Eyewear Market Size, Share, Trends and Forecast by Product, Gender, Distribution Channel, and Region, 2026-2034

Global Eyewear Market Size, Share, Trends & Forecast (2026-2034)

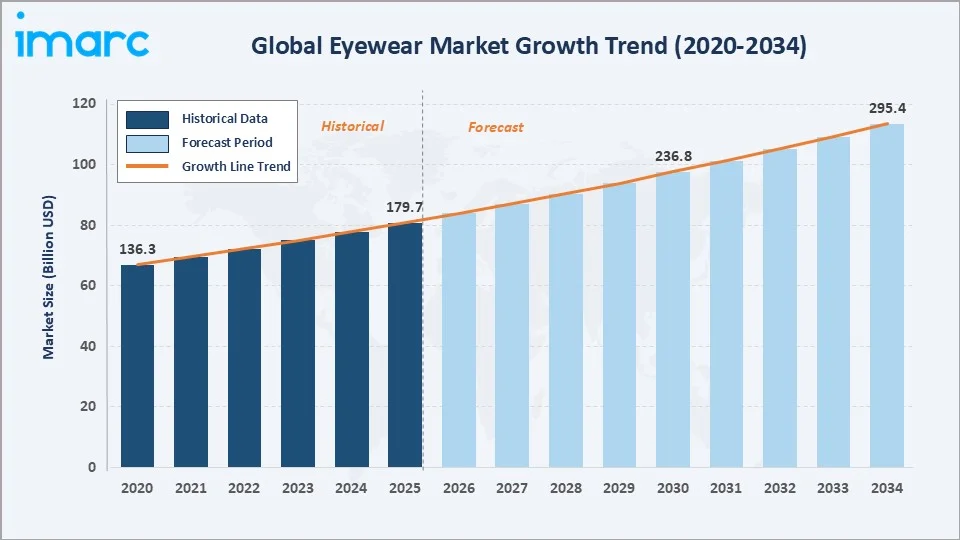

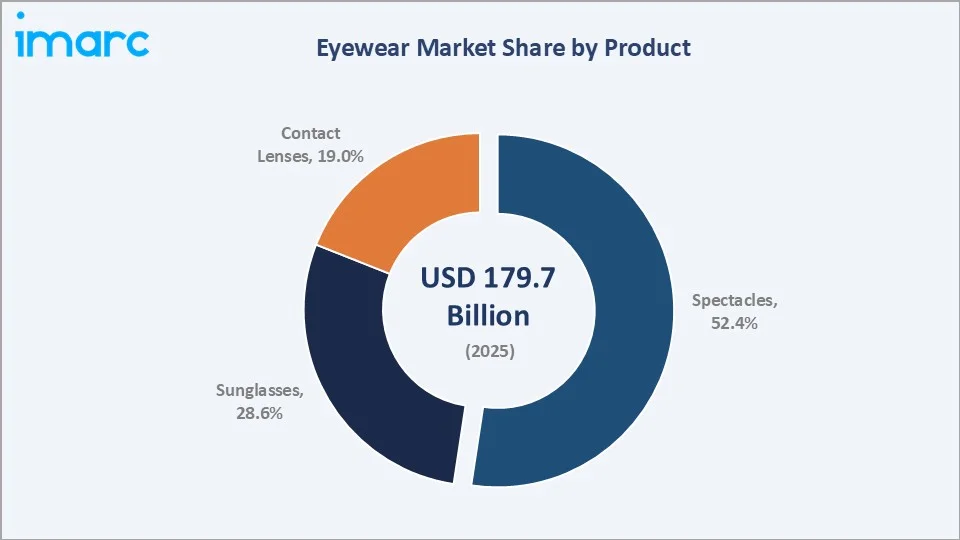

The global eyewear market size reached USD 179.7 Billion in 2025 and is projected to reach USD 295.4 Billion by 2034, exhibiting a CAGR of 5.68% during 2026-2034. Rising prevalence of visual impairments, growing fashion-driven demand, rapid technological advancements, and increasing accessibility of eye care services are the primary forces driving market growth.

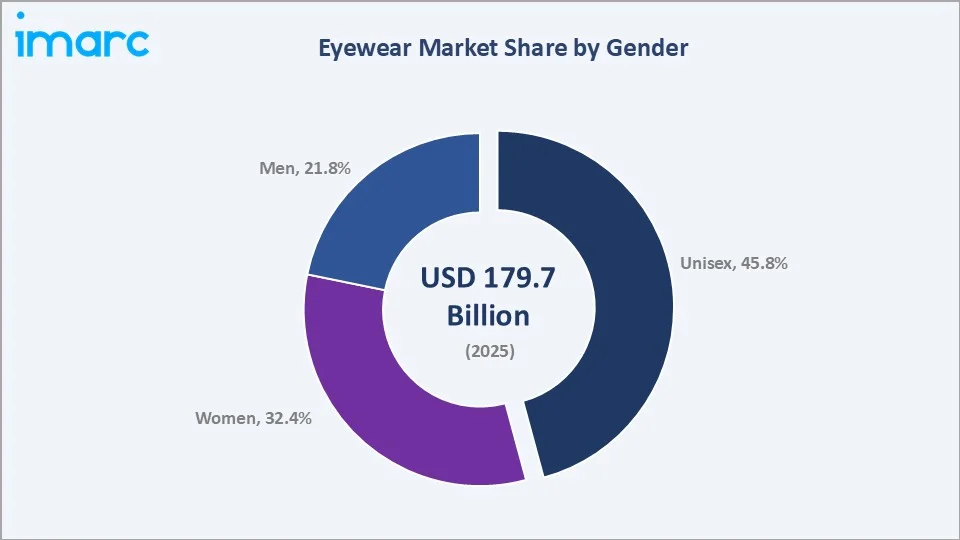

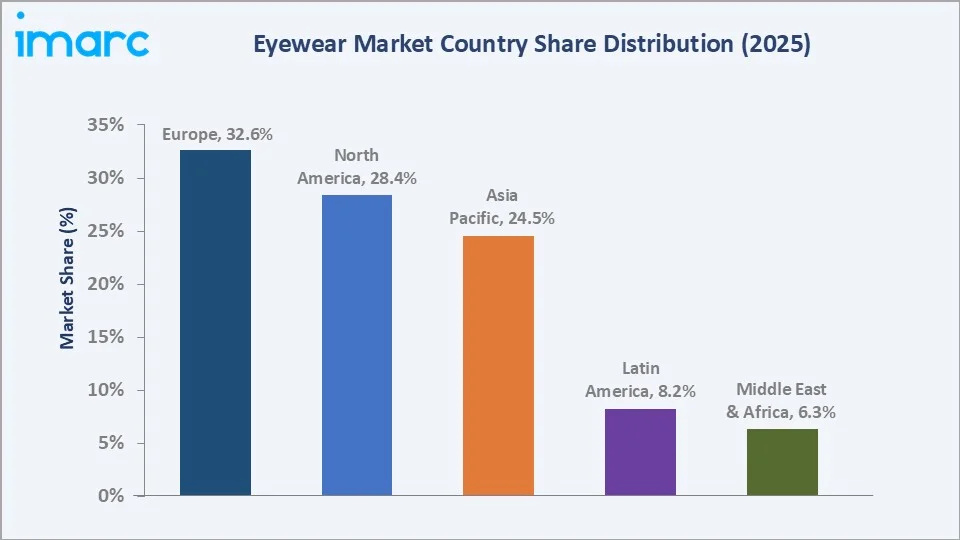

Spectacles dominate the product mix at 52.4% in 2025, while the unisex segment leads by gender at 45.8%. Europe commands a dominant 32.6% regional share in 2025, reflecting its strong fashion culture and advanced healthcare infrastructure.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 179.7 Billion |

|

Forecast Market Size (2034) |

USD 295.4 Billion |

|

CAGR (2026-2034) |

5.68% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Europe (32.6% share, 2025) |

|

Second Region |

North America (28.4% share, 2025) |

|

Leading Product |

Spectacles (52.4%, 2025) |

|

Leading Gender Segment |

Unisex (45.8%, 2025) |

The global eyewear market growth trajectory from 2020 through 2034, with historical expansion to USD 179.7 Billion in 2025, reflects consistent healthcare and fashion-driven demand, while the forecast to USD 295.4 Billion captures accelerating e-commerce penetration, technological product innovation, and Asia-Pacific vision care market expansion.

To get more information on this market, Request Sample

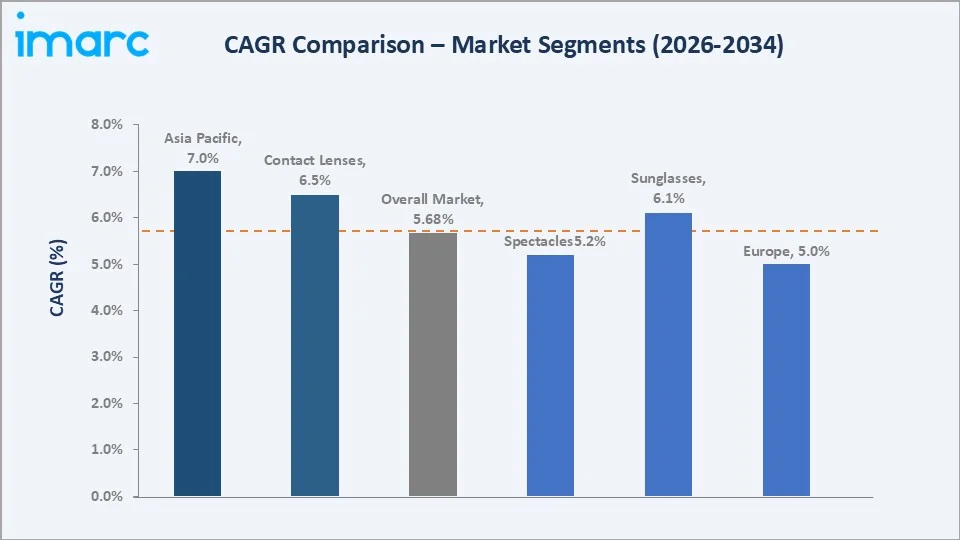

The CAGR trajectories across key product, gender, and regional sub-segments, with Contact Lenses at ~6.5% CAGR and Asia Pacific at ~7.0% CAGR, are the fastest-growing categories within the global eyewear industry analysis through 2034.

Executive Summary

The global eyewear market is on a sustained growth trajectory from USD 179.7 Billion in 2025 to USD 295.4 Billion by 2034. Eyewear encompasses a wide range of vision correction and protective products, such as spectacles, sunglasses, and contact lenses, serving both medical and fashion purposes across all demographic groups.

Spectacles dominate product at 52.4% in 2025, driven by the substantial global population requiring vision correction. Contact lenses (19.0%) represent the fastest-growing product segment at ~6.5% CAGR, fueled by increasing patient comfort with lens care routines, extended-wear innovations, and daily disposable adoption. Sunglasses (28.6%) combine UV protection with fashion positioning, commanding premium pricing globally.

Europe dominates at 32.6% in 2025, combining strong optical retail infrastructure, fashion-forward consumer preferences, and mature healthcare systems. North America (28.4%) and Asia Pacific (24.5%) follow, with Asia Pacific emerging as the fastest-growing region driven by rapidly expanding middle-class populations and unmet vision care needs.

Key Market Insights

|

Insight |

Data |

|

Leading Product |

Spectacles – 52.4% share (2025) |

|

Fastest-Growing Product |

Contact Lenses – ~6.5% CAGR (2026-2034) |

|

Leading Gender Segment |

Unisex – 45.8% revenue share (2025) |

|

Leading Region |

Europe – 32.6% revenue share (2025) |

|

Second Region |

North America – 28.4% revenue share (2025) |

|

Top Companies |

Alcon Inc., De Rigo Spa, EssilorLuxottica, Fielmann Group AG, Hoya Corporation, Johnson & Johnson, Marchon Eyewear, Inc., Safilo Group S.P.A. |

Key Analytical Observations Expanding On The Above Data:

- Spectacles, with 52.4% in 2025, dominate because approximately 2.2 billion people globally have a vision impairment, the majority correctable with prescription eyewear. The product category benefits from both recurring replacement demand and premiumization through coatings, materials, and designer brand licensing.

- Contact lenses, with 19.0% in 2025, are growing fastest at ~6.5% CAGR through 2034, driven by daily disposable format adoption across younger demographics, expanded silicone hydrogel material innovation offering superior oxygen transmission, and growing toric lens penetration for astigmatism correction.

- Europe's 32.6% dominance in 2025 reflects multiple structural advantages: the region hosts global luxury eyewear design hubs in Italy (Luxottica, Safilo, De Rigo), advanced optical retail chains (Specsavers, Fielmann), and consumer willingness to pay premium prices for designer frames as fashion accessories.

- North America, with 28.4% in 2025, is driven by the US optical retail market with around 44,850 optical dispensing locations, robust vision insurance penetration, and leading contact lens adoption rates globally.

Global Eyewear Market Overview

Eyewear encompasses optical products designed to correct vision, protect eyes, or serve as fashion accessories. The product categories include prescription spectacles (ophthalmic frames with corrective lenses), sunglasses (UV-protective lenses in fashion and performance frames), and contact lenses (soft, rigid gas-permeable, and specialty therapeutic lenses).

The global ecosystem integrates raw material suppliers (acetate, titanium, polycarbonate), frame and lens manufacturers, brand and design houses, optical retailers and e-commerce platforms, eye care professionals (optometrists, ophthalmologists), and diverse end-use segments spanning vision correction, UV protection, sports performance, and fashion accessories.

Market Dynamics

To evaluate market opportunities, Request Sample

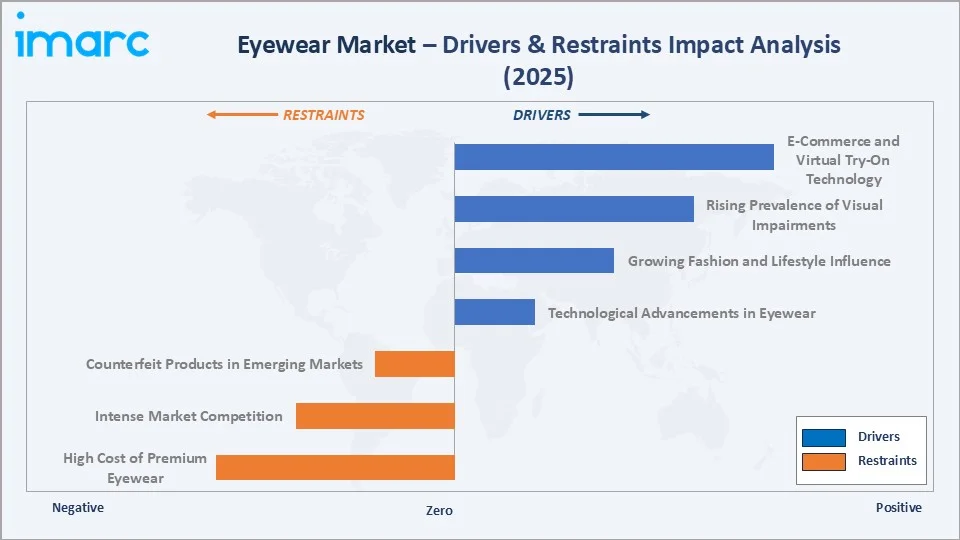

Market Drivers

- Rising Prevalence of Visual Impairments and Eye Disorders: According to the WHO, approximately 2.2 billion people globally have a vision impairment or blindness, of whom at least 1 billion have a preventable or not yet addressed condition, creating sustained corrective eyewear demand.

- Growing Fashion and Lifestyle Influence: The convergence of eyewear with fashion accessories, driven by luxury brand licensing agreements and designer collaborations, is expanding the market beyond purely functional vision correction into premium-priced lifestyle products.

- Technological Advancements in Lens Technology: The development of blue-light blocking lenses, photochromic lenses, progressive addition lenses, and high-index lens materials is driving consumers toward more frequent frame upgrades and higher average selling price transactions.

Market Restraints

- High Cost of Premium Eyewear: The significant retail price premium commanded by branded optical frames, with designer frames retailing at USD 300–700+, restricts market participation in price-sensitive emerging economies and limits replacement frequency among cost-conscious consumers.

- Intense Competition and Market Consolidation: The dominance of EssilorLuxottica, which controls both the largest frame brand portfolio and the largest lens manufacturing operation globally, creates significant barriers for independent retailers and smaller brand operators to compete on pricing and distribution scale.

Market Opportunities

- E-Commerce and Virtual Try-On Technology: The rapid adoption of AI-powered virtual try-on tools is eliminating traditional barriers to online eyewear purchasing, opening a high-margin direct-to-consumer distribution channel with significantly lower infrastructure costs than brick-and-mortar optical retail.

- Untapped Vision Care Markets in Asia and Africa: With over 800 million people in low- and middle-income countries lacking access to affordable vision correction, entry into emerging markets through affordable product lines and community-based screening programs represents a substantial growth opportunity.

Market Challenges

- Counterfeit and Gray Market Products: The proliferation of counterfeit eyewear products, particularly in online marketplaces and emerging market retail channels, erodes brand equity and creates safety risks for consumers, as counterfeit lenses frequently fail UV protection standards.

- Shifting Consumer Preferences and Laser Correction Alternatives: The growing adoption of LASIK and other refractive correction surgeries reduces the addressable population requiring corrective lenses over time, creating a structural headwind for the prescription eyewear segment in high-income markets.

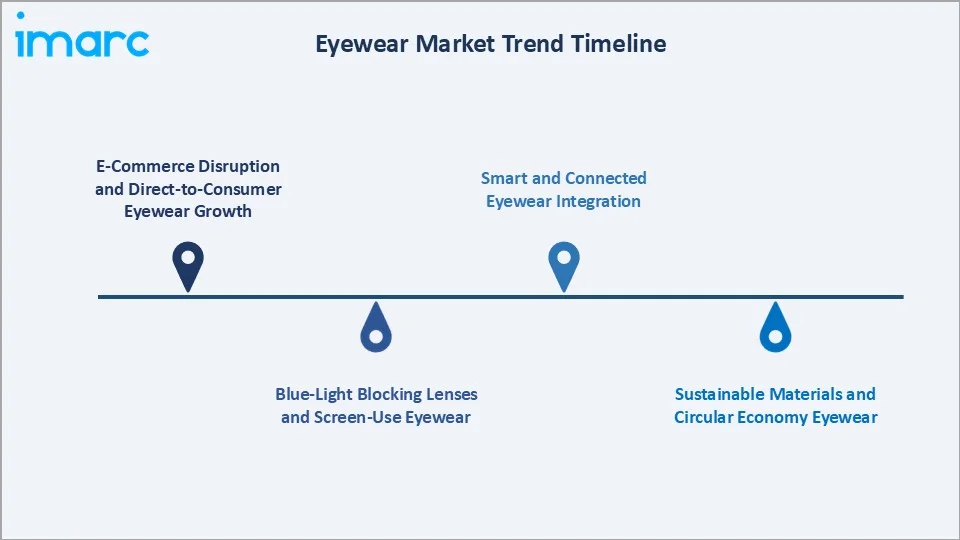

Emerging Market Trends

1. E-Commerce Disruption and Direct-to-Consumer Eyewear Growth

The direct-to-consumer eyewear segment, pioneered by Warby Parker, has expanded globally. Virtual try-on technology, home try-on programs, and online prescription verification tools are accelerating consumer comfort with online optical retail, reshaping the traditional optician-led distribution model.

2. Blue-Light Blocking Lenses and Screen-Use Eyewear

The explosion in screen time driven by remote work adoption and mobile device usage is generating consumer demand for blue-light blocking lens coatings and computer vision syndrome-addressing lens designs. This trend is converting previously non-eyewear users into customers seeking screen-specific optical products.

3. Smart and Connected Eyewear Integration

Smart eyewear incorporating augmented reality displays, health monitoring sensors, and voice-activated AI assistants is emerging as a high-growth adjacent category. Meta's Ray-Ban Stories collaboration and Google Glass Enterprise Edition are validating enterprise and consumer smart eyewear use cases.

4. Sustainable Materials and Circular Economy Eyewear

Environmental sustainability mandates and millennial and Gen Z consumer preferences are driving adoption of bio-acetate, recycled ocean plastic, and plant-based lens material innovations across premium eyewear brands. Subscription and frame recycling programs are emerging in optical retail as circular economy-aligned business models.

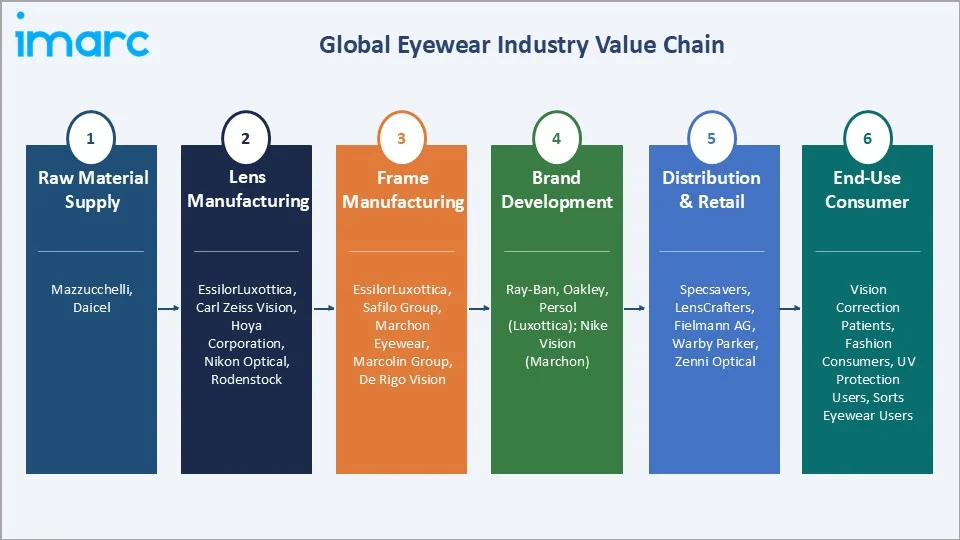

Industry Value Chain Analysis

The eyewear value chain spans six stages from raw material input through end-use consumption. Lens manufacturing and brand development capture the highest value-add margins, while optical retail and eye care professional channels generate significant revenue from service-bundled product sales.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Mazzucchelli, Daicel |

|

Lens Manufacturing |

EssilorLuxottica, Carl Zeiss Vision, Hoya Corporation, Nikon Optical, Rodenstock |

|

Frame Manufacturing |

EssilorLuxottica, Safilo Group S.p.A., Marchon Eyewear, Marcolin Group, De Rigo Vision |

|

Brand Development |

Ray-Ban, Oakley, Persol (Luxottica); Nike (Marchon) |

|

Distribution & Retail |

Specsavers, LensCrafters (Luxottica), Fielmann AG, Warby Parker, Zenni Optical |

|

End-Use Consumer |

Vision correction patients, fashion consumers, UV protection users, sports/performance eyewear users |

Technology Landscape in the Eyewear Industry

Advanced Lens Manufacturing and Coating Technologies

Free-form digital surfacing now dominates premium ophthalmic lens production, where computer-controlled generators produce back-surface geometries with sub-micron precision across progressives, single-vision, and occupational designs. Anti-reflective coatings deposited via vacuum magnetron sputtering achieve less than 0.2% residual reflection across the visible spectrum, with hydrophobic and oleophobic outer layers enhancing smudge resistance for everyday use.

Smart Eyewear and Integrated Electronics

Waveguide-based augmented reality displays embedded in conventional-profile frames use diffractive optical elements to project high-resolution imagery at luminance levels exceeding 3,000 units without degrading ambient vision. Open-ear directional audio systems integrated into temple arms are achieving IP54-rated durability, enabling brand owner positioning at the intersection of performance optics and wearable technology.

Sustainable Material Innovation: Bio-Based and Recycled Frames

Bio-acetate formulations derived from cotton fiber and wood pulp plasticizers are replacing petroleum-based cellulose acetate in premium frame production without compromising optical clarity or mechanical flex characteristics. Post-consumer recycled nylon and ocean-recovered plastic compounds are gaining certification traction for sports and lifestyle eyewear segments across North America and Europe.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product | Spectacles | 52.4% | 2025 |

| Gender | Unisex | 45.8% | 2025 |

| Distribution Channel | Optical Stores | 🔒 | 2025 |

| Region | Europe | 32.6% | 2025 |

By Product

Spectacles command a 52.4% majority share in 2025 owing to the large global population requiring vision correction and the recurring replacement demand cycle. The product segment benefits from both functional necessity and premiumization through designer brand licensing, blue-light blocking coatings, and progressive lens technology upgrades, making spectacle purchasing a high-frequency consumer interaction across optical retail channels.

To access detailed market analysis, Request Sample

Sunglasses at 28.6% in 2025 represent the highest-margin product category, combining UV protection functionality with fashion positioning. Contact lenses (19.0%) represent the fastest-growing segment, driven by daily disposable convenience, improved silicone hydrogel materials, and expanding specialty lens categories including orthokeratology and cosmetic lenses.

By Gender

The unisex segment dominates at 45.8% in 2025, reflecting the growing fashion industry trend toward gender-neutral design and inclusive sizing in eyewear frames. Major luxury brands are progressively expanding unisex collections to capture both male and female purchasers with single product line investments, reducing inventory complexity while broadening appeal.

The women's segment at 32.4% in 2025 reflects women's higher engagement with eyewear as fashion accessories and greater brand responsiveness to style trends, driving higher average frame replacement rates than the men's segment. Men's eyewear (21.8%) is experiencing growth through sports performance eyewear, premium optical retail channel expansion, and growing male consumer engagement with fashion eyewear as status accessories.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Europe |

32.6% |

Strong fashion heritage; mature optical retail; luxury brand hubs in Italy; premium pricing acceptance |

|

North America |

28.4% |

Vision insurance penetration; large contact lens market; e-commerce disruption; aging population demand |

|

Asia Pacific |

24.5% |

Highest myopia prevalence globally; expanding middle class; growing eye care infrastructure; Korea/Japan fashion influence |

|

Latin America |

8.2% |

Rising healthcare expenditure; Brazil optical retail growth; increasing sunglass demand in high UV regions |

|

Middle East & Africa |

6.3% |

GCC luxury eyewear consumption; unmet vision care needs in Africa; UV protection sunglass demand |

Europe's 32.6% market dominance in 2025 is driven by Italy's position as the global center of luxury eyewear manufacturing, hosting Luxottica and Safilo, two of the world's three largest eyewear companies, alongside a deeply embedded optical retail culture and consumer willingness to allocate significant discretionary spend to eyewear as a fashion statement.

North America, with 28.4% in 2025, is characterized by the highest contact lens penetration globally, a mature vision insurance ecosystem, and strong e-commerce disruption from direct-to-consumer brands like Warby Parker and Zenni Optical.

Competitive Landscape

The global eyewear market is moderately concentrated, with EssilorLuxottica holding the dominant global position through integrated lens manufacturing and frame brand ownership. Regional specialists and luxury brand license holders compete across premium segments, while e-commerce disruptors address price-sensitive segments directly.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

Alcon Inc. |

Contact Lenses |

Leader |

Global contact lens + surgical; premium daily disposable; expanding emerging markets |

|

De Rigo Spa |

Police, Lozza, Sting, Yalea |

Challenger |

Italy-based; mid-premium frames; European & Middle East distribution |

|

EssilorLuxottica |

Ray-Ban, Oakley, Persol; Varilux, Crizal |

Leader |

Dominant global integrated leader; vertically integrated lenses + frames + retail |

|

Fielmann Group AG |

Sunglasses, Glasses, Contact Lenses, Progressive Lenses |

Leader |

Germany; value optical retail chain; expanding pan-European and US footprint |

|

Hoya Corporation |

Contact Lenses, Eyeglass Lenses |

Leader |

Japan; global premium lens manufacturer; anti-reflective and blue-light lens focus |

|

Johnson & Johnson |

Acuvue contact lens range |

Leader |

Global leader in contact lenses; daily disposable innovation; eye health focus |

|

Marchon Eyewear, Inc. |

Nike Vision, Calvin Klein, Lacoste |

Leader |

US-based; largest independent frame company; broad license portfolio across lifestyle categories |

|

Safilo Group S.P.A. |

Smith, Carrera, Polaroid frames |

Leader |

Italy; premium frame manufacturing; brand portfolio restructuring toward owned brands |

Key players include Alcon Inc., De Rigo Spa, EssilorLuxottica, Fielmann Group AG, Hoya Corporation, Johnson & Johnson, Marchon Eyewear, Inc., Safilo Group S.P.A., and others.

Key Company Profiles

EssilorLuxottica

EssilorLuxottica is the world's largest eyewear company, formed by the 2018 merger of Essilor International and Luxottica Group. Headquartered in Paris and Milan, the company combines the world's leading prescription lens manufacturer with the world's largest frame and optical retail group, creating a uniquely vertically integrated position spanning the entire eyewear value chain.

- Product Portfolio: Ray-Ban, Oakley, Persol, Oliver Peoples frames; Varilux progressive lenses; Crizal anti-reflective coatings; LensCrafters, Sunglass Hut, Salmoiraghi & Viganò retail chains.

- Recent Developments: In March 2026, EssilorLuxottica and Meta Platforms strengthened their collaboration by broadening their portfolio of AI-powered smart glasses. Building on the success of earlier products like Ray-Ban Meta, the partnership aims to introduce a wider range of eyewear that blends advanced artificial intelligence with stylish, wearable design. By combining EssilorLuxottica’s expertise in eyewear design, manufacturing, and global distribution with Meta’s capabilities in AI and software, the companies are positioning smart glasses as a mainstream consumer technology.

- Strategic Focus: EssilorLuxottica's strategy leverages its unique vertical integration — from lens blank manufacturing through brand development, optical retail, and direct e-commerce — to capture margin at every stage of the value chain while protecting its brand portfolio from distribution channel conflicts through wholly-owned retail control.

Johnson & Johnson

Johnson & Johnson, that operates through Johnson & Johnson Vision Care, is one of the global leaders in soft contact lenses through the Acuvue brand family, with a product portfolio spanning daily disposable, extended wear, multifocal, and toric contact lenses distributed through eye care professional channels globally.

- Product Portfolio: Acuvue Oasys, Acuvue Moist, Acuvue Vita, Acuvue Define cosmetic lenses.

- Recent Developments: In February 2026, Johnson & Johnson introduced a new breakthrough in vision care with the launch of the first daily disposable multifocal toric contact lens designed specifically for adults experiencing both astigmatism and presbyopia. These new lenses are developed to address the complex and evolving vision needs of patients who experience multiple conditions simultaneously.

- Strategic Focus: J&J Vision focuses on premium daily disposable contact lens innovation — particularly in health-benefit positioning around UV protection and blue-light filtering — and myopia management as a high-growth adjacent category requiring proprietary clinical evidence and eye care professional advocacy.

Alcon Inc.

The company specializes in surgical and vision care products, holding the number one position in contact lens care solutions and a leading position in the global contact lens market through its comprehensive portfolio of daily disposable and extended wear lenses.

- Product Portfolio: Air Optix Night & Day, Dailies Total1, Dailies AquaComfort Plus, Total30 monthly contact lenses, and Opti-Free lens care solutions.

- Recent Developments: In February 2026, Alcon introduced TOTAL30 Multifocal for Astigmatism, the first and only monthly replacement multifocal toric contact lens featuring Water Gradient Technology. This innovation is designed for individuals who experience both astigmatism and presbyopia, addressing a significant unmet need in vision correction.

- Strategic Focus: Alcon's strategy centers on premiumizing its contact lens portfolio through differentiated material technologies, particularly water gradient and silicone hydrogel innovations, while simultaneously defending its dominant position in lens care solutions and expanding its surgical eye care division into high-growth emerging markets across Asia Pacific and Latin America.

Marchon Eyewear, Inc.

Marchon Eyewear, Inc. is one of the world's largest independent eyewear manufacturers and distributors. The company designs, manufactures, and distributes prescription frames and sunglasses under an extensive portfolio of owned and licensed brand partnerships, serving optical retailers and eye care professionals across more than 100 countries through a wholly owned global distribution network.

- Product Portfolio: Licensed frames under Nike Vision, Calvin Klein, Lacoste, Columbia, Ferragamo, Lanvin, and Dragon.

- Recent Developments: In January 2025, Marchon Eyewear entered an exclusive, long-term licensing agreement with Kendra Scott to develop and launch the brand’s first-ever eyewear collection. The partnership marks Kendra Scott’s expansion into the eyewear category, combining its signature design aesthetic with Marchon’s expertise in eyewear manufacturing and distribution.

- Strategic Focus: Marchon's strategy differentiates through the breadth and diversity of its licensed brand portfolio, spanning athletic, luxury, contemporary, and lifestyle categories, enabling it to serve the full optical retail price spectrum from accessible fashion to premium designer, while its proprietary Flexon memory metal technology provides a defensible owned-brand position in the functional performance segment.

Market Concentration Analysis

The global eyewear market is moderately concentrated at the top with EssilorLuxottica commanding an estimated 20–25% global revenue share through its integrated lens, frame, and retail operations. The remainder of the market is served by a tiered competitive structure including global frame specialists (Safilo, Marchon, Marcolin), contact lens multinationals (Alcon, J&J Vision, CooperVision), and thousands of regional manufacturers and independent optical retailers.

Consolidation at the lens manufacturing level is more advanced than the overall market suggests. The top four lens manufacturers, Essilor, Hoya, Carl Zeiss Vision, and Rodenstock, account for a majority of premium optical lens revenue globally. E-commerce consolidation is occurring rapidly, with Warby Parker and Zenni Optical establishing direct-to-consumer scale in North America.

Investment & Growth Opportunities

Fastest-Growing Segments

Contact lenses at ~6.5% CAGR through 2034 represent the highest-growth product segment, driven by daily disposable format penetration, myopia management lens adoption in children, and silicone hydrogel material innovation expanding wearer comfort and extended-wear options. Asia Pacific at ~7.0% CAGR is the fastest-growing region.

Emerging Markets

Asia Pacific at ~7.0% CAGR is the fastest-growing region for eyewear through 2034. China, with the world's highest prevalence of myopia affecting over 600 million people and a rapidly expanding middle-class consumer base, represents the single largest growth opportunity. India's 1.4 billion population, currently significantly underserved by optical retail infrastructure, represents a long-term structural growth market.

Venture & Investment Trends

Private equity and venture capital investment in eyewear has accelerated, particularly in direct-to-consumer optical brands and vision care technology platforms. Warby Parker's NASDAQ listing in 2021 validated the DTC optical retail model. AI-powered ophthalmic diagnostic tools enabling community-based vision screening and tele-optometry services are attracting healthcare technology investment in emerging market eye care access.

Future Market Outlook (2026-2034)

The global eyewear market is forecast to expand from USD 179.7 Billion in 2025 to USD 295.4 Billion by 2034 at a CAGR of 5.68%, adding USD 115.7 Billion in incremental annual market value over the forecast period. This consistent, sustained growth reflects the market's dual positioning as both a healthcare necessity and a fashion-driven consumer goods category.

Three technological forces will most significantly shape the eyewear industry through 2034: smart eyewear integration (AR displays and health sensors), AI-powered vision diagnostics enabling wider access to eye care in underserved populations, and advanced lens material innovations addressing growing myopia management demands in children and young adults across Asia Pacific.

Research Methodology

Primary Research

Primary research encompassed over 50 structured interviews with eyewear industry stakeholders, including optical retail category managers, licensed brand portfolio executives, contact lens clinical affairs professionals, independent optometrists, and e-commerce platform operators. Primary data validated market sizing, product segment shares, regional demand estimates, and technology adoption timelines.

Secondary Research

Key secondary sources include WHO World Report on Vision (2019, updated data), Vision Council of America VisionWatch reports, Euromonitor International eyewear category data, CDC vision impairment statistics, Contact Lens Spectrum, Optometry Times, and trade publications including Eyecare Business and Silmo Daily.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating vision impairment prevalence data, GDP growth rates, optical retail outlet expansion, contact lens adoption curve modeling, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty.

Eyewear Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Products Covered | Spectacles, Sunglasses, Contact Lenses |

| Genders Covered | Men, Women, Unisex |

| Distribution Channels Covered | Optical Stores, Independent Brand Showrooms, Online Stores, Retail Stores |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Alcon Inc., De Rigo Spa, EssilorLuxottica, Fielmann Group AG, Hoya Corporation, Johnson & Johnson, Marchon Eyewear, Inc., Safilo Group S.P.A., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the eyewear market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global eyewear market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the eyewear industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Eyewear Market Report

The global eyewear market reached USD 179.7 Billion in 2025, reflecting consistent demand from rising visual impairment prevalence, growing fashion-driven purchasing, and expanding contact lens adoption globally.

The market is projected to reach USD 295.4 Billion by 2034, growing at a CAGR of 5.68% during 2026-2034, driven by Europe's fashion-premium positioning, Asia Pacific's rapid vision care market expansion, and contact lens technology innovation.

Spectacles lead with a 52.4% product share in 2025, serving the largest global population requiring vision correction with a broad range of prescription, blue-light blocking, progressive, and designer frame options.

The Unisex segment dominates at 45.8% in 2025, reflecting fashion industry trends toward gender-neutral eyewear design and brands' strategic expansion of inclusive collections for broader market reach.

Europe commands a dominant 32.6% market share in 2025, driven by Italy's position as the global luxury eyewear manufacturing hub, strong fashion culture integrating eyewear as a premium accessory, and mature optical retail infrastructure.

Contact lenses are the fastest-growing product at ~6.5% CAGR through 2034, driven by daily disposable convenience innovation, myopia management adoption in pediatric patients, and expanding silicone hydrogel material options improving extended wear comfort.

Leading companies include Alcon Inc., De Rigo Spa, EssilorLuxottica, Fielmann Group AG, Hoya Corporation, Johnson & Johnson, Marchon Eyewear, Inc., Safilo Group S.P.A., and others.

Key applications include prescription vision correction, UV protection, digital screen blue-light filtering, sports and performance eyewear, occupational safety eyewear, and cosmetic/fashion accessory use across all demographic groups.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)