Europe Two-Wheeler Market Size, Share, Trends and Forecast by Vehicle Type, Motor Type, Engine Capacity, Transmission, and Country, 2026-2034

Europe Two-Wheeler Market Size, Share, Trends & Forecast (2026-2034)

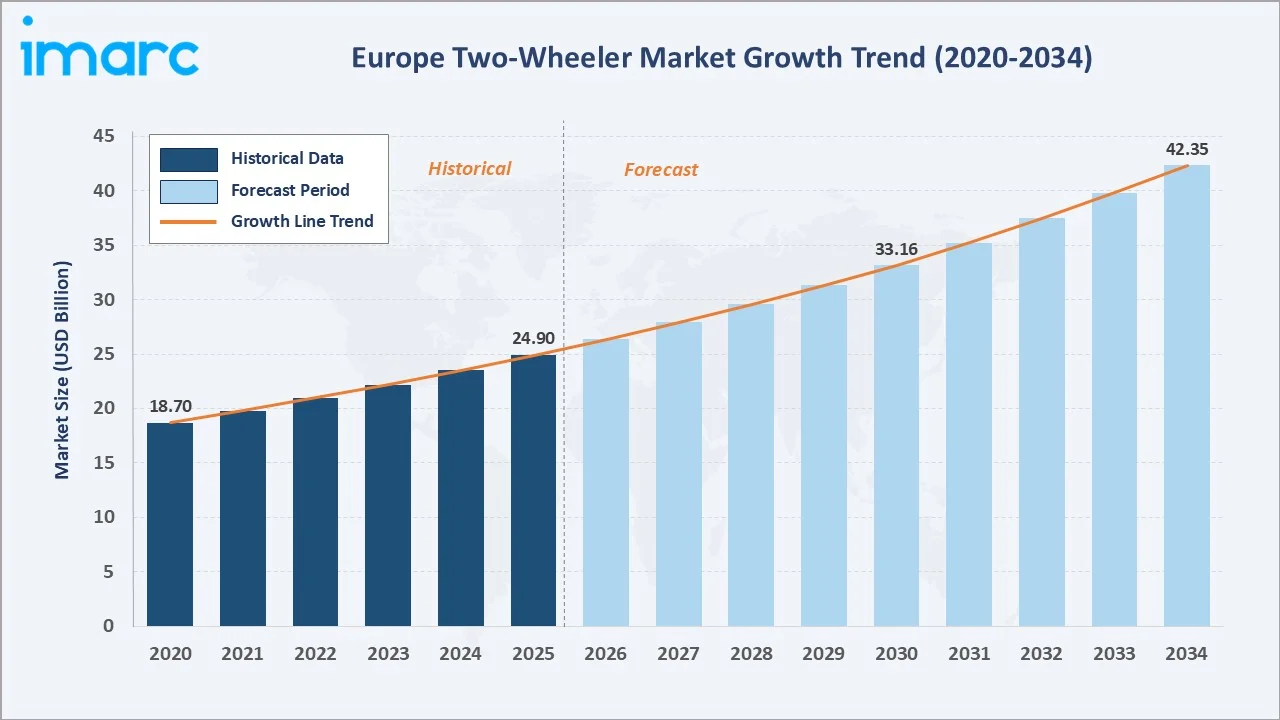

The Europe two-wheeler market reached USD 24.90 Billion in 2025 and is projected to reach USD 42.35 Billion by 2034, growing at a CAGR of 5.90% during 2026-2034. The expansion of urban micromobility, accelerating electrification of mopeds and scooters under EU Green Deal mandates, the Euro 5+ emissions transition reshaping product portfolios, and rising last-mile delivery demand are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 24.90 Billion |

|

Forecast Market Size (2034) |

USD 42.35 Billion |

|

CAGR (2026-2034) |

5.90% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

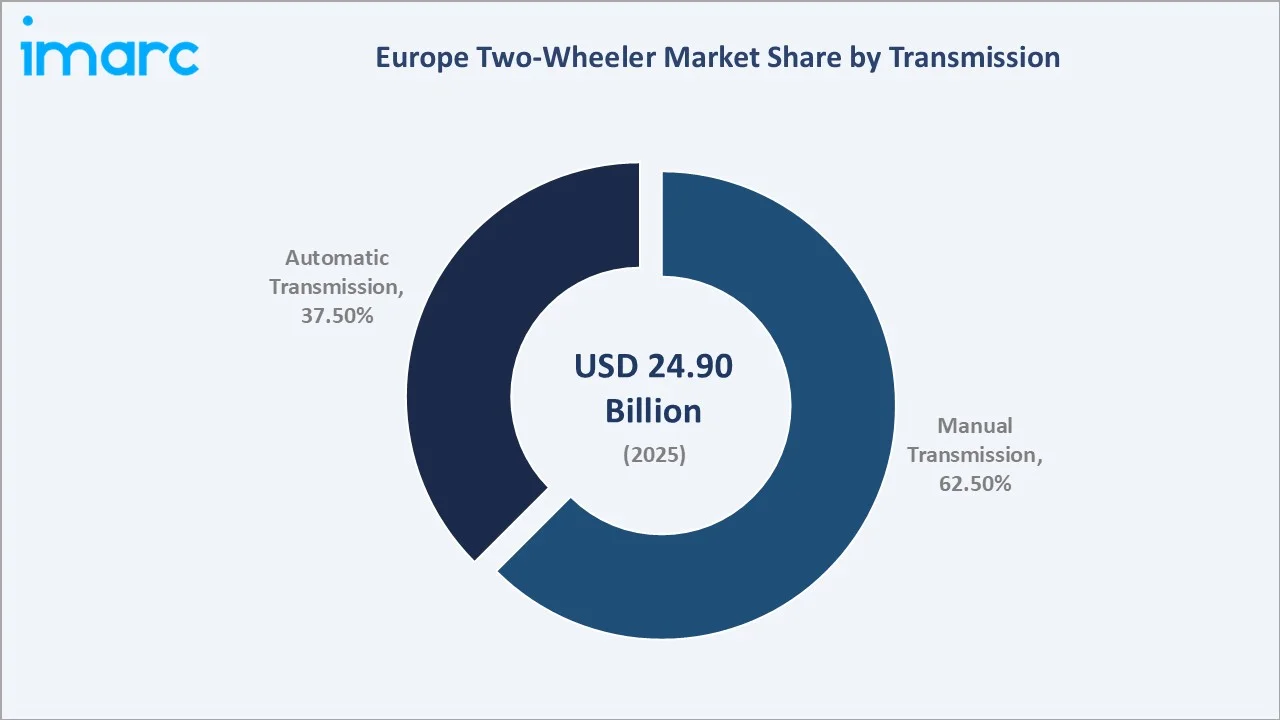

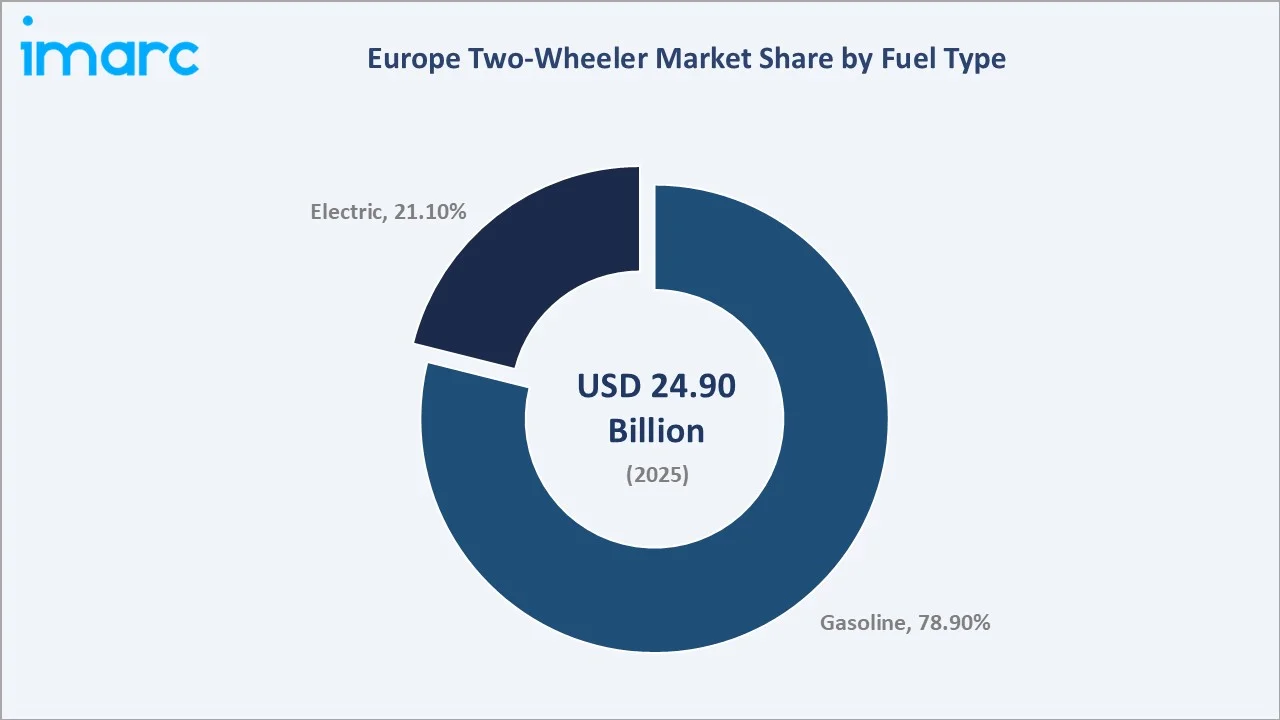

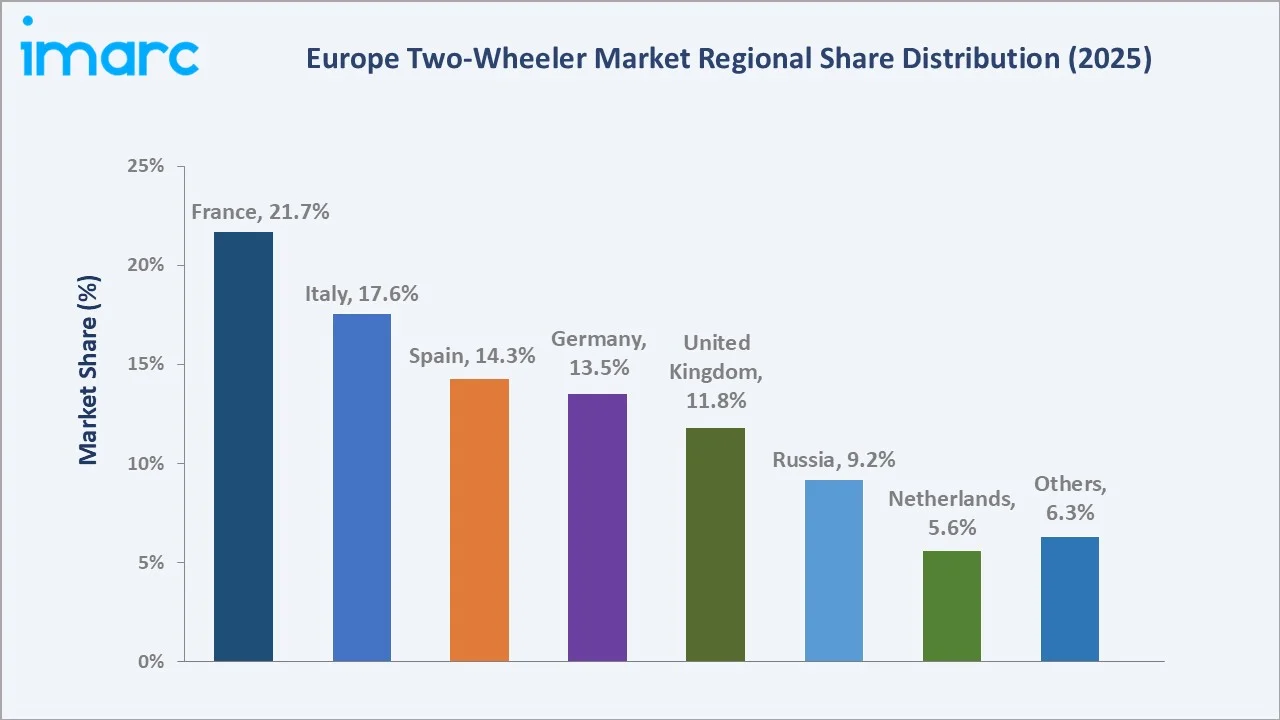

France leads the region at 21.7% in 2025, supported by Paris' large scooter culture and aggressive enforcement of low-emission zones. Italy follows at 17.6%, anchored by an entrenched two-wheeler commuting culture and Piaggio's domestic manufacturing base. Manual transmission products account for 62.5% of the breakdown by transmission, while gasoline models dominate the fuel-type mix at 78.9%, though electric two-wheelers are rapidly closing the gap.

To get more information on this market, Request Sample

Europe's two-wheeler market is underpinned by three structural forces: the region's shift toward decarbonized urban mobility under the EU Green Deal, the accelerating electrification of mopeds and small scooters driven by city access restrictions, and a generational expansion of premium leisure motorcycling. Each force broadens addressable demand, collectively sustaining a 5.90% CAGR through 2034 despite cyclical post-Euro 5+ corrections in 2025.

Executive Summary

The Europe two-wheeler market was valued at USD 24.90 Billion in 2025 and is forecast to reach USD 42.35 Billion by 2034, growing at a CAGR of 5.90%. This trajectory is anchored by ACEM-reported registrations of 1,002,848 units across the five European countries in 2025, Europe's over 39 million motorcycles and scooters operating in 2024, and an accelerating share of electric models in commuter categories.

Manual transmission dominates with a 62.5% share in 2025, reflecting European riders' preference for performance-oriented motorcycles and the persistent strength of premium leisure segments. Automatic transmission, at 37.5%, is expanding faster as urban scooters, electric mopeds, and CVT commuter models gain traction in cities such as Paris, Rome, and Madrid where automatic operation is the norm.

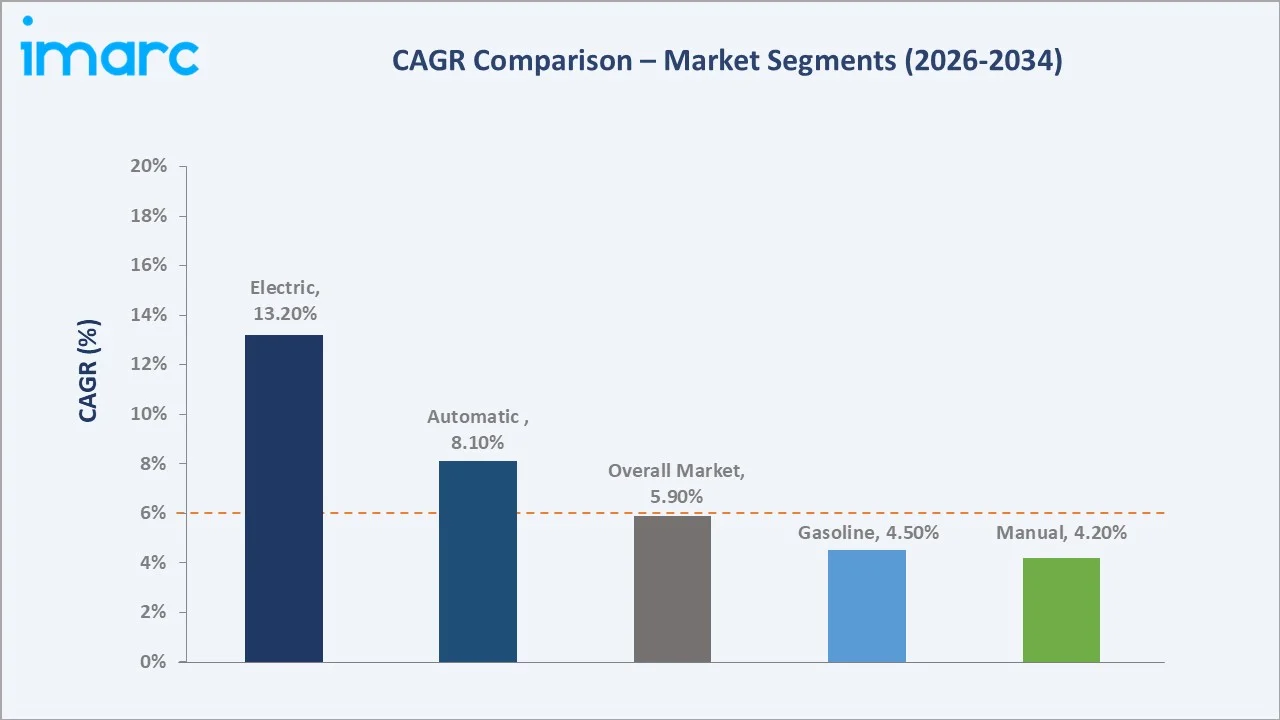

Gasoline two-wheelers represent 78.9% of fuel-type demand in 2025, while electric accounts for 21.1% and is growing fastest at ~13.2% CAGR through 2034. France leads regionally at 21.7%, anchored by Paris' restricted-traffic zones and the Prime à la Conversion subsidy. Leading manufacturers, including BMW AG, Honda Motor Co. Ltd., Immsi S.p.A., Kawasaki Heavy Industries, Ltd., and KYMCO, dominate the competitive landscape.

Key Market Insights

|

Insight |

Data |

|

Largest Transmission |

Manual Transmission – 62.5% share (2025) |

|

Fastest Growing Transmission |

Automatic Transmission – ~8.1% CAGR (2026-2034) |

|

Largest Fuel Type |

Gasoline – 78.9% share (2025) |

|

Fastest Growing Fuel Type |

Electric – ~13.2% CAGR (2026-2034) |

|

Leading Country |

France – 21.7% share (2025) |

|

Top Companies |

BMW AG, Honda Motor Co., Ltd., Immsi S.p.A., Kawasaki Heavy Industries, Ltd., and KYMCO |

Key Analytical Observations Supporting the Above Data:

- Manual transmission accounts for 62.5% of Europe's two-wheeler market in 2025, reflecting preference for performance motorcycles and mid-to-large displacement leisure segments above 500 cc, with ACEM reporting 1,002,848 motorcycle registrations in 2025.

- Automatic transmission at 37.5% is growing fastest as urban scooters, CVT commuters, and inherently automatic electric mopeds capture city-mobility demand. Piaggio Group retained an 18% European scooter share as of June 2025.

- Gasoline at 78.9% remains dominant as companies like TVS Motor Company launched its internal combustion engine models, including the Jupiter 125, NTORQ, Ronin 250, Apache RR 310, and Apache RTR 310, in France and Italy in July 2024.

- Electric two-wheelers at 21.1% are scaling rapidly, with Honda launching the WN7 in September 2025 and BMW Motorrad expanding its CE 02 and CE 04 lineup. France's Prime à la Conversion and Italy's Ecobonus lower the upfront premium.

- France's 21.7% share reflects Paris' status as Europe's largest scooter city, with low-emission zone enforcement accelerating ICE-to-EV substitution. France recorded 179,225 new motorcycle registrations in 2025 (ACEM).

Europe Two-Wheeler Market Overview

A two-wheeler is a motorized vehicle (combustion or electric) running on two wheels, encompassing motorcycles, scooters, mopeds, and electric variants used for commuting, leisure, sport, and commercial delivery. Europe's two-wheeler market spans road motorcycles (sport, touring, adventure, naked, cruiser), urban scooters and mopeds, off-road and dual-sport machines, and a fast-expanding electric mobility category covering L1e through L7e vehicle classes under EU type-approval frameworks.

Macroeconomic drivers include Europe's urban mobility reform agenda, full Euro 5+ enforcement from January 2025, the EU Green Deal aiming to cut emissions by at least 55% by 2030, and the proliferation of low-emission zones in Paris, Milan, Madrid, London, and Berlin. Rising fuel costs, congestion charging, and stringent CO2 regulations are compelling consumers and commercial fleets to migrate toward two-wheelers, while premiumization in touring and adventure categories expands average selling prices across Western markets.

Market Dynamics

To evaluate market opportunities, Request Sample

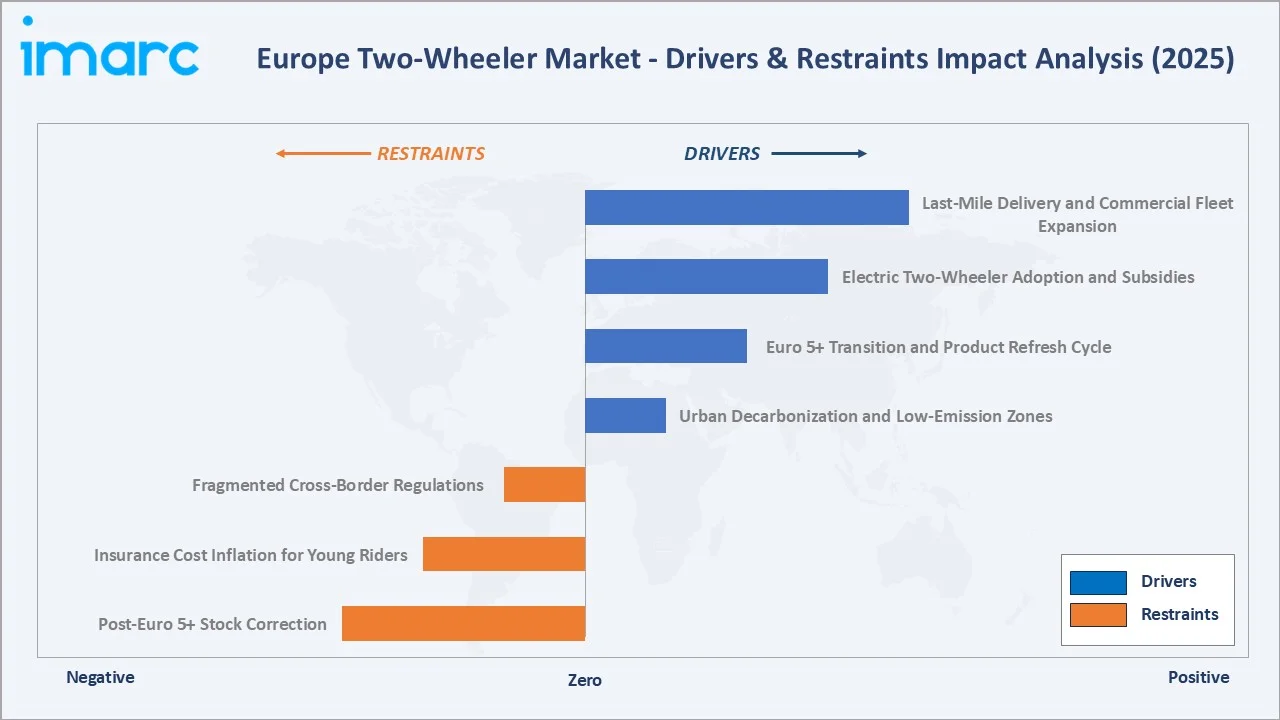

Market Drivers

- Urban Decarbonization and Low-Emission Zones: European cities are expanding restricted-traffic zones, with Paris, Milan, Madrid, and London enforcing access bans on older ICE vehicles, directly favoring compact, low-emission L1e and L3e two-wheelers that qualify for unrestricted ZFE access.

- Euro 5+ Transition and Product Refresh Cycle: Euro 5+, enforced from January 2025, triggered a substantial 2024 pre-buy (1,155,640 registrations per ACEM) and is now reshaping OEM portfolios with cleaner, electronics-rich platforms, sustaining replacement demand through 2030.

- Electric Two-Wheeler Adoption and Subsidies: France's Prime à la Conversion and Italy's Ecobonus reduce the upfront premium for electric scooters. The Swappable Batteries Motorcycle Consortium has standardized swap packs and rolled out interoperable stations across Europe.

- Last-Mile Delivery and Commercial Fleet Expansion: Food delivery and e-grocery platforms generate large fleet demand. Glovo, Deliveroo, and Just Eat operate scooter fleets across Spain, Italy, and France, with electric units increasingly favored for city emissions compliance.

Market Restraints

- Post-Euro 5+ Stock Correction: Motorcycle registrations across the five largest European markets declined 12.9% to 1,002,848 units in 2025 (ACEM), with Germany -35.7%, France -16.4%, and the UK -19.3%.

- Insurance Cost Inflation for Young Riders: Premiums for riders under 25 rose materially in 2025 due to higher claim severity, pricing many first-time owners out of the market and impacting electric scooter adoption among younger demographics.

- Fragmented Cross-Border Regulations: Electric two-wheeler classification and licensing vary across EU member states; Germany and Austria require licenses for many L1e classes while Italy and Spain permit lighter rules, creating compliance complexity for pan-European OEMs.

Market Opportunities

- Swappable Battery Ecosystems for Urban Mopeds: Battery-as-a-Service models reduce upfront EV costs and create predictable operating economics. Gogoro Inc.'s 2024 joint venture with Sumitomo Corporation accelerates swap-station deployment and builds scale for the SBMC pack.

- Premium Adventure and Touring Motorcycles: Demand for large-displacement adventure motorcycles continues expanding, exemplified by the BMW Motorrad introduction of three new R 1300 models, including the R 1300 R roadster, R 1300 RS sport tourer, and R 1300 RT touring motorcycle in April 2025, lifting ASPs across the touring category.

- Connected Two-Wheelers and OTA-Ready Electronics: EU’s General Safety Regulation 2 mandates from July 2024 require AEB, intelligent speed assistance, and enhanced cyclist/pedestrian detection on new powered two-wheelers, accelerating OEM investment in connected platforms with over-the-air updates.

Market Challenges

- Chinese Electric Entrant Price Competition: NIU Technologies, Yadea, and Super Soco have aggressively expanded European distribution, intensifying price competition in urban electric scooters and compressing margins in entry-level commuters.

- Charging and Battery-Swap Infrastructure Gaps: Despite SBMC progress, swap-station density remains uneven, with rural and intercity coverage particularly thin, limiting long-distance electric two-wheeler use cases.

Emerging Market Trends

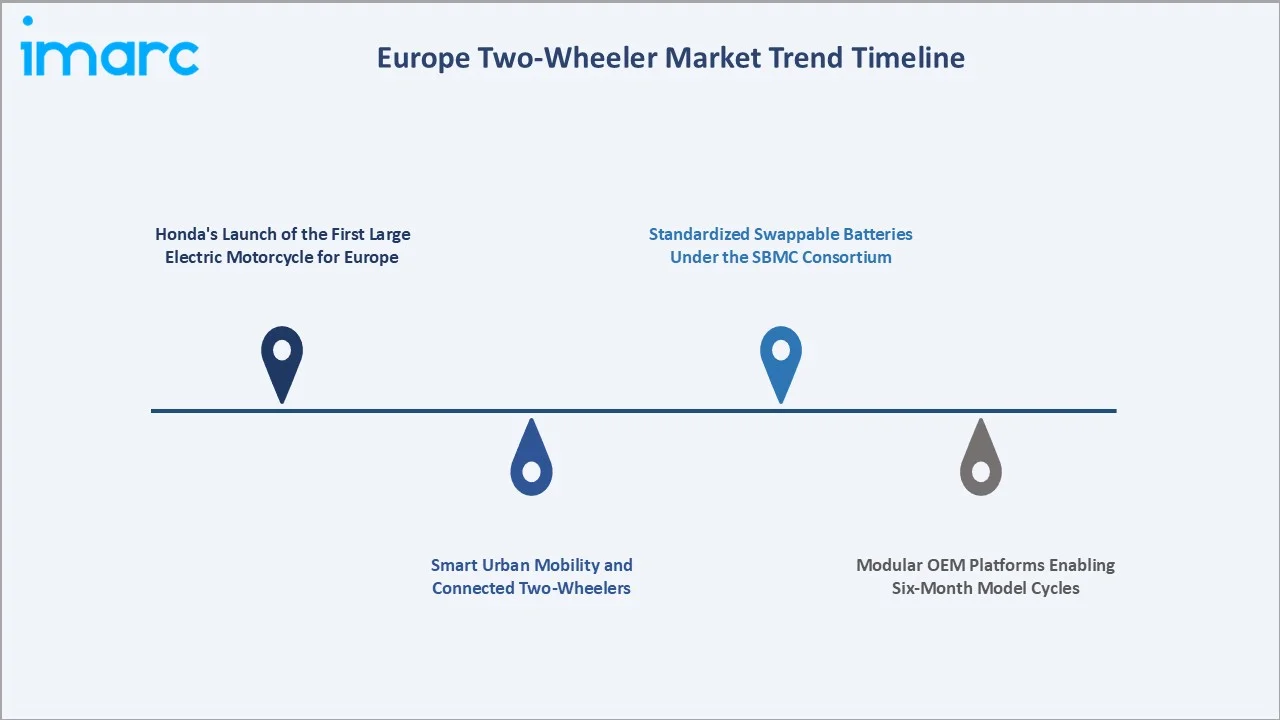

1. Honda's Launch of the First Large Electric Motorcycle for Europe

In September 2025, Honda Motor Co. Ltd. launched the Honda WN7 in Europe, its inaugural large electric motorcycle, priced at approximately GBP 12,999. The launch supports Honda's plan to carbon-neutralize its global motorcycle range by the 2040s and represents the entry of a top-three global OEM into the mid-displacement electric motorcycle category.

2. Standardized Swappable Batteries Under the SBMC Consortium

The Swappable Batteries Motorcycle Consortium, founded by Honda Motor Co. Ltd., KTM F&E GmbH, Yamaha Motor Co., Ltd., and Piaggio & C. SpA, has standardized battery packs and rolled out interoperable swap stations across multiple European countries. Early pilot stations are averaging multiple swaps per day, approaching commercial break-even, and lowering total-cost-of-ownership for urban electric scooter operators and last-mile delivery fleets.

3. Modular OEM Platforms Enabling Six-Month Model Cycles

European OEMs are adopting modular chassis architectures that decouple frames, suspensions, and electronic control units into interchangeable blocks. Piaggio's scooter platforms, including MP3, HPE engine family, and Aprilia's 660 parallel-twin base, are used as core mobility and performance platforms across the group’s scooter and motorcycle portfolio.

4. Smart Urban Mobility and Connected Two-Wheelers

In September 2025, Perseus Motor Corporation announced a strategic alliance to develop Europe’s first AI-powered electric vehicle platform. The initiative aims to combine AI-native vehicle architecture, software-defined mobility, and advanced electrification to support next-generation EV development in Europe. NIU’s NQi-Series app connects the scooter to NIU Cloud, giving riders real-time access to GPS location, anti-theft alerts, diagnostics, riding data, battery status, and nearby service stations.

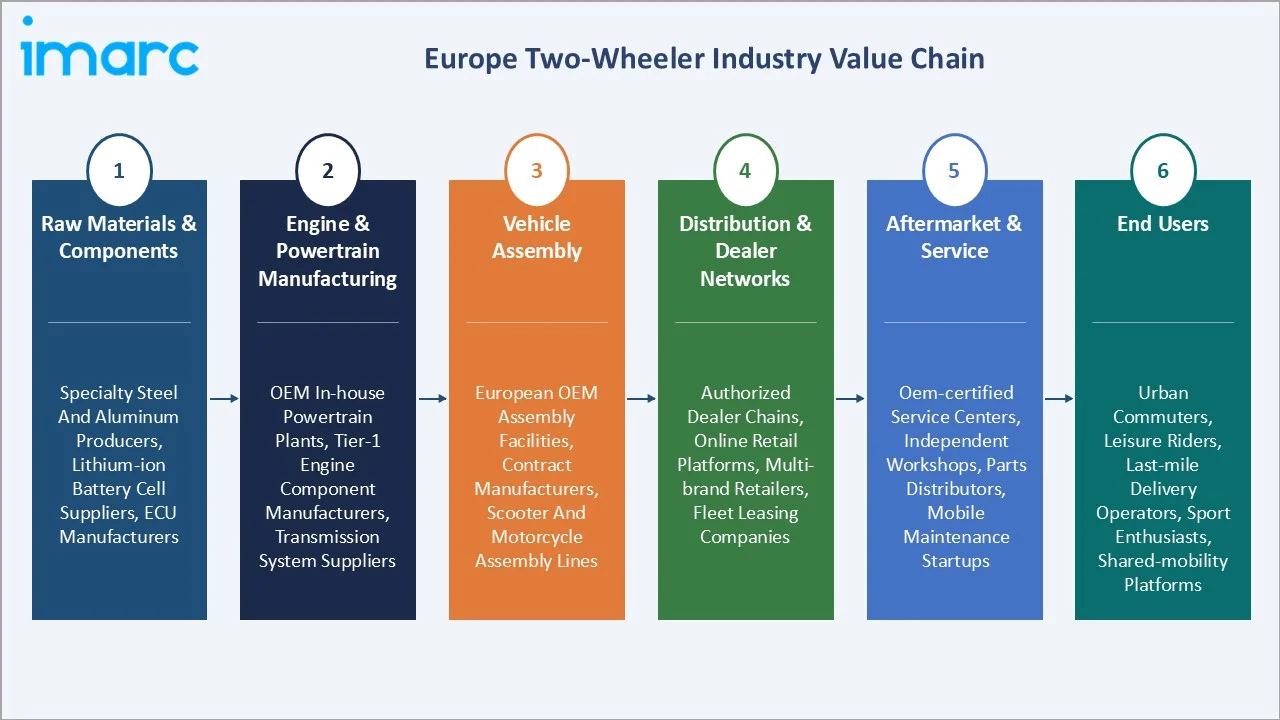

Industry Value Chain Analysis

Europe's two-wheeler value chain spans component supply through end-user retail, with each stage occupied by specialized manufacturers, distributors, and service providers whose performance directly influences product quality, regulatory compliance, and customer experience.

|

Stage |

Key Players / Examples |

|

Raw Materials & Components |

Specialty steel and aluminum producers, lithium-ion battery cell suppliers, electronic control unit (ECU) manufacturers |

|

Engine & Powertrain Manufacturing |

OEM in-house powertrain plants, tier-1 engine component manufacturers, transmission system suppliers |

|

Vehicle Assembly |

European OEM assembly facilities, contract manufacturers, scooter and motorcycle assembly lines |

|

Distribution & Dealer Networks |

Authorized dealer chains, online retail platforms, multi-brand independent retailers, fleet leasing companies |

|

Aftermarket & Service |

OEM-certified service centers, independent workshops, parts distributors, mobile maintenance startups |

|

End Users |

Urban commuters, leisure riders, last-mile delivery operators, sport and touring enthusiasts, shared-mobility platforms |

Technology Landscape in the Europe Two-Wheeler Industry

Internal Combustion Engine Platforms with Euro 5+ Compliance

Euro 5+ compliant single-, parallel-twin, V-twin, inline-three, inline-four, and boxer engines remain the dominant powertrain architecture across Europe's motorcycle base. BMW Motorrad, Ducati, Triumph, and Yamaha Motors have refreshed engine portfolios with advanced exhaust after-treatment, OBD, and ride-by-wire throttle systems.

Battery-Electric Two-Wheelers and L-Category EVs

Lithium-ion electric platforms now span L1e mopeds through L3e motorcycles, with leading platforms including the BMW CE 02 and CE 04 scooters, Energica Ego, Eva, and Esse Esse 9 motorcycles, Zero SR/F and DSR/X, and the newly launched Honda WN7. CATL EUR 4.1 billion battery plant joint venture with Stellantis in Figueruelas (November 2025) reflects long-term commitment to L-category electrification.

Continuously Variable Transmissions for Urban Scooters

CVTs dominate Europe's urban scooter segment, providing seamless acceleration without manual gear changes. Piaggio's Vespa and Beverly platforms, alongside Honda PCX, Yamaha XMAX, and KYMCO scooters, deploy CVT systems calibrated for stop-start urban duty cycles.

Connected Telematics and Rider Assistance Systems

Following the July 2024 EU mandate, new two-wheelers must integrate AEB, intelligent speed assistance, and enhanced cyclist/pedestrian detection. BMW Motorrad's ConnectedRide, Ducati Multimedia System, and Yamaha MyRide deliver smartphone integration, real-time navigation, and OTA firmware updates.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Vehicle Type |

🔒 |

🔒 |

2025 |

|

Transmission |

Manual Transmission |

62.5% |

2025 |

|

Fuel Type |

Gasoline |

78.9% |

2025 |

|

Engine Capacity |

🔒 |

🔒 |

2025 |

|

Country |

France |

21.7% |

2025 |

By Transmission

The manual transmission segment dominates with a 62.5% share in 2025, encompassing motorcycles equipped with traditional foot-shift gearboxes across sport, naked, touring, adventure, cruiser, and dual-sport categories. The segment's strength reflects European riders' preference for performance motorcycles and the structural dominance of brands such as BMW Motorrad, KTM, Ducati, Triumph, and Kawasaki across these categories.

To access detailed market analysis, Request Sample

Automatic transmission represents 37.5% of the market and is growing at approximately 8.1% CAGR through 2034. The segment captures CVT-equipped urban scooters, automatic mopeds, and electric two-wheelers. Demand is anchored by dense scooter cultures in Paris, Rome, Milan, and Madrid, and last-mile delivery fleets operated by Glovo, Deliveroo, and Just Eat.

By Fuel Type

Gasoline-powered two-wheelers commanded a 78.9% share in 2025, as more than 39 million motorcycles and scooters were estimated to be operating on European roads in 2024, owing to the performance and refueling convenience that gasoline platforms deliver across leisure, touring, and intercity use cases.

Electric two-wheelers represent 21.1% of the market in 2025 and are the fastest-growing fuel-type segment at approximately 13.2% CAGR through 2034. Adoption is concentrated in L1e mopeds and L3e urban scooters, supported by Honda's September 2025 WN7 launch, Energica's premium range, and Chinese entrants including NIU Technologies, Yadea, and Super Soco competing on price.

Regional Market Insights

France's market leadership at 21.7% in 2025 reflects Paris' status as Europe's largest scooter and moped city, structural enforcement of restricted-traffic zones across Paris, Lyon, and Marseille, and consumer access to the Prime à la Conversion subsidy. ACEM reported 179,225 new motorcycle registrations in France in 2025 within a broader ecosystem of dense urban moped fleets and rapidly expanding electric scooter usage.

|

Region |

Share (2025) |

Key Growth Drivers |

|

France |

21.7% |

Expanding low-emission zones in major cities, government EV subsidy schemes, dense urban moped and scooter fleets, large last-mile delivery operator base |

|

Italy |

17.6% |

Strong domestic OEM manufacturing base, deeply entrenched scooter commuting culture across major cities, national EV subsidy programs |

|

Spain |

14.3% |

Positive registration momentum, urban micromobility expansion in major metros, leading shared-scooter and rental-fleet penetration |

|

Germany |

13.5% |

Large premium and adventure motorcycle segment, strong domestic motorcycle heritage |

|

United Kingdom |

11.8% |

Large food-delivery scooter fleet, established premium and touring motorcycle culture, growing electric scooter adoption |

|

Russia |

9.2% |

Large geographic motorcycle market, strong off-road and dual-sport demand, increasing Asian OEM penetration in the entry-level segment |

|

Netherlands |

5.6% |

High share of electric scooters and L1e mopeds, strong battery-swap infrastructure rollout, supportive urban cycling and micromobility policy framework |

|

Others |

6.3% |

Belgium, Switzerland, Austria, Portugal, and Nordic markets; growing adventure motorcycle and electric scooter demand; expanding cross-border charter and tourism |

Italy at 17.6% remains Europe's second-largest market, anchored by Piaggio's 10% European share and 18% scooter-segment leadership as of June 2025. Spain at 14.3% was the only major market to record motorcycle registration growth in 2025, with new registrations reaching 242,580 units (+8.3% year-on-year per ACEM), reflecting expanding urban micromobility programs in Madrid, Barcelona, and Valencia.

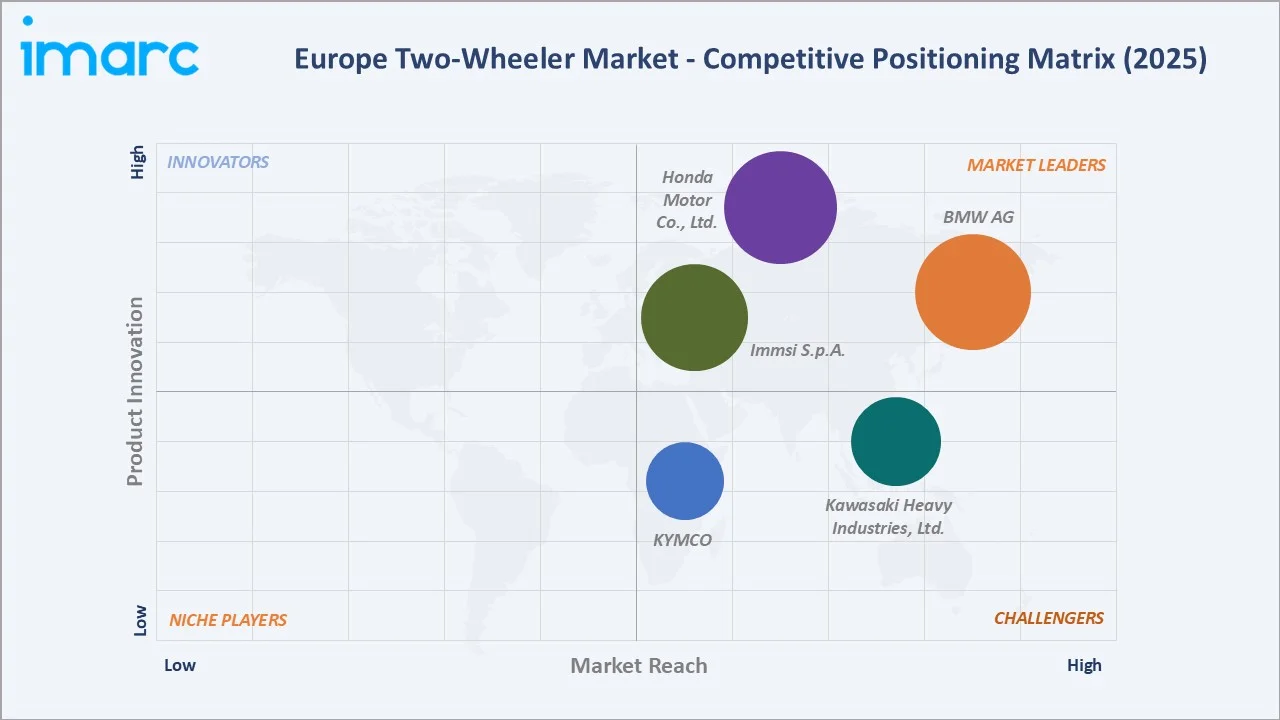

Competitive Landscape

Europe's two-wheeler market exhibits moderate concentration. Global OEMs including BMW AG, Honda Motor Co. Ltd., Immsi S.p.A., Kawasaki Heavy Industries, Ltd., and KYMCO collectively hold the majority of revenue share in 2025.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

BMW AG |

BMW Motorrad |

Market Leader |

Premium adventure, touring, and electric scooter platforms; strong EV leadership in urban mobility |

|

Honda Motor Co., Ltd. |

Honda |

Market Leader |

Broadest portfolio across scooters and motorcycles; first-mover advantage in electric motorcycles for Europe |

|

Immsi S.p.A. |

Piaggio, Scarabeo, Vespa, Aprilia, Moto Guzzi |

Market Leader |

Dominant European scooter share; modular manufacturing platform; consistent presence at major European motorcycle exhibitions |

|

Kawasaki Heavy Industries, Ltd. |

Kawasaki |

Strong Challenger |

Operational in the market via Kawasaki Motors Co., Ltd. Strong upcoming model pipeline; leadership in sport and commercial motorcycle segments; expanding electric platform development capabilities |

|

KYMCO |

KYMCO |

Challenger |

Strong scooter portfolio; affordable mid-displacement urban platforms; growing electric scooter range |

The market is also seeing rising competition from electric scooter and urban mobility brands, driven by low-emission transport policies and advancements in battery technology. At the same time, premium motorcycle brands are focusing on advanced rider-assistance systems, lightweight platforms, connectivity, and touring models to capture lifestyle-oriented consumers across major European markets.

Key Company Profiles

BMW AG

BMW Motorrad, the motorcycle division of BMW AG headquartered in Munich, Germany, is one of the world's leading premium two-wheeler manufacturers, operating a dedicated production facility in Berlin-Spandau and an electric scooter assembly plant for the CE-series.

- Product Portfolio: R 1300 GS, R 1300 RT, R 1300 RS, R 12 G/S adventure and touring motorcycles; S 1000 RR sport flagship; F-series mid-displacement; CE 02 and CE 04 electric scooters; M 1000 RR and Concept RR superbikes.

- Recent Developments: In May 2026, BMW Motorrad presented the BMW Motorrad Vision K18 at Concorso d'Eleganza Villa d'Este. The concept features a 1,800 cc inline six-cylinder engine, aircraft-inspired styling, six intakes, six tailpipes, six LED headlights, and hand-formed aluminum bodywork.

- Strategic Focus: Premium adventure leadership; electric urban mobility through CE series; connected ride technology integration; expansion of the M 1000 superbike platform.

Honda Motor Co. Ltd.

Honda Motor Co. Ltd., headquartered in Tokyo, Japan, is the world's largest motorcycle manufacturer by volume and one of Europe's top two-wheeler suppliers across scooter and motorcycle categories.

- Product Portfolio: CB and CBR sport and naked motorcycle ranges; CRF off-road and adventure series; Africa Twin adventure flagship; PCX, SH, and Forza CVT scooter range; Honda WN7 electric motorcycle.

- Recent Developments: In November 2025, Honda Motor Co. Ltd. premiered the CB1000GT sport tourer at EICMA 2025 in Milan, featuring a 1000cc liquid-cooled inline four-cylinder engine. The model combines sportbike performance with touring comfort, offering electronic suspension, riding modes, and a quick shifter.

- Strategic Focus: Electric motorcycle entry through WN7; PCX urban scooter dominance; SBMC swappable battery consortium leadership; carbon-neutrality roadmap by 2050.

Market Concentration Analysis

Europe's two-wheeler market exhibits moderate concentration, with top global OEMs collectively holding the majority of revenue in 2025. Below the top tier, a competitive mid-market of specialists including Triumph Motorcycles, Ducati Motor Holding, Yamaha Motor, and Suzuki, alongside Chinese electric entrants such as NIU Technologies, Yadea, and Super Soco, serves enterprise, retail, and shared-mobility segments with differentiated propositions.

Consolidation is occurring through electric powertrain capability acquisition and joint ventures: Stellantis and CATL's EUR 4.1 Billion European battery plant investment, Swappable Batteries Motorcycle Consortium (SBMC) created by Honda Motor Co. Ltd., KTM F&E GmbH, Yamaha Motor Co. Ltd., and Piaggio & C. SpA, reflect a strategic pivot toward capturing the faster-growing electric sub-market.

Investment & Growth Opportunities

Fastest Growing Segments

Electric two-wheelers (~13.2% CAGR), automatic-transmission urban scooters (~8.1% CAGR), premium adventure motorcycles, and connected/OTA-ready platforms represent the highest-growth investment vectors through 2034. Combined, these subcategories represent an incremental addressable opportunity exceeding USD 10 Billion within Europe's two-wheeler ecosystem by 2034.

Emerging Market Expansion

Spain, the Netherlands, and Portugal collectively represent the strongest near-term growth corridors beyond core France and Italy, supported by Spain's +8.3% motorcycle registration growth in 2025, the Netherlands' battery-swap density, and Portugal's expanding shared-mobility scooter programs.

Venture and Institutional Investment Trends

- CATL and Stellantis joint venture committed EUR 4.1 Billion to a European battery cell joint venture backed by 300 million euros in European Union funds, securing performance packs for accelerated model launches.

- Battery-as-a-Service models are emerging where vendors retain pack ownership and charge operators per swap, reducing operator CAPEX while enabling OEMs to capture lifecycle revenue.

- Government schemes including France's Prime à la Conversion and Italy's Ecobonus continue channeling institutional demand toward electric two-wheelers across L1e and L3e EV classes.

Future Market Outlook (2026-2034)

Europe's two-wheeler market is positioned for electrification-led expansion through 2034. From USD 24.90 Billion in 2025, it is projected to reach USD 42.35 Billion by 2034, representing incremental value of USD 17.45 Billion at a 5.90% CAGR, increasingly composed of electric platforms, premium adventure motorcycles, and connected scooter ecosystems.

The fuel-type mix is expected to rebalance materially by 2034: gasoline's share is projected to compress from 78.9% to roughly 60%, while electric two-wheelers grow from 21.1% toward 40% as Honda's WN7, BMW's CE-series, Piaggio Vespa Elettrica, Energica's range, and Chinese L1e entrants reshape the powertrain landscape.

Research Methodology

Primary Research

Primary research included structured interviews with over 100 industry participants in 2024–2025, European OEM executives, scooter dealers, last-mile fleet operators, battery-swap network managers, and ACEM-affiliated associations, validating market sizing, electrification adoption, and regional registration trends.

Secondary Research

Secondary research covered ACEM statistical releases (2024–2025), MotorCycles Data registration databases, EU and national type-approval records, OEM annual reports, EICMA 2025 disclosures, and ICCT data informing electric two-wheeler share analysis.

Forecasting Models

Market size estimations used combined top-down and bottom-up forecasting, incorporating country-level registrations, average selling price by category, fuel-type mix, and OEM revenue disclosures. The 5.90% base-case CAGR reflects validation against ACEM trends, Euro 5+ corrections, and announced electric platform launches.

Europe Two-Wheeler Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Vehicle Types Covered | Scooter/Moped and Motorcycle (Sport/Supersport, Enduro, Chopper, Classic, Commuter, Others) |

| Fuel Types Covered | Gasoline, Electric |

| Engine Capacities Covered | Up to 125 cc, 126-250 cc, 251-500 cc, Above 500 cc |

| Transmissions Covered | Manual Transmission and Automatic Transmission |

| Countries Covered | France, Italy, Spain, Germany, United Kingdom, Russia, Netherlands, Others |

| Companies Covered | BMW AG, Honda Motor Co., Ltd., Immsi S.p.A., Kawasaki Heavy Industries, Ltd., KYMCO, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe two-wheeler market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Europe two-wheeler market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe two-wheeler industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe Two-Wheeler Market Report

The Europe two-wheeler market reached USD 24.90 Billion in 2025 and is projected to reach USD 42.35 Billion by 2034.

The market is expected to grow at a CAGR of 5.90% during 2026-2034, driven by urban electrification, low-emission-zone enforcement, and the post-Euro 5+ refresh cycle.

France leads with a 21.7% share in 2025, anchored by Paris' large scooter culture, restricted-traffic zone enforcement, and the Prime à la Conversion EV subsidy.

Manual transmission dominates with a 62.5% share in 2025, reflecting European riders' preference for sport, naked, touring, and adventure motorcycles.

Gasoline-powered two-wheelers hold 78.9%, supported by Europe's 39 million operational ICE units (2024) and the range advantages of internal combustion.

Key players include BMW AG, Honda Motor Co., Ltd., Immsi S.p.A., Kawasaki Heavy Industries, Ltd., and KYMCO.

Electric two-wheelers are growing at approximately 13.2% CAGR due to low-emission zones, EV subsidies in France and Italy, the SBMC swappable battery standard, and Honda's WN7 launch.

Key challenges include post-Euro 5+ stock corrections (-12.9% in 2025), rising insurance premiums for young riders, fragmented cross-border EV rules, and Chinese price competition.

Battery-as-a-Service models, premium adventure motorcycles, OTA-ready connected platforms, and electric L1e/L3e urban scooters offer the highest-growth investment opportunities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)