Europe Furniture Market Size, Share, Trends and Forecast by Material, Distribution Channel, End-Use, and Country, 2026-2034

Europe Furniture Market Size, Share, Trends & Forecast (2026-2034)

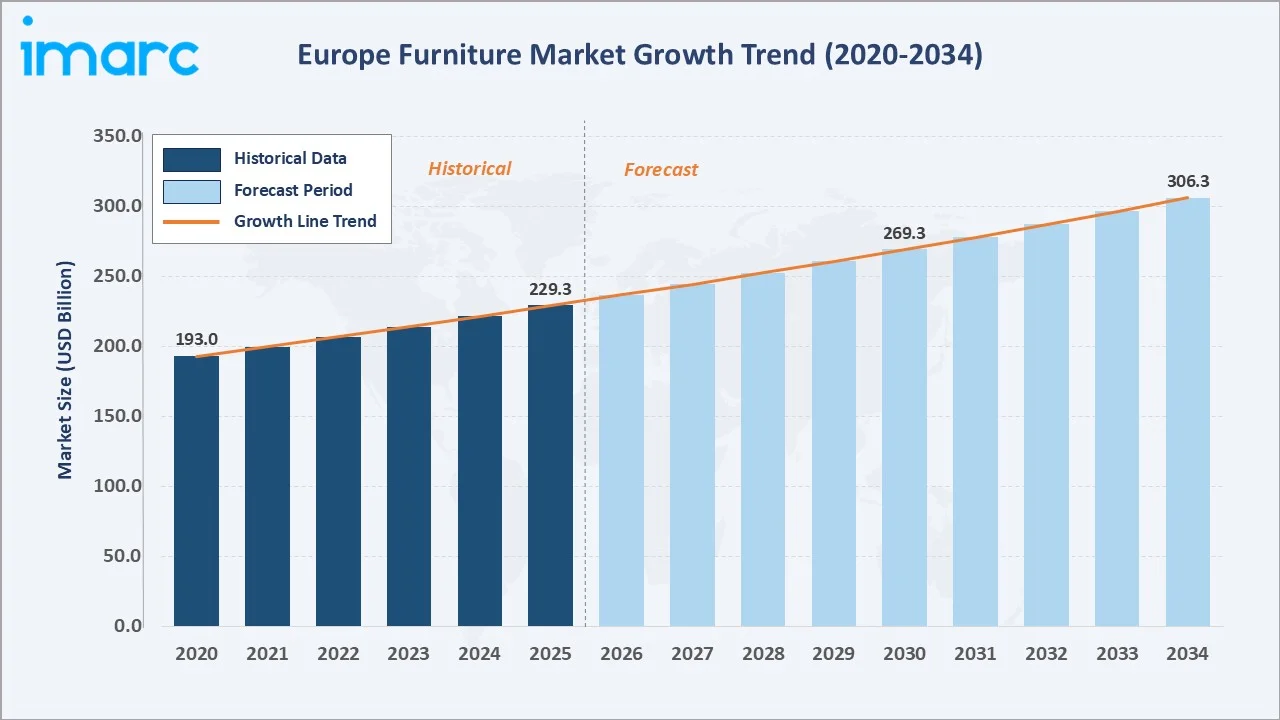

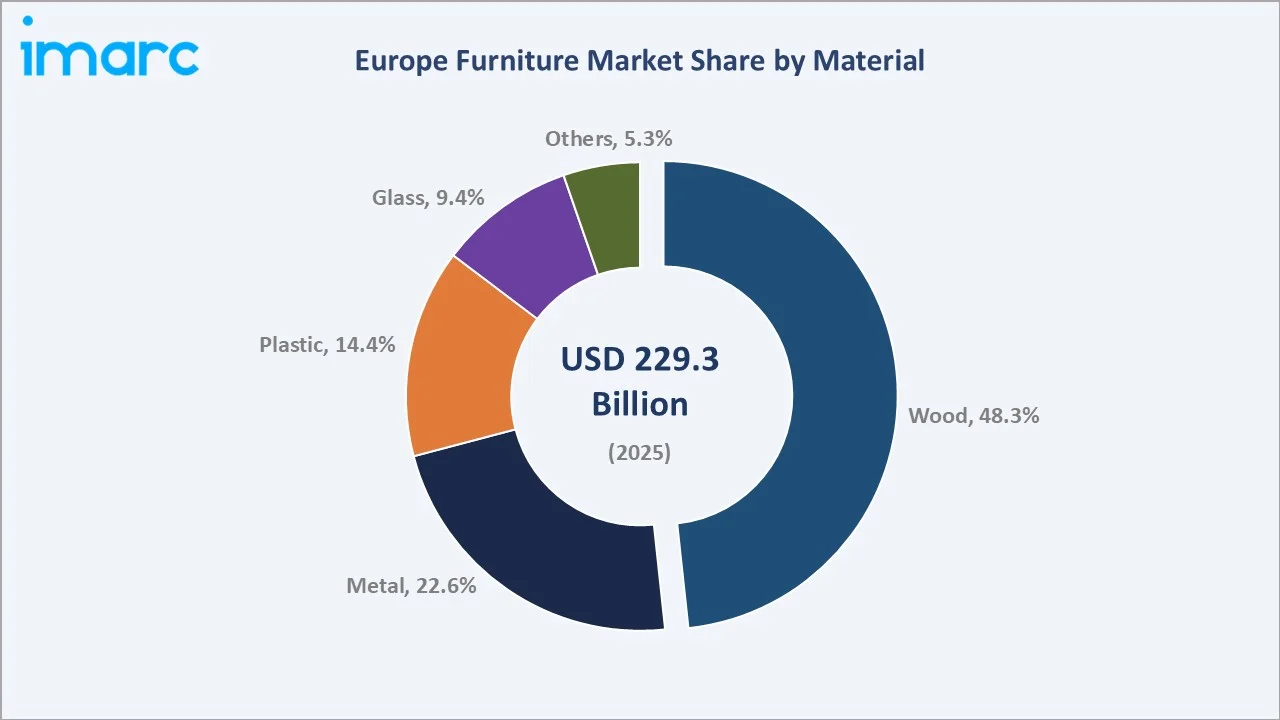

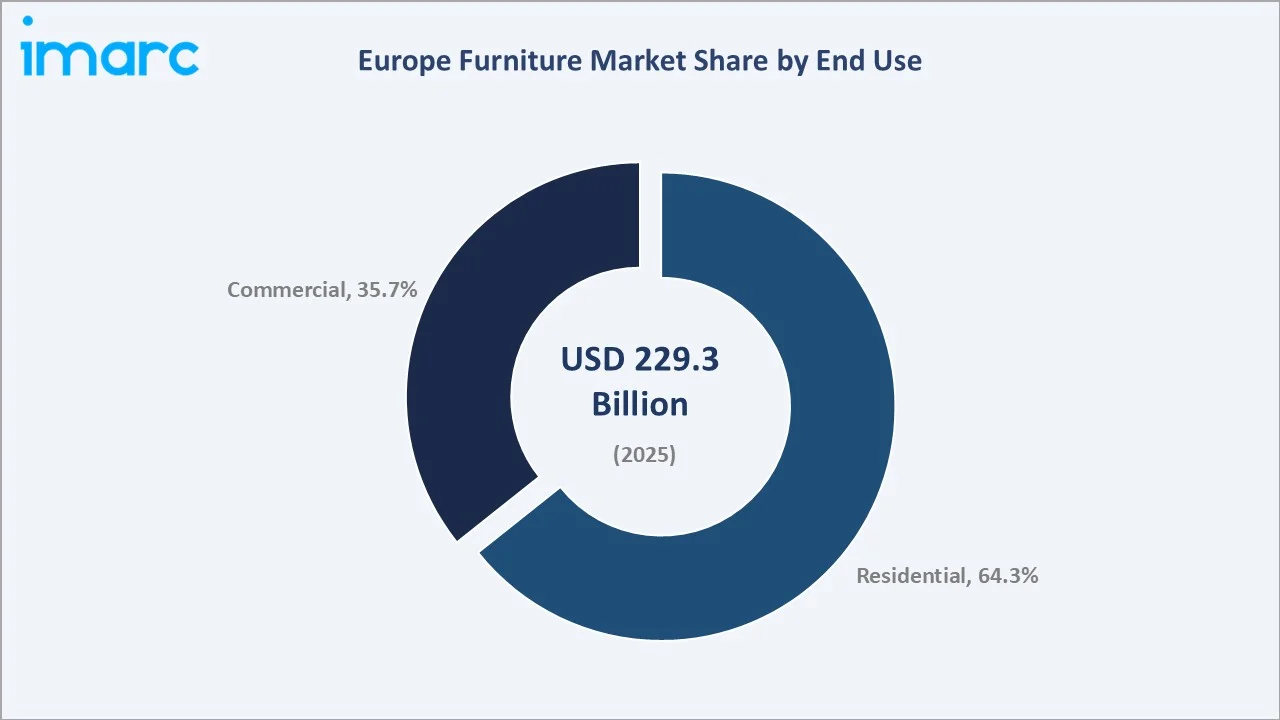

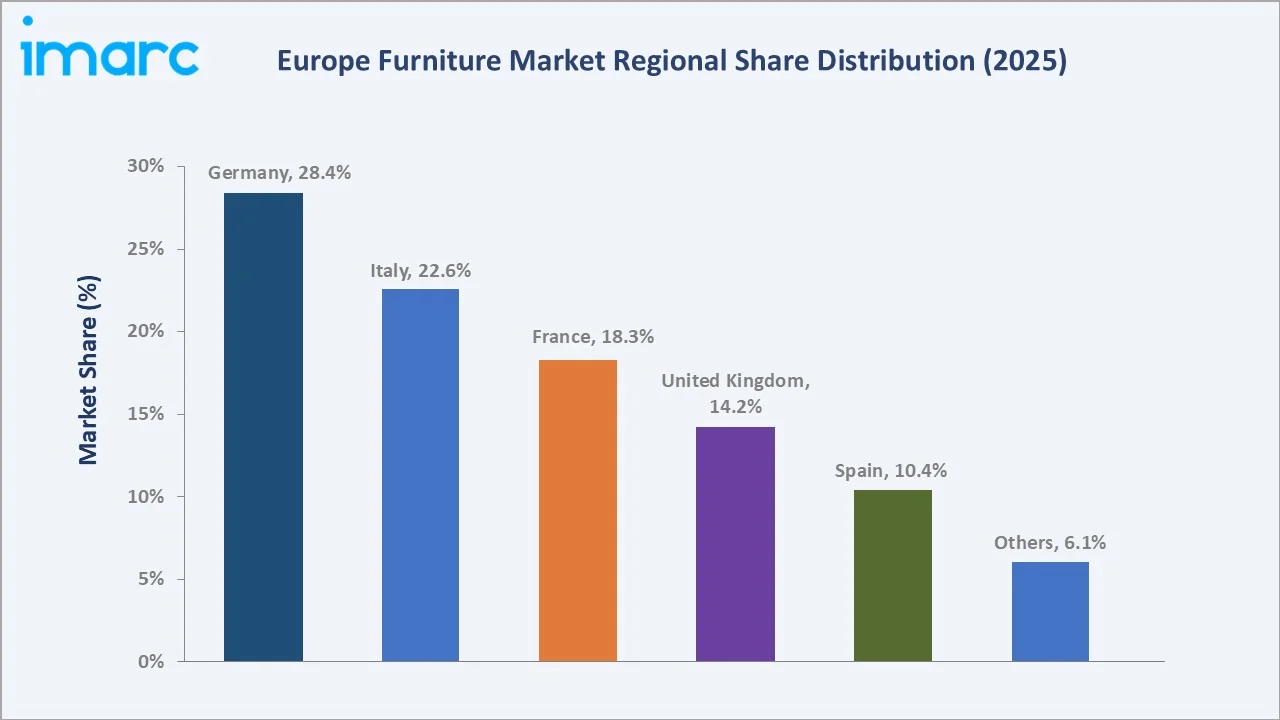

The Europe furniture market size was valued at USD 229.3 Billion in 2025 and is projected to reach USD 306.3 Billion by 2034, exhibiting a CAGR of 3.27% during 2026-2034. Rising urbanization, robust renovation activity, and surging e-commerce adoption are primary growth enablers. Wood dominates material choice at 48.3% in 2025, while Residential end use commands 64.3% of total revenue. Germany is the largest national market with 28.4% share, followed by Italy at 22.6%. The transition to sustainable, multifunctional, and digitally customized furniture is reshaping the competitive landscape across the region.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 229.3 Billion |

|

Forecast Market Size (2034) |

USD 306.3 Billion |

|

CAGR (2026-2034) |

3.27% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

Germany (28.4% share, 2025) |

|

Fastest Growing Country |

United Kingdom (online-driven growth) |

|

Leading Material |

Wood (48.3%, 2025) |

|

Leading End Use |

Residential (64.3%, 2025) |

To get more information on this market, Request Sample

Figure 1 illustrates the Europe furniture market growth trajectory from 2020 to 2034, covering historical expansion supported by post-pandemic renovation trends and a sustained forecast curve driven by urbanization and rising disposable incomes.

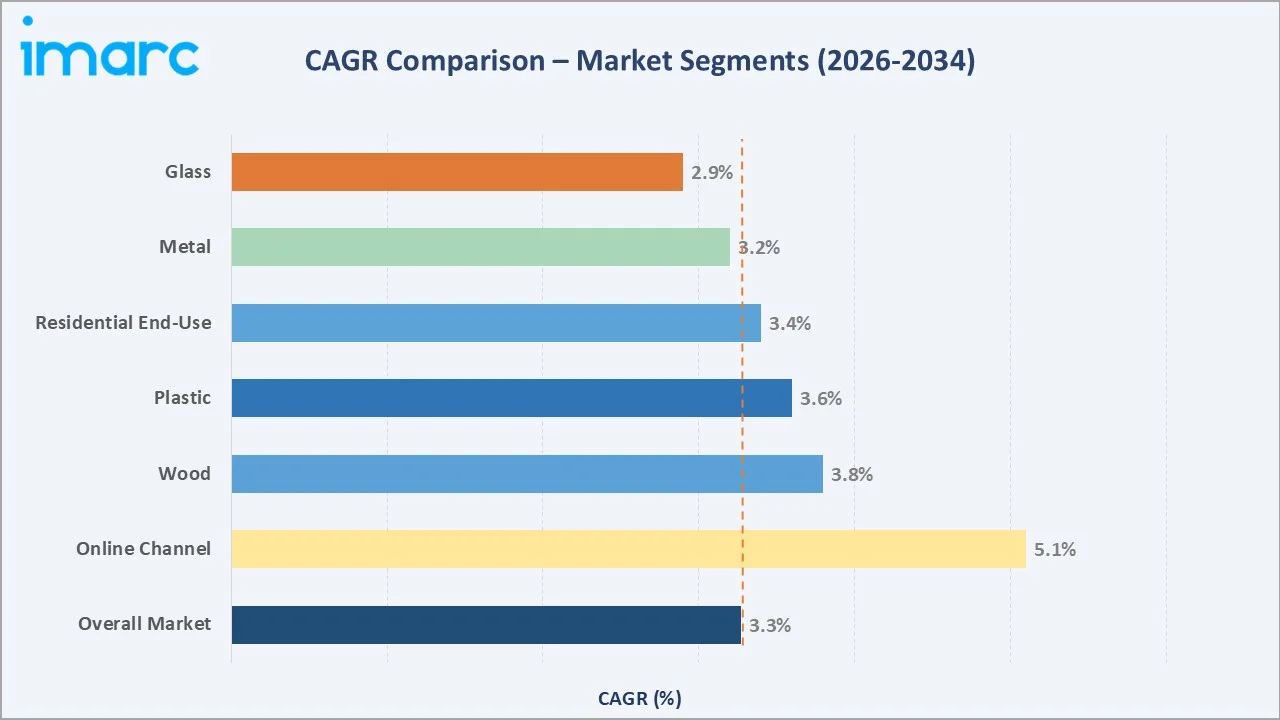

Figure 2 presents CAGR comparisons across material and channel sub-segments, with online distribution and wood-based furniture leading growth expectations through 2034.

Executive Summary

The Europe furniture market is undergoing a multi-dimensional transformation driven by demographic shifts, evolving consumer lifestyles, and the rapid digitalization of retail. Valued at USD 229.3 Billion in 2025, the market is forecast to reach USD 306.3 Billion by 2034 at a CAGR of 3.27%. Post-pandemic renovation momentum, accelerating urban housing completions across Germany and France, and growing workplace refurbishment activity across commercial real estate continue to sustain demand.

Wood retains its dominant position at 48.3% material share in 2025, underpinned by consumer preference for natural aesthetics, regulatory support for sustainably sourced timber, and its superior finish versatility. The residential end-use segment commands 64.3% of total market revenue, reflecting strong demand from both new housing projects and renovation upgrades. Online channels are emerging as the fastest-growing distribution route, with European e-commerce furniture sales growing at an estimated 5.1% CAGR through 2034, driven by platforms like IKEA.com and Wayfair.

Germany leads the regional landscape with a 28.4% market share in 2025, bolstered by its engineering-driven manufacturing heritage and premium consumer preference. Italy contributes 22.6%, anchored by its globally recognized design ecosystem and high-value export orientation.

Key Market Insights

|

Insight |

Data |

|

Largest Material Segment |

Wood – 48.3% share (2025) |

|

Fastest Growing Material |

Plastic – driven by design versatility & affordability |

|

Leading End Use |

Residential – 64.3% share (2025) |

|

Leading Country |

Germany – 28.4% share (2025) |

|

Fastest Growing Channel |

Online – e-commerce penetration rising across Europe |

|

Top Companies |

IKEA, Steelcase, Herman Miller, Kinnarps |

|

Market Opportunity |

Sustainable & smart furniture demand – growing at ~5% annually |

Key Analytical Observations Supporting The Above Data:

- Wood Material Leadership: Wood's 48.3% dominance in 2025 reflects deep-rooted consumer affinity for natural materials, further reinforced by EU sustainability mandates favoring FSC-certified timber supply chains.

- Germany's Market Dominance: Germany's 28.4% national share in 2025 is anchored by its high per-capita furniture expenditure, estimated at over EUR 750 per household annually, and by the presence of major contract furniture exporters serving pan-European B2B buyers.

- Residential End-Use Supremacy: The residential segment's 64.3% share reflects urbanization-led household formation, particularly in Tier-2 cities of Eastern Europe, where rising incomes are driving first-time furnishing expenditure.

- E-Commerce Growth Acceleration: Online channels are growing at a CAGR of approximately 5.1% through 2034, outpacing offline retail as augmented reality tools and AI-driven room planners reduce the physical inspection barrier to furniture purchase.

- Sustainability Premium Segment: Sustainable furniture lines - using recycled materials, low-VOC finishes, and circular take-back schemes - are growing at an estimated 6-8% annually, capturing a premium price segment increasingly prioritized by millennial and Gen Z consumers across Western Europe.

Global Europe Furniture Market Overview

The Europe furniture market encompasses a broad ecosystem of products spanning living room, bedroom, kitchen, bathroom, office, and outdoor furniture categories. Manufacturers serve both residential consumers and commercial customers including hospitality, corporate offices, healthcare, and educational institutions. Key raw materials include solid wood, engineered wood panels (MDF, particleboard), metals (steel, aluminum), plastics, glass, and textile upholstery fabrics.

Macroeconomic enablers include approximately 4.5 million housing completions annually across Europe, European household renovation expenditure exceeding EUR 180 Billion per year, and sustained corporate real estate investment despite hybrid work adoption. The ecosystem spans raw material extraction through finished product retail, with Italy and Germany serving as the continent's two most significant manufacturing and export hubs.

Market Dynamics

To evaluate market opportunities, Request Sample

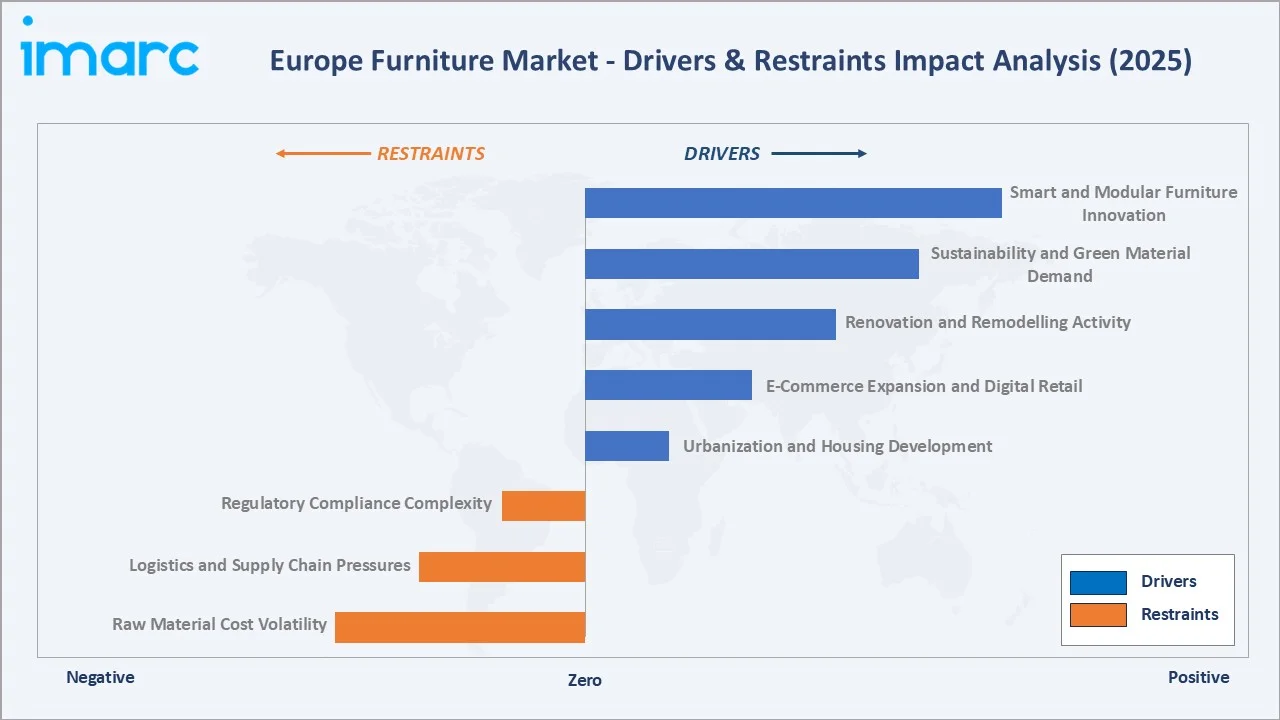

Market Drivers

- Urbanization and Housing Development: Europe adds approximately 2-2.5 million new urban households annually. This directly fuels baseline furniture demand. Germany alone saw over 251,900 new residential units completed in 2024, each requiring furnishing investment averaging EUR 8,000-12,000 per household.

- E-Commerce Expansion and Digital Retail: European e-commerce furniture sales reached a significant milestone in 2024, with digital channels playing an increasingly central role. IKEA’s online platform now contributes a substantial portion of its European revenue, reflecting a strong shift toward digital sales.

- Renovation and Remodelling Activity: Post-pandemic renovation momentum remains elevated. European households allocated an estimated average of EUR 4,200 to home improvement in 2024, with furniture representing the single largest expenditure category.

- Sustainability and Green Material Demand: Consumer preference for eco-certified, sustainable furniture is growing measurably, particularly in Germany, the Netherlands, and Scandinavia, where eco-labelled furniture commands a 15-25% price premium while still achieving strong sell-through rates.

Market Restraints

- Raw Material Cost Volatility: Timber price indices experienced significant volatility between 2022 and 2024, driven by supply chain disruptions and competing biomass energy demand. This compresses manufacturer margins and constrains pricing stability for retailers.

- Logistics and Supply Chain Pressures: European logistics costs have experienced significant upward pressure between 2021 and 2024. Furniture's volumetric weight characteristics make it disproportionately sensitive to freight rate increases compared to other consumer goods categories.

Market Opportunities

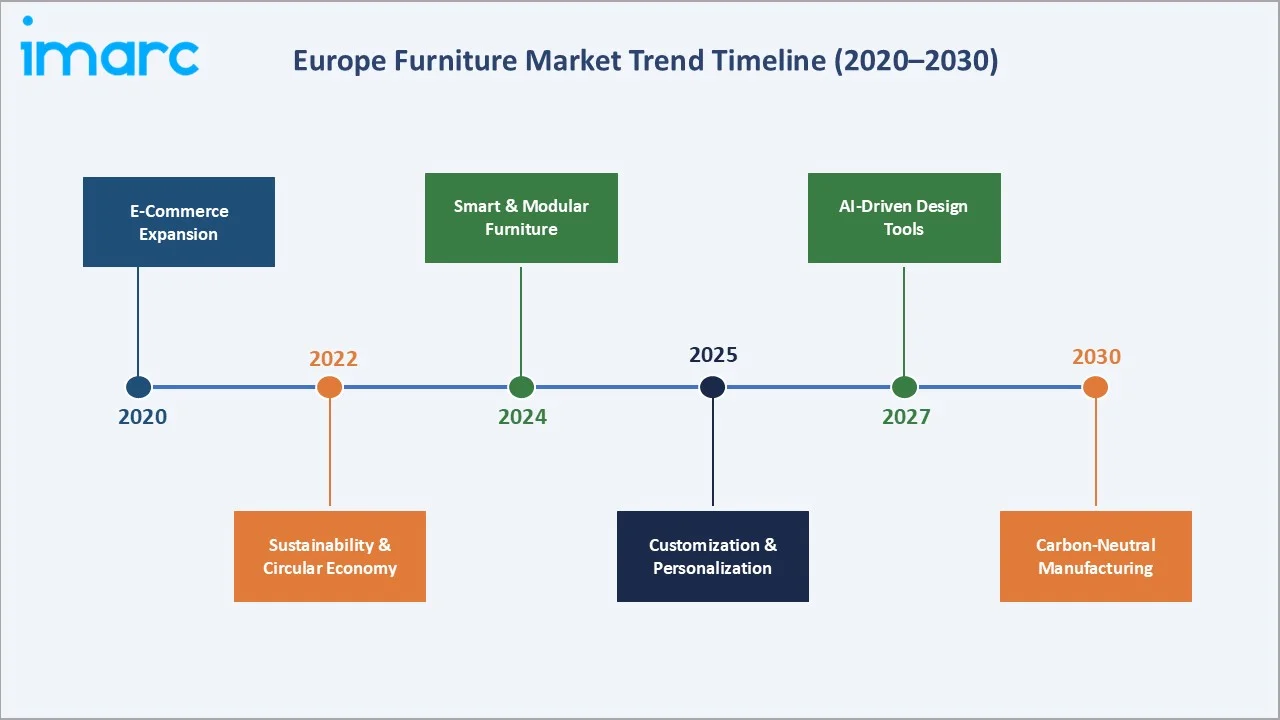

- Smart and Modular Furniture Innovation: Modular, space-efficient furniture designed for smaller urban apartments represents a high-growth opportunity. Smart furniture integrating USB charging, IoT sensors, and adjustable ergonomic features is entering commercial mainstream from 2025-2027.

- Eastern European Market Expansion: Poland, Czech Republic, Romania, and Hungary are experiencing 5-7% annual residential construction growth. These markets present significant under-penetrated demand for mid-range furniture that international brands are beginning to address systematically.

- Circular Economy Revenue Models: Circular furniture models - subscription-based office furniture (as pioneered by Feather and Fernish) and manufacturer take-back refurbishment schemes - open new recurring revenue streams with sustainability-driven institutional buyers.

Market Challenges

- Regulatory Compliance Complexity: EU Taxonomy regulations, REACH chemical compliance, and evolving FSC/PEFC certification requirements impose increasing compliance costs on manufacturers, particularly affecting smaller artisanal producers in Italy and Spain.

- Customization vs. Scale Tension: Consumer demand for mass-customized furniture (personalized dimensions, material combinations, color configurations) conflicts with manufacturing economies of scale, requiring manufacturers to invest in flexible production and digital configurator infrastructure.

Emerging Market Trends

1. E-Commerce and Omnichannel Retail Integration

Online furniture retail in Europe is expected to experience steady growth over the coming years, with the market projected to expand significantly by the middle of the decade. Augmented reality room visualization tools - deployed by IKEA, Wayfair, and Made.com - are reducing consumer hesitation around online furniture purchase, with AR-assisted browsers converting at 2.7x the rate of non-AR sessions.

2. Sustainability and Circular Economy Models

EU Green Deal directives are accelerating the transition to sustainably sourced materials. Over 68% of European furniture buyers in 2024 surveys cited environmental credentials as a purchase consideration. Manufacturers integrating FSC-certified wood, bio-based plastics, and circular take-back programs are commanding measurable market share gains.

3. Smart and Multifunctional Furniture

Urbanization in European cities is driving demand for space-efficient, multifunctional furniture. Products integrating wireless charging surfaces, IoT-enabled adjustable desks, and sensor-embedded ergonomic seating are growing at an estimated 8-10% annually within the premium commercial segment.

4. Nearshoring and European Manufacturing Resurgence

Post-pandemic supply chain vulnerabilities and rising Asian logistics costs are driving European OEMs to reshore or nearshore production. Poland's furniture manufacturing output exceeded EUR 14 Billion in 2024, as Western European brands increasingly source from Central European production bases to reduce lead times and carbon footprints.

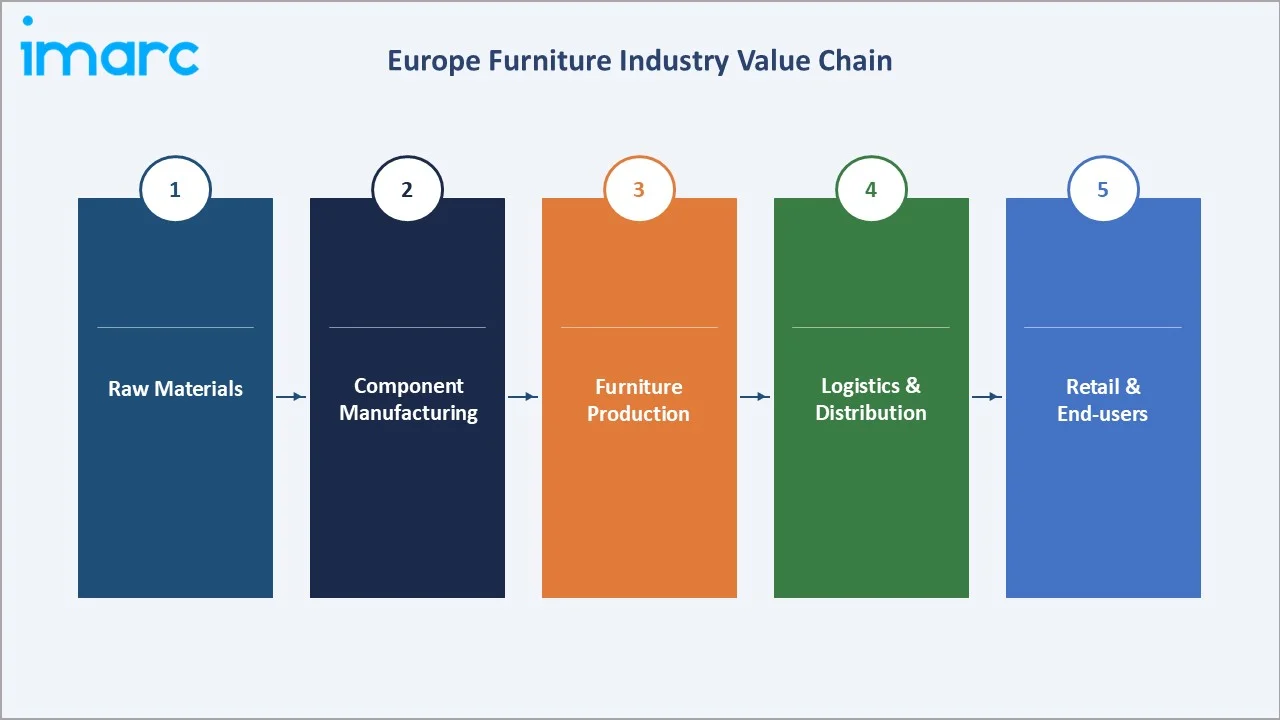

Industry Value Chain Analysis

The Europe furniture value chain spans five integrated stages from raw material extraction through end-user delivery. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Timber suppliers, metal smelters, glass producers, plastic resin manufacturers |

|

Component Manufacturing |

Hardware producers, foam & fabric suppliers, panel board mills |

|

Furniture Manufacturing |

IKEA, Steelcase, Kinnarps, USM, regional OEMs (Italy, Germany, Poland) |

|

Logistics & Distribution |

Rail/road freight, port logistics, Amazon Logistics, XPO Logistics, DSV |

|

Retail & End Users |

Specialty retailers, e-commerce platforms, B2B contract sales |

The manufacturing stage generates the highest value-add, with integrated manufacturers in Italy and Germany commanding 30-40% gross margins on premium product lines versus 12-18% for volume-oriented producers in Eastern Europe.

Technology Landscape in the Furniture Industry

Sustainable Material Innovation

Cross-laminated timber (CLT), thermally modified wood, and bio-based polymers are gaining adoption as Europe's furniture manufacturers seek to meet EU Taxonomy alignment requirements. Engineered wood panels with formaldehyde-free binders are becoming mainstream, particularly in Germany and Scandinavia where indoor air quality standards are most stringent. Recycled aluminum content in metal furniture frames has increased to an average of 62% across European OEM production in 2024.

Digital Design and Manufacturing Technologies

CNC routing, robotics-assisted assembly, and Industry 4.0 production management systems are transforming furniture manufacturing economics. Italian furniture cluster manufacturers (Brianza, Pesaro) are adopting digital twin production planning, reducing material waste by 15-20%. 3D-printed furniture components for bespoke residential applications are advancing beyond prototyping into limited commercial production by Voxel chair and other premium innovators.

Smart Connectivity and IoT Integration

Height-adjustable smart desks with integrated posture sensors and usage analytics represent the fastest-growing commercial furniture technology category, growing at approximately 11% annually in Western Europe. Herman Miller's Live OS ecosystem and Steelcase's CoRo platform are establishing the commercial standard for sensor-integrated, data-driven workspace furniture management.

E-Commerce and Virtual Reality Tools

Augmented reality furniture placement apps now feature in over 40 European retailer applications, including IKEA Place, Maisons du Monde, and Westwing. AI-powered space planning tools that generate furniture layouts from uploaded room photographs are reducing the sales-to-close cycle by an estimated 30% in online retail contexts.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Material |

Wood |

48.3% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

End Use |

Residential |

64.3% |

2025 |

|

Country |

Germany |

28.4% |

2025 |

By Material

To access detailed market analysis, Request Sample

Wood commands a 48.3% majority share in 2025, underpinned by its aesthetic versatility, structural durability, and alignment with sustainability preferences. Oak, walnut, and pine continue as the most commercially significant species in European residential furniture.

Metal at 22.6% is the second-largest material segment, driven by strong demand in commercial and contract furniture. Powder-coated steel and brushed aluminum dominate office furniture applications. Plastic (14.4%) benefits from design versatility and cost efficiency, while Glass (9.4%) maintains premium positioning in dining and display furniture categories. Others (5.3%) include emerging bio-composites and rattan.

By End Use

Residential end use leads at 64.3% in 2025, reflecting Europe's sustained household formation rates, renovation activity, and lifestyle-driven furniture replacement cycles averaging 7-10 years per category. Housing completions across Europe exceeded 1.8 million units in 2024, each representing a direct furnishing demand trigger.

Commercial end use at 35.7% in 2025 spans corporate office refurbishment, hospitality (hotels, restaurants), healthcare (hospital beds, clinical seating), and educational institution furniture. Return-to-office trends, estimated at 3.5 office days per week average across Europe in 2024, sustained corporate furniture procurement budgets at approximately 70% of pre-pandemic levels.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

Germany |

28.4% |

Manufacturing excellence, premium demand, strong interior design culture; IKEA, Steelcase presence |

|

Italy |

22.6% |

Global design hub; luxury and artisanal exports; Salone del Mobile driving global trend cycles |

|

France |

18.3% |

Strong renovation spending; rising e-commerce penetration; Roche Bobois and Maisons du Monde |

|

United Kingdom |

14.2% |

Post-Brexit sourcing shifts; online retail surge; DFS and John Lewis anchor market activity |

|

Spain |

10.4% |

Tourism-linked hospitality furniture demand; growing residential construction sector |

|

Others |

6.1% |

Poland, Netherlands, Sweden – growing manufacturing bases and rising consumer spending |

Germany's 28.4% market share in 2025 reflects its status as Europe's largest national economy, with per-household furniture expenditure among the highest in the continent. Leading companies including Steelcase GmbH, Vitra GmbH, and regional specialists benefit from Germany's precision manufacturing heritage.

Italy's 22.6% share in 2025 is underpinned by the country's globally recognized design ecosystems centered on the Brianza district and the Pesaro-Urbino cluster. The annual Salone del Mobile in Milan sets global design direction, influencing purchasing decisions from Dubai to Tokyo. France at 18.3% benefits from strong renovation grant programs (MaPrimeRénov') that indirectly stimulate interior furniture upgrades.

Competitive Landscape

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

IKEA |

IKEA |

Leader |

Flat-pack design, massive retail footprint, e-commerce dominance |

|

Steelcase Inc. |

Gesture, Leap |

Leader |

Contract commercial furniture; ergonomic innovation; global OEM |

|

Herman Miller, Inc. ( MillerKnoll ) |

Herman Miller |

Leader |

Premium ergonomic design; B2B & direct-to-consumer luxury |

|

Kinnarps |

Kinnarps |

Challenger |

Scandinavian sustainability focus; office & healthcare furniture |

|

USM Modular |

USM Haller |

Challenger |

Modular precision furniture; high-end commercial & residential |

|

Haworth |

Haworth |

Challenger |

Integrated workspace solutions; strong EMEA presence |

|

Nowy Styl |

Nowy Styl Group |

Challenger |

Central & Eastern European leader; office seating specialist |

|

Vitra |

Vitra |

Emerging |

Iconic designer collaborations; premium retail & contract |

|

Artifort |

Artifort |

Emerging |

Dutch design heritage; contract hospitality & office seating |

The European furniture competitive landscape is characterized by IKEA's dominant volume market position - estimated at 15-18% overall European revenue share - alongside a rich ecosystem of premium design brands, specialist commercial suppliers, and fast-growing e-commerce pure plays.

Key Company Profiles

IKEA

IKEA is the global and European leader in mass-market furniture retail, with extensive operations across Europe and a rapidly growing digital channel that plays a significant role in its European revenue. Its flat-pack design philosophy, vertically integrated supply chain, and in-house forestry operations through Ingka Group's forest assets deliver structural cost advantages that no competitor has fully replicated.

- Product Portfolio: Living, bedroom, kitchen, bathroom, outdoor furniture; home textiles, lighting, storage solutions.

- Recent Developments (2024-2025): IKEA plans to open 20 new small-format stores across Europe and North America, bringing its products closer to urban customers. These stores are part of IKEA’s broader strategy to expand retail reach and enhance customer convenience.

- Strategic Focus: Circular by 2030 commitment targeting 100% recycled or renewable material use; expansion of IKEA Buy Back & Resell program across all European markets by 2026.

Steelcase Inc.

Steelcase is the world's largest commercial furniture manufacturer, with its European operations centered in Munich and manufacturing in Sarrebourg, France. The company holds a leading position in ergonomic office seating, activity-based working environments, and healthcare furniture across the continent.

- Product Portfolio: Gesture seating, Leap V2, Flex Collection, Ology sit-stand desks, medical-grade clinical furniture.

- Recent Developments (2024-2025): In August 2025, Steelcase agreed to be acquired by HNI Corporation in a deal worth around USD 2.2 billion, creating a larger commercial furniture platform positioned to better serve global markets including Europe and the Americas.

- Strategic Focus: Hybrid work solutions architecture - designing furniture systems that serve both in-office and remote work environments - positions Steelcase to capture corporate redesign budgets estimated at EUR 4-6 Billion annually across Europe.

Herman Miller Inc. (MillerKnoll)

Herman Miller, now part of the MillerKnoll group following its 2021 merger with Knoll, is the global reference for premium ergonomic seating and design-led workspace furniture. Its European presence spans corporate clients, premium retail, and the hospitality contract sector.

- Product Portfolio: Aeron Chair, Embody, Mirra 2, Sayl; Knoll Florence Collection; OFS ancillary furniture.

- Recent Developments (2024-2025): Herman Miller will expand the brand's online store presence across Europe this spring with e-commerce websites for Denmark, Finland, Spain, and Sweden. Customers will be able to shop Herman Miller's award-winning ergonomic office chairs portfolio, including Aeron, Cosm, Mirra 2, Setu, and Embody.

- Strategic Focus: Premium positioning in the activity-based working segment, targeting Fortune 500 European headquarters redesigns; circular product take-back and refurbishment programs in Germany, UK, and France.

Kinnarps

Kinnarps is Scandinavia's largest office furniture manufacturer and one of Europe's most recognized sustainability-focused contract suppliers. Headquartered in Kinnarp, Sweden, the company operates manufacturing in Sweden and Poland and distributes through a pan-European dealer network.

- Product Portfolio: Capella seating, 55+ series desks, table collections, healthcare and educational furniture systems.

- Recent Developments (2024-2025): Kinnarps achieved EU Ecolabel certification across its full core seating range in 2024, making it the first European office furniture manufacturer to do so, and launched its furniture-as-a-service subscription pilot in Sweden and Germany.

- Strategic Focus: Sustainability leadership through extended product responsibility - offering 25-year guarantees and carbon footprint labeling on all products - targets the rapidly growing public sector and ESG-driven corporate procurement segment.

Market Concentration Analysis

The Europe furniture market exhibits moderate fragmentation at the overall market level, with the top four companies - IKEA, Steelcase, MillerKnoll, and Kinnarps - collectively accounting for approximately 28-30% of total European revenue in 2025. This relatively low top-4 concentration reflects the breadth of product categories, price tiers, and geographic sub-markets that constitute the overall European furniture landscape.

Within specific sub-segments, concentration is considerably higher. In ergonomic office seating, Steelcase, MillerKnoll, and Kinnarps command approximately 45-50% of the premium contract market. In mass-market retail, IKEA alone represents an estimated 15-18% of total European furniture consumer spending. The luxury and designer segment remains highly fragmented, with no single brand exceeding 3-5% share across Italy's artisanal manufacturer ecosystem.

Consolidation trends are evident in the mid-market commercial segment, where private equity platforms including Nowy Styl and Kinnarps have executed multiple bolt-on acquisitions of regional specialists since 2020.

Investment & Growth Opportunities

Fastest-Growing Segments

Online furniture retail is the highest-growth channel at approximately 5.1% CAGR through 2034. Investment in AI room planning, AR try-before-you-buy tools, and last-mile furniture delivery automation represents the highest-priority technology investment theme for both established retailers and venture-backed challengers.

Smart and IoT-integrated furniture is growing at 8-11% annually within the commercial premium segment. Startup ecosystems in Germany and the Netherlands are attracting seed and Series A investment for IoT-enabled desk systems, posture monitoring chairs, and sensor-embedded meeting room furniture.

Emerging Market Expansion

Central and Eastern European markets - Poland, Czech Republic, Hungary, and Romania - present high-growth opportunities with residential construction rates 2-3x higher than Western Europe and furniture penetration rates still 35-45% below German or French per-household levels.

Venture & Private Investment Trends

Sustainable material start-ups using mycelium composites and agricultural waste fiber for furniture panels attracted combined European VC investment of approximately EUR 85 Million in 2023-2024. Contract furniture software platforms enabling furniture-as-a-service billing models are attracting SaaS-multiple valuations from PE investors targeting the asset-light commercial real estate segment.

Future Market Outlook (2026-2034)

The Europe furniture market forecast projects consistent value expansion from USD 229.3 Billion in 2025 to USD 306.3 Billion by 2034 at a CAGR of 3.27%. This growth trajectory reflects a mature, innovation-driven market rather than a high-velocity emerging economy expansion - characterized by premiumization, sustainability-led replacement cycles, and digital channel share gains rather than raw volume growth.

Three structural shifts will most significantly reshape the market through 2034. First, the transition from transactional furniture retail to subscription and circular service models will fundamentally alter revenue recognition, brand loyalty economics, and competitive barriers to entry. Second, AI-driven design customization at scale - enabling genuine mass-personalization without mass-production cost penalties - will restructure competitive differentiation from aesthetics toward digital platform capability. Third, sustainability regulatory intensity will continuously raise the compliance baseline, progressively disadvantaging manufacturers without credible circular economy commitments from B2B and institutional procurement processes.

By 2034, Germany, Italy, France, and the UK will collectively retain approximately 83% of European market revenue, but the fastest absolute growth will occur in Central and Eastern Europe, where combined furniture market value is forecast to expand from approximately USD 28 Billion in 2025 to USD 42 Billion by 2034 - representing a regional CAGR of approximately 4.5%.

Research Methodology

Primary Research

Primary research encompassed over 50 structured interviews conducted in 2024-2025 with furniture industry stakeholders including product directors at leading European manufacturers, retail buyers at major furniture chains, real estate and interior design procurement managers, sustainability officers, and institutional investors in furniture technology. Primary insights validated market sizing, segmentation share estimates, technology adoption timelines, and competitive positioning assessments.

Secondary Research

Secondary sources include Eurostat housing construction and household expenditure data, CSIL (Centre for Industrial Studies) European furniture industry reports, EFIC (European Furniture Industries Confederation) trade statistics, Euromonitor Passport retail furniture market data, company annual reports (IKEA Group Sustainability Report 2024, MillerKnoll Annual Report 2024), and trade publications including Furniture News Europe, Interieur, and Business of Home.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, housing construction indices, household renovation expenditure trends, and channel-specific growth rate analysis. Scenario analysis covering base, optimistic, and conservative cases was performed to account for macroeconomic uncertainty including potential Eurozone growth slowdown and energy cost volatility.

Europe Furniture Market Report Coverage

|

Attribute |

Details |

|

Market Size |

USD 229.3 Billion (2025) to USD 306.3 Billion (2034) |

|

CAGR |

3.27% during 2026-2034 |

|

Segmentation – Material |

Wood, Metal, Plastic, Glass, Others |

|

Segmentation – Distribution Channel |

Supermarkets/Hypermarkets, Specialty Stores, Online Stores, Others |

|

Segmentation – End Use |

Residential, Commercial |

|

Regional Coverage |

Germany, Italy, France, United Kingdom, Spain, Others |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Companies Covered |

IKEA, Steelcase Inc., Herman Miller, Inc. ( MillerKnoll ), Kinnarps, USM Modular, Haworth, Nowy Styl, Vitra, Artifort, etc. |

|

Report Format |

PDF + Excel |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe furniture market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Europe furniture market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe furniture industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe Furniture Market Report

The Europe furniture market was valued at USD 229.3 Billion in 2025, driven by urbanization, renovation trends, and growing e-commerce channel adoption across the region.

The market is projected to reach USD 306.3 Billion by 2034, growing at a CAGR of 3.27% during 2026-2034, driven by sustainability-led premiumization, digital retail expansion, and Central European market growth.

Wood leads with a 48.3% share in 2025, driven by consumer preference for natural aesthetics, FSC-certified timber availability, and the versatility of wood in both mass-market and premium furniture categories.

Residential end use leads at 64.3% in 2025, reflecting sustained household formation, renovation activity, and lifestyle-driven furniture replacement cycles across European countries.

Germany leads with a 28.4% share in 2025, supported by high per-household furniture spend, strong manufacturing exports, and robust residential construction activity.

Key drivers include 4.5 million annual housing completions, EUR 180 Billion annual renovation spend, e-commerce adoption, sustainability demand, and smart furniture technology integration.

Online retail is the fastest-growing channel at approximately 5.1% CAGR through 2034, driven by AR visualization tools, AI room planners, and improved last-mile delivery infrastructure.

Leading companies include IKEA, Steelcase, Herman Miller (MillerKnoll), Kinnarps, USM Modular, Haworth, Nowy Styl, Vitra, and Artifort, etc.

EU Green Deal compliance, FSC certification demand, circular economy models, and consumer eco-preference are driving 6-8% annual growth in sustainable furniture lines across Western Europe.

E-commerce accounts for approximately 28-32% of European furniture sales in 2025 and is growing at 5.1% CAGR, with AR tools and AI configurators significantly improving online conversion rates.

Central and Eastern Europe (Poland, Czech Republic, Hungary, Romania) is growing at approximately 4.5% CAGR, driven by housing construction 2-3x faster than Western Europe.

Key challenges include raw material cost volatility (timber prices fluctuated 22% in 2022-2024), logistics cost inflation, EU regulatory compliance burden, and IKEA's dominant price-point competition.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade