Europe Ice Cream Market Size, Share, Trends and Forecast by Flavor, Category, Product, Distribution Channel, and Region, 2026-2034

Europe Ice Cream Market Size, Share, Trends & Forecast (2026-2034)

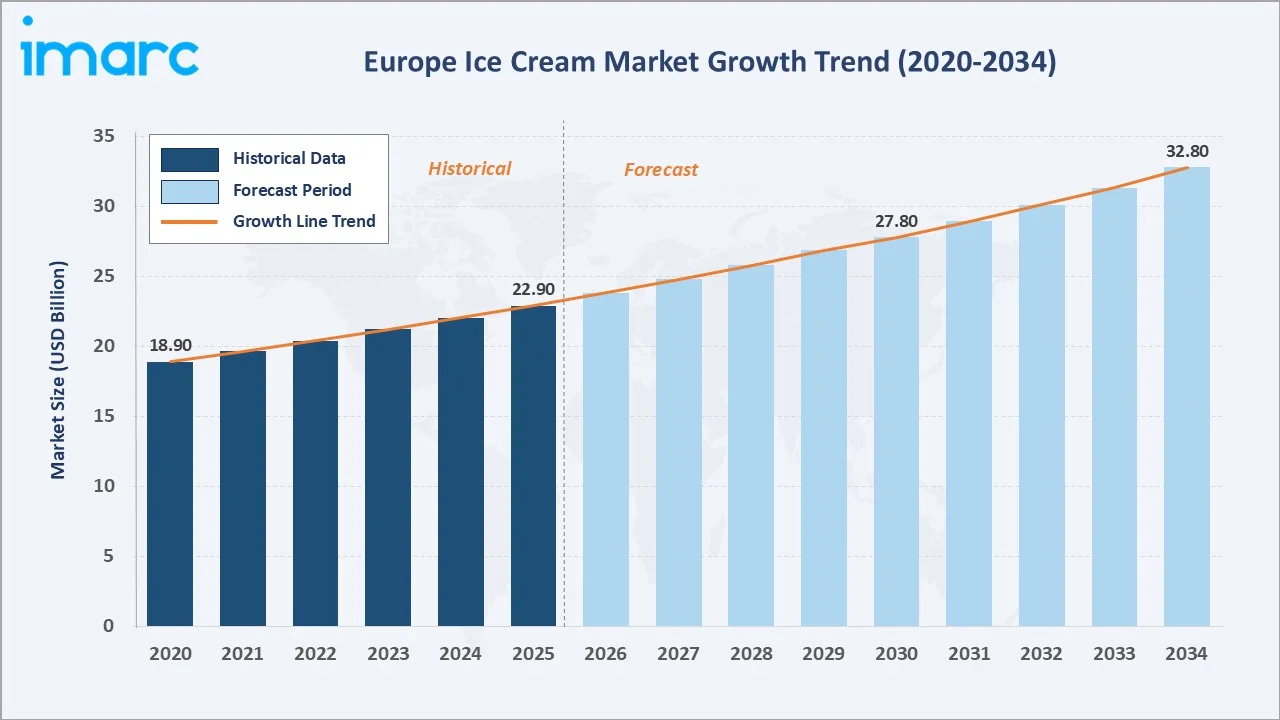

The Europe ice cream market size was valued at USD 22.9 Billion in 2025 and is projected to reach USD 32.8 Billion by 2034, exhibiting a CAGR of 3.94% during the forecast period 2026-2034. Rising consumer demand for premium and artisanal varieties, product innovation across flavor profiles, and expanding cold-chain infrastructure are driving ice cream market growth across the continent.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 22.9 Billion |

|

Forecast Market Size (2034) |

USD 32.8 Billion |

|

CAGR (2026-2034) |

3.94% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

Germany (24.0% share, 2025) |

|

Fastest Growing Country |

Spain (High Growth Momentum) |

|

Leading Flavor Segment |

Chocolate (36.0%, 2025) |

|

Leading Category Segment |

Impulse Ice Cream (45.0%, 2025) |

The following chart illustrates the Europe ice cream market growth trajectory from 2020 through 2034, contrasting historical expansion with a sustained forecast curve powered by premiumization, expanding distribution channels, and rising impulse buying behavior across European retail.

To get more information on this market, Request Sample

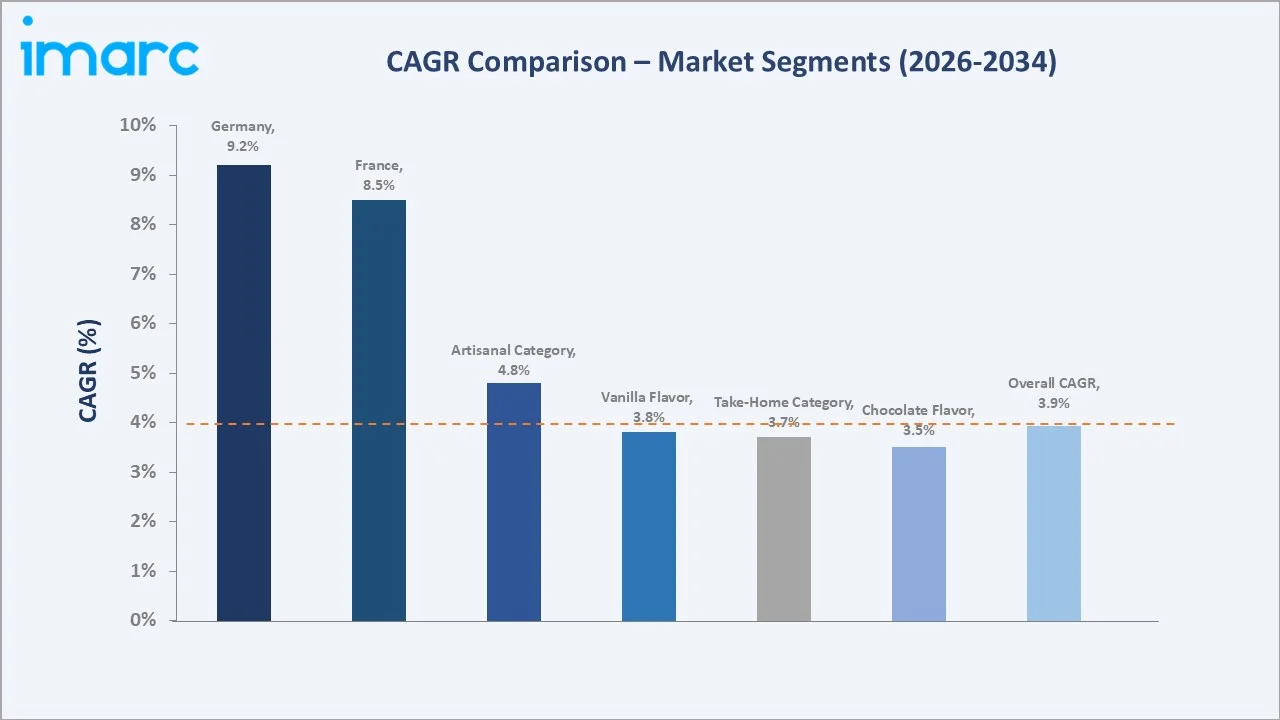

Segment-level CAGR comparisons highlight Artisanal Ice Cream and plant-based variants as the fastest-growing sub-categories, reflecting evolving consumer expectations for quality, authenticity, and health-conscious innovation within the Europe ice cream market forecast through 2034.

Executive Summary

The Europe ice cream market is experiencing steady value growth, driven by shifting consumer preferences toward premium, indulgent, and better-for-you frozen dessert products. Valued at USD 22.9 Billion in 2025, the market is forecast to reach USD 32.8 Billion by 2034 at a CAGR of 3.94%. Product innovation - spanning reduced-sugar formulations, plant-based alternatives, and artisanal single-origin offerings - is redefining category dynamics across both retail and foodservice channels.

Chocolate commands 36.0% of flavor-based demand in 2025, supported by its universal consumer appeal and its versatile application across impulse and take-home formats. Impulse Ice Cream leads the category segment at 45.0%, reflecting the seasonal and spontaneous purchase behavior that defines European summer consumption patterns. Artisanal Ice Cream, while holding a 15.0% share in 2025, is the most dynamically evolving segment, with consumers actively trading up to hand-crafted, locally-sourced, and premium-positioned products commanding 25-40% price premiums.

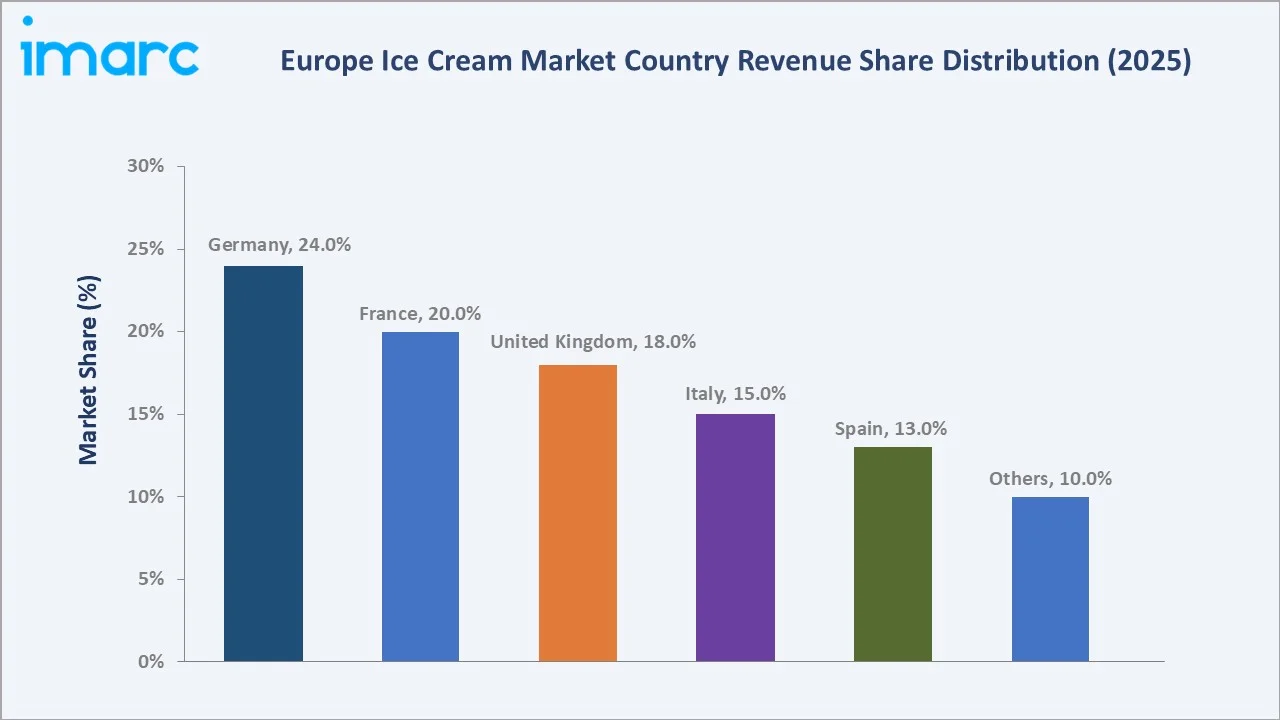

Germany leads European demand at 24.0% market share, followed by France at 20.0%, the United Kingdom at 18.0%, Italy at 15.0%, and Spain at 13.0%. The Europe ice cream market outlook remains constructive through 2034, as demographic shifts, premiumization trends, and expanding cold-chain infrastructure collectively support sustained volume and value growth.

Key Market Insights

|

Insight |

Data |

|

Largest Flavor |

Chocolate – 36.0% share (2025) |

|

Second Largest Flavor |

Vanilla – 28.0% share (2025) |

|

Largest Category |

Impulse Ice Cream – 45.0% share (2025) |

|

Fastest Growing Category |

Artisanal Ice Cream – ~4.8% CAGR Premium |

|

Leading Country |

Germany – 24.0% revenue share (2025) |

|

Top Companies |

Unilever, Froneri International Limited, Ferrero Group, Sammontana Italia S.p.A., Schwarz Group |

|

Biggest Opportunity |

Plant-based and low-sugar premium ice cream innovation |

Key Analytical Observations

- Chocolate's 36.0% dominance in 2025 reflects its enduring mass-market appeal across all age groups and its versatile application across bars, sticks, cones, and premium tubs throughout Germany, France, and the United Kingdom.

- Vanilla's 28.0% share is supported by its role as a base flavor in premium take-home multipack formats and its widespread use in artisanal and gelato-style premium positioning across Southern Europe.

- Impulse Ice Cream's 45.0% category leadership is underpinned by extensive distribution through convenience stores, petrol stations, and kiosks, especially during peak summer months across Western and Southern European markets.

- Artisanal Ice Cream's 15.0% share represents a high-value, fast-growing niche driven by consumer demand for authentic, locally-sourced products and willingness to pay premium prices in specialty retail and foodservice settings.

- Germany's 24.0% market share reflects its role as Europe's largest consumer market, supported by strong retail infrastructure, high disposable incomes, and well-established preference for diverse ice cream formats year-round.

- Spain and Italy are accelerating in premium gelato and artisanal segments, leveraging strong cultural affinity for craft ice cream and a growing tourist-driven foodservice demand base reaching nearly 900 million gelato servings annually in Italy alone.

Europe Ice Cream Market Overview

Ice cream is a frozen dairy dessert consumed in multiple forms - sticks, cones, tubs, bars, and sandwiches - and is produced across industrial, commercial, and artisanal settings. The European ice cream industry encompasses a diverse ecosystem spanning multinational manufacturers, regional producers, private-label brands, and independent artisanal makers, all serving distinct consumer segments across retail, foodservice, and direct-to-consumer channels.

The market intersects with macroeconomic trends including rising disposable incomes, tourism activity in Italy, France, and Spain, and expanding cold-chain logistics networks enabling year-round distribution. EU food labeling directives and allergen disclosure mandates are shaping reformulation strategies, while growing health consciousness is accelerating demand for low-sugar, dairy-free, and clean-label variants - fundamentally reshaping the Europe ice cream industry analysis landscape through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

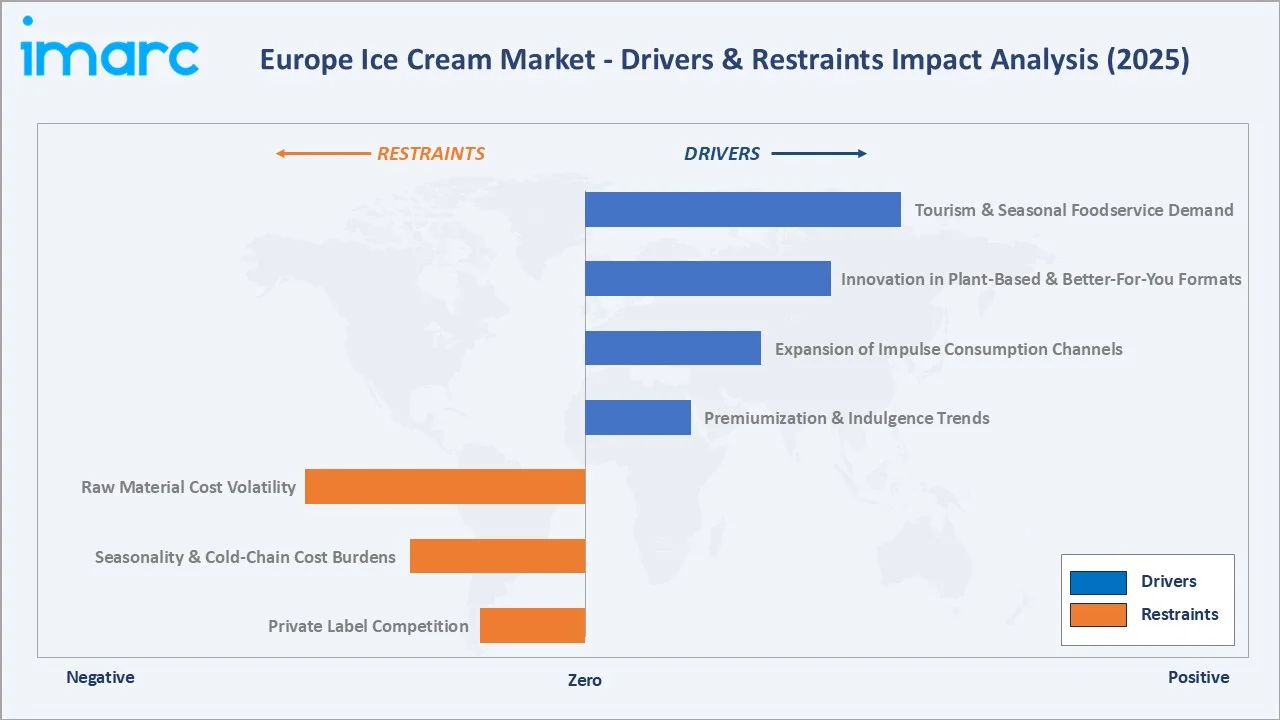

Market Drivers

- Premiumization and Indulgence Trends: European consumers are increasingly showing a strong inclination toward premium ice cream offerings. Market trends indicate a clear shift toward higher-value products, driven by growing demand for artisanal varieties, imported brands, and indulgent flavors such as single-origin chocolate, reflecting a broader preference for quality and differentiated experiences.

- Expansion of Impulse Consumption Channels: Convenience retail formats, forecourt outlets, and quick-service restaurants across Germany, the UK, and France are significantly supporting impulse-driven ice cream sales. The growing preference for on-the-go consumption is contributing to a substantial share of overall market revenue, highlighting the importance of accessible distribution channels in driving volume growth across Europe.

- Innovation in Plant-Based and Better-For-You Formats: Dairy-free ice cream launches in Europe are experiencing strong growth, supported by rising adoption of vegan lifestyles and increasing awareness of lactose intolerance. Plant-based alternatives such as oat milk, coconut cream, and almond-based formulations are expanding their presence across major supermarket chains, reflecting a broader shift toward inclusive and health-conscious product offerings.

- Tourism and Seasonal Foodservice Demand: Southern European markets - Spain, Italy, and France - benefit from significant tourist-driven foodservice ice cream consumption during summer months.

Market Restraints

- Raw Material Cost Volatility: Cocoa, dairy fat, and sugar price fluctuations - compounded by global supply chain disruptions since 2022 - are significantly pressuring gross margins for both multinational and regional ice cream manufacturers across Europe.

- Seasonality and Cold-Chain Cost Burdens: High dependence on summer demand creates revenue concentration risk, while maintaining cold-chain infrastructure year-round represents a substantial fixed-cost burden for manufacturers and distributors in Northern European markets.

- Private Label Competition: Retailer private-label ice cream products are increasingly gaining traction across price-sensitive consumer segments in the UK, Germany, and Spain. Their competitive pricing relative to branded offerings is strengthening their market presence, gradually putting pressure on branded manufacturers’ ability to maintain premium pricing and market share.

Market Opportunities

- Plant-Based and Vegan Ice Cream Innovation: The EU plant-based food market is expected to witness strong growth over the coming years, creating significant opportunities for ice cream manufacturers. Companies with advanced R&D capabilities that can deliver creamy, indulgent dairy-free products at affordable price points are well-positioned to capitalize on this expanding consumer base.

- Premiumization in Emerging European Markets: Eastern European markets - including Poland, Czech Republic, and Romania - are exhibiting accelerating ice cream per-capita consumption growth driven by rising middle-class incomes and expanding modern retail penetration.

- E-Commerce and Direct-to-Consumer Channels: Online ice cream delivery through platforms such as Gorillas, Getir, and Ocado continues to offer manufacturers direct engagement with premium consumers, enabling personalized product launches and subscription-based models.

Market Challenges

- Sustainability and Packaging Compliance: EU Single-Use Plastics Directive and Extended Producer Responsibility regulations are mandating material transitions in packaging, generating reformulation and capex requirements that disproportionately impact smaller regional producers.

- Health Labeling and Sugar Taxation Risk: Several European governments are implementing or considering sugar taxes on confectionery and ice cream products. France's Nutri-Score labeling system and the UK's sugar reduction program are creating competitive pressure for manufacturers with high-sugar legacy formulations.

Emerging Market Trends

1. Accelerating Plant-Based Ice Cream Adoption

Plant-based ice cream is transitioning from specialty health-food channels to mainstream retail across Western Europe. Oat milk-based varieties are gaining ground in the UK and Germany. Leading manufacturers including Unilever and Froneri International Limited have expanded their plant-based portfolios significantly since 2022, responding to a consumer base where over 9% of Europeans identify as flexitarian, vegan, or lactose-intolerant.

2. Premiumization and Artisanal Positioning

Artisanal and craft ice cream brands are achieving significant price premiums over mass-market alternatives across Italian gelato shops, French pâtisseries, and specialty dessert outlets in the UK. This segment represents a meaningful share of the European ice cream market and is expanding at a faster pace than the overall category, driven by strong consumer preference for experiential, high-quality frozen dessert occasions.

3. Functional and Better-For-You Formulations

High-protein, low-calorie, and probiotic ice cream products are expanding beyond niche positioning into mainstream grocery across Europe. European consumers increasingly demand indulgence without guilt, creating a high-growth subcategory that is attracting new entrants and reformulation investment from established players targeting health-conscious millennials and Gen Z consumers.

4. Sustainability-Led Packaging Innovation

Compostable cups, paper-based stick packaging, and refillable gelato tubs are gaining traction as the EU Single-Use Plastics Directive reshapes product presentation. Manufacturers investing in recyclable and biodegradable packaging are gaining retailer listing advantages, particularly in sustainability-driven markets such as the Netherlands, Denmark, and Sweden.

5. E-Commerce and On-Demand Delivery Expansion

Rapid grocery delivery platforms are expanding ice cream consumption beyond traditional seasonal, summer-driven impulse occasions into more consistent, year-round demand patterns. Online ice cream sales across Europe are showing steady growth, supported by urban consumers in major cities such as London, Paris, Berlin, and Amsterdam who are driving higher per-capita digital spending on frozen desserts.

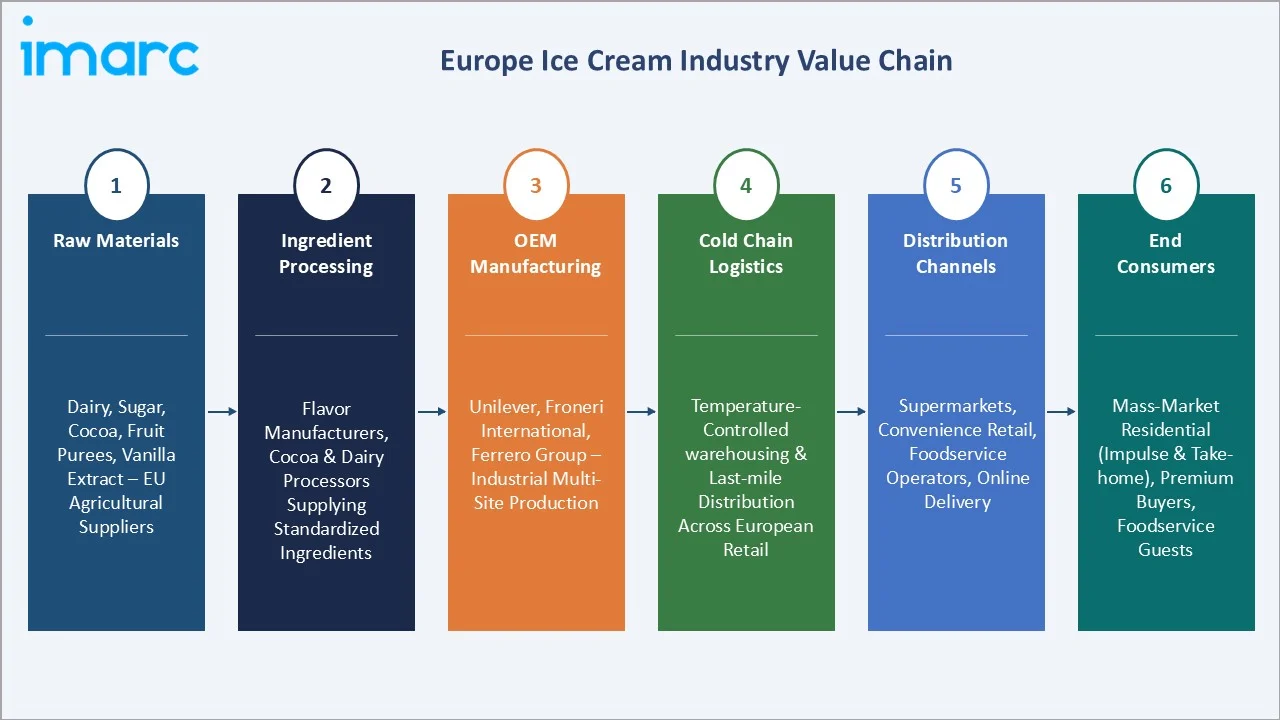

Industry Value Chain Analysis

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials |

Dairy (milk, cream, butter), sugar, cocoa, fruit purees, vanilla extract – sourced from EU agricultural suppliers |

|

Ingredient Processing |

Flavor manufacturers, cocoa processors, dairy processors supplying standardized ingredients to OEM manufacturers |

|

OEM Manufacturing |

Unilever, Froneri International Limited, Ferrero Group – industrial-scale multi-site European production; regional artisanal producers across Italy, France, Germany |

|

Cold Chain Logistics |

Temperature-controlled warehousing and last-mile distribution across European retail and foodservice networks |

|

Distribution Channels |

Supermarkets, convenience retail, foodservice operators, online delivery |

|

End Consumers |

Mass-market residential consumers (impulse & take-home), premium buyers (artisanal), foodservice guests (restaurants, gelaterie, cafés) |

The European ice cream industry value chain spans six integrated stages from raw material sourcing through end-consumer consumption. Each stage carries distinct competitive dynamics, margin profiles, and sustainability pressures relevant to a comprehensive Europe ice cream industry analysis.

OEM manufacturers hold the highest strategic value by integrating quality ingredients, cold-chain capabilities, and brand equity into turnkey offerings. Meanwhile, the emergence of online delivery platforms and direct-to-consumer gelato subscription services is reshaping distribution, enabling manufacturers to capture higher margins and strengthen brand relationships with premium consumers.

Technology Landscape in the Ice Cream Industry

Continuous Freezing and Extrusion Technology

Modern continuous freezer systems allow manufacturers to precisely control key quality parameters such as ice crystal size, overrun levels, and overall texture consistency. Leading equipment providers are advancing freezer technologies with intelligent, automated temperature regulation systems that enhance production efficiency, improve product uniformity across large-scale manufacturing, and contribute to reduced energy usage while maintaining high-quality output standards.

Plant-Based Formulation Technology

Achieving creamy, melt-resistant textures in dairy-free ice cream requires advanced emulsification and hydrocolloid technology. Enzyme-modified oat and pea proteins are enabling superior mouthfeel replication. Several European startups are leveraging precision fermentation to produce animal-free proteins that replicate dairy ice cream texture with clean-label ingredient declarations.

Smart Packaging and Cold-Chain Monitoring

IoT-enabled temperature monitoring systems embedded in packaging are enabling real-time visibility across the cold-chain, from production facilities to final consumer delivery. Recent pilots of smart packaging solutions in the UK have demonstrated the ability to track temperature deviations and communicate product freshness status, helping reduce waste throughout the distribution network and improve overall supply chain efficiency.

Sustainable Production Innovation

Heat recovery systems, solar-powered cold storage, and CO₂-based natural refrigerants are replacing HFC systems across European ice cream manufacturing facilities, driven by the EU F-Gas Regulation phase-down schedule. Blockchain-based traceability systems are being implemented to verify sustainably-sourced cocoa and dairy inputs, meeting emerging ESG disclosure requirements for branded manufacturers.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Flavor |

Chocolate |

36.0% |

2025 |

|

Category |

Impulse Ice Cream |

45.0% |

2025 |

|

Product |

🔒 |

🔒 |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Country |

Germany |

24.0% |

2025 |

By Flavor

To access detailed market analysis, Request Sample

Chocolate leads the European ice cream flavor segment with a 36.0% share in 2025, underpinned by its universal consumer appeal and versatile application across bars, sticks, cones, and premium tubs. Demand is particularly concentrated in Germany, the UK, and France - markets where premium dark chocolate and single-origin cocoa-based offerings are achieving consistent volume and value growth.

By Category

Impulse Ice Cream leads the category segment at 45.0% of Europe market revenue in 2025. This segment encompasses individually-portioned formats - bars, cones, sticks, and sandwiches - sold through convenience channels and consumed immediately at point of purchase. Seasonal summer demand across Mediterranean and Central European markets drives sustained volume concentration in this category.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

Germany |

24.0% |

Largest European consumer market; strong retail infrastructure; high per-capita income; year-round take-home demand |

|

France |

20.0% |

Premium artisanal positioning; foodservice gelato demand; strong private-label penetration in supermarkets |

|

United Kingdom |

18.0% |

Plant-based innovation leadership; e-commerce delivery growth; strong impulse channel via convenience retail |

|

Italy |

15.0% |

Artisanal gelato culture; tourism-driven foodservice; strong ingredient quality heritage; craft producer ecosystem |

|

Spain |

13.0% |

Mediterranean impulse consumption; tourism-driven summer demand; growing modern retail penetration |

|

Others |

10.0% |

Eastern European modernization; rising middle class; expanding cold-chain and retail infrastructure |

Germany commands 24.0% of European ice cream revenue in 2025, supported by its role as the continent's largest consumer market with a well-established retail infrastructure spanning discounters (ALDI, Lidl), supermarkets (REWE, EDEKA), and convenience formats. Year-round take-home consumption and growing premium market penetration sustain Germany's market leadership.

Competitive Landscape

|

Company Name |

Key Brand(s) |

Market Position |

Core Strength |

|

Unilever |

Magnum, Ben & Jerry's, Cornetto, Wall's |

Leader |

Portfolio breadth, distribution scale, brand equity across impulse and take-home |

|

Froneri International Limited |

Connoisseur, Drumstick, Extrême, Häagen-Dazs, Mövenpick, Nuii, and Outshine |

Leader |

Pan-European manufacturing, private-label scale, JV efficiency |

|

Ferrero Group |

Rocher ice cream, Raffaello |

Challenger |

Premium confectionery-to-ice-cream brand extension, gifting segment |

|

Sammontana Italia S.p.A. |

Sammontana |

Emerging |

Italian artisanal heritage, gelato sector leadership in Italy |

|

Schwarz Group |

Lidl (Gelatelli) |

Challenger |

Price-value leadership in German and pan-European discount channels |

The European ice cream market's competitive landscape is moderately concentrated at the premium branded tier, with Unilever, and Froneri International Limited commanding significant combined market share. However, the overall market remains fragmented at the regional level, with hundreds of artisanal producers, regional dairy cooperatives, and private-label manufacturers competing across distinct price and positioning tiers.

Key Company Profiles

Unilever

Unilever is the global leader in ice cream, operating under its dedicated Ice Cream division. The company's European portfolio spans impulse, take-home, and foodservice channels across more than 30 countries. Its brands Magnum, Ben & Jerry's, and Cornetto are among the most recognized ice cream names globally.

- Product & Brand Portfolio: Unilever's European ice cream portfolio includes Magnum (premium chocolate-coated bars), Ben & Jerry's (premium chunk-style take-home), Cornetto (impulse cones), Carte d'Or (take-home tubs), Langnese (Germany), Wall's (UK), and Frigo (Spain), plus a growing plant-based range.

- Recent Developments: In 2025, Unilever introduced its 2025 ice cream product lineup, expanding across major brands such as Magnum, Breyers, Talenti, Popsicle, Klondike, and Good Humor. The new range features innovative flavours and formats, including bakery-inspired gelato layers, s’mores-themed treats, non-dairy oat milk-based variants, and character-led frozen novelties.

- Strategic Focus: Unilever's ice cream strategy centers on premiumization through Magnum and Ben & Jerry's brands, acceleration of plant-based ice cream across European retail, and operational efficiency through the planned ice cream business separation.

Froneri International Limited

Froneri International Limited is a dedicated global ice cream company formed in 2016 as a joint venture between Nestlé and R&R Ice Cream. Operationally based in the UK, Froneri is one of the largest ice cream manufacturers in Europe by volume, with a broad portfolio spanning branded, licensed, and private-label products.

- Product & Brand Portfolio: Froneri's European portfolio includes Connoisseur, Drumstick, Extrême, Häagen-Dazs, Mövenpick, Nuii, and Outshine, and extensive contract manufacturing capability serving European retail chains.

- Recent Developments: In 2025, Froneri International Limited has entered into agreements to acquire the European ice cream business of Food Union. The deal covers multiple Northern and Eastern European markets, including Denmark, Norway, Estonia, Latvia, Lithuania, and Romania, and is expected to strengthen Froneri’s regional footprint and portfolio of locally popular brands. The transaction is subject to regulatory approvals and will be completed in the coming months.

- Strategic Focus: Froneri International Limited’s strategy combines scale-based efficiency in private-label and licensed brand production with selective premiumization through Italian artisanal heritage brands, positioning the company to serve both value-conscious and premium European consumer segments.

Ferrero Group

Ferrero Group is a privately owned Italian multinational confectionery company headquartered in Alba, Italy. Ferrero is one of the world’s largest sweet-packaged food companies, with a strong global presence across chocolates, confectionery, and an expanding ice cream category.

- Product & Brand Portfolio: Ferrero Group’s core portfolio includes globally recognized brands such as Rocher ice cream, and Raffaello.

- Recent Developments: In 2026, Ferrero Group’s is accelerating its European ice cream strategy by transforming its Ice Cream Factory Comaker (ICFC) plant in Alzira, Spain into a dedicated European ice cream technology hub. The company is investing heavily to modernize the facility, expand production capacity, and introduce advanced manufacturing technologies while phasing out private-label production by 2026.

- Strategic Focus: Ferrero Group’s strategy centers on premiumization, brand-led expansion, and category diversification beyond confectionery into ice cream and better-for-you indulgence segments. The company is leveraging its strong brand equity (especially Kinder and Nutella) to drive growth in frozen desserts, supported by investments in manufacturing modernization and European production consolidation.

Market Concentration Analysis

The European ice cream market exhibits moderate concentration at the premium branded tier, with the top three players - Unilever, Froneri International Limited, Ferrero Group - collectively estimated to account for approximately 45-55% of European branded ice cream revenue in 2025. However, when private-label, artisanal, and regional producers are included, the overall market demonstrates meaningful fragmentation, particularly across Southern and Eastern Europe.

The market is experiencing a bifurcated consolidation dynamic. At the premium OEM tier, Nestlé's joint venture with Froneri signals a structural reorganization aimed at increasing strategic focus and capital efficiency. Simultaneously, the artisanal segment is highly fragmented.

Investment & Growth Opportunities

Fastest-Growing Segments

Artisanal Ice Cream, holding 15.0% of the 2025 European market, is the fastest-growing value segment commanding 25-40% price premiums and attracting investment from specialty food investors and premium F&B brands. Plant-based ice cream is estimated to be growing at 8-12% annually across Europe, representing the highest-growth innovation opportunity for manufacturers with dairy-free formulation capabilities.

Emerging Market Expansion

Eastern European markets including Poland, Czech Republic, and Romania are demonstrating above-average ice cream consumption growth rates, supported by expanding modern retail infrastructure and rising middle-class incomes, presenting attractive white-space opportunities for both premium international brands and regional dairy cooperatives.

Venture and Strategic Investment Trends

The European ice cream sector is attracting strategic investment in three primary areas: (1) sustainable packaging technology and biodegradable material innovation to meet EU regulatory mandates; (2) plant-based and precision-fermentation ingredient platforms enabling dairy-free ice cream with superior texture; and (3) cold-chain logistics technology including IoT-enabled temperature monitoring and last-mile frozen delivery infrastructure supporting e-commerce growth.

Future Market Outlook (2026-2034)

The Europe ice cream market forecast projects sustained value expansion from USD 22.9 Billion in 2025 to USD 32.8 Billion by 2034 at a CAGR of 3.94%. Germany will retain regional leadership while France and the UK drive premium category growth. Southern European markets - Italy and Spain - will sustain impulse volume through tourism and Mediterranean lifestyle drivers.

Technological disruptions shaping the market include precision fermentation-derived dairy-free proteins enabling superior plant-based ice cream textures, AI-driven flavor development accelerating limited-edition product cycles, and smart cold-chain logistics reducing distribution waste while enabling economically viable e-commerce ice cream delivery across dense urban markets.

The industry's structural transformation over 2026-2034 will be characterized by three concurrent dynamics: premiumization of the top-tier driving disproportionate value growth relative to volume; private-label pressure compressing mid-market branded margins and accelerating category polarization; and artisanal and craft ice cream expansion redefining quality benchmarks and consumer expectations across Western European markets.

Research Methodology

Primary Research

IMARC Group's primary research program for the Europe ice cream market involved in-depth interviews and consultations with over 50 industry stakeholders including ice cream manufacturers, cold-chain logistics providers, retail category managers, foodservice operators, ingredient suppliers, and independent market specialists. Primary insights were used to validate quantitative estimates, identify emerging trends, and assess competitive dynamics.

Secondary Research

Secondary research encompassed analysis of published industry reports, regulatory filings, company annual reports, trade association data from EUROGLACES (European Ice Cream Association), Euromonitor International, Statista, Nielsen retail panel data, and European Commission food industry statistics. Historical market data covering 2020-2025 was triangulated across multiple sources to ensure accuracy.

Forecasting Models

Market forecasts for 2026-2034 were developed using a combination of bottom-up and top-down approaches. Bottom-up models aggregate segment-level demand estimates across flavor, category, and regional dimensions. Statistical regression models incorporating historical CAGR patterns were applied to derive the 3.94% CAGR projection for the forecast period 2026-2034.

Europe Ice Cream Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Flavors Covered | Chocolate, Fruit, Vanilla, Others |

| Categories Covered | Impulse Ice Cream, Take-Home Ice Cream, Artisanal Ice Cream |

| Products Covered | Cup, Stick, Cone, Brick, Tub, Others |

| Distribution Channels Covered | Supermarkets/Hypermarkets, Convenience Stores, Online Stores, Others |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | Unilever, Froneri International Limited, Ferrero Group, Sammontana Italia S.p.A., Schwarz Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe ice cream market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Europe ice cream market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe ice cream industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe Ice Cream Market Report

The Europe ice cream market was valued at USD 22.9 Billion in 2025, supported by strong impulse consumption and premium take-home demand across Germany, France, and the United Kingdom.

The market is projected to reach USD 32.8 Billion by 2034, growing at a CAGR of 3.94% during 2026-2034, driven by premiumization, artisanal growth, and plant-based innovation.

The Europe ice cream market is expected to grow at a CAGR of 3.94% from 2026 to 2034, reflecting steady demand growth across impulse, take-home, and artisanal ice cream categories.

Chocolate is the leading flavor, commanding 36.0% of European ice cream market revenue in 2025, followed by Vanilla at 28.0% and Fruit at 22.0%.

Impulse Ice Cream is the largest category, accounting for 45.0% of Europe's ice cream market in 2025, driven by convenience retail penetration and seasonal summer consumption patterns.

Germany holds the largest country share at 24.0% of the European ice cream market in 2025, followed by France at 20.0% and the United Kingdom at 18.0%.

Key players include Unilever, Froneri International Limited, Ferrero Group, Sammontana Italia S.p.A., and Schwarz Group.

Primary growth drivers include premiumization trends, plant-based innovation, expanding e-commerce delivery channels, tourism-driven foodservice demand in Southern Europe, and artisanal ice cream consumption growth.

Key emerging trends include plant-based and vegan ice cream adoption, functional formulations (high-protein, low-calorie), sustainable packaging innovation, and direct-to-consumer artisanal gelato delivery services.

Major challenges include raw material cost volatility (cocoa, dairy, sugar), private-label competition compressing branded margins, EU sustainability packaging regulations, and sugar tax risks in key European markets.

Artisanal ice cream holds 15.0% of the European market in 2025, commanding 25-40% price premiums over mass-market products and growing faster than the overall market, especially in Italy, France, and the UK.

The full IMARC Group report covering Europe ice cream market size, share, trends, and country-level forecasts through 2034 is available via the IMARC Group website at www.imarcgroup.com or by contacting the research team.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade