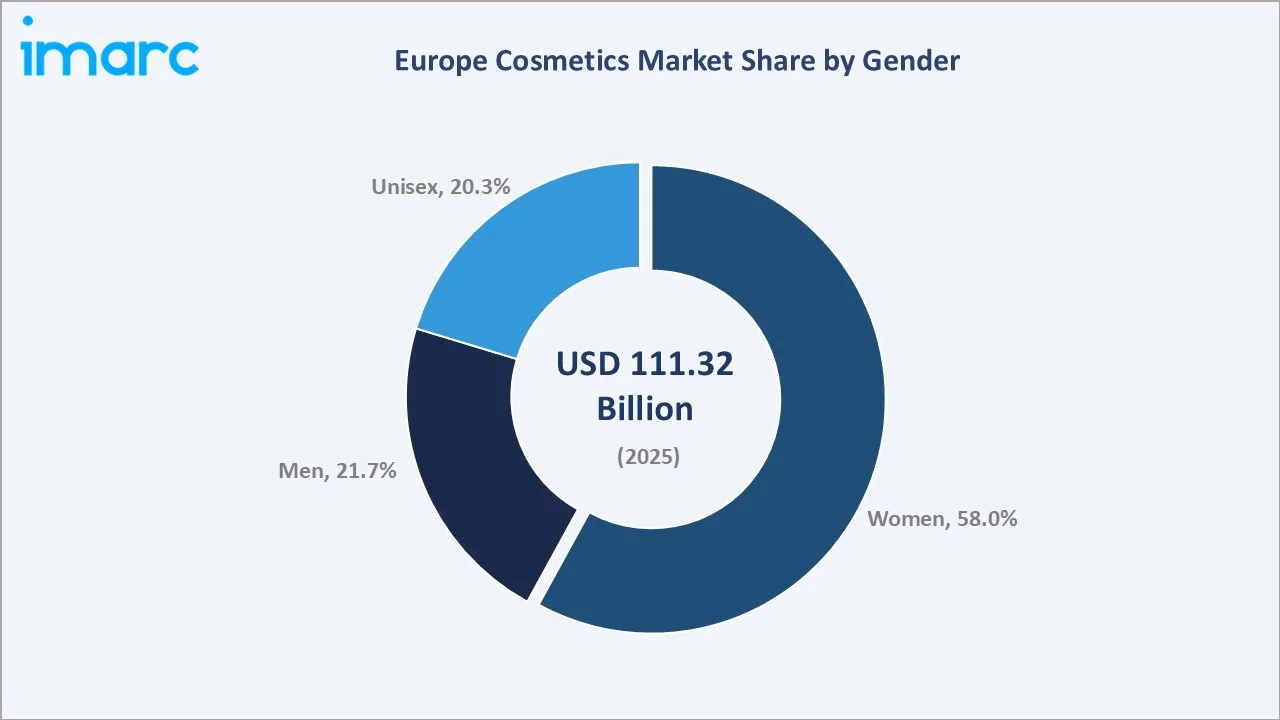

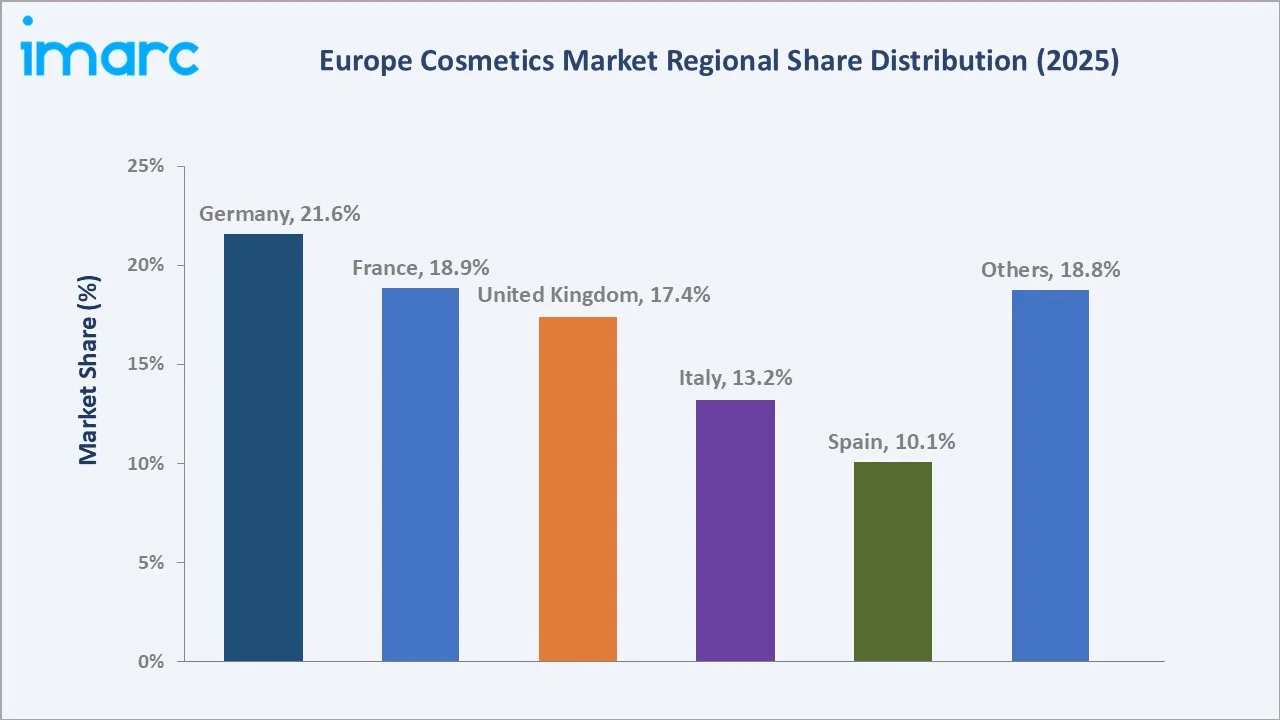

The Europe cosmetics market size was valued at USD 111.32 Billion in 2025 and is projected to reach USD 138.66 Billion by 2034, exhibiting a CAGR of 2.47% during the forecast period 2026-2034. Premiumization, the mainstreaming of clean and natural beauty, accelerated e-commerce and social-commerce adoption, rising male-grooming and unisex demand, and dermocosmetic innovation are driving the Europe cosmetics market growth. Conventional products lead the category mix at 80.0% share in 2025, while women account for 58.0% of consumer demand. Germany dominates country revenue with 21.6% of the European market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 111.32 Billion |

|

Forecast Market Size (2034) |

USD 138.66 Billion |

|

CAGR (2026-2034) |

2.47% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

Germany (21.6% share, 2025) |

|

Leading Category |

Conventional (80.0%, 2025) |

|

Leading Gender Segment |

Women (58.0%, 2025) |

The Europe cosmetics market growth trajectory from 2020 through 2034 reflects a resilient post-pandemic recovery, the sustained premiumization of skincare and fragrance, and the structural rise of clean-beauty, male-grooming, and unisex categories across Germany, France, the UK, Italy, and Spain.

To get more information on this market, Request Sample

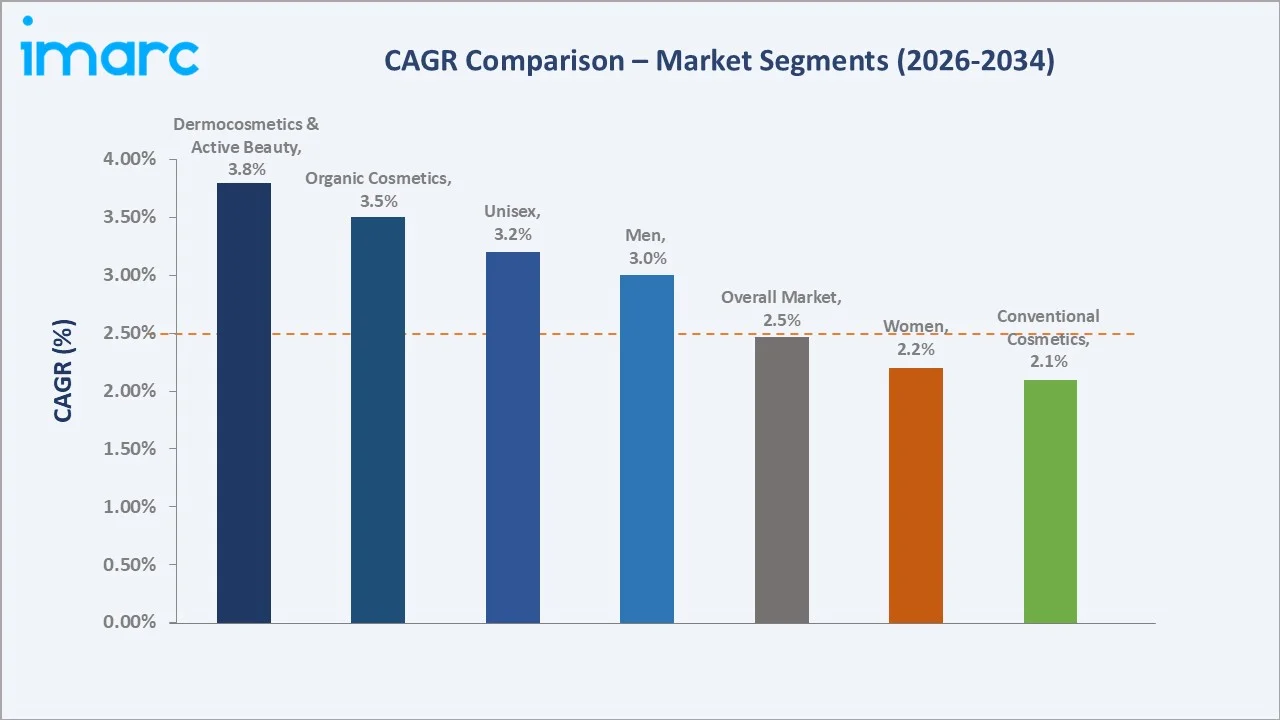

Segment-level CAGR comparisons highlight dermocosmetics & active beauty and organic cosmetics as the fastest-growing sub-categories within the Europe cosmetics market forecast through 2034, while conventional cosmetics and women-focused formulations trail the market average.

Executive Summary

The Europe cosmetics market is entering a mature but structurally evolving phase, shaped by premiumization, sustainability, and digital-first consumer behaviour. Valued at USD 111.32 Billion in 2025, the market is forecast to reach USD 138.66 Billion by 2034 at a CAGR of 2.47%, adding billions in incremental consumer spending over the forecast horizon.

Conventional products command 80.0% share in 2025, supported by the continued dominance of mass-market colour cosmetics, fragrance, and haircare. However, the organic category (20.0%) is expanding faster than the overall market, propelled by clean-beauty preferences, tightening ingredient regulation, and certified-natural positioning across premium and prestige channels. Women account for 58.0% of category spend, while men (21.7%) and unisex (20.3%) together represent the structural growth frontier, reshaping product development, merchandising, and marketing narratives.

Germany leads with a 21.6% share, followed by France (18.9%), the United Kingdom (17.4%), Italy (13.2%), and Spain (10.1%). The Europe cosmetics market outlook remains constructive as premiumization, dermocosmetic innovation, biotech-derived actives, and omnichannel retail converge across all major national markets through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Category |

Conventional – 80.0% share (2025) |

|

Second Category |

Organic – 20.0% share (2025) |

|

Largest Gender Segment |

Women – 58.0% share (2025) |

|

Second Gender Segment |

Men – 21.7% share (2025) |

|

Third Gender Segment |

Unisex – 20.3% share (2025) |

|

Largest Country |

Germany – 21.6% share (2025) |

|

Forecast CAGR (2026-2034) |

2.47% |

|

Top Companies |

L'Oréal, Unilever, Beiersdorf, LVMH, Estée Lauder, Coty |

Key Analytical Observations Supporting the Above Data:

- Conventional's 80.0% dominance in 2025 reflects the continued scale of mass-market colour cosmetics, haircare, and fragrance across hypermarkets, drugstores, and perfumery chains, particularly in Germany, France, and the UK.

- Organic's 20.0% share represents the fastest-growing category slice, reinforced by COSMOS, Ecocert, and NATRUE certifications, Gen-Z preference for clean formulations, and the premiumization of natural skincare in France, Germany, and the Nordics.

- Women's 58.0% share remains anchored by skincare, fragrance, and colour cosmetics, while male grooming (21.7%) is expanding on the back of dedicated skincare ranges, beard-care innovation, and premium fragrance growth in Italy, France, and the UK.

- Unisex at 20.3% captures the structural rise of gender-neutral fragrance, inclusive skincare, and Gen-Z-led brands, with Paris, Berlin, and London acting as creative hubs for new entrants and indie labels.

- Germany's 21.6% country lead reflects its large, mature consumer base, the strength of Beiersdorf and Henkel Beauty, and the scale of drugstore chains such as dm-drogerie markt and Rossmann distributing both conventional and organic ranges.

Europe Cosmetics Market Overview

The Europe cosmetics market encompasses the full portfolio of personal-care and beauty products sold across skincare, haircare, colour cosmetics, fragrance, oral care, deodorants, and bath-and-shower segments. The regional market includes mass, masstige, premium, and prestige tiers distributed through hypermarkets and supermarkets, drugstores, specialty perfumery chains (Sephora, Douglas, Marionnaud), pharmacies and para-pharmacies (a defining European channel), department stores, and a rapidly expanding e-commerce ecosystem covering marketplaces, direct-to-consumer brand sites, and social commerce.

Demand is shaped by the interplay of demographics (an ageing but affluent consumer base, an expanding Gen-Z cohort, and increasing male participation), lifestyle and wellness trends, and one of the world's most stringent regulatory environments, governed by the EU Cosmetics Products Regulation (EC) No 1223/2009, SCCS scientific opinions, CMR substance bans, and REACH. Supply-side dynamics revolve around continued consolidation among multinational beauty groups, the proliferation of indie and clean-beauty brands, and rising investment in biotech-derived actives, AI-powered personalization, and sustainable packaging to meet both consumer and regulatory expectations.

Market Dynamics

To evaluate market opportunities, Request Sample

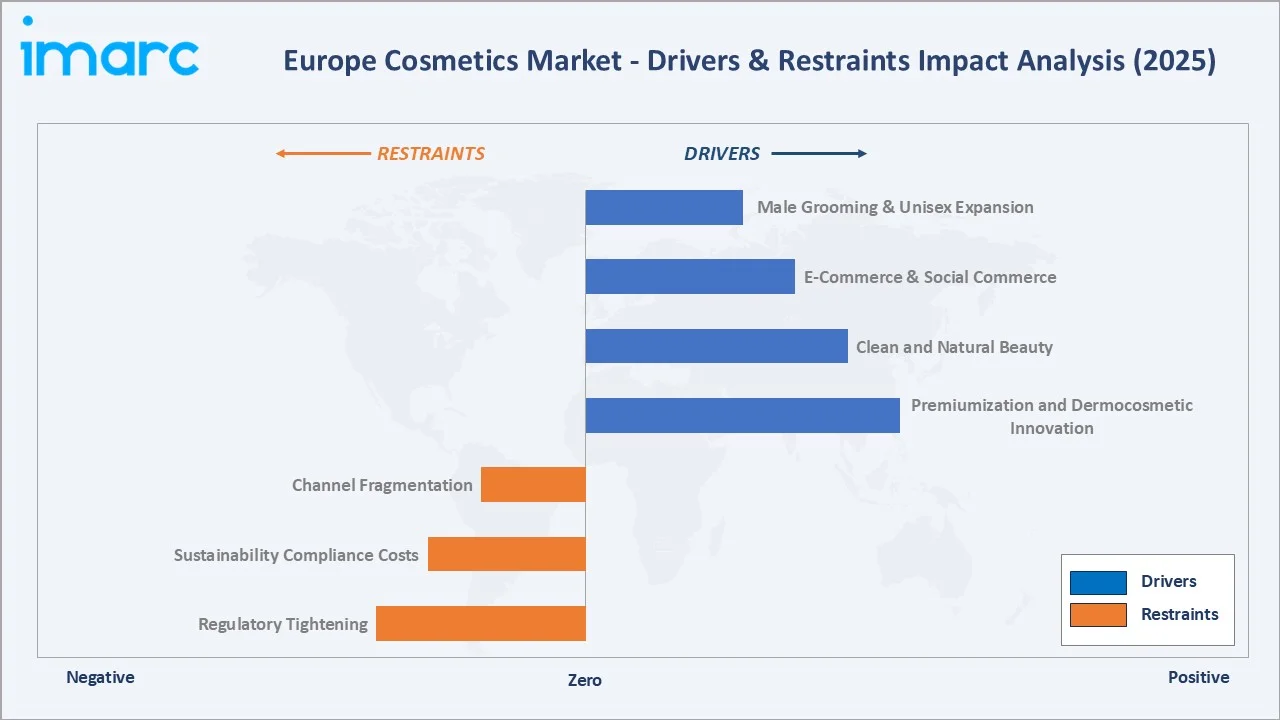

Market Drivers

- Premiumization and Dermocosmetic Innovation: European consumers increasingly trade up toward premium skincare, dermocosmetics, and prestige fragrance. Pharmacy-channel brands such as La Roche-Posay, Avène, Vichy, Bioderma, and Eucerin continue to gain share, reinforced by dermatologist endorsement, efficacy-led marketing, and strong repeat-purchase economics in France, Germany, Italy, and Spain.

- Clean and Natural Beauty: Clean-beauty and organic positioning is moving from niche to mainstream across mass and prestige channels. COSMOS-certified, Ecocert, and NATRUE-labelled products are expanding in both drugstore (dm-drogerie markt, Rossmann) and perfumery (Douglas, Sephora) shelves, driven by Gen-Z and Millennial demand and by tightening EU ingredient scrutiny.

- Male Grooming and Unisex Expansion: Male skincare, beard-care, and fragrance categories are expanding rapidly across Italy, France, the UK, and Germany. Unisex fragrance and gender-neutral skincare are reshaping prestige and indie portfolios, creating incremental category growth beyond the traditional women's segment.

- E-commerce and Social Commerce: Online penetration of European beauty has structurally stepped up post-pandemic. Platforms such as Douglas.de, Sephora.eu, Amazon Beauty, and Lookfantastic, combined with D2C brand sites and TikTok Shop, are capturing a rising share of category sales, particularly in Germany, the UK, and France.

Market Restraints

- Regulatory Tightening: The EU's Cosmetics Products Regulation, SCCS opinions, and ongoing CMR substance reclassifications impose continuous reformulation costs on global and regional beauty groups, particularly in fragrance and preservatives.

- Sustainability Compliance Costs: Packaging and Packaging Waste Regulation (PPWR), Extended Producer Responsibility schemes, and voluntary refill/recycling commitments are adding operational cost, especially for premium brands where glass and complex multi-material packaging dominate.

- Channel Fragmentation: Serving pharmacies, perfumery chains, drugstore, e-commerce marketplaces, and D2C simultaneously requires differentiated assortment, pricing, and marketing strategies, straining operational models of mid-size and regional brands.

- Consumer Price Sensitivity: Persistent inflation pressure in 2023-2025 shifted some demand toward private-label and value-tier ranges, particularly in Germany, the UK, and Spain, compressing mid-tier brand share.

Market Opportunities

- Biotech-Derived and Upcycled Actives: European formulators are scaling fermentation-derived peptides, bio-identical actives, and upcycled ingredients (grape, olive, coffee) to deliver both clean-beauty and sustainability credentials, creating a multi-year R&D frontier for L'Oréal, Beiersdorf, and the indie ecosystem.

- Refill, Reuse, and Circular Packaging: Refill stations in perfumery and pharmacy retail, reusable compacts in colour cosmetics, and recyclable mono-material bottles are expanding rapidly, particularly in France, the Nordics, and the UK, in line with PPWR requirements.

- AI-Powered Personalization: Skincare diagnostic tools, virtual try-ons, and AI-based recommendation engines are enabling both prestige and pharmacy brands to offer personalized regimens at scale, lifting basket size and lowering return rates across e-commerce and D2C channels.

Market Challenges

- Greenwashing Scrutiny: The EU Green Claims Directive and national consumer-protection authorities are actively policing environmental and natural claims, raising compliance burden for brands using ambiguous 'natural' or 'clean' messaging.

- Private-Label and Mass-Retailer Pressure: Drugstore private-label lines (dm Balea, Rossmann Isana) and mass-retailer ranges are capturing meaningful share in skincare and haircare, pressuring mid-tier brand economics.

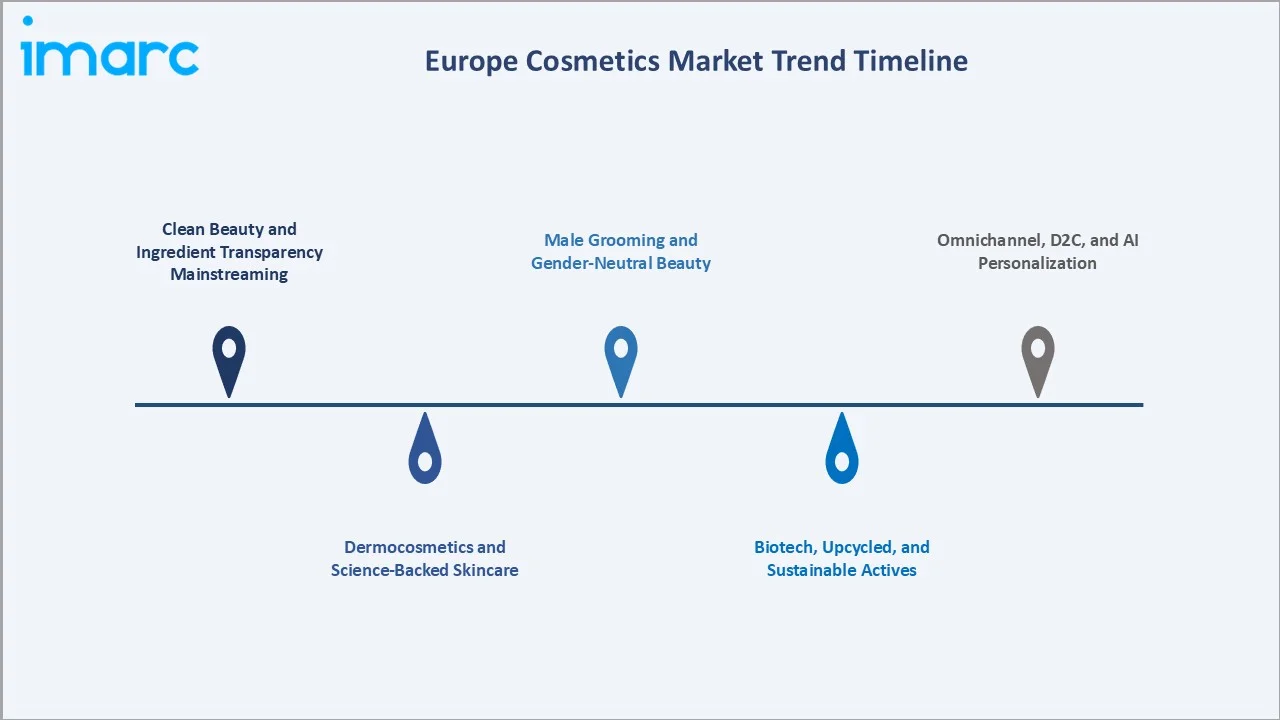

Emerging Market Trends

1. Clean Beauty and Ingredient Transparency Mainstreaming

Clean-beauty is moving from niche positioning to a sector-wide baseline expectation. European consumers increasingly scrutinise INCI lists, and retailers including Douglas, Sephora Europe, and Naturalia are expanding dedicated clean-beauty sections. Brands are progressively eliminating controversial preservatives, replacing them with bio-fermented alternatives, and leveraging third-party certifications such as COSMOS, Ecocert, and NATRUE to substantiate claims.

2. Dermocosmetics and Science-Backed Skincare

Dermocosmetic brands distributed through pharmacy and para-pharmacy channels continue to outgrow the broader skincare market. La Roche-Posay, Avène, Vichy, Bioderma, Eucerin, and Uriage are gaining prestige-adjacent pricing power in France, Germany, Italy, and Spain, supported by dermatologist endorsement and strong efficacy storytelling.

3. Male Grooming and Gender-Neutral Beauty

The male-grooming category is expanding well beyond shaving into skincare, haircare, and fragrance. At the same time, gender-neutral fragrance and unisex skincare are structurally reshaping prestige and indie assortments, led by creative hubs in Paris, Berlin, London, and Milan.

4. Biotech, Upcycled, and Sustainable Actives

Fermentation-derived peptides, bio-identical hyaluronic acid, lab-grown squalane, and upcycled botanicals are scaling into premium skincare. European formulators are leveraging these platforms to reduce water use, deforestation footprint, and price volatility tied to traditional botanical extracts.

5. Omnichannel, D2C, and AI Personalization

Europe's beauty consumer is now fundamentally omnichannel. Douglas, Sephora, Marionnaud, and pharmacy chains are integrating online and offline inventory, loyalty, and personalization, while indie and prestige brands invest in D2C platforms with AI-powered skin diagnostics, virtual try-on, and subscription models to deepen consumer relationships.

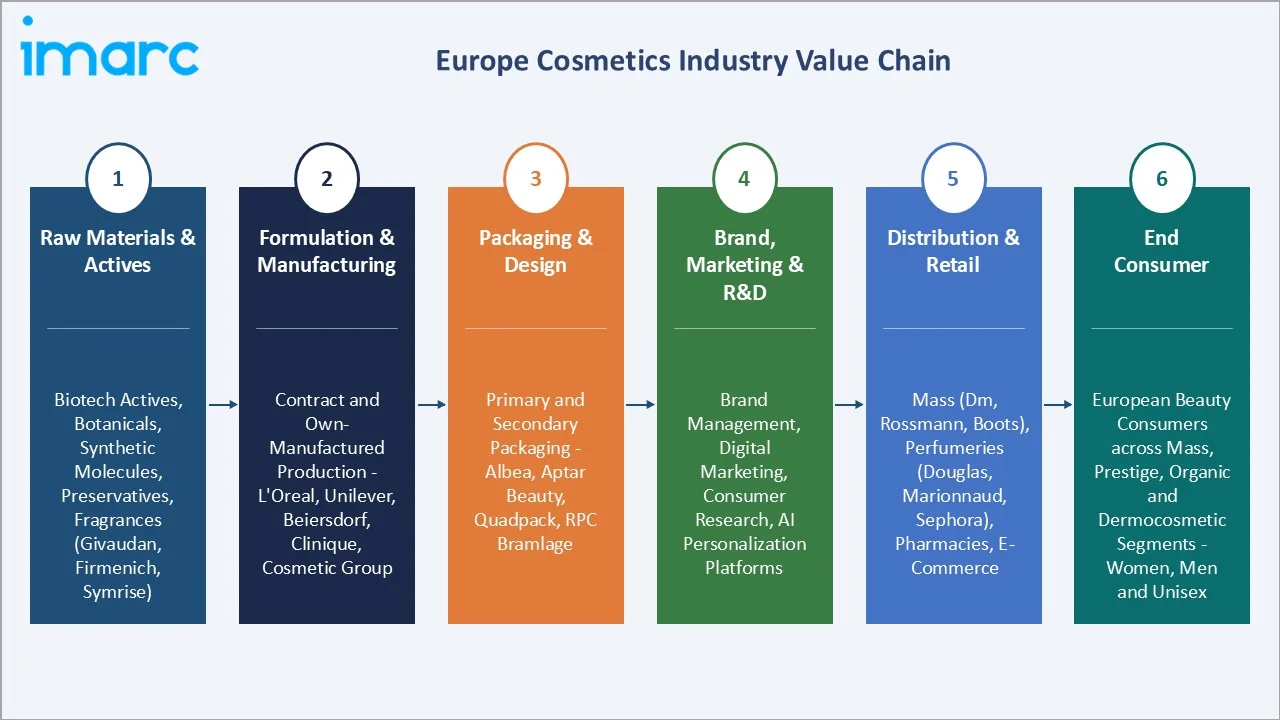

Industry Value Chain Analysis

The Europe cosmetics industry value chain spans five integrated stages from ingredient sourcing through the omnichannel consumer experience. Each stage carries distinct competitive dynamics, margin profiles, and sustainability-investment requirements relevant to the overall Europe cosmetics market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Ingredients & Actives |

Naturals, biotech-derived actives, fragrances, surfactants |

|

Formulation & R&D |

In-house brand labs and contract formulators developing dermocosmetic, clean-beauty, and biotech-driven products |

|

Manufacturing & Filling |

Global owned plants (L'Oréal, Beiersdorf) and contract manufacturers across Italy, Poland, France, Germany |

|

Brand Marketing & Retail |

Omnichannel distribution through perfumery chains, pharmacy, drugstore, department stores, marketplaces, and D2C |

|

Consumer Experience |

AI diagnostics, loyalty programmes, virtual try-ons, refill and subscription models driving repeat purchase |

Brand owners hold the highest strategic value by integrating R&D, brand equity, and omnichannel distribution into high-margin consumer experiences. Contract manufacturers and fragrance-and-flavour houses capture technology-led margins, while perfumery and pharmacy retail chains remain powerful gatekeepers to the European consumer.

Technology Landscape in the Europe Cosmetics Industry

Biotech-Derived Actives and Green Chemistry

Fermentation-derived peptides, bio-identical hyaluronic acid, lab-grown squalane, and precision-fermentation fragrance molecules are transitioning from niche to mainstream premium skincare. European formulators are leveraging biotech platforms to deliver efficacy, sustainability, and traceability, reducing dependence on volatile botanical supply chains.

Sustainable Packaging Innovation

Mono-material PET, post-consumer recycled resin, bio-based polymers, refillable glass, and compostable secondary packaging are being rolled out across mass and prestige tiers. PPWR compliance, Extended Producer Responsibility, and voluntary targets are collectively driving rapid packaging redesign through 2030.

AI, AR, and Digital Diagnostics

AI-powered skin diagnostics, augmented-reality virtual try-ons, and recommendation engines are now deployed by major beauty groups and retailers. L'Oréal's ModiFace, Sephora's Virtual Artist, and pharmacy-chain diagnostic tools enable personalization at scale, boosting conversion in both online and in-store channels.

Clean and Microbiome-Safe Formulation

Preservative reformulation, microbiome-friendly actives, and minimalist formulation philosophies ('skinimalism') are reshaping product design. Brands are replacing controversial preservatives and fragrance allergens with safer alternatives, in line with evolving SCCS opinions and consumer expectations.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Product Type | Skin and Sun Care Products | 33.0% |

2025 |

| Category | Conventional | 80.0% |

2025 |

| Gender | Women | 58.0% |

2025 |

| Distribution Channel | Supermarkets and Hypermarkets | 32.0% |

2025 |

| Country | Germany | 21.6% | 2025 |

IMARC Group provides an analysis of the key trends in each segment of the Europe cosmetics market, along with forecasts at the regional and country levels from 2026 to 2034. The market has been categorized based on category and gender.

Market Breakup by Category

Conventional cosmetics lead the Europe market with an 80.0% share in 2025, anchored by mass-market colour cosmetics, fragrance, haircare, and personal-care ranges distributed through hypermarkets, drugstore chains, and perfumery specialists. The category benefits from scale, price-point breadth, and deep loyalty to heritage brands such as Nivea, L'Oréal Paris, Garnier, Maybelline, and Dove across Germany, France, the UK, and Italy.

To access detailed market analysis, Request Sample

Organic cosmetics represent 20.0% of the market in 2025 and constitute the fastest-expanding slice. Growth is driven by clean-beauty preferences, COSMOS, Ecocert, and NATRUE certification uptake, and the premiumization of natural skincare. France's pharmacy and para-pharmacy ecosystem, Germany's drugstore chains (dm-drogerie markt Alverde, Rossmann Alterra), and the Nordics' sustainability-led consumer base are the principal demand pools.

|

Category |

Share (2025) |

Key Demand Drivers |

|

Conventional |

80.0% |

Mass colour cosmetics, haircare, fragrance, deodorants; legacy multinational dominance |

|

Organic |

20.0% |

COSMOS/Ecocert/NATRUE certified; clean-beauty positioning; premium natural skincare |

Market Breakup by Gender

Women represent 58.0% of Europe cosmetics spend in 2025, anchored by skincare, fragrance, and colour cosmetics. Demand is increasingly segmented across premium dermocosmetics, clean skincare, prestige fragrance, and indie colour ranges, with Gen-Z and Millennial cohorts reshaping brand loyalty toward purpose-led and ingredient-led propositions.

Men account for 21.7% and represent one of the most structurally dynamic segments. Growth is driven by dedicated male skincare ranges (Nivea Men, L'Oréal Men Expert, Bulldog), beard-care innovation, and premium male fragrance expansion, particularly in Italy, France, and the UK, where grooming culture remains deeply embedded.

Unisex products capture 20.3%, reflecting the rise of gender-neutral fragrance, inclusive skincare, and Gen-Z-aligned indie brands. Paris, Berlin, Milan, and London act as creative hubs, with prestige houses (Jo Malone, Le Labo, Byredo, Maison Margiela) and indie entrants jointly scaling the gender-neutral proposition.

|

Gender Segment |

Share (2025) |

Key Demand Drivers |

|

Women |

58.0% |

Skincare, fragrance, colour cosmetics; premiumization and dermocosmetics |

|

Men |

21.7% |

Male skincare, beard-care, premium fragrance; Italy, France, UK lead |

|

Unisex |

20.3% |

Gender-neutral fragrance, inclusive skincare, Gen-Z indie brands |

Regional (Country-Level) Market Insights

Germany commands 21.6% of Europe cosmetics revenue in 2025, reflecting the combined effect of a large, mature consumer base, the scale of Beiersdorf and Henkel Beauty, and the dominance of drugstore chains dm-drogerie markt and Rossmann. Germany is also Europe's largest organic-beauty market in absolute terms, supported by strong certified-natural private-label lines (Alverde, Alterra) and the country's pronounced sustainability orientation.

France captures 18.9% of regional revenue, anchored by its global beauty-heritage position, prestige-fragrance strength, and the dominance of pharmacy-channel dermocosmetics. L'Oréal's home market remains the single most influential creative and R&D hub, while Paris continues to act as the prestige capital of global beauty. Pharmacy and para-pharmacy channels (La Roche-Posay, Vichy, Avène, Bioderma) drive premium skincare penetration.

The United Kingdom contributes 17.4%, supported by the scale of Boots, Superdrug, and Space NK in specialty retail, rapid e-commerce penetration via Lookfantastic and Cult Beauty, and a dynamic indie ecosystem. London's creative scene incubates gender-neutral, clean-beauty, and Gen-Z-led brands that frequently scale across Europe.

Italy represents 13.2%, underpinned by prestige fragrance heritage (Ferragamo, Dolce & Gabbana, Giorgio Armani Beauty), strong male-grooming culture, and a dense perfumery-chain footprint (Douglas, Marionnaud). Spain accounts for 10.1%, led by Puig's portfolio (Paco Rabanne, Carolina Herrera, Jean Paul Gaultier), pharmacy-channel dermocosmetic strength, and a rapidly digitizing consumer base. The remaining 18.8% captured under Others is distributed across the Nordics, Benelux, Poland, Switzerland, Austria, and Central and Eastern Europe, where premium skincare, sustainable positioning, and digital-first indie brands continue to deepen category penetration.

|

Country |

Share (2025) |

Key Growth Drivers |

|

Germany |

21.6% |

Beiersdorf/Henkel base, dm-drogerie markt & Rossmann dominance, organic-beauty leadership |

|

France |

18.9% |

L'Oréal home market, prestige fragrance heritage, pharmacy dermocosmetics |

|

United Kingdom |

17.4% |

Boots, Superdrug, Space NK; e-commerce penetration; indie brand ecosystem |

|

Italy |

13.2% |

Prestige fragrance heritage, strong male grooming, dense perfumery retail |

|

Spain |

10.1% |

Puig portfolio, pharmacy dermocosmetics, digital consumer expansion |

|

Others |

18.8% |

Nordics, Benelux, Poland, Switzerland, CEE; organic and digital-first growth |

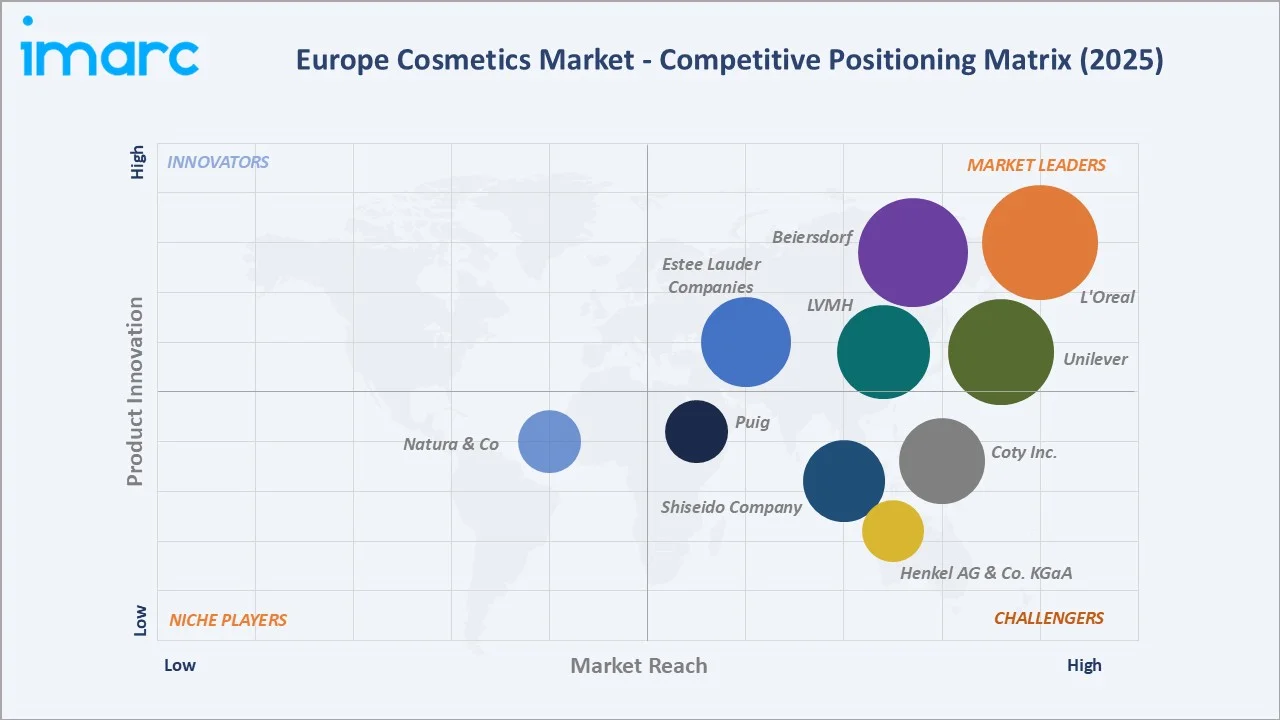

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

L'Oréal |

CeraVe, Vichy, Skin Better |

Leader |

Global #1 beauty, dermocosmetic leadership, R&D scale |

|

Unilever |

Dove, Vaseline, Ponds, Clear |

Leader |

Mass personal-care dominance, sustainability leadership |

|

Beiersdorf |

Nivea, Eucerin, La Prairie, Chantecaille |

Leader |

Skincare-anchored, German base, premium expansion |

|

LVMH |

Ole Henriksen, Make up Forever |

Leader |

Prestige luxury beauty, global retail through Sephora |

|

Estée Lauder Companies |

Clinique, Aveda, Bumble and Bumble |

Leader |

Prestige beauty scale, travel-retail strength |

|

Coty Inc. |

Paixao, Philosophy, Risque |

Challenger |

Fragrance-led, prestige licensing strategy |

|

Shiseido Company |

Anessa, Nars, IPSA |

Challenger |

Skincare expertise, Japanese premium heritage |

|

Henkel AG & Co. KGaA |

Bonacure, Authentic Beauty Concept |

Challenger |

Haircare leadership, German base |

|

Puig |

Apivita, Kama Ayurveda |

Challenger |

Premium fragrance, Spanish family-led independence |

|

Natura & Co |

Natura, Avon |

Emerging |

Direct-sales heritage, sustainability positioning |

The Europe cosmetics market's competitive landscape is moderately concentrated at the top, with L'Oréal, Unilever, Beiersdorf, LVMH, and Estée Lauder collectively controlling a significant share of regional revenue. A vibrant mid-tier of European champions (Coty, Henkel Beauty, Puig, Natura & Co) competes alongside a rapidly expanding layer of indie, clean-beauty, and dermocosmetic brands. Strategic acquisitions and brand incubation are actively reshaping the competitive map through 2034.

Key Company Profiles

L'Oréal

L'Oréal is the world's largest beauty company, headquartered in Clichy, France. Founded in 1909, it operates across mass, prestige, professional, and active-cosmetic divisions, with Europe representing its largest and most strategically significant region.

- Product & Platform Portfolio: L'Oréal's European portfolio spans mass brands (L'Oréal Paris, Garnier, Maybelline), prestige (Lancôme, Yves Saint Laurent, Giorgio Armani Beauty, Kiehl's), active cosmetics (La Roche-Posay, Vichy, CeraVe), and professional products (L'Oréal Professionnel, Kérastase, Redken).

- Recent Developments: In 2025, L'Oréal strengthened its BeautyTech leadership by showcasing a broad portfolio of innovations at Viva Technology, built on collaborations with biotech, tech, and startup partners, while advancing AI-powered, data-driven beauty services and personalised diagnostics through its digital ecosystem.

- Strategic Focus: L'Oréal's strategy emphasises the scaling of active-cosmetic brands, continued premiumization, biotech and sustainable sourcing, and the deep integration of AI personalization and omnichannel beauty experiences across Europe.

Unilever

Unilever is a London and Rotterdam-headquartered consumer-goods group with a global beauty-and-wellbeing division. In Europe, Unilever holds leading positions across mass personal care, haircare, and deodorants, alongside a growing prestige-beauty portfolio.

- Product & Platform Portfolio: Unilever's European beauty portfolio includes Dove, Vaseline, Axe/Lynx, Rexona, Sure, TRESemmé, and Suave, complemented by prestige acquisitions such as Hourglass, Dermalogica, REN Clean Skincare, and Paula's Choice.

- Recent Developments: In 2025, Unilever expanded its circular packaging efforts by scaling refill and reuse initiatives across key brands such as Dove, increasing post-consumer recycled plastic to 25% of its portfolio, and advancing the shift toward reusable and recyclable packaging formats.

- Strategic Focus: Unilever's strategy focuses on premium-and-prestige beauty expansion, sustainability-led product redesign, and digital-first brand building through D2C platforms and social-commerce channels across Europe.

Beiersdorf

Beiersdorf is a Hamburg-headquartered skincare specialist with a global footprint. Europe is Beiersdorf's largest region, anchored by the Nivea mass-skincare franchise and a fast-growing premium and dermocosmetic portfolio.

- Product & Platform Portfolio: Beiersdorf's European portfolio spans Nivea, Eucerin, Aquaphor, La Prairie, Chantecaille, and 8x4, alongside adhesive-technologies brand Tesa (separate segment).

- Recent Developments: In 2025, Beiersdorf accelerated its derma-led growth strategy, with Eucerin and Aquaphor gaining market share and delivering double-digit growth, supported by breakthrough ingredient innovations such as Epicelline® and Thiamidol®. At the same time, the company continued to expand La Prairie’s global luxury footprint despite short-term volatility.

- Strategic Focus: Beiersdorf's strategy centres on skincare specialization, the premiumization of Eucerin and La Prairie, continued biotech and sustainability investment, and deeper omnichannel activation across European markets.

Market Concentration Analysis

The Europe cosmetics market exhibits moderate-to-high concentration at the top of the market. The top five groups – Leading global players such as L’Oréal, Unilever, Estée Lauder, Beiersdorf, and LVMH collectively generate over $45B+ in beauty revenues, dominating the global rankings—though the broader market remains fragmented with multiple regional and niche competitors. The remaining share is distributed across a vibrant mid-tier of European champions (Coty, Henkel Beauty, Puig, Natura & Co, Shiseido Europe) and a rapidly expanding indie, clean-beauty, and dermocosmetic layer.

The market is experiencing a dual dynamic. At the top, multinational beauty groups consolidate around prestige, dermocosmetic, and biotech-active positioning through acquisitions and in-house brand incubation. Simultaneously, indie and digital-native brands are capturing meaningful share in clean beauty, gender-neutral ranges, and Gen-Z-targeted propositions, creating a continuously refreshed competitive frontier through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Organic and clean-beauty is the fastest-expanding category slice, growing at an estimated 3.5 CAGR through 2030 – well above the headline market rate. Male-grooming and unisex segments are the next most dynamic layers, supported by dermocosmetic skincare uptake, beard-care innovation, and gender-neutral fragrance expansion across France, Italy, and the UK.

Emerging Country Expansion

Poland, the Nordics, and the Netherlands represent the highest-potential growth markets in Europe, supported by rising per-capita beauty spend, strong organic-beauty uptake, and digitally native younger consumers. Southern European markets (Portugal, Greece) and the Balkans remain structurally lower-penetration pockets with meaningful premiumization headroom.

Venture and Strategic Investment Trends

Strategic capital continues to flow into biotech-derived actives, sustainable packaging, AI-powered personalization, and the indie clean-beauty ecosystem. L'Oréal's BOLD corporate venture arm, Unilever Ventures, LVMH Luxury Ventures, and specialist private-equity platforms remain the most active investors, with meaningful acquisition activity expected through 2034.

Future Market Outlook (2026-2034)

The Europe cosmetics market forecast projects steady value expansion from USD 111.32 Billion in 2025 to USD 138.66 Billion by 2034 at a CAGR of 2.47%. Germany, France, and the UK will retain their combined majority of regional revenue, while the Nordics, Poland, and Southern European markets will continue to expand the organic, clean-beauty, and digital-first proposition footprint.

Three key shifts will reshape the Europe cosmetics market through 2034. First, clean beauty, biotech-derived actives, and circular packaging will become the default regulatory and commercial baseline rather than a premium add-on, reshaping product roadmaps across mass and prestige tiers. Second, male-grooming and unisex categories will continue to outpace the headline market, rebalancing R&D, marketing, and retail allocation. Third, AI-powered personalization and omnichannel integration will become the principal competitive frontier, determining brand loyalty and lifetime value across both indie entrants and multinational incumbents.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with cosmetics-industry stakeholders, including brand directors at multinational beauty groups, category managers at European perfumery and pharmacy chains, procurement leads at ingredient and packaging suppliers, and institutional investors in European beauty and consumer-goods funds. Primary insights validated market sizing, segmentation estimates, and technology-adoption timelines.

Secondary Research

Secondary sources include Eurostat consumer-expenditure data, Cosmetics Europe publications, European Commission DG GROW cosmetics-sector reports, national statistics offices (Destatis, INSEE, ONS, ISTAT, INE), CosmeticsDesign-Europe and Premium Beauty News trade coverage, company annual reports, and retailer disclosures from Douglas, Boots, and dm-drogerie markt.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth, disposable-income trends, retail-channel evolution, and historical category performance. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic, regulatory, and consumer-behaviour uncertainty.

Europe Cosmetics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Skin and Sun Care Products, Hair Care Products, Deodorants and Fragrances, Makeup and Color Cosmetics, Others |

| Categories Covered | Conventional, Organic |

| Genders Covered | Men, Women, Unisex |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, Pharmacies, Online Stores, Others |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | L'Oréal, Unilever, Beiersdorf, LVMH, Estée Lauder Companies, Coty Inc., Shiseido Company, Henkel AG & Co. KGaA, Puig, Natura & Co, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe Cosmetics Market Report

The Europe cosmetics market was valued at USD 111.32 Billion in 2025, driven by premiumization, dermocosmetic innovation, e-commerce expansion, and rising male-grooming and unisex demand across major European economies.

The market is projected to reach USD 138.66 Billion by 2034, growing at a CAGR of 2.47% during 2026-2034, supported by clean beauty, biotech-derived actives, sustainable packaging, and AI-powered personalization.

Conventional cosmetics lead with an 80.0% share in 2025, anchored by mass-market colour cosmetics, fragrance, and haircare distributed through drugstore, perfumery, and hypermarket channels.

Organic cosmetics represent 20.0% of the Europe cosmetics market in 2025 and are the fastest-growing category slice, propelled by clean-beauty preferences, ingredient transparency, and COSMOS/Ecocert/NATRUE certification uptake.

Women account for 58.0% of the Europe cosmetics market in 2025, led by skincare, fragrance, and colour cosmetics. Men (21.7%) and unisex (20.3%) together represent the structural growth frontier of the market.

Germany dominates with a 21.6% share in 2025, followed by France (18.9%), the United Kingdom (17.4%), Italy (13.2%), and Spain (10.1%). Germany's leadership reflects its large consumer base and the strength of drugstore and Beiersdorf-led distribution.

Key drivers include premiumization, dermocosmetic innovation, clean-beauty adoption, male-grooming expansion, e-commerce and social-commerce growth, biotech-derived actives, and AI-powered personalization across omnichannel retail.

Major players include L'Oréal S.A., Unilever plc, Beiersdorf AG, LVMH, Estée Lauder Companies, Coty Inc., Henkel Beauty Care, Shiseido Company, Puig, and Natura & Co.

Key opportunities include biotech-derived and upcycled active ingredients, sustainable and refillable packaging, AI-powered personalization platforms, male-grooming and unisex brand building, dermocosmetic skincare expansion, and indie clean-beauty incubation.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)