Europe Safes and Vaults Market Size, Share, Trends and Forecast by Type, Function Type, Application, End User, and Country, 2026-2034

Europe Safes and Vaults Market Size, Share, Trends & Forecast (2026-2034)

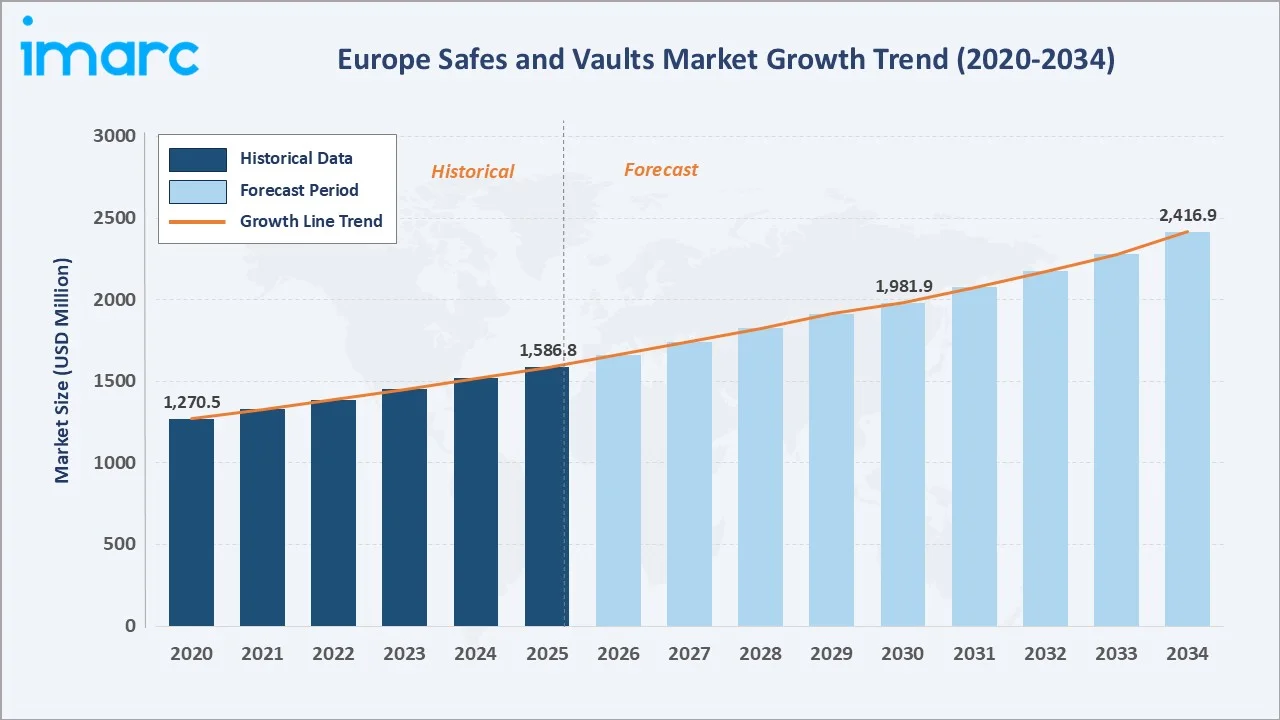

The Europe safes and vaults market size reached USD 1,586.8 Million in 2025 and is projected to reach USD 2,416.9 Million by 2034, exhibiting a CAGR of 4.55% during 2026-2034. Rising burglary rates, growing banking sector requirements, and accelerating adoption of biometric and smart safes are the primary drivers.

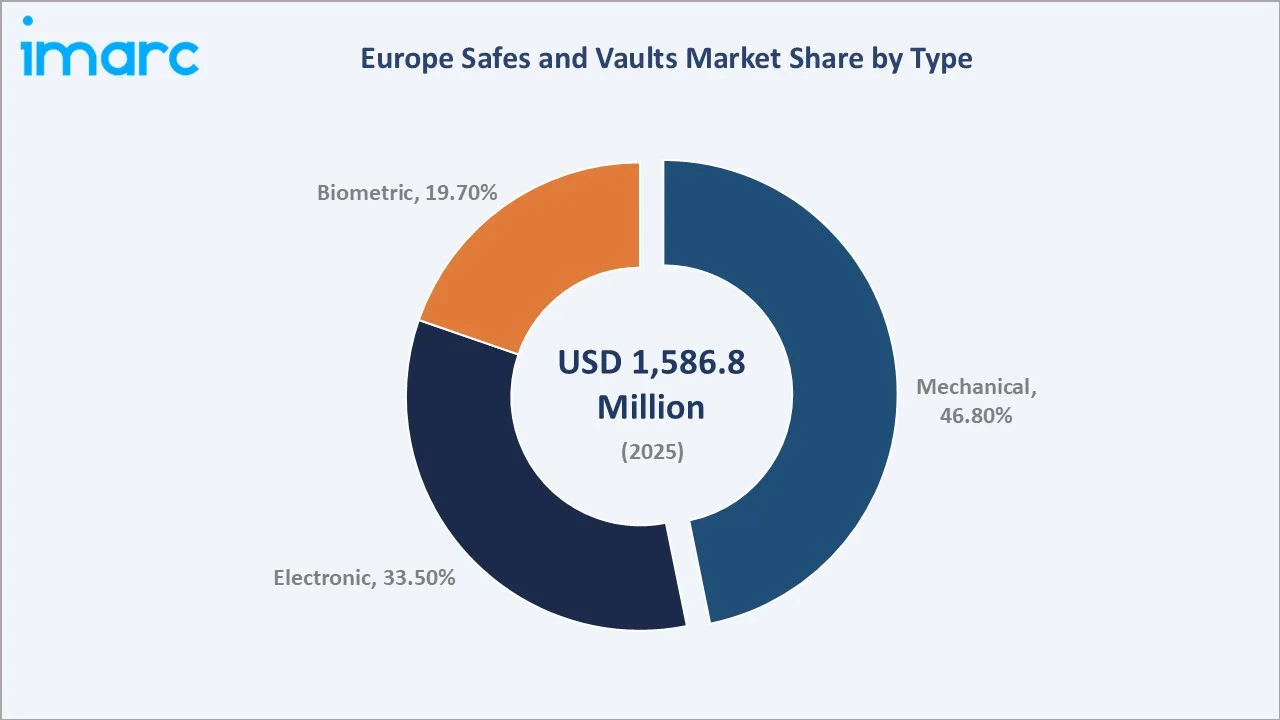

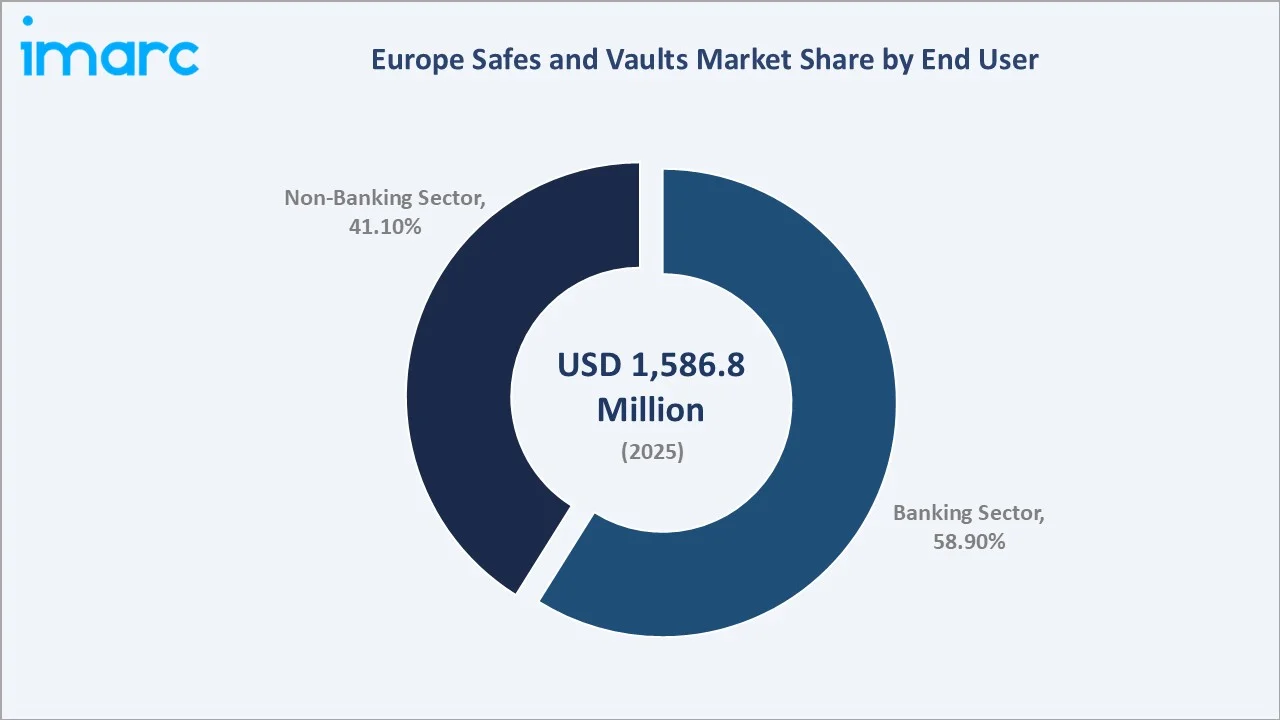

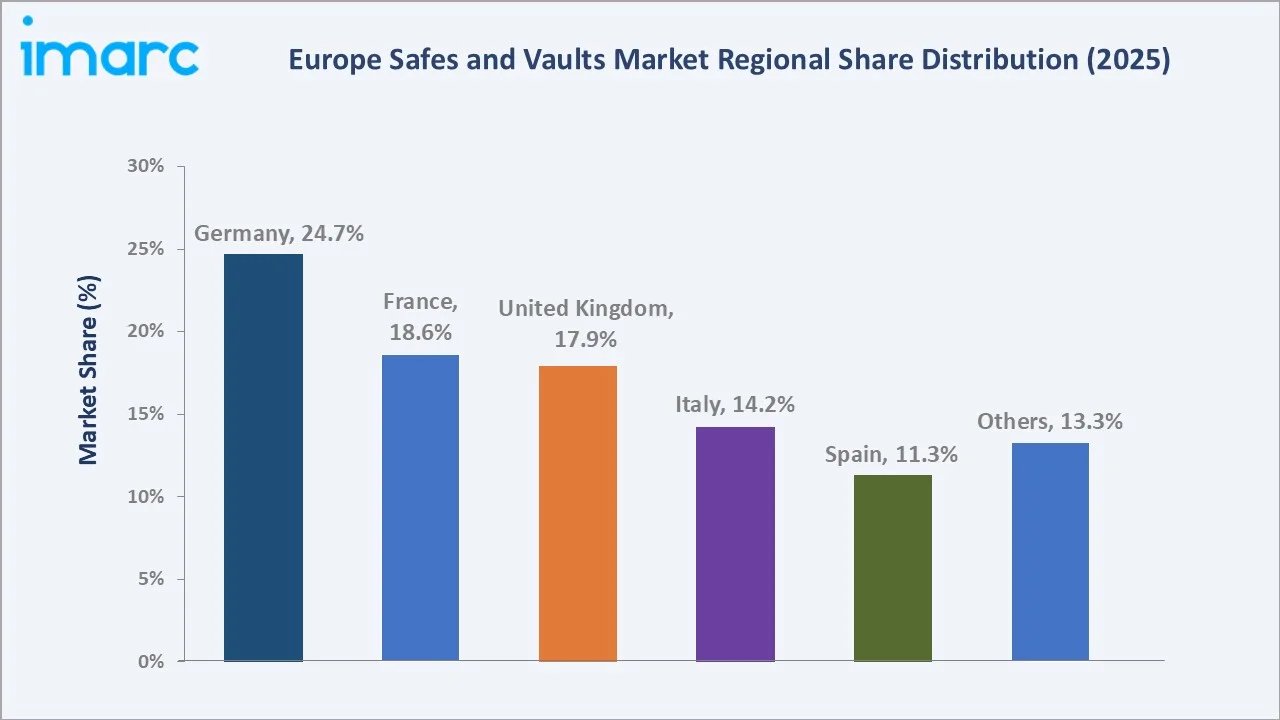

Mechanical safes dominate the type segment at 46.8% in 2025, while the banking sector leads end-user demand at 58.9%. Germany commands the largest country share at 24.7%, reflecting its robust financial infrastructure and advanced manufacturing base.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1,586.8 Million |

|

Forecast Market Size (2034) |

USD 2,416.9 Million |

|

CAGR (2026-2034) |

4.55% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

Germany (24.7% share, 2025) |

|

Second Largest Country |

France (18.6% share, 2025) |

|

Leading Type |

Mechanical (46.8%, 2025) |

|

Leading End User |

Banking Sector (58.9%, 2025) |

The Europe safes and vaults market growth trajectory from 2020 through 2034, with the historical expansion from USD 1,270.5 Million in 2020 to USD 1,586.8 Million in 2025, reflects consistent security-driven demand, while the forecast to USD 2,416.9 Million captures accelerating smart safe adoption, EU regulatory vault upgrades, and biometric technology penetration across Europe.

To get more information on this market, Request Sample

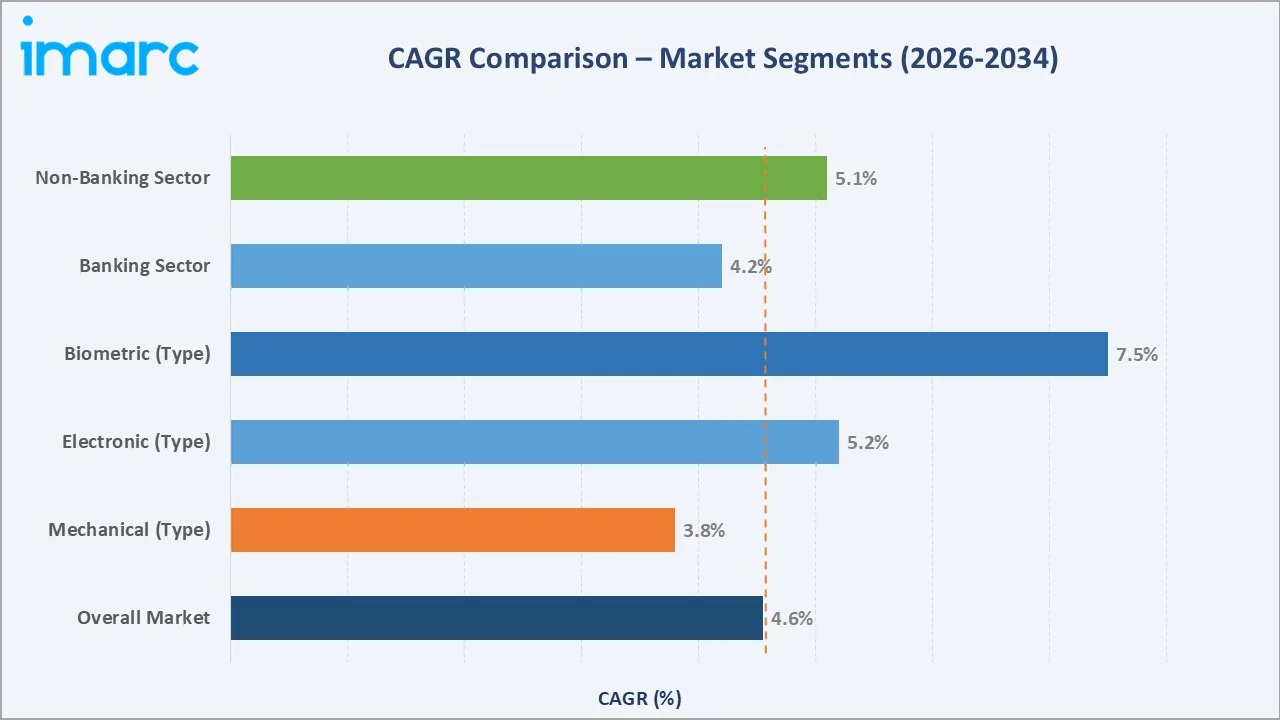

The CAGR trajectories across key type and end-user sub-segments, with biometric safes at ~7.5% CAGR and electronic safes at ~5.2% CAGR, represent the fastest-growing categories within the Europe safes and vaults industry analysis through 2034.

Executive Summary

The Europe safes and vaults market is on a sustained growth trajectory from USD 1,586.8 Million in 2025 to USD 2,416.9 Million by 2034. Safes and vaults are essential physical security products deployed across banks, retail outlets, residential properties, hotels, and government institutions to protect cash, valuables, documents, firearms, and sensitive data from theft, fire, and unauthorized access.

Mechanical safes dominate at 46.8% in 2025, owing to their reliability, power-independence, and cost-effectiveness across the broadest range of European commercial and residential applications. Electronic safes (33.5%) are gaining rapidly in commercial and institutional deployments, offering programmable multi-user access and digital audit-trail capabilities. Biometric safes (19.7%) are the fastest-growing segment as healthcare providers, luxury hotels, and financial institutions demand PIN-free access control.

Germany leads the regional landscape at 24.7% in 2025, supported by advanced manufacturing, a dense banking network, and stringent security regulations. France (18.6%) and the United Kingdom (17.9%) follow, driven by active commercial and hospitality sectors. Italy and Spain contribute 14.2% and 11.3% respectively, reflecting growing awareness among small and mid-sized businesses regarding certified physical security.

Key Market Insights

|

Insight |

Data |

|

Largest Type |

Mechanical – 46.8% share (2025) |

|

Second Largest Type |

Electronic – 33.5% share (2025) |

|

Fastest-Growing Type |

Biometric (~7.5% CAGR, 2026-2034) |

|

Leading End User |

Banking Sector – 58.9% revenue share (2025) |

|

Second End User |

Non-Banking Sector – 41.1% revenue share (2025) |

|

Leading Country |

Germany – 24.7% revenue share (2025) |

|

Top Companies |

Gunnebo AB, ASSA ABLOY Group, dormakaba Group, Diebold Nixdorf, Burg-Wächter, Bordogna Casseforti |

Key Analytical Observations Expanding on the Above Data:

- Mechanical safes, with 46.8% in 2025, lead because their non-reliance on power or digital systems makes them impervious to electronic attacks and malfunctions, a crucial advantage for jewelry retailers, firearms dealers, and residential users across Central and Southern Europe, where cost sensitivity and distrust of digital-only systems remain high.

- Banking Sector dominance at 58.9% in 2025 reflects the fundamental requirement of European financial institutions to physically secure cash reserves, gold, bearer instruments, and sensitive client documentation. Compliance with EU PSD2 directives and national banking security standards mandates regulated vault infrastructure across all licensed credit institutions.

- Germany's 24.7% country share is underpinned by its status as Europe's largest economy, housing approximately 1,500 banks and credit institutions and a sizeable private wealth management ecosystem. The presence of globally recognized safe manufacturers including Burg-Wächter further reinforces its domestic market depth and export capacity.

- The non-banking sector (41.1%) is growing in strategic importance, driven by luxury retail, hospitality, healthcare, and logistics firms adopting specialized vault solutions under EU GDPR and sector-specific compliance mandates for securing pharmaceuticals, precious goods, and confidential documentation.

Europe Safes and Vaults Market Overview

Safes and vaults are robust, reinforced-metal storage units constructed to protect physical assets from theft, fire, explosion, and unauthorized access. Products span wall safes, floor safes, gun safes, cash management safes, media safes, vault rooms, and vault doors, differentiated by locking mechanism (mechanical, electronic, biometric), fire-resistance rating (EN 1047-1, UL 72), and burglary resistance class (EN 1143-1 Grade I-VI).

The European ecosystem integrates raw steel and alloy suppliers, safe manufacturers, electronic and biometric component providers, security testing and certification bodies (ECB-S, VdS, CNPP), specialist security distributors and integrators, insurance providers, and diverse end-use sectors spanning banking, retail, hospitality, healthcare, and residential markets across Germany, France, the UK, Italy, Spain, and other European nations.

Market Dynamics

To evaluate market opportunities, Request Sample

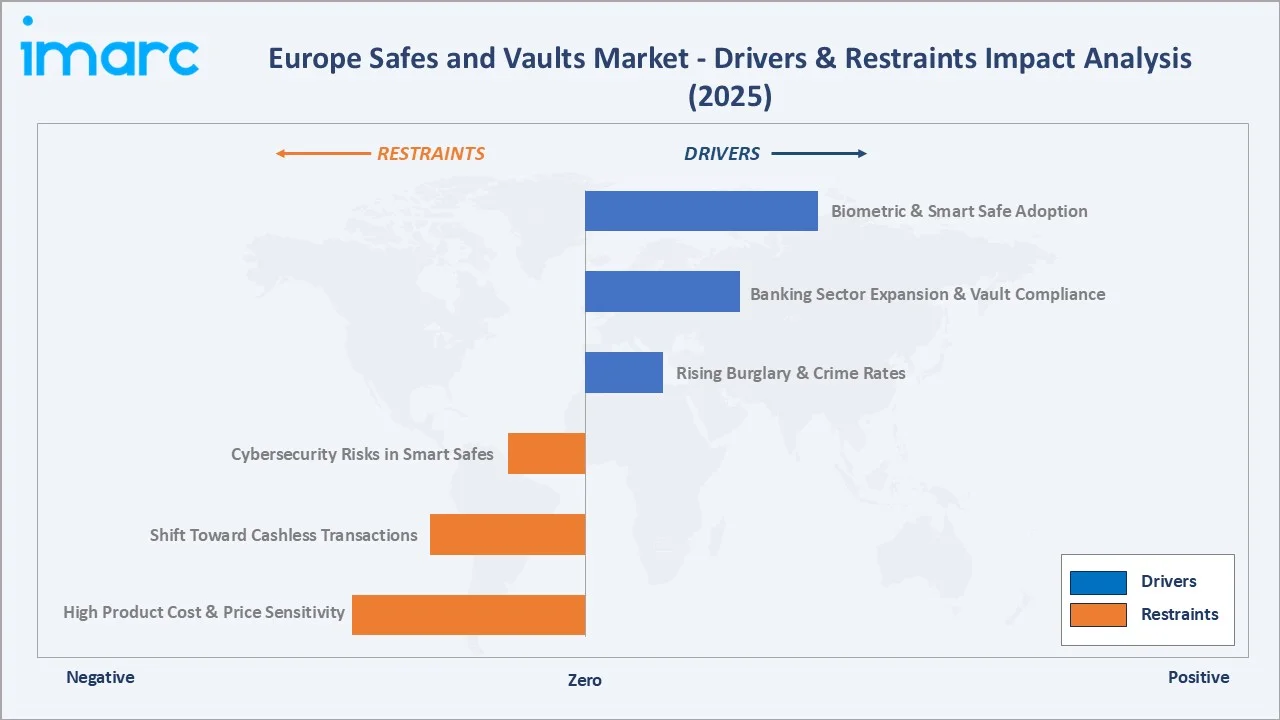

Market Drivers

- Rising Burglary and Crime Rates Across Europe: Domestic burglary, violent crime, armed robbery and street crime are identified as high-impact crimes due to the effect they can have on the victims. The police recorded 22 thousand domestic burglaries in 2024, around 500 fewer than in the previous year, directly boosting demand for certified safes in commercial and residential applications. The British Retail Consortium's 2025 survey confirmed retailers spent a record USD 2.3 Billion on crime prevention, up from USD 1.5 Billion the previous year — a 53% increase reflecting the urgency of physical security investment.

- Banking Sector Expansion and Vault Compliance Mandates: The January 2025 EU regulation requiring all financial institutions to upgrade vault systems to stricter security standards by 2027 is creating mandatory replacement demand. With over 3,700 credit institutions operating in the EU under ECB supervision, each maintaining regulated vault infrastructure, institutional procurement volumes are substantial, recurring, and largely non-discretionary.

Market Restraints

- High Cost of Premium Safe Products: Advanced biometric and fireproof-certified safes carry price points 3-5 times higher than standard mechanical models, constraining adoption among price-sensitive residential and SME buyers in Southern and Eastern Europe where disposable income levels and security awareness are comparatively lower than in German and UK markets.

- Shift Toward Cashless and Digital Transactions: The increasing adoption of contactless payments, digital wallets, and CBDC pilots across European economies is gradually reducing physical cash volumes in circulation, diminishing one of the primary use cases for commercial cash management safes in retail and hospitality environments across Northern and Western Europe.

Market Opportunities

- Gold Vaulting and Precious Metal Storage Growth: In April 2025, IBV International Vaults London launched IBV Gold, a division specializing in secure gold and silver storage, driven by unprecedented demand from geopolitical uncertainty and financial instability. This creates greenfield opportunities for specialized vault manufacturers targeting European precious metal investors and bullion dealers.

- Smart Safe-as-a-Service Platform Integration: The integration of smart safes with digital financial platforms is driving a shift toward real-time, in-store cash access and more efficient cash management, as partnerships between hardware providers and fintech or retail platform operators enable connected cash ecosystems. With API-enabled connectivity, these safes are increasingly embedded within broader retail and banking infrastructures, enhancing visibility, control, and operational efficiency.

Market Challenges

- Steel Price Volatility and Supply Chain Disruption: Raw material cost fluctuations, compounded by geopolitical tensions affecting European steel supplies, create margin pressure for safe manufacturers, particularly those reliant on spot-market steel procurement rather than long-term supply agreements with integrated steel producers.

- Cybersecurity Vulnerabilities in Connected Safes: IoT-enabled safes with remote monitoring and cloud reporting introduce new digital attack surfaces. Inadequately secured locking mechanisms and cloud platforms are vulnerable to hacking, creating reputational risk for manufacturers and a significant adoption barrier for risk-averse institutional buyers in banking and government sectors.

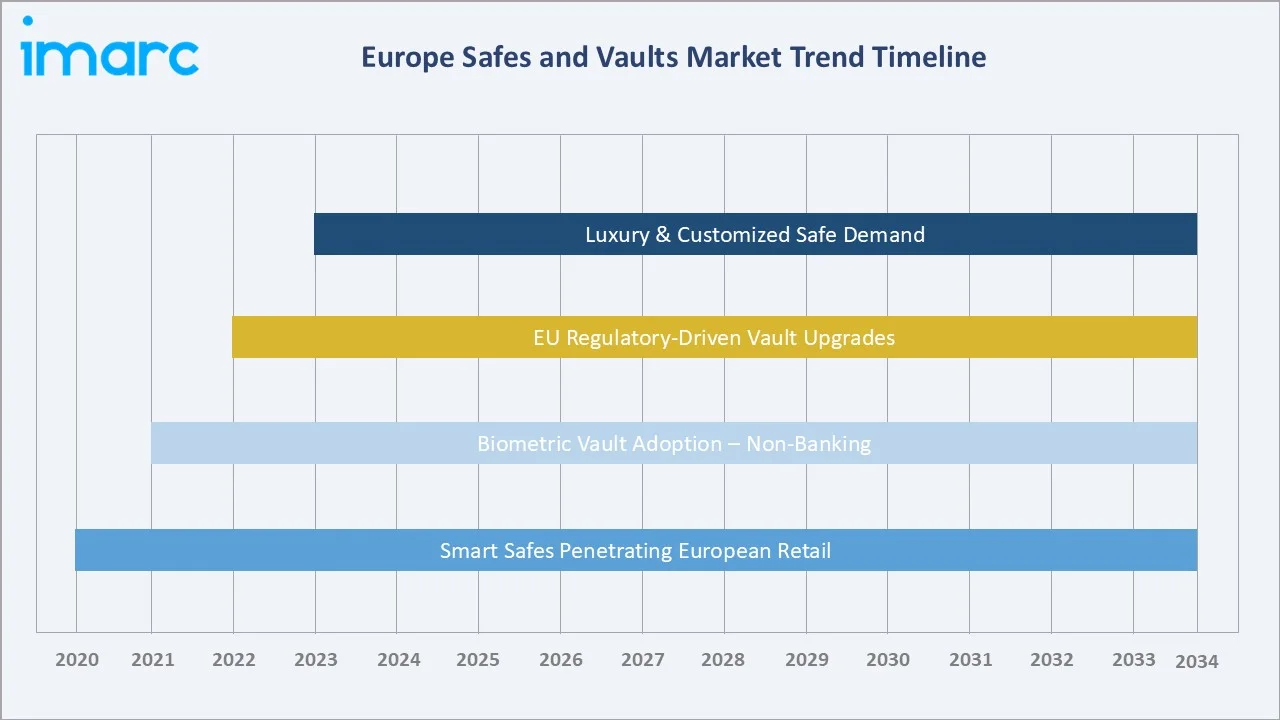

Emerging Market Trends

1. Smart Safes Making Inroads in European Retail

Retailers across Germany, the UK, and France are transitioning to smart safes at an accelerating rate, driven by the need to automate cash handling and reduce internal theft. The British Retail Consortium's 2025 crime survey — recording USD 2.3 Billion in security spending, up from USD 1.5 Billion — highlights the urgency behind this trend. Smart safes with POS integration, cloud reporting, and real-time monitoring are becoming standard procurement specifications for high-cash-turnover chains, supermarkets, and fuel station networks, offering traceable deposits and tamper-alert capabilities.

2. Biometric Vaults Expanding Beyond Banking

Biometric vaults are expanding their role across non-banking sectors in Europe. Healthcare providers, upscale hotels, and legal firms are adopting fingerprint- and iris-based vault access to secure pharmaceuticals, confidential documents, and guest valuables in alignment with EU GDPR requirements. Residential demand is growing among high-net-worth households in London, Paris, and Munich, where urban burglary rates are increasing.

3. EU Regulatory-Driven Vault Upgrade Cycle

The January 2025 EU regulation requiring financial institutions to upgrade vault systems to stricter security standards by 2027 is creating a structured, multi-year demand cycle. This compliance-driven replacement wave, affecting thousands of branch-level vault installations across EU member states, provides a high-visibility, predictable revenue stream for certified European vault specialists including Fichet-Bauche, dormakaba, and Diebold Nixdorf, which maintain the technical certification infrastructure required to meet institutional procurement standards.

4. Rise of Premium and Customised Safe Demand

Affluent European consumers are driving demand for bespoke safe solutions featuring customized interiors, premium finishes, concealment furniture integration, and brand-agnostic biometric upgrades. Swiss luxury safe specialists report growth from high-net-worth clients seeking safes for jewelry, watches, art, and firearms storage. This premium-segment growth supports higher per-unit revenue and favors specialist manufacturers with custom engineering and precision manufacturing capabilities over mass-market producers competing on price alone.

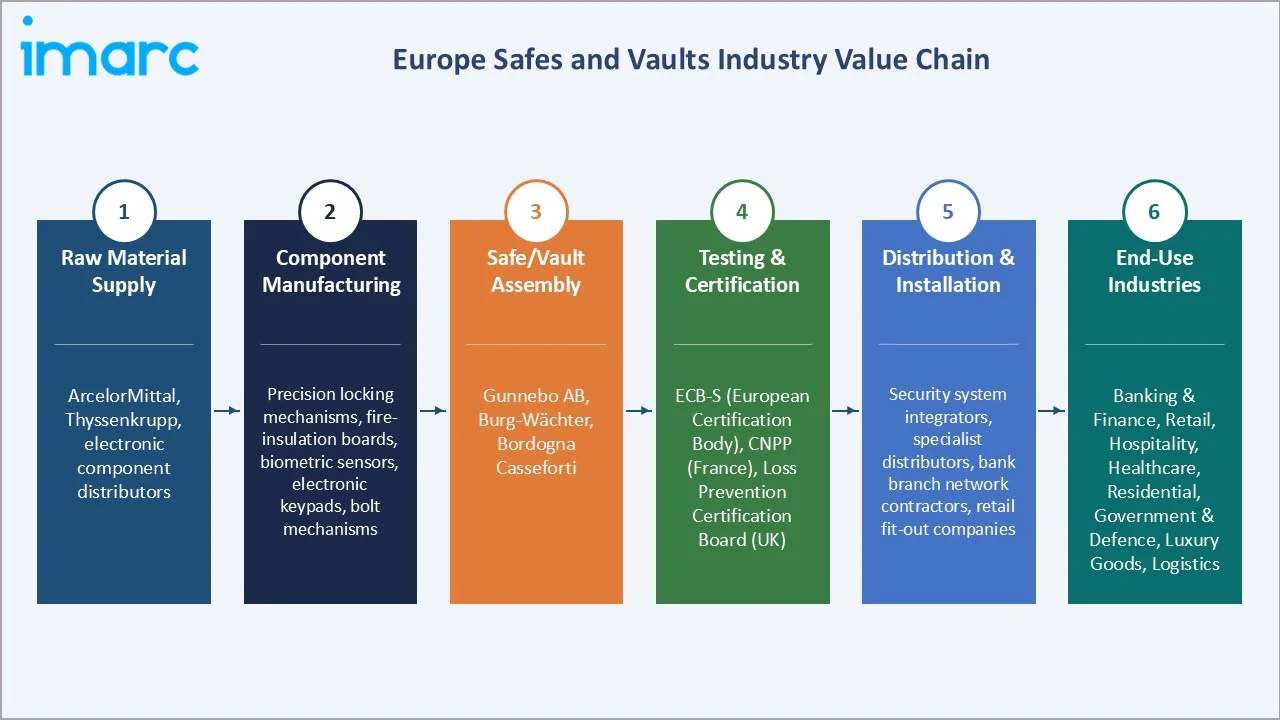

Industry Value Chain Analysis

The European safes and vaults value chain spans six stages from raw material procurement through end-use installation. Safe and vault assembly, quality certification, and service represent the highest value-add margins, while distribution and project-specific customization generate significant working capital requirements that favor well-capitalized mid-to-large manufacturers over smaller regional assemblers.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

ArcelorMittal, Thyssenkrupp; electronic component distributors |

|

Component Manufacturing |

Precision locking mechanisms, fire-insulation boards, biometric sensors, electronic keypads, bolt mechanisms |

|

Safe/Vault Assembly |

Gunnebo AB, Burg-Wächter, Bordogna Casseforti |

|

Testing & Certification |

ECB-S (European Certification Body), CNPP (France), Loss Prevention Certification Board (UK) |

|

Distribution & Installation |

Security system integrators, specialist distributors, bank branch network contractors, retail fitout companies |

|

End-Use Industries |

Banking & Finance, Retail, Hospitality, Healthcare, Residential, Government & Defence, Luxury Goods, Logistics |

Manufacturers with integrated locking mechanism production and in-house fire-insulation capability achieve cost structures below pure assemblers dependent on external components. This vertical integration is a meaningful competitive advantage, particularly in the certified Grade IV-VI high-security vault segment where component quality and supply-chain traceability are critical to maintaining EN 1143-1 certification status.

Technology Landscape in the Europe Safes and Vaults Industry

Locking Technology: From Mechanical Wheels to Biometric Sensors

The dominant locking mechanisms in European certified safes are high-quality mechanical combination locks (EN 1300 Class B/C) and Type 1/Type 2 electronic locks. CNC-machined relockers and glass-plate anti-drill barriers are standard in Grade III+ safes. Biometric integration extends beyond fingerprint to include iris recognition and palm-vein scanning for highest-security applications in banking and government vaults, with dual authentication combining biometric and PIN becoming standard in Grade V-VI institutional vault procurement specifications.

Fire-Resistance Technology and Material Innovation

EN 1047-1 certified media safes protect digital media at 125°C maximum internal temperature for up to 120 minutes. Advances in nano-engineered intumescent materials are enabling thinner fire barriers without sacrificing thermal insulation performance, improving the weight-to-protection ratio of portable fire safes for residential deployment. Composite concrete-steel body construction and differential-expansion plate layering are gaining adoption in premium vault door applications requiring both fire and ballistic resistance certification.

Digital Integration and IoT Connectivity

Leading manufacturers embed GSM/4G/Wi-Fi alarm transmission, remote access management, and cloud-hosted audit trail platforms into smart safe product lines. Integration with bank-grade API platforms, as demonstrated by the April 2025 Cennox-Retail365 partnership enabling real-time deposit crediting via Retail365's Lincsafe system, allows smart safe transactions to be credited to business bank accounts same day, fundamentally enhancing the value proposition for commercial retail and hospitality cash management applications.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Type | Mechanical | 46.8% |

2025 |

| Function Type | Cash Management Safes | 🔒 |

2025 |

| Application | Commercial |

🔒 |

2025 |

| End User | Banking Sector | 58.9% |

2025 |

| Country | Germany | 24.7% |

2025 |

By Type

Mechanical safes command a 46.8% majority share in 2025 owing to their proven reliability, power-independence, and cost-competitiveness across the broadest range of European commercial and residential applications. Their absence of electronic components eliminates malfunction and hacking risk, making them highly attractive to SMEs, jewelry retailers, firearms dealers, and residential users who prioritize durability over digital convenience.

To access detailed market analysis, Request Sample

Electronic safes at 33.5% in 2025 are increasingly preferred by commercial and institutional buyers requiring programmable multi-user access, time-delay locks, and digital audit trails. The ability to reprogram access codes without physical lock replacement offers meaningful total-cost-of-ownership advantage for high-turnover environments such as hotels, retail back-offices, and corporate facilities. The segment benefits from falling component costs driving electronic safe price points closer to equivalent mechanical models.

By End User

The banking sector holds the largest end-user share at 58.9% in 2025, reflecting the non-negotiable nature of physical vault infrastructure for European financial institutions. Banks, credit unions, and private wealth managers require Grade IV-VI certified vaults compliant with EN 1143-1 and national regulatory standards to secure cash, gold, bearer instruments, and customer valuables from both physical and sophisticated attack methodologies.

The non-banking sector at 41.1% in 2025 represents a strategically diversifying demand base. Retail chains, luxury goods stores, hotels, and healthcare providers are the primary non-banking buyers. The banking sector accounts for the highest revenue share at 58.9% in 2025, while the non-banking sector is growing at a faster rate driven by hospitality in-room biometric safe adoption and healthcare controlled-substance storage requirements under EU GMP guidelines.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

Germany |

24.7% |

Dense banking network; strict regulations; advanced manufacturing; high-net-worth wealth management |

|

France |

18.6% |

Banking vault demand; luxury goods sector; IBV Gold launch; regulatory upgrade cycle |

|

United Kingdom |

17.9% |

Retail crime escalation (USD 2.3 Bn spend); smart safe adoption; hospitality sector growth |

|

Italy |

14.2% |

Family business safe adoption; jewelry and luxury goods storage; growing SME security awareness |

|

Spain |

11.3% |

Expanding banking infrastructure; hotel and tourism sector demand; rising crime awareness |

|

Others |

13.3% |

Netherlands, Switzerland, Belgium, Nordics; affluent residential and institutional demand |

Germany's 24.7% market dominance in 2025 is driven by Europe's most structurally advanced combination of manufacturing expertise, banking density, and security regulation. With approximately 1,500 banking institutions and strict insurance requirements mandating certified safe installations across commercial premises, institutional procurement volumes are large, recurring, and supported by a domestic manufacturing ecosystem that includes globally recognized brands such as Burg-Wächter.

France, with 18.6% in 2025, is characterized by strong institutional vault demand from its five largest banking groups and a dynamic luxury goods sector requiring certified precious jewelry and watch storage. The April 2025 launch of IBV International Vaults London's IBV Gold division, offering immediately accessible secure gold and silver storage, exemplifies the growing precious-asset vaulting trend driving incremental institutional vault investment across European financial centers.

Competitive Landscape

The Europe safes and vaults market is moderately consolidated, with established regional leaders maintaining strong certification credentials and institutional distribution networks while facing increasing competition from Asian price-competitive imports in the mass-market residential and SME segments. Germany and France remain the primary manufacturing hubs, with national champions competing alongside global security conglomerates including ASSA ABLOY and dormakaba Group for major institutional contracts.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

|

Gunnebo Safe Storage AB |

SafeStore 3000F, SafeStore 2000C, SafeT, SafeStore Auto Midi, TransitGuard, Chubbsafes, Hamilton, Steelage |

Leader |

Banking & retail cash management; smart safe-fintech integration |

|

ASSA ABLOY |

Electronic & biometric safe locks |

Leader |

Security hardware integration; global presence; biometric systems |

|

dormakaba Group |

Safe locks |

Leader |

Banking vaults; multi-country EU presence; digital locking technology |

|

Diebold Nixdorf, Incorporated |

UL Rated CashGard Safes, UL Rated MasterGard Elite Composite Safes, Modular Vaults, DN Vault Doors |

Leader |

Banking technology integration; digital vault platforms; pan-European |

|

Burg-Wächter |

Money safe, Hotelsafes, Freestanding home safe |

Challenger |

German SME & residential market; broad value-range product line |

|

Bordogna Casseforti |

Freestanding safes, Modular safes, Money deposit safes, Key safes, Weapon safes |

Challenger |

Italian banking market; vault room specialization |

Key players include Gunnebo Safe Storage AB, ASSA ABLOY, dormakaba Group, Diebold Nixdorf, Incorporated, Burg-Wächter, Bordogna Casseforti, and others.

Key Company Profiles

Gunnebo Safe Storage AB

Gunnebo AB is a leading Swedish security group headquartered in Gothenburg, operating across safes, vault technology, and cash management through its globally recognized Chubbsafes and Steelage brands. The company serves banking, retail, and hospitality sectors across 25+ countries with a portfolio spanning certified safes, customized vault room solutions, and electronic security.

- Product Portfolio: The company offers SafeStore 3000F, SafeStore 2000C, SafeT, SafeStore Auto Midi, TransitGuard, Chubbsafes, Hamilton, Steelage, and others.

- Recent Developments: In November 2025, Gunnebo Safe Storage strengthened its presence in Europe by integrating its key manufacturing, design, and locking technology capabilities into a unified regional platform, bringing together major facilities and specialist entities to operate as a coordinated network. This consolidation enhances production capacity, improves supply chain resilience, and enables faster delivery while ensuring compliance with regional standards.

- Strategic Focus: Gunnebo's strategy prioritizes integration of physical safe products with digital cash management platforms, targeting the retail cash-in-transit optimization market while maintaining leadership in European banking vault installations through long-term institutional service contracts and recurring SafePay software subscriptions.

dormakaba Group

dormakaba Group is a Swiss global security and access solutions company headquartered in Rümlang, with extensive operations in safe locking systems, high-security vault locks, and integrated access control. The company serves financial institutions, hotels, and corporate campuses, combining physical security hardware with digital credentialing platforms across its European institutional product portfolio.

- Product Portfolio: High-security vault locks, electronic safe locks, and others

- Strategic Focus: dormakaba focuses on platform-based selling, embedding its vault and safe locking technology into broader access control and identity management ecosystems, targeting multi-site corporate clients and international hotel chains seeking unified security management across their European property networks.

Burg-Wächter

Burg-Wächter is a German security product manufacturer headquartered in Wetter (Ruhr), widely recognized across Europe for its broad portfolio of mechanical and electronic safes, key cabinets, deposit safes, and media safes. The company serves both residential and commercial markets with products certified to EN 14450 and EN 1143-1 standards, distributed across European retail, hardware, and professional security channels.

- Product Portfolio: The company offers Money safes, Hotelsafes, Freestanding home safe, media safes, deposit safes, key cabinets, gun safes, wall and floor safes, and others.

- Recent Developments: In September 2024, The Magno and Diplomat safe series recently achieved VSÖ certification, a recognized Austrian standard that validates high levels of security, quality, and reliability. This certification confirms that both product lines meet stringent requirements for burglary and fire protection, reinforcing their suitability for both residential and commercial use.

- Strategic Focus: Burg-Wächter focuses on value leadership across the European mid-market, offering certified products at accessible price points through its extensive distribution network spanning hardware stores, office furniture retailers, and professional security distributors, with growing emphasis on IoT-enabled products for commercial SMEs.

Market Concentration Analysis

The Europe safes and vaults market is moderately fragmented at the regional level, with no single company holding more than 10-12% of total European market revenue. Germany and France feature the highest market concentration among national champions, while the UK, Benelux, and Nordic markets are served by a mix of global security conglomerates and specialized local distributors. Asian manufacturers are gaining share in the mass-market residential and entry-level commercial segments on the basis of price.

Consolidation is occurring primarily through large security conglomerates — Gunnebo, ASSA ABLOY, dormakaba — acquiring niche regional specialists to expand product portfolios. The EU 2027 regulatory vault upgrade mandate is accelerating this trend, as smaller manufacturers lack the certification infrastructure and capital to efficiently meet institutional procurement requirements, creating M&A opportunities for well-capitalized industry leaders.

Investment & Growth Opportunities

Fastest-Growing Segments

Biometric safes at ~7.5% CAGR through 2034 represent the highest-growth product segment, driven by healthcare, luxury hospitality, and high-net-worth residential adoption of touchless biometric access. Electronic safes at ~5.2% CAGR offer the broadest-based commercial growth opportunity across retail, hospitality, and corporate applications, supported by falling component costs and increasing demand for digital audit trails.

Emerging Applications

Gold and precious metal vaulting services are emerging as a high-growth sub-sector, with IBV International Vaults London's April 2025 launch of IBV Gold illustrating sustained institutional investor demand for specialized bullion storage driven by geopolitical uncertainty. This trend creates greenfield opportunities for manufacturers developing EN 1143-1 Grade V-VI vault rooms with integrated inventory management and precious metal certification technology.

Venture & Investment Trends

Smart safe manufacturers integrating fintech payment reconciliation, real-time cash deposit crediting, and AI-powered cash forecasting are attracting private equity and corporate venture interest. The Cennox-Retail365 platform model demonstrates the value creation potential of safe-as-a-service recurring revenue, where software subscriptions and cash management service fees supplement traditional one-time hardware revenue with predictable income streams.

Future Market Outlook (2026-2034)

The Europe safes and vaults market is forecast to expand from USD 1,586.8 Million in 2025 to USD 2,416.9 Million by 2034 at a CAGR of 4.55%. This consistent growth reflects the market's regulatory-linked, non-discretionary demand characteristics across European financial and commercial security sectors.

Three structural forces will most significantly shape the European safes and vaults landscape through 2034: the EU regulatory compliance mandate creating a structured multi-year vault replacement wave across financial institutions; the smart safe platform economy where manufacturers evolve into recurring-revenue service providers; and the luxury and premium safe segment expanding as European wealth concentration and alternative asset investment in gold and collectibles accelerates bespoke security demand.

Research Methodology

Primary Research

Primary research encompassed structured interviews with European safes and vaults industry stakeholders, including senior commercial managers at major manufacturers, bank procurement managers, security consultants, insurance underwriters, and specialist distributors across Germany, France, the UK, and Italy. Primary data validated market sizing, type and end-user segment shares, country demand estimates, and technology adoption timelines across the 2020-2025 historical period.

Secondary Research

Key secondary sources include Europol European Serious and Organised Crime Threat Assessment, ECB Banking Supervision Annual Report, British Retail Consortium Retail Crime Survey 2025, EN 1143-1 and EN 14450 standard documentation, VdS certification database, ECB-S European Certification Body records, IMARC Group proprietary market databases, and trade publications including Security Management, Sicherheits Berater, and IFSEC International conference proceedings.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting models incorporating GDP growth rates, crime incidence indices, banking sector capital expenditure data, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty, with the base case reflecting the 4.55% CAGR trajectory supported by regulatory demand and technology adoption drivers.

Europe Safes and Vaults Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Electronic, Biometric, Mechanical |

| Function Types Covered | Cash Management Safes, Depository Safes, Gun Safes and Vaults, Vaults and Vault Doors, Media Safes, Others |

| Applications Covered | Residential, Commercial |

| End Users Covered | Banking Sector, Non Banking Sector |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | Gunnebo Safe Storage AB, ASSA ABLOY, dormakaba Group, Diebold Nixdorf, Incorporated, Burg-Wächter, Bordogna Casseforti, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe safes and vaults market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Europe safes and vaults market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe safes and vaults industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe Safes and Vaults Market Report

The Europe safes and vaults market reached USD 1,586.8 Million in 2025, growing from USD 1,270.5 Million in 2020, reflecting consistent demand from banking, retail, and residential security segments across major European economies.

The market is projected to reach USD 2,416.9 Million by 2034, growing at a CAGR of 4.55% during 2026-2034, driven by EU regulatory vault upgrades, smart safe adoption, and biometric technology penetration.

Mechanical safes lead with a 46.8% type share in 2025, valued for their reliability, power-independence, and cost-effectiveness across residential, SME, and regulated commercial applications throughout Europe, with particular strength in Central and Southern European markets.

The banking sector dominates at 58.9% in 2025, driven by mandatory vault infrastructure requirements for cash, gold, and document security across Europe's 5,000+ licensed credit institutions under ECB and national regulatory frameworks, creating substantial non-discretionary institutional procurement demand.

Germany commands a 24.7% country share in 2025, supported by its dense banking network, world-class safe manufacturing base including Burg-Wächter, and stringent security and insurance regulations mandating certified safe installations across commercial premises and financial institutions.

Leading companies include Gunnebo Safe Storage AB, ASSA ABLOY, dormakaba Group, Diebold Nixdorf, Incorporated, Burg-Wächter, Bordogna Casseforti, and others.

Key applications include banking vault rooms, retail cash management, hotel in-room safes, healthcare controlled-substance and record storage, residential precious item and firearm protection, government and corporate document security, and specialized precious metal vaulting for investment-grade gold and silver storage.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)