EV Charging Cables Market Size, Share, Trends and Forecast by Cable Length, Shape, Charging Level, Power Type, Application, and Region, 2026-2034

EV Charging Cables Market Size, Share, Trends & Forecast (2026-2034)

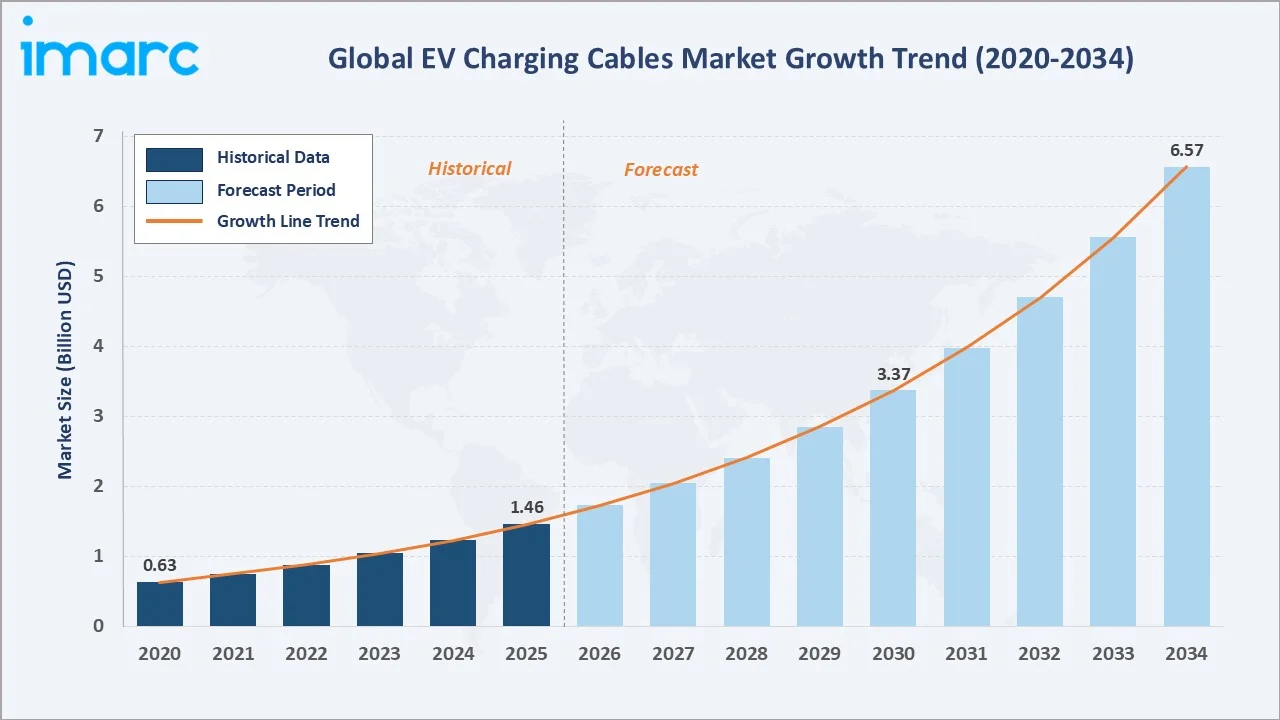

The EV charging cables market was valued at USD 1.46 Billion in 2025 and is projected to reach USD 6.57 Billion by 2034, exhibiting a CAGR of 18.18% during 2026-2034. The rapid global surge in EV registrations, accelerating public and private charging infrastructure investments, tightening emission mandates across major economies, rising demand for DC fast-charging solutions, and broadening fleet electrification programs across commercial and logistics sectors are the primary forces shaping market growth.

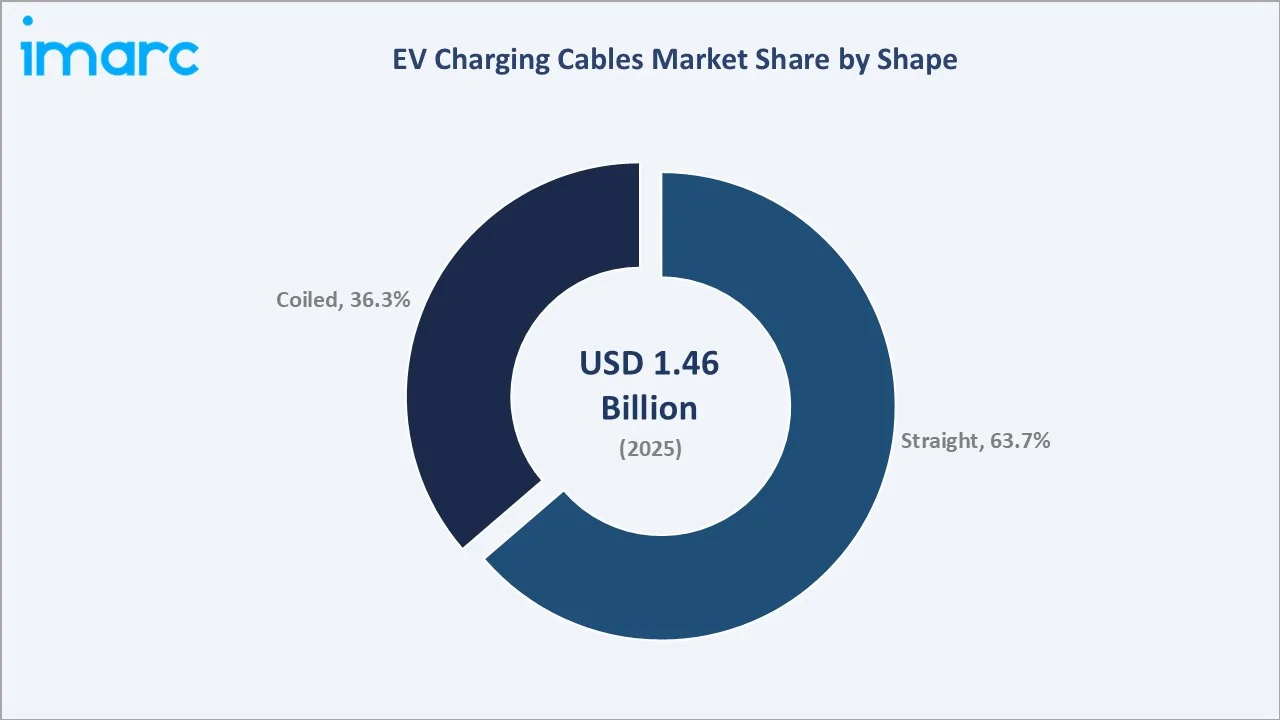

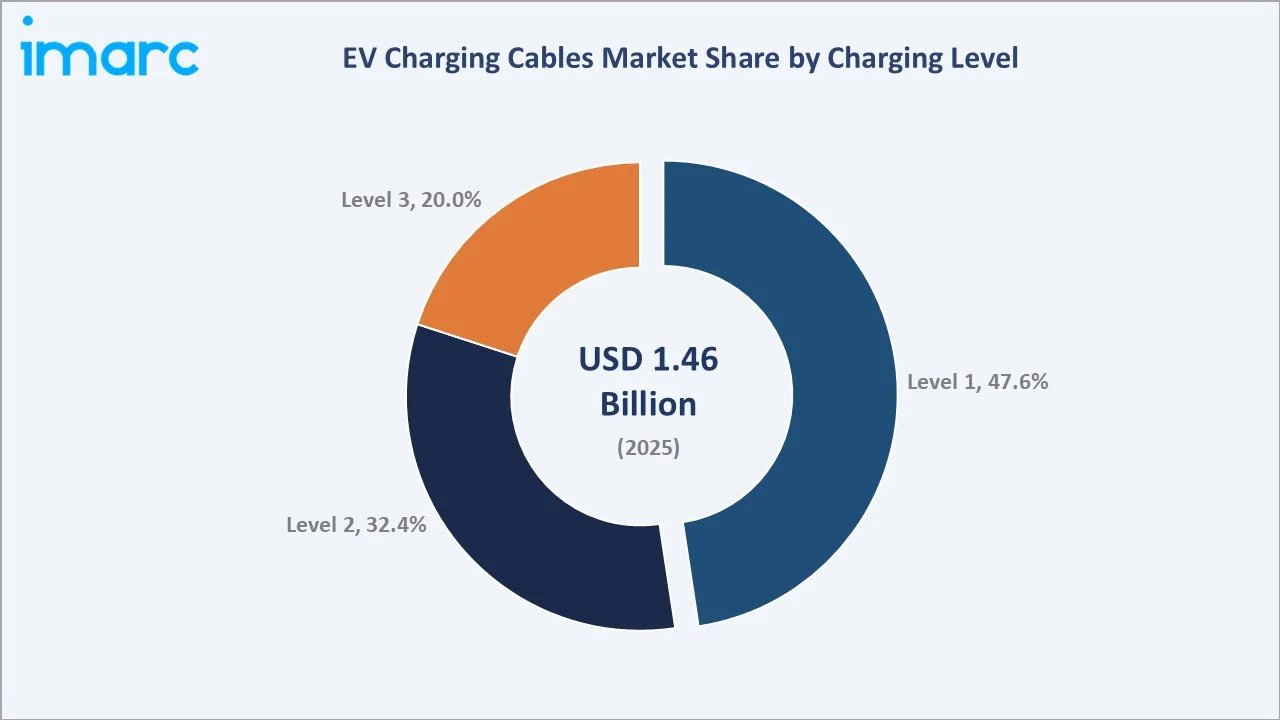

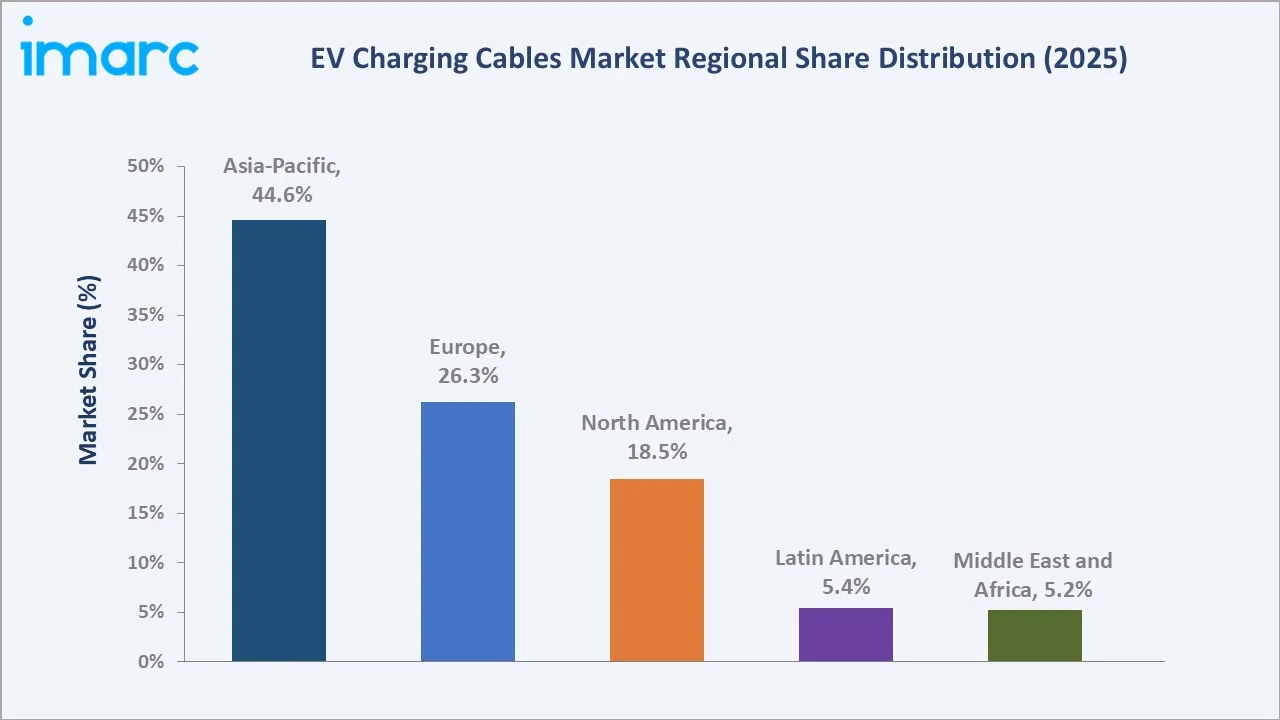

Straight dominates the shape segment at 63.7%, level 1 leads the charging level segment at 47.6%, and Asia-Pacific commands 44.6% of the regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.46 Billion |

|

Forecast Market Size (2034) |

USD 6.57 Billion |

|

CAGR (2026-2034) |

18.18% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (44.6%, 2025) |

|

Second Largest Region |

Europe (26.3%, 2025) |

|

Leading Shape |

Straight (63.7%, 2025) |

|

Leading Charging Level |

Level 1 (47.6%, 2025) |

The EV charging cables market expanded from USD 0.63 Billion in 2020 to USD 1.46 Billion in 2025, driven by rising EV adoption, government subsidies for clean mobility, and expanding residential and commercial charging infrastructure. Anchored at USD 3.37 Billion in 2030, the forecast to USD 6.57 Billion by 2034 is supported by accelerating DC fast-charging deployments, growing demand for smart and high-current cables, and the shift towards vehicle-to-grid (V2G) capable charging systems.

To get more information on this market, Request Sample

CAGR trajectories across shape and charging level sub-segments indicate that level 3 and coiled are expanding at rates above the overall 18.18% market CAGR, driven by the growing deployment of highway fast-charging stations, EV fleet corridors, and the adoption of premium cable formats in commercial applications.

Executive Summary

The EV charging cables market is on a high-growth trajectory from USD 0.63 Billion in 2020 to USD 6.57 Billion by 2034. The market has transitioned from niche residential accessories to mission-critical infrastructure components used in residential, commercial, and public DC fast-charging networks. Increasing EV penetration in China, Europe, and North America, combined with aggressive charging infrastructure mandates, is driving sustained demand for reliable, standards-compliant cables.

Straight commands 63.7% of the shape segment in 2025, favored for its ease of use in fixed wall-mount and pedestal-type charging units. Level 1 leads the charging level segment at 47.6%, reflecting the large installed base of residential and low-power commercial chargers. Asia-Pacific holds 44.6% of the regional share in 2025, anchored by China's dominant EV market, India's accelerating EV push, and Southeast Asia's expanding charging rollouts. In May 2026, 1.36 Million passenger electric vehicles were sold by domestic EV manufacturers in China, marking a 12% increase compared to the same month in 2025.

Key Market Insights

|

Insight |

Data |

|

Leading Shape |

Straight - 63.7% share (2025) |

|

Second Largest Shape |

Coiled - 36.3% share (2025) |

|

Leading Charging Level |

Level 1 - 47.6% share (2025) |

|

Second Largest Charging Level |

Level 2 - 32.4% share (2025) |

|

Leading Region |

Asia-Pacific - 44.6% share (2025) |

|

Second Largest Region |

Europe - 26.3% share (2025) |

|

Top Companies |

TE Connectivity, Amphenol Corporation, Nexans, Phoenix Contact |

Key Analytical Observations Expanding On The Data Above:

- Straight dominance at 63.7% reflects its widespread use in tethered AC home chargers, public pedestals, and workplace EV charging stations where flexibility and compact storage are less critical than low-cost, durable delivery.

- Coiled at 36.3% is gaining share in premium and portable charging applications, offering tangle-free handling and compact storage, particularly in commercial and semi-public settings where cable management is a priority.

- Level 1 leadership at 47.6% is underpinned by the widespread adoption of residential and workplace charging infrastructure, where standard AC charging solutions favor cost-effective, easy-to-install charging cables that are compatible with existing electrical systems.

- Level 2 at 32.4% is the second largest charging level segment, driven by commercial deployments in retail, hospitality, and workplace environments where faster charging is the standard choice.

- Asia-Pacific at 44.6% leads regional share, anchored by China's world-leading EV market, India's accelerating domestic EV push, and expanding charging network buildouts across South and Southeast Asian urban centers. As per IMARC Group, the India electric vehicle market size reached USD 3,712.2 Million in 2025.

EV Charging Cables Market Overview

EV charging cables are the physical interface between EVs and charging infrastructure, transmitting electrical power and data signals required for safe, efficient, and standards-compliant energy transfer. They span AC level 1, AC level 2, and DC fast-charging applications and are designed for residential, commercial, and high-power public fast-charging environments. The market encompasses tethered cables permanently attached to charging units and untethered portable cables supplied with vehicles or sold as accessories.

The ecosystem integrates raw material suppliers providing copper, aluminum, and specialty polymers; component manufacturers producing connectors, plugs, and sockets; cable assembly OEMs and aftermarket suppliers; certification and compliance bodies; distribution networks; and end users ranging from private EV owners to fleet operators and charge point operators. Macroeconomic drivers, including government EV mandates, clean energy transition investments, and decarbonization targets, are reshaping procurement and supply chain strategies across the value chain.

Market Dynamics

To evaluate market opportunities, Request Sample

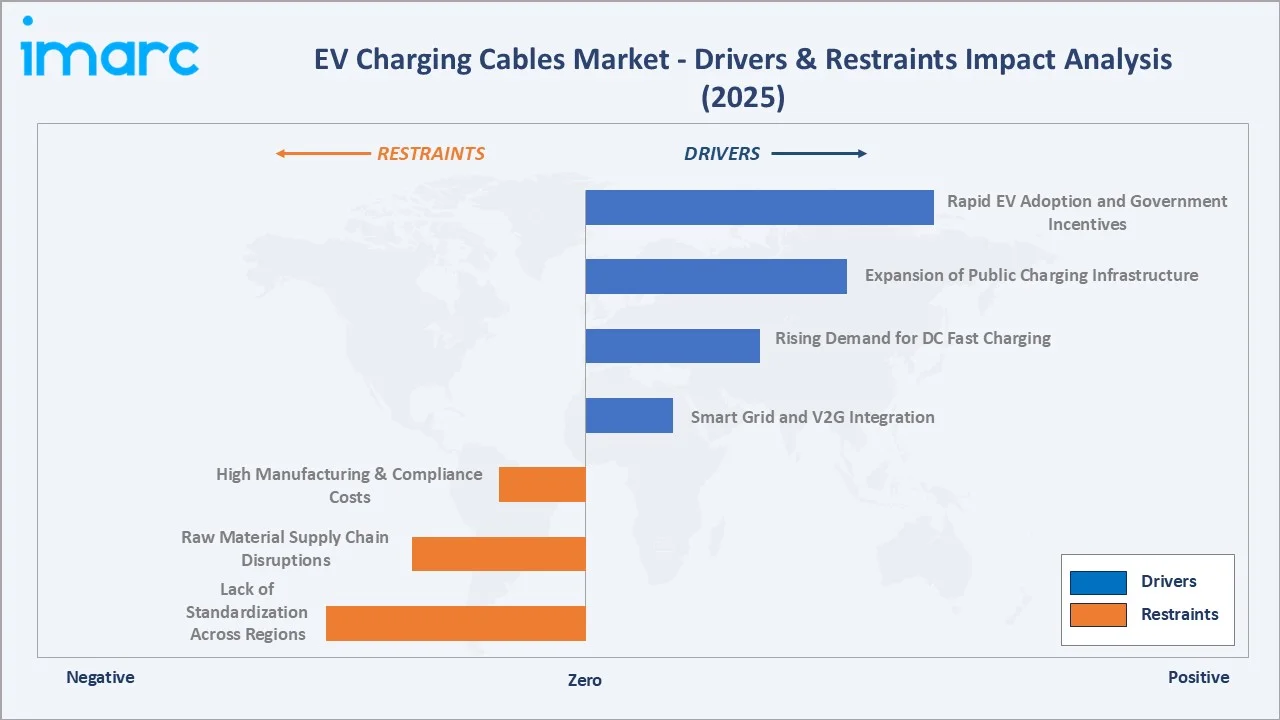

Market Drivers

- Rapid EV Adoption and Government Incentives: Surging EV sales globally, supported by government purchase subsidies, tax credits, and fleet electrification mandates, are driving direct demand for home and public charging cables at scale. Governments across Europe, North America, and Asia-Pacific are committing multi-billion-dollar investments to expand EV-ready infrastructure, creating sustained volume uplift for cable suppliers. On 9 October 2025, a Memorandum of Cooperation and Interaction was signed between the Electricity System Operator (ESO), its subsidiary ESO Charge, and the National Company ‘Railway Infrastructure’ (NRIC) to signify the launch of a national initiative aimed at creating a network of charging stations for EVs at railway stations throughout Bulgaria.

- Expansion of Public Charging Infrastructure: Rapid rollout of public and semi-public charging stations along highways, in parking structures, and at commercial destinations is driving large-scale procurement of tethered and portable charging cables in AC and DC fast configurations.

- Rising Demand for DC Fast Charging: Growing consumer and fleet operator demand for faster vehicle replenishment times is accelerating installations of DC fast-charging stations that require high-current, thermally managed, liquid-cooled cables. The global DC fast charging equipment market is expanding in parallel, creating a direct multiplier effect on premium cable demand.

- Smart Grid and V2G Integration: Increasing deployment of smart charging platforms supporting bidirectional power flow, demand response, and grid balancing is creating demand for advanced charging cables with integrated communication capabilities, smart connectors, and V2G-compatible specifications.

Market Restraints

- High Manufacturing and Compliance Costs: Production of high-current DC charging cables involves expensive materials, precision engineering for thermal management, and extensive certification processes under IEC, UL, and SAE standards. These costs limit affordability and restrict entry into the premium cable segment for smaller manufacturers.

- Lack of Standardization Across Regions: Fragmented charging connector standards require cable manufacturers to maintain multiple product variants, increasing tooling and inventory complexity. This lack of global harmonization constrains economies of scale and extends product qualification timelines.

- Raw Material Supply Chain Disruptions: Dependence on copper and aluminum, subject to significant price volatility and geopolitical supply risks, exposes cable manufacturers to margin compression and production planning challenges, particularly for high-current DC charging cable programs.

Market Opportunities

- Fleet Electrification and Commercial Charging: The rapid electrification of logistics, public transport, and commercial vehicle fleets is creating demand for ruggedized, high-cycle, and high-current charging cables tailored to 24/7 depot and on-route fast-charging operations.

- Emerging Markets in Asia-Pacific and Latin America: Rapidly growing EV ecosystems in India, Southeast Asia, and Latin America represent large untapped opportunities for affordable, standards-compliant AC and DC charging cable solutions aligned with evolving local infrastructure rollouts.

Market Challenges

- Connector Standard Fragmentation: The coexistence of multiple regional charging connector specifications increases product design complexity and manufacturing costs for cable suppliers, requiring broad compatibility across diverse electric vehicle and charging infrastructure ecosystems while limiting the emergence of a unified global standard.

- Product Life Cycle and Durability Pressures: EV charging cables used in public and commercial settings must withstand thousands of mating cycles, exposure to weather and UV, and high thermal stresses. Meeting durability and safety requirements while keeping costs competitive remains a persistent engineering and commercialization challenge.

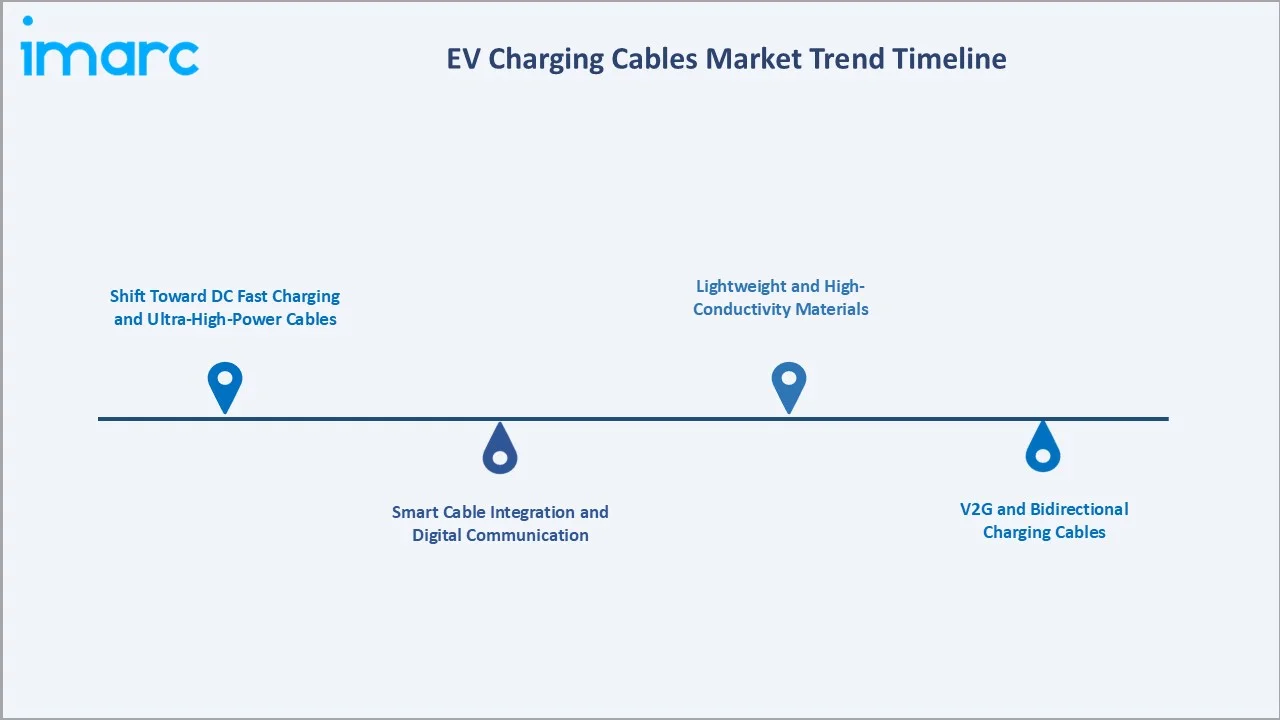

Emerging Market Trends

1. Shift Toward DC Fast Charging and Ultra-High-Power Cables

The accelerating deployment of 150 kW to 350 kW-class DC fast-charging stations is driving demand for advanced high-current cables with active liquid cooling systems. These cables represent a premium product category that requires specialized materials, precision manufacturing, and rigorous certification, positioning capable manufacturers for higher margin growth as the fast-charging network scales globally.

2. Smart Cable Integration and Digital Communication

Cable manufacturers are increasingly integrating advanced digital communication and smart charging capabilities into next-generation charging cables, enabling enhanced connectivity, automated authentication, and seamless interaction between electric vehicles and charging infrastructure. Smart cable platforms enable plug-and-charge functionality, automated billing, and grid-responsive demand management, aligning with the evolving requirements of smart charging infrastructure operators.

3. Lightweight and High-Conductivity Materials

Research and development in aluminum alloy conductors, carbon nanotube-enhanced wiring, and high-performance polymer insulations is enabling manufacturers to produce lighter, more flexible charging cables without compromising current-carrying capacity or thermal performance. Weight reduction is particularly valued in portable and vehicle-supplied cable segments.

4. V2G and Bidirectional Charging Cables

V2G and bidirectional charging applications require cables and connectors engineered for sustained bidirectional power flow, reinforced insulation, and enhanced communication protocols. As utilities and grid operators expand V2G pilot programs across Europe, Japan, and North America, demand for compliant bidirectional charging cable solutions is expected to grow substantially through the forecast period.

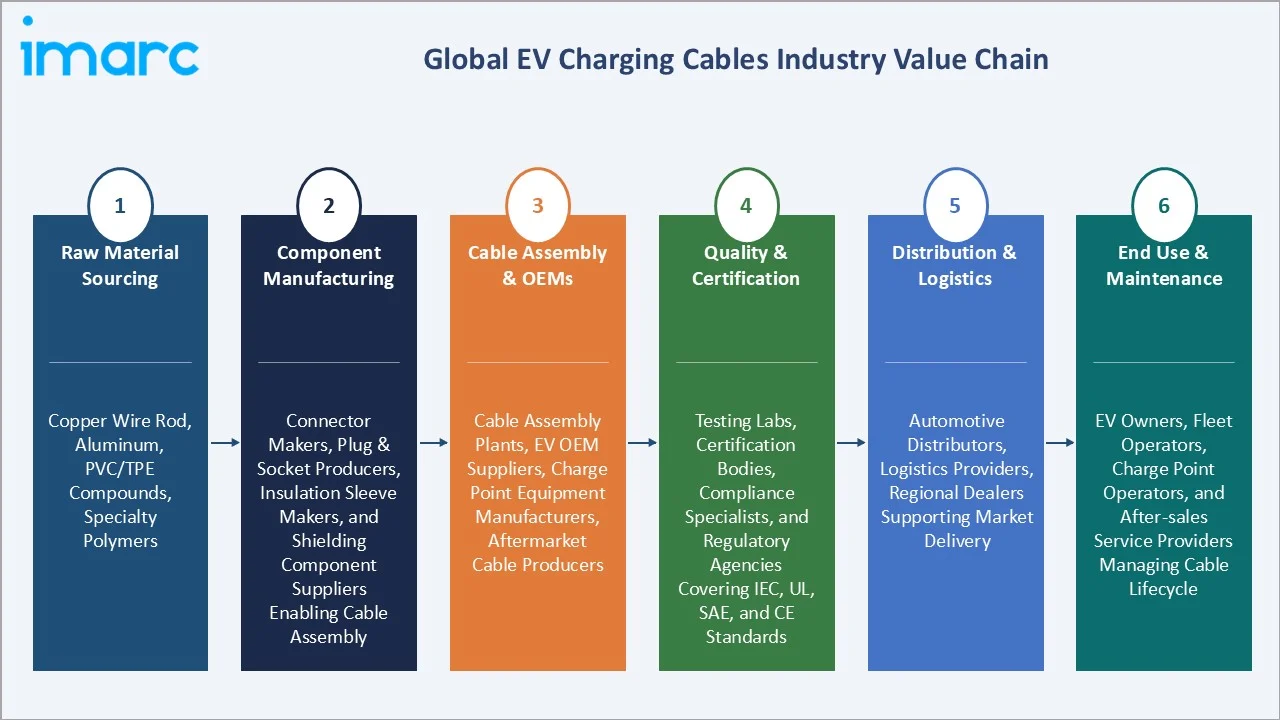

Industry Value Chain Analysis

The EV charging cables market value chain spans six stages from raw material sourcing through end-user deployment and lifecycle management. Cable assembly, certification, and distribution capture the highest value-add, while compliance and smart integration capabilities are increasingly determining competitive differentiation across the ecosystem.

|

Stage |

Key Players / Examples |

|

Raw Material Sourcing |

Copper wire rod producers, aluminum suppliers, PVC/TPE compound makers, and specialty polymer suppliers providing base materials for cable construction |

|

Component Manufacturing |

Connector manufacturers, plug and socket producers, insulation sleeve makers, and shielding component suppliers enabling cable assembly |

|

Cable Assembly & OEMs |

Cable assembly plants, EV OEM suppliers, charge point equipment manufacturers, and aftermarket cable producers |

|

Quality & Certification |

Testing laboratories, certification bodies, compliance specialists, and regulatory agencies covering IEC, UL, SAE, and CE standards |

|

Distribution & Logistics |

Automotive and industrial distributors, logistics providers, wholesalers, and regional dealers supporting market delivery |

|

End Use & Maintenance |

EV owners, fleet operators, charge point operators, and after-sales service providers managing cable lifecycle |

Vertically integrated players owning proprietary material compounding, assembly, and testing capabilities are positioned to capture greater margin than partners relying on third-party material or certification services.

Technology Landscape in the EV Charging Cables Industry

High-Current Conductors and Thermal Management

The shift to DC fast charging is driving innovation in large-diameter copper conductors, aluminum-copper composites, and active liquid-cooling systems embedded within cable structures. Liquid-cooled charging cables enable ultra-thin, highly flexible form factors at 350 kW-plus power levels, improving user experience and enabling high-cycle commercial deployments.

Advanced Insulation and Jacket Materials

TPE, cross-linked polyethylene (XLPE), and silicone-based compound technologies are replacing traditional PVC insulations in premium cable segments. These materials deliver superior flexibility at low temperatures, better UV and oil resistance, longer service life in outdoor and high-cycle environments, and compliance with stricter flame-retardancy and halogen-free requirements.

Connector Durability and Mating Cycle Innovation

High-durability connectors with enhanced resistance to wear, corrosion, and environmental exposure, along with secure locking mechanisms, are becoming increasingly important for commercial and public charging applications that experience frequent and intensive usage. Material science advances in silver-plated and gold-contact technologies, combined with precision molded housings, are extending service intervals and reducing total cost of ownership for infrastructure operators.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Cable Length |

Below 5 Meter |

🔒 |

2025 |

|

Shape |

Straight |

63.7% |

2025 |

|

Charging Level |

Level 1 |

47.6% |

2025 |

|

Power Type |

AC Charging |

🔒 |

2025 |

|

Application |

Private Charging |

🔒 |

2025 |

|

Region |

Asia-Pacific |

44.6% |

2025 |

By Shape

Straight commands a 63.7% majority share in 2025, driven by its widespread use in tethered AC wall-box and pedestal-type chargers, vehicle-supplied portable cables, and public AC charging installations. Its simple linear design, lower manufacturing cost, and compatibility with standard cable management accessories make it the default choice across residential, commercial, and public AC charging segments.

To access detailed market analysis, Request Sample

Coiled at 36.3% in 2025 serves premium and portable charging markets, offering self-retracting, tangle-free handling valued in vehicle-supplied chargers, portable emergency kits, and commercial multi-port charging stations.

By Charging Level

Level 1 dominates with 47.6% share in 2025, reflecting its widespread adoption in residential and workplace charging applications, where standard electrical infrastructure and lower-cost cable solutions make it the preferred choice for everyday EV charging.

Level 2 at 32.4% is the second largest mainstream tier, driven by its growing adoption in commercial, workplace, retail, and public charging environments where faster charging speeds and greater convenience are increasingly prioritized.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

44.6% |

Rapid EV adoption in China and India, government EV mandates, strong automotive manufacturing base, and expanding public charging networks |

|

Europe |

26.3% |

Stringent emission regulations, accelerating EV penetration, robust charging infrastructure investment, and active standardization bodies |

|

North America |

18.5% |

Growing federal and state EV incentives, expanding highway charging corridors, strong consumer EV demand, and rising fleet electrification |

|

Latin America |

5.4% |

Nascent EV adoption, growing government incentive programs, rising urban mobility needs, and increasing charging infrastructure buildout |

|

Middle East and Africa |

5.2% |

Emerging EV policies, expansion of smart city initiatives, growing renewable energy integration, and gradual EV infrastructure development |

Asia-Pacific at 44.6% in 2025 leads the regional landscape, anchored by China's world-leading EV production and sales, India's expanding EV policy framework under FAME and state EV schemes, and rapidly growing charging network buildouts across South Korea, Japan, and Southeast Asia. Dense OEM manufacturing, deep supply chain integration, and strong government mandates support sustained regional leadership.

Europe at 26.3% is the second largest regional market, driven by the EU's strict CO2 fleet emission standards and strong consumer EV adoption in Germany, France, Netherlands, Norway, and the United Kingdom.

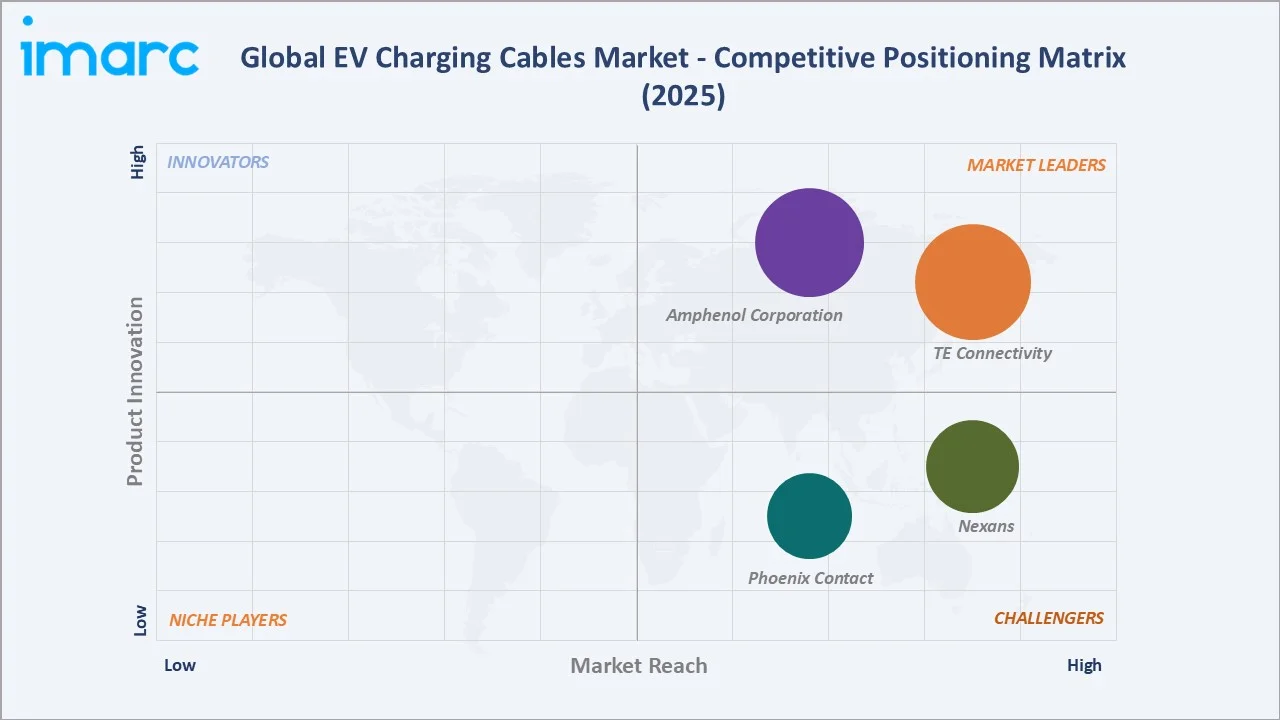

Competitive Landscape

The EV charging cables market is moderately fragmented, with global cable conglomerates and specialized EV connectivity players competing on product breadth, certification coverage, manufacturing scale, and smart cable technology. Brand strength, multi-standard product capability, vertically integrated manufacturing, and regulatory readiness form the key competitive moats as the market scales rapidly.

|

Company Name |

Key Products / Brands |

Market Position |

Core Strength |

| TE Connectivity | AMP, HIVONEX |

Leader |

Strengthening connector and cable assembly leadership through integrated EV charging system solutions |

| Amphenol Corporation | ER Series SAE J1772, CHARGESOK |

Leader |

Growing EV charging cable and connector presence across automotive and industrial charging segments |

| Nexans | Electric Vehicle Charging Solutions |

Challenger |

Expanding dedicated EV charging cable portfolio through infrastructure-grade product lines and European market coverage |

| Phoenix Contact | CHARX connect eco |

Challenger |

Deploying specialist EV charging cable and connector solutions across AC, DC fast, and ultra-high-power charging segments |

Key players include TE Connectivity, Amphenol Corporation, Nexans, and Phoenix Contact, among others.

Key Company Profiles

TE Connectivity

TE Connectivity is a global technology company specializing in connectivity and sensor solutions. The company is an established supplier of EV charging connectors, terminals, and integrated cable assemblies used across residential, commercial, and fast-charging applications worldwide, serving automotive OEMs and charge point operators across major markets.

- Product Portfolio: AMP+ Charging Inlets Type 2 cable assemblies and HIVONEX connector and charging solutions for high-voltage EV applications, covering AC and DC charging infrastructure for passenger vehicles and commercial fleets.

- Recent Developments: TE Connectivity has been expanding its EV charging product range with higher-current connector and cable solutions aligned with evolving CCS and NACS adoption trends and has been scaling its automated assembly capabilities for EV charging cable programs.

- Strategic Focus: Growing integrated EV charging cable and connector system solutions, deepening OEM supply partnerships, and advancing thermal management technologies for next-generation ultra-high-power charging applications.

Nexans

Nexans is a global leader in cable and optical fiber manufacturing, headquartered in Paris, France. The company supplies a dedicated range of EV charging cables and infrastructure cabling solutions, serving residential, commercial, and public charging segment customers across Europe and global markets.

- Product Portfolio: EV charging cables and infrastructure connection solutions under the Nexans Electric Vehicle Charging Solutions range, covering AC charging cables for home, workplace, and public charging point installations.

- Recent Developments: Nexans has been expanding its EV charging cable portfolio and investing in production capacity to support the growing deployment of public and commercial charging infrastructure across European and global markets.

- Strategic Focus: Growing the dedicated EV charging cable product range, strengthening supply to charge point operators and grid operators, and expanding European manufacturing capacity to serve increasing demand for standards-compliant EV charging infrastructure cables.

Phoenix Contact

Phoenix Contact is a German industrial automation and electrification technology company. The company is an established specialist in EV charging cable and connector solutions for AC, DC fast, and ultra-high-power charging infrastructure.

- Product Portfolio: CHARX connect eco AC charging cables for residential and commercial EV charging applications.

- Recent Developments: Phoenix Contact has been expanding its CHARX product ecosystem with new DC fast-charging and ultra-high-power cable solutions, and has been growing its partnerships with charge point equipment manufacturers and commercial fleet charging operators globally.

- Strategic Focus: Leveraging deep industrial connectivity expertise to deliver integrated EV charging cable and connector solutions, growing CHARX product coverage across AC and DC charging segments, and expanding the EV charging infrastructure supply business in North American and European markets.

Market Concentration Analysis

The EV charging cables market is moderately fragmented, with global cable conglomerates commanding significant shares of the professional-grade AC and DC charging cable segments, while a broad range of regional manufacturers and specialty suppliers compete in entry-level residential and portable cable markets.

Barriers to entry include high capital requirements for certified manufacturing facilities, lengthy product testing and regulatory approval processes, and the need to develop products compatible with multiple regional charging systems. These factors favor established manufacturers with proven production capabilities, broad certification expertise, and scalable global operations.

Consolidation is progressing as larger cable and connectivity groups acquire EV-specialized manufacturers and technology platforms to fill product gaps in smart cable, high-power DC, and liquid-cooled cable segments. Strategic collaborations between cable suppliers and EV OEMs, charging network operators, and grid technology providers are further reinforcing competitive positioning in the premium and fast-charging cable market tiers.

Investment & Growth Opportunities

Fastest-Growing Segments

Level 3 is growing the fastest among the charging level segments, driven by accelerating highway fast-charging network deployments and commercial fleet charging requirements. Coiled is the fastest-growing shape sub-segment, fueled by rising premium portable cable demand and multi-port commercial charging station requirements. Both segments represent high-value, high-margin product opportunities for manufacturers with advanced thermal management and materials capabilities.

Emerging Markets

Europe is the fastest-growing major region, anchored by accelerating electric vehicle adoption, stringent sustainability regulations, and rising investments in high-power charging networks across commercial and residential applications. Asia-Pacific outside China, particularly India, Southeast Asia, and South Korea, represents significant untapped opportunity for affordable, compliant AC and DC charging cable solutions aligned with growing domestic EV infrastructure investments.

Venture & Investment Trends

Capital investment is concentrating in smart charging cable technology platforms, liquid-cooled ultra-high-power cable systems, V2G-compatible cable solutions, and advanced materials for next-generation lightweight cable designs. Infrastructure-oriented investors are also directing capital toward charging cable supply chain localization programs in Europe and North America to reduce dependence on Asian cable component supply chains.

Future Market Outlook (2026-2034)

The EV charging cables market is forecast to expand from USD 1.46 Billion in 2025 to USD 6.57 Billion by 2034 at a CAGR of 18.18%, adding roughly USD 5.11 Billion in incremental annual market value over the forecast period.

Four forces will shape the market through 2034: accelerating global EV adoption and charging infrastructure mandates; the rise of DC fast charging, smart cable, and V2G applications; growing standardization around NACS and CCS connector ecosystems; and the shift toward lightweight, high-conductivity, and thermally managed cable materials for ultra-high-power charging platforms.

By 2034, the EV charging cables market is expected to be defined by premium smart cable platforms, compliant multi-standard product portfolios, and vertically integrated manufacturing positioned to serve both global OEM supply chains and regional charging infrastructure operators at scale.

Research Methodology

Primary Research

Primary research included structured interviews with EV charging cable manufacturers, automotive OEM procurement teams, charge point equipment suppliers, certification specialists, and distribution channel partners, validating market sizing, segment evolution, regional demand trends, and competitive dynamics.

Secondary Research

Secondary sources included International Energy Agency (IEA) EV Outlook publications, European Commission Alternative Fuels Infrastructure Regulation documents, US Department of Energy charging infrastructure reports, IEC and SAE standard publications, company annual reports, press releases, and industry association data from CharIN, ACEA, and national EV industry bodies.

Forecasting Models

Market forecasts used bottom-up and top-down models combining EV fleet size projections, charging point installation rates by level, average cables per charging point, regional EV adoption trajectories, and pricing trend analysis. Scenario analysis addressed regulatory pace, connector standard consolidation, and raw material cost dynamics.

EV Charging Cables Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Cable Lengths Covered | Below 5 Meter, 6 Meter to 10 Meter, Above 10 Meter |

| Shapes Covered | Straight, Coiled |

| Charging Levels Covered | Level 1, Level 2, Level 3 |

| Power Types Covered | AC Charging, DC Charging |

| Applications Covered | Private Charging, Public Charging |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | TE Connectivity, Amphenol Corporation, Nexans, Phoenix Contact, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the EV charging cables market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global EV charging cables market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the EV charging cables industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the EV Charging Cables Market Report

The EV charging cables market was valued at USD 1.46 Billion in 2025, driven by rapid EV adoption, expanding charging infrastructure, and growing demand for DC fast-charging cable solutions.

The market is projected to grow at 18.18% CAGR from 2026-2034, reaching USD 6.57 Billion, supported by DC fast-charging expansion and smart cable technology adoption.

Straight leads at 63.7% in 2025, driven by its widespread use in tethered AC wall-box and pedestal chargers, residential installations, and public AC charging stations.

Level 1 dominates at 47.6% in 2025, reflecting the large global residential charger base. Its widespread compatibility with standard household electrical infrastructure and suitability for overnight charging continue to support strong demand for Level 1 charging cables.

Asia-Pacific commands 44.6% in 2025, led by China's dominant EV market, India's accelerating EV push, and rapidly expanding charging network deployments across the region.

Leading players include TE Connectivity, Amphenol Corporation, Nexans, and Phoenix Contact, among others.

Government EV mandates, charging infrastructure investment programs, and connector standardization regulations directly drive large-scale procurement of compliant cables across residential, commercial, and public charging applications.

Key challenges include regional connector standard fragmentation, high certification costs, raw material price volatility, and the engineering demands of developing durable, high-cycle cables for commercial charging environments.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)