Europe Nickel Market Size, Share, Trends and Forecast by Product Type, Application, End-Use Industry, and Country, 2026-2034

Europe Nickel Market Size and Share:

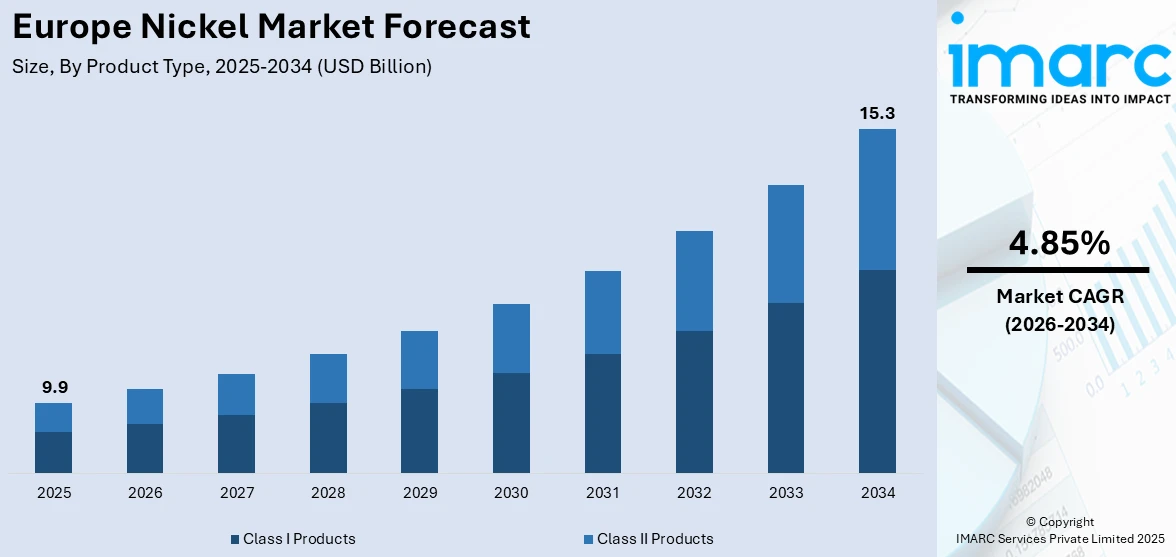

The Europe nickel market size was valued at USD 9.9 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 15.3 Billion by 2034, exhibiting a CAGR of 4.85% from 2026-2034. The market is witnessing significant growth due to the escalating demand for electric vehicles and rising stainless steel production. Additionally, increasing focus on sustainable mining practices, surging demand for high-grade nickel in battery applications, and technological advancements in nickel processing are favoring market expansion.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 9.9 Billion |

|

Market Forecast in 2034

|

USD 15.3 Billion |

| Market Growth Rate (2026-2034) | 4.85% |

The rapid adoption of electric vehicles (EVs) in Europe is significantly driving the nickel market. For instance, in 2024, Tesla Model Y remained Europe’s top-selling EV, with 11,236 units sold across major markets, including the UK, France, Germany, and the Netherlands. This rising popularity is driving a significant increase in the demand for nickel, a vital component in EV battery production. Nickel is vital in the production of lithium-ion batteries, particularly in high-energy-density cathode materials. With Europe striving to achieve ambitious carbon neutrality goals, governments are offering substantial incentives to promote EV adoption. This trend is further supported by stringent emissions regulations, compelling automakers to transition toward electric mobility. As Europe scales up EV production to meet growing consumer and regulatory demands, the region is also investing in refining and processing facilities to secure a stable supply of battery-grade nickel.

To get more information on this market Request Sample

Europe’s stainless-steel industry remains a key consumer of nickel, driving market growth. Nickel enhances stainless steel’s corrosion resistance, durability, and strength, making it essential for various industrial applications, including construction, automotive, and aerospace. For instance, in 2024, Europe's stainless steel producers relied on cheaper Indonesian nickel pig iron (NPI) imports, totaling 10,000 tons, due to high raw material costs and limited stainless steel scrap availability. This strategic use of NPI as a cost-effective alternative to higher-grade nickel ensures a reliable supply of alloying materials, enabling manufacturers to maintain operational efficiency. By addressing resource constraints through this approach, the industry sustains rising production levels, catering to increasing demand while staying competitive in global markets.

Europe Nickel Market Trends:

Increasing Focus on Sustainable Mining Practices

Sustainability is becoming a critical focus in the Europe nickel market as environmental regulations tighten and stakeholders prioritize eco-friendly practices. Companies are adopting greener mining technologies and processes, including the use of renewable energy in operations and advanced waste management systems. For instance, in 2024, VELUX Group signed a 10-year deal with ArcelorMittal to use low-carbon XCarb steel in roof window components, replacing conventional steel by 2025 to enhance sustainability efforts. In addition, recycling initiatives are gaining prominence, with a rising emphasis on recovering nickel from end-of-life batteries and stainless steel scrap. These efforts align with Europe’s broader goals of promoting a circular economy and reducing the environmental footprint of industrial activities, enhancing the appeal of sustainably sourced nickel for industries like electric vehicles and construction.

Surging Demand for High-Grade Nickel in Battery Applications

The rapid transformation towards electric mobility is causing a surge in the demand for high-grade nickel which is mainly used in lithium-ion battery production. Nickel-rich chemistry controllers, among them NMC and NCA, are now being progressively used by manufacturers of batteries for the purpose of energy density and prolonging battery life. Europe's goal of localizing battery production by means of the European Battery Alliance and others has led to an increase in demand for nickel of high purity levels. For example, in 2024, France helped KL1's plan to build a nickel and cobalt refinery near Bordeaux. Furthermore, in 2028, it intends to allocate 20-30% of its EV battery needs by 2030. The advantages gained from this are investments in the refining sectors, as well as partnerships across the value chain, that assure a stable supply of high-quality nickel.

Technological Advancements in Nickel Processing

Technological innovations are reshaping nickel extraction and processing in Europe. Companies are leveraging advanced hydrometallurgical and pyrometallurgical techniques to enhance efficiency and reduce operational costs. For instance, in 2024, Mercedes-Benz opened Germany’s first solar-powered battery recycling plant, using hydrometallurgical methods to recover 96% of cobalt, nickel, and lithium from EV batteries, with an annual capacity of 2,500 tonnes. In addition, the adoption of digital solutions, including AI and IoT, enables real-time monitoring of mining operations, optimizing resource utilization, and minimizing waste. These advancements are helping the industry address challenges related to ore grade depletion and environmental compliance, positioning Europe as a leader in sustainable and efficient nickel production. Such innovations also support the region's ambitions to meet the growing demand for nickel in critical applications while maintaining global competitiveness.

.webp)

Europe Nickel Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the Europe nickel market, along with forecasts at the regional and country levels from 2026-2034. The market has been categorized based on product type, application, and end-use industry.

Analysis by Product Type:

- Class I Products

- Class II Products

Class I products, including high-purity nickel, are essential for the Europe nickel market, particularly for battery production in electric vehicles and high-performance alloys in aerospace and industrial applications. Their superior purity and quality make them indispensable for advanced technologies, aligning with Europe’s sustainability goals and increasing demand for high-grade nickel solutions.

Class II products, such as ferronickel and nickel pig iron, primarily cater to the Europe nickel market in the production of stainless steel. These products are cost-effective solutions for industries requiring materials that are durable and resistant to corrosion. Their widespread use in construction, automotive, and industrial sectors supports infrastructure development and industrial growth across the European region.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

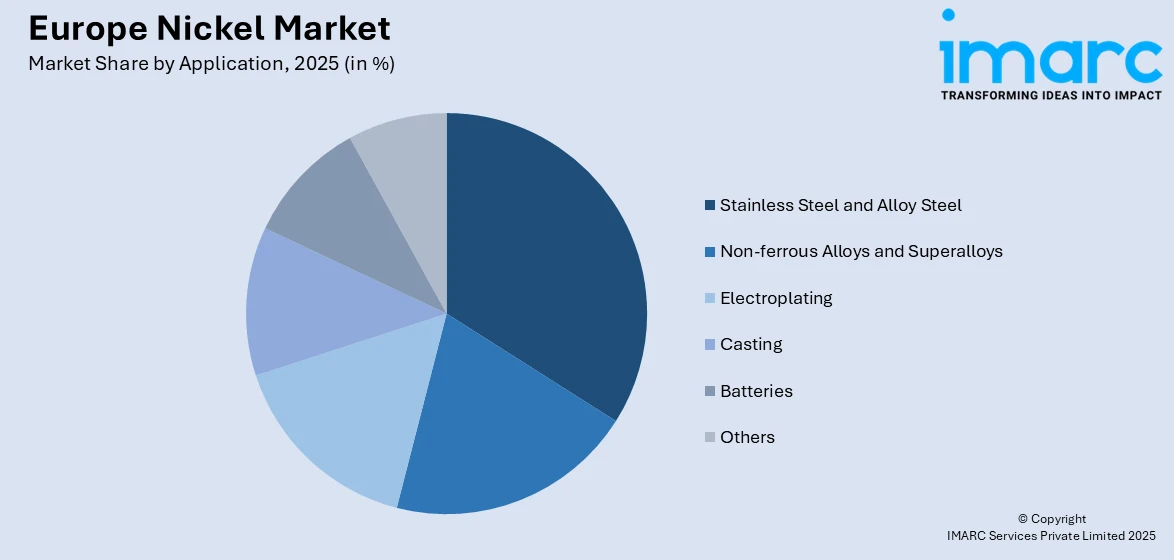

- Stainless Steel and Alloy Steel

- Non-ferrous Alloys and Superalloys

- Electroplating

- Casting

- Batteries

- Others

Stainless steel and alloy steel, the most important applications for the Europe nickel market, use nickel to improve strength, corrosion resistance, and wear resistance. These materials are vital for the construction, automotive, and industrial sectors, all of which support infrastructure development and advanced manufacturing. Nickel properties ensure reliability and performance in critical European industries.

Non-ferrous alloys and superalloys, critical applications in the Europe nickel market, use nickel to provide high strength, heat resistance, and corrosion protection. These materials are indispensable to aerospace, power generation, and advanced engineering sectors where they enable high-performance components that drive innovation in industries requiring superior durability and operational reliability.

Electroplating is one of the primary applications in the Europe nickel market, as it offers a protective and decorative coating on metals to enhance durability, corrosion resistance, and aesthetic appeal. This process is widely adopted across automotive, electronics, and industrial sectors, supporting product longevity and aligning with Europe's focus on quality manufacturing standards.

Casting is a significant application in the Europe nickel market, using nickel to create intricate and durable parts through molten metal shaping. It is critical for manufacturing in the automotive, aerospace, and industrial machinery industries, providing high-performance, corrosion-resistant parts that meet Europe's strict standards for quality and reliability.

Batteries are the most essential application in the Europe Nickel market. Nickel in lithium ion battery cathodes adds energy density, durability, and performance-very important for an expanding EV market and renewable energy storage applications, which supports the transformation of Europe toward sustainable power systems.

Analysis by End-Use Industry:

- Transportation & Defense

- Fabricated Metal Products

- Electrical & Electronics

- Chemical

- Petrochemical

- Construction

- Consumer Durables

- Industrial Machinery

- Others

Transportation and defense, two major end-use industries in the Europe nickel market, require nickel for its strength, corrosion resistance, and heat tolerance. It is important in aircraft manufacture, military vehicle production, and advanced transportation systems; durability, performance, and innovation are required in sectors that are critical to Europe's infrastructure and national security.

Fabricated metal products, an essential end-use sector in the Europe nickel market, utilize nickel for its hardening and corrosion, and resistance with aesthetic value in metallic elements in their manufacture. Diverse industries that find applications for these fabricated metals range from construction to automotive to machine-related equipment industries.

The electrical and electronics sector constitutes one of the most significant downstream sectors in the Europe nickel market, utilizing nickel mainly for its conductivity, strength, as well as resistance to corrosion. Nickel is an elemental part of producing components like batteries and connectors and plating. These have supported technological trends as well as rising local demand for high-performance electronics.

The chemical industry in the Europe nickel market consumes nickel as a catalyst in hydrogenation and to produce specialty chemicals. Thus, its performance ensures adequate efficiency and reliability in application, and as such there is a consequent demand for nickel to service the manufacture of advanced chemical products across Europe.

The petrochemical industry is a critical end-use segment in the Europe nickel market, relying on nickel for its role in catalysts and corrosion-resistant alloys. Nickel enables efficient processing of hydrocarbons and production of petrochemical derivatives, supporting operational durability and aligning with Europe's stringent industrial performance and environmental standards.

The construction industry, a significant end-use sector in the Europe nickel market, uses nickel for strength, corrosion resistance, and aesthetic applications in stainless steel and alloy uses. Nickel supports sustainable and long-lasting infrastructure development to satisfy the demand for high-quality materials in modern architectural and structural projects across Europe.

The consumer durables sector is one of the major end-use industries in the Europe nickel market. Nickel is used in appliances and household goods for its durability, corrosion resistance, and aesthetic appeal. Nickel improves the performance and life of products like kitchenware and electronics, which consumers want to be of high quality and reliable.

The industrial machinery sector, a major end-use application in the Europe nickel market, uses nickel for strength, heat resistance, and protection against corrosion. Nickel plays a critical role in producing long-lasting parts for heavy machinery, improving performance, reliability, and operational efficiency, which are highly important to Europe's advanced industrial and manufacturing activities.

Country Analysis:

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

Germany is an important center for advanced manufacturing, automotive production, and renewable energy technologies in Europe. The country's focus on sustainable industrial practices and strong demand for stainless steel and nickel-based alloys drive innovation, production, and consumption within the regional nickel market.

France is a significant contributor to the nickel market in Europe through its advanced aerospace and defense industries, which use nickel-based superalloys for high-performance components. The country's focus on sustainable construction and renewable energy technologies also creates demand for nickel in stainless steel and battery applications, driving market growth and innovation.

The United Kingdom contributes to the Europe nickel market through its strong aerospace, automotive, and renewable energy sectors. Nickel is integral to the production of high-performance superalloys and electric vehicle batteries. Moreover, the UK’s focus on sustainable industrial practices and advanced manufacturing bolsters regional demand for nickel-based materials and technologies.

Italy provides nickel to the European market by offering a strong base in stainless steel and industrial machinery sectors. Nickel is used due to its strength and corrosion resistance. Its thriving manufacturing and construction sectors boost the demand for nickel-based alloys, while the country's emphasis on quality production further promotes growth and innovation in the regional market.

Spain also contributes to the Europe nickel market as construction, automotive, and renewable energy sectors are growing, with increasing utilization of nickel for its strength, corrosion resistance, and efficiency in energy storage. The focus on sustainability and advanced manufacturing processes in Spain's industry continues to drive demand for nickel-based materials, supporting regional market growth.

Competitive Landscape:

The European nickel market represents a case in point of tough competition where existing players, such as historical big ones, are striving to make more strategic expansions and also show their technological excellence. These companies are exploring the use of the latest extraction and refining techniques to boost operational efficiency over the implementation of environmental regulations enforced by the authorities. On account of business combinations and takeovers, firms can reshape their supply chains and consequently, they are able to build efficient energy storage units and stainless steel production facilities. For instance, in 2024, ArcelorMittal announced a €1.8 billion investment, supported by the French government, to decarbonize its Dunkirk site, aiming to cut France's industrial CO2 emissions by nearly 6%. As nickel is a critical component in the production of stainless steel, the move to decarbonize is expected to drive increased demand for sustainably sourced nickel.

The report provides a comprehensive analysis of the competitive landscape in the Europe nickel market with detailed profiles of all major companies.

Latest News and Developments:

- In July 2024, RecycLiCo Battery Materials Inc., a leader in sustainable lithium-ion battery recycling, secured its 16th global patent with the grant of a European Unitary Patent for its hydrometallurgical recycling process. This advanced technology recovers up to 99% of lithium, cobalt, nickel, and manganese from battery waste, converting them into battery-grade materials like lithium hydroxide and carbonate.

Europe Nickel Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Class I Products, Class II Products |

| Applications Covered | Stainless Steel and Alloy Steel, Non-ferrous Alloys and Superalloys, Electroplating, Casting, Batteries, Others |

| End Use Industries Covered | Transportation & Defense, Fabricated Metal Products, Electrical & Electronics, Chemical, Petrochemical, Construction, Consumer Durables, Industrial Machinery, Others |

| Countries Covered | Germany, France, the United Kingdom, Italy, Spain, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe nickel market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Europe nickel market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe nickel industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe Nickel Market Report

The nickel market in Europe was valued at USD 9.9 Billion in 2025.

The market is primarily driven by the growing demand for electric vehicle (EV) battery technology, increased stainless steel production, ongoing developments of decarbonizing technologies, escalating industrial sustainability and infrastructural development receiving more attention, which is giving the metal a considerable head starts in the key sectors of construction, automotive, and aerospace.

The nickel market in Europe is projected to exhibit a CAGR of 4.85% during 2026-2034, reaching a value of USD 15.3 Billion by 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)