Europe Semiconductor Market Size, Share, Trends and Forecast by Components, Material Used, End User, and Country, 2026-2034

Europe Semiconductor Market Size, Share, Trends & Forecast (2026-2034)

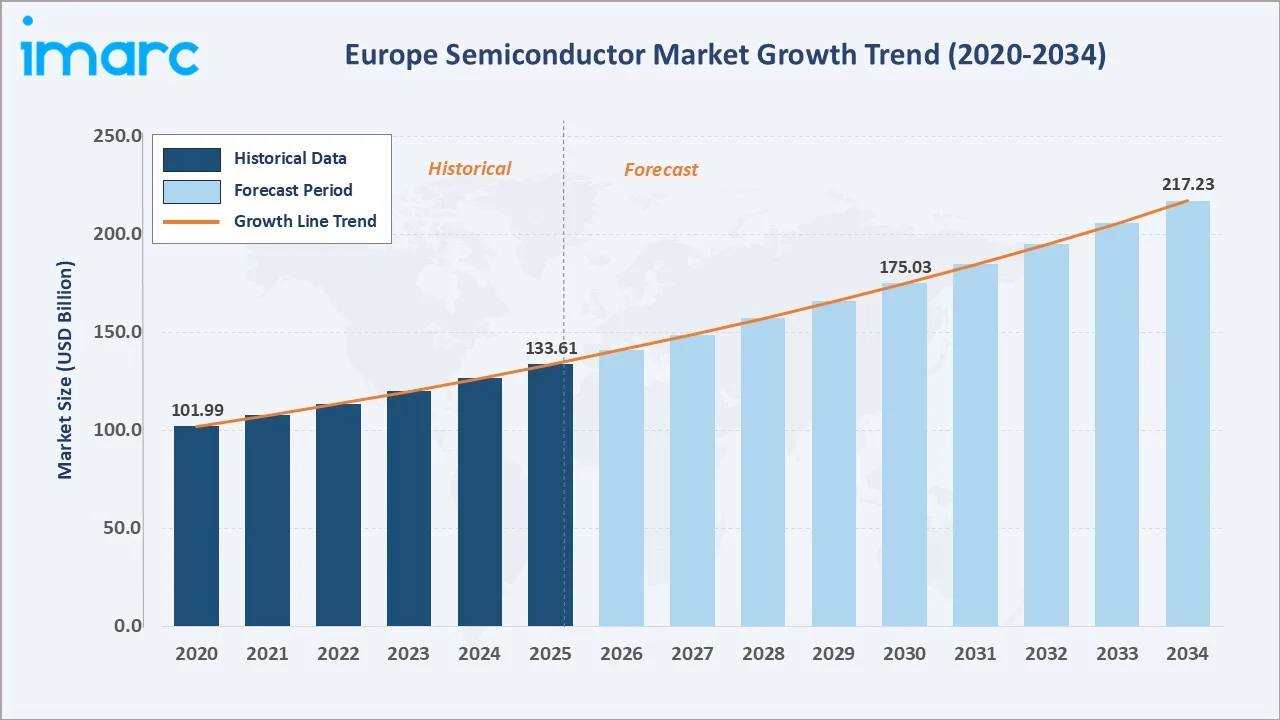

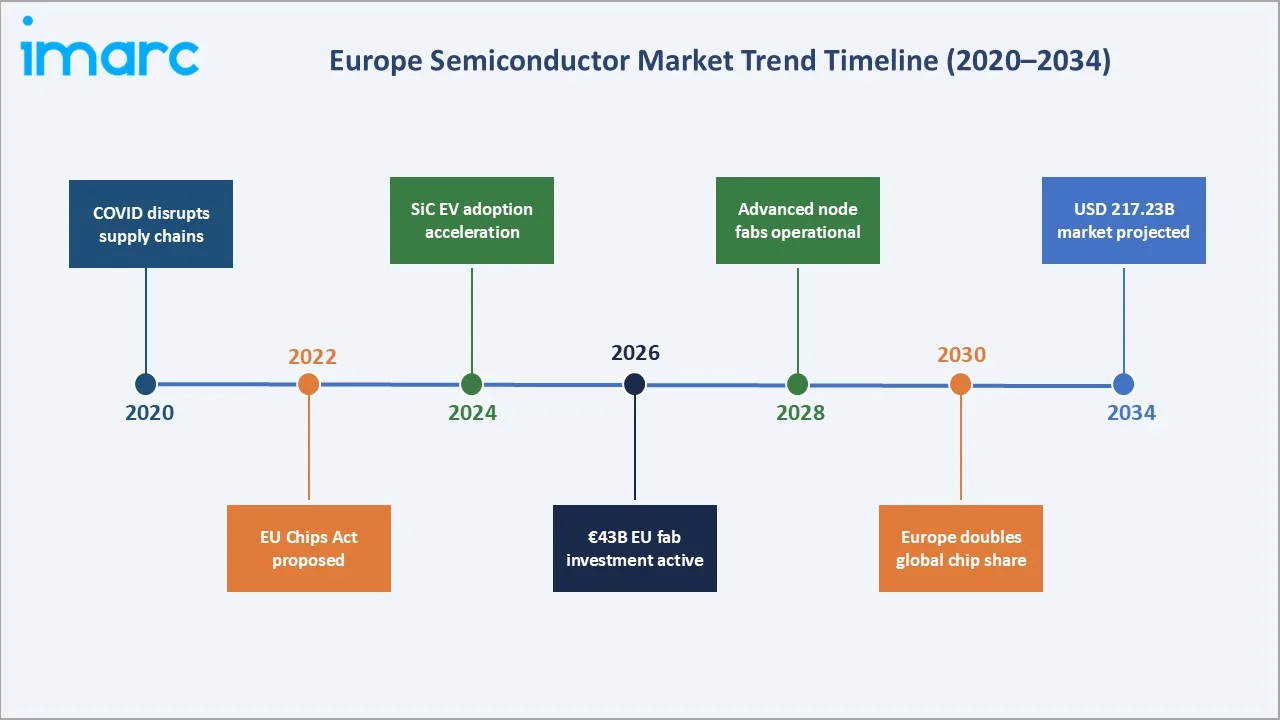

The Europe semiconductor market size reached USD 133.61 Billion in 2025 and is projected to reach USD 217.23 Billion by 2034, exhibiting a CAGR of 5.55% during 2026-2034. The EU Chips Act mobilising €43 billion in public and private funding, accelerating EV adoption driving silicon carbide demand, and 5G/IoT proliferation are the primary forces driving the Europe semiconductor market growth.

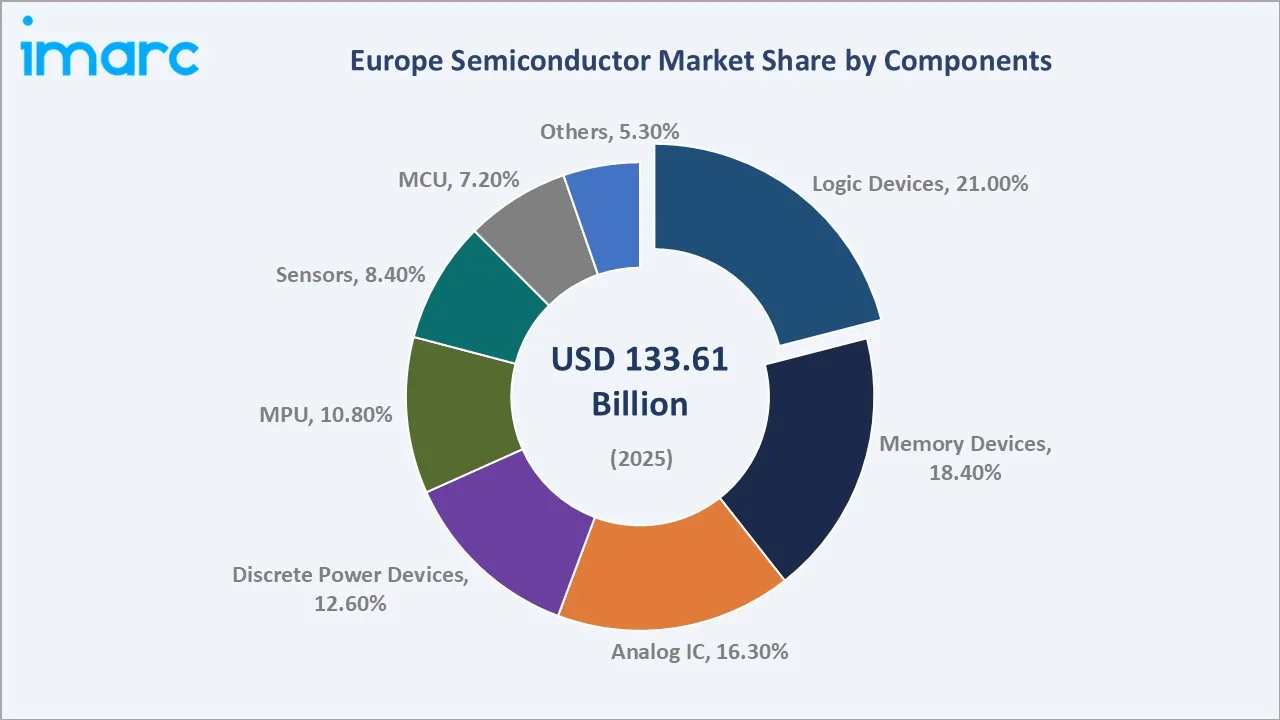

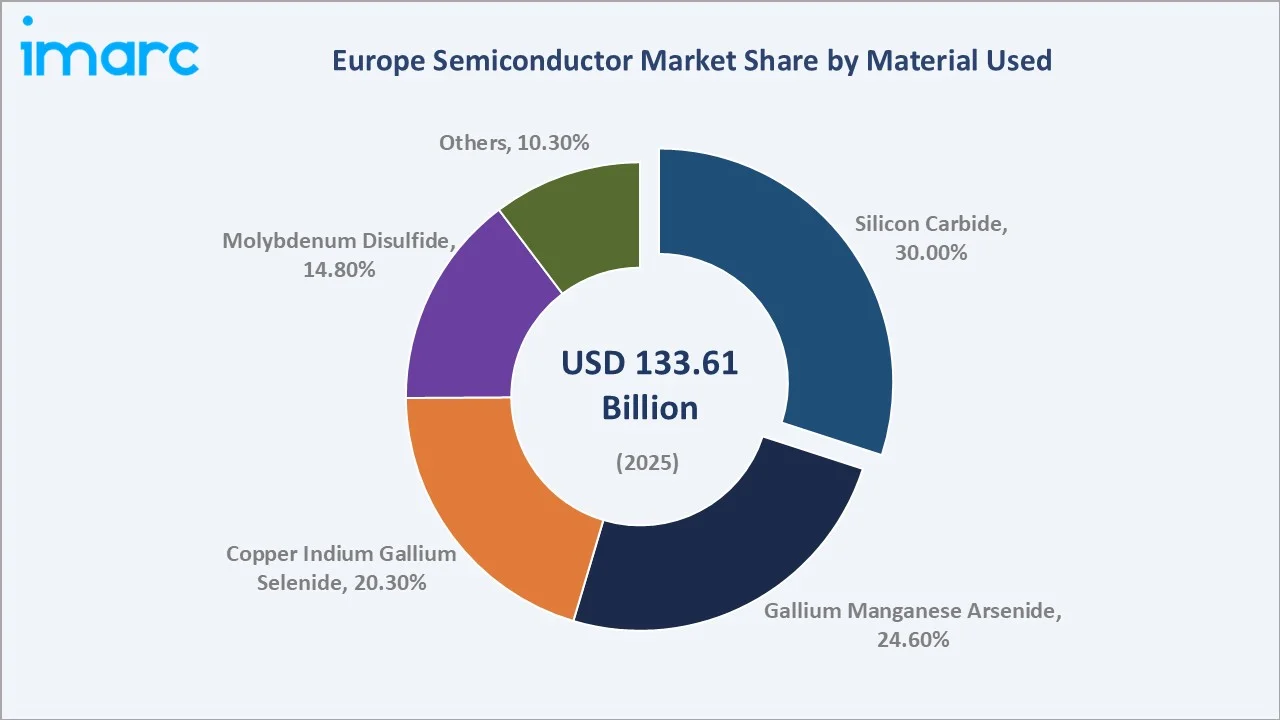

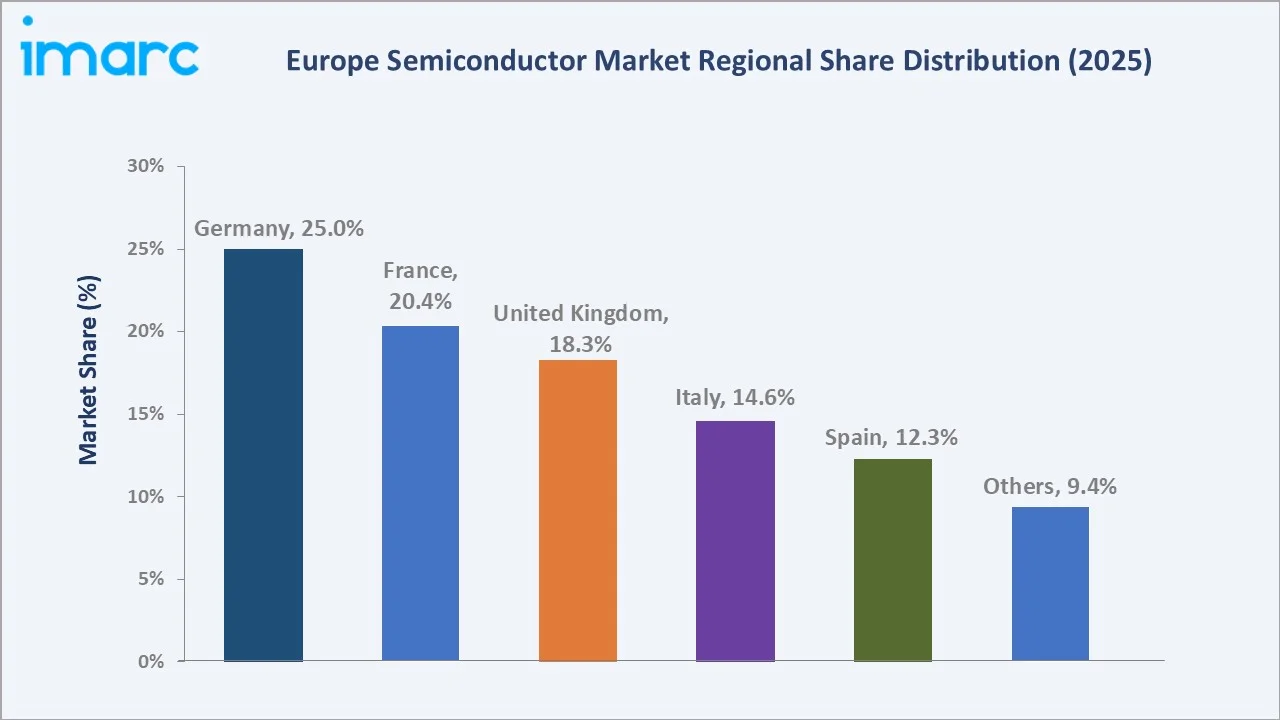

Logic Devices dominate the components mix at 21.0% in 2025, while Silicon Carbide leads the materials segment at 30.0%. Germany commands a 25.0% country share in 2025, underpinned by its automotive semiconductor ecosystem.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 133.61 Billion |

|

Forecast Market Size (2034) |

USD 217.23 Billion |

|

CAGR (2026-2034) |

5.55% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

Germany (25.0% share, 2025) |

|

Second Country |

France (20.4% share, 2025) |

|

Leading Component |

Logic Devices (21.0%, 2025) |

|

Leading Material |

Silicon Carbide (30.0%, 2025) |

To get more information on this market, Request Sample

The Europe semiconductor market growth trajectory from 2020 through 2034, with the historical expansion to USD 133.61 Billion in 2025, reflects consistent policy-driven demand, while the forecast to USD 217.23 Billion captures accelerating EU Chips Act investment, electrification, and digital infrastructure expansion.

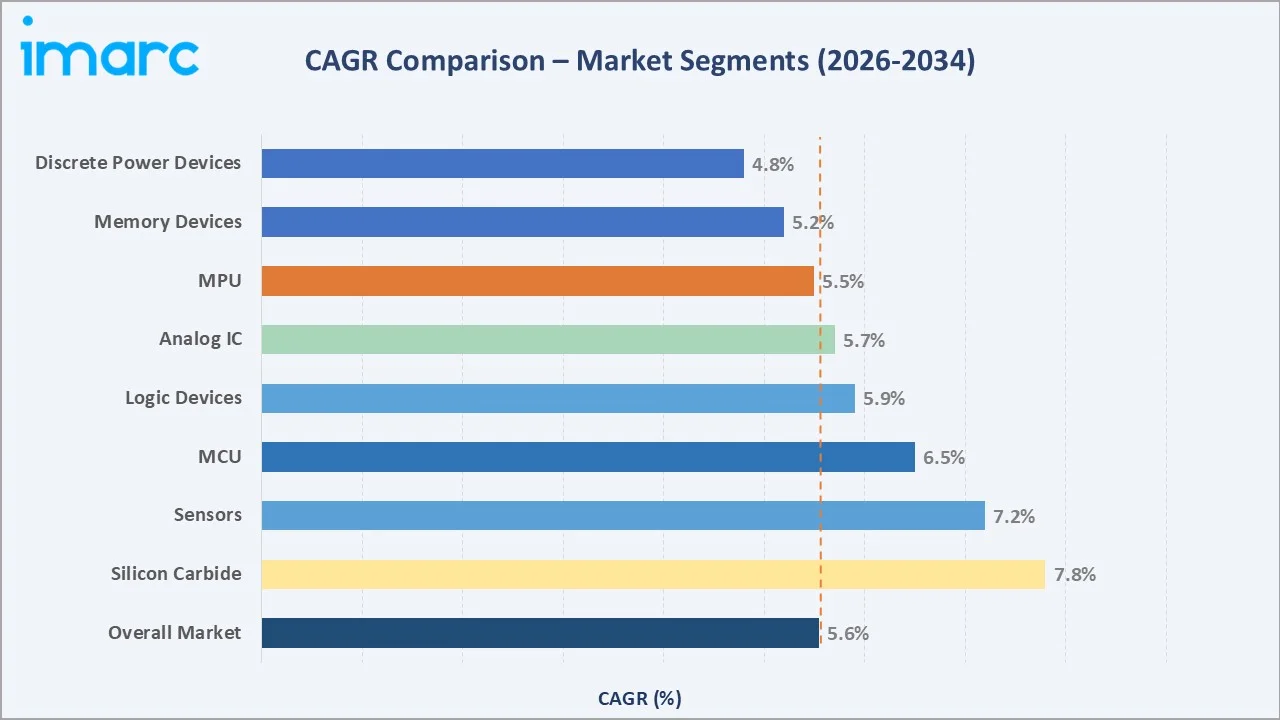

The CAGR trajectories across key components and material sub-segments, with Silicon Carbide at ~7.8% CAGR and Sensors at ~7.2% CAGR, are the fastest-growing categories within the Europe semiconductor industry analysis through 2034.

Executive Summary

The Europe semiconductor market is on a sustained growth trajectory from USD 133.61 Billion in 2025 to USD 217.23 Billion by 2034. Semiconductors, the foundational components enabling modern electronics, power systems spanning automotive, industrial automation, telecommunications, and consumer electronics.

Logic Devices dominate the components mix at 21.0% in 2025, driven by widespread integration in industrial automation and advanced computing. Memory Devices (18.4%) and Analog IC (16.3%) follow, underpinned by expanding data centre and IoT infrastructure across the region.

Silicon Carbide leads the materials segment at 30.0% in 2025, owing to its high thermal conductivity and performance in EV power electronics. Gallium Manganese Arsenide (24.6%) supports high-frequency RF applications in 5G infrastructure, while Copper Indium Gallium Selenide (20.3%) serves photovoltaic and thin-film applications.

Germany commands 25.0% in 2025, supported by automotive OEM semiconductor procurement. France (20.4%) and the United Kingdom (18.3%) follow, driven by defence electronics and financial-sector data infrastructure respectively.

Key Market Insights

|

Insight |

Data |

|

Largest Component |

Logic Devices – 21.0% share (2025) |

|

Leading Material |

Silicon Carbide – 30.0% share (2025) |

|

Leading Country |

Germany – 25.0% revenue share (2025) |

|

Second Country |

France – 20.4% revenue share (2025) |

|

Top Companies |

Infineon Technologies AG, STMicroelectronics, ASML, NXP Semiconductors, Texas Instruments Incorporated, Micron Technology, Inc. |

Key Analytical Observations Expanding On The Above Data:

- Logic Devices, with 21.0% in 2025, dominate because they constitute the processing backbone across industrial automation, 5G base stations, and advanced computing platforms widely adopted across Europe's manufacturing and technology sectors.

- Silicon Carbide, with 30.0% in 2025, leads due to its critical role in EV traction inverters and renewable energy power electronics. European automotive OEMs and Tier-1 suppliers have mandated SiC for next-generation 800V battery architectures.

- Germany's 25.0% dominance reflects its status as Europe's largest automotive market. ACEA data shows German OEMs account for over 30% of European EV production, generating substantial semiconductor procurement from domestic and global chip suppliers.

- France, with 20.4% in 2025, benefits from strategic government investments under France 2030, targeting semiconductor R&D and advanced electronics manufacturing through STMicroelectronics and Soitec capacity expansions.

Europe Semiconductor Market Overview

A semiconductor is a material with electrical conductivity intermediate between conductors and insulators, enabling precisely controlled electron flow through doping, junction formation, and gate modulation. These properties underpin all integrated circuits, from simple logic gates to multi-billion transistor system-on-chip designs.

The European semiconductor ecosystem integrates raw material suppliers, wafer fabricators, fabless design houses, integrated device manufacturers, packaging and testing specialists, equipment manufacturers, and end-use industries spanning automotive, industrial, telecommunications, and consumer electronics.

Market Dynamics

To evaluate market opportunities, Request Sample

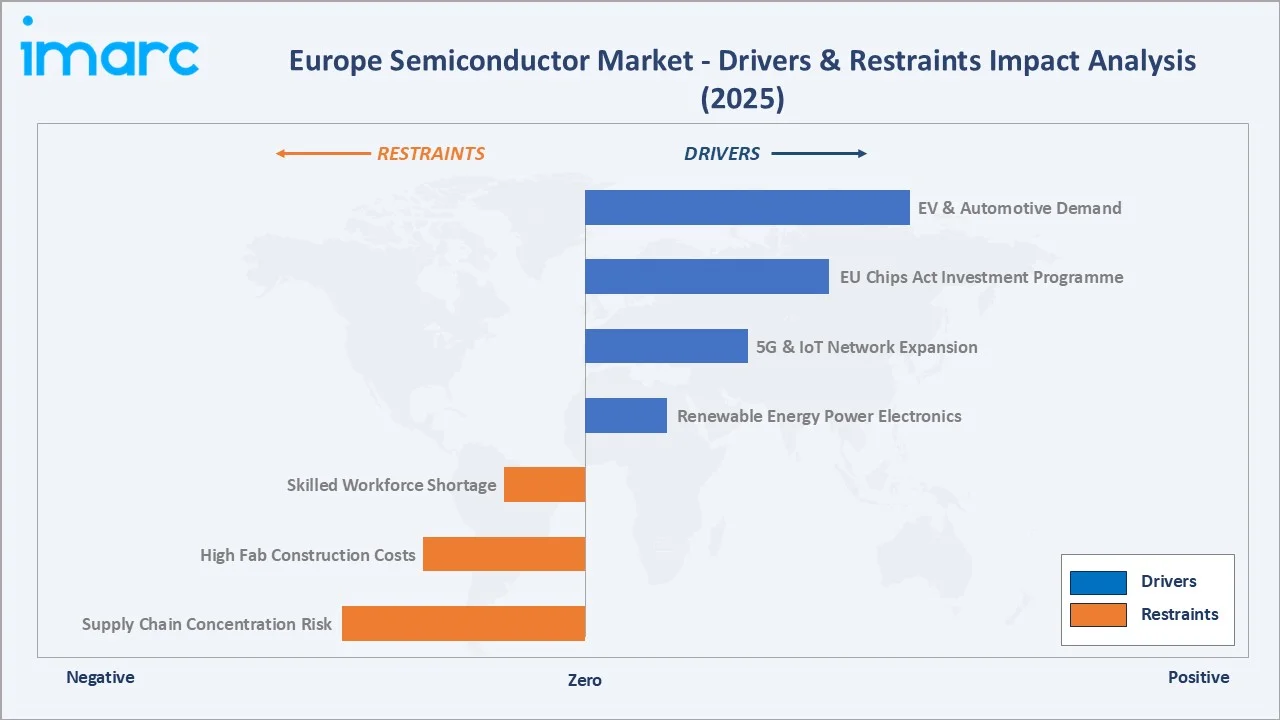

Market Drivers

- Electric Vehicle and Automotive Electrification: Europe's automotive sector is transitioning to EVs at scale, with the EU mandating zero-emission new car sales by 2035. Each BEV requires 2–3x semiconductor content compared to ICE vehicles, particularly SiC power devices and automotive-grade microcontrollers.

- EU Chips Act Investment Programme: The European Chips Act mobilises €43 billion in combined public and private investment to double Europe's share of global semiconductor production to 20% by 2030. This has catalysed fab announcements from TSMC in Dresden and Infineon's SiC expansion in Germany.

- 5G Network Rollout and IoT Proliferation: For 2030, the Digital Decade Policy Programme (DDPP) sets clear targets for digital maturity across the EU, including that 100% of populated areas have access to 5G services. At the end of 2024, 5G population coverage across the EU’s 27 Member States was 94.3%, with 79.6% in rural areas, thereby is driving demand for RF semiconductors, baseband processors, and low-power MCUs for connected device applications.

Market Restraints

- Supply Chain Concentration and Geopolitical Risk: Europe remains dependent on Taiwan and South Korea for advanced logic fabrication. Any disruption to these supply nodes creates significant risk for European automotive and industrial OEMs with limited domestic leading-edge alternatives.

- High Fabrication Facility Costs: Building advanced semiconductor fabrication plants requires extremely high capital investment, often running into tens of billions of dollars, which creates a major barrier for regions trying to develop domestic manufacturing capabilities. These costs include not just construction, but also expensive equipment, cleanroom infrastructure, and ongoing upgrades to keep up with rapid technological advancements. As a result, even with government incentives, scaling up competitive manufacturing remains financially challenging and risky.

Market Opportunities

- Power Semiconductor Leadership for Renewable Energy: Europe's aggressive renewable energy targets, with the EU aiming for 45% renewables by 2030, create sustained demand for wide-bandgap semiconductors in solar inverters, wind turbine converters, and grid-scale storage power electronics.

- Automotive-Grade Chip Localisation: European automotive OEMs are actively pursuing supply chain regionalisation post-pandemic. Nearshore semiconductor sourcing from European or European-allied fabs commands a premium and offers design partnership opportunities for European chip houses.

Market Challenges

- Semiconductor Talent and Skills Gap: The semiconductor industry faces a significant shortage of skilled professionals, particularly in specialized domains such as design, manufacturing, and process engineering. This talent gap limits innovation capacity and slows down both research and production activities. The issue is further compounded by the highly technical nature of the field, which requires years of training and experience. Without sustained investment in education and workforce development, this shortage is likely to persist and constrain industry growth.

- Export Controls and Technology Access Restrictions: US and allied export controls on semiconductor equipment and advanced chip technology create compliance complexity for European companies operating globally, particularly those serving dual-use industrial and defence markets.

Emerging Market Trends

1. Silicon Carbide Adoption Accelerating Across European Automotive OEMs

Infineon's CoolSiC and STMicroelectronics's SiC MOSFET platforms are being designed into 800V EV architectures across BMW, Mercedes-Benz, Stellantis, and Renault platforms. Multi-year supply agreements are locking in SiC capacity years in advance, compressing market access windows for new entrants.

2. EU Chips Act Reshaping Competitive Dynamics and Fab Investment

The European Semiconductor Manufacturing Company joint venture in Dresden broke ground in 2024 with €5 billion in German federal support. This initiative fundamentally alters the competitive landscape by creating domestic supply for automotive grade 22nm and 28nm logic chips in Europe.

3. Chiplet Architecture and Advanced Packaging Gaining Traction

European research consortia led by imec are pioneering chiplet integration standards that allow semiconductor components from different manufacturers to interoperate. This enables European fabless companies to compete with monolithic designs by integrating best-in-class IP blocks.

4. AI-Optimised Semiconductor Design for Industrial Automation

European industrial automation leaders such as Siemens, Bosch, and ABB are demanding application-specific AI inference chips with deterministic latency profiles suited for real-time process control, creating a demand pull for custom European chip design activity.

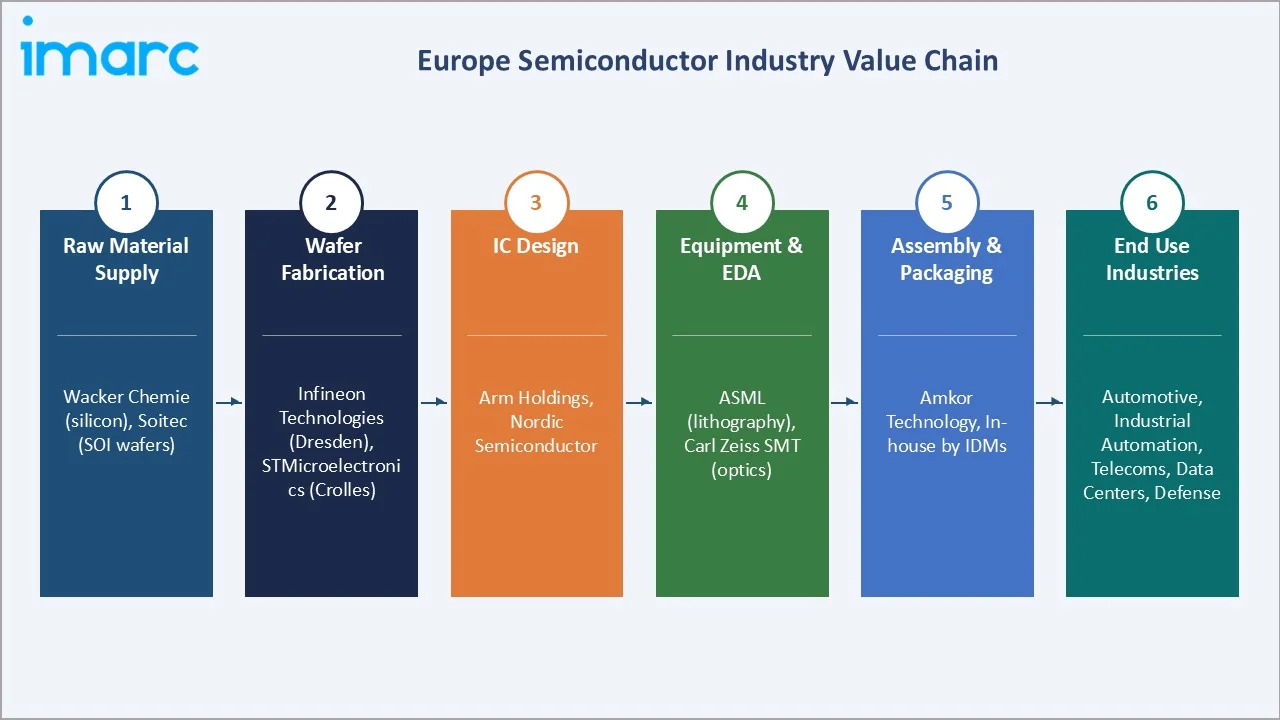

Industry Value Chain Analysis

The European semiconductor value chain spans six stages from raw material supply through end-use deployment. Wafer fabrication and equipment manufacturing capture the highest value-add margins, with ASML's lithography systems representing a unique global monopoly held within Europe.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Wacker Chemie (silicon), Soitec (SOI wafers) |

|

Wafer Fabrication |

Infineon Technologies (Dresden), STMicroelectronics (Crolles) |

|

IC Design |

Arm Holdings, Nordic Semiconductor (fabless design) |

|

Equipment & EDA |

ASML (lithography), Carl Zeiss SMT (optics) |

|

Assembly & Packaging |

Amkor Technology, in-house by IDMs |

|

End Use Industries |

Automotive, Industrial Automation, Telecoms, Data Centres, Defence |

Integrated device manufacturers with captive wafer fabrication and in-house packaging capabilities, such as Infineon and STMicroelectronics, achieve lower total cost structures than pure fabless companies dependent on TSMC and Samsung foundry services.

Technology Landscape in the Europe Semiconductor Industry

Wide-Bandgap Semiconductor Technology: SiC and GaN

Silicon carbide MOSFETs rated at 650V to 1700V are displacing silicon IGBTs in EV inverter, industrial motor drive, and railway traction applications across Europe. GaN-on-Silicon HEMTs are gaining traction in data centre power supply and wireless charging applications.

Advanced Node Lithography and EUV Expansion

ASML's High-NA EUV lithography systems, priced above USD 350 million per unit, enable sub-2nm patterning and will form the foundation of next-generation European logic fab investment. ASML holds a global monopoly on EUV systems, making it the most strategically significant European semiconductor company.

Heterogeneous Integration and 3D Packaging

European research institutes including imec, Fraunhofer IIS, and CEA-Leti are advancing 3D chip stacking, through-silicon via interconnects, and embedded die packaging. These technologies enable performance scaling without relying solely on transistor shrink.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Components |

Logic Devices |

21.0% |

2025 |

|

Material Used |

Silicon Carbide |

30.0% |

2025 |

|

End User |

Consumer Electronics |

62.24% |

2025 |

|

Country |

Germany |

250% |

2025 |

By Components

To access detailed market analysis, Request Sample

Logic Devices command a 21.0% majority share in 2025 owing to their role as the processing core across industrial PLCs, automotive ECUs, telecommunications base stations, and enterprise computing. Application-specific integrated circuits designed for European automotive and industrial applications represent the primary Logic Device category.

Memory Devices at 18.4% in 2025 support data-intensive industrial automation, automotive ADAS stacks, and edge computing infrastructure. Analog IC at 16.3% serves power management, signal conditioning, and sensor interface applications. Discrete Power Devices (12.6%) are critical for EV power trains and industrial drives. MPU (10.8%), Sensors (8.4%), MCU (7.2%), and Others (5.3%) complete the components landscape.

By Material Used

Silicon Carbide dominates the materials segment at 30.0% in 2025, driven by its irreplaceable performance advantages in high-voltage, high-temperature power conversion applications. Europe's EV manufacturing concentration and renewable energy investment have accelerated SiC adoption beyond global averages, making it the defining semiconductor material of the current investment cycle.

Gallium Manganese Arsenide at 24.6% underpins high-frequency amplifiers and RF power devices in 5G infrastructure. Copper Indium Gallium Selenide at 20.3% serves thin-film solar cell and photovoltaic power conversion applications. Molybdenum Disulfide (14.8%) is an emerging 2D semiconductor material for next-generation transistors. Others account for 10.3%.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

Germany |

25.0% |

Automotive OEM SiC demand; Infineon fab expansion; TSMC Dresden; EV transition |

|

France |

20.4% |

STMicroelectronics Crolles expansion; France 2030 semiconductor R&D; Soitec SOI wafers |

|

United Kingdom |

18.3% |

Arm Holdings IP licensing; data centre semiconductor demand; defence electronics |

|

Italy |

14.6% |

STMicroelectronics Catania SiC fab; industrial automation semiconductor demand |

|

Spain |

12.3% |

Renewable energy power electronics; telecom infrastructure; EV manufacturing ramp-up |

|

Others |

9.4% |

Netherlands (ASML equipment); Sweden (Ericsson 5G chips); Finland (Nokia RF) |

Germany's 25.0% market dominance in 2025 is driven by its position as Europe's largest automotive producer and most advanced industrial automation market. The ESMC joint venture fab in Dresden, backed by EUR 5 billion in German state aid, is the most significant domestic semiconductor capacity addition in European history.

France, with 20.4% in 2025, benefits from the France 2030 plan's EUR 6 billion semiconductor allocation and STMicroelectronics's Crolles facility expansion targeting 300mm FD-SOI production. The United Kingdom (18.3%) leverages Arm Holdings' global IP licensing revenues and growing hyperscale data centre semiconductor procurement.

Competitive Landscape

The Europe semiconductor market is fragmented, with European-headquartered IDMs holding strong positions in power electronics and automotive segments, while global leaders such as Intel, Samsung, and Micron compete across the full spectrum of logic, memory, and foundry services.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

Infineon Technologies AG |

CoolSiC MOSFETs, AURIX MCU, AIROC Connected MCU |

Leader |

Europe leader in automotive & industrial power; SiC expansion |

|

STMicroelectronics |

SiC MOSFETs, STM32 MCU |

Leader |

European IDM; automotive & IoT; FD-SOI platform |

|

ASML |

EUV & DUV Lithography Systems |

Leader |

Global monopoly in EUV; enabler of all advanced nodes |

|

NXP Semiconductors |

MCX Series, i.MX processors |

Leader |

Automotive & secure connectivity; global presence |

|

Texas Instruments Incorporated |

Microcontrollers (MCUs) & processors, DSPs, Analog ICs |

Challenger |

Analog & embedded processing; European industrial focus |

|

Micron Technology, Inc. |

DDR5 DRAM, Memory Devices, HBM3E/HBM4 |

Challenger |

Memory & storage; data centre DRAM supply to Europe |

Key players include Infineon Technologies AG, STMicroelectronics, ASML, NXP Semiconductors, Texas Instruments Incorporated, Micron Technology, Inc., and others.

Key Company Profiles

Infineon Technologies AG

Infineon Technologies AG is one of the Europe's largest semiconductor companies by revenue, headquartered in Munich, Germany. Infineon specialises in power semiconductors, automotive-grade microcontrollers, and security ICs, with leading global positions in SiC MOSFETs and automotive ECU chips.

- Product Portfolio: The company offers CoolSiC MOSFETs, AURIX MCU, AIROC Connected MCU, and others.

- Recent Developments: In February 2025, Under the EU Chips Act, Infineon Technologies AG secured approval for public funding to expand semiconductor manufacturing capacity in Europe, including the development of an advanced fabrication facility in Dresden. This initiative is aimed at strengthening Europe’s position in the global semiconductor supply chain while supporting key sectors such as automotive, industrial, and energy-efficient technologies.

- Strategic Focus: Infineon's strategy centres on SiC leadership for EV and renewable energy, expanding its Dresden fab to achieve cost parity with silicon IGBTs in key power ranges, while defending its automotive MCU dominance through AURIX functional safety certifications.

STMicroelectronics

STMicroelectronics is a global semiconductor company with European operational and R&D headquarters, serving automotive, industrial, IoT, and consumer markets. ST's unique FD-SOI process technology, manufactured at its Crolles facility in France, is a competitive differentiator in low-power, radiation-hardened applications.

- Product Portfolio: SiC MOSFETs, STM32 MCU

- Recent Developments: In June 2023, STMicroelectronics partnered with Sanan Optoelectronics to establish a joint venture focused on high-volume production of silicon carbide (SiC) devices in China, aimed at meeting growing demand in automotive electrification and industrial energy applications. The project includes the construction of a 200mm wafer fabrication facility, expected to begin production by 2025 and expand further by 2028, supported by significant capital investment and local funding.

- Strategic Focus: ST's dual-track strategy targets SiC leadership in automotive power electronics while maintaining IoT and industrial microcontroller design-win momentum through the STM32 ecosystem, the world's largest embedded developer community.

ASML

ASML is the world's sole manufacturer of extreme ultraviolet lithography systems, headquartered in Veldhoven, Netherlands. ASML's EUV systems are essential for manufacturing semiconductor chips below the 7nm node, making ASML the most strategically critical company in the global semiconductor supply chain.

- Product Portfolio: EUV & DUV Lithography Systems

- Recent Developments: In March 2025, ASML Holding N.V. and imec entered a five-year strategic partnership aimed at advancing semiconductor research and promoting sustainable innovation in Europe. The collaboration brings together their combined expertise to develop next-generation chip technologies, including sub-2nm nodes, by leveraging ASML’s full portfolio of advanced lithography and metrology systems within imec’s pilot line infrastructure.

- Strategic Focus: ASML's strategy focuses on High-NA EUV system commercialisation to sustain Moore's Law scaling, while managing export control compliance complexity as it navigates US-China technology restrictions affecting China-bound DUV shipments.

Market Concentration Analysis

The Europe semiconductor market is moderately concentrated at the European level, with Infineon and STMicroelectronics as clear regional leaders in power and automotive segments, while no single company holds more than 8–10% of total European market revenue across all segments.

Consolidation through M&A in European semiconductor equipment and materials is more advanced than end-product consolidation. Carl Zeiss's optics for ASML EUV systems and Siltronic's silicon wafer supply represent concentrated chokepoints in the European semiconductor supply chain with limited near-term substitutability.

Investment & Growth Opportunities

Fastest-Growing Segments

Silicon Carbide at ~7.8% CAGR through 2034 is the highest-growth material segment, driven by European EV production mandates and renewable energy power conversion. Sensors at ~7.2% CAGR represent the fastest-growing component, driven by ADAS, industrial IoT, and smart manufacturing adoption across German and French industry.

Emerging Markets

Spain and Italy are the fastest-growing markets within Europe for semiconductor demand through 2034. Spain's renewable energy buildout and emerging EV manufacturing, combined with Italy's STMicroelectronics SiC fab in Catania, are creating localised semiconductor demand clusters.

Venture & Investment Trends

The EU Chips Act joint undertaking Chips for Europe is allocating EUR 1.67 billion to semiconductor R&D across imec, Fraunhofer, and national research institutes. Venture investment in European fabless semiconductor design companies reached record levels in 2024, with automotive AI chip and edge inference startups attracting the largest funding rounds.

Future Market Outlook (2026-2034)

The Europe semiconductor market is forecast to expand from USD 133.61 Billion in 2025 to USD 217.23 Billion by 2034 at a CAGR of 5.55%.

Three forces will most significantly shape the Europe semiconductor landscape through 2034. The EU Chips Act's EUR 43 billion investment programme will deliver multiple new 300mm fabs by 2028, fundamentally reducing Europe's dependence on Asian foundry services for automotive and industrial chips.

Artificial intelligence semiconductor demand across European data centres and edge industrial applications will add a second growth vector, requiring European companies to develop AI inference chip capabilities competitive with US and Asian alternatives.

Research Methodology

Primary Research

Primary research encompassed over 50 structured interviews with European semiconductor industry stakeholders, including senior commercial managers at Infineon, STMicroelectronics, and NXP, European Semiconductor Industry Association (ESIA) representatives, automotive OEM procurement specialists, and investment analysts covering European technology.

Secondary Research

Key secondary sources include ESIA European Semiconductor Industry Data (2020–2025), SEMI Europe market statistics, European Commission Chips Act implementation reports, ACEA European Automobile Manufacturers' Association EV data, Eurostat industrial production statistics, and IEEE and VLSI symposia publications.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting models, incorporating GDP growth rates, automotive production forecasts, EU industrial policy timelines, and historical semiconductor market elasticity patterns. Scenario analysis was performed across base, optimistic, and conservative cases.

Europe Semiconductor Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Memory Devices, Logic Devices, Analog IC, MPU, Discrete Power Devices, MCU, Sensors,Others |

| Materials Used Covered | Silicon Carbide, Gallium Manganese Arsenide, Copper Indium Gallium Selenide, Molybdenum Disulfide, Others |

| End Users Covered | Automotive, Industrial, Data Center, Telecommunication, Consumer Electronics, Aerospace and Defense, Healthcare, Others |

| Countries Covered | Germany, France, the United Kingdom, Italy, Spain, Others |

| Companies Covered | Infineon Technologies AG, STMicroelectronics, ASMLm, NXP Semiconductors, Texas Instruments Incorporated, Micron Technology, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe Semiconductor Market Report

The Europe semiconductor market reached USD 133.61 Billion in 2025, reflecting consistent demand from automotive electrification, industrial automation, and EU-funded digital infrastructure investment.

The market is projected to reach USD 217.23 Billion by 2034, growing at a CAGR of 5.55% during 2026-2034, driven by EV adoption, EU Chips Act capacity expansion, 5G rollout, and AI infrastructure investment.

Logic Devices lead with a 21.0% component share in 2025, driven by demand from automotive ECUs, industrial automation controllers, and advanced computing applications across the region.

Silicon Carbide leads at 30.0% in 2025, driven by EV traction inverter adoption and renewable energy power electronics. European automotive OEMs have committed to SiC-based 800V architectures in next-generation platforms.

Germany commands a 25.0% share in 2025, driven by its automotive OEM semiconductor demand, Infineon’s home market leadership, and the TSMC Dresden fab investment backed by EUR 5 billion in German federal funding.

Leading companies include Infineon Technologies AG, STMicroelectronics, ASML, NXP Semiconductors, Texas Instruments Incorporated, Micron Technology, Inc., and others.

Silicon Carbide is the fastest-growing material at ~7.8% CAGR through 2034, driven by EV power electronics mandates and renewable energy conversion applications where no viable silicon substitute exists.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade