Europe Data Center Market Size, Share, Trends and Forecast by Component, Type, Enterprise Size, End User, and Country, 2026-2034

Europe Data Center Market Size, Share, Trends & Forecast (2026-2034)

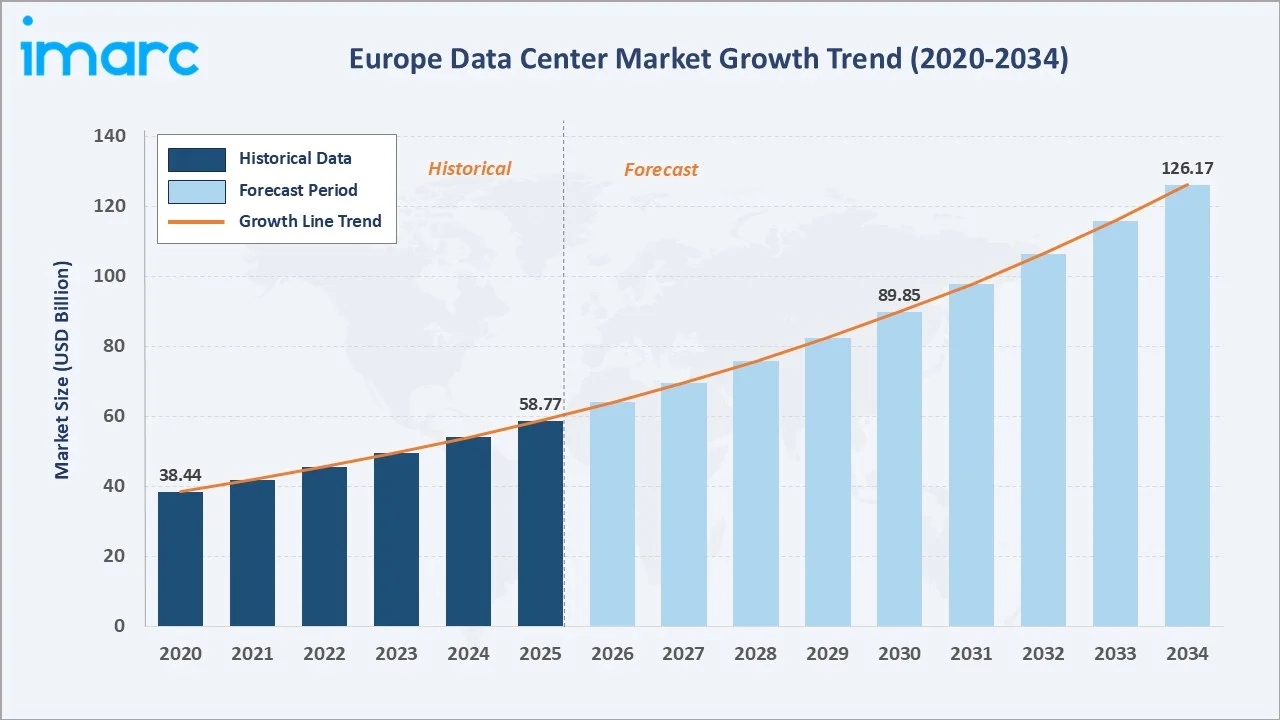

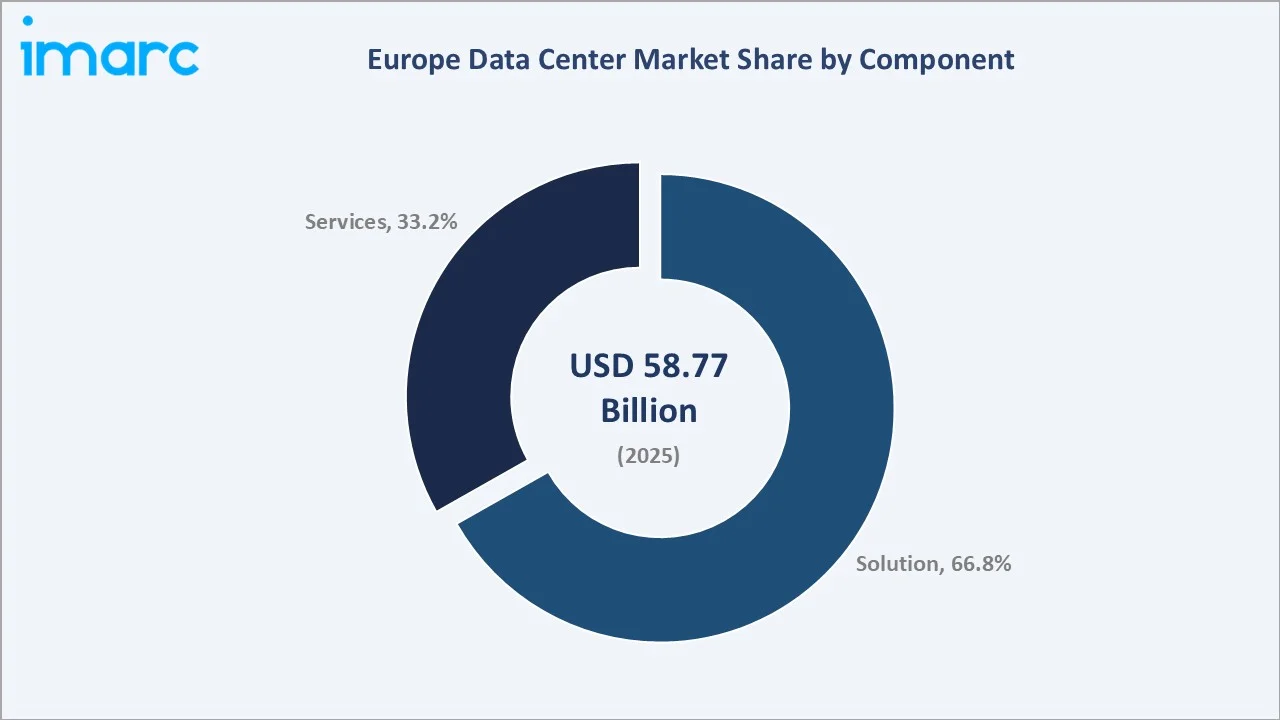

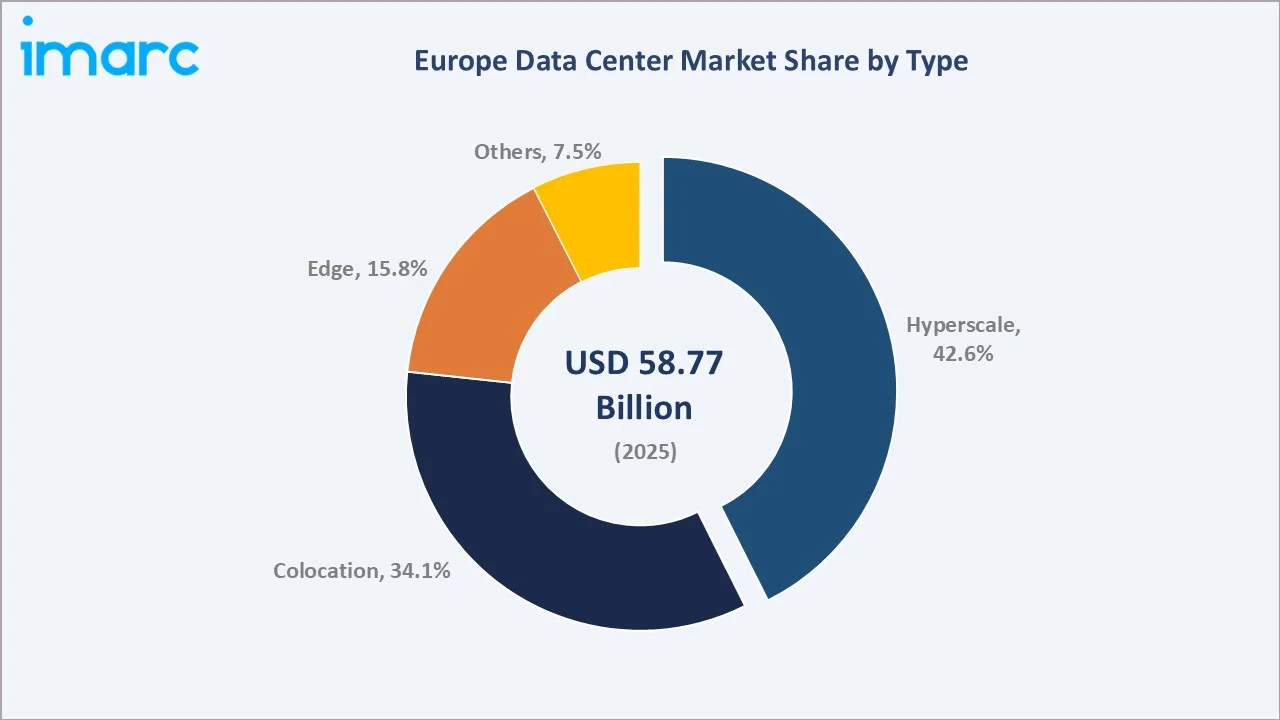

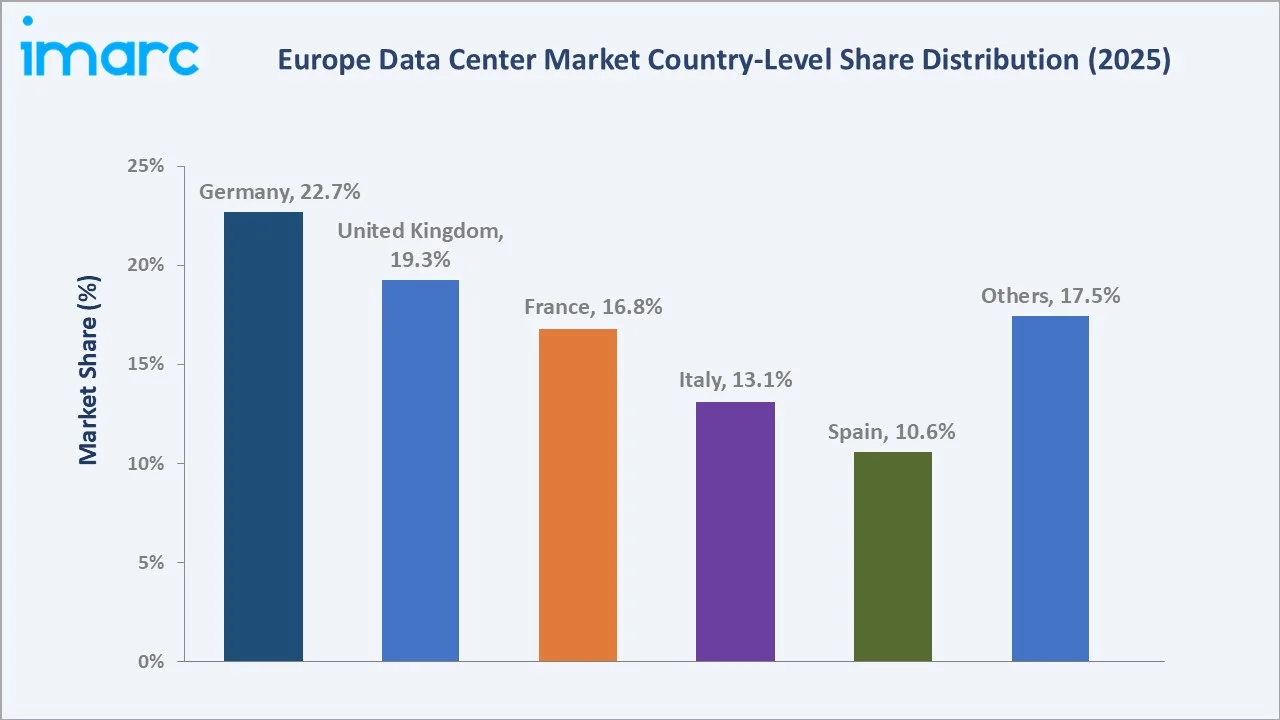

The Europe data center market size was valued at USD 58.77 Billion in 2025 and is projected to reach USD 126.17 Billion by 2034, exhibiting a CAGR of 8.86% during the forecast period 2026-2034. Solution leads the component segment at 66.8% in 2025, while Hyperscale dominates the type segment at 42.6%. Germany accounts for 22.7% of regional revenue in 2025, the largest country market in Europe.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 58.77 Billion |

|

Forecast Market Size (2034) |

USD 126.17 Billion |

|

CAGR (2026-2034) |

8.86% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

Germany (22.7% share, 2025) |

|

Fastest Growing Country |

United Kingdom (~10.2% CAGR) |

|

Leading Component |

Solution (66.8%, 2025) |

|

Leading Type |

Hyperscale (42.6%, 2025) |

The Europe data center market growth trajectory from 2020 through 2034 contrasts steady historical expansion with an accelerating forecast curve powered by AI workload build-outs, sovereign-cloud migration, and hyperscale infrastructure commitments across the region.

To get more information on this market, Request Sample

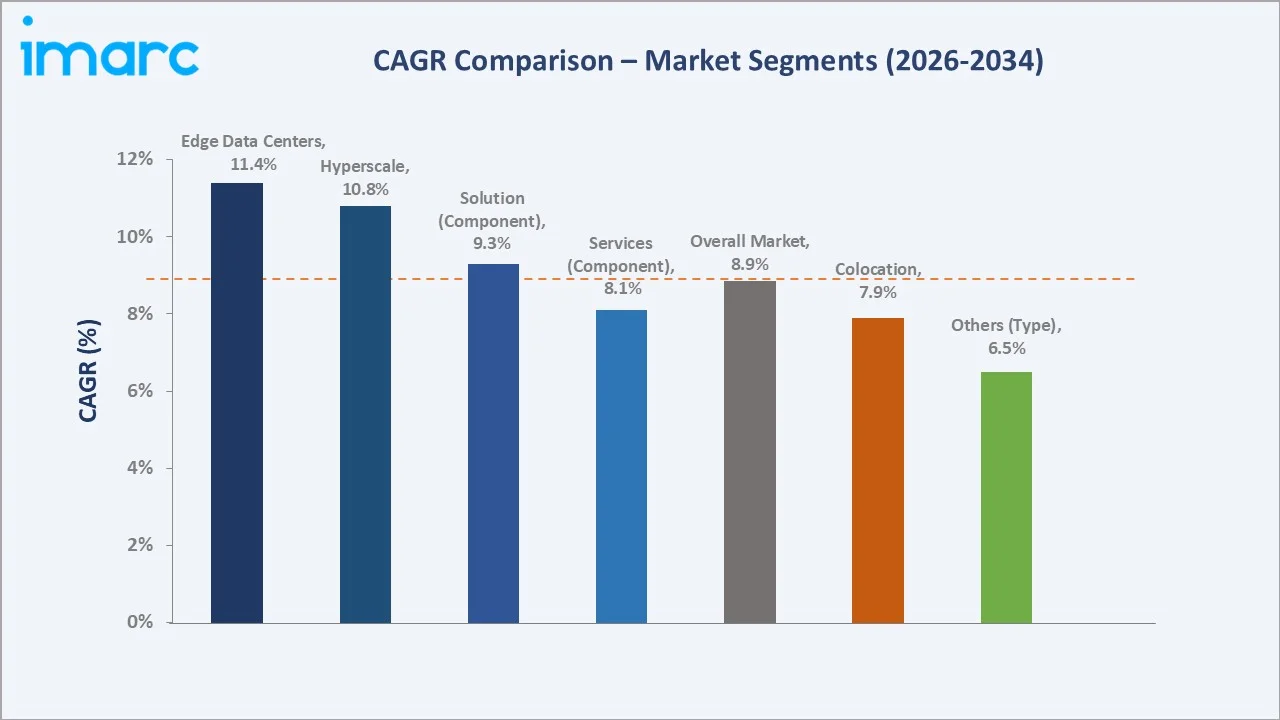

Segment-level CAGR comparison highlights Edge and Hyperscale as the fastest-growing type sub-categories within the Europe data center industry analysis through 2034, driven by AI inference at the edge and large-scale AI training hubs, respectively.

Executive Summary

The Europe data center market is undergoing a rapid structural transformation, driven by the convergence of AI compute demand, digital sovereignty regulation, and renewable-energy siting economics. Valued at USD 58.77 Billion in 2025, the market is forecast to reach USD 126.17 Billion by 2034 at a CAGR of 8.86%. In December 2025, HPE and NVIDIA inaugurated their first AI Factory Lab in Grenoble, France, enabling secure, AI-ready data center validation locally.

Solution leads the component segment with a 66.8% share in 2025, backed by capital spending on servers, storage, power infrastructure, and advanced cooling. Services at 33.2% is the fastest-growing sub-segment as operators outsource design-build, managed hosting, and migration workloads. Hyperscale facilities capture 42.6% of the type segment in 2025, reflecting mega-campus builds by AWS, Microsoft, Google, and Meta across Germany, Ireland, Spain, and the Nordics.

Germany dominates with a 22.7% country share in 2025, anchored by Frankfurt's DE-CIX interconnection hub. The UK holds 19.3%, France 16.8%, Italy 13.1%, and Spain 10.6%, with Spain and Italy emerging as the fastest-rising markets due to favorable land and renewable-energy pricing.

Key Market Insights

|

Insight |

Data |

|

Largest Component |

Solution – 66.8% share (2025) |

|

Leading Type |

Hyperscale – 42.6% share (2025) |

|

Leading Country |

Germany – 22.7% revenue share (2025) |

|

Second Country |

United Kingdom – 19.3% revenue share (2025) |

|

Top Companies |

Equinix, Inc., Digital Realty Trust, NTT DATA Inc., Microsoft, Google (Alphabet Inc.) |

Key Analytical Observations Supporting the Above Data:

- Solution's 66.8% dominance in 2025 reflects sustained capital spend on servers, storage, networking gear, UPS systems, and liquid-cooling infrastructure tied to AI workload build-outs.

- Hyperscale leads type at 42.6% in 2025, powered by AWS, Microsoft, Google, and Meta, announcing more than EUR 50 billion in European commitments in 2024 alone.

- Germany's 22.7% country share in 2025 reflects Frankfurt's role as the DE-CIX interconnection hub and one of the largest internet exchange points globally.

- Edge data center is the fastest-growing type sub-segment at ~11.4% CAGR, driven by 5G rollout, IoT, and real-time AI inference across manufacturing and smart-city applications.

- Services, at 33.2% in 2025, are the fastest-growing component sub-segment, fueled by migration programs and managed cloud operations.

- Spain and Italy are the most under-penetrated hyperscale markets in Western Europe, positioning them for double-digit growth through 2030.

Global Europe Data Center Market Overview

Data centers are physical facilities designed to house computing infrastructure, including servers, storage systems, networking equipment, power distribution, and advanced cooling, enabling enterprises and hyperscale operators to deliver cloud services, AI workloads, and mission-critical applications at scale. Modern European facilities increasingly integrate liquid cooling, renewable-power PPAs, and modular construction methods to meet sustainability mandates.

Applications span BFSI, IT and telecom, government, energy and utilities, healthcare, retail, and media, with IT and telecom being the largest end-use vertical in Europe in 2025. Macroeconomic enablers include EU internet penetration reaching 94% in 2024, sovereign-cloud policy adoption under GAIA-X, and the EU climate-neutral infrastructure target for 2030.

Market Dynamics

To evaluate market opportunities, Request Sample

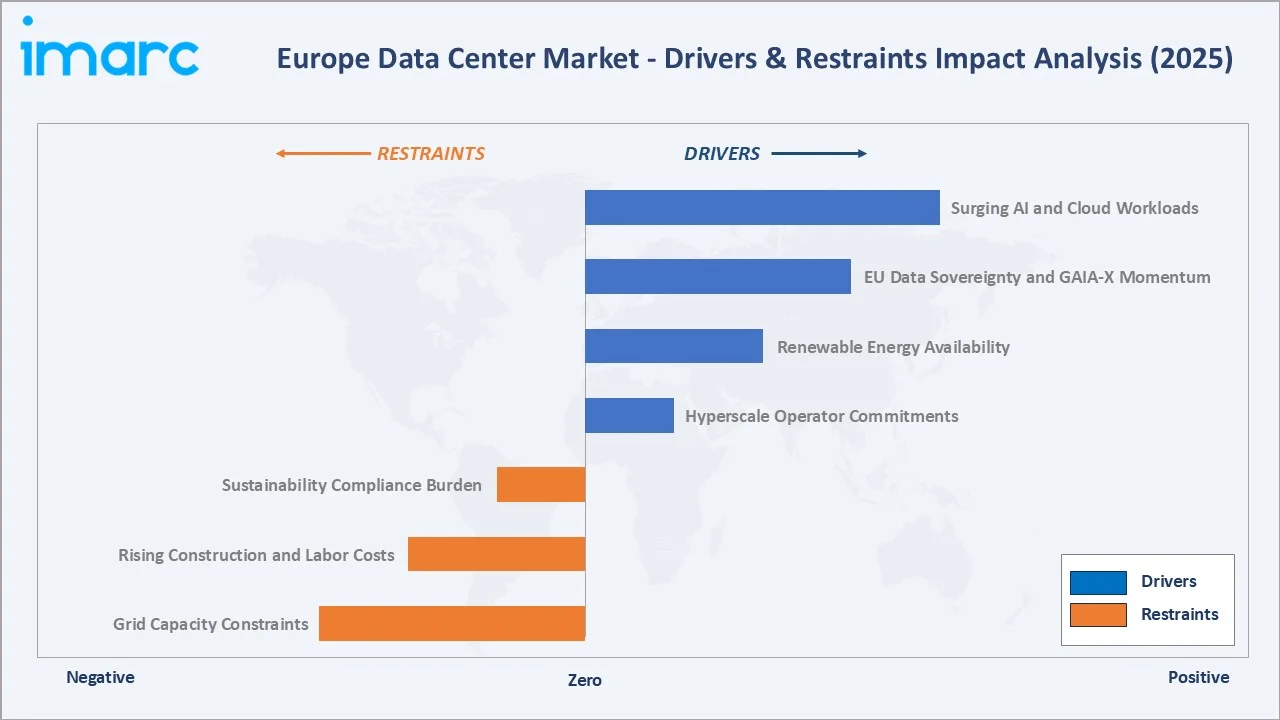

Market Drivers

- Surging AI and Cloud Workloads: Hyperscale investment in AI-ready infrastructure surpassed USD 300 billion in 2025, with Europe gaining incremental share. AI training clusters require 5–10× higher power density than conventional workloads, accelerating new capacity deployment across Germany, France, and the Nordic regions.

- EU Data Sovereignty and GAIA-X Momentum: Frameworks such as the EU Data Act, NIS2 Directive, and GAIA-X are enforcing localized data processing. This is driving multinational enterprises to shift workloads from US-based regions to in-country European data centers.

- Renewable Energy Availability: Nordic markets (Sweden, Norway, Finland) offer 4,000+ annual free cooling hours and strong hydropower availability, while Spain and Portugal are leveraging large-scale solar capacity to attract hyperscale investments.

- Hyperscale Operator Commitments: Over EUR 50 billion in hyperscale investments were announced in 2024, reflecting sustained long-term demand and capacity expansion across key European markets.

Market Restraints

- Grid Capacity Constraints: Key hubs such as Frankfurt, Dublin, and Amsterdam face prolonged grid connection delays, with some projects extending to 2028, pushing demand toward secondary markets.

- Rising Construction and Labor Costs: Labor shortages and cost inflation are extending build timelines beyond 24 months for large-scale facilities, impacting project feasibility and returns.

- Sustainability Compliance Burden: EU regulations on energy efficiency, including PUE disclosure and waste heat utilization, are increasing compliance costs, particularly for legacy colocation assets.

Market Opportunities

- Secondary City Expansion: Milan, Warsaw, Madrid, Berlin, and Zurich are emerging as preferred locations as operators sidestep grid and land constraints in FLAP-D (Frankfurt-London-Amsterdam-Paris-Dublin).

- Liquid Cooling and High-Density Build-outs: In September 2025, Schneider Electric announced new reference designs supporting rack deployments of up to 142 kW per rack, signaling a structural shift in European cooling architecture.

- Waste Heat Reuse Partnerships: District heating partnerships with city utilities offer new revenue streams, with several German and Nordic operators already monetizing server heat for residential networks.

Market Challenges

- Permitting Delays and Community Opposition: Local planning approvals in the Netherlands, Ireland, and parts of Germany now routinely extend 18-30 months amid concerns over power draw and land use.

- Supply Chain Concentration: Advanced GPU and optical module supply remains concentrated in a handful of suppliers, creating volatility in project delivery schedules across European hyperscale programs.

Emerging Market Trends

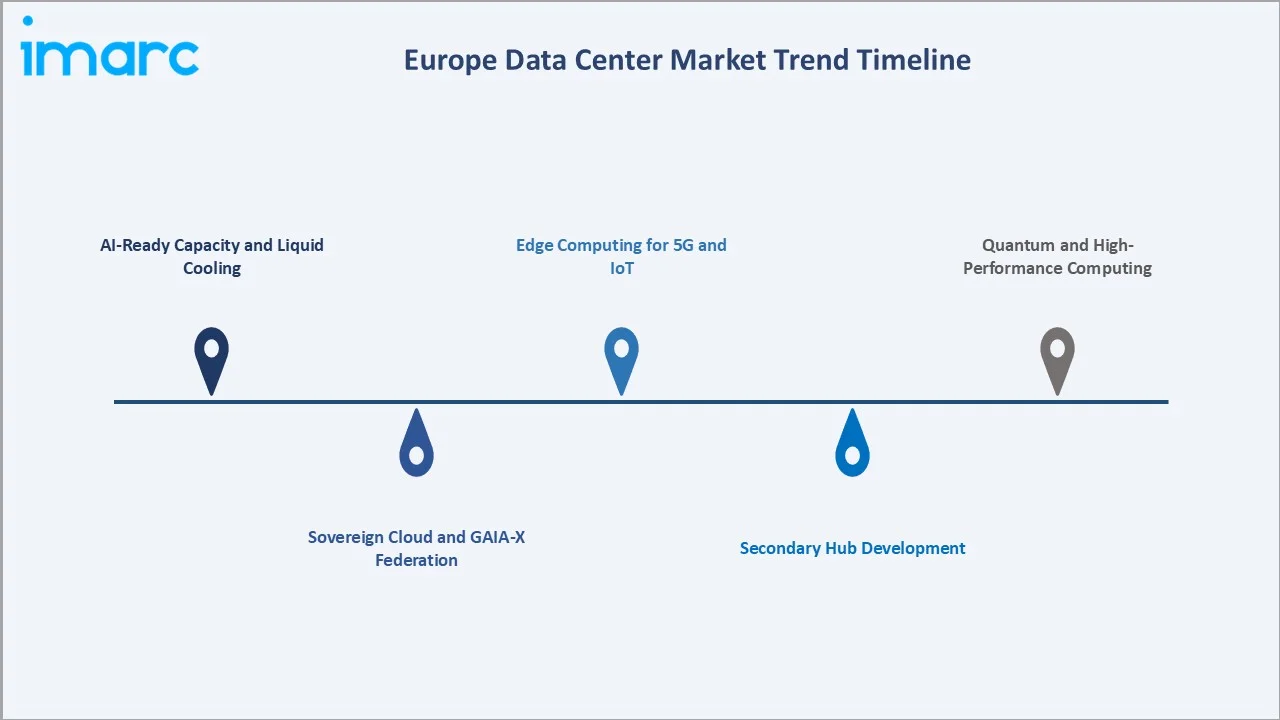

1. AI-Ready Capacity and Liquid Cooling

AI training clusters demand rack densities above 60 kW, forcing adoption of direct-to-chip liquid cooling and immersion systems. In December 2025, HPE and NVIDIA launched the first AI Factory Lab in Grenoble, France.

2. Sovereign Cloud and GAIA-X Federation

The EU's push for digital sovereignty is accelerating local-region cloud deployments. GAIA-X has onboarded more than 350 members by 2025, driving certified European colocation demand across BFSI, public sector, and healthcare verticals.

3. Edge Computing for 5G and IoT

Vodafone Germany inaugurated its nationwide 5G Standalone network in October 2024, covering over 92% of the population. Edge providers such as Quetta and EDGNEX are rapidly expanding micro-facilities to support sub-10 millisecond latency services.

4. Secondary Hub Development

Milan, Madrid, Warsaw, and Berlin are attracting fresh capital as FLAP-D cities face grid saturation. Start Campus's 1.2 GW Sines project (SIN01 opened April 2025) nearly doubled Portugal's national data center capacity.

5. Quantum and High-Performance Computing

IBM launched its first European quantum data center in Ehningen, Germany (October 2024). Germany's JUPITER system ranked as Europe's fastest supercomputer in 2025, reinforcing the region's HPC ecosystem.

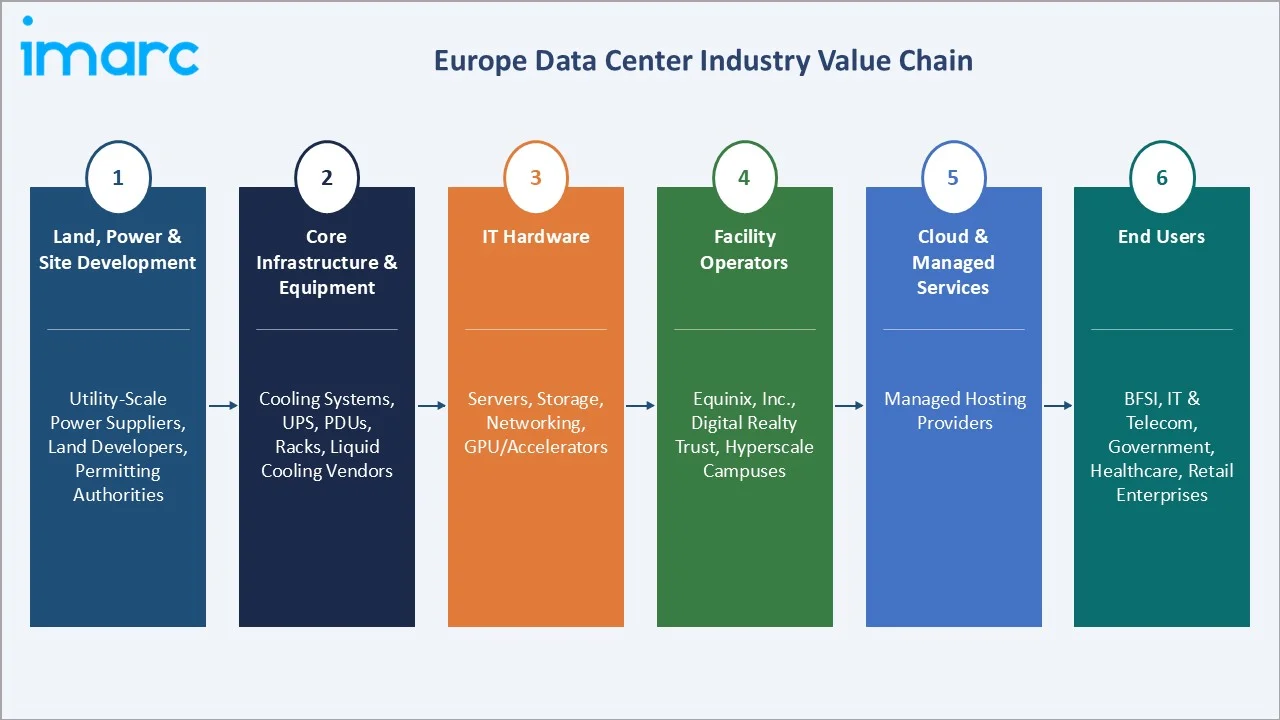

Industry Value Chain Analysis

The Europe data center value chain spans six stages from infrastructure supply through end-user service delivery. Each stage carries distinct capital intensity, regulatory exposure, and margin profile.

|

Stage |

Key Players / Examples |

|

Land, Power & Site Development |

High capital intensity with long permitting cycles; strategic location near power grids creates durable entry barriers |

|

Core Infrastructure & Equipment |

The specialized industrial supply segment is facing rising demand from AI-driven densification and supply chain constraints. |

|

IT Hardware |

Rapidly evolving compute layer reshaped by AI/GPU demand; vendor concentration provides pricing leverage |

|

Facility Operators (Colocation/Hyperscale) |

Highest strategic-value stage; benefits from long-term contracts, high switching costs, and hyperscaler demand |

|

Cloud & Managed Services |

Recurring subscription model with strong ecosystem lock-in via integrated platforms and enterprise relationships |

|

End Users |

Demand for the origination layer is increasingly outsourcing infrastructure, prioritizing uptime, compliance, and cost efficiency. |

Facility operators and hyperscale cloud providers occupy the highest strategic-value position in the European chain, consolidating infrastructure, power, connectivity, and software layers into integrated service offerings. Tier-1 equipment suppliers are increasingly bundling cooling, power, and rack-level reference designs, pushing the value chain toward end-to-end turnkey delivery.

Technology Landscape in the Europe Data Center Industry

Cooling Architecture: Liquid and Immersion

AI workloads with rack densities exceeding 60-100 kW are driving a structural migration from air to liquid cooling. Schneider Electric's September 2025 reference designs support 142 kW per rack deployments, signaling mainstream adoption in France and Germany.

Power and Renewable Energy Integration

Nordic hydropower, Iberian solar, and offshore wind PPAs are anchoring new hyperscale builds. Operators are deploying battery storage and hydrogen-ready backup systems to align with EU Energy Efficiency Directive reporting thresholds on PUE and water usage.

AI Infrastructure and GPU Clusters

European hyperscalers and sovereign-cloud providers are ring-fencing GPU capacity for regulated customers. HPE and NVIDIA's Grenoble AI Factory Lab (December 2025) is one of several European-located AI compute validation environments launched since 2024.

Sovereign Cloud and Confidential Computing

GAIA-X certification, SecNumCloud in France, and BSI C5 in Germany are setting region-specific compliance baselines. Confidential computing technologies, including Intel TDX and AMD SEV-SNP, are integrated into sovereign-cloud instances for defense, healthcare, and BFSI workloads.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Component | Solution | 66.8% |

2025 |

| Type | Hyperscale | 42.6% |

2025 |

| Enterprise Size | 🔒 | 🔒 |

2025 |

| End User | 🔒 | 🔒 |

2025 |

| Country | Germany | 22.7% | 2025 |

By Component

Solution commands a 66.8% majority share in 2025, reflecting the region's heavy capital deployment into servers, storage arrays, network switches, UPS systems, PDUs, precision cooling, and rack infrastructure. AI training hardware, particularly GPU-accelerated servers, has been the single largest growth driver within solutions since 2023.

To access detailed market analysis, Request Sample

Services at 33.2% in 2025 is the fastest-growing component sub-segment, driven by design-build engagements for greenfield hyperscale campuses, managed hosting, workload migration, and ongoing operations and maintenance. Outsourcing is rising as enterprises prefer OPEX-based colocation over legacy on-premise builds.

By Type

Hyperscale leads at 42.6% in 2025, driven by mega-campus programs from AWS, Microsoft, Google, and Meta. In February 2025, Brookfield Infrastructure Partners and Data4 announced plans to invest over USD 20.7 Billion in AI infrastructure across France over five years. NTT DATA in May 2025 disclosed plans exceeding USD 10 Billion for European builds, including a 128 MW Milan campus.

Colocation holds 34.1% share in 2025, underpinned by operators including Equinix, Digital Realty, Interxion, and Global Switch across FLAP-D hubs. Colt Technology Services' April 2025 sale of eight European data centers to NorthC marked a notable consolidation event in the colocation tier.

Edge captures 15.8% in 2025 and is the fastest-growing type sub-segment at approximately 11.4% CAGR through 2034, tied to 5G network deployments, real-time AI inference, and distributed content delivery. Others, at 7.5%, include modular, container, and micro data centers used for remote and mobile deployments.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

Germany |

22.7% |

DE-CIX Frankfurt hub, industrial IoT, IBM quantum center, GAIA-X leadership |

|

United Kingdom |

19.3% |

London financial workloads, AI investment, SWI Group 330 MW plan |

|

France |

16.8% |

Brookfield-Data4 USD 20.7B AI plan, SecNumCloud regulation, Paris hub |

|

Italy |

13.1% |

Milan hyperscale campuses, Microsoft USD 4.8B commitment, NTT 128 MW site |

|

Spain |

10.6% |

Madrid/Aragón AWS investments, solar PPA availability, Start Campus |

|

Others |

17.5% |

Netherlands, Ireland, Nordics free cooling, Poland/Austria emerging hubs |

Germany leads with a 22.7% country share in 2025, anchored by Frankfurt's DE-CIX internet exchange, one of the world's largest interconnection hubs. Germany hosts IBM's first European quantum data center (Ehningen, October 2024) and Europe's fastest supercomputer (JUPITER, 2025).

The United Kingdom holds 19.3% in 2025, centered on London's financial services workloads. SWI Group's 330 MW proposal between Cambridge and Peterborough and Scotland's GBP 3.9 billion Ravenscraig green plan signal pipeline depth.

France, at 16.8% in 2025, is defined by Paris as the primary hyperscale cluster and the Brookfield-Data4 USD 20.7 Billion AI commitment. Italy's 13.1% share is driven by Milan hyperscale build-outs, including Microsoft's USD 4.8 Billion and NTT's 128 MW campus (May 2025).

Spain (10.6%) is emerging as the fastest-rising Western European market, supported by AWS's Aragón investment. Others (17.5%) include the Netherlands, Ireland, and the Nordics, where free cooling and hydropower continue to attract AI-hyperscale projects such as Brookfield's SEK 95 billion Strängnäs expansion in June 2025.

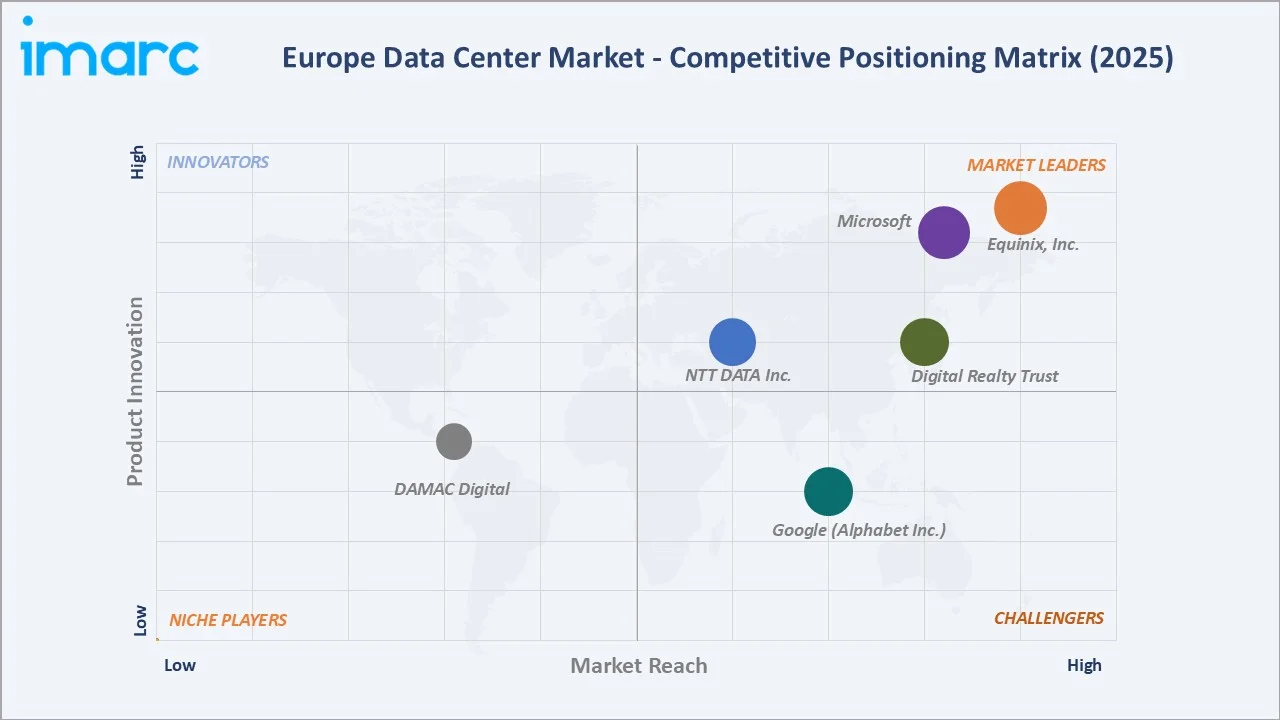

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Equinix, Inc. |

Platform Equinix |

Leader |

Retail colocation, interconnection, global footprint |

|

Digital Realty Trust |

PlatformDIGITAL |

Leader |

Hyperscale wholesale, data-gravity platform |

|

NTT DATA Inc. |

Global Data Centers |

Leader |

Wholesale hyperscale, Milan/Frankfurt campuses |

|

Microsoft |

Microsoft datacenters |

Leader |

Europe cloud regions, Italy/Spain investment |

|

Google (Alphabet Inc.) |

Data Centers |

Challenger |

AI compute, renewable PPAs, sustainability |

|

DAMAC Digital |

Edgnex Data Center |

Emerging |

Multi-country edge and hyperscale build-out |

Key Company Profiles

Equinix, Inc.

Equinix is the retail colocation operator, with more than 260 data centers globally and a strong European footprint spanning Frankfurt, London, Amsterdam, Paris, and Dublin. Platform Equinix and xScale hyperscale joint ventures anchor its European strategy.

- Product & Platform Portfolio: Platform Equinix, xScale Hyperscale, Equinix Fabric, Network Edge.

- Recent Developments: In March 2026, Equinix, Inc. announced that construction had begun on a new data center in Dublin. DB7x, which will be located in Blanchardstown, will be sited close to two of Equinix’s existing data centers for enhanced connectivity.

- Strategic Focus: Interconnection-led retail colocation, hyperscale wholesale joint ventures, and sustainability leadership via 100% renewable-energy procurement commitments.

Digital Realty Trust

Digital Realty operates one of the largest wholesale data center platforms worldwide, integrated with Interxion in Europe. Its PlatformDIGITAL strategy emphasizes 'data gravity' and multi-cloud interconnection.

- Product & Platform Portfolio: PlatformDIGITAL, ServiceFabric Connect, Interxion colocation.

- Recent Developments: In November 2025, Digital Realty announced the start of construction on its latest state-of-the-art data center in Frankfurt. Known as FRA20, the facility is expected to deliver approximately 16 megawatts (MW) of installed IT capacity across more than 8,100 square meters. It will be completed in two phases, supporting the growing demand for digital infrastructure in one of Europe’s key data hubs.

- Strategic Focus: Wholesale hyperscale delivery, enterprise-grade interconnection, and sustainability-aligned campus planning across Western Europe.

NTT DATA Inc.

NTT is a leading pan-European wholesale hyperscale operator, with large campuses in Frankfurt, London, Madrid, and Milan. In May 2025, NTT DATA disclosed plans exceeding USD 10 Billion for European builds, including a 128 MW Milan campus.

- Product & Platform Portfolio: NTT Global Data Centers, GDCE hyperscale campuses, edge solutions.

- Recent Developments: In May 2025, NTT DATA announced the accelerated expansion of its Global Data Centers division, securing land across North America, Europe, and Asia over the past six months to support nearly a gigawatt of planned data center capacity.

- Strategic Focus: Pan-European hyperscale wholesale, AI workload readiness, and enterprise managed services.

Market Concentration Analysis

The Europe data center market is moderately concentrated. The top five operators, including Equinix, Inc., Digital Realty Trust, NTT DATA Inc., Microsoft, Google (Alphabet Inc.), together command approximately 38-45% of colocation revenue in 2025.

Consolidation is accelerating at the operator tier. Portfolio aggregators Brookfield, KKR, DigitalBridge, and Blackstone have been acquiring regional operators, including Data4 and NorthC's 2025 addition of eight ex-Colt facilities. Fragmentation remains higher in edge and tier-3 retail colocation, where new entrants continue to emerge.

Investment & Growth Opportunities

Fastest-Growing Segments

Edge data centers are the highest-growth type sub-segment at approximately 11.4% CAGR through 2034, driven by 5G rollout, connected vehicle data, and distributed AI inference. Hyperscale remains the largest absolute growth contributor, adding an estimated USD 28-32 billion in new annual revenue between 2026 and 2034.

Emerging Market Expansion

Spain, Italy, Poland, and Portugal are transitioning from 'emerging' to 'core' markets. Start Campus's 1.2 GW Sines project in Portugal (SIN01 opened April 2025) nearly doubled national capacity in a single phase. Microsoft's USD 4.8 billion Italy commitment and AWS's multi-region Aragón build are anchoring the Iberian AI cluster.

Venture & Private Investment Trends

Hyperscale operator commitments in Europe exceeded EUR 50 billion in 2024. A EUR 720 million asset-backed securitization in 2024 reflected rising institutional trust in European data center real estate yields. Brookfield's June 2025 SEK 95 billion Sweden expansion and continuing infrastructure-fund sponsorship from KKR, Blackstone, and DigitalBridge underpin a deep forward pipeline.

Future Market Outlook (2026-2034)

The Europe data center market is projected to grow from USD 58.77 billion in 2025 to USD 126.17 billion by 2034 at a CAGR of 8.86%, more than doubling across the forecast window. Three structural shifts will define the outlook.

First, AI compute capacity will continue reshaping facility design, with liquid cooling, high-density racks exceeding 100 kW, and dedicated GPU campuses becoming mainstream. Second, regulatory localization under the EU Data Act, NIS2, and GAIA-X will drive sustained wholesale demand across Germany, France, and Italy. Third, secondary hubs, including Milan, Madrid, Warsaw, Berlin, and Lisbon, will absorb most net new capacity as FLAP-D hubs reach grid saturation.

By 2034, the European data center industry is forecast to be dominated by three operator archetypes: integrated hyperscale clouds, pan-European wholesale platforms, and sovereign-cloud specialists. Edge and modular deployments will complete the geographic density required for latency-sensitive AI inference.

Research Methodology

Primary Research

Primary research included structured interviews conducted in 2024-2025 with European data center stakeholders, including colocation operators, hyperscale cloud leads, infrastructure fund managers, equipment suppliers, and enterprise IT buyers. Interviews validated market sizing, segmentation splits, technology adoption timelines, and competitive positioning assessments.

Secondary Research

Secondary sources include the International Energy Agency (IEA), Uptime Institute, DE-CIX interconnection reports, GAIA-X federation publications, European Commission Data Act documentation, Eurostat digital economy statistics, operator annual reports, investor presentations, and trade publications, including Data Center Dynamics, BroadGroup, and Datacenter Forum.

Forecasting Models

Market size estimates and growth projections were derived using combined top-down and bottom-up modeling, integrating country-level IT spending, power capacity pipelines, hyperscale capex announcements, and regulatory milestones. Scenario analysis (base, optimistic, conservative) accounts for grid-approval timing, AI capex volatility, and energy cost variability.

Europe Data Center Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Components Covered | Solution, Services |

| Types Covered | Colocation, Hyperscale, Edge, Others |

| Enterprise Sizes Covered | Large Enterprises, Small and Medium Enterprises |

| End Users Covered | BFSI, IT and Telecom, Government, Energy and Utilities, Others |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others. |

| Companies Covered | Equinix, Inc., Digital Realty Trust, NTT DATA Inc., Microsoft, Google (Alphabet Inc.), DAMAC Digital, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe Data Center Market Report

The Europe data center market was valued at USD 58.77 Billion in 2025, driven by cloud migration, AI workload expansion, and sovereign-cloud mandates across Western Europe.

The market is projected to reach USD 126.17 Billion by 2034, growing at a CAGR of 8.86% during 2026 to 2034, propelled by AI capacity and hyperscale investments.

Solution leads with a 66.8% share in 2025, driven by heavy capital spend on servers, storage, networking equipment, UPS systems, and advanced liquid-cooling infrastructure.

Hyperscale dominates with a 42.6% share in 2025, supported by AWS, Microsoft, Google, and Meta announcing more than EUR 50 Billion in European commitments in 2024.

Germany leads with a 22.7% share in 2025, driven by Frankfurt's DE-CIX hub, industrial IoT demand, IBM's quantum data center, and GAIA-X federation leadership.

Key drivers include AI workload expansion, EU sovereign-cloud mandates, over EUR 50 billion in hyperscale commitments in 2024, 5G rollout, and renewable-energy availability.

Edge data centers are the fastest-growing type of sub-segment at approximately 11.4% CAGR through 2034, driven by 5G, IoT, and real-time AI inference deployments.

Leading companies include Equinix, Inc., Digital Realty Trust, NTT DATA Inc., Microsoft, Google (Alphabet Inc.), and DAMAC Digital.

AI drives rack densities above 60 kW, liquid-cooling adoption, GPU cluster builds, and an estimated USD 300+ Billion in global hyperscale capex in 2025 alone.

Germany leads with 22.7% share in 2025 due to Frankfurt's DE-CIX interconnection hub, Industry 4.0 demand, strong regulation, and large sovereign-cloud adoption.

EU climate-neutral infrastructure targets for 2030, renewable PPAs, waste-heat reuse, and strict PUE reporting under the Energy Efficiency Directive shape all new builds.

Milan, Madrid, Warsaw, Berlin, Lisbon, and Zurich are expanding fastest as FLAP-D cities face grid saturation and land constraints across central European locations.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)