Europe Recycled Plastics Market Size, Share, Trends and Forecast by Source, Application, Plastic Type, and Country, 2026-2034

Europe Recycled Plastics Market Size, Share, Trends & Forecast (2026-2034)

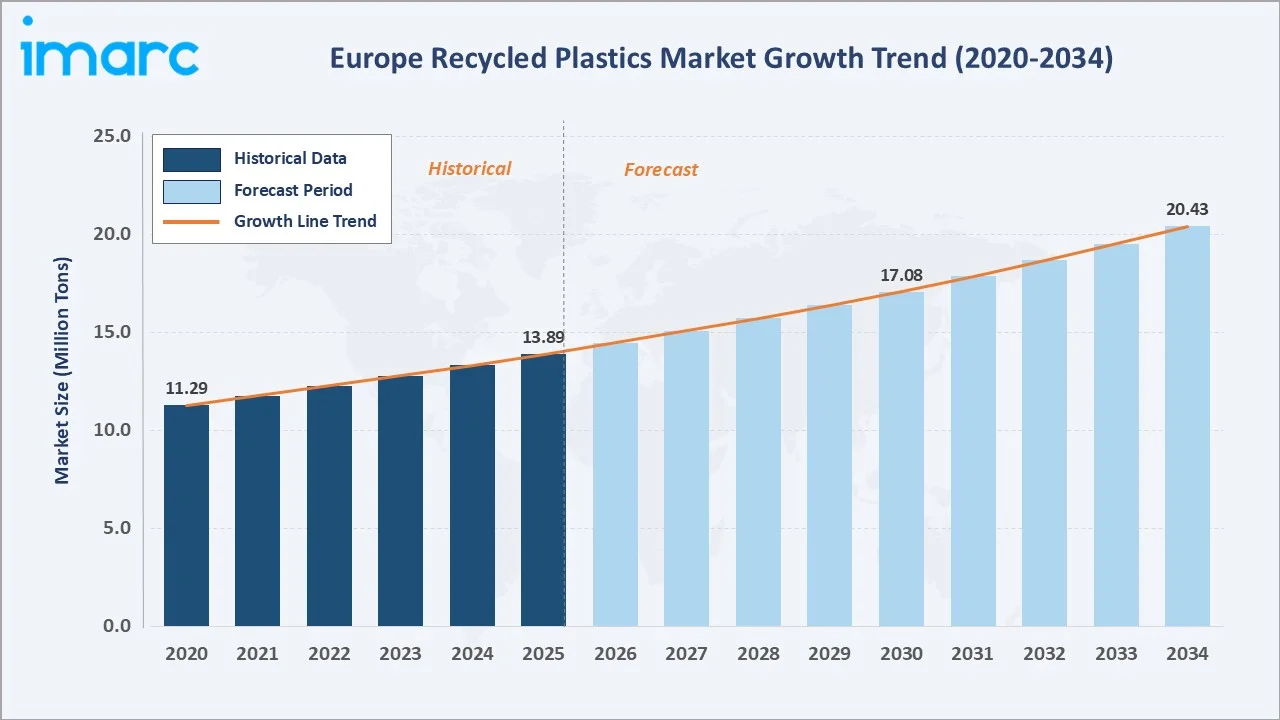

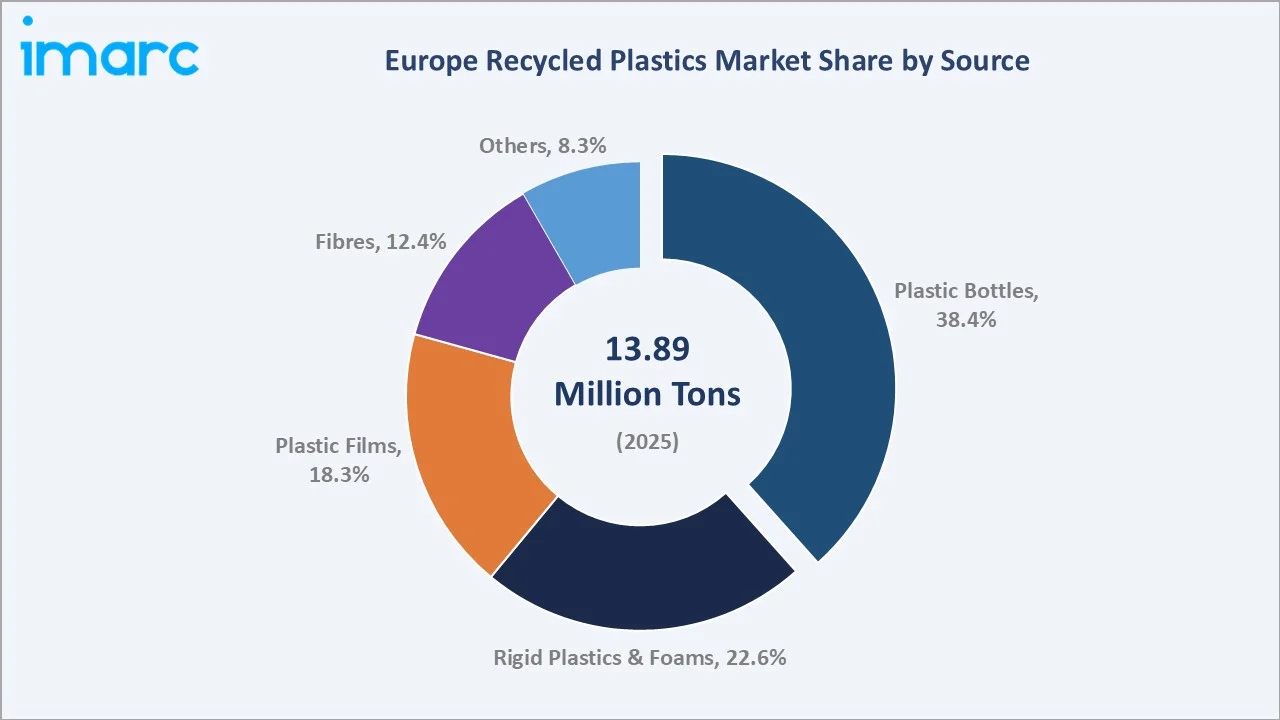

The Europe recycled plastics market size was valued at 13.89 Million Tons in 2025 and is projected to reach 20.43 Million Tons by 2034, exhibiting a CAGR of 4.22% during the forecast period 2026-2034. Strengthening EU circular economy legislation, escalating Extended Producer Responsibility (EPR) mandates, surging corporate sustainability commitments, and rapidly scaling mechanical and chemical recycling technologies are powering the market's steady expansion. Plastic Bottles dominate the source segment at a 38.4% share in 2025, while PET leads the plastic type breakdown at 34.2%. Germany commands the largest country share at 22.5%, underpinned by the region's mature collection infrastructure and the world-renowned Pfund deposit-return system, achieving 98% PET bottle collection.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

13.89 Million Tons |

|

Forecast Market Size (2034) |

20.43 Million Tons |

|

CAGR (2026-2034) |

4.22% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

Germany (22.5% share, 2025) |

|

Fastest Growing Country |

United Kingdom (CAGR ~5.0%) |

|

Leading Source Segment |

Plastic Bottles (38.4%, 2025) |

|

Leading Plastic Type |

PET (34.2%, 2025) |

The Europe recycled plastics market growth trajectory from 2020 through 2034 contrasts a consistent historical expansion base against a sustained forecast curve powered by PPWR compliance timelines, national plastics tax adoption, and closed-loop packaging investments from leading FMCG brands.

To get more information on this market, Request Sample

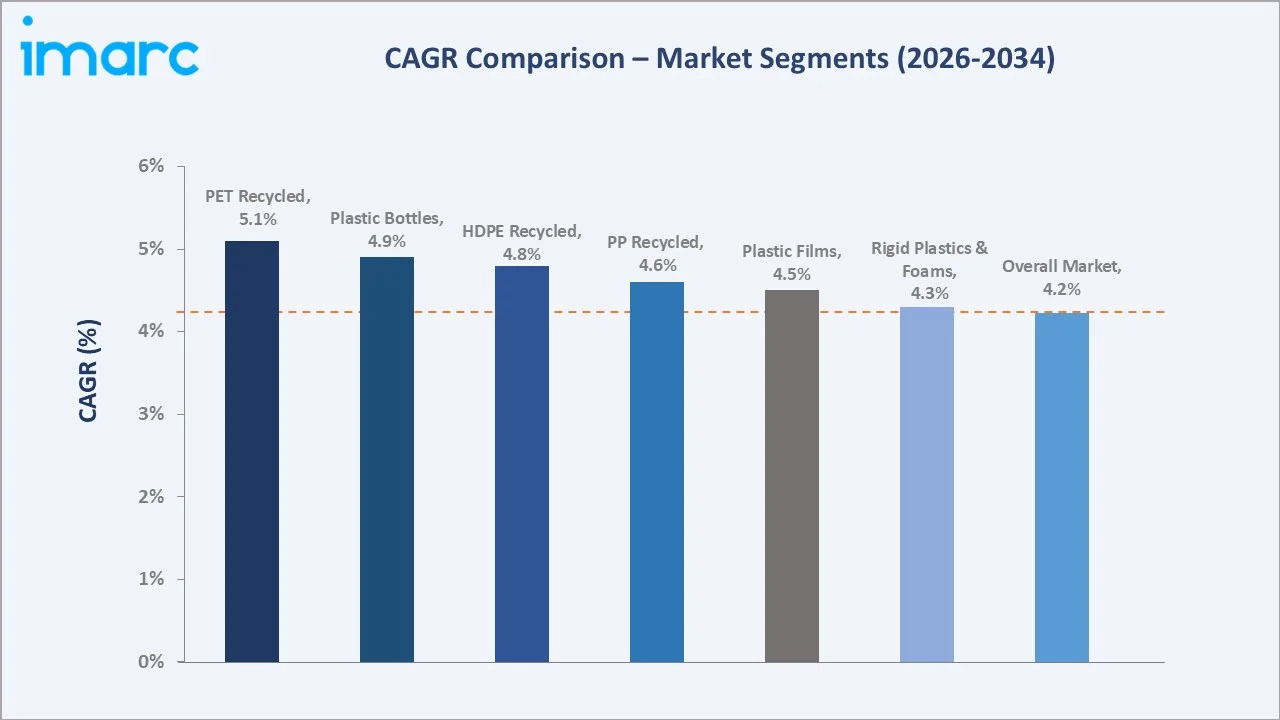

Segment-level CAGR comparisons highlighting PET recycled and Plastic Bottles as the two fastest-growing sub-categories within the Europe recycled plastics industry analysis through 2034, driven by beverage packaging regulations and food-contact-approved RPET demand from global FMCG brands.

Executive Summary

The Europe recycled plastics market is undergoing a fundamental structural shift driven by the convergence of EU regulatory mandates, corporate ESG commitments, and advancing recycling technology. Valued at 13.89 Million Tons in 2025, the market is forecast to reach 20.43 Million Tons by 2034 at a CAGR of 4.22%.

Plastic Bottles command the dominant source segment share at 38.4% in 2025, driven by Europe's best-in-class PET beverage collection infrastructure - deposit-return schemes in Germany, Norway, Sweden, Finland, and the Netherlands are generating a clean, consistently coloured PET stream for food-contact RPET production.

PET recycled plastics represent the leading plastic type segment at 34.2% share in 2025, benefiting from the highest FMCG brand demand, with Coca-Cola targeting 50% recycled content across all packaging by 2030 and Danone committing to 100% RPET bottles in specific markets.

Germany holds a 22.5% country share in 2025, anchored by the world's oldest deposit-return system since 2003, stringent EPR regulations, and robust industrial demand for recycled engineering polymers. The United Kingdom at 20.4% and France at 18.3% follow, with both markets experiencing accelerating legislative-driven demand through 2034. The competitive landscape is consolidating around vertically integrated recyclers - ALBA, Biffa (Energy Capital Partners Management, LP), Indorama Ventures- capable of producing food-contact-approved, consistently coloured recycled pellets at commercial scale.

Key Market Insights

|

Insight |

Data |

|

Largest Source Segment |

Plastic Bottles – 38.4% share (2025) |

|

Leading Plastic Type |

PET – 34.2% share (2025) |

|

Fastest Growing Type |

PET (CAGR ~5.1%, 2026-2034) |

|

Dominant Country |

Germany – 22.5% revenue share (2025) |

|

Second Largest Country |

United Kingdom – 20.4% share (2025) |

|

Top Companies |

ALBA, Biffa, Indorama Ventures, Covestro AG |

Key Analytical Observations Supporting The Above Data:

- Plastic Bottles' 38.4% source segment dominance in 2025 reflects Europe's best-in-class PET beverage collection infrastructure, including Deposit-Return Schemes across Germany, Norway, Sweden, Finland, and the Netherlands.

- PET's 34.2% plastic type share is driven by strong FMCG and beverage industry commitments. Companies such as Coca-Cola (targeting 50% recycled content in packaging by 2030), along with Danone and Nestlé Waters, have committed to scaling 100% rPET bottles in select European markets, significantly accelerating demand for food-grade recycled plastics.

- Germany's 22.5% country leadership is supported by its large packaging waste base and strong recycling systems. Germany generates over 12 million tonnes of packaging waste annually, with recycling rates for packaging overall exceeding ~65–70%, placing it among the top performers in Europe, though exact rates vary by material category and reporting methodology.

- The UK Plastics Packaging Tax, implemented in 2022 and revised upward in 2024, applies to plastic packaging containing less than 30% recycled content. This has structurally increased demand for recycled polymers such as rPET and rHDPE, as manufacturers shift toward compliance and cost optimization.

- Chemical recycling capacity expansion in Europe is gaining momentum, with cumulative investments exceeding EUR 2.5 billion through 2030. Industry participants such as Plastic Energy (pyrolysis), PureCycle Technologies (solvent-based purification), and BASF (ChemCycling mass-balance program) are advancing technologies, including pyrolysis and solvent-based purification, to complement mechanical recycling.

- France has established a progressive regulatory pathway under its circular economy framework, mandating rising recycled content incorporation in plastic packaging starting mid-decade and targeting full circularity over the long term. This creates a strong, policy-driven demand trajectory for recycled materials.

Europe Recycled Plastics Market Overview

Recycled plastics are polymers produced from post-consumer and post-industrial plastic waste through collection, sorting, and reprocessing via mechanical and emerging chemical recycling. The European ecosystem spans the full value chain—from waste collection to the production of recycled pellets, flakes, and compounds used as secondary raw materials.

Applications include packaging, automotive, electrical & electronics, construction, agriculture, and consumer goods, each defined by specific quality standards and regulatory requirements. This creates a tiered market, ranging from commodity-grade recyclates to high-purity, food-contact-approved resins.

Market growth is driven by rising cost pressure on virgin polymers, tightening recycled content mandates across the EU, and brand-owner ESG commitments.

Europe currently processes ~13–15 million tonnes of plastic waste annually via mechanical recycling, while chemical recycling is scaling, with ~1–1.5 million tonnes of additional capacity expected by 2030, subject to project execution.

Market Dynamics

To evaluate market opportunities, Request Sample

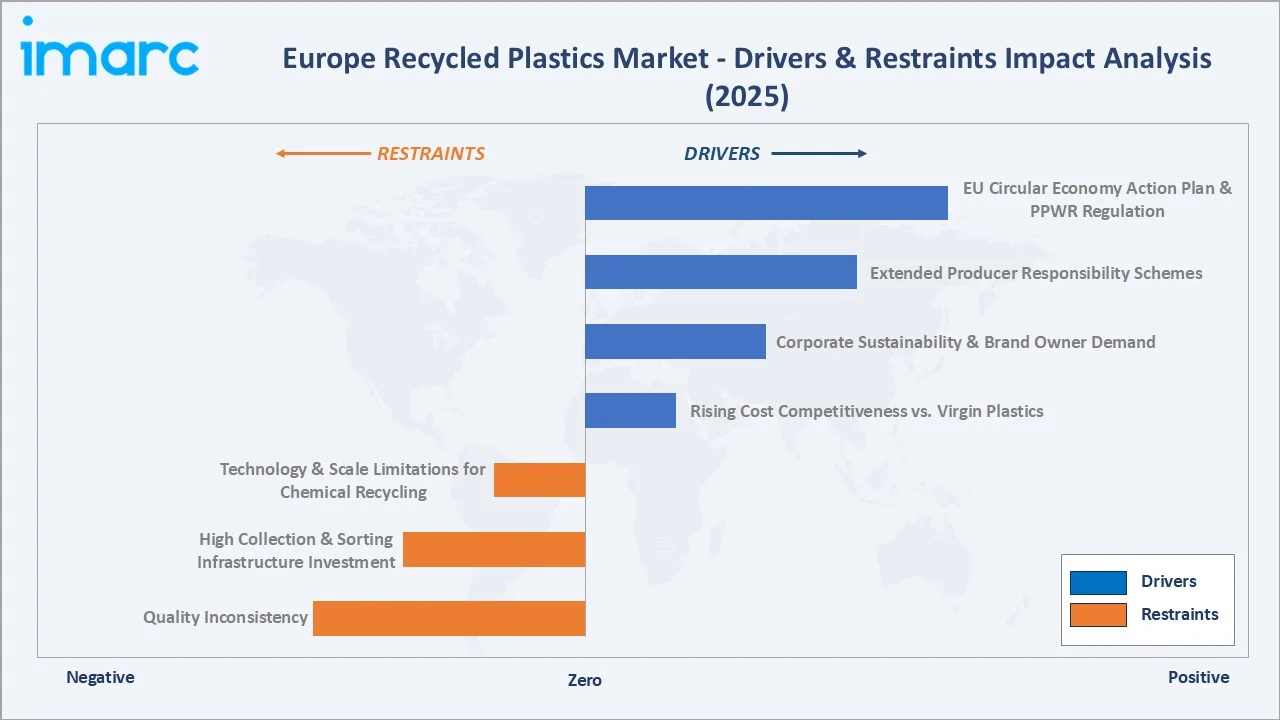

Market Drivers

- EU Circular Economy Action Plan and PPWR Regulation: The EU’s Circular Economy Action Plan (2020) and the proposed Packaging and Packaging Waste Regulation (PPWR) are core demand drivers, introducing binding recycled content targets across plastic packaging by 2030 and beyond. Plastic packaging placed on the EU market remains substantial (tens of millions of tonnes annually), making this the single largest demand lever for recycled polymers.

- Extended Producer Responsibility Schemes Expansion: Strengthened EPR schemes across countries, such as Germany, France, and Italy, are shifting waste management costs to producers. Fee modulation based on recyclability and recycled content directly incentivizes higher recycled polymer usage.

- Corporate Sustainability Commitments and Brand Owner Demand: Over 400 global brands under the Ellen MacArthur Foundation Global Commitment are targeting ~25% average recycled content in plastic packaging. This creates sustained demand for high-quality, food-grade rPET and rHDPE, often commanding premium pricing.

- Rising Cost Competitiveness of Recycled vs. Virgin Plastics: Recycled polymers—particularly rPET—are increasingly competitive with virgin materials. In recent market conditions, food-grade rPET has traded near parity with virgin PET, supporting adoption even beyond regulatory compliance.

Market Restraints

- Feedstock Contamination and Quality Inconsistency: Inconsistent collection systems, particularly in parts of Southern and Eastern Europe, result in contaminated and heterogeneous waste streams, increasing processing costs and limiting suitability for high-end applications.

- High Collection and Sorting Infrastructure Investment: Scaling deposit-return systems and advanced sorting infrastructure requires significant national-level investment (hundreds of millions to >EUR 1 billion). Several markets still lack the infrastructure density needed to meet upcoming EU recycling targets.

- Technology and Scale Limitations for Chemical Recycling: Technologies such as pyrolysis and depolymerisation are not yet fully commercial at scale, with challenges around cost, energy intensity, and yield efficiency, slowing near-term capacity ramp-up.

Market Opportunities

- Chemical Recycling Scale-Up for Hard-to-Recycle Streams: Advanced recycling technologies are unlocking value from multi-layer, contaminated, and mixed plastics currently directed to incineration. Companies such as Plastic Energy are demonstrating scalable pathways, potentially expanding the recyclable feedstock pool over the next decade.

- Recycled Engineering Polymers in Automotive: The shift toward electric vehicles is accelerating demand for lightweight, recycled-content polymers (e.g., PP compounds, ABS, PA). OEMs, including BMW, Volkswagen, and Stellantis, are incorporating recycled content targets in vehicle components, supporting long-term demand growth.

- Export Growth to Markets with Emerging Sustainability Regulations: Emerging regulatory frameworks in Asia and the Middle East are creating opportunities for European recyclers to export high-quality rPET and technical know-how, particularly where local recycling infrastructure is still developing.

Market Challenges

- Regulatory Uncertainty in Post-2025 Transition Period: While EU policy direction is clear, variation in national implementation, timelines, and verification methodologies creates short-term uncertainty for producers and converters.

- Competition from Low-Cost Virgin Plastics in Export Markets: Producers in regions with lower energy costs and limited carbon pricing exposure (e.g., the Middle East, parts of Asia) continue to supply cheaper virgin polymers, compressing margins for European recyclers, especially in export markets.

Emerging Market Trends

1. Advanced AI-Powered Sorting Technology

Adoption of AI-enabled optical sorting systems using near-infrared (NIR) spectroscopy is significantly improving material identification and separation efficiency. Solutions from Tomra and Sesotec are enhancing sorting accuracy and throughput across European MRFs. While purity levels vary by stream and facility, high-purity outputs for PET, HDPE, and PP are increasingly achievable, directly improving recyclate quality, yield, and suitability for food-contact applications.

2. Chemical Recycling Commercialisation

Chemical recycling is transitioning from pilot to early commercial scale. Companies such as Plastic Energy (pyrolysis), PureCycle Technologies (solvent-based purification), and BASF (ChemCycling mass-balance program) are scaling operations across Europe. Announced project pipelines indicate potential capacity exceeding ~1–1.5 million tonnes annually by 2030, complementing mechanical recycling by processing mixed and contaminated plastic waste streams.

3. Digital Traceability and Recycled Content Certification

Digital traceability platforms, including solutions from Circularise and Sourcemap, are being deployed to enable chain-of-custody tracking for recycled content. These systems support compliance with evolving EU regulations and corporate ESG reporting. In parallel, digital product passport frameworks under EU sustainability regulations are expected to drive broader adoption of lifecycle material tracking over the coming years.

4. Closed-Loop Packaging Systems

Brand owners and retailers are increasingly investing in closed-loop collection and recycling models to secure consistent, high-quality feedstock. Initiatives such as Renew3 (led by ALPLA Group and partners) and retailer-led take-back programs from Carrefour and Tesco demonstrate a shift toward vertically integrated recycling systems, reducing feedstock variability and improving traceability.

5. PPWR-Driven Recyclability by Design

The PPWR's recyclability-by-design requirements - mandating that all plastic packaging be recyclable at scale by 2030 - are driving a major product redesign wave across European packaging manufacturers. Removal of black carbon from packaging (invisible to NIR sorters), elimination of multi-layer film barriers, and replacement of PVC labels with PE/PET alternatives are increasing the fraction of packaging that can be effectively sorted and recycled, expanding the feedstock supply base throughout the forecast period.

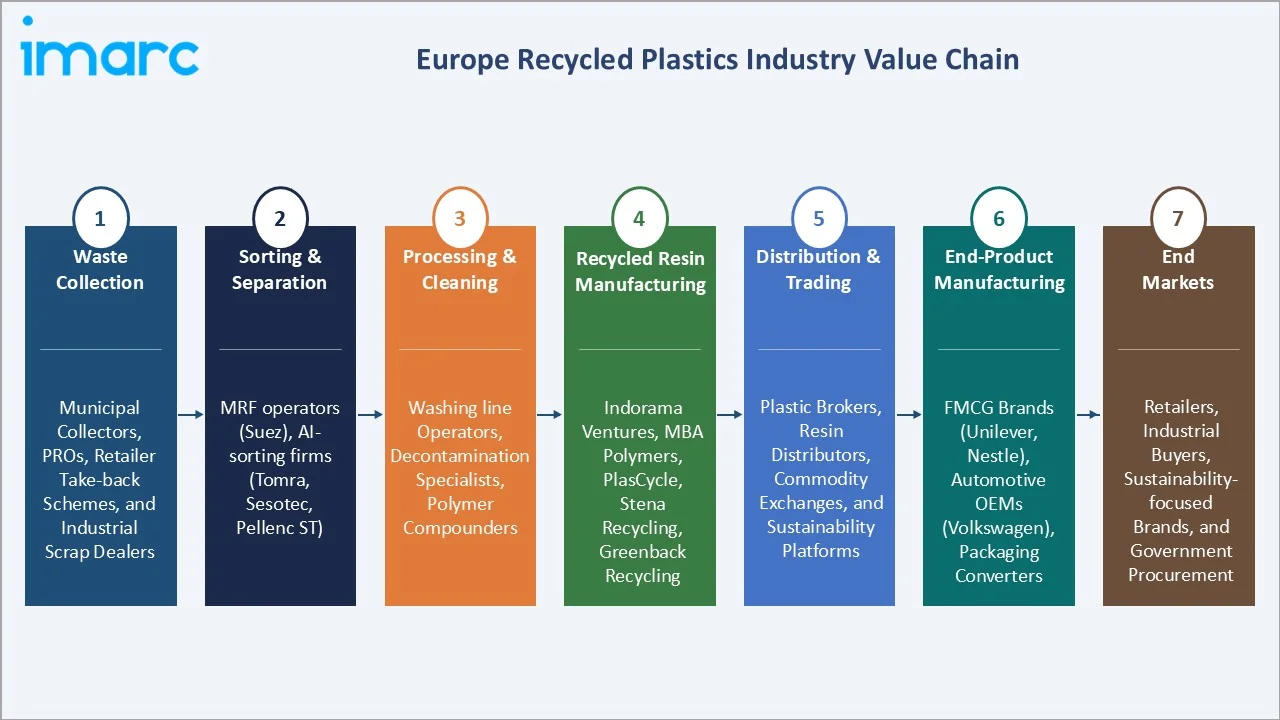

Industry Value Chain Analysis

The European recycled plastics value chain spans seven integrated stages from waste collection through end markets. Each stage presents distinct competitive dynamics, investment requirements, and margin profiles. The most capital-intensive stages - sorting and processing - are currently experiencing major investment inflows driven by PPWR compliance deadlines and brand-owner offtake commitments for certified recycled content.

|

Value Chain Stage |

Key Players / Examples |

|

Waste Collection |

Municipal collectors, PROs, retailer take-back schemes, and industrial scrap dealers |

|

Sorting & Separation |

MRF operators (Suez), AI-sorting firms (Tomra, Sesotec, Pellenc ST) |

|

Processing & Cleaning |

Washing line operators, decontamination specialists, polymer compounders |

|

Recycled Resin Manufacturing |

Indorama Ventures, MBA Polymers, PlasCycle, Stena Recycling, Greenback Recycling |

|

Distribution & Trading |

Plastic brokers, resin distributors, commodity exchanges, and sustainability platforms |

|

End-Product Manufacturing |

FMCG brands (Unilever, Nestle), automotive OEMs (Volkswagen), packaging converters |

|

End Markets |

Retailers, industrial buyers, sustainability-focused brands, and government procurement |

Tier-1 recyclers occupy the highest strategic value position in the European recycled plastics value chain, integrating collection, sorting, washing, and extrusion into a turnkey certified-resin supply that brand owners can adopt with guaranteed quality consistency. However, this structural position is being challenged by brand owners internalising collection infrastructure through closed-loop partnerships to capture greater supply chain control and reduce price volatility from open-market feedstock procurement.

Technology Landscape in the Recycled Plastics Industry

Mechanical Recycling: Washing Line and Extrusion Technology

Mechanical recycling remains the primary pathway in Europe, supported by advanced washing, sorting, and extrusion systems. Modern technologies from Starlinger and EREMA enable high-purity recyclates with consistent melt flow and colour, supporting use in food-contact and premium applications (subject to regulatory approval).

Chemical Recycling: Pyrolysis and Depolymerisation

Chemical recycling in Europe is scaling toward commercial deployment, complementing mechanical recycling by enabling the processing of mixed and hard-to-recycle plastic waste streams. Pyrolysis technologies convert heterogeneous plastic waste into hydrocarbon-rich feedstock suitable for petrochemical production, while depolymerisation processes break down polymers—particularly PET—into their monomer components, enabling true closed-loop, bottle-to-bottle recycling. Companies such as Indorama Ventures are at the forefront of advancing PET-to-PET recycling technologies toward commercial-scale implementation.

AI-Enabled Sorting and Near-Infrared Spectroscopy

NIR-based sorting systems, enhanced with AI, enable high-accuracy polymer identification and separation. Providers like Tomra, Sesotec, and Pellenc ST are improving sorting efficiency and output quality, supporting higher-value recycling streams.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Source |

Plastic Bottles |

38.4% |

2025 |

|

Application |

Packaging |

52.6% |

2025 |

|

Plastic Type |

Polyethylene Terephthalate (PET) |

34.2% |

2025 |

|

Country |

Germany |

22.5% |

2025 |

Market Breakup by Source (2025)

Plastic Bottles (38.4%) dominate due to Europe’s highly efficient PET collection systems. Deposit-return schemes ensure clean, colour-consistent feedstock, supporting food-contact rPET production. The segment will remain dominant, reinforced by PPWR targets for recycled content in PET beverage bottles by 2030.

To access detailed market analysis, Request Sample

Rigid Plastics & Foams (22.6%) include HDPE and PP containers from household and industrial use. Strong kerbside collection systems, particularly in Northern Europe, support supply, while demand is growing across construction, automotive, and agriculture applications.

Plastic Films (18.3%) cover flexible packaging from retail take-back, agriculture, and industrial sources. Despite high sorting complexity, this is the fastest-evolving segment, driven by recyclability mandates and expanding retailer-led collection programs from Lidl, Carrefour, and Tesco.

Fibres (12.4%) consist mainly of PET textiles and fibres. Growth is supported by EU-wide textile collection requirements by 2025, increasing feedstock availability for applications such as non-wovens, insulation, and geotextiles.

Market Breakup by Plastic Type (2025)

PET (34.2%) leads due to Europe’s mature recycling ecosystem, with high collection and recycling rates relative to other polymers. It is widely available in food-contact grades, supported by multiple EFSA-approved bottle-to-bottle processes, making it the most commercially advanced recycled plastic.

HDPE (26.4%) benefits from broad usage in household, food, and industrial packaging. Recycled HDPE is widely used in pipes, construction materials, and automotive components, with infrastructure and construction demand supporting steady growth.

Polypropylene (22.3%) faces sorting and quality challenges due to diverse grades and additives. However, advancements in sorting and compounding technologies are improving recyclability. Demand is driven by the automotive sector, with companies like Volkswagen Group and BMW targeting higher recycled content in components.

LDPE (11.8%) is primarily sourced from flexible films. Growth is supported by expanding retailer take-back programs and increasing adoption in film applications such as refuse bags, carrier bags, and agricultural films.

Regional Market Insights

|

Country |

Share (2025) |

Key Drivers & Notes |

|

Germany |

22.5% |

Pfand DRS (98% PET collection), strict EPR laws, strong auto & packaging industrial demand |

|

United Kingdom |

20.4% |

Plastics Packaging Tax (GBP 217.85/tonne, 2024), expanding DRS, and leading RPET processing capacity. |

|

France |

18.3% |

AGEC law mandates 20% recycled content by 2025, Citeo EPR system collecting ~1.1M tonnes (2023) |

|

Italy |

16.2% |

Large HDPE/PP recycling capacity, agricultural film programs, COREPLA EPR at 48% recycling rate |

|

Spain |

12.4% |

Law 7/2022 mandating DRS implementation, growing automotive converter demand for rPP and rABS. |

|

Others |

10.2% |

Poland, the Netherlands, and Belgium are driving incremental volume; Eastern Europe's infrastructure is expanding. |

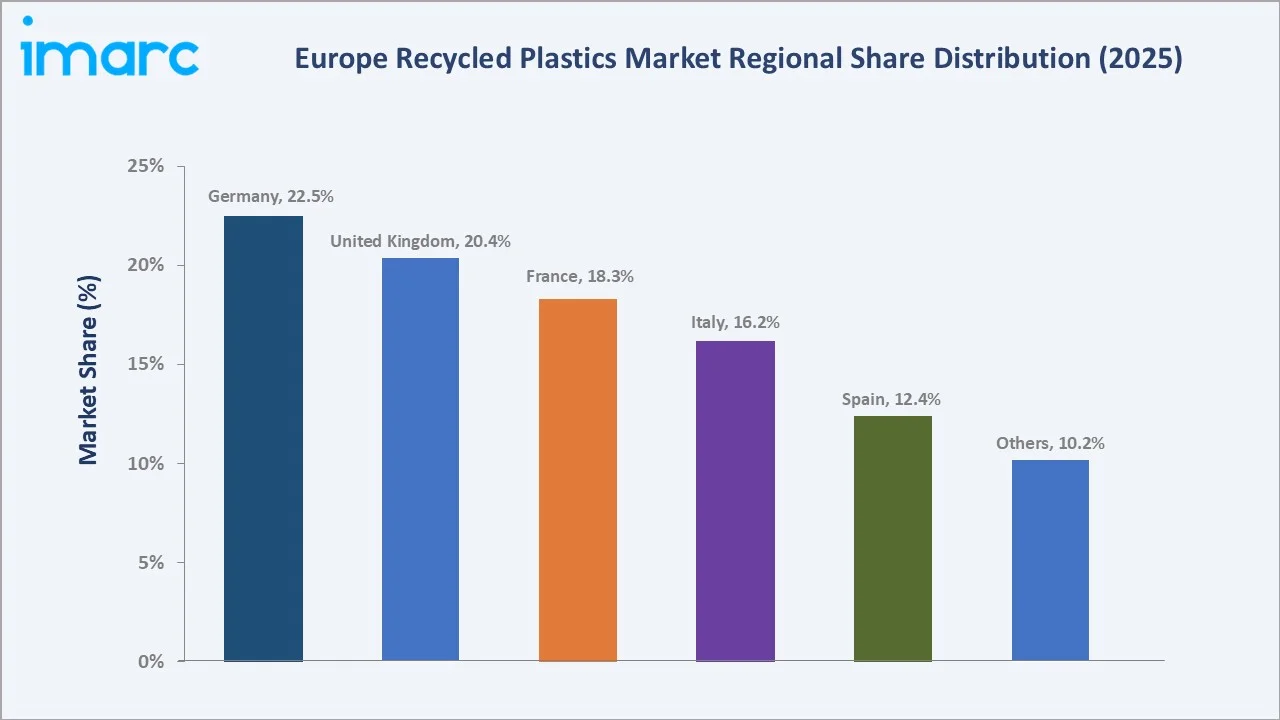

Germany represents the largest and most mature market, supported by its Pfand deposit-return system, dual collection structure, and strong regulatory framework. High collection efficiency and large packaging waste volumes ensure a stable supply of high-quality recyclates, with established domestic capacity serving European FMCG demand.

The United Kingdom (20.4%) is driven by the Plastics Packaging Tax and upcoming EPR reforms and DRS implementation. These measures are expected to significantly improve collection rates and expand the availability of food-grade recyclable feedstock.

France benefits from its progressive circular economy legislation, with rising recycled content requirements strengthening demand. A well-structured EPR system is driving consistent improvements in collection and recycling volumes.

Spain (12.4%) is the fastest-growing major market, supported by evolving waste regulations and planned deposit-return system implementation, which will enhance collection efficiency and feedstock availability.

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

ALBA |

Interseroh |

Leader |

Integrated collection, sorting, and compounding across Germany, Poland, and the UK. |

|

Biffa |

Biffa Polymers / Esterpet |

Leader |

UK’s largest food-grade RPET plant; ~80,000 tonnes/annum processing capacity |

|

Indorama Ventures |

IVSR / Wellman International |

Challenger |

Global PET/RPET leader; major RPET flake and resin supplier across EU markets |

|

Covestro AG |

Evocycle CQ |

Challenger |

Circular economy PC and PU; chemical recycling investments via Evocycle CQ |

|

Stena Metall AB |

Stena Recycling |

Challenger |

Scandinavian leader expanding mechanically recycled output toward PPWR targets |

|

Greenback Recycling Technologies Ltd. |

Greenback |

Emerging |

AI-enabled sorting, focus on hard-to-recycle films and flexible packaging streams. |

|

REMONDIS SE & Co. KG |

REMONDIS Electrorecycling, MIREC BV |

Challenger |

operates one of Europe's most advanced PET sorting and washing plants in; key provider for Germany's bottle deposit (Pfand) return system; processes HDPE, PP, and polyamide alongside PET from dual-system municipal collections across 30+ countries. |

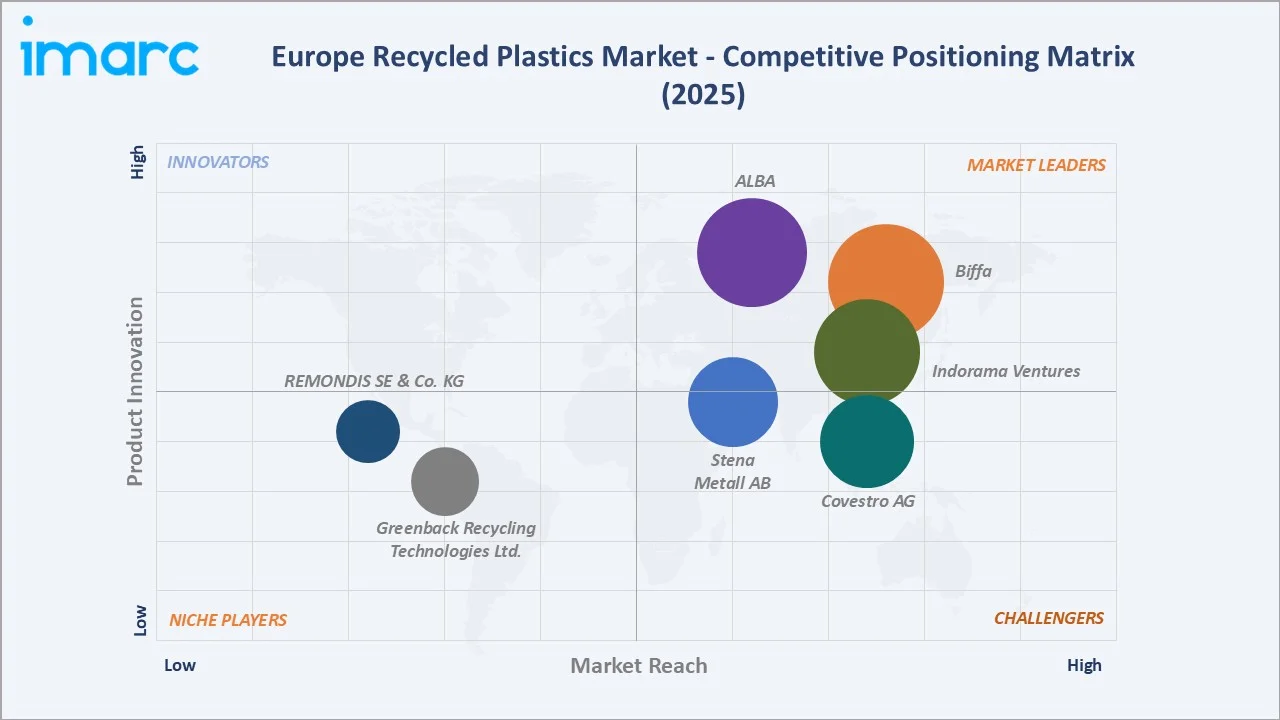

The competitive landscape is bifurcating between large-scale commodity recyclers focusing on volume and cost efficiency, and specialist high-value recyclers commanding premium prices for food-contact RPET and recycled engineering polymers.

Key Company Profiles

ALBA

ALBA is a Germany-based recycling and environmental services company, with a strong presence in plastics collection, sorting, and recycling across Europe. Through its Interseroh+ platform, the company is also a key player in EPR compliance and circular packaging solutions.

- Product & Platform Portfolio: rPE, rPP, and rPET recyclates, plastic flakes and regranulates, packaging recycling solutions, and integrated waste collection and sorting systems.

- Recent Developments: In October 2022, Covestro AG (ADNOC/XRG) and the environmental service provider Interseroh, a company of ALBA Group, intend to cooperate in the field of innovative recycling of plastic waste. This includes resistant plastic products made from Covestro materials, such as polyurethanes and polycarbonates.

- Strategic Focus: ALBA's strategy centres on vertical integration from collection through compounding, enabling control of feedstock quality from municipal DRS streams. The company is investing in AI-driven sorting upgrades and building capacity for food-contact RPET certification across its German and Polish facilities, targeting premium brand-owner markets ahead of the 2030 PPWR compliance wave.

Biffa

Biffa is a UK-headquartered integrated waste management and recycling company, owned by Energy Capital Partners Management, LP since 2023. It is one of the UK’s leading circular economy players, providing end-to-end services across waste collection, sorting, recycling, and energy recovery, with strong capabilities in plastics recycling and material recovery infrastructure.

- Product & Platform Portfolio: Plastic recycling (including food-grade PET), material recovery facilities (MRFs), waste collection and sorting, landfill and energy-from-waste, and surplus redistribution platforms.

- Recent Developments: In January 2023, Biffa was acquired by Energy Capital Partners in a ~£2.1 billion transaction, strengthening investment in recycling and circular economy infrastructure. The company has also expanded its plastics recycling capabilities through acquisitions such as Esterpet, enhancing food-grade rPET production capacity.

- Strategic Focus: Targets large-scale recycling infrastructure with secured feedstock and offtake agreements, aiming to scale capacity and reduce supply chain and pricing risks.

Indorama Ventures Public Company Limited

Indorama Ventures, a Thailand-headquartered global chemical company, is the world's largest PET and RPET producer. In Europe, the company operates through Wellman International in the Netherlands and acquired facilities in France and the UK.

- Product & Platform Portfolio: RPET flake, food-grade RPET pellets, bottle-to-bottle and bottle-to-fibre RPET grades, polyester staple fibre from recycled PET feedstock for non-woven and textile applications.

- Recent Developments: In February 2022, Indorama Ventures Public Company Limited completed a deal for an 85% equity stake in Czech Republic-based PET plastic recycler, UCY Polymers CZ s.r.o. (UCY), boosting the country and Europe’s plastic collection and recycling ambitions.

- Strategic Focus: Indorama's European strategy focuses on securing long-term brand-owner offtake agreements for food-contact RPET at competitive pricing enabled by scale, integrating European operations with global procurement and distribution networks to reduce feedstock cost volatility relative to domestic-only European recyclers.

Market Concentration Analysis

The European recycled plastics market is moderately fragmented, with a mix of large integrated players and numerous regional recyclers. Companies such as ALBA, Biffa (Energy Capital Partners Management, LP), Indorama Ventures, Covestro AG (ADNOC/XRG), and Stena Metall AB are among the key participants, collectively holding a meaningful but not dominant share, with the majority of volumes processed by a long tail of regional operators.

The market exhibits a bifurcated structure. In the premium food-contact segment, consolidation is underway due to high capital and regulatory barriers, including EFSA-approved processes, advanced washing and extrusion systems, and stringent quality control requirements. This limits participation to a relatively small group of certified operators, creating higher entry barriers and more stable margins.

In contrast, the commodity-grade segment (e.g., recycled PP, HDPE, and LDPE) remains highly fragmented, with numerous local recyclers serving regional end markets. This segment is more exposed to price volatility, feedstock competition, and fluctuations in virgin polymer prices, which can compress margins across the value chain.

Investment & Growth Opportunities

Fastest-Growing Segments

PET leads growth, driven by EU recycled content mandates and strong FMCG demand for rPET. Plastic Bottles are the fastest-growing source, supported by expanding deposit-return systems (DRS) ensuring high-quality feedstock.

Emerging Investment Themes

Chemical recycling is the key investment focus, targeting hard-to-recycle plastics, with ~EUR 2–3 billion committed across Europe. Digital traceability platforms are gaining traction, enabling recycled content verification and regulatory compliance.

Venture & Private Investment Trends

Investment in Europe’s recycled plastics market is accelerating, driven by regulation and demand for recycled content. Capital is focused on scaling recycling infrastructure (mechanical and chemical) and integrated platforms to secure feedstock and stable returns. Overall, investors prioritize long-term circular economy assets and vertical integration.

Future Market Outlook (2026-2034)

The Europe recycled plastics market forecast projects steady value expansion from 13.89 Million Tons in 2025 to 20.43 Million Tons by 2034 at a CAGR of 4.22% - a near-50% increase in market value underpinned by regulatory compliance deadlines, recycled content mandates, and structural shifts in collection infrastructure investment through the forecast period.

The PPWR is set to drive a step-change in demand for food-grade recycled plastics, particularly in PET beverage and other contact-sensitive packaging, potentially leading to supply tightness toward 2030 if collection and recycling capacity do not scale in parallel. By 2034, the market is expected to evolve into a strategic secondary raw materials industry, shaped by integrated recyclers such as ALBA, Biffa (Energy Capital Partners Management, LP), Indorama Ventures supplying certified materials, chemical recyclers like Plastic Energy processing complex waste streams, and traceability platforms enabling compliance and recycled content certification.

Research Methodology

Primary Research

Primary research included 45+ structured interviews (2024–2025) with key European recycled plastics stakeholders—recyclers, FMCG procurement leaders, EPR operators, regulatory experts, and investors—validating market size, segmentation, technology adoption, and competitive dynamics.

Secondary Research

Secondary sources include European Environment Agency plastics waste statistics, Plastics Europe Market Data and Trends reports, PlasticsEurope Recycling Annual Reports, IHS Markit (S&P Global) polymer price data, Ellen MacArthur Foundation New Plastics Economy Progress Reports, EPRO (European Association of Plastics Recycling) Annual Statistics, national EPR operator reports (Citeo France, Recupel Belgium, Grune Punkt Germany), company annual reports, and trade publications including Plastics News Europe, Recycling International, and European Plastics News.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates across EU-27 member states, plastic packaging waste generation indices, collection rate trajectory analysis, legislative compliance timelines under PPWR, and historical market evolution patterns. Scenario analysis across base, optimistic, and conservative cases was performed to account for regulatory implementation uncertainty and macroeconomic variables.

Europe Recycled Plastics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Tons |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook. Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Sources Covered | Plastic Bottles, Plastic Films, Rigid Plastics and Foams, Fibres, Others |

| Applications Covered | Packaging, Electrical and Electronic, Automotive, Agriculture, Construction and Demolition, Household (Non-Packaging Use), Others |

| Plastic Types Covered | Polyethylene Terephthalate (PET), High Density Polyethylene (HDPE), Polypropylene (PP), Low Density Polyethylene (LDPE), Others |

| Countries Covered | Germany, UK, Italy, France, Spain, Others |

| Companies Covered | ALBA, Biffa, Indorama Ventures, Covestro AG, Stena Metall AB, Greenback Recycling Technologies Ltd., REMONDIS SE & Co. KG, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe Recycled Plastics Market Report

The Europe recycled plastics market was valued at 13.89 Million Tons in 2025, driven by EU regulatory mandates, EPR scheme expansion, and corporate sustainability commitments from leading FMCG brands.

The market is projected to reach 20.43 Million Tons by 2034, growing at a CAGR of 4.22% during 2026-2034, driven by PPWR recycled content mandates, expanding DRS collection infrastructure, and chemical recycling capacity scale-up.

Plastic Bottles lead with a 38.4% share in 2025, driven by Europe's best-in-class PET beverage collection infrastructure through deposit-return schemes achieving 85-98% collection rates across Germany, Norway, Sweden, Finland, and the Netherlands.

PET leads with a 34.2% share in 2025, driven by the highest FMCG brand demand for food-contact-approved RPET, the most mature collection and processing infrastructure of any European polymer, and PPWR's specific beverage bottle recycled content mandate for 2030.

Germany leads with a 22.5% share in 2025, driven by the Pfand deposit-return system (98% PET collection), the Green Dot EPR scheme, and one of Europe's highest plastic packaging recycling rates at 68%, combined with strong automotive and packaging industrial demand.

Key drivers include the EU PPWR recycled content mandates (10-65% by 2030), national plastics taxes (UK GBP 217.85/tonne), EPR scheme strengthening across EU-27, FMCG corporate sustainability commitments pledging 25%+ recycled content, and chemical recycling capacity expansion for hard-to-recycle streams.

PET recycled plastics is the fastest-growing polymer type at approximately 5.1% CAGR through 2034, while Plastic Bottles is the fastest-growing source segment at approximately 4.9% CAGR, both driven by PPWR's specific beverage packaging mandates and expanding DRS infrastructure.

Leading companies include ALBA, Biffa, Indorama Ventures, Covestro AG, Stena Metall AB, Greenback Recycling Technologies Ltd., and REMONDIS SE & Co. KG.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)