European Cross-Laminated Timber Market Size, Share, Trends and Forecast by Application, Product Type, Element Type, Raw Material Type, Bonding Method, Panel Layer, Adhesive Type, Press Type, Storey Class, Application Type, and Country, 2026-2034

European Cross-Laminated Timber Market Summary:

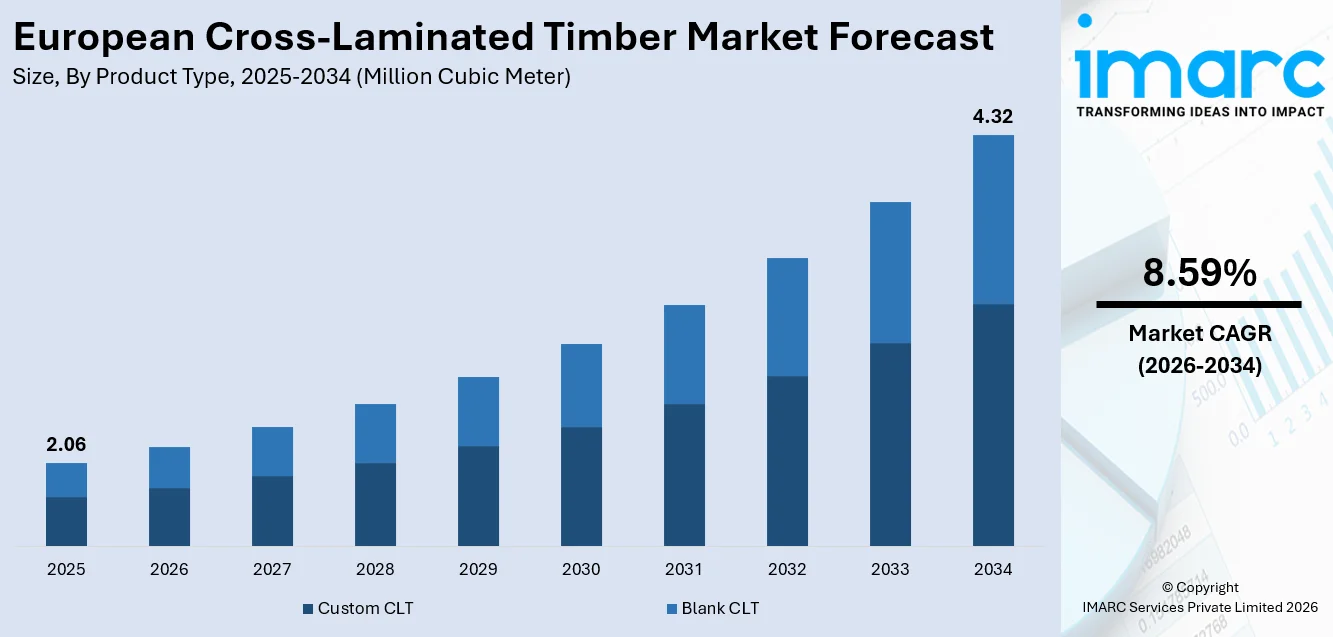

The European cross-laminated timber market size reached 2.06 Million Cubic Meter in 2025 and is projected to reach 4.32 Million Cubic Meter by 2034, growing at a compound annual growth rate of 8.59% from 2026-2034.

The European cross-laminated timber market is expanding rapidly as governments and construction industries prioritize low-carbon building solutions and circular economy principles. Supportive regulatory frameworks, advancements in prefabrication technologies, and the growing acceptance of engineered wood products among architects and builders are strengthening adoption across the region. Rising demand for energy-efficient residential housing, combined with CLT’s superior thermal and acoustic insulation properties, is reshaping modern construction practices, positioning Europe as the global leader in sustainable timber-based building solutions and expanding European cross-laminated timber market share.

Key Takeaways and Insights:

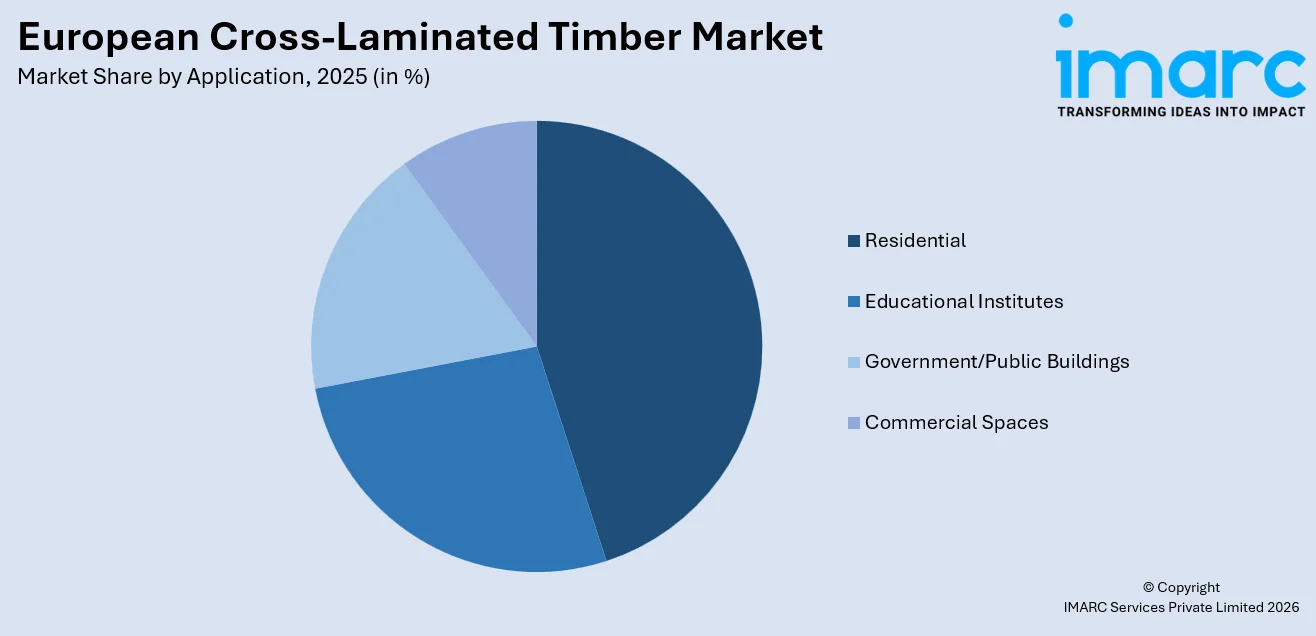

- By Application: Residential dominates the market with a share of 45% in 2025, driven by accelerating demand for sustainable housing solutions and prefabricated modular construction across European urban centers.

- By Product Type: Custom CLT leads the market with a share of 62% in 2025, owing to its ability to meet specific architectural and structural design requirements for diverse construction projects.

- By Element Type: Wall panels dominate the market with a share of 46% in 2025, supported by their exceptional strength, insulation properties, and widespread use in both residential and commercial structures.

- By Raw Material Type: Spruce represents the largest segment with 52% share in 2025, owing to its optimal strength-to-weight ratio, dimensional stability, and abundant availability across European forests.

- By Bonding Method: Adhesive bonded dominates with 71% market share in 2025, providing superior structural integrity and smooth surface finishes essential for modern CLT applications.

- By Panel Layer: 5-Ply represents the largest share at 41% in 2025, delivering an optimal balance of structural strength and design versatility for mid-rise construction applications.

- By Adhesive Type: PUR (Polyurethane) leads with a 44% share in 2025, offering exceptional bonding strength, fast curing times, and environmental compatibility.

- By Press Type: Hydraulic press dominates with 49% share in 2025, ensuring uniform pressure distribution and high-throughput manufacturing capabilities.

- By Storey Class: Mid-rise buildings (5–10 storeys) represent the largest share at 44% in 2025, reflecting urban densification trends and updated building codes supporting taller timber structures.

- By Application Type: Structural applications represent 78% of the market in 2025, underscoring CLT’s established role as a primary load-bearing material in modern construction.

- Key Players: The European CLT market is moderately consolidated, with leading manufacturers investing heavily in production capacity expansion, advanced CNC machining technologies, digital design platforms, and strategic partnerships to strengthen their positions and promote sustainable timber construction across the region. Some of the major market players are Stora Enso Oyj, KLH Massivholz GmbH, Binderholz GmbH, Mayr Melnhof Karton AG and Hasslacher Holding GmbH.

To get more information on this market Request Sample

The European cross-laminated timber (CLT) market is strengthening as the region emerges as a global leader in mass timber construction. Supportive environmental regulations and green building standards are fostering a favorable framework for CLT adoption, encouraging sustainable practices across the construction sector. Countries such as Austria, Germany, and Sweden serve as key hubs for CLT manufacturing, supported by established forestry supply chains and advanced production technologies. Stringent building codes emphasizing low embodied carbon are driving increased use of timber-based structural systems in new construction projects. Initiatives focused on circular timber construction and the integration of reclaimed materials are further advancing sustainability in the industry. Combined with pressures for affordable, high-performance housing and ongoing technological innovation, these factors position the European CLT market for steady growth and greater adoption across both residential and commercial construction segments. For instance, in June 2025, a German data center company unveiled a new prefabricated timber module designed for data center applications. The IT Container Eco Fix measures 6.5 × 3.0 × 3.4 meters and accommodates five server racks. It features a propane-powered indirect free cooling system and a 15kVA UPS module, combining compact design with efficient infrastructure support.

European Cross-Laminated Timber Market Trends:

Growing Adoption of Prefabricated and Modular CLT Construction

The shift toward off-site construction and modular building is accelerating CLT adoption across Europe. CLT’s dimensional stability, high strength, and compatibility with CNC machining make it ideal for prefabricated structures, enabling faster project completion with reduced waste. Digital fabrication tools and Building Information Modeling integration allow precision manufacturing and rapid on-site assembly. In April 2024, Stora Enso completed a prefabricated timber school building in Nantes, France, utilizing its automated coating line for CLT, demonstrating the efficiency and sustainability of modular CLT construction in educational infrastructure.

Expansion of CLT into Mid-Rise and High-Rise Urban Developments

European countries are gradually revising building codes to allow taller timber constructions, increasing the potential for CLT in urban environments where sustainability and densification priorities converge. Municipal housing projects in countries such as Germany, Austria, and Sweden are driving substantial demand for CLT products, while initiatives like the Paris Timber Tower project demonstrate growing interest in high-rise timber buildings. These developments underscore the expanding role of CLT in large-scale urban construction, highlighting its suitability for sustainable, innovative, and environmentally conscious building solutions across Europe.

Circular Economy and Sustainable Timber Innovation

The European cross-laminated timber industry is increasingly adopting circular economy approaches, with producers focusing on the use of reclaimed wood and demountable construction methods. Growing interest in mechanically fastened CLT panels reflects a shift toward reusable systems that avoid chemical bonding and support material recovery. Collaborative research and innovation initiatives are exploring ways to reuse and reprocess timber without compromising structural performance. Together, these developments are advancing circular timber construction practices, improving resource efficiency, and strengthening the role of CLT as a sustainable building solution across Europe. For instance, in December 2023, the UK government introduced an ambitious new strategy aimed at expanding the use of timber in residential and commercial construction to lower carbon emissions and support the transition toward net-zero targets.

.webp)

Market Outlook 2026-2034:

The European cross-laminated timber market is poised for robust expansion as sustainability mandates intensify and construction industries accelerate the transition toward low-carbon building materials. Growing investments in production capacity, advancements in automated manufacturing processes, and expanding regulatory support for timber-based construction are expected to drive sustained demand. The EU Emissions Trading System, which by 2027 will bring a significant share of construction emissions under carbon pricing, is anticipated to add cost premiums to conventional materials like concrete and steel, further strengthening CLT’s competitive positioning. The market size was estimated at 2.06 Million Cubic Meter in 2025 and is expected to reach 4.32 Million Cubic Meter by 2034, reflecting a compound annual growth rate of 8.59% over the forecast period 2026-2034.

European Cross-Laminated Timber Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Application |

Residential |

45% |

|

Product Type |

Custom CLT |

62% |

|

Element Type |

Wall Panels |

46% |

|

Raw Material Type |

Spruce |

52% |

|

Bonding Method |

Adhesive Bonded |

71% |

|

Panel Layer |

5-Ply |

41% |

|

Adhesive Type |

PUR (Polyurethane) |

44% |

|

Press Type |

Hydraulic Press |

49% |

|

Storey Class |

Mid-Rise Buildings (5–10 Storeys) |

44% |

|

Application Type |

Structural Applications |

78% |

Application Insights:

Access the comprehensive market breakdown Request Sample

- Residential

- Educational Institutes

- Government/Public Buildings

- Commercial Spaces

Residential dominates with a market share of 45% of the total European cross-laminated timber market in 2025.

Residential construction represents the largest application for CLT in Europe, driven by escalating demand for sustainable, energy-efficient housing solutions that address urban densification challenges. Social housing programs and affordability pressures across European cities are accelerating the adoption of prefabricated CLT modules that significantly reduce construction timelines and labor requirements. The material’s superior thermal and acoustic insulation properties enhance occupant comfort, making it increasingly preferred for premium urban housing developments. In Austria, a substantial proportion of new multi-family residential units now utilize CLT, driven by faster build times, lower on-site noise pollution, and strong regulatory support for timber-based construction.

The residential sector’s leading position is reinforced by CLT’s suitability for modular construction, allowing factory-finished housing units to be transported and assembled efficiently on-site. This approach supports faster project timelines, reduced labor intensity, and improved construction quality. Adoption of CLT in multi-family housing projects highlights its scalability and flexibility in addressing Europe’s housing needs. At the same time, CLT enables developers to meet strict environmental and sustainability requirements, reinforcing its role as a preferred material for modern, high-performance residential construction across the region.

Product Type Insights:

- Custom CLT

- Blank CLT

Custom CLT leads the market with a share of 62% of the total European cross-laminated timber market in 2025.

Custom cross-laminated timber has emerged as the dominant product type, reflecting the European construction industry’s increasing demand for architectural flexibility and project-specific solutions. Custom CLT allows architects and designers to specify unique shapes, sizes, panel configurations, and surface finishes that standard panels cannot adequately address. Advancements in CNC machining technology and digital design platforms have made precision manufacturing more accessible, enabling panels to be produced with integrated openings, embedded mechanical systems, and exact dimensional specifications that support rapid on-site assembly.

The growing sophistication of European construction projects, particularly in mid-rise residential and commercial developments, necessitates customized structural solutions. KLH Massivholz, a pioneer in CLT manufacturing with over twenty-five years of experience, has invested in advanced CNC production technology at its facilities in Austria to enhance panel customization capabilities and reduce lead times for structural timber applications. This investment in precision manufacturing aligns with the broader industry trend toward BIM-integrated, digitally fabricated construction components that minimize waste and optimize material performance.

Element Type Insights:

- Wall Panels

- Flooring Panels

- Roofing Slabs

- Others

Wall panels represent the largest share at 46% of the total European cross-laminated timber market in 2025.

Wall panels represent the largest element type in the European CLT market, driven by their versatile application across residential, commercial, and institutional construction. CLT wall panels deliver exceptional structural strength, thermal insulation, and acoustic performance while enabling faster construction timelines through prefabrication. The growing emphasis on sustainable construction practices and green building certifications across Europe is pushing builders and architects toward CLT wall panels as an environmentally favorable alternative to conventional materials.

The prefabricated nature of CLT wall panels supports modular construction approaches that significantly reduce on-site labor requirements and construction waste. Stora Enso’s CLT solutions have been utilized in numerous landmark projects, including the world’s first large-scale timber data center in Falun, Sweden, developed by EcoDataCenter, which is expanding with two additional facilities. These projects demonstrate how CLT wall panels can deliver structural performance comparable to concrete and steel while reducing embodied carbon by up to seventy percent.

Raw Material Type Insights:

- Spruce

- Pine

- Fir

- Others

Spruce leads the market with a share of 52% of the total European cross-laminated timber market in 2025.

Spruce is the primary raw material used in European CLT manufacturing, favored for its strong stiffness-to-weight performance, dimensional reliability, and consistent grain structure. The wide source in the regional forests helps in sourcing of the product in a stable manner whereas its natural thermal and acoustic insulation properties are useful in building performance. The interior appearance of the species is very convenient with the interior design taste of the homes and commercial areas. Moreover, spruce is compatible with the adhesive bonding systems, and its presence is confirmed by long-established performance standards in the European CLT product standards, which only contributes to its popularity.

The CLT industry is slowly diversifying its source of raw materials in reaction to environmental issues like climate effects and pressure associated with pests that are affecting the supply of spruce. Other wood species that will be used as feedstocks in CLT production are fast-growing hardwoods, which manufacturers and researchers are examining as an option. These solutions provide a chance to enhance the resilience of the resources, with the performance and sustainability of the structures. The development of technical standards and design principles is more accommodative to a broader variety of species, which contributes to the diversification of materials and improves the security of long-term supply of the European CLT market.

Bonding Method Insights:

- Adhesive Bonded

- Mechanically Fastened

Adhesive bonded dominates the market with a share of 71% of the total European cross-laminated timber market in 2025.

Adhesive bonding is the overwhelmingly dominant method in European CLT production, providing superior structural integrity, dimensional stability, and seamless surface finishes that are essential for modern construction. The technology is fully compatible with automated CNC manufacturing, enabling precision tolerances critical for BIM-driven construction workflows. In Austria and Germany, where the majority of mass timber buildings use adhesive-bonded CLT, building codes such as DIN EN 16351 explicitly certify the long-term durability and structural performance of adhesive-bonded panels, reinforcing confidence among architects and builders.

Industrial-grade polyurethane and phenol-resorcinol-formaldehyde adhesives create monolithic panels with consistent load distribution across all layers, making adhesive bonding indispensable for multi-storey construction. The method produces smoother surfaces that are easier to finish and treat, offering significant aesthetic advantages for exposed timber applications. While mechanically fastened systems are gaining interest for their alignment with circular economy principles and demountable construction concepts, adhesive bonding’s established regulatory pathways and proven performance continue to underpin its market dominance.

Panel Layer Insights:

- 3-Ply

- 5-Ply

- 7-Ply

- Others

5-ply represent the highest share at 41% of the total European cross-laminated timber market in 2025.

The 5-ply panel configuration has established itself as the most widely adopted in the European CLT market, offering an optimal balance of structural performance, thermal insulation, and cost-effectiveness. These panels deliver enhanced load-bearing capacity compared to 3-ply alternatives while maintaining manageable weight and manufacturing efficiency, making them suitable for a broad range of residential and commercial applications including load-bearing walls, floors, and mid-rise construction elements.

The versatility of 5-ply panels allows architects to achieve longer spans between structural supports, enabling more flexible and open floor plans in modern buildings. Their improved acoustic performance, achieved through the additional cross-oriented layers, meets the increasingly stringent sound insulation requirements of European residential building codes. Manufacturers across the DACH region, which produced a record 1.42 million cubic meters of CLT in 2024 representing a nine percent increase over the previous year, rely heavily on 5-ply configurations to serve the growing mid-rise urban housing market.

Adhesive Type Insights:

- PUR (Polyurethane)

- PRF (Phenol Resorcinol Formaldehyde)

- MUF (Melamine-Urea-Formaldehyde)

- Others

PUR (Polyurethane) represents the leading segment with a 44% share of the total European cross-laminated timber market in 2025.

Polyurethane adhesives have captured the largest share of the European CLT adhesive market due to their exceptional bonding strength, fast curing times, and compatibility with diverse wood species. PUR adhesives produce cleaner, smoother surfaces that enhance the aesthetic quality of exposed CLT panels, while offering excellent resistance to moisture and temperature fluctuations. Their environmental profile has improved significantly as manufacturers formulate products to meet European health and safety standards, supporting the industry’s sustainability credentials.

The ongoing development of bio-based and formaldehyde-free polyurethane formulations is further strengthening PUR’s position in the market. These innovations align with tightening EU regulations on volatile organic compound emissions in construction materials and the growing demand for healthier indoor environments. PUR adhesives’ versatility in bonding different wood species also provides manufacturers with greater flexibility as the industry explores alternative feedstocks beyond traditional spruce.

Press Type Insights:

- Hydraulic Press

- Vacuum Press

- Pneumatic Press

- Others

Hydraulic press leads the largest share at 49% of the total European cross-laminated timber market in 2025.

Hydraulic presses dominate CLT manufacturing in Europe due to their ability to deliver consistent and uniform pressure across large panel surfaces during the bonding process, ensuring structural integrity and dimensional accuracy. These presses are highly adaptable, accommodating various panel sizes and thicknesses from 3-ply to 7-ply configurations without requiring separate pressing machinery. The latest generation of hydraulic presses, such as Ledinek’s X-Press systems installed at Mayr-Melnhof Holz’s facility in Leoben, Austria, can produce panels up to sixteen meters long and 3.5 meters wide.

The automated nature and rapid cycle times of hydraulic presses enable high-throughput manufacturing that meets the accelerating European demand for CLT. Their precision capabilities minimize material waste during production, aligning with the industry’s sustainability objectives. As CLT production capacity continues to expand across Europe, hydraulic press technology remains the cornerstone of efficient, large-scale manufacturing operations.

Storey Class Insights:

- Low-Rise Buildings (1–4 Storeys)

- Mid-Rise Buildings (5–10 Storeys)

- High-Rise Buildings (More Than 10 Storeys)

Mid-rise buildings (5–10 storeys) represent the largest segment with a 44% share of the total European cross-laminated timber market in 2025.

Mid-rise buildings have become the fastest-growing application segment for CLT in Europe, reflecting the intersection of urban densification pressures, housing shortage solutions, and progressive building code reforms. European countries have progressively revised their regulations to permit taller timber structures, with several jurisdictions now allowing wooden buildings of up to eighteen storeys under updated building classification systems. This regulatory evolution has positioned CLT as a primary structural solution for five to ten-storey urban residential and mixed-use developments.

CLT’s seismic performance, fire resistance through natural charring behavior, and reduced construction weight compared to conventional materials make it particularly suited for mid-rise urban applications. Municipal housing initiatives in Germany, Austria, and Sweden have been instrumental in driving mid-rise CLT adoption, with these countries collectively accounting for significant CLT consumption. The segment’s growth is further supported by CLT’s ability to reduce construction timelines by approximately thirty percent compared to conventional building methods.

Application Type Insights:

- Structural Applications

- Non-Structural Applications

Structural applications exhibit clear dominance with a 78% share of the total European cross-laminated timber market in 2025.

Structural applications overwhelmingly dominate the European CLT market, reflecting the material’s established credentials as a primary load-bearing solution for modern construction. CLT serves as a direct replacement for concrete and steel in walls, floors, roofs, and structural cores, offering comparable strength with significantly lower embodied carbon. The material’s favorable strength-to-weight ratio, seismic resilience, and prefabrication compatibility have established it as a critical component in mainstream architectural practice across Europe.

The structural segment’s commanding share is underpinned by CLT’s compliance with European harmonized standards and its integration into national building codes across key markets. The updated Eurocode 5, currently under revision, includes comprehensive provisions for CLT design that will further standardize and facilitate its structural use. CLT’s capacity to store carbon within building structures while providing long-term durability makes it a cornerstone of Europe’s strategy to decarbonize the built environment.

Regional Insights:

- Austria

- Germany

- Italy

- Switzerland

- Czech Republic

- Spain

- Norway

- Sweden

- United Kingdom

- Others

Austria’s CLT market is driven by its strong forestry base, advanced timber engineering expertise, and early adoption of mass timber construction. Supportive building regulations, export-oriented CLT manufacturers, and growing use of timber in residential and public buildings continue to reinforce domestic demand and innovation leadership.

Germany’s CLT market growth is supported by stringent climate policies, low-embodied-carbon building standards, and expanding urban housing projects. Increasing acceptance of mid-rise and high-rise timber construction, combined with municipal housing initiatives and strong prefabrication capabilities, is accelerating CLT adoption across residential and commercial sectors.

Italy’s CLT demand is driven by seismic-resistant construction requirements, rapid post-earthquake rebuilding, and growing use of prefabricated timber systems. CLT’s structural performance, speed of installation, and suitability for low- to mid-rise residential buildings support its expanding role in both urban regeneration and rural housing projects.

Switzerland’s CLT market benefits from strict sustainability standards, advanced engineering practices, and high-quality construction requirements. Strong demand for energy-efficient residential buildings, combined with favorable timber design codes and public sector support for sustainable materials, continues to promote CLT use in housing and institutional projects.

The Czech Republic’s CLT market is expanding due to increasing investment in prefabricated construction, rising housing demand, and growing alignment with European sustainability standards. Improvements in domestic manufacturing capacity and evolving building regulations are supporting wider adoption of CLT in residential and mixed-use developments.

Spain’s CLT market growth is driven by energy-efficient building regulations, urban redevelopment projects, and increasing focus on low-carbon construction materials. Public sector initiatives promoting sustainable housing and growing interest in modular timber systems are encouraging the use of CLT in residential and public infrastructure projects.

Norway’s CLT demand is supported by ambitious climate goals, strong public procurement policies favoring low-carbon materials, and widespread acceptance of timber in construction. CLT is increasingly used in multi-storey residential and public buildings due to its sustainability credentials and structural performance in cold climates.

Sweden’s CLT market is driven by abundant forest resources, strong government support for timber construction, and a well-developed prefabrication industry. High demand for sustainable housing, combined with carbon-focused building policies, continues to position CLT as a preferred structural material nationwide.

The UK’s CLT market is supported by net-zero building targets, growing adoption of modern methods of construction, and demand for rapid housing delivery. Interest in offsite construction, sustainable materials, and urban densification is increasing CLT usage in residential, education, and mixed-use developments.

Market Dynamics:

Growth Drivers:

Why is the European Cross-Laminated Timber Market Growing?

Supportive EU Environmental Regulations and Green Building Mandates

The European Union’s environmental agenda is establishing a strong regulatory foundation that supports wider adoption of renewable construction materials such as cross-laminated timber. Climate neutrality objectives, green building certification schemes, and embodied carbon regulations are encouraging the construction sector to reduce reliance on carbon-intensive materials like steel and concrete. Several countries have introduced building codes that prioritize life-cycle carbon assessment and promote the use of bio-based materials in both new developments and renovation projects. In parallel, carbon pricing mechanisms applied to construction-related emissions are increasing the relative cost of conventional materials. Together, these policy measures are improving the economic and environmental attractiveness of CLT, reinforcing its role in sustainable construction across Europe.

Rapid Expansion of CLT Manufacturing Capacity Across Europe

Major European CLT producers are significantly expanding their manufacturing capabilities to meet accelerating demand. In 2024, CLT manufacturers in the DACH region, Italy, and the Czech Republic collectively produced 1.42 million cubic meters, a nine percent increase over the previous year and a new industry record. European CLT manufacturers are making significant investments to expand and modernize production facilities, strengthening the region’s manufacturing base for mass timber construction. New plants and capacity expansions are enhancing production efficiency, scale, and geographic reach across key timber-producing countries. These developments are improving supply reliability, supporting technological advancement, and enabling manufacturers to meet rising demand from residential, commercial, and public construction projects. Collectively, the expansion of CLT manufacturing infrastructure is reinforcing Europe’s ability to support large-scale adoption of sustainable, timber-based building solutions.

Advancements in Digital Fabrication and Manufacturing Technologies

Technological innovation in CLT manufacturing is significantly enhancing product quality, production efficiency, and architectural possibilities. Advanced CNC machining centers enable precision cutting and customization of CLT panels with integrated openings, connection details, and embedded service channels, reducing on-site modification requirements. Digital design platforms that integrate CLT performance data with BIM workflows are streamlining the design-to-construction process, enabling architects and engineers to optimize structural solutions more efficiently. Automated production lines with high-speed hydraulic pressing systems, such as Ledinek’s third-generation X-Press technology capable of producing panels up to sixteen meters long and 3.5 meters wide, are increasing throughput while maintaining dimensional accuracy. These technological advances are expanding CLT’s use cases beyond traditional applications into complex architectural designs, large-span structures, and hybrid construction systems that combine mass timber with other materials.

Market Restraints:

What Challenges the European Cross-Laminated Timber Market is Facing?

Raw Material Supply Volatility and Rising Timber Costs

The European CLT market faces challenges from fluctuating timber prices and supply constraints. Climate change impacts, including bark beetle infestations and shifting spruce viability zones, are reducing the availability of preferred raw materials in some regions. Sanctions-driven shortages and increasing stumpage fees have contributed to rising input costs, squeezing margins for smaller manufacturers that lack vertical integration and creating uncertainty in project pricing.

Skilled Labor Shortages in Mass Timber Construction

The shortage of workers trained in CLT-specific construction techniques, including crane coordination, connection installation, and prefabricated assembly, represents a significant constraint. Construction firms across several European countries report difficulty finding workers with specialized mass timber assembly skills, leading to assembly errors, schedule delays, and compromised structural performance in complex joints, limiting the industry’s ability to scale efficiently.

Competition from Established Conventional Construction Materials

Despite growing adoption, CLT continues to compete against deeply entrenched concrete and steel construction practices that benefit from established supply chains, extensive professional familiarity, and well-documented performance histories. Higher initial material costs compared to conventional alternatives, combined with limited awareness in some market segments about CLT’s long-term economic and environmental advantages, continue to slow broader market penetration.

Competitive Landscape:

The European cross-laminated timber market exhibits a moderately consolidated competitive structure, with several Austrian-based manufacturers holding significant market positions alongside Nordic and German producers. Leading companies are pursuing aggressive capacity expansion strategies, investing in advanced manufacturing technologies including automated CNC machining and high-throughput hydraulic pressing systems. Strategic differentiation is achieved through product innovation, custom engineering capabilities, digital design platforms, and comprehensive project support services. Sustainability-driven investments, including circular timber initiatives and solar-powered manufacturing facilities, are becoming key competitive differentiators. Companies are also engaging in consumer education campaigns and professional training programs to promote CLT adoption and ensure quality implementation across the construction value chain. Some of the major market players include:

- Stora Enso Oyj

- KLH Massivholz GmbH

- Binderholz GmbH

- Mayr Melnhof Karton AG

- Hasslacher Holding GmbH

Recent Developments:

- In September 2025, Stora Enso successfully produced a CLT panel entirely from reclaimed wood at its Ybbs Mill in Austria, as part of the EU-funded Woodcircles initiative. The panels will form the structural core of a modular demonstration building to be assembled and toured across European cities including Turin, Rotterdam, and Tartu.

- In November 2024, Mayr-Melnhof Holz announced an investment of approximately EUR 13 million in solar power installations across its plants in Leoben, Gaishorn, Reuthe, Paskov, Wismar, and Olsberg, advancing its commitment to sustainable manufacturing operations and ecological power supply across its European production network.

European Cross-Laminated Timber Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD, Million Cubic Metres |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Applications Covered | Residential, Educational Institutes, Government/Public Buildings, Commercial Spaces |

| Product Types Covered | Custom CLT, Blank CLT |

| Element Types Covered | Wall Panels, Flooring Panels, Roofing Slabs, Others |

| Raw Material Types Covered | Spruce, Pine, Fir, Others |

| Bonding Methods Covered | Adhesive Bonded, Mechanically Fastened |

| Panel Layers Covered | 3-Ply, 5-Ply, 7-Ply, Others |

| Adhesive Types Covered | PUR (Polyurethane), PRF (Phenol Resorcinol Formaldehyde), MUF (Melamine-Urea-Formaldehyde), Others |

| Press Types Covered | Hydraulic Press, Vacuum Press, Pneumatic Press, Others |

| Storey Classes Covered | Low-Rise Buildings (1-4 Storeys), Mid-Rise Buildings (5-10 Storeys), High-Rise Buildings (More Than 10 Storeys) |

| Application Types Covered | Structural Applications, Non-Structural Applications |

| Countries Covered | Austria, Germany, Italy, Switzerland, Czech Republic, Spain, Norway, Sweden, United Kingdom, Others |

| Companies Covered | Stora Enso Oyj, KLH Massivholz GmbH, Binderholz GmbH, Mayr Melnhof Karton AG and Hasslacher Holding GmbH |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the European Cross-Laminated Timber Market Report

The European cross-laminated timber market size reached a volume of 2.06 Million Cubic Meter in 2025.

The European cross-laminated timber market is expected to grow at a compound annual growth rate of 8.59% from 2026-2034 to reach 4.32 Million Cubic Meter by 2034.

Residential, representing the largest share at 45% in 2025, remains the primary application segment for CLT in Europe, driven by accelerating demand for sustainable, prefabricated housing solutions that address urban densification challenges and housing shortages.

Key factors driving the European cross-laminated timber market include supportive EU environmental regulations, expanding CLT manufacturing capacity, advancements in digital fabrication technologies, progressive building code reforms allowing taller timber structures, and growing demand for sustainable construction materials.

Major challenges include raw material supply volatility and rising timber costs due to climate change impacts, skilled labor shortages in mass timber construction, competition from established conventional materials, and the need for further regulatory harmonization across European markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)